Chronic Obstructive Pulmonary Disease (COPD) Drugs Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 27.58 Billion |

| Market Size (2030) | USD 35.36 Billion |

| Growth Rate (2025 - 2030) | 5.09% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Chronic Obstructive Pulmonary Disease (COPD) Drugs Market Analysis by Mordor Intelligence

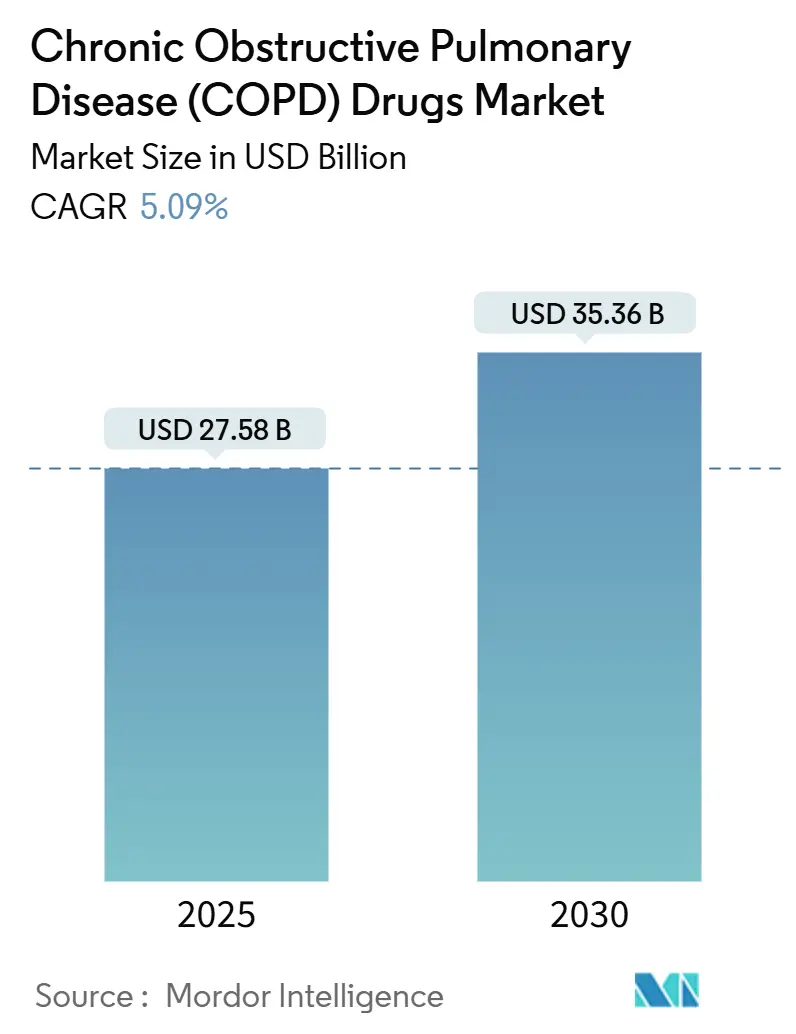

The Chronic Obstructive Pulmonary Disease Drugs Market size is estimated at USD 27.58 billion in 2025, and is expected to reach USD 35.36 billion by 2030, at a CAGR of 5.09% during the forecast period (2025-2030).

The chronic obstructive pulmonary disease (COPD) Market size reached USD 27.58 billion in 2025 and is projected to expand to USD 35.36 billion by 2030, posting a 5.09% CAGR over the forecast period. The demand for precision medicine, breakthrough biologic approvals, smart-inhaler rollouts, and steady reimbursement expansion in emerging economies underpins momentum in the chronic obstructive pulmonary disease (COPD) market. Competitive intensity is rising as first-in-class biologics for chronic obstructive pulmonary disease (COPD) reshape treatment algorithms, while fixed-dose triple inhalers and once-daily regimens address adherence shortfalls. Digital inhaler sensors that supply real-time data to clinicians are moving care toward anticipatory management, and payers in the Asia-Pacific and Latin America regions are expanding access to high-value respiratory therapies. Alongside these forces, escalating air pollution exposure in large urban centers continues to expand the addressable patient pool for the chronic obstructive pulmonary disease (COPD) market.

Key Report Takeaways

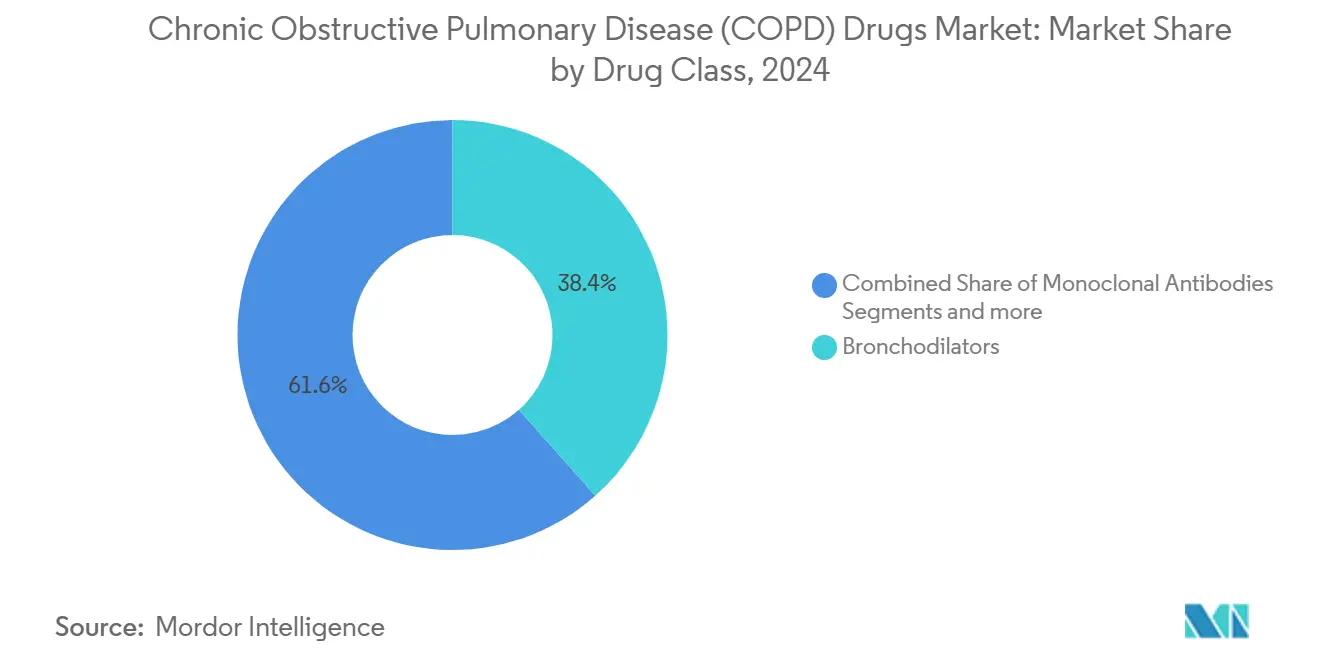

- By drug class, bronchodilators led the chronic obstructive pulmonary disease (COPD) market with a 38.44% share in 2024. Monoclonal antibodies recorded the fastest growth, advancing at a 6.81% CAGR through 2030.

- By route of administration, inhaled therapies captured 68.45% of the chronic obstructive pulmonary disease (COPD) market size in 2024, while injectable/parenteral treatments are forecast to expand at a 6.71% CAGR between 2025 and 2030.

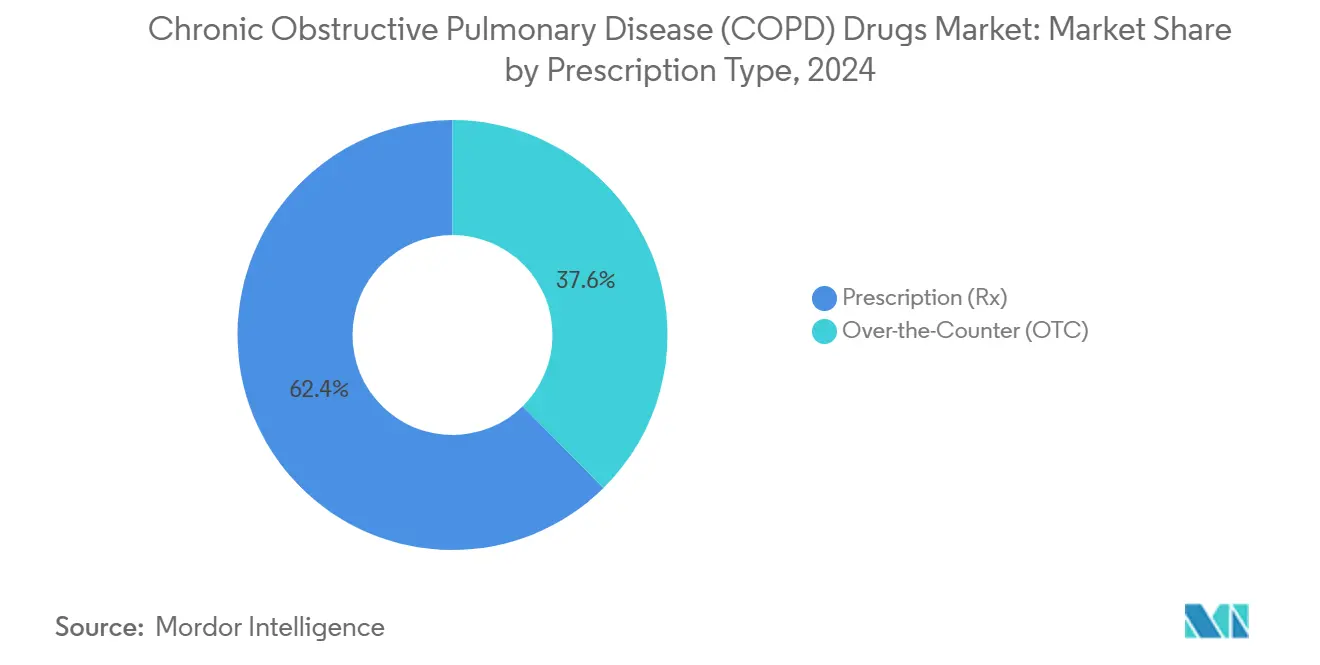

- By prescription type, prescription drugs dominated the chronic obstructive pulmonary disease (COPD) market with a 62.39% share in 2024; over-the-counter products are projected to post a 5.92% CAGR.

- By distribution channel, retail pharmacies accounted for 40.43% of the chronic obstructive pulmonary disease (COPD) market size in 2024, while online pharmacies are poised to grow at a 6.91% CAGR through 2030.

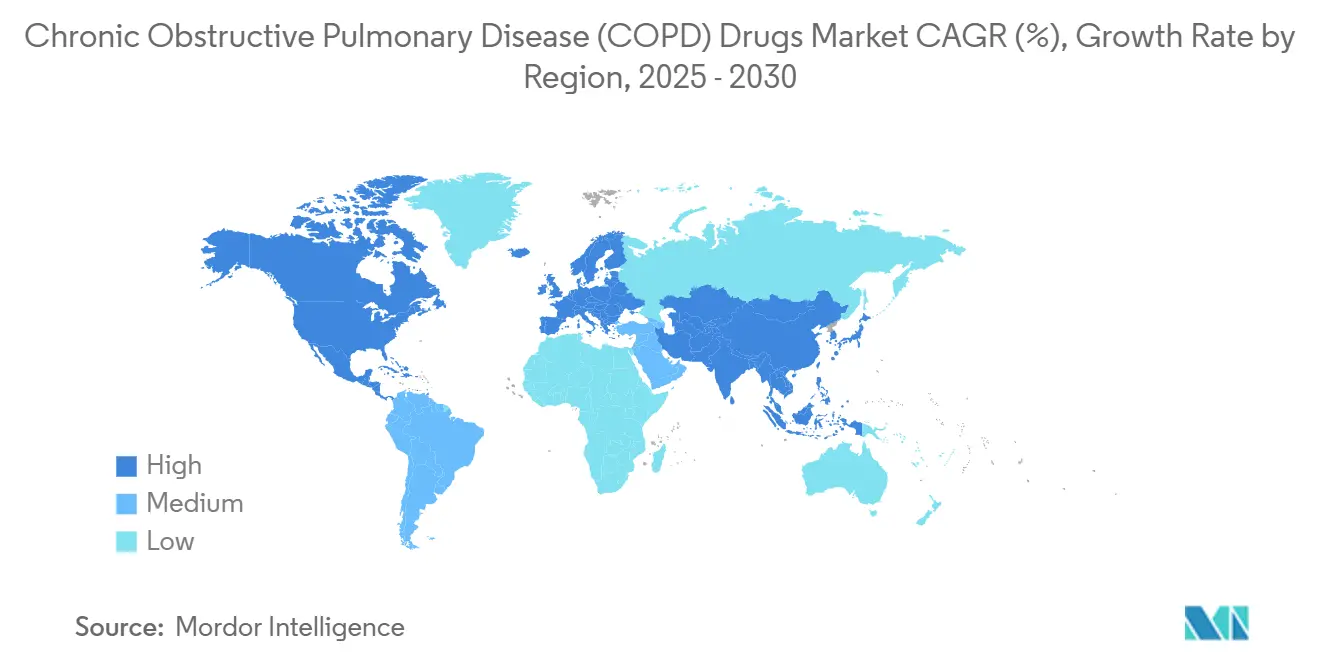

- By geography, North America accounted for 36.56% of the chronic obstructive pulmonary disease (COPD) market size in 2024, while Asia-Pacific is poised to grow at 6.43% CAGR through 2030.

Global Chronic Obstructive Pulmonary Disease (COPD) Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Biologics and Targeted Therapy Approvals | +1.8% | Global, with early gains in North America, Europe | Medium term (2-4 years) |

| Expansion of Healthcare Expenditure and Reimbursement for Respiratory Therapies in Emerging Markets | +1.2% | Asia-Pacific core, spill-over to Latin America | Long term (≥ 4 years) |

| Growing Adoption of Fixed-Dose Combination & Once-Daily Inhalers to Improve Patient Compliance | +0.9% | Global | Short term (≤ 2 years) |

| Advancements in Inhaler Technologies Enhancing Drug Delivery | +0.7% | North America & EU, expanding to Asia-Pacific | Medium term (2-4 years) |

| Rising Prevalence of COPD around the World | +0.6% | Global, concentrated in low-middle SDI countries | Long term (≥ 4 years) |

| Increasing Air Pollution in Densely Populated Countries | +0.5% | Asia-Pacific, Middle East, urban centers globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Biologics and Targeted Therapy Approvals

The United States Food and Drug Administration (FDA) cleared dupilumab for COPD in September 2024, following trials that showed a 30-34% reduction in exacerbations, sparking a cascade of biologic launches.[1]Mary Caffrey, “Dupilumab Gains Landmark FDA Approval for COPD,” ajmc.com GSK’s mepolizumab won COPD approval in May 2025, and AstraZeneca’s benralizumab is in late-stage trials aimed at eosinophilic inflammation. Collectively, these biologics shift treatment focus from symptom control to disease modification, positioning the chronic obstructive pulmonary disease (COPD) market for sustainable value growth.

Expansion of Healthcare Expenditure and Reimbursement for Respiratory Therapies in Emerging Markets

Governments in the Asia-Pacific are instituting reference-pricing frameworks and pharmacoeconomic reviews that reward confirmed clinical benefit while containing spend. China projects a USD 3,296 billion burden of COPD by 2039, prompting expansion of reimbursement for biologics and investment in infrastructure. Australia has piloted financially based patient-access schemes for high-budget-impact respiratory drugs. Such initiatives support reliable market entry for innovation, cushioning price-sensitive populations, and driving growth in the chronic obstructive pulmonary disease (COPD) market.

Growing Adoption of Fixed-Dose Combination & Once-Daily Inhalers to Improve Patient Compliance

Triple fixed-dose inhalers, such as AstraZeneca’s Breztri, are experiencing rapid share gains while deploying next-generation propellants with a 99.9% lower warming potential.[2]AstraZeneca, "AstraZeneca announces the completion of the clinical programme to support the transition of Breztri to next-generation propellant with near-zero Global Warming Potential," astrazeneca.com GSK’s Trelegy Ellipta delivered USD 2.2 billion in 2023 sales and could reach USD 3.8 billion by 2027 on adherence benefits. Studies confirm that once-daily therapy maintains efficacy and simplifies routines, thereby lowering the risk of exacerbations and supporting recurring revenue for the chronic obstructive pulmonary disease (COPD) market.

Advancements in Inhaler Technologies Enhancing Drug Delivery

Teva’s ProAir Digihaler sensors revealed inhalation-metric declines two weeks before COPD flare-ups in over 9,600 monitored events, allowing for preemptive intervention. Smart-inhaler clearances for AstraZeneca device platforms permit real-time adherence coaching. Vibrating-mesh devices achieve lung deposition rates surpassing 80%, broadening the feasibility of inhaled biologics and underscoring the integral role of device innovation in the chronic obstructive pulmonary disease (COPD) market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying Generic Competition Following Key Inhaler Patent Expiries | -1.4% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Stringent Regulatory & Safety Requirements Prolonging Approval Timeline | -0.8% | Global, particularly FDA and EMA jurisdictions | Medium term (2-4 years) |

| High Treatment Costs of Biologics Limiting Access in Cost-Sensitive Regions | -0.9% | Emerging markets, uninsured populations globally | Long term (≥ 4 years) |

| Long-Term Corticosteroid & Long-Acting Beta-Agonists (LABA) Safety Concerns Impacting Prescriber Confidence | -0.3% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Intensifying Generic Competition Following Key Inhaler Patent Expiries

Patents on major inhalers such as Flovent HFA lapse in July 2025, exposing brands to generic attack. Complex device patents and rigorous bio-equivalence demands limit the number of approved generics, yet erosion pressures are unavoidable, trimming near-term value in portions of the chronic obstructive pulmonary disease (COPD) market.

High Treatment Costs of Biologics Limiting Access in Cost-Sensitive Regions

Health-economic models indicate that current biologic prices must decrease by 60-80% to meet cost-effectiveness thresholds in large emerging economies. Out-of-pocket costs remain key decision drivers in China, and pharmacy-benefit-manager mark-ups influence US affordability. Biosimilar pipelines and innovative contracting are underway, but high list prices will restrain portions of the chronic obstructive pulmonary disease (COPD) market until affordability improves.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Precision Biologics Reshape Traditional Bronchodilator Dominance

Bronchodilators retained a 38.44% share of the chronic obstructive pulmonary disease (COPD) market in 2024, but monoclonal antibodies charted the swiftest climb at a 6.81% CAGR through 2030. Generic short-acting Beta 2-agonists remain the mainstay of rescue; however, AstraZeneca’s albuterol-budesonide combo introduces anti-inflammatory rescue in a single device, challenging long-established patterns. Long-acting agents are progressively packaged into triple combinations, while phosphodiesterase-4 inhibitors gain relevance through Verona Pharma’s dual pathway Ohtuvayre. Antibody developers are now outpacing small-molecule launches, delivering sustained symptom control and disease-modification prospects that lift average revenue per patient.

In the second half of the decade, the ability of biologics to tap overlapping inflammatory cascades is expected to sustain a leadership premium, steering formulary positioning toward broad-spectrum agents. The chronic obstructive pulmonary disease (COPD) market size for monoclonal antibodies is therefore projected to narrow the gap left by legacy bronchodilators, despite the higher complexity of the injection route. Differentiation by dosing interval and phenotype-agnostic efficacy should drive brand loyalty, while exposure to upcoming biosimilars remains a medium-term consideration.

By Route of Administration: Injectable Therapies Challenge Inhaled Dominance

Inhaled drugs controlled 68.45% of the chronic obstructive pulmonary disease (COPD) market size in 2024 and remain the frontline modality, thanks to their localized delivery and rapid bronchodilation. Patent expiries on inhaler brands and ecological pressure to replace hydrofluoroalkane propellants are prompting device innovation with near-zero warming potential. Smart-inhaler connectivity embeds analytics into routine care, nudging adherence upward.

Injectable and other parenteral formats are projected to log the strongest trajectory at a 6.71% CAGR through 2030, driven by the uptake of dupilumab, mepolizumab, and tezepelumab. Four- to six-month subcutaneous schedules ease clinic visits, mitigating the historic aversion to injections and elevating the share in the chronic obstructive pulmonary disease (COPD) market. Oral agents preserve a niche for anti-leukotrienes and emerging PDE-4 inhibitors, while early-stage inhaled biologics may further fragment delivery-route dynamics beyond 2030.

By Prescription Type: OTC Growth Reflects Self-Management Trends

Prescription products delivered 62.39% of 2024 revenue, anchored by high-value biologics, triple fixed-dose inhalers, and newly-approved dual-pathway agents requiring physician stewardship. Telehealth enables virtual consults for titration and adverse-event monitoring, preserving clinician oversight and reinforcing prescription dominance.

OTC medications, primarily legacy bronchodilators and mild anti-inflammatories, are projected to grow at a 5.92% CAGR through 2030. Connected inhalers and smartphone-based coaching allow patients to self-manage stable disease, while payers promote OTC switches to curtail cost. Safety controls for unsupervised use will nonetheless cap share within the chronic obstructive pulmonary disease (COPD) market.

By Distribution Channel: Online Pharmacies Capitalize on Digital Transformation

Retail outlets accounted for 40.43% of sales in 2024 through the integration of established insurance and pharmacist training on inhaler technique. Hospital pharmacies remain pivotal for initiating biologics and severe COPD rescue therapies.

Online pharmacies are exhibiting a 6.91% CAGR as telehealth normalizes, e-prescriptions rise, and cold-chain logistics mature. Direct-to-patient models enhance refill continuity and data capture, allowing manufacturers to track adherence trends across the chronic obstructive pulmonary disease (COPD) market. Regulatory hurdles for biologic delivery are easing as specialist platforms partner with courier networks that guarantee temperature integrity.

Geography Analysis

North America contributed 36.56% of the chronic obstructive pulmonary disease (COPD) market revenue in 2024, driven by advanced insurance coverage and an innovation-friendly FDA that granted first-in-class COPD biologic status to dupilumab. High inhaler prices, often exceeding USD 600 per month for the uninsured, are intensifying policy debates on patent reform and generic incentives. Canada benefits from provincial reimbursement but negotiates aggressively on biologic pricing, whereas Mexico’s expanding private healthcare segment opens new demand corridors.

Europe maintains a strong market stature, with centralized EMA approvals accelerating multi-country launches. Environmental regulation is nudging manufacturers toward climate-neutral propellants, a shift that is being adopted in product pipelines. Health-technology-assessment bodies in Germany, the United Kingdom, and France scrutinize the cost-effectiveness of health technologies, promoting outcome-based pricing models. Southern Europe exhibits slower biological uptake due to budget constraints, yet long-term savings from exacerbation prevention underpin gradual listing decisions.

Asia-Pacific is the fastest-growing bloc, advancing at 6.43% CAGR between 2025-2030. China’s projected COPD economic burden of USD 3,296 billion by 2039 is pushing authorities to expand specialty clinics and reimburse novel modalities. Japan’s super-aged population drives premium product uptake, while India leverages domestic manufacturing for cost-efficient generics without forfeiting biologic imports for severe cases. Southeast Asia’s urban pollution, linked to 8.1 million global deaths in 2021, is heightening awareness and screening, thereby enlarging the chronic obstructive pulmonary disease (COPD) market.

Competitive Landscape

The chronic obstructive pulmonary disease (COPD) market demonstrates moderate concentration. AstraZeneca, GSK, Sanofi-Regeneron, and Boehringer Ingelheim anchor leadership through broad inhaler lines and expanding biologic franchises. AstraZeneca’s USD 2 billion purchase of Almirall’s respiratory assets and Merck’s USD 10 billion acquisition of Verona Pharma showcase the strategic pivot toward novel mechanisms and dual-pathway inhibitors.

GSK’s Ellipta platform enables device continuity across 80% of respiratory classes and underpins quarterly respiratory revenue of near GBP 1.6 billion. Dupixent’s multibillion-dollar sales remain the biologic benchmark, but emerging IL-5 and TSLP rivals are challenging its dominance. Digital-health collaborations—such as AstraZeneca’s inhaler sensor integrations—differentiate brands by delivering real-time analytics that pre-empt exacerbations.

White-space opportunities include pediatric biologic formulations, early-intervention COPD antibodies, and combination biologics that simultaneously inhibit multiple inflammatory pathways. Generic manufacturers position for post-2025 inhaler patent cliffs, yet complex device replication will moderate erosion speed, allowing innovators room to transition portfolios toward next-generation delivery systems.

Chronic Obstructive Pulmonary Disease (COPD) Drugs Industry Leaders

-

GlaxoSmithKline PLC

-

AstraZeneca PLC

-

Boehringer Ingelheim GmbH

-

Novartis AG

-

Teva Pharmaceutical Industries Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Tech Launch Arizona unveiled Aspiro Therapeutics, advancing an inhaled therapy platform licensed from the University of Arizona.

- September 2025: Sanofi and Regeneron secured FDA approval for Dupixent as the first biologic for eosinophilic COPD, benefitting an estimated 300,000 US patients.

- May 2024: Verona Pharmaceuticals gained FDA clearance for Ensifentrine (Ohtuvayre), the inaugural dual PDE3/4 inhibitor for COPD maintenance.

Global Chronic Obstructive Pulmonary Disease (COPD) Drugs Market Report Scope

According to the report's scope, chronic obstructive pulmonary disease (COPD) is caused by a blockage in the airways, resulting in difficulty breathing.

The chronic obstructive pulmonary disease (COPD) market is segmented by drug class, route of administration, indication, prescription type, distribution channel, and geography. By drug class, the market is segmented into bronchodilators (short-acting beta-2 agonists, long-acting beta-2 agonists, and anticholinergic agents), anti-inflammatory drugs (oral and inhaled corticosteroids, anti-leukotrienes, phosphodiesterase type 4 inhibitors, and other anti-inflammatory agents), monoclonal antibodies, and combination drugs. By route of administration, the market is segmented into inhaled, oral, and injectable/parenteral. By prescription type, the market is segmented into prescription (Rx) and over-the-counter (OTC). By distribution channel, the market is segmented into hospital pharmacies, retail pharmacies, and online pharmacies. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across the major regions globally. The report offers the value (in USD billion) for the above segments

| Bronchodilators | Short-acting Beta 2 Agonists |

| Long-acting Beta 2 Agonists | |

| Anticholinergic Agents | |

| Anti-inflammatory Drugs | Oral & Inhaled Corticosteroids |

| Phosphodiesterase-4 Inhibitors | |

| Other Anti-inflammatory Drugs | |

| Combination Drugs |

| Inhaled |

| Oral |

| Prescription (Rx) |

| Over-the-Counter (OTC) |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class | Bronchodilators | Short-acting Beta 2 Agonists |

| Long-acting Beta 2 Agonists | ||

| Anticholinergic Agents | ||

| Anti-inflammatory Drugs | Oral & Inhaled Corticosteroids | |

| Phosphodiesterase-4 Inhibitors | ||

| Other Anti-inflammatory Drugs | ||

| Combination Drugs | ||

| By Route of Administration | Inhaled | |

| Oral | ||

| By Prescription Type | Prescription (Rx) | |

| Over-the-Counter (OTC) | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the chronic obstructive pulmonary disease (COPD) market?

It stood at USD 27.58 billion in 2025 and is forecast to hit USD 35.36 billion by 2030.

Which drug class is growing fastest?

Monoclonal antibodies are advancing at a 6.81% CAGR through 2030.

Why is COPD growth outpacing asthma?

First-ever biologic approvals for eosinophilic COPD are expanding eligible patient pools and raising average treatment spend.

What delivery route shows the highest forecast growth?

Injectable/parenteral therapies are projected to rise at 6.71% CAGR thanks to subcutaneous biologics.

How will patent expiries affect pricing?

Key inhaler expiries starting 2025 will introduce generics, tempering prices in certain segments but sparking innovation in device technology.

Which sales channel is expanding quickest?

Online pharmacies are set to register 6.91% CAGR as telehealth and direct-to-patient logistics mature.

Page last updated on: