Chromatography Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.49 Billion |

| Market Size (2031) | USD 2.24 Billion |

| Growth Rate (2026 - 2031) | 8.55% CAGR |

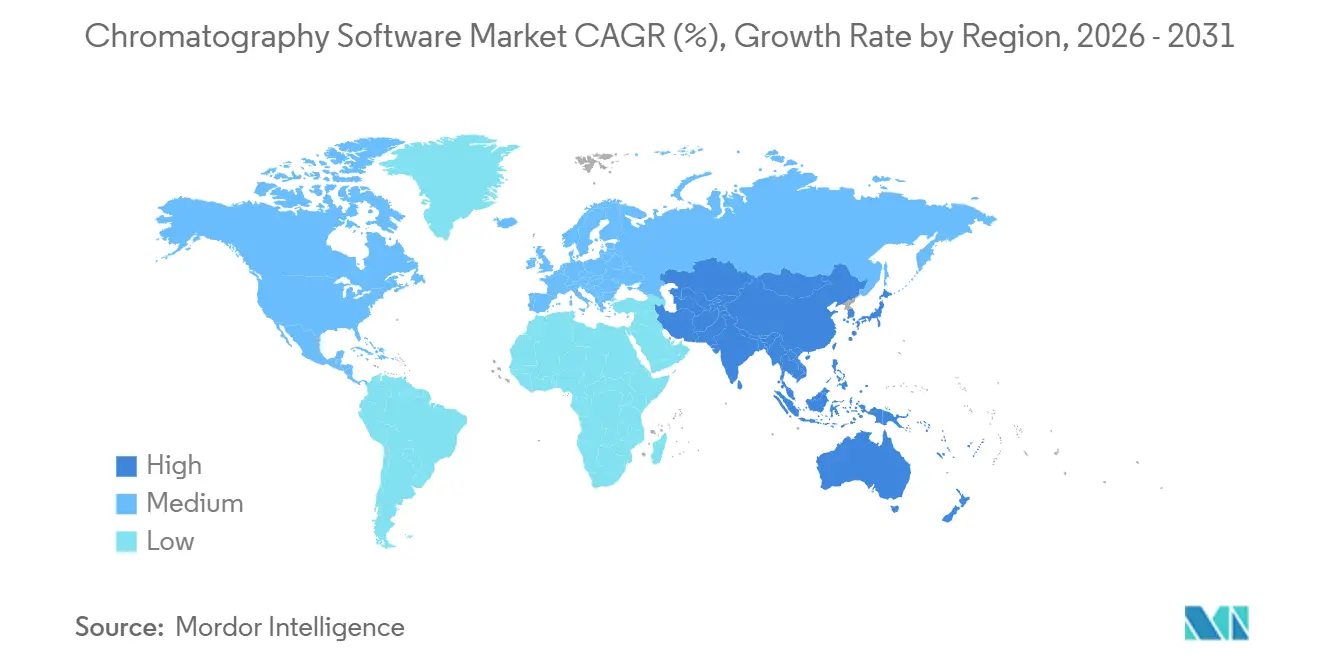

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chromatography Software Market Analysis by Mordor Intelligence

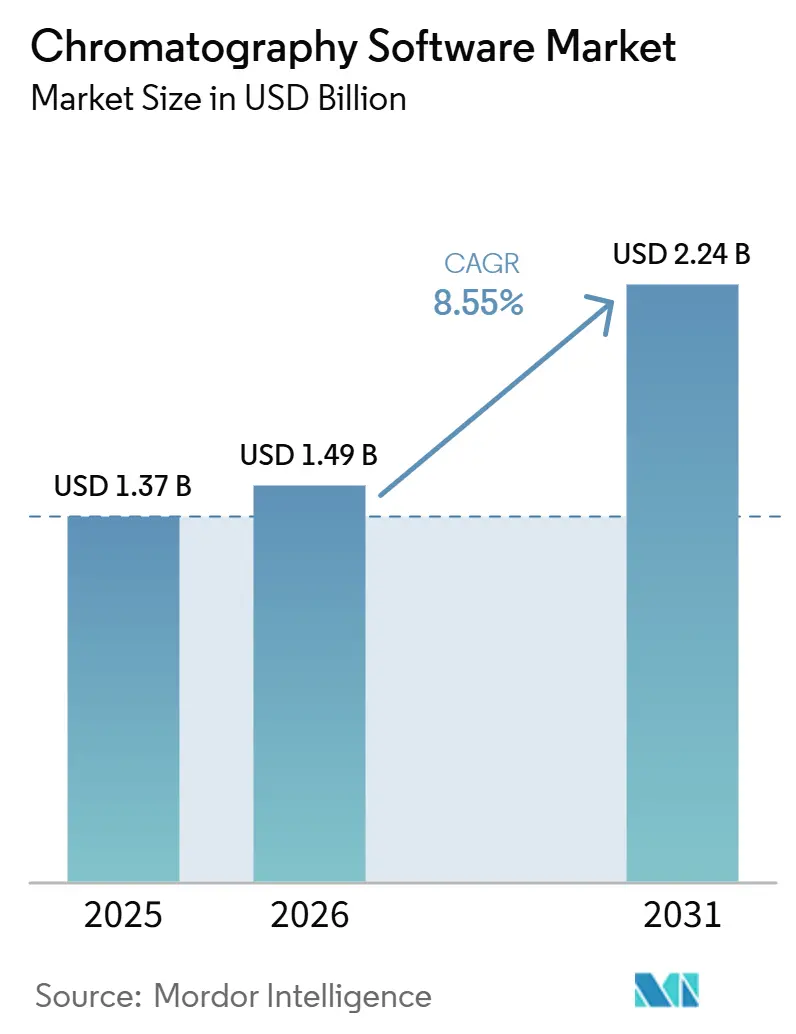

The Chromatography Software Market size is projected to expand from USD 1.37 billion in 2025 and USD 1.49 billion in 2026 to USD 2.24 billion by 2031, registering a CAGR of 8.55% between 2026 to 2031.

The chromatography software market is being shaped by rising pharmaceutical pipeline complexity, tighter data integrity requirements, and a steady move from instrument-linked workstations toward enterprise informatics platforms that connect data, users, and sites. The chromatography software market is also gaining broader value as chromatography data systems connect more closely with LIMS, ELN, and SDMS environments, which moves software demand beyond data capture and into enterprise data governance. North America remains the largest regional base in the chromatography software market, while Asia-Pacific is expanding the fastest as compliance expectations rise and outsourcing activity grows in China and India. The chromatography software market is also seeing a clear shift in deployment preference, with on-premise systems still holding the largest installed base while web and cloud models gain traction in multi-site pharmaceutical companies and CROs that need flexible but controlled data access. Competition in the chromatography software market remains moderate at the enterprise tier, and the main purchase filters continue to be compliance strength, interoperability across mixed instrument fleets, and the ability to reduce validation, cybersecurity, and operational risk.

Key Report Takeaways

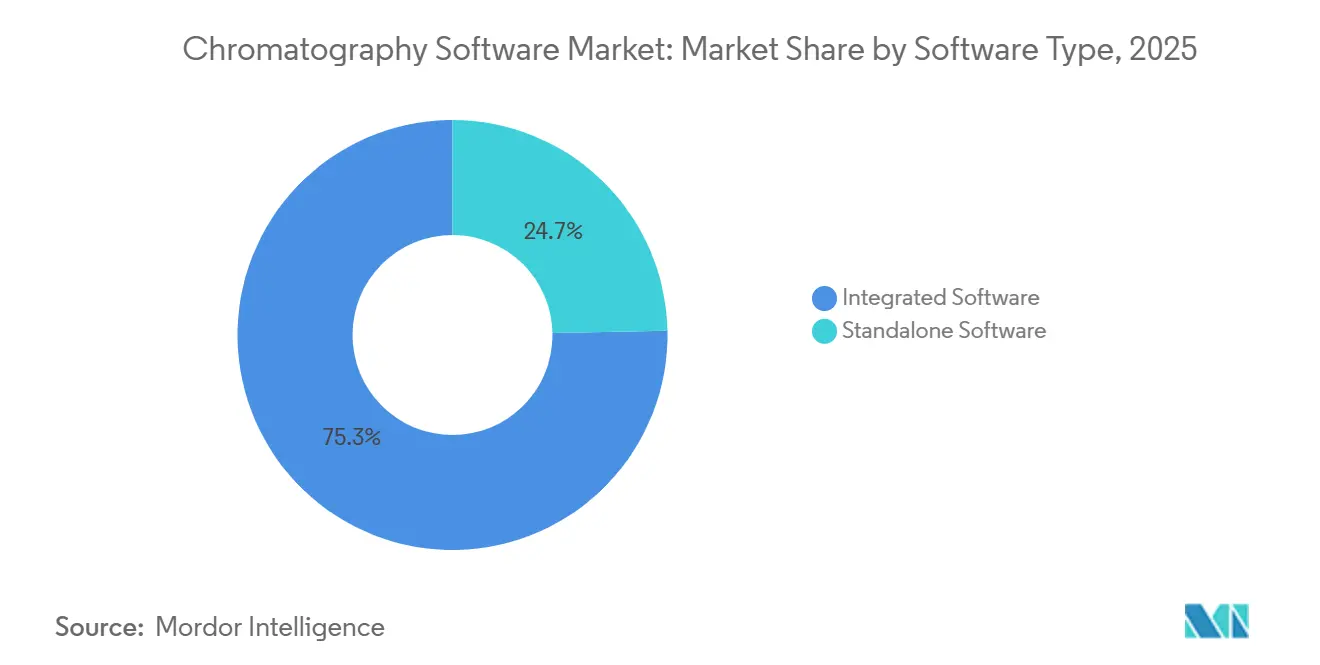

- By software type, Integrated Software held 75.31% share in 2025, and is expected to grow with a 9.38% CAGR through 2031.

- By deployment model, On-Premise Software held 55.24% share in 2025, while Web and Cloud-Based Software is forecast to grow at a 9.52% CAGR through 2031.

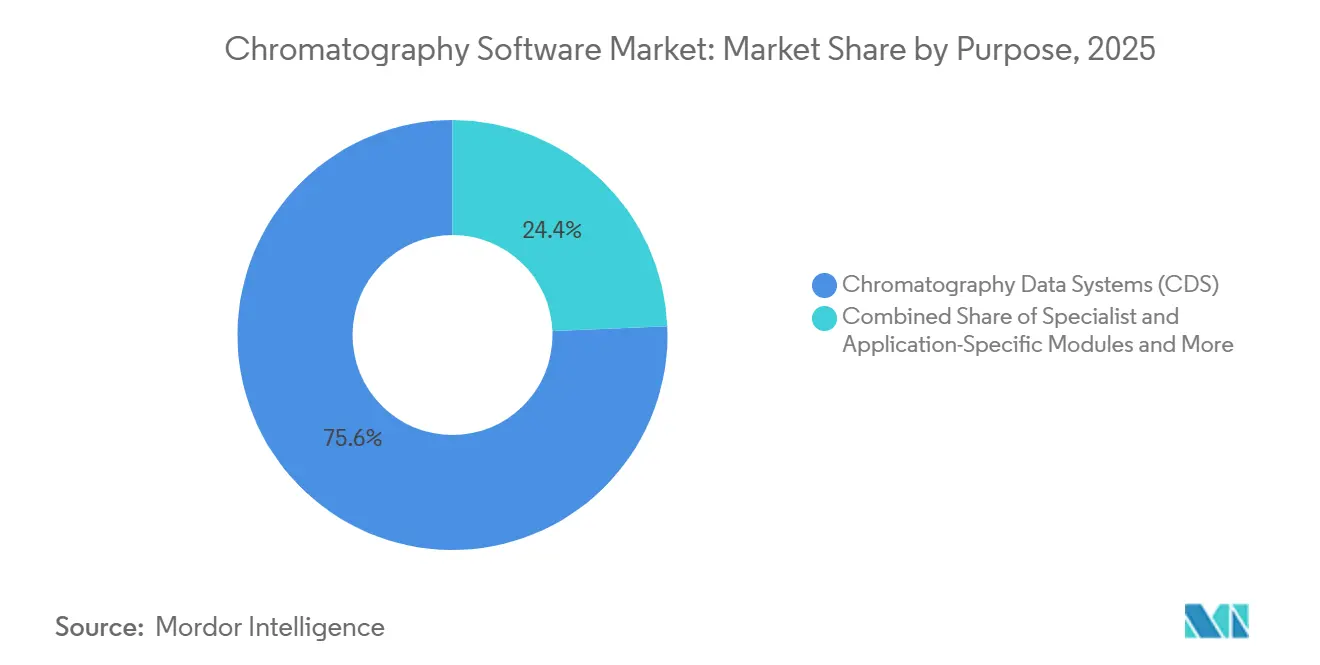

- By purpose, Chromatography Data Systems held 75.64% share in 2025, while Specialist and Application-Specific Modules are forecast to expand at a 9.62% CAGR through 2031.

- By end user, Pharmaceutical and Biotechnology companies held 36.26% share in 2025, while Contract Research Organizations are projected to grow at an 8.95% CAGR through 2031.

- By geography, North America held 46.61% share in 2025, while Asia-Pacific is forecast to grow at a 9.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Chromatography Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pharmaceutical And Biotech Workflow Digitization | +2.5% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Regulatory Data-Integrity Requirements | +1.9% | North America, Europe, and APAC | Short term (≤ 2 years) |

| Laboratory Automation And High-Throughput Analysis Needs | +1.4% | Global, with APAC showing the fastest adoption curve | Medium term (2-4 years) |

| Cloud-Enabled Remote Collaboration And Access | +1.1% | North America and Europe, with spillover into APAC | Medium term (2-4 years) |

| Multi-Vendor Interoperability Pressure In Mixed Instrument Fleets | +0.6% | Global, especially in multi-site pharmaceutical enterprises | Long term (≥ 4 years) |

| Validation-Ready AI-Assisted Peak Review And Exception Handling | +0.7% | North America and Europe, with early adoption in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Pharmaceutical And Biotech Workflow Digitization

The chromatography software market is moving deeper into full workflow digitization inside pharmaceutical and biotechnology laboratories. Companies are no longer using software only for data capture, because method transfer, execution guidance, review, and release support are becoming digital steps inside one connected process. Agilent’s OpenLab Sync shows this change clearly because it links machine-readable USP method content with guided digital execution, which reduces manual handling and makes workflows easier to standardize across sites. This raises switching costs over time, since a laboratory that builds validated, machine-readable methods into one platform becomes less willing to move those methods into another system. The same shift is reinforced by biologics quality control, where Agilent’s Multi-Attribute Method workflow for LC/HRMS reflects how complex products are increasing demand for software that can support regulated, high-content analysis in routine operations.

Regulatory Data-Integrity Requirements

The chromatography software market continues to be supported by regulatory frameworks that require secure electronic records, controlled access, audit trails, and electronic signatures. FDA 21 CFR Part 11 remains central because basic workstation tools and paper-heavy processes do not meet the control standards expected in regulated environments[1]U.S. Food and Drug Administration, “Electronic Records, Electronic Signatures,” Electronic Code of Federal Regulations, ecfr.gov. The same pattern extends into Europe through Annex 11 and into Asia through regulators that are aligning with ICH-driven expectations, which creates upgrade pressure across the main pharmaceutical production regions. Waters addressed this need with Alliance iS HPLC System Software 2.0, which links authenticated touchscreen access checks with Empower audit trails and reduces common user errors by up to 40% inside the traceability chain. As regulators continue to tighten expectations, the chromatography software market is likely to keep seeing mandatory spending cycles tied less to optional productivity gains and more to minimum compliance thresholds.

Laboratory Automation And High-Throughput Analysis Needs

The chromatography software market is also being pushed by laboratory automation, which is increasing the amount and speed of data that laboratories must receive, process, review, and archive. Research in Accounts of Chemical Research showed that automated feedback loops and predictive models can reduce method development timelines from weeks of manual work to a much smaller set of automated experiments, which shifts more of the workload into software-controlled environments. In proteomics, ProteoAutoNet reported a twofold throughput improvement and processed six 96-well plates in three days, which shows how quickly high-throughput environments can outgrow software built for slower manual review cycles. Shimadzu’s Nexera X4 UHPLC launch in 2026 adds to that pressure because faster analysis at the instrument layer raises expectations for software speed, exception handling, and downstream review capacity. As a result, the chromatography software market is shifting toward platforms that can manage more data without adding proportional review effort.

Cloud-Enabled Remote Collaboration And Access

The chromatography software market is seeing stronger demand for cloud-enabled collaboration, especially in multi-site pharmaceutical companies and CRO networks. Waters’ work with Amazon Web Services on waters_connect highlights this direction because it enables browser-based access to laboratory information for monitoring, review, and cross-site visibility without keeping every workflow tied to one local workstation. This matters because software selection starts to move away from a one-instrument purchase decision and toward a broader infrastructure decision that covers multiple labs and users. Thermo Fisher’s Chromeleon 7.4 also reflects this move through centralized storage, remote control, and support across mass spectrometry instrument classes from multiple vendors. As these models gain acceptance, the chromatography software market is likely to see larger platform-level buying decisions and stronger rivalry among vendors that can support remote access without weakening compliance controls.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Validation And Change-Control Burden | -0.7% | Global, most acute in North America and Europe | Short term (≤ 2 years) |

| Legacy Instrument And Data-Format Lock-In | -0.5% | Global, highest prevalence in mature pharmaceutical markets | Medium term (2-4 years) |

| Shortage Of Chromatography Informatics Talent | -0.4% | North America, Europe, and emerging APAC CRO hubs | Medium term (2-4 years) |

| Cybersecurity And Audit-Trail Exposure In Connected Labs | -0.3% | Global, with growing exposure in APAC and MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Validation And Change-Control Burden

The chromatography software market still faces a meaningful brake from the validation burden attached to new implementations and major upgrades in GMP environments. FDA and EU expectations require documented installation, operation, and performance qualification work, which turns even beneficial upgrades into multi-month projects for quality and informatics teams. That burden creates a conservative buying pattern in the chromatography software market, where laboratories often prefer long version cycles instead of frequent feature adoption. Waters’ Empower CDS has moved through many version updates since its 2010 base release, and each laboratory still has to validate its own deployed version under internal procedures before using newer capabilities at scale. This leaves a gap between what vendors release and what many regulated laboratories actually operate, especially in smaller organizations that do not have dedicated validation teams.

Legacy Instrument And Data-Format Lock-In

The chromatography software market is also constrained by long-lived mixed instrument fleets and the proprietary data formats that come with them. Laboratories often need to retrieve raw data across multiple instrument generations, and that makes migration risk higher when data must remain searchable, reviewable, and submission-ready over long retention periods. The Pistoia Alliance’s methods database work showed a credible path toward vendor-agnostic HPLC-UV method transfer using Allotrope-based ontologies across Agilent OpenLab and Waters Empower environments, which directly addresses one of the most persistent barriers to software mobility. The Allotrope Simple Model Certification Pilot Program, launched in 2026, is important for the same reason because broad certification is still needed before laboratories can treat open interoperability as a standard procurement assumption. Until that transition is more mature, the chromatography software market will continue to favor incumbents in laboratories where proprietary formats are deeply embedded in regulated workflows.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Software Type: Integrated Platforms Extend Their Lead Across Technique Types

Integrated Software held 75.31% of the chromatography software market share in 2025, and it is also the fastest-growing software type with a 9.38% CAGR through 2031. That combination shows that the chromatography software market is not only led by integrated platforms, but is also moving further in that direction as laboratories replace siloed instrument software with unified environments. This change is visible in multi-technique laboratories that want LC, GC, IC, and mass spectrometry workflows under one audit trail, one user structure, and one review framework. Agilent’s OpenLab CDS version 3.0 supports that move by extending high-resolution mass spectrometry capability into the same broader platform used for existing LC and GC workflows[2]Agilent Technologies, “OpenLab CDS Version 3.0 Release Notes,” Agilent Technologies, agilent.com.

The chromatography software market still leaves space for standalone products in academic laboratories and independent research settings where regulatory demands are lighter and instrument-level flexibility remains attractive. Wider instrument compatibility remains a practical selling point for these tools, especially in smaller environments that want one lower-cost system to support diverse hardware rather than a full enterprise rollout. That said, the core comparison in the chromatography software market is increasingly between standalone flexibility and integrated governance. As regulated users expand their need for shared audit trails, centralized permissions, and harmonized review across techniques, the balance continues to move toward integrated deployments. The chromatography software market therefore shows a clear preference for platforms that reduce fragmentation rather than preserve it.

By Deployment Model: Cloud Economics Are Tilting A Conservative Market

On-Premise Software represented 55.24% of the chromatography software market size in 2025, which shows that validated local infrastructure still anchors most regulated deployments. The chromatography software market keeps this large installed base because many GMP laboratories prefer systems that fit into already qualified environments and established internal control processes. Even so, Web and Cloud-Based Software is projected to grow at a 9.52% CAGR through 2031 as CROs and multi-site pharmaceutical companies look for easier cross-site visibility and more scalable deployment models. Waters’ waters_connect example shows how remote access, monitoring, and review can be delivered in a compliant structure rather than only through workstation-bound tools.

The move in the chromatography software market is not a direct jump from all local to all cloud, because many laboratories are adopting hybrid patterns first. Data viewing, collaboration, and oversight can move into web environments while acquisition and some processing activities remain on site during the earlier stages of migration. Annex 11 matters here because it gives regulated users a concrete checklist for supplier controls around access, recovery, continuity, and backup in computerized systems. Once vendors satisfy those expectations, cloud deployments can become very sticky because validated migrations remain difficult even after the architecture changes. The chromatography software market is therefore becoming more favorable to vendors that can support hybrid adoption without asking laboratories to accept unnecessary compliance risk.

By Purpose: CDS Dominance Masks A Rapid Rise In Specialist Modules

Chromatography Data Systems accounted for 75.64% of the chromatography software market size in 2025, which confirms that CDS platforms remain the core working environment for most regulated users. The chromatography software market still depends on CDS for acquisition, processing, reporting, and routine review across major end-user groups, which keeps these platforms central to the revenue base. At the same time, Specialist and Application-Specific Modules are forecast to grow at a 9.62% CAGR through 2031 as laboratories add focused tools around complex biologics, metabolomics, and advanced analytical workflows. Agilent’s MAM workflow for BioPharma quality control shows this pattern well because it extends value into an area where general-purpose CDS tools alone are not enough for the full analytical requirement.

The chromatography software market is also broadening the role of review-oriented tools and open platforms inside selected user groups. Waters’ Empower Data Viewer shows how offline review is shifting toward browser-based collaboration and near-real-time access across distributed partner laboratories rather than simple file viewing. Academic and research users continue to leave room for open-source and flexible platforms when customization and vendor independence matter more than full validation support. That leaves the chromatography software market with a two-layer structure, where CDS platforms hold the center while specialist modules and review tools capture added value around specific workflows. The fastest growth in purpose-based demand is therefore coming from software that complements the core system instead of trying to replace it.

By End User: CRO Growth Momentum Reshapes Software Requirements

Pharmaceutical and Biotechnology companies held 36.26% of the chromatography software market in 2025, which reflects the volume of chromatographic work embedded in drug development, quality control, and commercial manufacturing. The chromatography software market still draws its largest revenue base from these users because regulated analysis, release testing, and submission support all depend on controlled data handling. Contract Research Organizations are growing faster at an 8.95% CAGR through 2031, and that matters because CROs must support multiple client methods, mixed regulatory contexts, and faster onboarding cycles than many internal laboratories. Agilent’s collaboration with Virscidian shows why this segment matters, since real-time OpenLab CDS access inside Analytical Studio supports higher-throughput workflows that are common in outsourced discovery and medicinal chemistry environments.

The chromatography software market also has an important secondary demand layer in academic, environmental, and food laboratories. Academic institutions do not deliver the same level of commercial revenue, but they influence platform familiarity and user preference before staff move into industrial roles. Environmental and food laboratories create adjacent demand because accreditation and compliance frameworks still require dependable data handling, even when their spending profile differs from pharmaceutical users. Thermo Fisher’s positioning of Chromeleon 7.4 toward PFAS and pesticide testing workflows shows that leading vendors are actively extending their reach beyond the core pharmaceutical base. The chromatography software market is therefore broadening by end user, but growth remains strongest where regulated complexity and client turnover make software agility a direct operating requirement.

Geography Analysis

North America held 46.61% of the chromatography software market share in 2025, which keeps it as the largest regional revenue base. The chromatography software market is strongest in the region because U.S. pharmaceutical manufacturing scale and FDA data integrity expectations combine to make compliant software a routine operating need rather than a discretionary purchase. Canada supports the chromatography software market through biopharma investment and academic research activity, while Mexico adds steady demand through export-oriented pharmaceutical manufacturing. Another advantage for the region is the concentration of chromatography informatics talent in major U.S. life sciences clusters, which helps larger organizations adopt enterprise platforms faster and creates reference cases for smaller buyers.

Europe remains the second-largest regional base in the chromatography software market, with Germany, the United Kingdom, France, and Switzerland forming the main demand centers. Annex 11 continues to shape the chromatography software market in Europe because validated computerized systems, electronic records, and business continuity planning are built into regulatory expectations across pharmaceutical operations. Europe also stands out for its role in open-standard work, as the Pistoia Alliance project used Allotrope-based ontologies to demonstrate vendor-agnostic digital transfer between Agilent and Waters CDS platforms. Germany remains an important launch venue for analytical technologies, and PerkinElmer’s Analytica 2026 showcase reflects that position in the regional ecosystem[3]PerkinElmer, “PerkinElmer Showcases Enhanced Clarus Nova GC at Analytica 2026,” PerkinElmer Corporate News, perkinelmer.com.

Asia-Pacific is the fastest-growing regional segment in the chromatography software market with a 9.15% CAGR through 2031. China is expanding its role in the chromatography software market as data integrity expectations rise and domestic biopharma producers need compliant electronic records for both local and export-facing submissions. India adds a second growth layer because CRO and CDMO expansion requires outsourcing partners to use software controls that match sponsor expectations across regulated workflows. Japan supports the chromatography software market as both a buyer and an innovator, with Shimadzu’s PeakIntelligence showing how AI-assisted peak handling is moving into routine chromatography software environments. Middle East and Africa and South America remain smaller markets, but they are still developing as pharmaceutical manufacturing, accredited testing, and local compliance frameworks create a broader installed base over time.

Competitive Landscape

The chromatography software market is moderately consolidated at the enterprise tier, where Agilent Technologies, Waters Corporation, Thermo Fisher Scientific, and Shimadzu Corporation hold the largest installed bases through linked hardware and software offerings. The chromatography software market increasingly rewards ecosystem depth rather than isolated features, because buyers want method execution, compliance, integration, review, and connectivity to work inside one validated environment. Agilent has widened this ecosystem through OpenLab, USP-linked method execution, and Virscidian connectivity, while Waters has expanded waters_connect as a cloud-enabled informatics layer across broader laboratory workflows. Waters’ 2026 combination with BD’s Biosciences and Diagnostic Solutions businesses also points to a wider push toward connected life sciences data platforms rather than stand-alone separations informatics.

The chromatography software market is more fragmented in the mid-market and specialist layers. Companies such as ACD/Labs, S-Matrix, ChromSword, DataApex, and Lablicate compete where buyers want method optimization, open compatibility, or workflow-specific depth that large integrated suites do not always provide in equal measure. The Allotrope Simple Model Certification Pilot Program could become a meaningful competitive turning point because broader open-standard certification would reduce vendor lock-in in mixed fleet environments and raise the value of interoperability support. Research published in Digital Discovery also shows that AI-native anomaly detection for automated HPLC work is moving closer to practical deployment, which adds pressure on established vendors to bring more automation into routine data review.

The chromatography software market still favors vendors that can provide strong compliance documentation and migration support, because those services reduce friction in regulated buying decisions. Interoperability is now a stronger competitive factor as laboratories try to manage older instruments and newer platforms without breaking data continuity. Cloud and hybrid readiness are becoming more important in the chromatography software market because multi-site organizations want broader data visibility without rebuilding every local environment from the ground up. Specialist vendors can still win when they solve a clear workflow problem better than enterprise suites do, especially in method development, metabolomics, and open-format use cases. Competition in the chromatography software market is therefore active across tiers, but leadership remains strongest with vendors that combine validation support, installed base depth, and platform connectivity.

Chromatography Software Industry Leaders

Agilent Technologies, Inc.

Shimadzu Corporation

Thermo Fisher Scientific Inc.

Waters Corporation

PerkinElmer Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: Molnár-Institute extended DryLab Automation integration to Agilent OpenLab CDS, enabling automated method optimization data import from OpenLab directly into DryLab for accelerated method evaluation without manual data transfer. Agilent users gain access to the Automation Module's enhanced efficiency and network-integrated access across laboratory systems.

- June 2026: Agilent Technologies and Sound Analytics announced a collaboration to deliver an integrated LC–triple quadrupole MS workflow for drug metabolism and pharmacokinetics (DMPK) laboratories, combining Agilent's 1290 Infinity III LC system and 6495D triple quadrupole mass spectrometer with Sound Analytics' LeadScape software. The partnership targets biopharma DMPK labs seeking to improve data quality and accelerate drug development timelines through workflow-optimized software integration.

Global Chromatography Software Market Report Scope

As per the scope of the report, chromatography software refers to specialized computer programs designed to control, acquire, analyze, and interpret data generated from chromatography experiments. These software solutions assist in managing instrument operation, processing complex analytical data, identifying and quantifying compounds, and generating reports.

The chromatography software market is segmented by software type into standalone software and integrated software; by deployment model into on-premise software and web- and cloud-based software; by purpose into chromatography data systems, CDS, specialist and application-specific modules, offline and data review software, and open-source and cloud platforms; by end user into pharmaceutical and biotechnology companies, contract research organizations, academic and research institutes, environmental testing laboratories, food and beverage companies, and other end users; and by geography into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Standalone Software |

| Integrated Software |

| On-Premise Software |

| Web and Cloud-Based Software |

| Chromatography Data Systems (CDS) |

| Specialist and Application-Specific Modules |

| Offline and Data Review Software |

| Open-Source and Cloud Platforms |

| Pharmaceutical and Biotechnology Companies |

| Contract Research Organizations |

| Academic and Research Institutes |

| Environmental Testing Laboratories |

| Food and Beverage Companies |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Software Type | Standalone Software | |

| Integrated Software | ||

| By Deployment Model | On-Premise Software | |

| Web and Cloud-Based Software | ||

| By Purpose | Chromatography Data Systems (CDS) | |

| Specialist and Application-Specific Modules | ||

| Offline and Data Review Software | ||

| Open-Source and Cloud Platforms | ||

| By End User | Pharmaceutical and Biotechnology Companies | |

| Contract Research Organizations | ||

| Academic and Research Institutes | ||

| Environmental Testing Laboratories | ||

| Food and Beverage Companies | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2026 value of chromatography software demand worldwide?

The chromatography software market stands at USD 1.49 billion in 2026 and is forecast to reach USD 2.24 billion by 2031 at an 8.55% CAGR.

Which region leads software revenue for chromatography labs?

North America led with 46.61% share in 2025, supported by U.S. pharmaceutical scale and strong regulatory enforcement around electronic records and audit trails.

Which region is expanding the fastest through 2031?

Asia-Pacific is the fastest-growing regional segment with a 9.15% CAGR through 2031, supported by compliance upgrades in China and outsourcing growth in India.

Which software type is strongest in chromatography labs?

Integrated Software is the leading and fastest-growing software type, holding 75.31% share in 2025 and advancing at a 9.38% CAGR through 2031.

Why are cloud deployments gaining attention in laboratory informatics?

Web and Cloud-Based Software is growing at a 9.52% CAGR through 2031 because multi-site pharmaceutical companies and CROs need easier remote access, cross-site review, and scalable deployments.

Which end users create the strongest growth opportunity?

Pharmaceutical and Biotechnology companies remain the largest end-user group with 36.26% share in 2025, while CROs offer the fastest growth at an 8.95% CAGR through 2031 because they need flexible, compliance-ready platforms.

Page last updated on: