Chromatography Accessories And Consumables Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

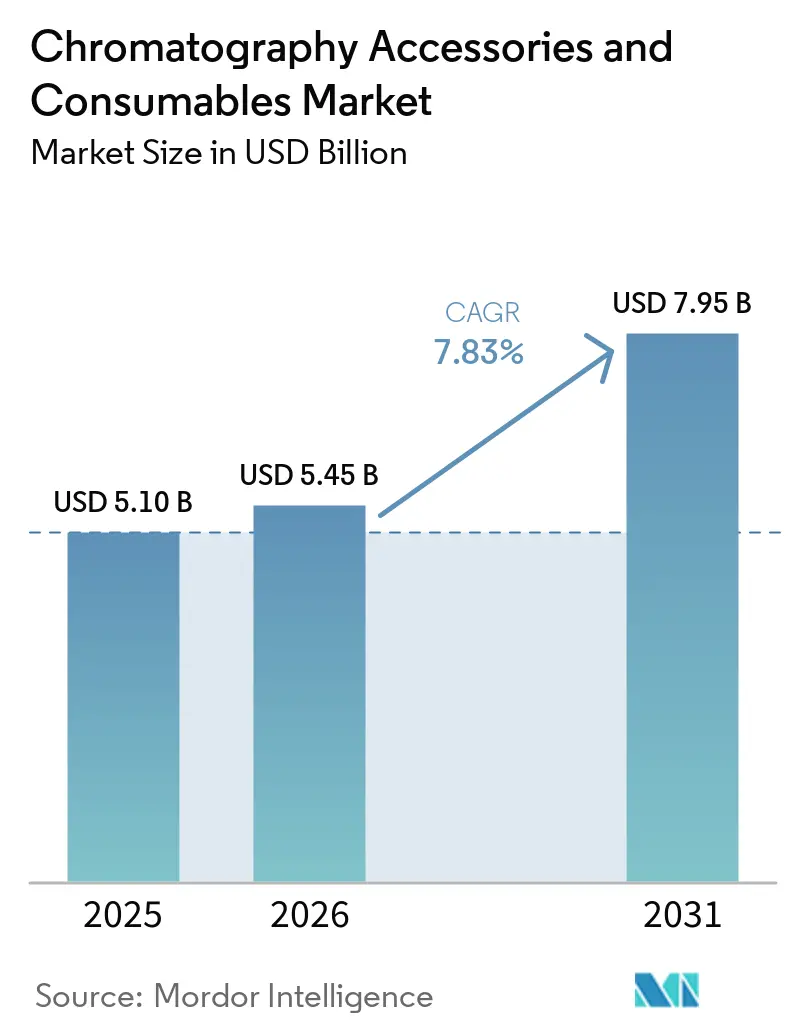

| Market Size (2026) | USD 5.45 Billion |

| Market Size (2031) | USD 7.95 Billion |

| Growth Rate (2026 - 2031) | 7.83% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chromatography Accessories And Consumables Market Analysis by Mordor Intelligence

The Chromatography Accessories And Consumables Market size is expected to increase from USD 5.10 billion in 2025 to USD 5.45 billion in 2026 and reach USD 7.95 billion by 2031, growing at a CAGR of 7.83% over 2026-2031.

Demand accelerates as biopharma pipelines add complex modalities that require more chromatographic tests per batch, while food-safety and environmental laboratories face tighter global regulations that expand routine sample volumes. Instrument vendors simultaneously migrate customers from conventional HPLC to UHPLC and LC-MS platforms, shortening column lifetimes and lifting recurring spend on vials, filters, fittings, and MS-grade solvents. Smart, barcoded consumables embedded in new LC systems automate method set-up and reinforce proprietary supply chains that favor large manufacturers. Sustainability mandates intensify product redesign toward miniaturized columns and low-volume solvent workflows, creating premium SKUs that offset price pressure in generic vials and filters.

Key Report Takeaways

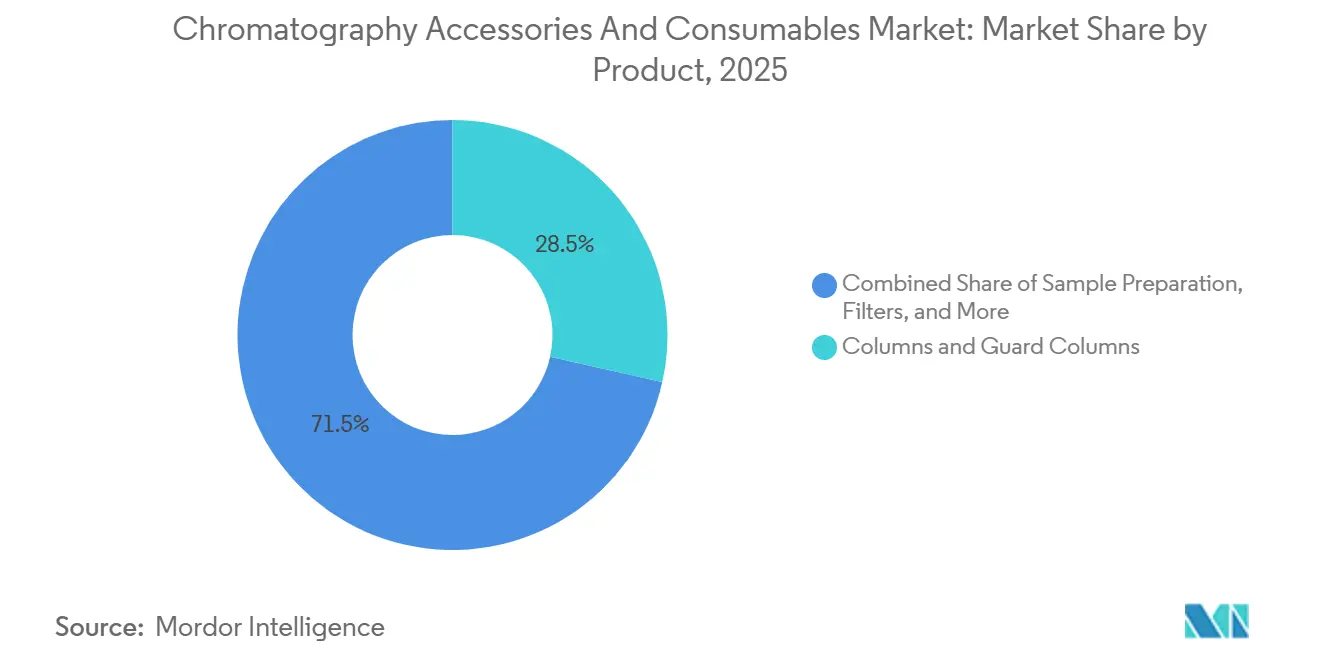

- By product category, Columns & Guard Columns led with 28.5% of the chromatography accessories and consumables market share in 2025, while Filters are projected to advance at an 8.43% CAGR through 2031.

- By chromatography type, Liquid Chromatography commanded 57.38% of the chromatography accessories and consumables market size in 2025 and is forecast to expand at an 8.34% CAGR between 2026 and 2031.

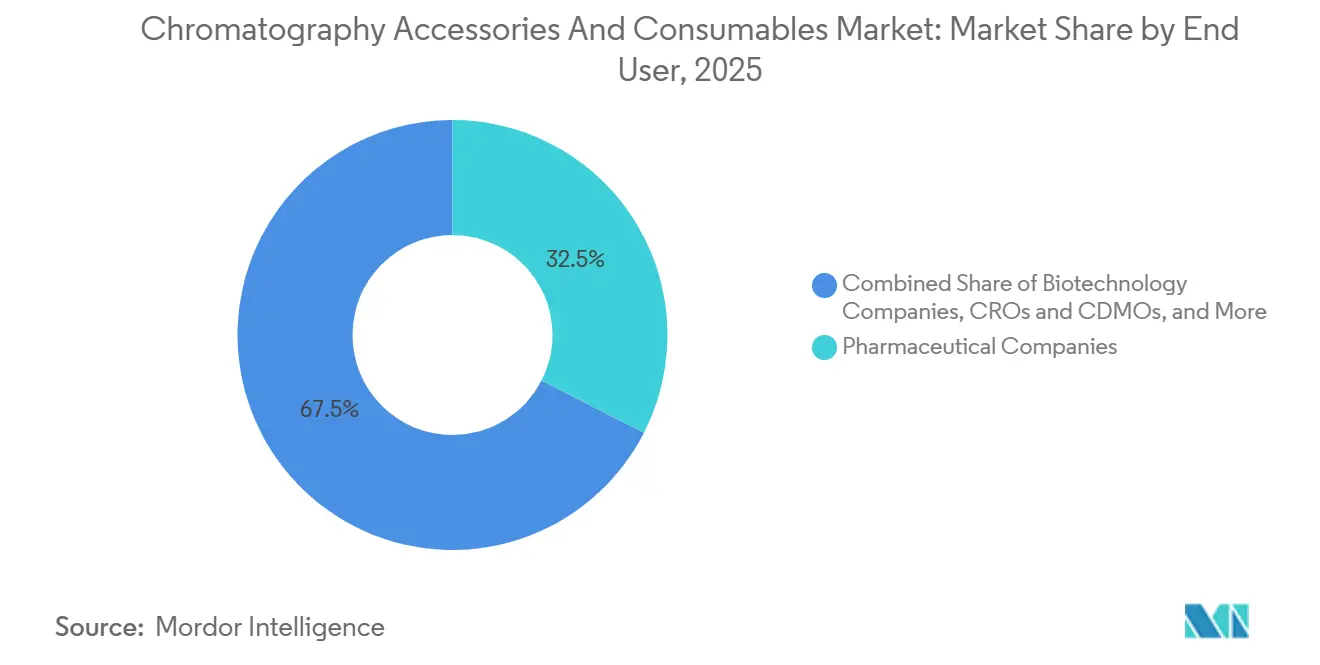

- By end user, Pharmaceutical Companies held 32.48% revenue share in 2025, whereas Biotechnology Companies are set to post the fastest 8.54% CAGR up to 2031.

- By application, QA/QC in Pharmaceutical Manufacturing accounted for a 35.46% share of the chromatography accessories and consumables market size in 2025, and Drug Discovery & Preclinical is climbing at an 8.01% CAGR through 2031.

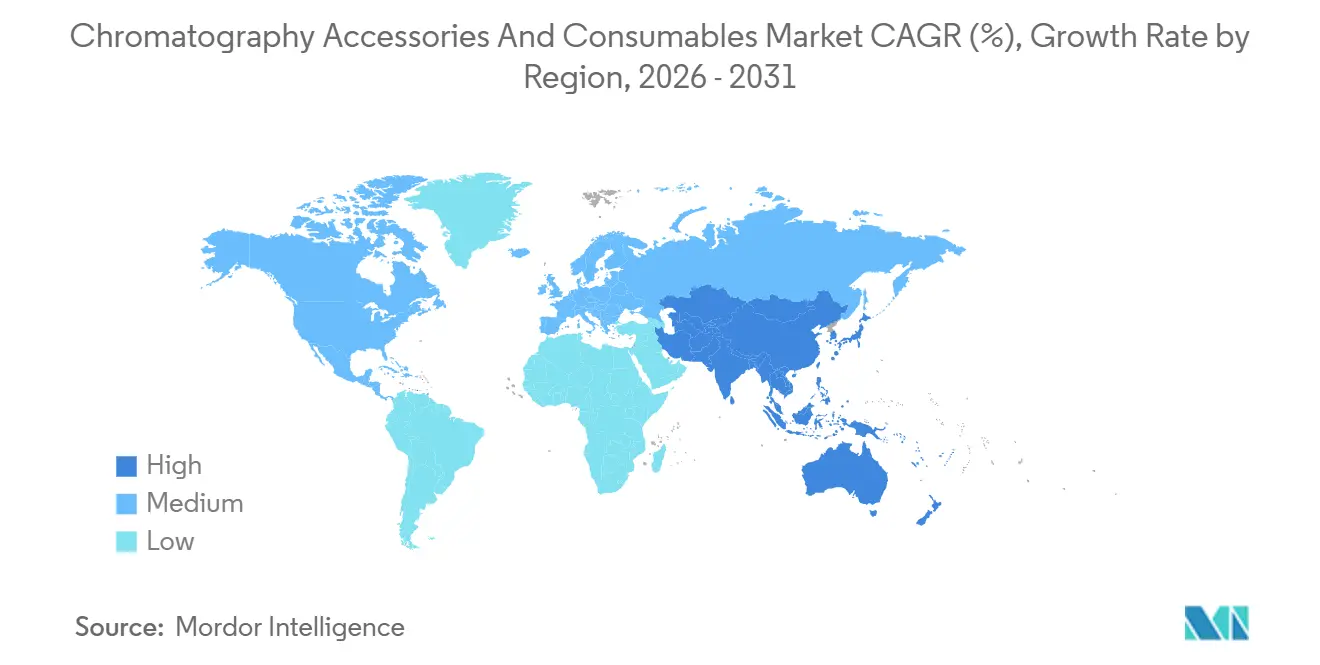

- By geography, North America captured 42.45% revenue in 2025; however, Asia-Pacific is projected to record the highest 8.48% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Chromatography Accessories And Consumables Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Biopharma pipeline expansion and rising GMP analytics drive recurring LC/GC consumable demand | +2.1% | Global, with concentration in North America, Europe, and Asia-Pacific biomanufacturing hubs | Medium term (2-4 years) |

| Regulatory stringency in food safety and environmental testing expands test volumes and lab throughput | +1.8% | Global, with heightened enforcement in EU, North America, and emerging APAC markets | Short term (≤ 2 years) |

| Installed-base upgrades to UHPLC/LC-MS boost pull-through of columns, vials, filters, and solvents | +2.3% | North America & Europe lead; APAC adoption accelerating in China, India, South Korea | Medium term (2-4 years) |

| Vendor-integrated ecosystems with smart/barcoded consumables increase lock-in and repeat purchases | +1.2% | Global, with strongest adoption in regulated pharma/biotech sectors | Long term (≥ 4 years) |

| Green chromatography spurs demand for new low-volume SKUs | +0.9% | Europe leads; North America and APAC following with sustainability mandates | Long term (≥ 4 years) |

| Outsourced R&D/QA to CROs/CDMOs concentrates spend with standardized consumables lists | +1.4% | Global, with CDMO capacity concentrated in North America, Europe, China, and India | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Biopharma Pipeline Expansion And Rising GMP Analytics Drive Recurring LC/GC Consumable Demand

Complex modalities such as gene therapies, mRNA vaccines, and antibody-drug conjugates require multiple chromatographic assays per batch, raising column replacement frequency and solvent consumption. Waters launched the BioAccord LC-MS in 2025, optimized for viral-vector and lipid-nanoparticle characterization, which uses specialized reversed-phase and size-exclusion columns at up to five times the rate of small-molecule QC tests. Agilent’s AdvanceBio oligonucleotide columns, commercialized in 2024, deliver high-resolution separation for antisense and siRNA therapeutics and command 20% price premiums over generic C18 phases. Contract manufacturers scale capacity to meet sponsor demand; Lonza’s USD 1 billion Stein facility opening in 2026 will house multiple GMP suites that consume prepacked columns and single-use flow paths continuously. Samsung Biologics reported 784,000 liters of bioreactor capacity in 2025, implying linear growth in downstream purification consumables locked into validated vendor lists.

Regulatory Stringency In Food Safety And Environmental Testing Expands Throughput

The U.S. FDA’s LAAF program, effective December 2024, obliges ISO/IEC 17025 accreditation for mycotoxin and allergen testing, accelerating orders for certified reference materials and traceability-enabled columns[1]U.S. Food and Drug Administration, “Laboratory Accreditation for Analyses of Foods,” fda.gov. European Regulation 2025/854 adds 27 pesticide residues to the mandatory monitoring list for the 2026-2028 cycle, forcing laboratories to adopt multi-residue LC-MS/MS methods that rely on QuEChERS kits and high-capacity analytical columns. Global networks such as Eurofins and SGS standardize consumables across hundreds of labs to streamline audits and method transfer, concentrating spend with a handful of approved suppliers. The U.S. EPA’s enforceable PFAS limits promulgated in 2024 pushed vendors to offer PFAS-free hardware; Agilent delivered a contamination-free conversion kit that opened a new consumables sub-segment. ECHA’s 2025 compendium spelled out LC-MS/MS and SPE requirements for REACH enforcement, codifying pull-through of vials, SPE cartridges, and extraction sorbents across the European Union.

Installed-Base Upgrades To UHPLC/LC-MS Boost Pull-Through Of Columns, Vials, And Solvents

UHPLC systems operate above 15,000 psi, and their sub-2 µm particle columns wear out after 500-1,000 injections versus 2,000-plus on conventional HPLC, lifting replacement rates by 2-3×. Agilent’s Infinity III LC, released in 2024, auto-reads barcoded columns to set flow and gradient parameters, shrinking setup times and anchoring consumable loyalty. Waters’ ACQUITY UPLC and Arc HPLC refresh drove double-digit chemistry revenue in late 2025 as customers accelerated column swaps every three to six months under high-throughput QC protocols. Thermo Fisher bundled Vanquish Neo UHPLC with application-specific kits, embedding future column and solvent orders into initial capital contracts. LC-MS workflows additionally require MS-grade solvents and certified low-bleed vials, further expanding the chromatography accessories and consumables market.

Vendor-Integrated Ecosystems With Smart Consumables Increase Lock-In

Manufacturers embed RFID chips and two-dimensional codes into vials, columns, and reagent bottles so software can log part numbers, usage life, and method parameters automatically. InfinityLab Assist links barcoded consumables to LC control software, ensuring only Agilent-approved parts populate validated methods and reducing human error by 40%. Waters ties its NuGenesis SDMS to instrument logs, triggering auto-reorder alerts when column usage nears end-of-life, a feature valued by pharmaceutical QC labs that cannot afford downtime. The razor-and-blade model secures annuity streams, but cost-sensitive academic labs resist proprietary barcodes and often switch to unbranded products, giving Chinese firms such as Welch Materials price-driven openings. Still, regulated sites prefer the compliance documentation that integrated ecosystems supply, sustaining premium margins for top vendors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Commoditization and price pressure in generic vials/filters constrain ASPs | -1.5% | Global, with most acute pressure in Asia-Pacific and price-sensitive academic/environmental segments | Short term (≤ 2 years) |

| Supply volatility in high-purity solvents/silica media extends lead times and safety stocks | -0.8% | Global, with bottlenecks in North America and Europe raw-material supply chains | Medium term (2-4 years) |

| Alternative direct MS/ambient ionization workflows can bypass separations in niche use-cases | -0.6% | North America and Europe clinical/forensic labs; limited APAC adoption | Long term (≥ 4 years) |

| Lab sustainability mandates penalize single-use plastics, tightening demand in disposables | -0.4% | Europe leads; North America and APAC following with regulatory pressure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Commoditization And Price Pressure In Generic Vials And Filters Constrain ASPs

High-volume SKUs such as 2 mL autosampler vials and 0.45 µm syringe filters attract Chinese and Indian producers offering ISO-9001 certified parts at 20-30% discounts, eroding multinational vendor margins. Academic research and environmental labs award tenders to the lowest bid, reducing average selling prices (ASPs) even for premium brands. Global giants bundle consumables with service contracts or instrument purchases to defend volume, but discounts compress gross profit. Merck KGaA maintains premium positioning in GMP applications, yet loses share in routine testing to lower-cost alternatives. As e-commerce platforms expand, buyers compare prices in real time, intensifying competition in commoditized segments.

Supply Volatility In High-Purity Solvents And Silica Extends Lead Times

Spot prices for acetonitrile spiked 40% in early 2025 after production outages, forcing QC labs to carry up to 90 days of inventory to avoid interruptions. High-purity silica, needed for column packing, faces capacity constraints because semiconductor and solar industries compete for the same feedstock, prolonging lead times to 12-16 weeks in the United States and Europe. Vendor vertical integration, exemplified by Merck’s in-house bead production network, mitigates supply risk, but smaller suppliers struggle to guarantee continuity, prompting laboratories to dual-source whenever possible[2]Merck KGaA, “Sustainability and Supply-Chain Report 2025,” merckgroup.com. Some users convert to solvent-saving microflow LC or supercritical fluid chromatography to limit dependence on volatile chemicals, yet capital budgets and method re-validation slow widespread adoption. The resulting uncertainty weighs on procurement plans and tempers growth of the chromatography accessories and consumables market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Columns Continue To Anchor Revenue While Filters Accelerate

Columns & Guard Columns delivered 28.5% of 2025 revenue, cementing their role as the highest-value disposables in liquid and gas separations. The chromatography accessories and consumables market size for columns reached USD 1.46 billion in 2025 and is forecast to climb steadily as laboratories shorten replacement cycles to ensure peak performance. Filters, although lower in ticket price, are set to rise at an 8.43% CAGR due to single-use bioprocessing lines that require sterile, pre-validated membrane units before every batch. Vendors differentiate columns through novel stationary-phase chemistries; Restek’s Raptor ARC-18 column addresses acidic and basic drugs where legacy C18 phases falter, commanding price premiums without sacrificing lifetime. Meanwhile, generic vial suppliers crowd the commodity end, dragging margins but expanding overall unit volume, especially in academic procurement channels. Tubing and fittings grow in tandem with UHPLC deployment because high-pressure ratings and low-dispersion geometries cannot be met by low-cost substitutes, sustaining high return on invested capital for niche component makers.

Agilent’s roll-out of Poroshell 120 HILIC-OH5 and PFP phases speaks to a shift toward application-specific consumables that solve emerging analytical pain points like PFAS or oligonucleotide separations. Waters complements this strategy with ionKey/MS for proteomics, a microfluidic cartridge that trims solvent waste by 99% yet sells at USD 800-1,200 despite shorter lifetimes, reinforcing a premium recurring model. Conversely, autosampler vials, caps, and closures face intense commoditization, pushing branded players to focus on traceability, certified cleanliness, and smart-tag features that generic entrants cannot easily replicate. Solvents and buffers remain a large but low-margin pool where vertical integration, logistics scale, and bulk contracts dictate profitability.

By Chromatography Type: Liquid Chromatography Dominates As Ion Chromatography Gains Attention

Liquid platforms accounted for 57.38% of 2025 spend, underpinned by regulatory reliance on LC-UV and LC-MS for drug release testing, food residue monitoring, and metabolite profiling. The chromatography accessories and consumables market share for liquid methods is projected to widen because LC-MS workflows consume more columns per study and require MS-grade solvents that sell at double the price of analytical-grade equivalents. Gas chromatography maintains relevance in volatile organic compound and petrochemical assays, yet unit growth lags LC as environmental regulations skew toward multi-residue pesticide and PFAS methods best handled by LC-MS/MS.

Ion chromatography, historically a niche, is enjoying new relevance after U.S. and European agencies set parts-per-trillion PFAS limits in water, driving purchases of suppressor cartridges, eluent regenerators, and specialty columns that integrate seamlessly with Thermo Fisher’s ICS-7000 Plus. Shimadzu’s Nexera IC-40, launched in 2025, further democratizes ion analysis for mid-sized labs by packaging high-sensitivity detectors with compact footprints. Supercritical fluid chromatography, though below 2% of revenue, grows in pharma purification because reduced solvent disposal aligns with corporate sustainability mandates. Such diversification across separation modes insulates the chromatography accessories and consumables market from technology substitution risk.

By End User: Pharma Remains The Revenue Anchor, Biotech Emerges As The Growth Engine

Pharmaceutical manufacturers contributed 32.48% of revenue in 2025, reflecting stringent batch-release testing across small-molecule and biologic pipelines. Yet the modality shift towards nucleic-acid and cell-based therapies propels biotech companies to an 8.54% CAGR, boosting demand for high-resolution sizing columns, sterile filters, and MS-grade solvents tailored to large biomolecules. CROs and CDMOs consolidate orders across dozens of sponsor programs, amplifying purchasing power and ensuring supply-chain reliability; Catalent’s Maryland expansion alone will house enough LC-MS capacity to triple column turnover versus 2023 levels.

Academic institutes and government labs focus on cost, opting for generic consumables except when grant mandates specify certified traceability. Clinical and diagnostic laboratories adopt LC-MS/MS for therapeutic drug monitoring and steroid profiling, but also experiment with direct, ambient ionization devices that bypass chromatography to save time and disposables, partially cannibalizing future column demand. Food and environmental testing labs, led by Eurofins and SGS, broaden their test menus in response to evolving regulations, locking in multi-year agreements with suppliers able to guarantee global lot consistency.

By Application: QA/QC Anchors Volume As Early-Stage Discovery Shows Rapid Upside

QA/QC in Pharmaceutical Manufacturing represented 35.46% of 2025 spend because every commercial batch must pass identity, potency, and impurity checks, consuming columns and solvents at predictable intervals. Drug Discovery & Preclinical, though smaller, is forecast to outpace the overall chromatography accessories and consumables market at an 8.01% CAGR since high-throughput screens for lead identification often sacrifice column longevity for speed, elevating replacement frequencies. Biologics & Bioprocess analytics surges alongside expanded monoclonal antibody and viral-vector production, creating recurring orders for protein-A columns, 0.22 µm sterilizing filters, and single-use flow paths.

Clinical diagnostics gain share as hospitals migrate immunosuppressant and hormone assays from immunoassays to LC-MS/MS for greater specificity, although reimbursement pressure caps ASPs. Food safety tests, guided by EU pesticide directives and U.S. FDA rules, keep QuEChERS, SPE sorbents, and multi-residue columns in continuous demand. Environmental monitoring remains a steady, regulation-driven niche, especially for PFAS and microplastic studies that rely on robust chromatographic separations to reach sub-ng/L detection limits.

Geography Analysis

North America contributed 42.45% of 2025 revenue as the United States concentrates FDA-regulated pharmaceutical output and houses a dense network of CROs and reference labs. Instrument upgrades gained pace after the FDA formalized electronic-record guidance that favors barcoded consumables, accelerating proprietary pull-through. Canada’s environmental authorities adopted stringent PFAS guidelines in 2025, triggering provincial funding for LC-MS/MS modernization in public laboratories, further enlarging consumables demand.

Europe ranks second by value and leads sustainability trends. EMA’s ICH Q3D guideline incentivizes low-volume separations, pushing adoption of 1.0 mm internal-diameter columns that trim solvent waste by up to 90%. Laboratories in Germany, France, and the Nordics integrate life-cycle assessments into procurement, prioritizing recycled packaging and microflow devices. EU Regulation 2025/854 on pesticide residues compels at least 30% more annual LC-MS/MS runs across official control labs, translating into higher column turnover and higher purity solvent orders. Eastern Europe shows fast take-up of ion chromatography for PFAS thanks to cohesion-fund grants earmarked for water-quality improvements.

Asia-Pacific is the growth engine, posting an 8.48% CAGR through 2031 as China and India scale biosimilar and vaccine capacity. Agilent inaugurated a 12,500 sq ft Solution Center in Manesar, India, in May 2025 to train users on UHPLC and LC-MS maintenance, cementing downstream consumables pull-through. Chinese domestic reagent makers, backed by local venture capital, penetrate tier-two city markets with sub-USD 200 C18 columns, reshaping competitive dynamics[3]China General Administration of Customs, “Reagent Import Statistics 2024,” customs.gov.cn. Japan supports demand through precision equipment exports, while Australia’s PFAS remediation programs fuel local adoption of ion chromatography and SPE cartridges.

South America grows at mid-single digits led by Brazil’s agribusiness, which relies on multi-residue pesticide testing for export certification, driving purchases of QuEChERS kits and GC liners. The Middle East benefits from petrochemical diversification; Shimadzu expanded a 3,800 m² integration facility in Dubai in 2024 to deliver GC systems pre-configured for refinery applications, pushing regional demand for septa and liners. Africa remains nascent but gains incremental momentum as multinational mining and beverage firms establish compliance labs that mirror European QA protocols.

Competitive Landscape

Five suppliers, Agilent Technologies, Thermo Fisher Scientific, Waters Corporation, Merck KGaA, and Danaher’s Cytiva unit, control a majority share, leveraging broad portfolios and captive instrument ecosystems. Agilent’s InfinityLab Assist, introduced in 2024, embeds barcode recognition to enforce exclusive use of branded columns and vials, trimming set-up errors by 40% and locking repeat purchases. Waters links column serial numbers with NuGenesis SDMS to trigger automatic replenishment, ensuring GMP labs never breach validated method conditions. Merck extends vertical integration by acquiring JSR Life Sciences’ chromatography arm in April 2026, adding Amsphere Protein A resins and strengthening its downstream antibody purification lineup.

Price competition intensifies below the premium tier. Chinese challengers Welch Materials and Agela Technologies sell barcode-compatible columns at 20-30% discounts, winning share in academic and environmental segments that lack strict brand requirements. Ambient ionization devices such as Thermo Fisher’s VeriSpray PaperSpray system threaten to bypass LC in targeted clinical assays, potentially diverting consumables spend into direct-MS reagents. Innovation now orbits sustainability and miniaturization: Waters’ ionKey/MS cuts solvent volume 99%, Agilent removed 6,073 lb of plastic trays from column packaging in 2024, and Shimadzu’s IC-40 achieves sub-ppt PFAS limits in a compact footprint, all differentiators that justify premium pricing despite rising raw-material costs.

CRO and CDMO consolidation further concentrates purchasing. Lonza, Catalent, and WuXi Biologics negotiate multiyear, volume-based contracts that favor suppliers capable of global lot consistency and audit support. Such agreements stabilize revenue for top vendors but intensify margin pressure on smaller firms unable to meet stringent delivery windows. The net effect sustains moderate market concentration and high barriers to entry in regulated niches even as value-tier offerings proliferate elsewhere.

Chromatography Accessories And Consumables Industry Leaders

Agilent Technologies, Inc.

Merck KGaA

Thermo Fisher Scientific Inc.

Waters Corporation

Danaher Corporation (Cytiva)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Merck closed the acquisition of JSR Life Sciences’ chromatography business, adding Amsphere Protein A resins to its downstream portfolio.

- May 2025: Shimadzu partnered with Core Separations to distribute supercritical fluid chromatography and extraction systems across Southeast and South Asia (ex-India), broadening regional access to solvent-saving technology.

Global Chromatography Accessories And Consumables Market Report Scope

As per the scope of the report, chromatography accessories and consumables refer to the supplementary items and materials used in chromatography processes to facilitate, enhance, or support the separation and analysis of chemical substances.

The segmentation for the chromatography accessories and consumables market is categorized by product, chromatography type, end user, application, and geography. By product, the market includes columns and guard columns, sample preparation, filters, vials, caps, closures, well plates, tubing, fittings, ferrules, unions, valves, solvents, buffers, adsorbents, GC supplies, autosampler and detector accessories, calibration and derivatization reagents, and column hardware and packing materials. By chromatography type, it is segmented into liquid chromatography (HPLC, UHPLC), gas chromatography, ion chromatography, and others (size-exclusion chromatography, affinity chromatography, chiral chromatography, etc.). By end user, the market is divided into pharmaceutical companies, biotechnology companies, CROs and CDMOs, academic and research institutes, clinical and diagnostic laboratories, and others (food and beverage testing labs, environmental testing laboratories, forensics and public safety labs, etc.).

By application, the segmentation includes drug discovery and preclinical, QA/QC in pharmaceutical manufacturing, biologics and bioprocess analytics, clinical diagnostics and therapeutic drug monitoring, food safety and quality, and others (environmental monitoring, forensics and toxicology, specialty chemicals and petrochemicals, etc.). By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Columns & Guard Columns |

| Sample Preparation |

| Filters |

| Vials, Caps, Closures, Well Plates |

| Tubing, Fittings, Ferrules, Unions, Valves |

| Solvents, Buffers, Adsorbents |

| GC Supplies |

| Autosampler & Detector Accessories |

| Calibration & Derivatization Reagents |

| Column Hardware & Packing Materials |

| Liquid Chromatography (HPLC, UHPLC) |

| Gas Chromatography |

| Ion Chromatography |

| Others (Size-Exclusion Chromatography, Affinity Chromatography, Chiral Chromatography, etc.) |

| Pharmaceutical Companies |

| Biotechnology Companies |

| CROs & CDMOs |

| Academic & Research Institutes |

| Clinical & Diagnostic Laboratories |

| Others (Food & Beverage Testing Labs, Environmental Testing Laboratories, Forensics & Public Safety Labs, etc.) |

| Drug Discovery & Preclinical |

| QA/QC in Pharmaceutical Manufacturing |

| Biologics & Bioprocess Analytics |

| Clinical Diagnostics & Therapeutic Drug Monitoring |

| Food Safety & Quality |

| Others (Environmental Monitoring, Forensics & Toxicology, Specialty Chemicals & Petrochemicals, etc.) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Columns & Guard Columns | |

| Sample Preparation | ||

| Filters | ||

| Vials, Caps, Closures, Well Plates | ||

| Tubing, Fittings, Ferrules, Unions, Valves | ||

| Solvents, Buffers, Adsorbents | ||

| GC Supplies | ||

| Autosampler & Detector Accessories | ||

| Calibration & Derivatization Reagents | ||

| Column Hardware & Packing Materials | ||

| By Chromatography Type | Liquid Chromatography (HPLC, UHPLC) | |

| Gas Chromatography | ||

| Ion Chromatography | ||

| Others (Size-Exclusion Chromatography, Affinity Chromatography, Chiral Chromatography, etc.) | ||

| By End User | Pharmaceutical Companies | |

| Biotechnology Companies | ||

| CROs & CDMOs | ||

| Academic & Research Institutes | ||

| Clinical & Diagnostic Laboratories | ||

| Others (Food & Beverage Testing Labs, Environmental Testing Laboratories, Forensics & Public Safety Labs, etc.) | ||

| By Application | Drug Discovery & Preclinical | |

| QA/QC in Pharmaceutical Manufacturing | ||

| Biologics & Bioprocess Analytics | ||

| Clinical Diagnostics & Therapeutic Drug Monitoring | ||

| Food Safety & Quality | ||

| Others (Environmental Monitoring, Forensics & Toxicology, Specialty Chemicals & Petrochemicals, etc.) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will the chromatography accessories and consumables market be by 2031?

The chromatography accessories and consumables market size is forecast to reach USD 7.95 billion by 2031, expanding at a 7.83% CAGR over 2026-2031.

Which product category contributes the most revenue today?

Columns & Guard Columns accounted for 28.5% of 2025 sales, making them the single largest revenue generator across all product lines.

Which region is expected to grow the fastest through 2031?

Asia-Pacific is projected to post the highest 8.48% CAGR through 2031 as China and India scale biosimilar manufacturing and contract testing capacity.

What factors are driving demand among biotechnology companies?

Rapid expansion of gene therapies, mRNA vaccines, and antibody-drug conjugates increases analytical throughput, lifting biotechnology company spend at an 8.54% CAGR through 2031.

How are sustainability mandates influencing product design?

Laboratories favor miniaturized columns and solvent-saving devices such as Waters' ionKey/MS, which reduces solvent use by 99% and aligns with corporate carbon commitments.

Page last updated on: