Choroidal Neovascularization Treatment Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

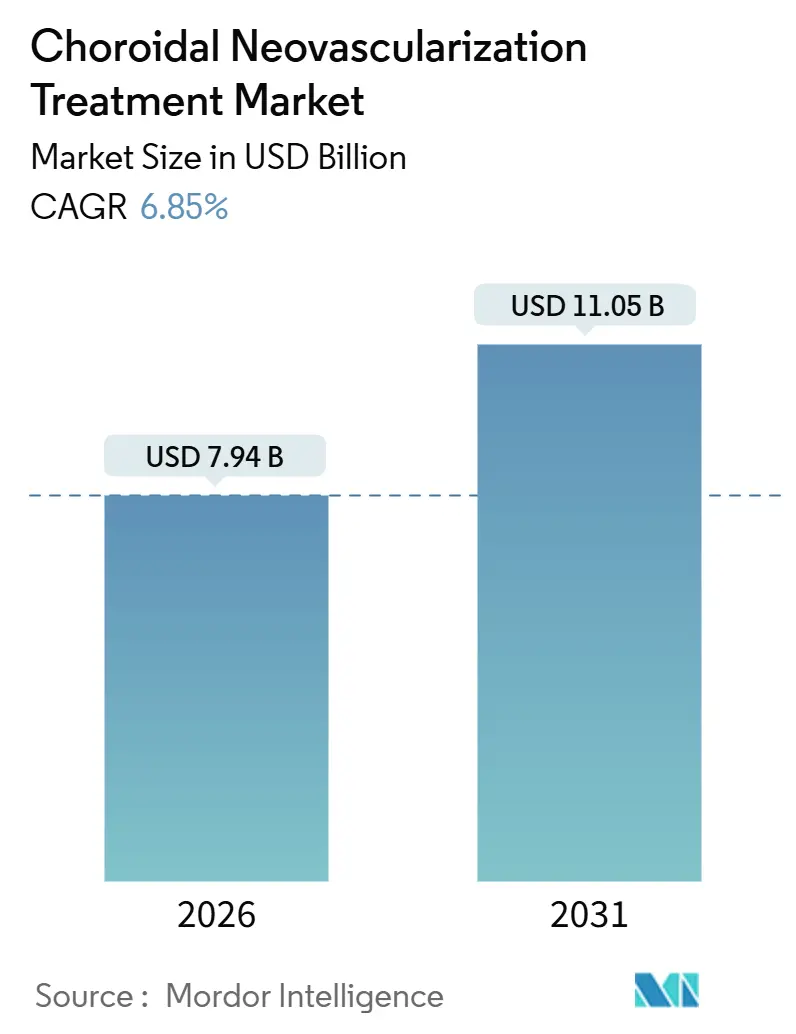

| Market Size (2026) | USD 7.94 Billion |

| Market Size (2031) | USD 11.05 Billion |

| Growth Rate (2026 - 2031) | 6.85% CAGR |

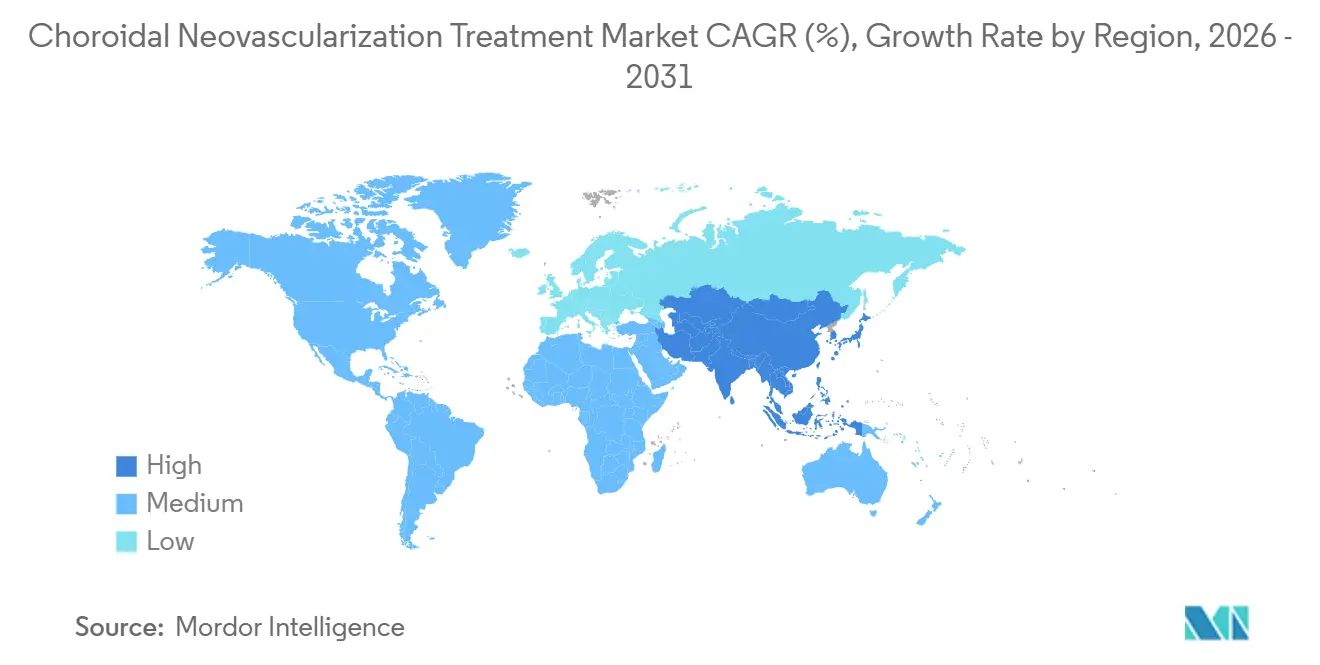

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Choroidal Neovascularization Treatment Market Analysis by Mordor Intelligence

The Choroidal Neovascularization Treatment Market size is estimated at USD 7.94 billion in 2026, and is expected to reach USD 11.05 billion by 2031, at a CAGR of 6.85% during the forecast period (2026-2031).

Biosimilar aflibercept and ranibizumab, launched between 2024 and 2025, are lowering unit prices across Europe and several Asia-Pacific economies, while treat-and-extend regimens are trimming annual injection counts without eroding visual gains. Wider optical coherence tomography angiography (OCTA) reimbursement, growing home OCT use, and an aging global population enlarge the therapy-eligible pool, partly offsetting revenue compression. Concurrently, sustained-delivery implants and high-dose aflibercept aim to defend originator margins, yet payer step-therapy rules and biosimilar mandates temper premium uptake. Altogether, pricing pressure, dosing-interval expansion, and demographic tailwinds interact to re-shape profit pools inside the choroidal neovascularization treatment market.

Key Report Takeaways

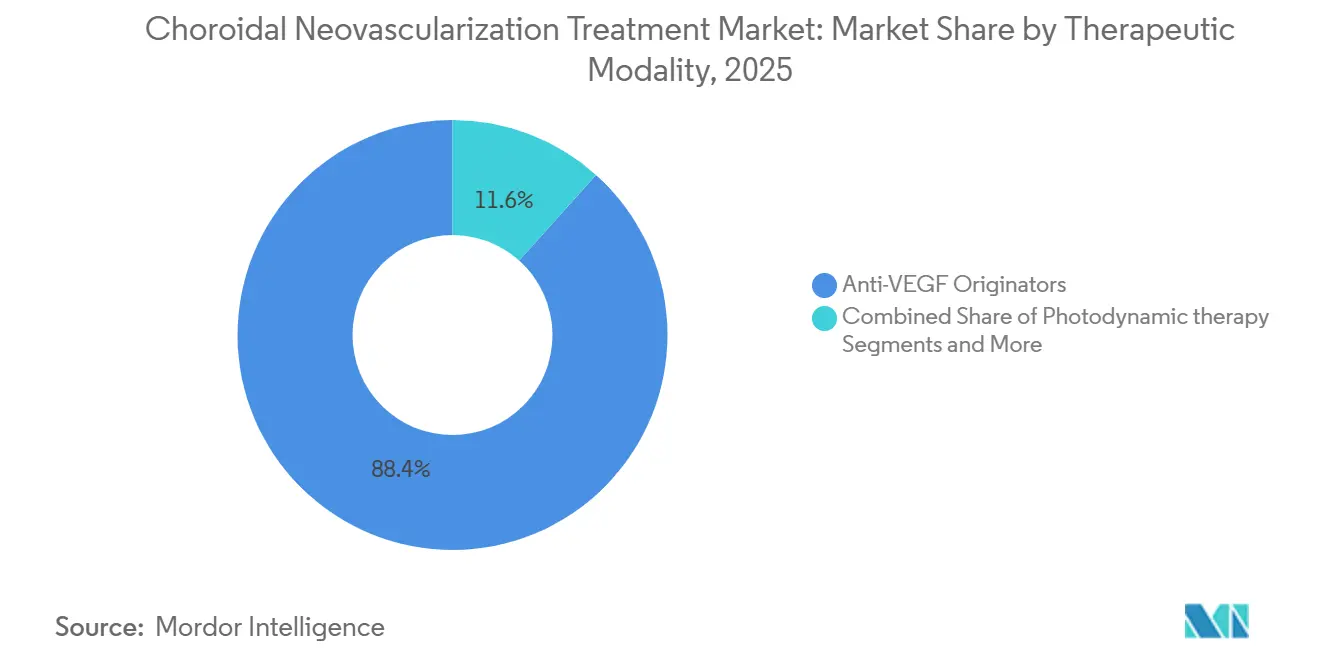

- By therapeutic modality, anti-VEGF originators led with 88.36% choroidal neovascularization treatment market share in 2025, sustained-delivery implants are forecast to expand at a 10.22% CAGR through 2031.

- By delivery modality, intravitreal injection retained 74.24% of the choroidal neovascularization treatment market size in 2025, sustained-release implants are expected to grow at a 9.63% CAGR between 2026 and 2031.

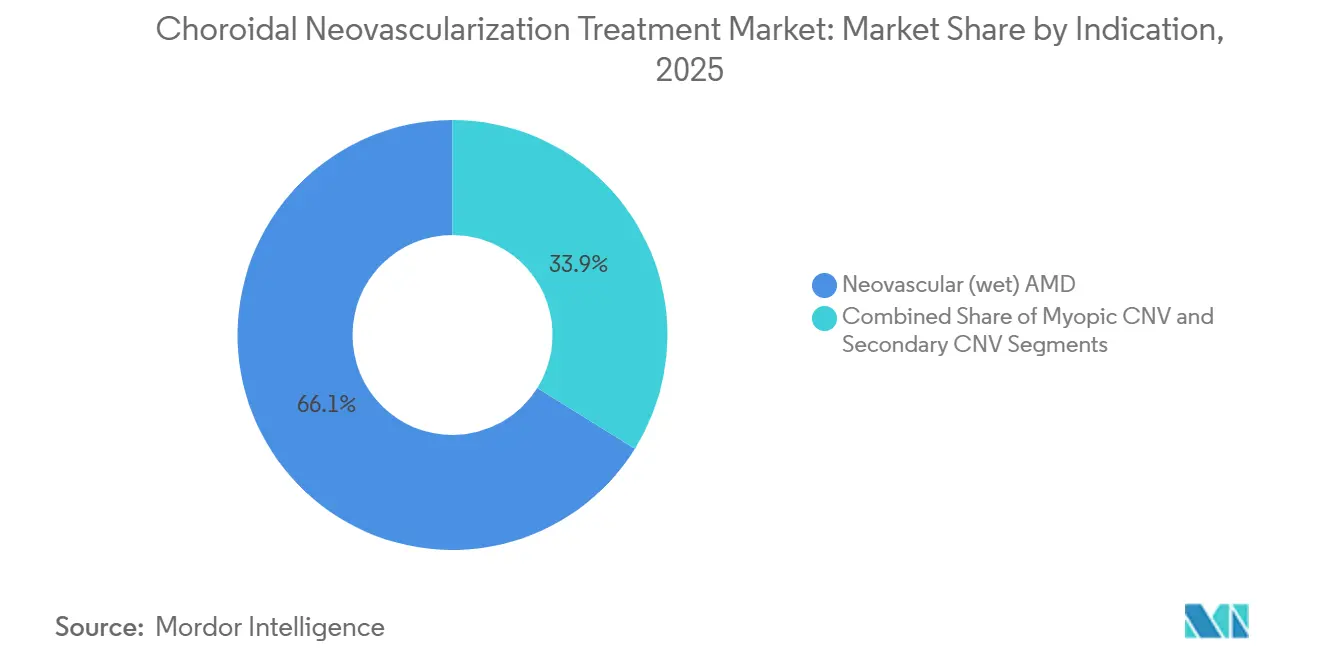

- By indication, neovascular AMD contributed 66.13% revenue share in 2025; myopic CNV is projected to post an 8.77% CAGR to 2031.

- By geography, North America held 37.44% of 2025 revenue, whereas Asia-Pacific is set to advance at an 8.14% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Choroidal Neovascularization Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Shift to Extended-Interval Anti-VEGF | 1.8% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| Expanding Access Via Anti-VEGF Biosimilars | 1.5% | EU, APAC core (Japan, South Korea, Australia), emerging in Latin America | Short term (≤ 2 years) |

| Wider OCT/OCTA Adoption and Reimbursement Expanding Detection and Treatment | 1.3% | North America, EU, urban APAC (China Tier-1 cities, Japan) | Medium term (2-4 years) |

| Aging Populations Expanding the nAMD Patient Pool | 1.2% | Global, with highest impact in Japan, Germany, Italy, South Korea | Long term (≥ 4 years) |

| Home OCT and Remote Monitoring Expand Treated Pool | 0.7% | North America pilot markets, select EU regions | Long term (≥ 4 years) |

| APAC High-Myopia Surge Increases mCNV Incidence | 0.9% | APAC core (China, Japan, South Korea, Singapore) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Shift to Extended-Interval Anti-VEGF

Treat-and-extend regimens now dominate real-world practice, dropping average injections per eye from 7–9 to 5–6 each year. Faricimab supports 16-week intervals for 60% of patients in its first treatment year, easing clinic congestion and travel burdens while lowering per-patient revenue.[1]Roche Communications, “Roche Announces TENAYA and LUCERNE Trial Extensions for Vabysmo,” Roche, roche.comPhysicians welcome the balance between fewer visits and maintained acuity, yet manufacturers must chase volume growth in cost-sensitive regions to offset revenue dilution within the choroidal neovascularization treatment market.

Expanding Access Via Anti-VEGF Biosimilars

Yesafili, Opuviz, and other aflibercept biosimilars launched in 2025 at 20–30% discounts, triggering mandatory substitution policies in Germany, France, and the United Kingdom and reaching roughly one-fifth of new-start patients within months.[2]European Medicines Agency, “First Aflibercept Biosimilars Recommended for Approval,” European Medicines Agency, ema.europa.eu Japan approved Byooviz for ranibizumab in 2024, and middle-income Asia-Pacific nations rapidly followed, lifting treated volumes and broadening geographic participation in the choroidal neovascularization treatment market.

Wider OCT/OCTA Adoption and Reimbursement

Medicare broadened CPT 92134 reimbursement in 2024, propelling OCTA penetration from 20% of U.S. retina clinics in 2022 to nearly 40% in 2025.[3]Centers for Medicare & Medicaid Services, “Medicare Physician Fee Schedule 2024 Final Rule,” Centers for Medicare & Medicaid Services, cms.govOCTA detects subclinical neovascular membranes sooner than fluorescein angiography, enabling earlier therapy starts that enlarge lifetime treatment demand. Germany and France adopted similar reimbursement codes the same year, while Beijing and Shanghai pilots signal forthcoming nationwide Chinese coverage—collectively strengthening diagnostic pipelines that feed the choroidal neovascularization treatment market.

Aging Populations Expanding the nAMD Patient Pool

United Nations projections show the global 65-plus cohort rising from 770 million in 2025 to 950 million by 2031. Wet AMD prevalence escalates rapidly beyond age 70, so Japan, Germany, and Italy face sustained anti-VEGF volumes even amid unit-price erosion. This demographic engine steadies baseline revenue across mature markets and reinforces the underlying trajectory of the choroidal neovascularization treatment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Treatment Burden and Adherence Drop-Off with Frequent Intravitreal Injections | -0.9% | Global, with highest impact in rural and underserved regions | Short term (≤ 2 years) |

| Pricing Pressure and Reimbursement Headwinds | -0.7% | North America, EU core markets, Japan | Medium term (2-4 years) |

| Global Verteporfin (PDT) Supply Constraints Limiting Certain CNV Care Pathways | -0.4% | Global, with acute shortages in North America and EU | Short term (≤ 2 years) |

| Anti-VEGF Non-Responders/Tachyphylaxis Necessitating Alternatives | -0.6% | Global, affecting 10-15% of treated patients | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Treatment Burden and Adherence Drop-Off

A JAMA Ophthalmology study of 12,000 Medicare enrollees showed that monthly injection regimens doubled discontinuation risk compared with quarterly schedules. Travel logistics, caregiver strain, and needle fatigue cause nearly half of patients to lapse within two years, clipping lifetime revenue potential inside the choroidal neovascularization treatment market. Depot implants aim to cut visit frequency, but surgical requirements and reimbursement gaps slow substitution.

Pricing Pressure and Reimbursement Headwinds

Medicare trimmed facility fees for intravitreal injections by up to 5% in 2025 while Germany’s AMNOG framework forced a 25% EYLEA list-price cut once biosimilars entered. Japan’s biennial revisions reduced ranibizumab reimbursement by 8% in 2024 and will shave aflibercept by 6% in 2026. Step-therapy rules now require biosimilar trials before premium approvals, slowing high-dose and dual-pathway uptake and tightening margins across the choroidal neovascularization treatment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Therapeutic Modality: Originator Dominance Faces Biosimilar and Implant Pressure

Anti-VEGF originators commanded 88.36% of the choroidal neovascularization treatment market during 2025, spearheaded by Regeneron’s EYLEA, Roche’s Lucentis, and Novartis’ Beovu.. Biosimilars quickly gained 12–15% of new-start share in Europe, while sustained-delivery implants such as Susvimo are set for a 10.22% CAGR through 2031. Susvimo generated USD 45 million in 2025, with uptake capped by surgical needs and reimbursement inconsistency. Photodynamic therapy remains niche because of verteporfin shortages, and corticosteroid implants target edema-driven variants rather than mainstream CNV. Regeneron’s high-dose aflibercept achieved USD 1.2 billion in 2025 sales after proving 16-week durability, helping offset biosimilar erosion in the choroidal neovascularization treatment market.

Depot innovation continues. EyePoint adapts Durasert for anti-VEGF delivery, and Ocular Therapeutix advances a six-month tyrosine-kinase inhibitor insert. Biosimilar developers plan pre-filled syringes and auto-injectors by 2026 to streamline clinic workflows and reinforce injection dominance. Gene therapy candidates RGX-314 and ADVM-022 aim for one-time subretinal administration; if pivotal data succeed, implants and injections could face structural demand shifts after 2028, altering long-term revenue patterns in the choroidal neovascularization treatment market.

By Delivery Modality: Injection Entrenchment Meets Implant Upswing

Intravitreal injection held 74.24% of the choroidal neovascularization treatment market in 2025, reflecting two decades of entrenched workflow, with endophthalmitis rates below 0.05%. High-volume practices deliver 30–40 injections daily, sustaining provider revenue. Sustained-release implants are forecast to climb 9.63% per year through 2031 as patients seek fewer visits and payers weigh lifetime cost parity with higher front-loaded device spend. Verteporfin-PDT intravenous infusion has fallen below a 3% share because of drug shortages and anti-VEGF dominance, while gene therapy’s subretinal delivery remains restricted to trials. Auto-injector designs from Coherus and Samsung Bioepis promise quicker in-office turnover, reinforcing injection relevance in the choroidal neovascularization treatment market even as implants accelerate.

By Indication: Wet AMD Still Rules, Myopic CNV Accelerates

Neovascular AMD generated 66.13% of 2025 revenue and will maintain primacy as 70-plus populations expand across the G7, even though extended intervals and biosimilars compress per-patient income. Myopic CNV is projected to grow at an 8.77% CAGR through 2031, fueled by rising high-myopia prevalence in China, Japan, and South Korea. The FDA expanded aflibercept’s label to myopic CNV in 2024, and Japan approved ranibizumab for the same condition in 2023, removing reimbursement hurdles and energizing segment growth inside the choroidal neovascularization treatment market. Secondary CNV, encompassing trauma and inflammatory causes, remains small at 8–10% share but offers steady demand due to younger patient age and higher visual expectations.

Longer life expectancy in younger myopic CNV patients increases cumulative treatment duration and amplifies interest in depot systems or future gene therapy. Under-diagnosis persists where ophthalmic imaging access is scarce, suggesting that wider OCTA availability could unlock incremental volumes for the choroidal neovascularization treatment market.

Geography Analysis

North America captured 37.44% of 2025 revenue. Medicare and commercial coverage remain robust, and dense specialist networks adopt extended-interval therapy early, supporting a 5.8% CAGR through 2031 despite delayed biosimilar availability until at least 2028. Canada broadened faricimab and EYLEA HD coverage in 2025, while Mexico’s public systems lag, limiting access mainly to self-pay urban clinics.

Automatic substitution in Germany, France, and the United Kingdom drove biosimilar share to 22% of new starts within one year, whereas Italy and Spain trail at under 12% due to slower policy roll-out. Price cuts tied to biosimilar entry shaved originator margins, yet broad reimbursement preserves high treatment penetration across major markets.

Asia-Pacific is the fastest growth region at an 8.14% CAGR. Japan enjoys above-80% anti-VEGF uptake and rapidly integrates biosimilars, while China expanded its National Reimbursement Drug List to include both ranibizumab and aflibercept biosimilars by 2025, extending coverage beyond Tier-1 cities. India’s market remains nascent, with anti-VEGF penetration below 30% of eligible eyes, yet domestic biosimilar launches in 2026–2027 are expected to lower prices and widen adoption, further scaling the choroidal neovascularization treatment market.

The Middle East, Africa, and South America collectively contribute lesser share of global value, facing limited specialist density and reimbursement gaps. Nevertheless, private hospital chains in the Gulf states and Brazil import originator products for affluent self-pay patients, and tele-ophthalmology pilots backed by multilateral agencies may improve diagnostic reach over the forecast period, potentially adding incremental volume to the choroidal neovascularization treatment market.

Competitive Landscape

Regeneron/Bayer, Roche/Genentech, and Novartis together held high share of 2025 sales, underscoring a concentrated seller structure. Yet Samsung Bioepis, Coherus, Formycon/Bioeq, and Biocon captured 12–18% of new-start patients in Europe and early Asia-Pacific adopters, fragmenting share and narrowing price corridors. Originators pivot toward premium extensions—high-dose aflibercept, dual-pathway faricimab, and microfluidic Susvimo—to defend value, while biosimilars lean on cost leadership and fast formulary wins.

Technology increasingly differentiates players. Roche’s implant leverages microfluidics to release ranibizumab over six months, and Regeneron explores subcutaneous depots with longer shelf life. Coherus and Samsung Bioepis invest in auto-injector devices that could eventually enable home dosing under telehealth supervision, an innovation that might redraw service models inside the choroidal neovascularization treatment market.

White-space opportunities target anti-VEGF non-responders, APAC myopic CNV, and single-dose gene therapy. Adverum’s ADVM-022, Regenxbio’s RGX-314, and Ocular Therapeutix’s TKI implant remain in late trials and are unapproved as of 2026. Successful pivotal data could transform lifetime revenue architecture by shifting from recurring visits to one-time or semi-annual interventions, fundamentally altering dynamics in the choroidal neovascularization treatment market.

Choroidal Neovascularization Treatment Industry Leaders

Regeneron Pharmaceuticals

F. Hoffmann‑La Roche

Novartis

Samsung Bioepis

Coherus BioSciences

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Chugai won Japanese approval for Vabysmo in angioid-streaks CNV, marking the first therapy cleared for this niche.

- February 2025: Astellas removed dosing-duration limits on IZERVAY for geographic atrophy after FDA label expansion, granting clinicians flexibility in chronic management.

- February 2025: Regeneron reported Phase 3 success for EYLEA HD in myopic CNV, with 40% of eyes reaching 16-week intervals; an sBLA filing is planned for Q2 2026.

- November 2024: Samsung Bioepis and Biogen partnered to commercialize SB15 aflibercept biosimilar across the EU and Japan starting 2026.

Global Choroidal Neovascularization Treatment Market Report Scope

Choroidal Neovascularization (CNV) treatment refers to medical procedures aimed at stopping the growth and leakage of abnormal blood vessels beneath the retina, commonly caused by age-related macular degeneration (AMD), with intravitreal anti-VEGF injections as the primary approach.

The Choroidal Neovascularization Treatment Market Report is segmented by Therapeutic Modality, Delivery Modality, Indication, and Geography. By Therapeutic Modality, the market is segmented into Anti-VEGF Originators, Anti-VEGF Biosimilars, Photodynamic Therapy, Sustained-Delivery Implants, and Others. By Delivery Modality, the market is segmented into Intravitreal Injection, Sustained-Release Implant, and Intravenous Infusion for Photodynamic Therapy (PDT). By Indication, the market is segmented into Neovascular Age-Related Macular Degeneration (AMD), Pathologic Myopia, Diabetic Macular Edema–Associated CNV, Retinal Vein Occlusion–Associated CNV, Ocular Histoplasmosis Syndrome, Angioid Streaks, Inflammatory CNV, and Other Secondary Choroidal Neovascular Disorders. By Geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East & Africa (MEA), and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. Market Forecasts are Provided in Terms of Value (USD).

| Anti‑VEGF originators |

| Anti‑VEGF biosimilars |

| Photodynamic therapy |

| Sustained‑delivery implants |

| Others |

| Intravitreal injection |

| Sustained‑release implant |

| Intravenous infusion for PDT |

| Neovascular (wet) AMD |

| Myopic CNV |

| Secondary CNV |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Therapeutic Modality | Anti‑VEGF originators | |

| Anti‑VEGF biosimilars | ||

| Photodynamic therapy | ||

| Sustained‑delivery implants | ||

| Others | ||

| By Delivery Modality | Intravitreal injection | |

| Sustained‑release implant | ||

| Intravenous infusion for PDT | ||

| By Indication | Neovascular (wet) AMD | |

| Myopic CNV | ||

| Secondary CNV | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the choroidal neovascularization treatment market?

The choroidal neovascularization treatment market is valued at USD 7.94 billion in 2026.

How fast will the market grow over the forecast period?

It is expected to advance at a 6.85% CAGR to reach USD 11.05 billion by 2031.

Which therapeutic modality is expanding the quickest?

Sustained-delivery implants are forecast to post the fastest growth at a 10.22% CAGR through 2031.

Why are biosimilars significant for future market dynamics?

Biosimilars lower treatment costs, expand access in cost-sensitive regions, and already command about 20% of new-start share in Europe.

Which region will register the highest growth rate?

Asia-Pacific is set for the fastest regional expansion at an 8.14% CAGR, fueled by aging populations and high-myopia prevalence.

Page last updated on: