Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

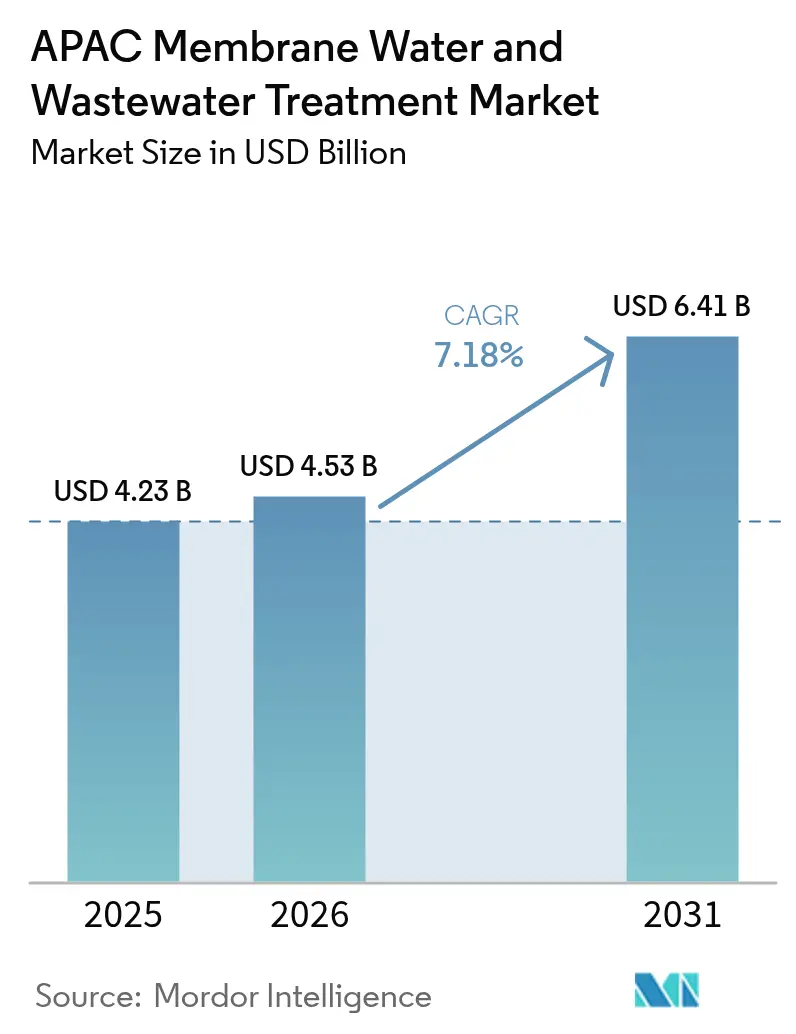

| Base Year Market Size (2025) | USD 4.23 Billion |

| Market Size (2026) | USD 4.53 Billion |

| Market Size (2031) | USD 6.41 Billion |

| Growth Rate (2026 - 2031) | 7.18% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

APAC Membrane Water And Wastewater Treatment Market Analysis by Mordor Intelligence

The APAC Membrane Water And Wastewater Treatment Market size in 2026 is estimated at USD 4.53 billion, growing from 2025 value of USD 4.23 billion with 2031 projections showing USD 6.41 billion, growing at 7.18% CAGR over 2026-2031. Demand is expanding as industrial hubs in China, India, and ASEAN nations confront tighter reuse mandates, rising raw-water tariffs, and constrained freshwater allocations. Reverse osmosis remains indispensable for seawater desalination and zero-liquid-discharge (ZLD) processes; however, nanofiltration and membrane bioreactors are gaining favor where energy efficiency, footprint, and selective ion removal are key considerations. Public-sector subsidies and multilateral loans are shrinking payback periods, while predictive-maintenance software reduces chemical cleaning frequency and extends membrane life. At the same time, polymer price spikes and persistent fouling challenges are prompting end users to adopt ceramic and smart membranes that can tolerate aggressive cleaning and achieve higher flux rates.

Key Report Takeaways

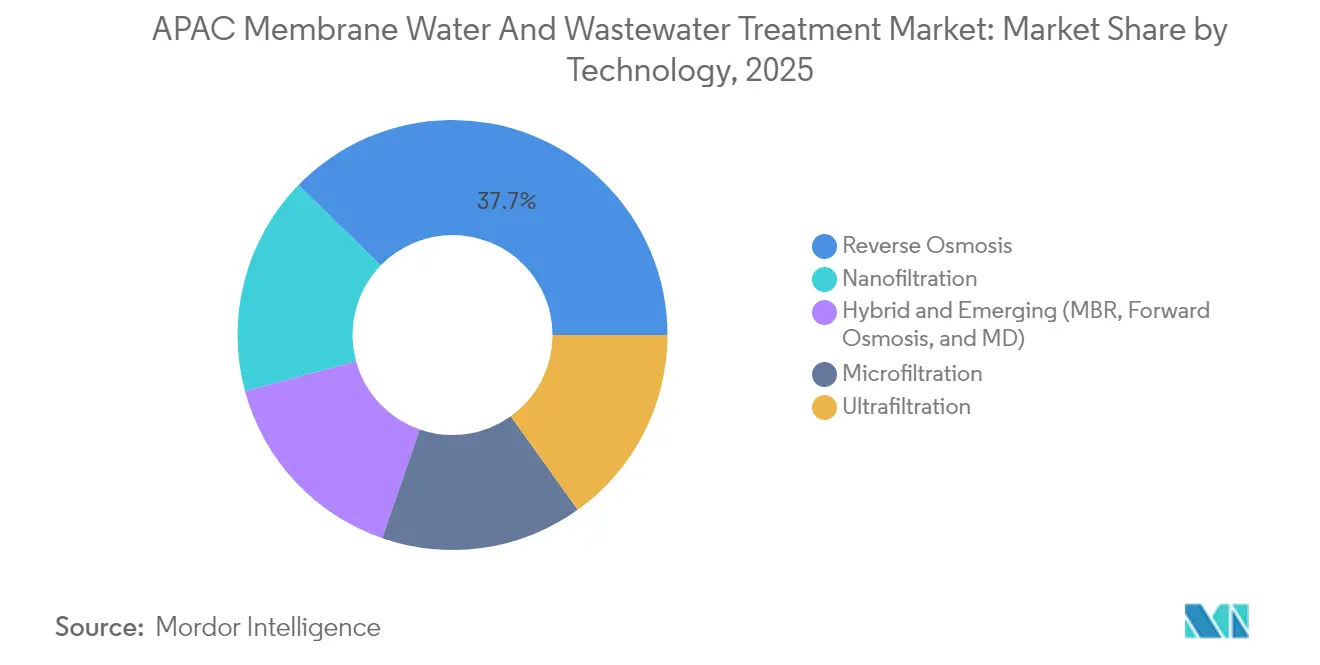

- By technology, reverse osmosis led the membrane water wastewater treatment market with a 37.72% market share in 2025. Nanofiltration is forecast to register an 8.05% CAGR through 2031, the fastest among major technologies.

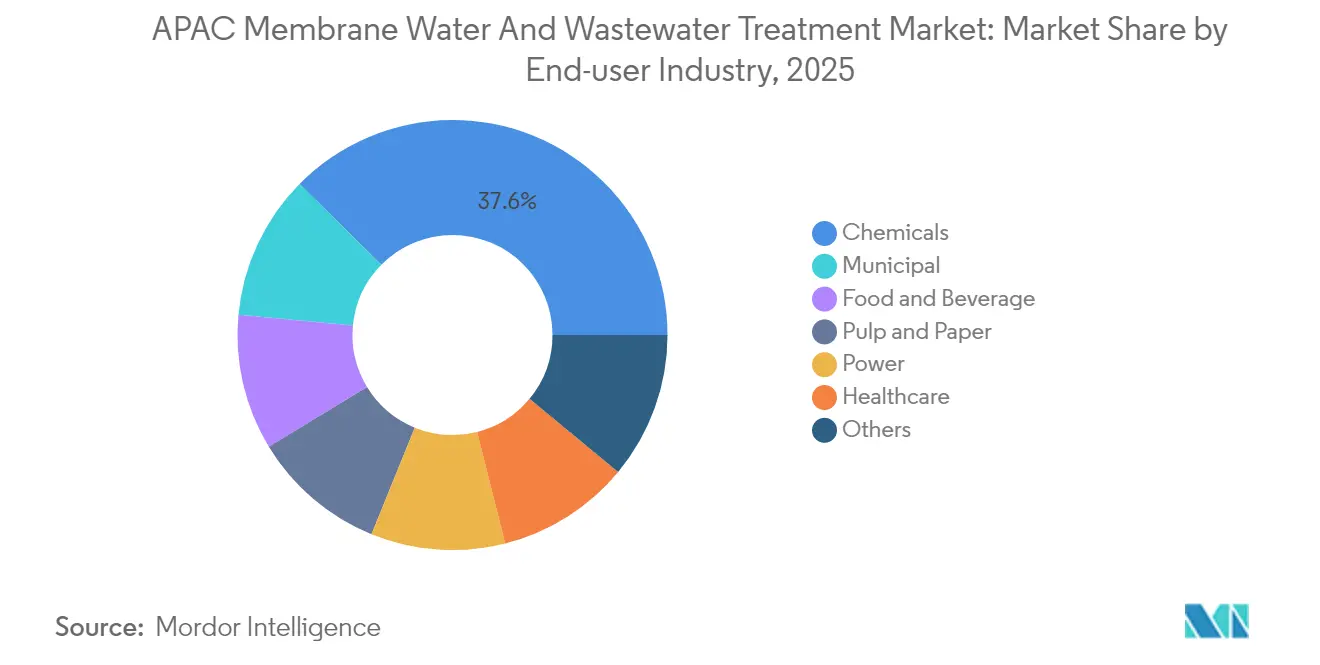

- By end-user industry, chemicals captured 37.60% of the membrane water wastewater treatment market size in 2025. Municipal wastewater treatment is expected to expand at an 8.12% CAGR between 2026-2031, the highest among end users.

- By geography, China held 42.70% revenue share in 2025; India is on track for a 8.92% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of APAC Membrane Water And Wastewater Treatment Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid urban-industrial growth boosting wastewater volumes | +1.8% | China, India, ASEAN core (Vietnam, Indonesia, Thailand) | Medium term (2-4 years) |

| Stringent effluent-discharge regulations | +2.1% | Global, with enforcement concentration in China, South Korea, Singapore | Short term (≤ 2 years) |

| Government funding for zero-liquid-discharge | +1.5% | India, China coastal provinces, South Korea industrial zones | Medium term (2-4 years) |

| Rising adoption of membrane bio-reactors | +0.9% | ASEAN, Japan, South Korea | Long term (≥ 4 years) |

| Surging demand for ceramic and smart membranes with AI-enabled O&M | +0.7% | South Korea, Japan, Singapore, spillover to China tier-1 cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Urban-Industrial Growth Boosting Wastewater Volumes

Industrial wastewater generation in the Asia-Pacific is expected to exceed 45 billion m³ annually by 2028, with chemicals, textiles, and pulp and paper industries creating nearly two-thirds of the biochemical oxygen demand loads[1]Ministry of Ecology and Environment, “China Environmental Statistics Bulletin 2024,” mee.gov.cn. India’s USD 50 billion Jal Jeevan Mission has increased household consumption, but it has also simultaneously strained peri-urban sewage networks that already trail demand by 35-40%. Vietnam’s 480,000 m³/d Ho Chi Minh City plant, commissioned in 2025, demonstrates how megacities are leapfrogging to membrane bioreactors to satisfy strict river-discharge norms. Enforcement actions across 18 Chinese provinces that exceeded 2024 discharge quotas illustrate how latent demand quickly converts to signed contracts for ultrafiltration and nanofiltration equipment.

Stringent Effluent-Discharge Regulations

China’s revised GB/T 19923-2024 compels 50% industrial wastewater reuse in water-stressed provinces by 2030-31, making membrane polishing mandatory for facilities discharging more than 500 m³/d. India’s Liquid Waste Management Rules 2024 mirror the 50% reuse target and escalate penalties up to plant shutdown for repeat offenses. South Korea’s 2024 framework steers public-private capital toward high-recovery reverse osmosis, while Singapore lowered the permissible total dissolved solids in trade effluent to 3,000 mg/L, forcing semiconductor fabs to adopt nanofiltration pretreatment. The growing adoption of ISO 20468 certification by 14 utilities between 2024 and 2025 further de-risks large procurements.

Government Funding for Zero-Liquid-Discharge

India unlocked USD 1.8 billion in concessional ZLD loans across 17 designated industrial clusters during 2024. Jiangsu and Guangdong provinces in China offered capital subsidies of 30-40%, approving 47 projects worth RMB 3.2 billion in H1 2024. K-water launched a USD 200 million co-investment fund in March 2024 for pilots with a 95%+ recovery rate. The Asian Development Bank has earmarked USD 419.6 million for membrane-based reuse in Indonesia’s manufacturing corridors, thereby shortening ZLD payback periods that would otherwise run 7-10 years.

Rising Adoption of Membrane Bio-Reactors

Singapore operates four large-scale MBR plants with a combined capacity exceeding 300,000 m³/d, producing permeate that is pure enough for NEWater reverse osmosis feed without the need for secondary clarifiers. Japan raised the share of new municipal builds using MBR from 24% in 2020 to 38% in 2024 as aging coastal facilities required compact nutrient removal upgrades. South Korea’s Yeoncho ceramic MBR delivers a flux of 2.5 m³/m²/d, halving the footprint compared to polymeric systems while tolerating chlorine-based cleaning. Containerized MBR units, totaling 8,000 m³/d, were installed across Phuket and Krabi to protect coral reefs, underscoring the tourism-driven environmental needs.

Restraints Impact Analysis of APAC Membrane Water And Wastewater Treatment Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex and replacement costs | -1.2% | ASEAN, India tier-2 cities, China inland provinces | Short term (≤ 2 years) |

| Membrane fouling and concentrate disposal issues | -0.9% | Global, acute in high-TDS industrial applications (chemicals, textiles, power) | Medium term (2-4 years) |

| Volatile polymer prices disrupting local supply chains | -0.6% | China, India, ASEAN (import-dependent markets) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capex and Replacement Costs

A 10,000 m³/d industrial RO reuse plant still requires an upfront investment of USD 8-12 million, and membrane swaps every 3-5 years add another USD 1.5-2 million[2]World Bank, “Costing Membrane Reuse Systems in Emerging Markets,” worldbank.org . India’s tier-2 municipalities face a USD 6.2 billion wastewater funding gap to 2030, and only 18% of eligible ZLD projects tapped National Clean Energy Fund loans in 2024 because collateral rules shut out small firms. Inland Chinese provinces record 25-30% lower adoption rates than their coastal peers, even under identical standards, highlighting fiscal limitations. Build-operate-transfer models shift the burden to end users through tariff hikes, sparking public pushback in secondary ASEAN cities.

Membrane Fouling and Concentrate Disposal Issues

Fouling shortens the life of polymeric membranes by 20-30% in petrochemical service, while concentrate disposal can exceed USD 50/m³ when deep-well injection is banned. One-third of India’s ZLD systems, commissioned 2020-2023, operated below 70% capacity in 2024 because brine crystallizers and evaporators scaled faster than expected. SK EcoPlant’s CSRO raises recovery to 97% but needs feed TSS below 500 mg/L, adding USD 2-3 million of pretreatment hardware. Ceramic membranes solve many fouling challenges, but they cost three to four times more than polymeric modules, limiting their uptake to hazardous-waste or high-TDS effluent where chemical savings justify the premium.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

APAC Membrane Water And Wastewater Treatment Market Segment Analysis

By Technology:

High-Recovery Systems Reshape EconomicsReverse osmosis held 37.72% of APAC Membrane Water And Wastewater Treatment Market share in 2025, underpinned by desalination mega-projects and ZLD mandates. The Daesan plant, which has been online since H1 2025, processes 100,000 t/d using Toray high-rejection elements that achieve over 98% salt removal. Nanofiltration is projected to grow at an 8.05% CAGR, with LG Chem trials demonstrating 95% divalent-ion rejection at 30% lower pressure compared to RO, a key metric for dairy and beverage plants. Nearly 68% of new RO builds specify ultrafiltration pretreatment to control fouling, and ceramic microfiltration variants are entering Japanese municipal plants where chlorine tolerance is valued. Hybrid MBR-RO lines already account for 42% of China’s 2025 industrial tenders, reflecting land scarcity and ever-tighter discharge rules.

The forward-looking pipeline emphasizes energy-saving configurations, such as closed-circuit RO and two-stage NF-RO hybrids. In contrast, forward osmosis and membrane distillation remain limited to fewer than 10 commercial sites due to draw-solution and thermal-energy hurdles. Ceramic MBRs, such as K-water’s Yeoncho project, demonstrate that higher capital expenditure can pay off if flux doubles and the lifespan extends beyond 10 years. As subsidies offset initial costs, multibarrier trains that integrate UF-RO or MBR-RO will likely dominate new installations through 2031.

By End-User Industry:

Compliance Drives Chemicals, Scarcity Propels MunicipalChemical producers accounted for 37.60% of 2025 revenue in APAC Membrane Water And Wastewater Treatment Market, as discharge permits in petrochemical parks are often capped or unavailable, necessitating the adoption of multi-stage membrane ZLD. Veolia’s USD 500 million Jubail contract underscores this compliance-driven demand. Municipal utilities, however, are poised for the fastest growth, at an 8.12% CAGR, as tier-2 Indian and ASEAN cities with per-capita capacity below 50 L/day upscale to MBRs and NF-RO polishing. The pulp-and-paper, food and beverage, and power sectors contribute steady incremental volumes, each turning to membranes for chemical recovery, process water polishing, or boiler feed conditioning.

Diversifying influences include healthcare facilities in Japan and South Korea addressing antibiotic residues, and shared effluent parks in China, where tenants amortize capital across a common treatment line, reducing unit costs by 20-25%. The membrane water wastewater treatment market size for municipal reuse is projected to widen as public health standards tighten and climate stress heightens the value of reclaimed water. Meanwhile, the “Others” basket—encompassing textiles, electronics, and mining—adds resiliency, with Indian dyeing clusters retrofitting NF-RO steps to meet stringent color limits.

Geography Analysis

China Membrane Water And Wastewater Treatment Market

China accounted for 42.70% of the 2025 expenditure in APAC Membrane Water And Wastewater Treatment Market, driven by 1,200 compulsory retrofits scheduled to be completed before December 2026 under the GB/T 19923-2024 reuse mandate. Veolia’s EUR 10 million ion-exchange resin expansion and SUEZ’s trio of 2024 contracts demonstrate the commitment of foreign OEMs, yet local brands like Origin Water use cost leadership to undercut imports by up to 20%. The membrane water wastewater treatment market size is now large enough for both premium and value tiers to coexist.

APAC Membrane Water And Wastewater Treatment Market

India’s 8.92% CAGR reflects USD 50 billion Jal Jeevan Mission spending and new ZLD zones across 17 industrial clusters. Financing gaps persist for secondary cities, but concessional funds and blended-finance models are advancing. Japan and South Korea showcase high-specification deployments; 38% of Japanese municipal builds in 2025 integrated MBR, while Korean conglomerates push high-recovery RO and ceramic options.

ASEAN and Oceania Membrane Water And Wastewater Treatment Market

ASEAN nations have pooled USD 1.2 billion in multilateral loans; Indonesia’s 260,000 m³/d Buaran III and Vietnam’s 480,000 m³/d Ho Chi Minh City plants illustrate a shift towards membrane technology to curb non-revenue water and protect waterways. Australia and other Pacific players contribute a smaller but steady desalination and potable-reuse niche, funded via the AUD 3.5 billion National Water Grid.

Regulatory Landscape

Across APAC, wastewater rules are tightening around reuse thresholds, sector-specific discharge limits, and centralized industrial-park compliance, which is accelerating adoption of UF/NF/RO polishing and MBRs. China is a key anchor market, with GB/T 19923-2024 driving industrial reuse mandates and complemented by the Ministry of Ecology and Environment (MEE) strengthening oversight through the Measures for the Supervision and Management of River Discharge Outlets (Order No. 35, implemented in 2025) and technical guidance for industrial-park discharge standard setting (HJ 945.4-2026, effective September 1, 2026). MEE also approved a revised national standard for water pollutants in the textile industry (revision of GB 4287-2012), effective September 1, 2026, raising compliance stakes for high-load sectors that frequently require membrane-based tertiary treatment.

Southeast Asia is also formalizing stricter baselines. Indonesia enacted Permen LH 11/2025, updating domestic wastewater quality and technology standards with a two-year transition window for existing businesses (compliance deadline September 9, 2027), while Vietnam implemented Circular 06/2025/TT-BTNMT (QCVN 40:2025/BTNMT for industrial effluent) and Circular 05/2025/TT-BTNMT (QCVN 14:2025/BTNMT for domestic and municipal wastewater). Policy and funding signals are reinforcing the shift to reclamation and advanced treatment: Singapore PUB awarded close to SGD 100 million under RIE2030 for water technologies R&D in June 2026, and Malaysia announced drafting of a National Water Reclamation Policy in June 2026 to support industrial demand such as data centers and manufacturing.

Value Chain Analysis

The APAC membrane water and wastewater treatment value chain covers polymer and inorganic raw materials, membrane sheet and module manufacturing (including RO, NF, UF, MF, and ceramic formats), skid and system integration (MBR-RO, UF-RO, ZLD trains), EPC delivery, and long-term O&M with consumables (chemicals, cartridges, and membrane replacement). Large OEMs and material science players, such as Toray in Japan and LG Chem in South Korea, alongside multiple Chinese suppliers, support regional scale, but differentiation is increasingly tied to system integrators and operators that can deliver performance guarantees on recovery, energy, and discharge compliance for industrial parks, municipal utilities, and desalination assets.

Downstream pull is being reinforced by policy-led reuse programs and standards that shape technology choice and procurement timing. In India, state-level treated-water reuse policies notified in 2026 (including Uttar Pradesh, Odisha, and Andhra Pradesh covering 123 urban local bodies) expand municipal and industrial offtake pathways for reclaimed water, supporting demand for MBRs and polishing membranes alongside distribution and storage infrastructure. In Indonesia, Permen LH 11/2025 includes technology-linked requirements for smaller domestic wastewater producers, and the 2025-2027 transition window is prompting earlier engagement with consultants, local fabricators, and service partners to secure compliant packaged systems and spares. Across the chain, volatility in polymer inputs and fouling-driven replacement cycles keeps lifecycle services, local warehousing, and technical support central to vendor selection.

Competitive Landscape

The APAC Membrane Water And Wastewater Treatment Market is moderately concentrated. Toray, Nitto Denko, and Asahi Kasei defend their shares through their expertise in polymer chemistry and service contracts, but face price pressure from Korean and Chinese rivals. LG Chem’s KRW 124.6 billion investment in doubling its capacity to 800,000 RO units by 2025 leverages captive polymer streams to lower costs and accelerate innovation for brine-tolerant products. SK EcoPlant’s CSRO launch shows process differentiation; its 97% recovery brine loops reposition ZLD economics. Western EPC majors Veolia and SUEZ thrive where turnkey delivery, O&M, and project financing outweigh the cost of membrane units.

APAC Membrane Water And Wastewater Treatment Industry Leaders

Veolia

Kurita Water Industries Ltd.

TORAY INDUSTRIES, INC.

Asahi Kasei Corporation

Koch Technology Solutions

- *Disclaimer: Major Players sorted in no particular order

APAC Membrane Water And Wastewater Treatment Market Companies Covered in this Report

- Alfa Laval

- Aquatech International LLC

- Asahi Kasei Corporation

- DuPont

- Evoqua Water Technologies LLC

- Hitachi Ltd

- Hydranautics - A Nitto Group Compan

- Kemira

- Koch Membrane Systems, Inc.

- Kurita Water Industries Ltd.

- Litree Purifying Technology

- Origin Water

- Pentair

- TORAY INDUSTRIES, INC.

- Veolia Water Technologies

- Xylem

Read Analysis of APAC Membrane Water And Wastewater Treatment Companies

Market Opportunities and Future Outlook

Industrial circular-water programs are creating whitespace for higher-spec membrane trains that move beyond compliance toward recovery, particularly for semiconductors, chemicals, and industrial parks. In South Korea, the Ministry of Climate, Energy and Environment (MCEE) announced a phase-two R&D project in May 2026 aimed at localizing 90% of ultrapure water production equipment for semiconductors by 2030, creating qualification and procurement windows for membranes, polishing steps, and integrated UPW and reclaim systems across the regional electronics supply chain. In China, large industrial desalination and reuse builds provide reference sites for membrane-based infrastructure at industrial-park scale, including SUEZ commissioning a 300,000 m3/day industrial membrane seawater desalination plant for Wanhua Chemical’s Penglai Industrial Park (Shandong) in April 2025.

Municipal utilities are also upgrading treatment resilience, creating opportunities for durable and higher-fouling-tolerance formats and retrofit-led growth. In the Philippines, Acuriant Technologies received phase one of a 100 MLD ceramic ultrafiltration retrofit at Maynilad’s Putatan Water Treatment Plant 1 in June 2026, which points to ceramic membranes as a way to manage variable raw-water quality while targeting longer cleaning intervals and more stable flux. On the desalination side, India is adding new capacity backed by international funding, including the Chennai Metropolitan Water Supply and Sewerage Board’s 400 MLD Perur desalination project funded by JICA with commissioning targeted for end-2026. This expands the installed base for RO elements and pretreatment membranes and supports an aftermarket for replacements and O&M optimization tools.

Recent Industry Developments in APAC Membrane Water And Wastewater Treatment Market

- July 2026: Kurita Water Industries Ltd. and Membrane Group India established Kurita Membrane India Pvt. Ltd. to deliver water and wastewater treatment, ultrapure water, and resource recovery solutions for semiconductor and electronics customers in India. The initiative tightens capability alignment with high-purity and reuse requirements and expands localized delivery and service capacity for membrane-intensive projects.

- April 2026: Veolia launched Mizu Partner Joyo, a joint venture in Joyo City, Japan, to manage drinking water and wastewater services under a 10-year contract. The arrangement expands private participation into integrated operations and asset renewal planning, supporting longer-term deployment of advanced treatment upgrades and lifecycle membrane services in municipal networks.

- October 2025: Toray Industries, Inc. launched the TLF-400ULD reverse osmosis membrane, developed with Toray Membrane (Foshan) Co., Ltd. and Toray Advanced Materials Research Laboratories (China) Co., Ltd., for industrial wastewater reuse and sewage treatment. The product introduction targets lower energy and higher durability performance needs that are becoming central in reuse-driven tenders across China and other APAC industrial hubs.

APAC Membrane Water And Wastewater Treatment Market Report Scope and Research Methodology

Market Definition and Coverage

For this market, we size the value of membrane-based systems used to treat water and wastewater across Asia-Pacific, where spending is counted when membrane processes are deployed to separate, purify, or concentrate water streams.

Scope exclusions: We exclude non-membrane treatment processes and any revenues outside Asia-Pacific.

Segments Covered in This Report

- By Technology

- Microfiltration

- Ultrafiltration

- Nanofiltration

- Reverse Osmosis

- Hybrid and Emerging (MBR, Forward Osmosis, and MD)

- By End-user Industry

- Municipal

- Pulp and Paper

- Chemicals

- Food and Beverage

- Healthcare

- Power

- Others

- By Geography

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to map the demand environment and to anchor macro assumptions that later get checked in interviews. We mainly relied on public, non-paywalled sources such as national water and environment ministries, water utility regulator publications, WHO and UNEP water indicators, and OECD water statistics where available for relevant economies.

To keep the model practical, we also reviewed sources such as customs and trade statistics for membrane-related equipment flows, patent databases to track technology intensity, and peer-reviewed journals that discuss membrane performance and adoption in municipal and industrial settings. In parallel, we reviewed company annual reports, investor presentations, association websites, and reputable press to understand capacity additions and bidding activity. A paid subscription for company financials and news helped cross-check supplier exposure and timing. These desk sources are illustrative only, and many other references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what is actually being bought and deployed, and how pricing and replacement cycles move in the field. We spoke with stakeholders across municipal utilities, industrial users, EPC and O&M participants, and membrane ecosystem specialists across key APAC hubs, so assumptions from desk research could be corrected where needed.

To reduce bias, responses were balanced across company sizes and job roles, and follow-up questions were used when there were gaps on adoption pace, average selling price movements, and project timing signals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 17% | |

| Mid tier: 55% | Functional/Unit leaders: 40% | |

| Smaller Players: 18% | Managers: 43% |

Market-Sizing & Forecasting

Market sizing starts with a top-down demand pool reconstruction that ties APAC water and wastewater treatment needs to membrane process adoption, and then translates that into value using observed price bands. Once this structure is built, we corroborate it with selective bottom-up checks, such as sampled supplier revenue exposure to APAC, channel discussions on module and system pricing, and a few volume-times-ASP sanity checks to keep totals realistic.

Key inputs in the model include wastewater discharge and reuse targets, desalination and advanced treatment additions, municipal capex cycles, industrial water intensity in sectors that frequently use membranes, and the mix shift across microfiltration, ultrafiltration, nanofiltration, reverse osmosis, and hybrid configurations like MBR. Because pricing can swing with resin and energy costs and with specification changes, ASP progressions were applied with step changes when project mix or procurement behavior was expected to change.

Forecasting is driven through scenario analysis, where base, conservative, and accelerated cases are built around policy enforcement strength, project execution pace, and cost curves discussed in interviews. When country-level gaps exist, proxies such as population served, industrial output indicators, and observed installation activity are used first, then adjusted once primary feedback confirms the direction and magnitude.

Data Validation & Update Cycle

Outputs are checked against independent signals like reported tender flows, announced capacity additions, and import patterns, and then variances are investigated before sign-off. When a data point creates an unusual jump, we recheck the assumption chain, confirm currency conversions and timing, and, if needed, re-contact a subset of respondents to confirm whether the move is real or an artifact.

A multi-step internal review is followed so the final numbers are consistent across the narrative and the model. Reports are refreshed annually, with interim updates made when material events occur that can shift demand, pricing, or the technology mix. Before delivery, an analyst runs a final pass to align the model to the most recent information available.

Mordor Intelligence's APAC Membrane Water and Wastewater Treatment Wwt Market Sizing Compared With Other Published Estimates

Published market sizes for APAC membrane water and wastewater treatment often differ because the boundaries are not always the same, and because pricing and timing assumptions are handled differently. In practice, differences show up most in what gets counted as membrane WWT versus broader membrane filtration, what year the currency conversion is anchored to, and how fast ASPs are allowed to rise or normalize.

A major spread driver is refresh cadence and cut-off timing, since project award cycles and input costs can move within a year and change the stated market value without any real change in underlying demand. By using a consistent FX timing rule, updating ASP bridges when procurement patterns shift, and re-validating outlier jumps through callbacks, Mordor Intelligence keeps the estimate aligned to what APAC buyers are paying for membrane-based water and wastewater treatment in the base year.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.23 B (2025) | |

| Industry Research Group A | USD 10.86 B (2024) | This figure appears to use a broader counting frame and a different base year, which can pull in adjacent membrane filtration and application spend beyond core membrane WWT, and it is also sensitive to the currency timing used for conversion. |

| Global Analytics Publisher B | USD 7.07 B (2025) | This estimate is for the wider membrane filtration market across applications, and it is segmented by material focus rather than being limited to water and wastewater treatment deployment, which typically lifts totals versus a WWT-only scope. |

The benchmark spread is mainly explained by scope boundaries first, and then by timing choices that affect FX and ASP steps. When the scope is held to membrane-based water and wastewater treatment in APAC and assumptions are rechecked against project and pricing signals, the resulting market size stays easier to trace and repeat year over year.

Key Questions Answered in the Report

What is the 2026 value of the APAC Membrane Water And Wastewater Treatment Market?

The market stands at USD 4.53 billion in 2026.

How fast is demand expected to grow through 2031?

Revenue is forecast to rise at a 7.18% CAGR to reach USD 6.41 billion by 2031 (2026-2031).

Which technology currently dominates regional installations?

Reverse osmosis commands 37.72% market share, driven by desalination and ZLD applications.

Why is India the fastest-growing geography?

New reuse mandates, USD 50 billion Jal Jeevan Mission funding, and concessional ZLD loans underpin a 8.92% CAGR forecast for India.

What are the biggest operational challenges today?

High capex for smaller utilities, membrane fouling in high-TDS effluent, and volatile polymer prices that squeeze module assembler margins.

Page last updated on: