China Turning Machine and Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

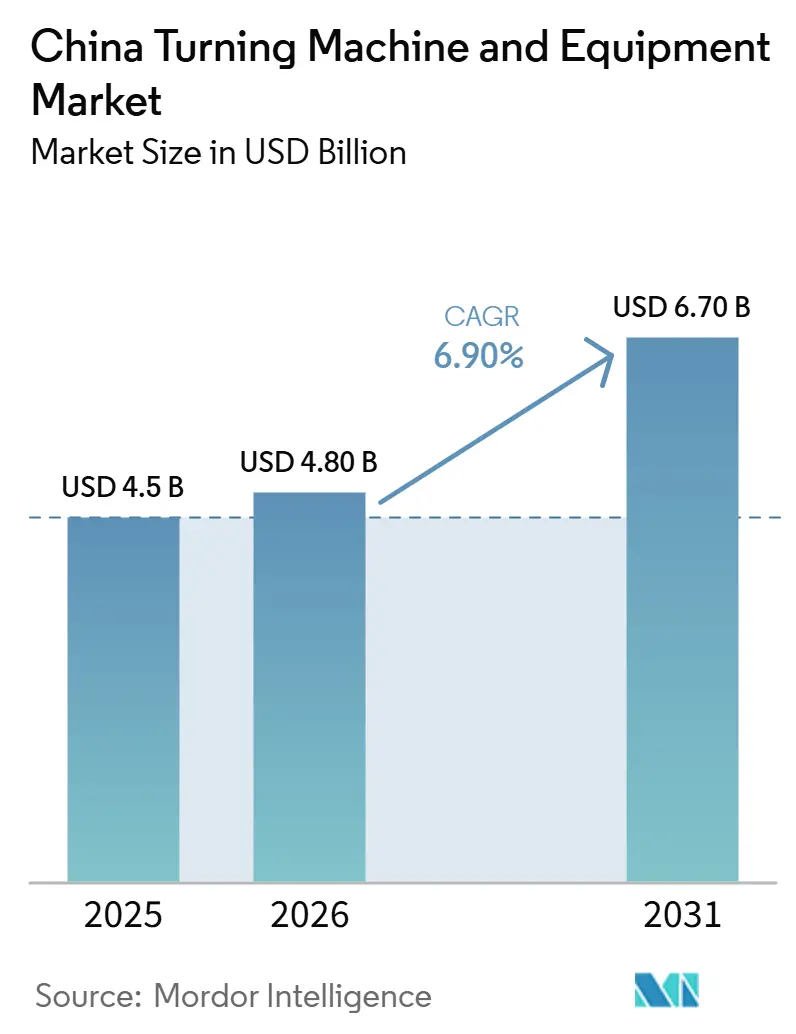

| Base Year Market Size (2025) | USD 4.5 Billion |

| Market Size (2026) | USD 4.80 Billion |

| Market Size (2031) | USD 6.70 Billion |

| Growth Rate (2026 - 2031) | 6.90% CAGR |

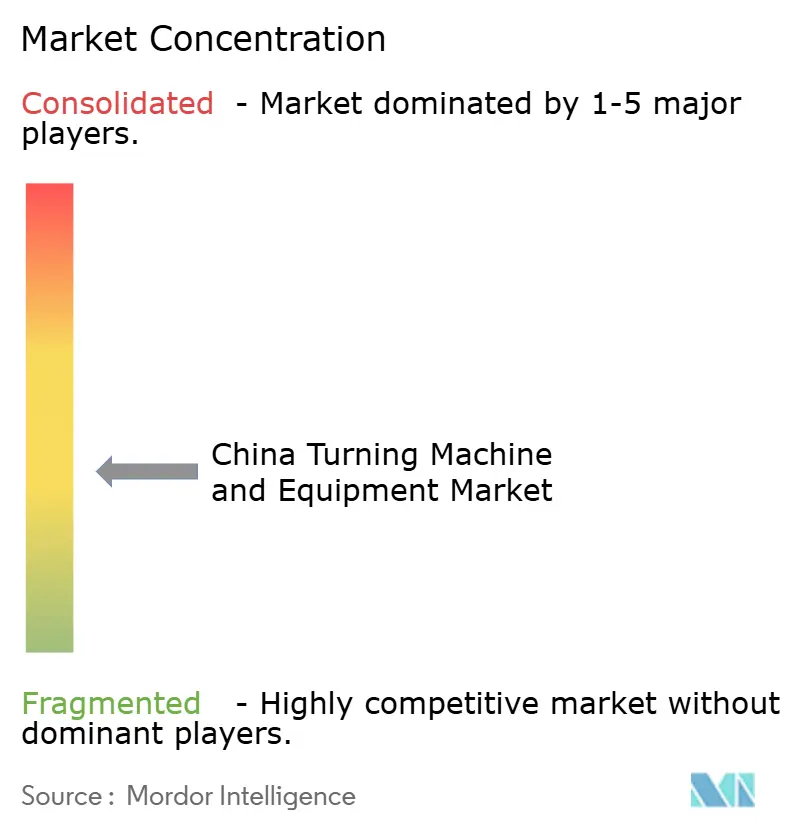

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Turning Machine and Equipment Market Analysis by Mordor Intelligence

The China Turning Machine and Equipment Market size is expected to grow from USD 4.5 billion in 2025 to USD 4.80 billion in 2026 and is forecast to reach USD 6.70 billion by 2031 at 6.90% CAGR over 2026-2031.

Demand is being supported by factory modernization, stronger electric vehicle output, and broader adoption of CNC-based precision machining across core manufacturing chains. China’s metal processing machine tool production value rose 6.9% year over year to CNY 219.8 billion (USD 31.4 billion) in 2025, while metal cutting machine output reached 868,000 units. Policy support under the 15th Five-Year Plan also keeps replacement and localization demand active because industrial machine tools are now treated as a strategic core technology priority. Labor shortages and margin pressure still constrain growth, and average profit margins for metal-cutting machine manufacturers were 7.3% in 2025, limiting reinvestment capacity for many domestic producers in the China turning machine and equipment market.

Key Report Takeaways

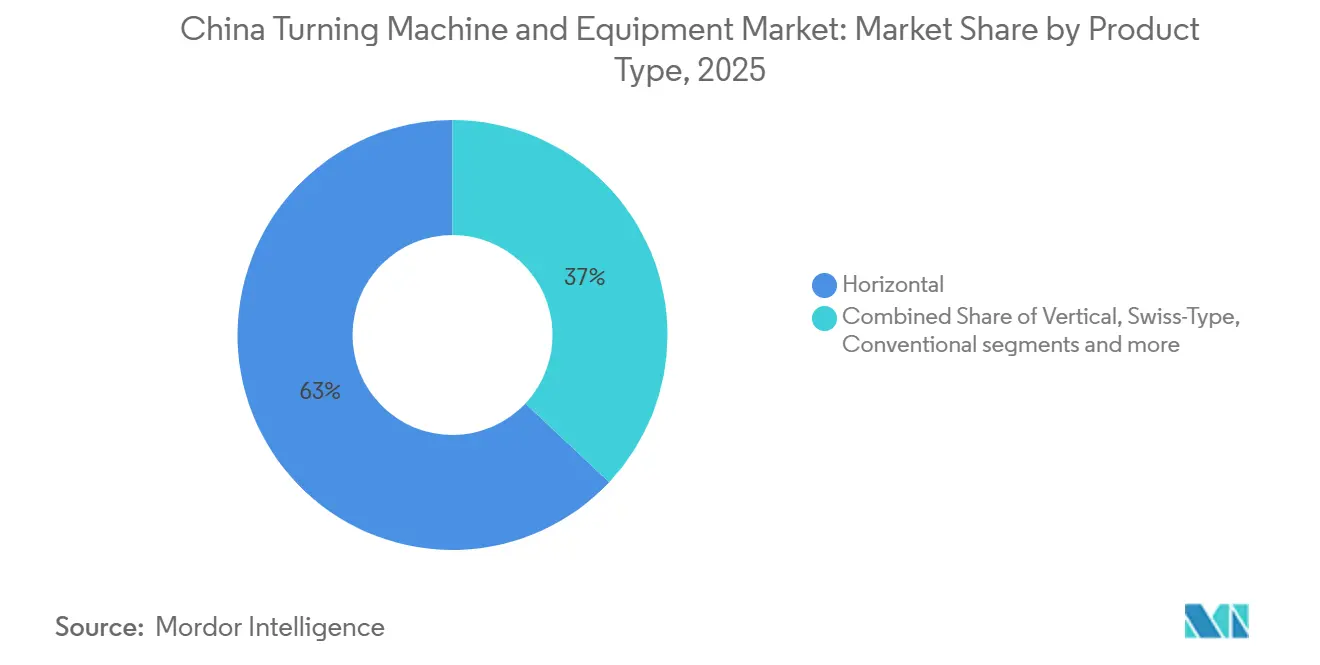

- By product type, the horizontal segment accounted for 63% of the China turning machine and equipment market size in 2025, while the multi-tasking segment is forecast to grow at an 8.4% CAGR through 2031.

- By automation type, fully automatic CNC held 78% of the China turning machine and equipment market share in 2025 and is projected to expand at an 8.1% CAGR through 2031.

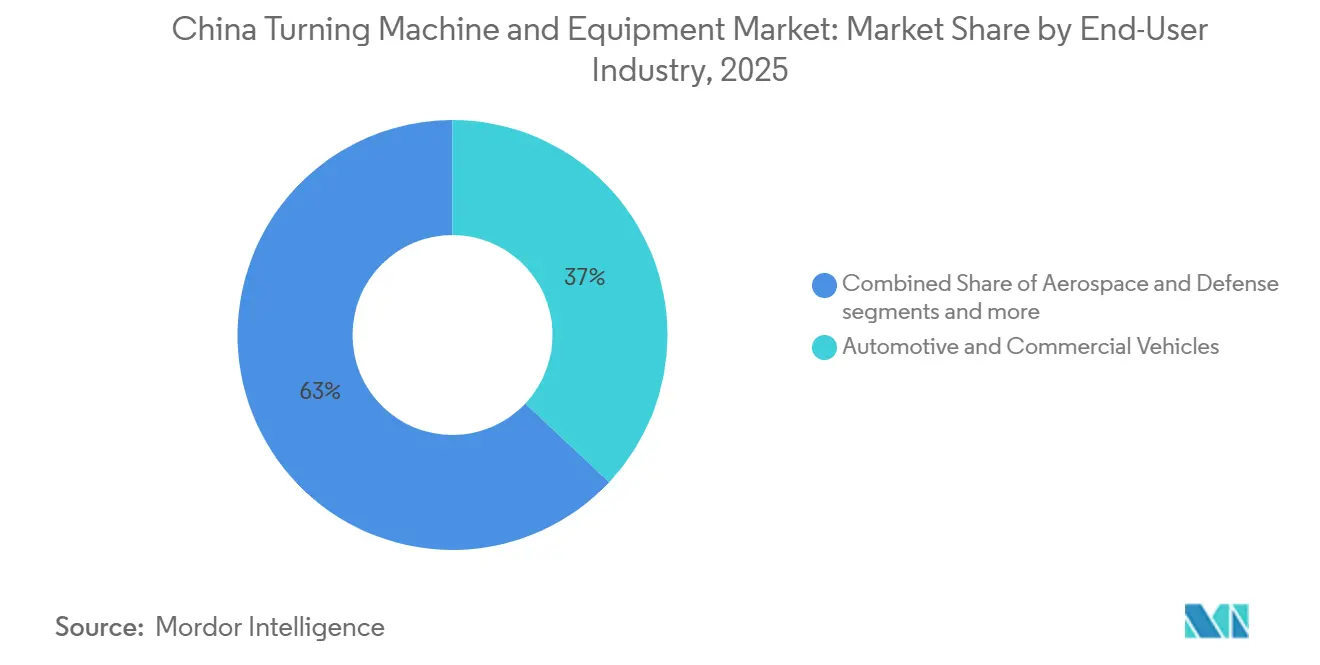

- By end-user industry, automotive and commercial vehicles accounted for 37% of the China turning machine and equipment market size in 2025, while the aerospace and defense segment is advancing at an 8.6% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China Turning Machine and Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in Electric Vehicle Production Fueling Demand for Advanced Turning Equipment | +2.0% | National, concentrated in the Yangtze River Delta and Pearl River Delta EV clusters. | Short term (≤ 2 years) |

| Made in China 2025 / MIC2025 policy and successor programs | +1.8% | National, with emphasis on coastal advanced manufacturing zones and Northeast industrial bases | Medium term (2-4 years) |

| Growth of Industrial Automation and Smart Factories | +1.2% | National, with Eastern China leading and inland provinces following | Medium term (2-4 years) |

| Expansion of High-Precision Aerospace Manufacturing | +0.9% | Northeast China, Southwest China, and the Yangtze River Delta | Long term (≥ 4 years) |

| Increasing Localization of Precision Component Production | +0.7% | National | Medium term (2-4 years) |

| Growth in High-Mix, Low-Volume Manufacturing | +0.5% | Yangtze River Delta, Pearl River Delta, and the Chengdu-Chongqing corridor | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growth in Electric Vehicle Production Fueling Demand for Advanced Turning Equipment

China’s shift toward electric mobility is creating a different demand pattern for the China turning machine and equipment market than in earlier automotive cycles. MIIT reported new energy vehicle production of 1.554 million units in May 2026, up 22.4% year over year, while cumulative output for January through May reached 5.841 million units.[1]Ministry of Industry and Information Technology, “May 2026 Automotive Industry Economic Performance Report,” MIIT, miit.gov.cn Electric vehicle powertrains are shifting machining demand toward high-precision components, including motor shafts, reduction gear components, battery thermal management parts, and lightweight structural components. These changes in equipment demand at the process level are driven by suppliers' need for repeatable CNC turning capability across a broader set of critical parts. It also means that many EV production programs require additional investment in precision machining for the electric drivetrain and associated components. The result is a steadier, more structural base order for the China turning machine and equipment market across automotive supply chains.

Made in China 2025 / MIC2025 Policy and Successor Programs

The earlier MIC2025 framework has now moved into more binding industrial policy channels that matter directly for the China turning machine and equipment market. China’s 15th Five-Year Plan for 2026 to 2030 identifies industrial machine tools, described as industrial mother machines, as a strategic core technology area for national capability building.[2]State Council of the People’s Republic of China, “China Approves 2026-2030 Blueprint 15th Five-Year Plan,” State Council News, english That policy direction matters because it links machine tools to broader goals of equipment independence, advanced manufacturing resilience, and deep local supply chains. It also gives domestic buyers stronger reasons to replace older equipment with higher-precision CNC systems that fit newer policy and technical standards. The same push supports domestic component sourcing and reduces the long-term case for relying on imported subsystems in standard applications. In the China turning machine and equipment market, this creates a more predictable demand floor than a typical capital-spending cycle would.

Growth of Industrial Automation and Smart Factories

Factory digitalization is becoming a practical purchasing driver for the China turning machine and equipment market rather than a long-range concept. MIIT’s action plan for industrial internet platforms set a target of penetration above 55% by 2028 and called for upgrades to industrial networks across at least 50,000 enterprises. China’s industrial digitalization policies are encouraging broader adoption of smart manufacturing facilities.[3]Ministry of Industry and Information Technology and Seven Other Agencies, “Implementation Plan for the Digital Transformation of the Machinery Industry 2025-2030,” Digital China Summit Secretariat, szzg.gov.cn These programs matter because turning centers are often among the first assets upgraded when factories need traceability, networked controls, and consistent process quality. Buyers are also moving toward equipment that reduces manual intervention and integrates into connected production cells. This keeps the China turning machine and equipment market aligned with broader automation spending, even when some sectors slow their greenfield expansion.

Expansion of High-Precision Aerospace Manufacturing

Aerospace is emerging as a higher-value demand pool for the China turning machine and equipment market because its parts require tighter tolerances, better traceability, and more stable machining performance. China’s 15th Five-Year Plan named aerospace among the emerging pillar industries expected to drive future industrial growth. These regulations are expected to support greater standardization in aerospace manufacturing, potentially increasing demand for certified precision machining processes. These changes raise the need for multi-axis turning, turn-mill centers, and larger vertical turning systems in aviation and defense supply chains. The demand is especially relevant in Shenyang, Sichuan, and the Chengdu-Chongqing corridor, where aircraft and defense manufacturing are already concentrated. Over time, aerospace requirements are likely to influence technical specifications across a wider share of the China turning machine and equipment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Cost of Advanced Turning Equipment | -1.8% | National, with stronger pressure on inland provinces and SME clusters | Short term (≤ 2 years) |

| Skilled CNC Programmer and Machinist Shortages | -1.3% | National, most acute in advanced manufacturing hubs | Medium term (2-4 years) |

| Intense Price Competition Among Domestic Machine Tool Manufacturers | -1.0% | National, concentrated in coastal supplier networks | Medium term (2-4 years) |

| Cyclical Industrial Investment Patterns | -0.8% | National, with SME-heavy provincial markets more exposed | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Advanced Turning Equipment

The cost gap between standard and advanced systems still limits how fast China's turning machine and equipment market can move up the value curve. Entry-level CNC lathes can be sourced at much lower prices, but 5-axis turn-mill compound centers used in aerospace and EV programs often range from USD 80,000 to more than USD 200,000 per unit, and a full production cell can exceed USD 500,000. That spending level is difficult for many Tier-2 and Tier-3 suppliers to absorb, given that average industry profit margins were only 7.3% in 2025. The burden is heavier in inland provinces where service depth, spare part availability, and application support are thinner than in the coastal belt. Subsidies and lending support help larger enterprises, but smaller buyers still have to weigh equipment purchases against working capital needs and customer price pressure. This keeps part of the China turning machine and equipment market on a slower upgrade path even when demand conditions are favorable.

Skilled CNC Programmer and Machinist Shortages

Labor capability remains one of the clearest operating constraints on the China turning machine and equipment market. The issue is no longer limited to basic machine operation, as modern turning centers increasingly require familiarity with CAD/CAM, process monitoring skills, and confidence with automation-linked workflows. Industry reports indicate that shortages of skilled CNC operators can reduce effective machine utilization and delay capacity expansion decisions. This means some buyers are delaying new equipment orders until they are sure they can effectively staff additional capacity. The problem is especially important in advanced manufacturing zones where production schedules are tight, and quality expectations are high. Training programs are expanding, but the time needed to build capable operators is long enough to slow near-term growth in the China turning machine and equipment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Horizontal Machines Anchor Volume, Multi-Tasking Gaining Strategic Priority

The horizontal segment held 63% of the China turning machine and equipment market in 2025, reflecting its role as the standard configuration across automotive, general machinery, and energy equipment, as well as in export-oriented supplier networks. The segment keeps its lead because the installed base is large, service support is widely available, and operators are already familiar with the format. That combination supports replacement demand even when buyers become more selective of new projects. The vertical segment remains important for heavy parts such as bearing rings, wind turbine hubs, and large marine or compressor housings, where workpiece size and chip handling are critical. Swiss-type segment serves a smaller installed base, but it stays critical in medical device and semiconductor equipment clusters where very tight tolerances and stable repeatability are required.

The multi-tasking segment is the fastest-growing product category, with the China turning machine and equipment market for this segment expected to grow at an 8.4% CAGR from 2026 to 2031. Buyers are shifting toward these systems because a single setup can combine turning and milling steps, reduce handling, and cut the risk of dimensional error on complex parts. This is especially useful for EV motor housings, aerospace structures, and other components that need higher precision and shorter cycle times. Conventional segment still serves smaller inland workshops and lower-spec applications. Still, it is losing ground as buyers face tighter quality requirements and greater pressure to replace from modernization programs. Within the China turning machine and equipment industry, the product mix is moving away from simple like-for-like replacements toward equipment that supports more complex machining in fewer steps.

By Automation Type: Fully Automatic CNC Dominant as Smart Upgrades Intensify

Fully automatic CNC captured 78% of the China turning machine and equipment market share in 2025, and it is also the fastest-growing automation segment with an 8.1% CAGR expected through 2031. This position reflects the wider move toward traceability, repeatability, and more stable process control in Chinese factories. Buyers are increasingly choosing full CNC systems because they support tighter tolerances and are easier to integrate into automated cells and monitored production lines. The segment also benefits from policy support for smarter manufacturing and for deeper domestic capability in advanced equipment. Even after years of upgrades, the installed base still contains many conventional and semi-automatic machines, so the conversion runway remains meaningful.

Semi-automatic equipment plays a role in medium-volume plants where batch economics still do not justify a full automation jump. These machines often serve as a bridge for buyers in central and western China who are gradually moving into CNC-based production. Manual equipment is in a clear structural retreat because labor costs, customer quality demands, and expectations for process documentation are rising simultaneously. While replacement demand dominates in mature coastal regions, greenfield and capacity-expansion opportunities remain significant in developing inland provinces. That shift continues to favor fully automatic CNC over manual or partial-automation formats.

By End-User Industry: Automotive Leads, Aerospace Precision Requirements Redefine Equipment Standards

Automotive and commercial vehicles accounted for 37% of the China turning machine and equipment market in 2025, making it the largest end-user segment by a wide margin. The segment benefits from China’s scale in vehicle manufacturing and from the higher machining content carried by EV drivetrains and associated component systems. Suppliers serving this customer group are increasingly specifying multi-axis CNC lathes, robotic loading setups, and more stable process control for shafts, housings, and gearbox elements. The strength of automotive demand also gives the China turning machine and equipment market a broad volume base that supports both mainstream and higher-spec machine categories.

Aerospace and defense is the fastest-growing end-user segment, with an 8.6% CAGR projected from 2026 to 2031. Its growth is tied to tighter certification requirements, rising demand for high-integrity components, and broader investment in aircraft, engines, and low-altitude platforms. Medical devices and surgical instruments remain a premium segment because implants and robotic surgery components often require Swiss-type and multi-axis CNC turning with extremely tight tolerances. Electrical, electronic, and semiconductor equipment shows strong demand in provinces such as Guangdong and Jiangsu, where connector housings, motor shafts, and handler parts require high surface finishes and dimensional stability. Oil, gas, and energy, and general industrial machinery contribute significant volume, but their replacement cycles are slower, and their price sensitivity is usually higher. The other segment still captures diverse demand from consumer goods and defense-related manufacturing, though equipment specifications vary widely across buyer groups.

Geography Analysis

The eastern coastal provinces remain the core demand and production base for the China turning machine and equipment market. The eastern region accounted for 82.2% of China’s metal-cutting machine tool output in 2025, making it the clear center of both supply and consumption for turning machines and equipment. Guangdong led national production with 28.62%, followed by Zhejiang at 27.95% and Jiangsu at 11.51%, indicating the market's concentration in the coastal manufacturing belt. This concentration creates a large customer base for CNC turning machine and equipment suppliers serving automotive, electronics, and industrial machinery sectors. This concentration continues to support stronger demand for precision turning, turn-mill systems, and related automation. The Pearl River Delta also remains important because its electronics and consumer goods base supports steady demand for high-speed precision lathes, small-diameter systems, and compact CNC configurations.

Northeast China holds a smaller share of the China turning machine and equipment market, but it remains strategically important in heavy-duty and large-diameter turning applications. The Shenyang-Dalian corridor combines legacy machine tool capability with ongoing demand from aerospace and defense manufacturers. This gives the region a durable role in vertical turning, heavy cutting, and more specialized multi-tasking systems. It also stands to benefit from policy-led R&D support for industrial mother-machine technologies within the current national planning cycle.

Western and central China represent the most important incremental expansion zone for the China turning machine and equipment market, given its lower installed base. The Chengdu-Chongqing corridor is becoming more relevant because aerospace, defense, and advanced equipment projects there require higher-value 5-axis turning and turn-mill systems. NDRC has linked future industrial growth to emerging pillars, such as advanced aerospace and intelligent equipment, that support longer-term investment in inland manufacturing capabilities. Inland provinces also carry a larger installed base of older conventional and semi-automatic machines, so the replacement cycle remains one of the clearest demand drivers for new CNC turning machine and equipment across these regions.

Competitive Landscape

The China turning machine and equipment market is moderately fragmented. Tsugami, INDEX-Werke, EMAG, and Nakamura-Tome continue to hold an edge in demanding aerospace, medical, and semiconductor applications because buyers in those fields place heavy weight on precision stability, certifications, and service support. Domestic manufacturers such as Shenyang Machine Tool, Dalian Machine Tool Group, Qinchuan Machine Tool, Ningbo Haitian Precision, Baoji Machine Tool Group, Guangzhou CNC Equipment, and others compete more aggressively on price, delivery speed, and application fit in the middle of the market. This split keeps competition intense across the China turning machine and equipment market because performance expectations are rising even in categories that were once mostly price-led. It also means buyers can no longer be grouped neatly into premium and budget tiers, since many are trying to balance technical quality with capital discipline.

Localization remains a central strategy for foreign suppliers serving the China turning machine and equipment market. DMG MORI highlighted its China-manufactured NLC 2500|700 turning center from Pinghu and the NHC 6300 from Tianjin at CCMT 2026, demonstrating how it is leveraging local production to stay close to Chinese demand. Mazak’s production footprint in Liaoning serves a similar purpose by pairing an international brand position with local delivery and support. These moves matter because local manufacturing helps foreign players respond more quickly to pricing pressure and customer lead-time expectations. They also reduce some of the friction that comes with serving China from offshore production bases alone.

Domestic companies are also moving beyond simple volume competition. Shenyang Machine Tool held a product launch in March 2026 for the VMC850Q, HTC40H/500, and VMU30P, while its 2025 R&D investment reached CNY 215 million (USD 30.7 million), and capital raised for high-end capability development reached CNY 1.7 billion (USD 242.8 million). Ningbo Haitian Precision Machinery signed a CNY 173 million (USD 24.7 million) equipment supply agreement in April 2026 and reported overseas revenue of CNY 558 million (USD 79.7 million) in 2025, indicating both domestic scale-up and a wider export ambition. Smaller specialists are using faster delivery, adaptive pricing, and narrower application focus to defend space in the mid-range. The least developed opportunity still sits in swiss-type and multi-axis turning for medical device and semiconductor clusters, where demand quality is high and domestic capability remains less mature than in mainstream horizontal CNC categories.

China Turning Machine and Equipment Industry Leaders

Shenyang Machine Tool Co., Ltd.

Mazak Corporation

DMG MORI

Dalian Machine Tool Group Corporation

Qinchuan Machine Tool & Tool Group Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Ningbo Haitian Precision Machinery Co., Ltd. signed a CNY 173 million (USD 24.7 million) equipment supply agreement with Haitian International's injection molding affiliate for CNC lathes, automatic machining lines, and machining centers, confirming the company's domestic intra-group expansion and scaling of high-capacity CNC turning production.

- March 2026: Shenyang Machine Tool Co., Ltd. held a product launch event showcasing the VMC850Q vertical machining center, the HTC40H/500 CNC horizontal lathe, and the VMU30P five-axis machining center, targeting humanoid robot structural component machining. The company's 2025 R&D investment reached CNY 215 million (USD 30.7 million), with CNY 1.7 billion (approximately USD 242.8 million) raised from capital markets for high-end capability development, and an innovation consortium formed with upstream and downstream partners.

China Turning Machine and Equipment Market Report Scope

The China Turning Machine and Equipment Market is Segmented by Product Type (Horizontal, Vertical, Conventional, and More), by Automation Type (Manual, Semi-Automatic, and Fully Automatic CNC), and by End-User Industry (Automotive & Commercial Vehicles, Aerospace & Defense, Medical Devices & Surgical Instruments, Oil, Gas, & Energy, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

| Horizontal Turning Equipment |

| Vertical Turning Equipment |

| Swiss-Type Turning Equipment |

| Multi-Tasking Turning Equipment |

| Conventional Turning Equipment |

| Manual |

| Semi-Automatic |

| Fully Automatic CNC |

| Automotive & Commercial Vehicles |

| Aerospace & Defense |

| Medical Devices & Surgical Instruments |

| Oil, Gas, & Energy |

| Electrical, Electronics & Semiconductor Equipment |

| General Industrial Machinery |

| Others (Consumer Goods, Defense Ordnance) |

| By Product Type | Horizontal Turning Equipment |

| Vertical Turning Equipment | |

| Swiss-Type Turning Equipment | |

| Multi-Tasking Turning Equipment | |

| Conventional Turning Equipment | |

| By Automation Type | Manual |

| Semi-Automatic | |

| Fully Automatic CNC | |

| By End-User Industry | Automotive & Commercial Vehicles |

| Aerospace & Defense | |

| Medical Devices & Surgical Instruments | |

| Oil, Gas, & Energy | |

| Electrical, Electronics & Semiconductor Equipment | |

| General Industrial Machinery | |

| Others (Consumer Goods, Defense Ordnance) |

Key Questions Answered in the Report

What is the market size of the China turning machine and equipment market in 2026, and how is it expected to grow by 2031?

The China turning machine and equipment market is forecast to grow from USD 4.8 billion in 2026 to USD 6.7 billion by 2031 at a 6.9% CAGR, supported by automation upgrades, EV-related machining demand, and replacement of older machine tools.

Which product category leads demand in China?

Horizontal segment led in 2025 with a 63% share, as it remains the standard setup across automotive, energy equipment, and general industrial machining.

Which automation setup is gaining the most traction?

Fully automatic CNC is both the largest and fastest-growing automation segment, with 78% share in 2025 and 8.1% CAGR expected through 2031.

Why are EVs important for equipment demand?

EV production increases the need for precision-turning shafts, housings, thermal management components, and gearbox elements, so each new EV production line tends to require more turning capacity than a comparable legacy vehicle line.

Which end-user group is growing fastest?

Aerospace and defense is expected to grow at a 8.6% CAGR through 2031, driven by certification, traceability, and higher-precision requirements that push buyers toward more advanced turning systems.

Which region matters most for suppliers and investors?

Eastern China remains the main hub, accounting for 82.2% of national metal-cutting machine tool output in 2025, while the Chengdu-Chongqing corridor is becoming increasingly important for higher-value inland demand.

Page last updated on: