China Social Commerce Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

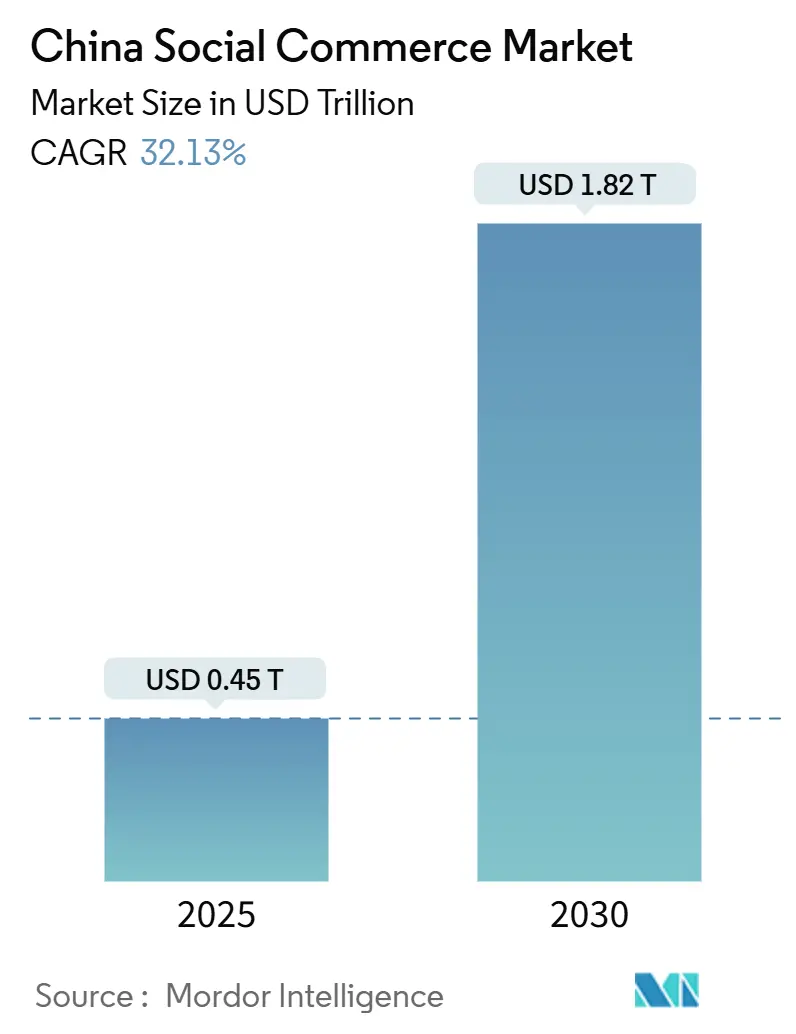

| Market Size (2025) | USD 0.45 Trillion |

| Market Size (2030) | USD 1.82 Trillion |

| Growth Rate (2025 - 2030) | 32.13% CAGR |

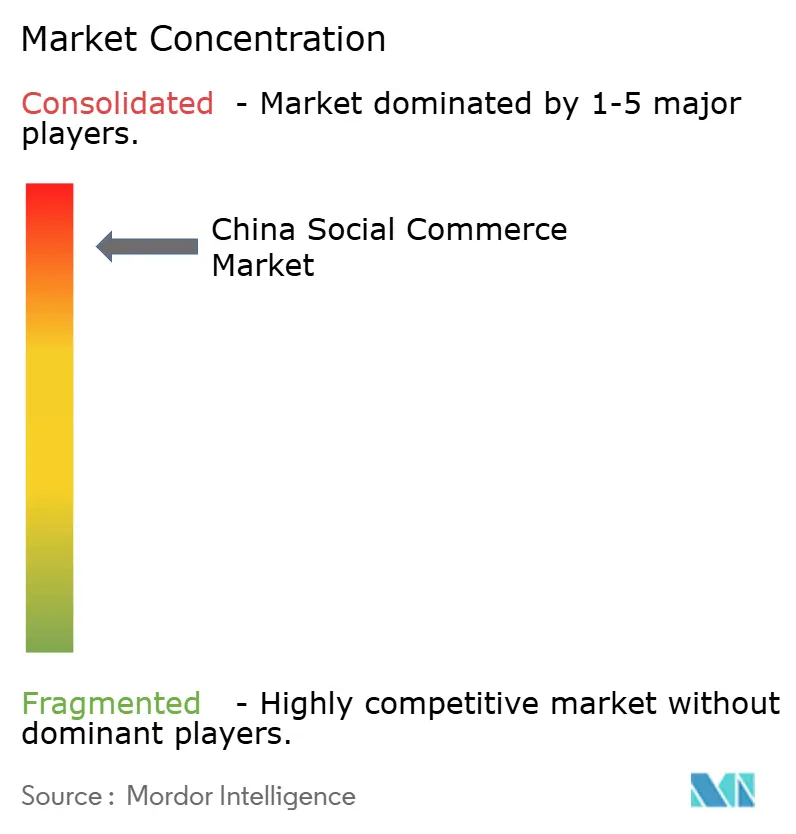

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Social Commerce Market Analysis by Mordor Intelligence

The China social commerce market size stands at USD 0.451 trillion in 2025 and is expected to reach USD 1.816 trillion by 2030, displaying a 32.13% CAGR during the forecast period. Rapid adoption of live-streaming, frictionless in-app payments, and AI-driven product discovery tools are reshaping consumer journeys from inspiration to checkout. Alipay and WeChat Pay play a significant role in streamlining transactions, reducing average checkout times to a few seconds.[1]“Digital Payment Infrastructure Development Report,” People’s Bank of China, pbc.gov.cn Features such as algorithm-driven impulse purchases, seamless mini-program interoperability across platforms like Douyin, Kuaishou, and Xiaohongshu, and enhanced cross-border sales supported by real-time translations are broadening the addressable demand. However, increasing costs associated with acquiring creators and stricter regulations on underage users are impacting short-term profitability, as platforms manage higher compliance and marketing expenditures.

Key Report Takeaways

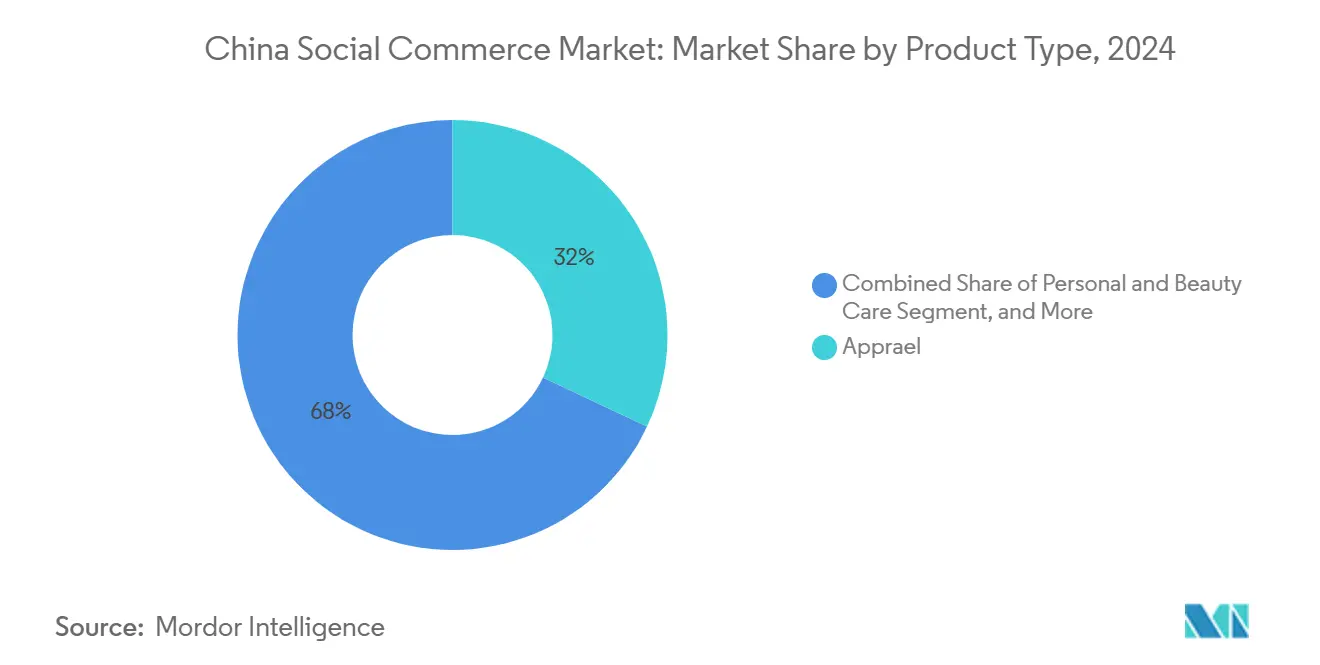

- By product type, apparel led with 32.12% of the China social commerce market share in 2024, while personal and beauty care is projected to expand at a 34.16% CAGR through 2030.

- By device, smartphones accounted for 92.11% of the China social commerce market size in 2024 and are advancing at a 33.23% CAGR through 2030.

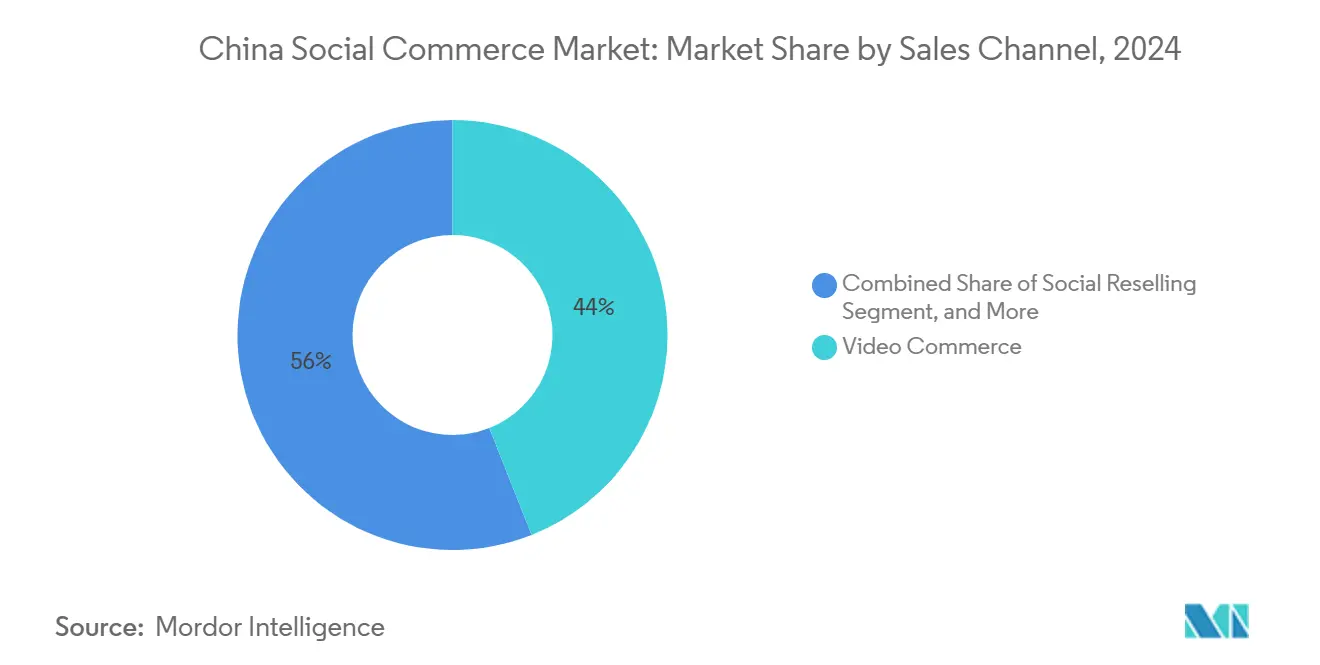

- By sales channel, video commerce captured 44.21% revenue share in 2024; social reselling records the highest forecast CAGR at 34.01% to 2030.

Proportional positioning is established by comparing country level and regional contributions against the global total, including that of China. The social commerce market share in our global report expresses these relative weights.

China Social Commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising live-stream GMV monetization efficiency | +8.2% | National, concentrated in tier-1 cities | Medium term (2-4 years) |

| Platform mini-program innovations beyond WeChat | +6.8% | National, expanding to lower-tier cities | Long term (≥ 4 years) |

| Commerce-focused algorithms driving impulse buys | +7.1% | National, most effective in urban areas | Short term (≤ 2 years) |

| Integration of China-specific social payment rails | +4.9% | National coverage with rural penetration | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Live-Stream GMV Monetization Efficiency

Between 2024 and 2025, the gross merchandise value per viewer in live-streaming experienced significant growth, transforming what were once entertainment-focused broadcasts into efficient sales channels. Leading streamers on Douyin now generate substantial revenue per hour, reflecting a notable increase from early 2024 levels. AI segmentation tools enable brands to align SKUs with micro-audiences in real time, significantly enhancing conversion rates. Post-sale strategies emphasize lifetime value optimization, utilizing exclusive drops and membership perks to encourage repeat purchases. This cycle strengthens platform take rates and ensures hosts are incentivized through tiered commission structures, maintaining content quality.

Platform Mini-Program Innovations Beyond WeChat

By 2025, WeChat is expected to host a significant number of mini-programs.[2]“Investor Relations Financial News,” Tencent Holdings, tencent.com However, cross-platform frameworks introduced by ByteDance and Kuaishou are transforming the economics of scale. Merchants are now leveraging a single code base across various social platforms while maintaining consistent inventory, CRM, and payment reconciliation. This streamlined integration is particularly advantageous for SMEs in smaller cities, enabling them to expand consumer touchpoints and enhance their data repositories with insights from omnichannel behaviors. These unified datasets support more precise personalization, which helps improve average order values and reduce customer churn.

Commerce-Focused Algorithms Driving Impulse Buys

Douyin's predictive engine identifies purchase intent shortly after users engage with content, leveraging real-time indicators such as scroll speed, pause duration, and tap frequency to optimize SKU placements during peak buyer interest.[3]“Douyin Algorithm Purchase Prediction Reaches New Accuracy Levels,” TechCrunch, techcrunch.com Similarly, Xiaohongshu utilizes sentiment analysis on lifestyle posts to recommend products like premium cosmetics or athleisure wear in alignment with user moods, encouraging impulse purchases. This adaptability supports platform-wide feedback loops, enabling continuous adjustments that maintain session engagement without overly commercializing user feeds.

Integration of China-Specific Social Payment Rails

One-touch embedded payments simplify checkout processes, integrating features such as social sharing, group buying, and payment splitting directly within chats. Alipay and WeChat Pay APIs facilitate multi-currency transactions, addressing increasing cross-border demand from regions like Southeast Asia and North America. By combining transaction data with behavioral insights, merchants can develop a comprehensive understanding of their customers, improving re-targeting efforts, pricing strategies, and inventory management.

Restraints Impact Analysis*

| Restraint | (~) (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating KOL/creator acquisition costs | -4.7% | National, most acute in tier-1 cities | Short term (≤ 2 years) |

| Tighter CAC regulations on under-age users | -3.2% | National regulatory compliance | Medium term (2-4 years) |

| Regional logistics bottlenecks in lower-tier cities | -2.8% | Lower-tier cities and rural areas | Medium term (2-4 years) |

| Counterfeit-goods crack-downs raising compliance costs | -2.1% | National, cross-border trade focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating KOL/Creator Acquisition Costs

In early 2024, top influencers experienced a significant increase in campaign fees as platforms prioritized established sellers in their ranking algorithms.[4]“China Influencer Marketing Costs Surge in 2024,” Wall Street Journal, wsj.com Mid-tier brands have shifted their focus toward allocating a substantial portion of their marketing budgets to creator fees, reducing opportunities to explore emerging talent. Additionally, new disclosure mandates have introduced administrative challenges and extended production timelines. In response, brands are developing in-house hosts and utilizing private-domain traffic. However, the time required to implement these strategies is delaying returns on investment, creating financial pressures for newer entrants.

Tighter CAC Regulations on Under-Age Users

In 2024, newly implemented minor-protection regulations require age verification, parental consent, and daily usage limits, significantly reducing youth engagement.[5]“Enhanced Minor Protection Regulations Implementation,” Cyberspace Administration of China, cac.gov.cn Platforms are allocating resources to biometric ID verification systems and AI-driven moderation, resulting in substantial industry-wide costs. Marketing strategies are shifting focus toward adult demographics, while apps with a predominantly younger user base are exploring international markets to offset traffic declines. Content creators are adjusting their tone and product offerings to align with compliance requirements while maintaining audience engagement, though they are encountering slower organic growth in the evolving environment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Apparel Leadership Faces Beauty Disruption

Apparel retained 32.12% of the China social commerce market share in 2024, this performance was supported by the implementation of virtual try-on tools, which reduced return rates compared to traditional e-commerce. Furthermore, live styling sessions and size recommendation engines strengthened consumer trust and facilitated faster purchase decisions. Yet personal and beauty care is on track for a 34.16% CAGR through 2030, powered by AR-enabled shade matching and influencer-led authenticity checks that resonate with Gen Z.

By 2029, if the current trend continues, beauty products are anticipated to surpass apparel in China's social commerce market. Home products and health supplements are gaining traction, driven by group-buy discounts and community-focused health narratives. Seasonal campaigns emphasizing regional specialties sustain the momentum for food and beverages, while accessories benefit from impulse purchases influenced by fashion content. The increasing preference for premium and experiential goods reflects a shift in consumer behavior toward lifestyle enhancement rather than purely functional purchases.

At the same time, diversifying the product mix helps reduce revenue concentration risks for platforms. Brands are adopting strategies such as curated bundles, subscription models, and exclusive product launches to encourage repeat purchases and increase average transaction values. Rising disposable incomes in tier-2 cities are driving demand for mid-to-high-end beauty and wellness products. Peer reviews play a significant role in reducing perceived switching risks, enabling niche brands to establish a presence without substantial advertising investments. The integration of mini-program data supports real-time tracking of product performance, allowing for agile inventory management and pricing strategies to maintain profitability in a dynamic market environment.

By Device: Smartphone Supremacy Reinforces Mobile-First Strategy

Smartphones controlled 92.11% of the China social commerce market size in 2024, driven by native payment modules and one-hand navigation optimized for vertical video. High-definition streams, enabled by the 5G rollout, enhance user engagement and contribute to increased transaction values. Desktops and laptops are primarily utilized for B2B or bulk orders that require larger screens and the ability to download spreadsheets. Voice search, along with in-app camera tools, facilitates new discovery methods, allowing users to scan products in physical stores and quickly access their social commerce listings.

With smartphones maintaining dominance, platforms are optimizing low-bandwidth modes for rural users and developing gesture-based interfaces designed for seniors. Battery-efficient streaming codecs and AI-driven video compression help manage data costs, supporting broader adoption among lower-income groups. As mobile wallets become a standard payment method, merchants utilize purchase history, location, and social graph data to deliver highly relevant offers. In China, the social commerce market benefits businesses that integrate inspiration, evaluation, and payment into a seamless mobile experience.

By Sales Channel: Video Commerce Maturity Meets Social Reselling Innovation

Video commerce garnered 44.21% of 2024 transaction value, proving that shoppable live and short clips anchor the mainstream purchase journey. Hosts blend entertainment and product demos, shortening decision cycles and boosting cart sizes. Yet social reselling outpaces all channels with a 34.01% CAGR, as micro-entrepreneurs mobilize trusted peer networks to curate and recommend goods. In lower-tier cities, where word-of-mouth holds significant influence, group chats, red-envelope incentives, and commission sharing drive viral diffusion.

Social network-driven commerce and group buying address distinct shopper motivations: content discovery and cost optimization. Positioned upstream, review-and-discovery platforms influence consumer decisions by utilizing authentic testimonials and unboxing videos to validate product quality. This interaction among channels illustrates a multifaceted purchase journey: consumers gather information in one channel, seek social validation in another, and complete transactions during live-stream sessions. As a result, cross-channel attribution analytics play a critical role in optimizing marketing expenditure within China's social commerce landscape.

Geography Analysis

In China, Tier-1 cities—Beijing, Shanghai, Guangzhou, and Shenzhen—represent a substantial portion of the nation's market value, despite accounting for a small segment of the population. This highlights their advanced logistics capabilities and higher income levels. These cities, with their efficient same-day delivery services, concentration of premium creators, and early adoption of technology, function as testing grounds for AI-driven recommendations and augmented reality commerce initiatives. Platforms strengthen customer engagement by offering city-specific features, such as expedited fulfillment for fashion launches and exclusive live-streamed events.

Tier-2 and Tier-3 cities are becoming significant contributors to the growth of China's social commerce market. Cities such as Chengdu, Wuhan, and Xi’an utilize their skilled talent pools and expanding technology ecosystems to drive digital shopping adoption. Investments in logistics by major players have considerably reduced delivery times, narrowing the service gap with coastal urban centers. Additionally, households focused on cost-efficiency are increasingly adopting group-buying models and social reselling, enabling merchants to broaden their customer base while managing acquisition costs effectively.

Rural areas encounter challenges due to inadequate warehousing and payment infrastructure; however, government-led digital inclusion initiatives are gradually improving access. Measures such as mobile wallet subsidies and the rollout of 5G networks in villages are supporting incremental progress. Internationally, Chinese platforms are extending their reach by customizing interfaces for markets in Southeast Asia, North America, and Europe. These efforts, supported by features like real-time translation and multi-currency payment options, enable seamless transactions and expand the scope of China's social commerce market beyond domestic boundaries.

Mordor Intelligence examines the social commerce market across diverse other regional markets as well, offering granular country-level perspectives for India, Brazil, Canada, and France and more.

Competitive Landscape

The social commerce market in China is highly fragmented, with no single ecosystem dominating the space. Differentiation in this competitive environment depends on proprietary algorithms, community-focused features, and integrated payment systems. WeChat leverages its social graph to offer mini-program storefronts that integrate seamlessly into users' messaging activities. Douyin utilizes short-video content to drive higher conversion rates compared to traditional e-commerce platforms. Taobao Live benefits from Alibaba's extensive logistics infrastructure and merchant network to efficiently manage a wide range of SKUs.

Patent filings related to social commerce have significantly increased in 2024, reflecting intensified investment in areas such as real-time translation, augmented reality try-ons, and blockchain-based authentication. Luxury brands are exploring exclusive capsule collections on Kuaishou, while niche platforms like Dewu focus on sneaker authentication to build trust among younger consumers. Larger players are allocating resources to compliance systems to meet stricter data and content regulations, creating higher entry barriers for new participants. Opportunities exist in developing senior-friendly interfaces and promoting ESG-driven product categories. However, successful entrants must integrate entertainment, community engagement, and streamlined checkout processes into a cohesive user experience to establish a foothold in China's social commerce market.

China Social Commerce Industry Leaders

Tencent Holdings Ltd.

Beijing ByteDance Technology Co., Ltd.

Kuaishou Technology

PDD Holdings Inc. (Pinduoduo)

Alibaba Group Holding Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: ByteDance's Lemon8 is expanding, reflecting the application of China's Xiaohongshu model to international markets. Lemon8's increasing presence in Southeast Asia and the West highlights the adoption of China's content-focused commerce strategy. This global engagement supports domestic innovation, strengthens ByteDance's market position, and contributes to the evolution of social commerce formats in China, particularly among Gen Z consumers who prefer lifestyle-oriented, creator-driven shopping experiences.

- August 2025: At WAIC 2025, Tencent presented its AI strategy. By integrating AI-driven personalization, content generation, and mini-program functionality into WeChat's ecosystem, Tencent aims to enhance user engagement and optimize e-commerce processes. These developments support merchants in implementing more precise and targeted campaigns, aligning with China's mobile-first and socially integrated shopping behaviors. This approach strengthens Tencent's position within China's digital retail environment.

- July 2025: Taobao experienced significant user growth in Thailand following its launch in the local language. This development reflects Alibaba's strategic efforts to expand its social commerce presence beyond China. The success in Thailand demonstrates the effectiveness of localized, mobile-centric shopping—an integral aspect of China's social commerce framework—and highlights Alibaba's capability to adapt and scale its platforms internationally. These efforts are likely to contribute to innovation and enhance competitiveness within China's domestic market, particularly in cross-border commerce and platform design.

- July 2025: Bilibili’s rise as a Gen Z-focused video platform is reshaping China’s social commerce market. With over 80% of users under 35, it offers brands a unique space to engage young consumers through influencer marketing, live streaming, and native ads. Its interactive features like bullet comments foster deep community engagement, making it ideal for product discovery and viral campaigns. Bilibili’s integration of e-commerce tools enables seamless shopping experiences directly within content.

- November 2024: Live streaming on Weibo serves as a key component in China's social commerce market. It enables real-time interaction, product demonstrations, and influencer collaborations, contributing to brand visibility and conversions. With features such as interactive comments, virtual gifts, and direct shopping links, Weibo Live integrates entertainment with commerce. This format aligns with China's mobile-first consumer behavior and supports the integration of content, community, and commerce—core elements of the country's digital retail ecosystem.

China Social Commerce Market Report Scope

The China Social Commerce Market Report is Segmented by Product Type (Apparel, Personal and Beauty Care, Accessories, Home Products, Health Supplements, Food and Beverages, Other Product Types), Device (Laptops and Desktops, Smartphones), Sales Channel (Video Commerce, Social Network-Led Commerce, Social Reselling, and Other Sales Channel Types), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Apparel |

| Personal and Beauty Care |

| Accessories |

| Home Products |

| Health Supplements |

| Food and Beverages |

| Other Product Types |

| Laptops and Desktops |

| Smartphone |

| Video Commerce |

| Social Network-Led Commerce |

| Social Reselling |

| Group Buying / Team Purchase |

| Product Review and Discovery Platforms |

| By Product Type | Apparel |

| Personal and Beauty Care | |

| Accessories | |

| Home Products | |

| Health Supplements | |

| Food and Beverages | |

| Other Product Types | |

| By Device | Laptops and Desktops |

| Smartphone | |

| By Sales Channel | Video Commerce |

| Social Network-Led Commerce | |

| Social Reselling | |

| Group Buying / Team Purchase | |

| Product Review and Discovery Platforms |

Key Questions Answered in the Report

What is the 2025 valuation of the China social commerce market?

It is valued at USD 450.97 billion in 2025.

How fast is the market expected to grow?

Forecasts indicate a 32.13% CAGR through 2030.

Which product category currently leads spending?

Apparel leads with 32.12% share in 2024.

What device channels dominate transactions?

Smartphones account for 92.11% of 2024 value.

Which sales channel shows the fastest future growth?

Social reselling is projected to grow at 34.01% CAGR.

What is a key risk facing platforms?

Rising creator acquisition costs that have more than doubled since 2024.

Page last updated on: