China Robotics CNC Turning Centers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

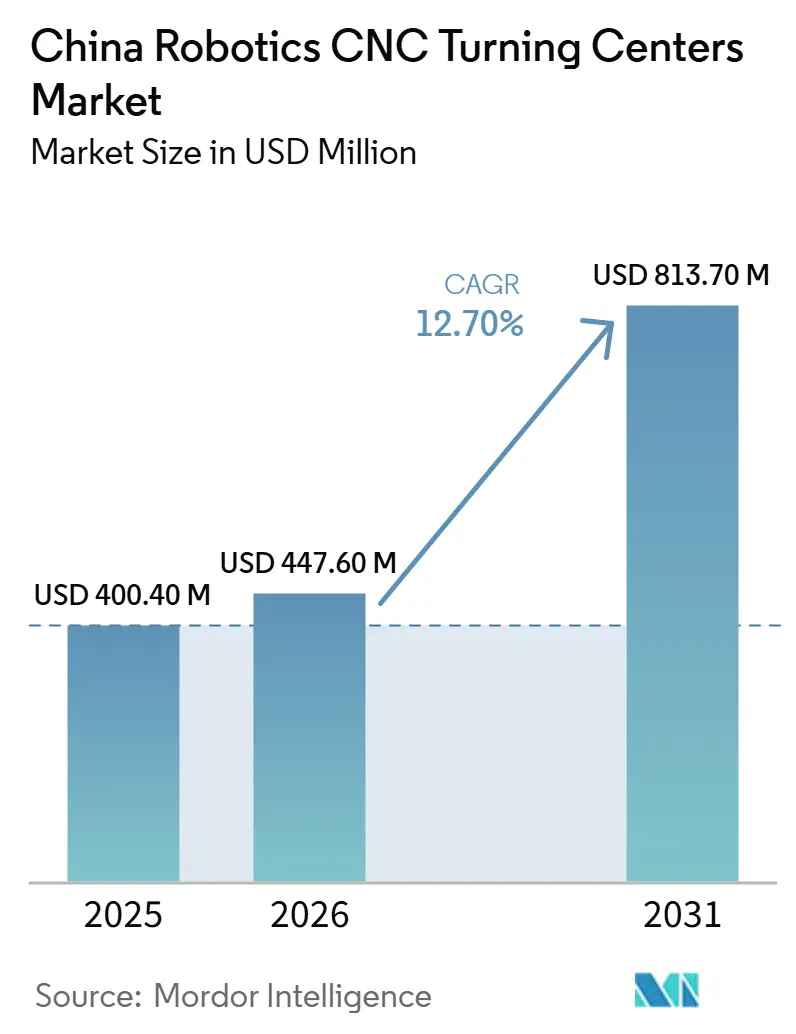

| Base Year Market Size (2025) | USD 400.40 Million |

| Market Size (2026) | USD 447.60 Million |

| Market Size (2031) | USD 813.70 Million |

| Growth Rate (2026 - 2031) | 12.70% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Robotics CNC Turning Centers Market Analysis by Mordor Intelligence

The China Robotics CNC Turning Centers Market size is expected to increase from USD 400.40 million in 2025 to USD 447.60 million in 2026 and reach USD 813.70 million by 2031, growing at a CAGR of 12.70% over 2026-2031.

The China robotics CNC turning centers market is advancing as industrial robotics has become a core part of national manufacturing policy, and automation now shapes plant qualification, export readiness, and production consistency across many factories. China installed 295,000 industrial robots in 2024, bringing its operating stock to 2,027,000 units, keeping replacement, upgrade, and new-turning-cell demand active across precision manufacturing lines. Domestic suppliers also gained ground in 2024, capturing 57% of industrial robot installations in China, which shows that the competitive center of the China robotics CNC turning centers market is shifting toward local suppliers with stronger price positions and closer integration support. Policy support remains a major stabilizer because the 15th Five-Year Plan names robotics as a strategic emerging industry and because the 2025 AI plus manufacturing initiative directly supports AI-enabled CNC systems and industrial robots. At the same time, the China robotics CNC turning centers market still faces pressure from imported high-end motion components and tighter supplier margins. Still, strong NEV output, dense robot adoption, and subsidy-backed equipment renewal keep the medium-term demand base firm.

Key Report Takeaways

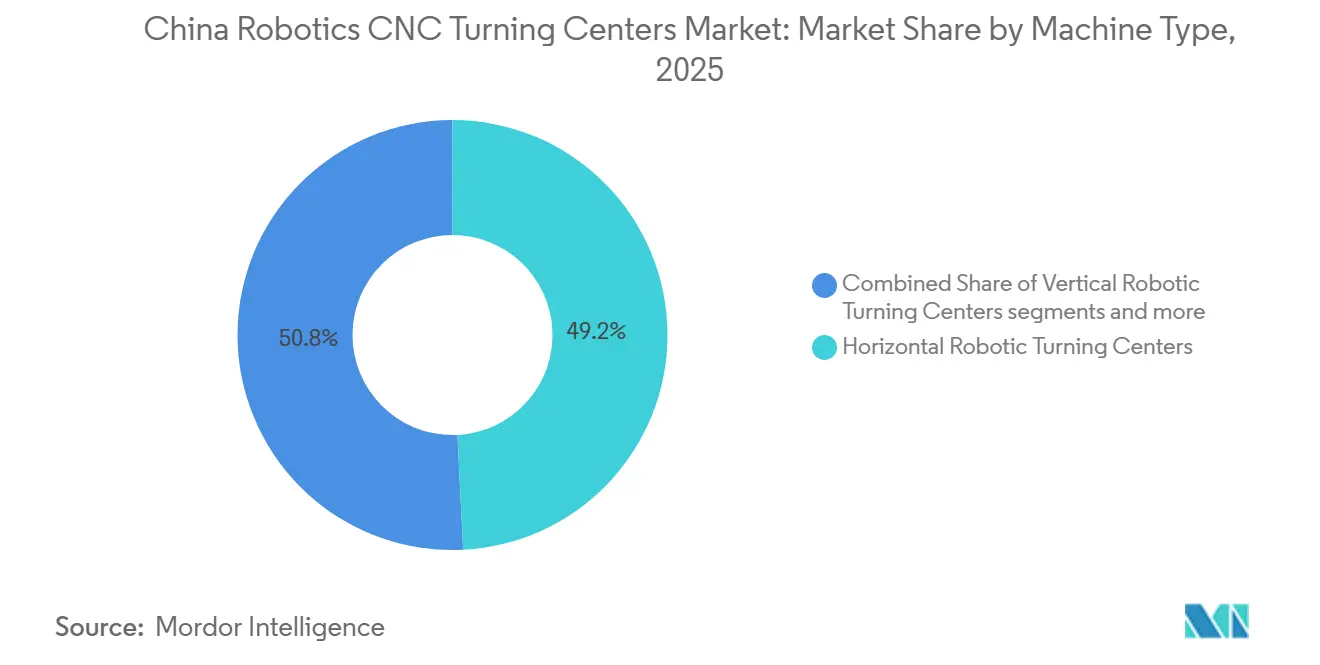

- By machine type, horizontal robotic turning centers led with 49.21% of the China robotics CNC turning centers market share in 2025, while multi-tasking robotic turning centers are projected to record the fastest CAGR at 13.52% through 2031.

- By robot type, articulated robots accounted for 57.61% of the China robotics CNC turning centers market size in 2025, while collaborative robots are forecast to expand at a 14.78% CAGR through 2031.

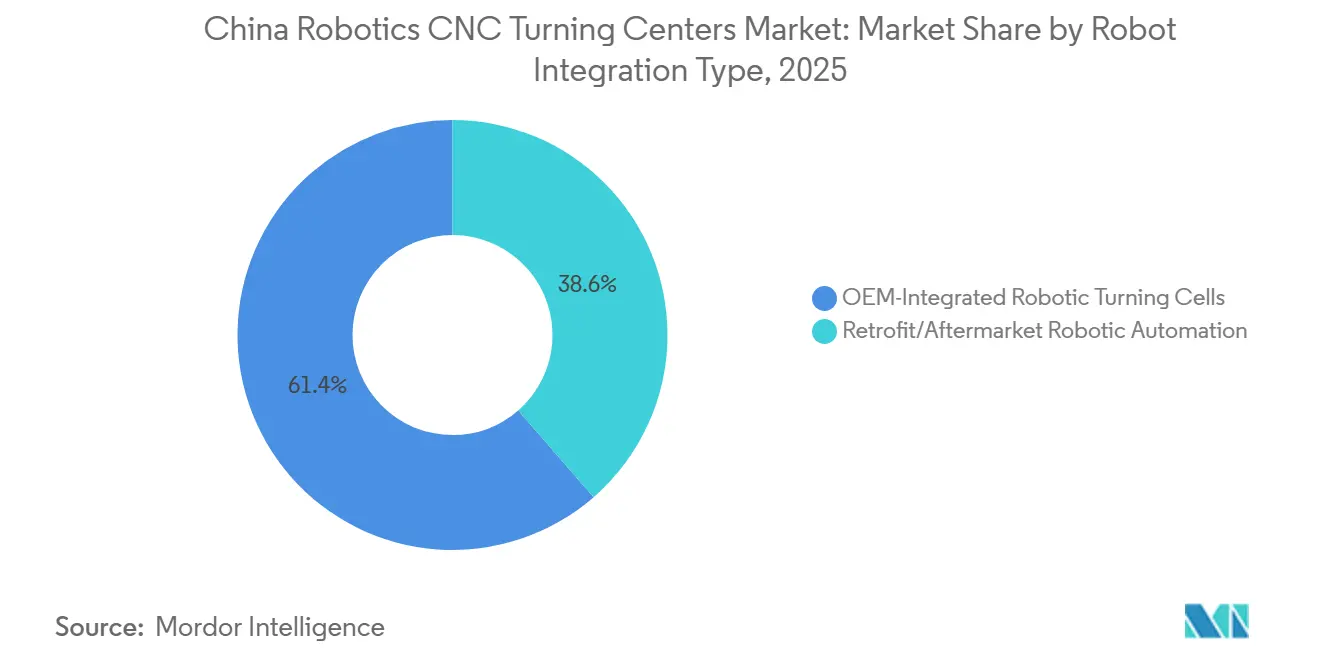

- By robot integration type, OEM-integrated robotic turning cells accounted for 61.40% of revenue in 2025, while retrofit/aftermarket robotic automation is projected to grow at a 15.21% CAGR through 2031.

- By end-user industry, automotive and commercial vehicles accounted for 32.80% of revenue in 2025, while medical devices and surgical instruments are forecast to grow at a 16.76% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China Robotics CNC Turning Centers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Made in China 2025 and Successive Industrial Policies Accelerating Robotic Manufacturing Automation | +3.2% | National | Short term (≤ 2 years) |

| Rising Industrial Robot Density Accelerating Manufacturing Automation | +2.8% | National, with high concentration in Guangdong, Jiangsu, and Shandong | Short term (≤ 2 years) |

| Direct Government Subsidy Programs Lowering Automation Capex for Manufacturers | +2.3% | National, extended to Tier-2 cities including Chongqing, Wuhan, and Qingdao. | Medium term (2-4 years) |

| New Energy Vehicle and EV Component Manufacturing Scaling Rapidly | +2.0% | Guangdong, Shanghai, Hubei, Shandong, and Jilin | Medium term (2-4 years) |

| Aggressive Export Expansion by Chinese Robot Makers Building Global Credibility and Scale Economies | +1.5% | National, with spillover to ASEAN, the Middle East, and the EU | Long term (≥ 4 years) |

| Ongoing Capacity Expansion by Domestic Robotics Manufacturers Supporting Long-Term Market Growth | +1.2% | National, with manufacturing clusters in Liaoning, Hebei, and Zhejiang | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Made in China 2025 and Successive Industrial Policies Accelerating Robotic Manufacturing Automation

Industrial policy remains the clearest structural support for the China robotics CNC turning centers market. The Made in China 2025 program identified industrial robots as a priority technology area and set the tone for local component development, even though later policy frameworks largely absorbed its language and direction.[1]Ministry of Industry and Information Technology, “Economic Operation of the Automotive Industry, May 2026,” Ministry of Industry and Information Technology, miit.gov.cn The 15th Five-Year Plan for 2026 to 2030 now places robotics among eight strategic emerging industries and lists embodied intelligence among future industries, giving provincial and sector plans a clear signal to keep automation spending active. The 2025 AI plus manufacturing initiative also calls for AI agents in CNC machine tools and industrial robots, broadening the application range for robotic turning cells and supporting higher-value system configurations.[2] International Federation of Robotics, “China Makes AI-Powered Robots Core of National Strategy,” International Federation of Robotics, ifr.org This policy layering shortens adoption cycles, supports localization of key mechanical subsystems, and gives the China robotics CNC turning centers market a stronger demand floor than a purely cyclical capex market would normally have.

Rising Industrial Robot Density Accelerating Manufacturing Automation

Robot density is now a direct growth lever for the China robotics CNC turning centers market. China reached 567 robots per 10,000 manufacturing workers in 2024, ranked third globally, and built an operating stock of 2,027,000 units after installing 295,000 robots in that year alone. The metal and machinery sector, one of the closest end markets for robotic turning cells, recorded 54,600 installations in 2024, with Chinese suppliers accounting for 90% of those units and domestic installations rising 31% year over year. As robot adoption increases, customers increasingly judge systems by cell orchestration, predictive maintenance, and process software rather than arm hardware alone. That shift favors suppliers in the China robotics CNC turning centers market that can combine the robot, the CNC controller, and the software layer into a single integrated offering.

Direct Government Subsidy Programs Lowering Automation Capex for Manufacturers

Subsidies and tax support are reducing the upfront cost of automation across the China robotics CNC turning centers market. MIIT and related agencies formalized qualification rules for industrial mother machine enterprises that can benefit from an extra deduction treatment tied to advanced CNC systems, functional components, and controllers, thereby lowering effective acquisition costs for qualified buyers. The State-led equipment renewal agenda also keeps CNC machine tool upgrades within the eligible investment pool, supporting both new system purchases and plant modernization programs. The 15th Five-Year Plan further strengthens this framework through a CNY 60 billion (USD 8.82 billion) fund for AI-linked industrial investment, designed to crowd in provincial and private capital. These measures matter most for retrofit projects and mid-sized manufacturers, where a lower payback period can shift automation from a delayed plan to an approved purchase.

New Energy Vehicle and EV Component Manufacturing Scaling Rapidly

The NEV production cycle is one of the strongest near-term supports for the China robotics CNC turning centers market. MIIT reported NEV production of 1.554 million units in May 2026, up 22.4% year over year, and 5.841 million units across January to May 2026, equal to 47.5% of total auto sales. These volumes keep demand high for motor shafts, battery casings, drive unit housings, and gear hubs that need repeatable tolerances and stable unattended machining conditions. MIIT has also extended the NEV purchase tax exemption conditions for qualifying models through 2026 and 2027, improving production visibility for downstream machining suppliers planning multi-year equipment investments. As drivetrain designs standardize across more platforms, process repeatability improves, making robotic turning more attractive than labor-intensive setups for an increasing share of parts programs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dependence on Imported High-End Servo Systems, Controllers, and Precision Components | -1.8% | National, most acute in Guangdong and Liaoning | Medium term (2-4 years) |

| Intensifying Price Competition that Compresses Supplier Margins and Threatens Long-Term R&D Investment | -1.4% | National, most visible in coastal export-oriented manufacturing clusters | Short term (≤ 2 years) |

| Cyclical Sensitivity to Capital Expenditure in Manufacturing Sectors | -1.0% | National | Short term (≤ 2 years) |

| Shortage of Skilled Robotics Integration and Maintenance Talent Despite High Adoption Rates | -0.7% | National, most severe in inland manufacturing hubs, including Chengdu and Wuhan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Dependence on Imported High-End Servo Systems, Controllers, and Precision Components

Imported high-end components remain a real constraint on the China robotics CNC turning centers market. The servo motors, gear reducers, and motion controllers account for close to 70% of an industrial robot's bill of materials, and the 15th Five-Year Plan directly identifies these areas as localization priorities. The same draft notes that localization improved in low to mid-range servo components by 2025, but high-end encoders, power semiconductors, and precision transmission parts still rely heavily on imports. That leaves turning-center builders exposed to exchange rate fluctuations, export controls, and component-level supply disruptions. It also creates technical lock-in because switching an installed design from one servo family to another often requires changes to the control architecture, revalidation, and customer requalification.

Intensifying Price Competition that Compresses Supplier Margins and Threatens Long-Term R&D Investment

Price competition is also restraining the China robotics CNC turning centers market, especially in the mid-range segment. Chinese industrial robots are priced 20% to 35% below comparable foreign models, which helps adoption but puts pressure on margins and weakens reinvestment capacity. That is important because suppliers need steady margin support to fund software, motion control, vision systems, and adaptive machining features that take years to develop. If margins keep tightening, vendors may struggle to build the premium software layers that increasingly define performance in automated turning cells. This risk does not stop growth in the China robotics CNC turning centers market, but it can slow the move from cost-led competition to deeper product differentiation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machine Type: Horizontal Centers Anchor Volume, Multi-Tasking Redefines Value

Horizontal robotic turning centers accounted for 49.21% of the China robotics CNC turning centers market in 2025. They remain the default choice for high-volume machining because gravity assists chip evacuation, workholding is straightforward for rotational parts, and gantry-style loading fits well with the layout. These strengths matter in automotive shafts, bearing rings, and EV motor housing programs where uptime and repeatability drive purchasing decisions. Vertical robotic turning centers still serve shorter, heavier disc or flange parts common in brake systems and in the production of heavy machinery.

The multi-tasking robotic turning centers segment is forecast to grow at a 13.52% CAGR from 2026 to 2031, which makes it the fastest-growing machine type in the China robotics CNC turning centers market. Its appeal lies in combining turning, milling, drilling, and grinding in a single setup, reducing transfers, cutting setup time, and lowering tolerance stacking in complex parts. That fits rising demand from NEV drivetrains and aerospace structural components, where part geometry and precision requirements are becoming harder to manage across separate machines. The China robotics CNC turning centers market is therefore moving toward systems that do more work within a single envelope, especially as AI-enabled CNC control becomes more relevant in multi-process sequences.

By Robot Type: Articulated Arms Maintain Scale, Cobots Rewrite Integration Economics

Articulated robots accounted for 57.61% of the China robotics CNC turning centers market share in 2025. They keep the largest position because they cover a broad payload range and because automotive and machinery integrators in China already have deep experience with their use in tending, loading, and transfer tasks. Gantry and Cartesian systems remain useful in dedicated transfer lines where linear motion, high payload handling, and repetitive travel paths matter more than arm flexibility. This keeps articulated robots in the leading role for scale, while other robot types grow around specific layout or cost needs.

Collaborative robots are projected to expand at a 14.78% CAGR from 2026 to 2031, making them the fastest-growing robot category in the China robotics CNC turning centers market. Cobot sales reached 49,500 units in China in 2025, and domestic manufacturers held close to 90% of the domestic cobot segment, indicating that local support and low system costs are widening adoption. Cobots matter in turning applications because they need less safety guarding and shorter programming cycles, which opens robotic tending to mid-tier job shops that could not justify full articulated automation before. The China robotics CNC turning centers market is seeing this shift most clearly, as smaller batch sizes, tighter labor availability, and lower capex budgets push customers toward simpler deployment economics.

By Robot Integration Type: OEM Cells Dominate, Retrofit/Aftermarket Robotic Automation Unlocks Untapped Scale

OEM-Integrated robotic turning cells accounted for 61.40% of revenue in 2025, making them the largest integration mode in the China robotics CNC turning centers market. Large automotive, NEV, and aerospace manufacturers prefer these systems because they arrive with validated process settings, coordinated tooling logic, and warranty-backed support from the machine builder. That reduces commissioning risk and supports strict launch timelines at high-volume suppliers. It also allows machine builders to increase revenue per system and generate recurring service income from maintenance, upgrades, and software support.

Retrofit/aftermarket robotic automation is forecast to grow at a 15.21% CAGR from 2026 to 2031, the fastest rate among integration types in the China robotics CNC turning centers market. China has a large installed base of conventional turning centers that remain mechanically usable but lack robotic loading, unattended running, and modern software coordination. Retrofitting these machines costs much less than replacing them with full new cells, which is why the segment is gaining traction among cost-sensitive manufacturers. MIIT's technology and equipment renewal framework supports this direction, as retrofit automation is part of the broader upgrade agenda for manufacturing plants.

By End-User Industry: Automotive Anchors Demand, Medical Precision Sets the Growth Pace

Automotive and commercial vehicles held 32.80% of the China robotics CNC turning centers market share in 2025. This base is wide because vehicle production requires a broad mix of turned parts across conventional and electric platforms, including engine blocks, brake components, differential housings, EV motor shafts, and battery module connectors. NEV growth is raising the specification of these programs because drivetrains use tighter tolerances and harder materials, which increases the value of robotic turning systems. The automotive segment therefore remains the main demand anchor for the China robotics CNC turning centers market, even as the mix of parts changes.

Medical devices and surgical instruments are forecast to grow at a 16.76% CAGR from 2026 to 2031, making them the fastest-growing end-user group in the China robotics CNC turning centers market. The growth case rests on the need for very high-dimensional control, repeatable process documentation, and consistent unattended machining for small precision parts. That favors robotic turning centers with vision support, in-process gauging, and stable machine behavior over long production runs. Aerospace and defense, electronics and semiconductor equipment, general industrial machinery, and oil, gas, and energy also remain meaningful outlets because they drive demand for titanium parts, wafer-handling components, valves, fittings, and pump elements across the China robotics CNC turning centers market.

Geography Analysis

China accounted for 43.5% of the global operational robot stock in 2025, according to IFR reporting, underscoring how deeply the China robotics CNC turning centers market is tied to the country's manufacturing base. The Yangtze River Delta remains the densest domestic cluster for demand and supply because Shanghai, Jiangsu, and Zhejiang bring together automotive suppliers, electronics producers, precision machining firms, and CNC equipment makers. This concentration supports shorter delivery cycles, denser technical talent, and easier coordination between OEMs, integrators, and end users. It also supports export logistics for machine tool shipments moving through coastal infrastructure. China's machine tool exports reached USD 9.68 billion in 2025, up 17.9% year over year, which reinforces the role of these coastal clusters in the China robotics CNC turning centers market.[3]China Machine Tool & Tool Builders’ Association, “2025 Annual Economic Report of the Machine Tool and Tool Industry,” China Machine Tool & Tool Builders’ Association, cjcsc.cn

The Pearl River Delta is the second major hub in the China robotics CNC turning centers market because Guangdong combines electronics production with a fast-growing base of NEV components. The region benefits from strong robot adoption in electrical and electronics manufacturing, where domestic Chinese suppliers accounted for 59% of 83,000 robot installations in 2024. This makes Guangdong important not only as an end-demand center but also as a proving ground for locally integrated robotic turning solutions. Its role is likely to remain strong as electronics, EV systems, and export manufacturing continue to overlap within a single industrial corridor.

Northeast China, especially Liaoning, remains relevant to the China robotics CNC turning centers market because of its machine tool heritage and heavy industrial base. Demand is more closely linked to oil and gas, energy, and general machinery applications than to electronics-heavy production. Inland cities such as Chongqing, Wuhan, and Chengdu are also becoming more important as subsidy-backed equipment renewal spreads automation beyond the main coastal centers. The national scope of the renovation city pilot framework means the China robotics CNC turning centers market is no longer concentrated only in first-tier manufacturing regions, even though those regions still hold the densest installed base.

Competitive Landscape

The China robotics CNC turning centers market is moderately fragmented. Global OEMs remain strongest in premium precision areas such as advanced multi-axis control, high-end spindles, and demanding aerospace or medical applications. Domestic suppliers are gaining ground fastest in mid-volume, cost-sensitive programs where pricing, localized service, and rapid integration matter most. That shift became clearer in 2024 when Chinese domestic manufacturers captured 57% of industrial robot installations in the country for the first time. The China robotics CNC turning centers market is therefore becoming increasingly contested at both the machine and system integration levels.

Competitive strategy is moving toward vertical integration and software control across the China robotics CNC turning centers market. Domestic players are seeking to reduce their reliance on external suppliers by investing in servo systems, controllers, and software layers that enhance overall system performance and protect margins. Estun Automation's 2026 Hong Kong listing prospectus stated that around 20% of net IPO proceeds would be allocated to next-generation R&D, indicating that product depth and platform capabilities are now central to competition. This strategy matters because buyers increasingly compare vendors based on uptime tools, adaptive control logic, and service responsiveness rather than hardware alone.

Foreign suppliers are also adapting their approach in the China robotics CNC turning centers market rather than relying only on imported premium positioning. KUKA used NVIDIA GTC 2026 to introduce the KUKA Automation Management Platform, which links industrial robots with AI-driven production orchestration and real-time cell management for manufacturing environments. That move shows how the software layer is becoming one of the most important competitive spaces. White space remains in real-time adaptive turning control, digital twin simulation, and in-cycle spindle health prediction, where no supplier has established a decisive lead. Compliance with recognized robot performance standards also favors established vendors because tender requirements increasingly reward proven qualification depth over low upfront price alone.

China Robotics CNC Turning Centers Industry Leaders

DMG MORI Co., Ltd.

Yamazaki Mazak Corporation

Makino Milling Machine Co., Ltd.

Okuma Corporation

DN Solutions Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: KUKA unveiled the KUKA Automation Management Platform (KUKA AMP) at NVIDIA GTC 2026, a Physical AI software platform designed to bridge industrial robots with AI-driven production orchestration and real-time adaptive cell management for Chinese manufacturing customers.

- March 2026: Estun Automation completed its Hong Kong Stock Exchange H-share debut, raising HKD 1,407.35 million (USD 181 million). Proceeds are earmarked for global expansion of production capacity, next-generation robotics R&D, and overseas strategic acquisitions.

China Robotics CNC Turning Centers Market Report Scope

The China Robotics CNC Turning Centers Market is Segmented by Machine Type (Horizontal Robotic Turning Centers, Vertical Robotic Turning Centers, and more), by Robot Type (Articulated Robots, and More), by Robot Integration Type (OEM, Retrofit/Aftermarket Robotic Automation), by End-User Industry (Oil, Gas, and Energy, Aerospace & Defense, and More), The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

| Horizontal Robotic Turning Centers |

| Vertical Robotic Turning Centers |

| Multi-Tasking Robotic Turning Centers |

| Others |

| Articulated Robots |

| Collaborative Robots (Cobots) |

| Gantry/Cartesian Robots |

| OEM-Integrated Robotic Turning Cells |

| Retrofit/Aftermarket Robotic Automation |

| Automotive and Commercial Vehicles |

| Aerospace & Defense |

| Medical Devices and Surgical Instruments |

| Oil, Gas, and Energy |

| Electrical, Electronics and Semiconductor Equipment |

| General Industrial Machinery |

| Others |

| By Machine Type | Horizontal Robotic Turning Centers |

| Vertical Robotic Turning Centers | |

| Multi-Tasking Robotic Turning Centers | |

| Others | |

| By Robot Type | Articulated Robots |

| Collaborative Robots (Cobots) | |

| Gantry/Cartesian Robots | |

| By Robot Integration Type | OEM-Integrated Robotic Turning Cells |

| Retrofit/Aftermarket Robotic Automation | |

| By End-User Industry | Automotive and Commercial Vehicles |

| Aerospace & Defense | |

| Medical Devices and Surgical Instruments | |

| Oil, Gas, and Energy | |

| Electrical, Electronics and Semiconductor Equipment | |

| General Industrial Machinery | |

| Others |

Key Questions Answered in the Report

What is the projected value of the China robotics CNC turning centers space by 2031?

The market projects the value to reach USD 813.7 million by 2031, up from USD 447.6 million in 2026, with a 12.7% CAGR from 2026 to 2031.

What is driving demand for robotic CNC turning systems in China?

The strongest demand factors are national robotics policy support, high industrial robot density, subsidy-backed equipment renewal, and rapid growth in NEV production.

Which machine type generates the most revenue in China?

Horizontal robotic turning centers led revenue with a 49.21% share in 2025, owing to their ability to handle high-volume rotational part machining and unattended loading.

Which robot type is growing fastest in CNC turning applications?

Collaborative robots are the fastest-growing robot type, with a projected 14.78% CAGR through 2031, as they reduce guarding requirements and reduce programming effort.

Which end-user group creates the largest demand base?

Automotive and commercial vehicles held the largest share at 32.80% in 2025, driven by broad demand for turned components across conventional and electric vehicle platforms.

What is the biggest competitive shift taking place in China?

The largest shift is the rise of domestic suppliers, which captured 57% of industrial robot installations in 2024, while competition is moving toward software, integration depth, and localization.

Page last updated on: