China Printed Circuit Board Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 50.57 Billion |

| Market Size (2026) | USD 53.73 Billion |

| Market Size (2031) | USD 71.47 Billion |

| Growth Rate (2026 - 2031) | 5.87% CAGR |

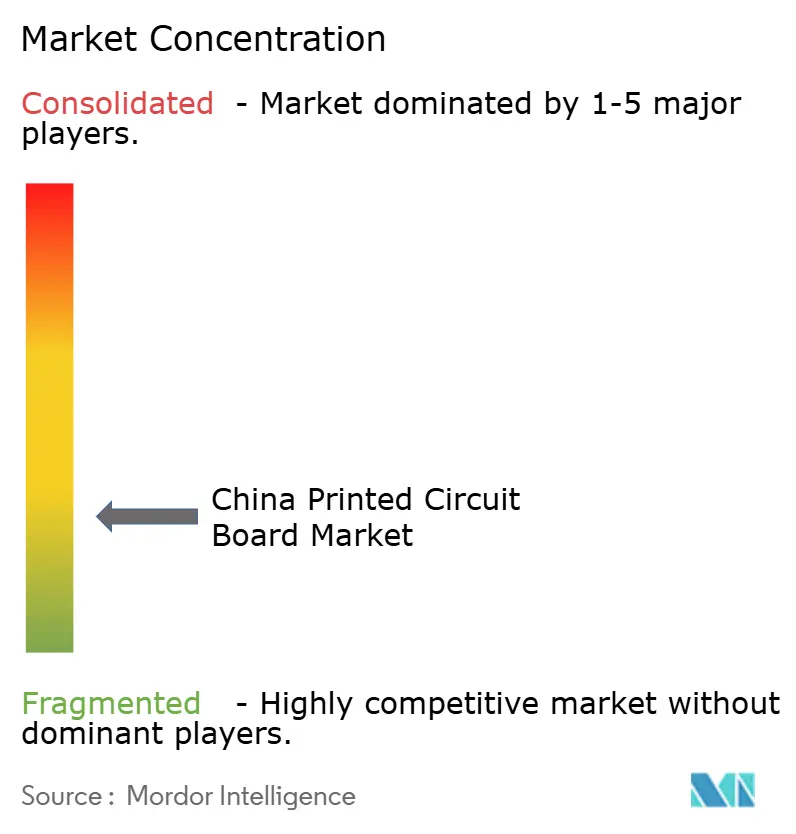

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Printed Circuit Board Market Analysis by Mordor Intelligence

The China printed circuit board market size is expected to grow from USD 50.57 billion in 2025 to USD 53.73 billion in 2026 and is forecast to reach USD 71.47 billion by 2031 at 5.87% CAGR over 2026-2031. Ongoing migration toward high-speed low-loss laminates, rising demand for IC substrates, and large-scale 5G and EV rollouts keep order books strong. Consumer electronics sales have leveled off, yet telecom and data-center operators continue to specify higher layer counts and tighter impedance control, lifting average selling prices. Meanwhile, automotive OEMs are shifting to 800-volt platforms, increasing copper thickness requirements, and pushing flexible-circuit adoption. Foreign players add capacity in Jiangsu and Chongqing, but local champions leverage policy incentives to deepen vertical integration and secure laminate supply.

Key Report Takeaways

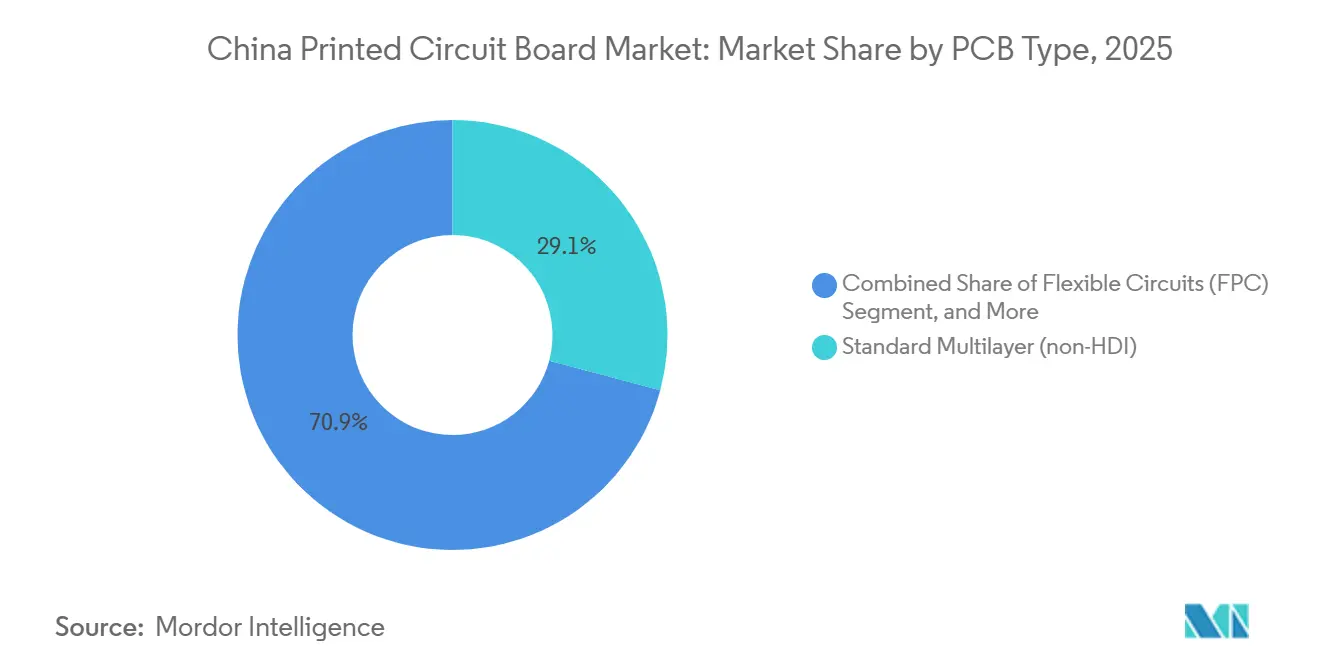

- By PCB type, standard multilayer boards captured 29.13% of the China printed circuit board market share in 2025, whereas flexible circuits are forecast to log the fastest 7.23% CAGR through 2031.

- By substrate material, glass epoxy FR-4 accounted for 43.21% of the China printed circuit board market share in 2025, while high-speed, low-loss laminates are set to expand at a 6.82% CAGR through 2031.

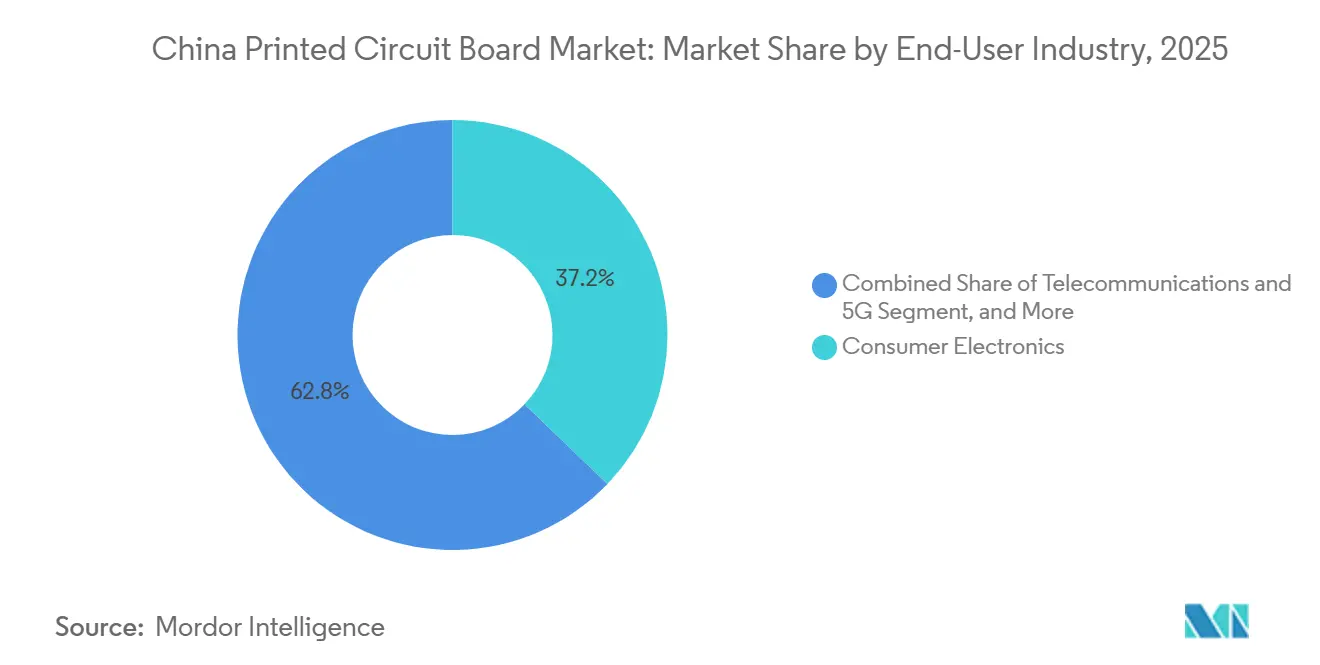

- By end-user industry, consumer electronics led with 37.18% of the China printed circuit board (PCB) market in 2025; telecommunications and 5G applications are poised for a 7.44% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China Printed Circuit Board Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in 5G Infrastructure Deployment | +1.2% | Tier-1 and Tier-2 cities nationwide | Medium term (2-4 years) |

| Rapid Growth of EV Manufacturing Demand | +1.4% | Guangdong, Jiangsu, Shanghai, Chongqing | Long term (≥ 4 years) |

| Government Incentives for Semiconductor Self-Sufficiency | +1.0% | Yangtze River Delta and Pearl River Delta | Long term (≥ 4 years) |

| Proliferation of Consumer IoT and Wearables | +0.8% | Shenzhen and Dongguan export clusters | Short term (≤ 2 years) |

| Localization of Hyperscale Data-Center Supply Chains | +0.9% | Beijing, Shanghai, Guangzhou, Chengdu, Guiyang | Medium term (2-4 years) |

| Adoption of 2.5D/3D Advanced IC Packaging | +1.1% | Jiangsu and Shanghai semiconductor zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge In 5G Infrastructure Deployment

China installed 507,000 new 5G macro and small cells in 2025, lifting the total live to 4.76 million. Each macro site integrates 15-20 multilayer boards with low-loss laminates to handle massive-MIMO antenna arrays. Operators extend sub-6 GHz coverage to rural counties while densifying millimeter-wave cells in urban cores, creating parallel demand for cost-efficient FR-4 and premium polyimide substrates. Open RAN adoption consolidates baseband and fronthaul functions onto a single high-layer-count board, saving tower real estate and installation time. Ministry-mandated electromagnetic-compatibility rules tighten impedance tolerances, spurring laser-direct imaging and sequential lamination upgrades.[1]Ministry of Industry and Information Technology, “China’s 5G Base Station Deployment Statistics,” miit.gov.cn

Rapid Growth Of EV Manufacturing Demand

Battery-electric and plug-in hybrid models comprised nearly half of domestic passenger-car sales in 2025.[2]China Association of Automobile Manufacturers, “New Energy Vehicle Production and Sales Data,” caam.org.cn Each EV incorporates up to 8 times more PCB content than its internal-combustion counterpart, covering the battery-management, traction inverter, and ADAS domains. Thermal-cycling and vibration resistance drive AEC-Q200 certified sourcing, favoring plants with automated optical inspection and X-ray laminography. The leap to 800-volt batteries raises copper foil weights to 6-10 ounces to handle 400-ampere peaks, a niche where Chinese fabricators hold cost advantages over offshore rivals. Flexible-circuit penetration is rising in digital cockpits and infotainment clusters where thin, bendable interconnects enable aggressive styling.

Government Incentives For Semiconductor Self-Sufficiency

Beijing earmarked USD 70 billion in tax breaks and equity funding to lift domestic IC self-reliance to 70% by 2025.[3]State Council of China, “Made in China 2025 Strategic Plan,” gov.cn Packaging houses scaling fan-out wafer-level and chiplet modules require organic substrates with line-and-space below 25 µm and near-silicon CTE. Grants finance pilot lines for through-silicon via, hybrid bonding, and high-density redistribution layers, expanding demand for build-up substrates and ultra-flat carrier panels. Material localization accelerates as reliance on imported Ajinomoto build-up film is viewed as a strategic vulnerability. These measures underpin double-digit growth in substrate shipments despite broader semiconductor cyclicality.

Adoption Of 2.5D/3D Advanced IC Packaging

Chinese OSATs are now ramping 2.5D interposers and 3D-stacked dies to extend Moore’s Law without new nodes. These packages require silicon or glass interposers with tens of thousands of micro-bumps at a pitch of less than 40 µm. Domestic PCB makers invest in deep-via etch and copper fill to bring interposer work in-house, lowering reliance on Taiwan suppliers. Fan-out panel-level packaging is gaining traction for mid-range ASICs, leveraging large substrates to boost die-per-panel economics. Advanced formats are expected to rise from 12% of China PCB revenue in 2025 to beyond 20% by 2031.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Copper Prices | -0.6% | Export hubs in Guangdong and Jiangsu | Short term (≤ 2 years) |

| Stricter Environmental Compliance Costs | -0.5% | Yangtze River Delta and Pearl River Delta | Medium term (2-4 years) |

| Bottlenecks in High-Speed Low-Loss Laminates | -0.4% | Global supply, domestic telecom and data-center lines | Medium term (2-4 years) |

| US Export Controls on High-End Equipment | -0.7% | Advanced substrate fabs nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility In Copper Prices

Copper touched USD 11,104 per ton in May 2024 then slid to USD 9,200 by December 2025, cutting gross margins by up to 300 basis points for board makers locked into quarterly price clauses. Metal accounts for up to one-third of multilayer material cost, and small fabricators seldom hedge futures because of working-capital limits. Quarterly price resets lag spot movements, amplifying margin swings. Concentrated refining capacity in Chile and Zambia exposes the chain to labor strikes and policy shifts. Diversifying foil sources and adopting lean inventory help but cannot fully absorb near-term price swings.

Stricter Environmental Compliance Costs

In 2025 provincial regulators lowered allowable VOC emissions to 50 mg/m³ and mandated closed-loop wastewater systems, forcing USD 2-5 million retrofits per plant. Temporary shutdowns hit smaller Dongguan and Huizhou shops, speeding consolidation as compliant peers expanded share. Extended producer responsibility pilots could add another 1-2% to costs by 2028, making ISO 14001 certification essential for global customer audits. Larger players pass some cost to customers through premium pricing tied to sustainability validations. Compliance spending therefore weighs on margins while raising barriers for new entrants.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By PCB Type: Flexible Circuits Emerge As High-Growth Format

Standard multilayer boards accounted for 29.13% of the China PCB market value in 2025, serving computing, industrial, and legacy telecom platforms where cost and drop-in reliability prevail. Rigid one- and two-sided boards remain staples in lighting modules and white goods. High-density interconnect designs are widely adopted in flagship smartphones thanks to any-layer via stacks that exceed 150 components per square inch. Flexible circuits, projected at a 7.23% CAGR through 2031, benefit from wearable, foldable, and EV cockpit programs that demand 100,000-plus bend cycles without trace cracking.

IC substrates, with their premium pricing for sub-25 µm lines and panel warpage under 50 µm, demonstrate the highest unit economics within the industry. Rigid-flex assemblies, increasingly adopted in aerospace and medical implants, command a 30-50% price premium compared to traditional separate rigid and flex sets. Additionally, metal-core boards cater to the LED lighting sector, while ceramic boards address the requirements of RF power modules, both serving profitable niche markets.

By Substrate Material: High-Speed Laminates Gain On Data-Center Upgrades

FR-4 maintained 43.21% of the China PCB market size in 2025 due to broad suitability across consumer and industrial products. High-speed low-loss materials are forecast to capture share at a 6.82% CAGR, propelled by 800 GbE switch backplanes that need Df ≤ 0.005 and Dk ≈ 3.0 at 56 GHz PAM4 signaling. Polyimide sheets dominate foldable and under-hood environments where 260 °C thermal stability and low moisture uptake are critical. Bismaleimide-triazine and build-up films underpin IC substrates supporting flip-chip BGA and fan-out wafer-level packages.

Domestic resin manufacturers are investing in halogen-free, low-loss blends to reduce reliance on Japanese imports. By 2025, lead times for premium laminates extended to 16-20 weeks due to capacity constraints, prompting OEMs to establish long-term supply agreements. Metal-core substrates remain critical for high-power LED drivers, while liquid-crystal polymer films are gradually being adopted in millimeter-wave antenna modules.

By End-User Industry: Telecom Surges Past Consumer Electronics

Consumer electronics accounted for 37.18% of the China printed circuit board market share in 2025, but handset shipments plateau and longer replacement cycles tempered their forward trajectory. Telecommunications and 5G infrastructure are projected to deliver the fastest 7.44% CAGR as operators roll out macro towers, small cells, and fiber CPEs that collectively consume a large amount of board area. Automotive orders rise on 800-volt battery introductions and ADAS penetration, driving demand for thick-copper and rigid-flex formats. Computing and cloud-AI clusters require massive motherboards and retimer backplanes, sustaining multi-year high-layer-count growth.

Industrial, medical, and defense segments keep steady momentum, emphasizing reliability over volume. Healthcare boards must meet IPC Class 3 standards, driving gold-plated contacts and conformal coatings. Aerospace demand commands premium pricing due to stringent qualification requirements and low run rates. Rail transit and smart-grid projects add incremental volume for specialized high-temperature boards.

Geography Analysis

China accounts for over half of global PCB output, with pronounced clustering in the Yangtze River Delta and the Pearl River Delta. Guangdong accounted for 28% of national shipments in 2025 through plants concentrated in Shenzhen, Huizhou, and Dongguan. Jiangsu is fast catching up, supported by investments from Kunshan, Suzhou, and Wuxi that pursue semiconductor substrate opportunities, and is anticipated to post a leading 6.3% CAGR through 2031. Shanghai’s preferential tax treatment sustains high-value HDI and substrate projects, while inland Chongqing and Chengdu attract expansion as coastal wages rise and logistics corridors improve.

Eight computing hubs, designated by the state, are now central to the localized demand for data-center backplanes. This move not only cuts down transit times from coast to inland but also aligns with the nation's dual-circulation strategy. As central inspections begin to standardize rules, the once pronounced regional disparities in environmental enforcement are diminishing. This shift is transitioning the competitive edge from lenient regulations to a mastery of technology.

Reliance on overseas high-speed laminates and build-up films remains a vulnerability amid geopolitical tensions. Domestic resin initiatives are scaling but still cover less than one-third of premium grades used in 56 GHz applications. Cross-border import lead times for high-speed laminates reached 16-20 weeks in 2025, encouraging OEMs to hold larger safety stocks in Guangdong and Jiangsu warehouses. Rail upgrades linking Sichuan to coastal ports shorten the delivery of copper foil and fiberglass cloth to inland plants by two days. Local governments now offer water-recycling grants covering 20% of capital outlay, helping western provinces attract greenfield builds. Earthquake-resilience standards in the southwest require thicker substrate cores, adding cost but improving reliability for aerospace programs anchored in Chengdu. Overall, regional diversification balances cost, policy, and logistics factors, enabling the China PCB market to keep production close to end demand while mitigating single-site risks.

Competitive Landscape

The five largest domestic manufacturers captured 35% of industry revenue in 2025, confirming moderate fragmentation. Shennan Circuits leads in HDI, flexible, and IC substrate production, supported by in-house copper-foil rolling and laminate synthesis. WUS Printed Circuit, Suntak Technology, and Kinwong Electronic concentrate on consumer and telecom HDI while boosting auto-grade output to meet AEC-Q200 demand. Dongshan Precision reinforced material security by acquiring a majority stake in a high-speed laminate mill, illustrating the shift toward upstream control. Foreign incumbents, including Unimicron, AT&S, and TTM Technologies, have expanded their plants in Chongqing, Kunshan, and Suzhou to serve multinational OEMs, yet rising wages and tighter audits are eroding their early cost advantages.

Investment now targets advanced carrier formats where gross margins top 25%. Factories install laser direct imaging, automated optical inspection, and sequential lamination lines to sustain 15 µm trace widths at volume scale. Specialist entrants in rigid-flex for wearables and ultra-thin substrates for chiplet assemblies bundle design assistance with rapid prototyping, compressing customer development cycles. Collaboration with OSATs and resin vendors is critical to co-engineer fan-out panel-level substrates that balance low warpage with fine redistribution layers.

Producers also court EV makers by integrating thick-copper and high-voltage process flows and by securing multi-year supply contracts that lengthen customer lock-in. Automotive qualification cycles raise switching costs, improving revenue visibility for certified plants. Strategic equity in laminate or copper-foil suppliers hedges raw-material volatility and guarantees feedstock priority. Environmental compliance spending accelerates consolidation because smaller shops struggle to fund scrubbers and closed-loop wastewater systems, allowing top-quartile players to widen share. These dynamics point to a gradually rising concentration without an imminent shift to oligopoly.

China Printed Circuit Board Industry Leaders

Shenzhen Shennan Circuits Co., Ltd.

WUS Printed Circuit Co., Ltd.

Suntak Technology Co., Ltd.

Victory Giant Technology Co., Ltd.

Shenzhen Kinwong Electronic Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Shennan Circuits announced a CNY 3.2 billion (USD 450 million) IC substrate plant in Wuxi targeting 2027 start-up.

- December 2025: AT and S expanded Chongqing capacity by 30% with a CNY 1.8 billion (USD 250 million) spend.

- November 2025: Unimicron partnered with a Chinese automaker to co-develop thick-copper boards for 800-volt EVs, with shipments slated for mid-2026.

- October 2025: WUS Printed Circuit added 1.2 million m² of HDI output in Huizhou through a CNY 2.5 billion (USD 350 million) build-out.

China Printed Circuit Board Market Report Scope

The China Printed Circuit Board Market is Segmented by PCB Type (Standard Multilayer (non-HDI), Rigid 1-2 Sided, High-Density Interconnect (HDI), Flexible Circuits (FPC), IC Substrates (Package Substrates), Rigid-Flex, Other PCB Types), Substrate Material (Glass Epoxy (FR-4), High-Speed Low-Loss, Polyimide (PI), Packaging Resins (BT / ABF), Other Substrate Materials), and End-user Industry (Consumer Electronics, Computing and Data Centers, Telecommunications and 5G, Automotive and EV, Industrial and Power, Healthcare / Medical, Aerospace and Defense, Other End-user Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Standard Multilayer (non-HDI) |

| Rigid 1-2 Sided |

| High-Density Interconnect (HDI) |

| Flexible Circuits (FPC) |

| IC Substrates (Package Substrates) |

| Rigid-Flex |

| Other PCB Types |

| Glass Epoxy (FR-4) |

| High-Speed / Low-Loss |

| Polyimide (PI) |

| Packaging Resins (BT / ABF) |

| Other Substrate Materials |

| Consumer Electronics |

| Computing and Data Centers |

| Telecommunications and 5G |

| Automotive and EV |

| Industrial and Power |

| Healthcare / Medical |

| Aerospace and Defense |

| Other End-user Industries |

| By PCB Type | Standard Multilayer (non-HDI) |

| Rigid 1-2 Sided | |

| High-Density Interconnect (HDI) | |

| Flexible Circuits (FPC) | |

| IC Substrates (Package Substrates) | |

| Rigid-Flex | |

| Other PCB Types | |

| By Substrate Material | Glass Epoxy (FR-4) |

| High-Speed / Low-Loss | |

| Polyimide (PI) | |

| Packaging Resins (BT / ABF) | |

| Other Substrate Materials | |

| By End-user Industry | Consumer Electronics |

| Computing and Data Centers | |

| Telecommunications and 5G | |

| Automotive and EV | |

| Industrial and Power | |

| Healthcare / Medical | |

| Aerospace and Defense | |

| Other End-user Industries |

Key Questions Answered in the Report

What was the China PCB market size in 2026?

It reached USD 53.73 billion, with a forecast to hit USD 71.47 billion by 2031.

Which PCB type will grow fastest through 2031?

Flexible circuits are projected at a 7.23% CAGR as smartphone, wearable, and EV cockpit designs demand bendable interconnects.

How large is telecom demand in the China PCB market?

Telecommunications and 5G applications are set to post a 7.44% CAGR, making them the fastest-growing end-user segment.

Which province is expanding capacity fastest?

Jiangsu is anticipated to record a 6.3% CAGR, driven by investments in Kunshan, Suzhou, and Wuxi substrate plants.

What is the main raw-material risk for PCB fabricators?

Copper price volatility can trim margins by up to 300 basis points during sharp rallies, given copper’s 25-35% share of board material cost.

Who leads the domestic high-density interconnect segment?

Shennan Circuits commands the lead, operating HDI, flex, and IC substrate lines across Shenzhen, Wuxi, and Nantong campuses.

Page last updated on: