China HBM Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

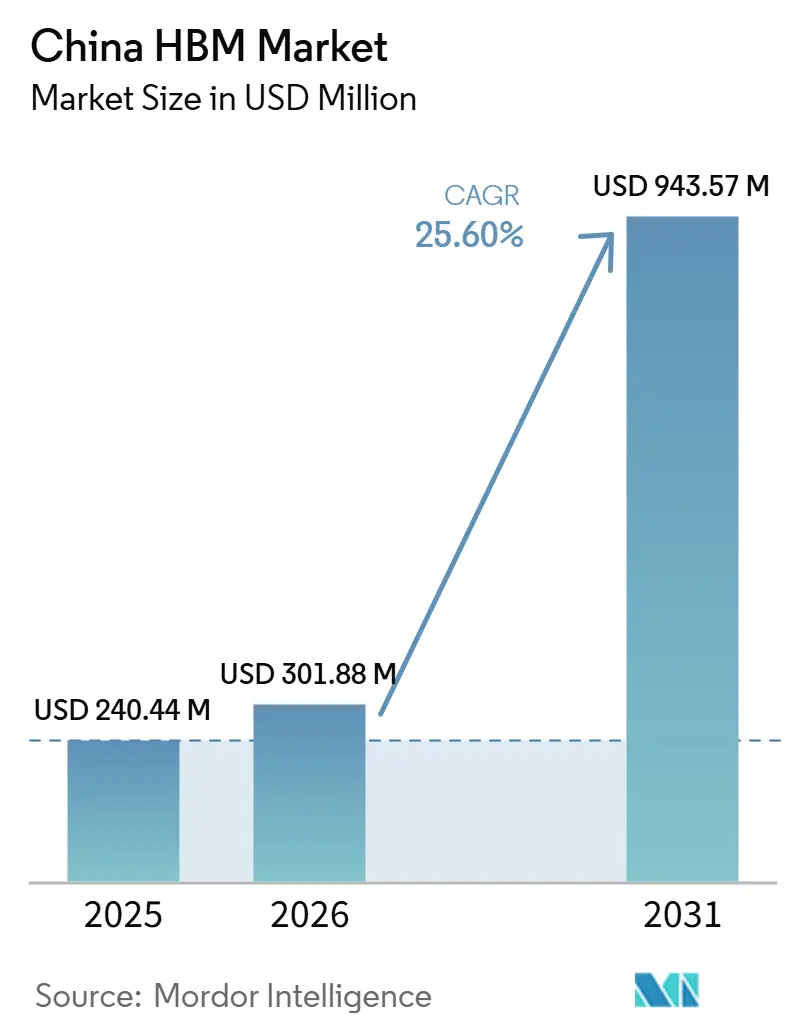

| Base Year Market Size (2025) | USD 240.44 Million |

| Market Size (2026) | USD 301.88 Million |

| Market Size (2031) | USD 943.57 Million |

| Growth Rate (2026 - 2031) | 25.60% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China HBM Market Analysis by Mordor Intelligence

The China HBM market size is projected to be USD 240.44 million in 2025, USD 301.88 million in 2026, and reach USD 943.57 million by 2031, growing at a CAGR of 25.60% from 2026 to 2031. The China HBM market is being shaped by AI compute demand that is increasingly focused on higher memory bandwidth, driving the need for denser, faster memory configurations across domestic accelerator programs. Export controls have made supply access more uncertain, so local production, packaging, and qualification efforts are moving from planning into execution. This has turned the China HBM market into a supply security story as much as a demand story, with investment decisions now tied closely to procurement continuity and policy alignment. Domestic packaging expansion is becoming a practical lever for near-term delivery, because packaging readiness will decide how quickly new HBM capacity can reach commercial scale. The result is a market where growth is supported not only by rising AI infrastructure needs, but also by the push to reduce dependence on foreign supply at every critical step of the value chain.

Key Report Takeaways

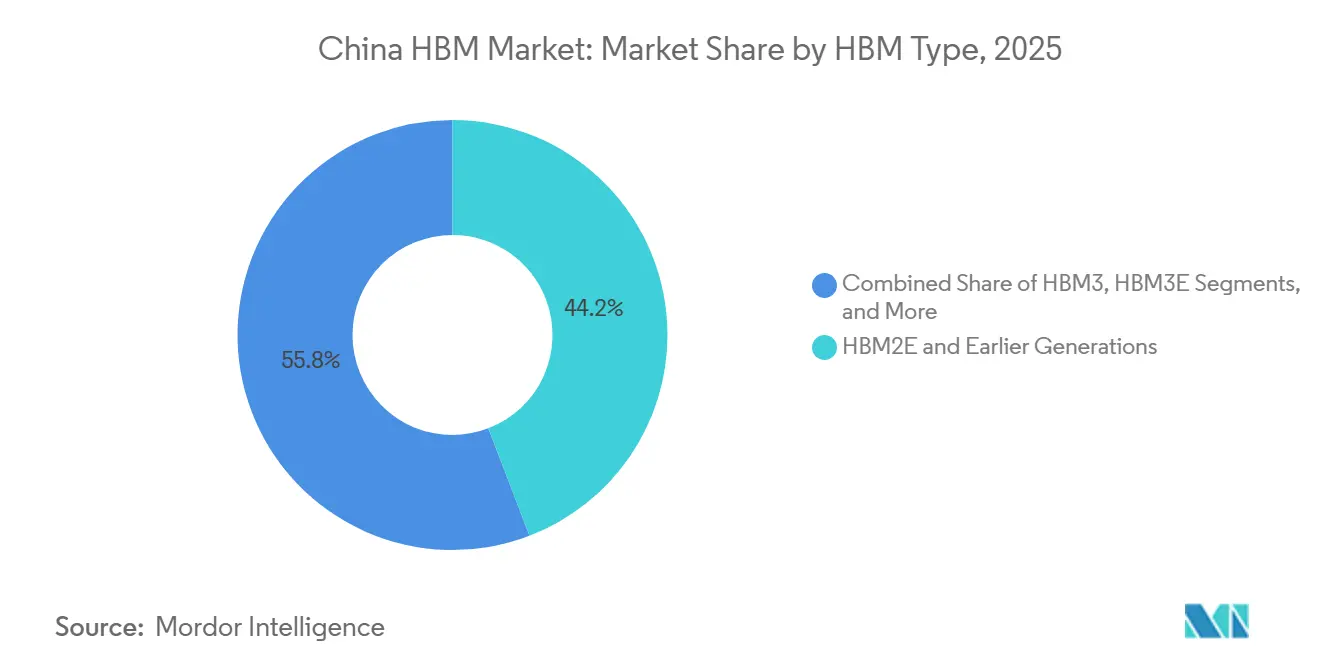

- By HBM type, HBM2E and earlier generations held 44.17% of the China HBM market in 2025, while HBM4 is projected to expand at a 26.57% CAGR through 2031.

- By technology node, advanced nodes below 1Z accounted for 49.63% of the China HBM market in 2025, and this category is expected to grow at a 26.32% CAGR through 2031.

- By end use industry, cloud service providers and hyperscalers held 51.77% of the China HBM market share in 2025, while internet platforms and AI model developers are projected to expand at a 26.78% CAGR through 2031.

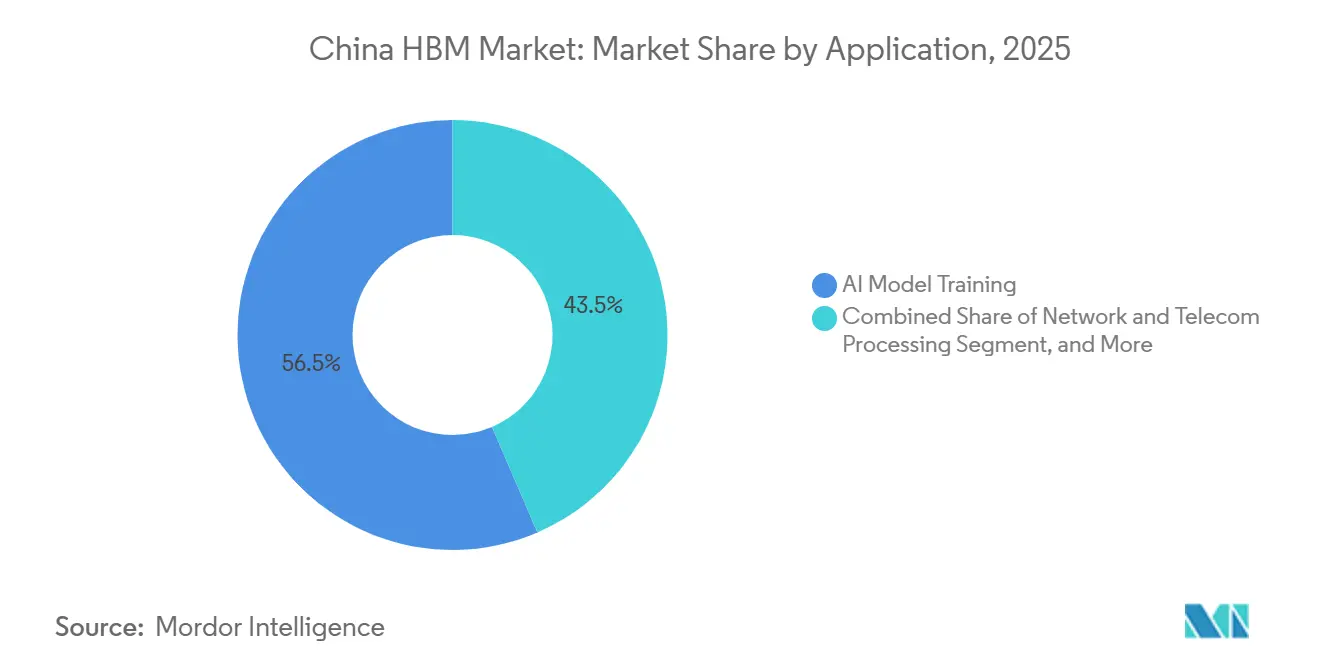

- By application, AI model training accounted for 56.46% share of the China HBM market size in 2025, while AI model inference is projected to grow at a 26.79% CAGR through 2031.

- By packaging type, 2.5D interposer-based packaging captured 84.69% of the China HBM market in 2025, while fan-out advanced packaging is expected to grow at a at 26.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China HBM Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Export-Control-Induced Import Substitution | +6.5% | China, concentrated in the Yangtze River Delta and the Greater Bay Area AI chip clusters | Short term (≤ 2 years) |

| Accelerating AI Server and GPU Memory Density Requirements | +5.5% | Global demand, with China as a major uptake center for domestic AI accelerators | Long term (≥ 4 years) |

| China-Specific AI Compute Localization Programs | +4.8% | China, with early procurement effects in Beijing, Shanghai, Shenzhen, and Hangzhou | Medium term (2-4 years) |

| Rapid Expansion of Domestic Advanced Packaging Capacity | +3.2% | Yangtze River Delta, with spillover into Chengdu and Wuhan | Medium term (2-4 years) |

| Hyperscale Cloud Procurement of Domestic Memory | +2.4% | Beijing, Shanghai, Hangzhou, and Shenzhen data center corridors | Short term (≤ 2 years) |

| Hybrid Bonding and TSV Ecosystem Catch-Up | +1.8% | Shanghai, Wuhan, and Hefei | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Export-Control-Induced Import Substitution Reshapes Procurement Logic

US export controls remain the most disruptive force in the China HBM market because they changed both sourcing options and investment timing. In December 2024, the Bureau of Industry and Security expanded controls to cover HBM, DRAM, and advanced packaging semiconductor manufacturing equipment, which sharply narrowed access to HBM3 and higher products for Chinese buyers.[1]Bureau of Industry and Security, “Policy Statement on Controls That May Apply to Advanced Computing Integrated Circuits and Other Commodities Used to Train AI Models,” BIS, bis.gov That shift pushed Chinese AI chip companies to rely on previously secured inventory while advancing domestic qualification programs much faster than a typical product cycle would allow. The issue is not only industrial policy, because delayed HBM supply directly limits the shipment pace of domestic AI accelerators and slows the deployment of new computing clusters. The China HBM market, therefore, moved from a cost-and-performance discussion toward a supply-assurance model in which local capacity carries strategic value even before it reaches full-scale economics. CXMT’s June 2026 IPO approval also showed how quickly capital formation followed this change in trade policy, with the new funding directed toward capacity and HBM commercialization.

Accelerating AI Server and GPU Memory Density Requirements Set the Demand Baseline

The demand floor for the China HBM market is rising because each new AI accelerator generation requires more capacity and more bandwidth per device. Huawei’s Ascend 950PR, launched in March 2026, integrated 112 GB of HBM and delivered 1.6 TB/s of memory bandwidth, which marked a major increase over the earlier platform. The next step was already visible in the Ascend 950DT roadmap, which moved toward 144 GB of HBM and 4 TB/s of bandwidth for more demanding training and inference tasks. This matters because memory requirements do not increase linearly, and each chip generation increases the strain on local HBM availability, packaging readiness, and validation cycles. The China HBM market is therefore being boosted by a technical requirement that is difficult to defer, especially as domestic accelerator programs aim to match global performance benchmarks. Higher memory density has also widened the importance of packaging and thermal integration, so demand growth now reaches well beyond memory die production alone.

China-Specific AI Compute Localization Programs Create Captive Demand

The localization policy has made the China HBM market more predictable on the demand side, as public and strategic projects are now more closely tied to domestic chip procurement. Reuters reported in November 2025 that new state-funded data center projects were directed to use domestically made AI chips, and even partially completed projects were asked to remove foreign chip plans if they remained below the completion threshold. That rule matters for HBM because local AI chip purchases pull memory demand into the same domestic procurement channel. The policy effect is larger than a simple substitution shift, because it creates a built-in order stream that is less exposed to short-term pricing changes and more tied to compliance and national capacity building. The China HBM market gains unusual visibility from this structure, especially in segments connected to government, research, and state-backed infrastructure. It also shortens the commercial distance between a qualified domestic memory supplier and a confirmed downstream customer.

Rapid Expansion of Domestic Advanced Packaging Capacity Removes a Critical Bottleneck

Advanced packaging is becoming one of the clearest near-term growth drivers for the China HBM market, as it sits between pilot output and commercial delivery. In June 2026, JCET announced a CNY 7.8 billion (USD 1.15 billion) investment in an advanced packaging and testing facility in Shanghai’s Lingang Special Area, aimed at meeting demand for HPC, HBM, and chiplet integration. In January 2026, Tongfu Microelectronics also announced a CNY 4.4 billion (USD 620 million) fundraising plan to expand packaging and testing capacity for memory chips and computing applications. These moves matter because packaging remains the practical bottleneck between domestic HBM design progress and volume shipment capability. The concentration of these projects in the Yangtze River Delta also improves access to tooling, engineering talent, and customer coordination, thereby shortening integration timelines. For the China HBM market, this means packaging investment is not just about supporting supply; it is about improving the odds that supply can achieve qualified, repeatable output.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Yield Losses in High-Stack HBM Manufacturing | -3.5% | China, most acute at Hefei and Shanghai-linked HBM production and packaging sites | Medium term (2-4 years) |

| Limited Access to Leading-Edge EDA and Process Tools | -2.8% | China, with the strongest effect in Shanghai, Hefei, and Shenzhen, advanced node programs | Long term (≥ 4 years) |

| Tight Qualification Cycles for AI Accelerator Customers | -1.5% | China, centered in Shenzhen and Shanghai, AI chip design hubs | Short term (≤ 2 years) |

| Dependence on Imported Advanced Materials and Substrates | -0.9% | China, especially eastern coastal supply chains tied to interposer substrates | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Yield Losses in High-Stack HBM Manufacturing Constrain Volume Scale-Up

Yield remains a serious restraint because high-stack HBM production becomes harder with every additional layer and every tighter bonding tolerance. The original draft noted that even when per-layer performance is strong, cumulative stack yield can fall meaningfully before packaging is complete, slowing and increasing the cost of scale-up. This issue is broader than a single process step because it touches through-silicon via formation, bonding consistency, thermal control, test coverage, and final package reliability. The China HBM market will therefore remain sensitive to production maturity until domestic suppliers can stabilize commercially viable yields across engineering and early mass production runs. Export restrictions also matter here because they reduce access to foreign tools, calibration support, and yield-improvement know-how that would normally help shorten the ramp period.

Limited Access to Leading-Edge EDA and Process Tools Imposes a Structural Ceiling

Tool access is a long-term restraint because advanced HBM depends on process and design infrastructure that China still cannot fully replace. The December 2024 US control package added deep ultraviolet immersion lithography and related techniques to the broader set of restrictions affecting advanced semiconductor production for China. Separate BIS guidance in 2025 also showed that access to EDA tools could become uncertain with limited notice, making planning even more fragile, where full bans were not permanent. Domestic equipment suppliers are progressing in selected process steps, but the gap remains widest in the most advanced lithography and design environments that support sub-20nm DRAM development. For the China HBM market, this means local supply can improve meaningfully in packaging and selected memory stages while still facing a slower path in generation advancement and quality parity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By HBM Type: Legacy Supply Still Leads, but the Technology Mix Is Moving Forward

HBM2E and earlier generations accounted for 44.17% of the China HBM market in 2025, indicating that the installed demand base still relied on legacy supply during a period of restricted access to newer imported products. That leading share did not reflect a settled customer preference, because domestic AI programs increasingly require higher bandwidth classes that older HBM cannot support for long. The segment remained important because pre-control procurement had created a temporary inventory cushion, which gave buyers a short window to sustain deployments while local alternatives moved through qualification. In the China HBM industry, this legacy tier therefore acted as a bridge rather than a stable end state. HBM3 and HBM3E sit in the middle of that transition, because they connect current deployment needs with the next stage of domestic production readiness.

HBM4 is projected to expand at a 26.57% CAGR through 2031, which makes it the clearest marker of where long-term product demand is heading. That growth reflects procurement plans that are already looking beyond present supply constraints and toward performance levels needed by later accelerator generations. The segment is still early in commercial terms, but its growth signal shows that Chinese buyers are not planning around yesterday’s specification set. HBM4E and later generations remain smaller today, yet the direction of demand suggests that once tooling, yield, and packaging barriers ease, these tiers could gain momentum quickly. The China HBM market is therefore being pulled forward by future performance requirements even while present shipments still lean on older memory families.

By Technology Node: Advanced Node Consolidation Mirrors AI Accelerator Priorities

Advanced nodes below 1Z accounted for 49.63% of the China HBM market size in 2025, which confirms that the leading demand pool is already concentrated around the densest die configurations available. This node category also represented the fastest-moving part of the technology mix, because domestic accelerators need higher density and tighter performance envelopes to remain viable in training and inference deployments. That leaves 1Z and 1Y nodes with an important but narrower role, mainly in workloads where cost, availability, and compatibility still matter more than absolute bandwidth. Older 1X and above nodes continue to serve legacy and less demanding use cases, but they are losing relative weight as AI-centered deployments become more dominant. The China HBM market is therefore consolidating around advanced nodes for structural reasons tied to chip architecture, not only for marketing or roadmap reasons.

This shift also explains why the discussion of technology nodes cannot be separated from export controls and tool access. The draft linked advanced node progression to the same process capabilities that remain exposed to lithography and EDA constraints, meaning supply improvements will not advance evenly across all node tiers. In practical terms, leading node demand can stay strong even when local supply remains tight, because customer requirements keep moving upward regardless of domestic manufacturing readiness. The China HBM industry is therefore likely to show a persistent gap between the most attractive node segment and the easiest node segment to supply. That imbalance is one reason the advanced-node tier held the lead in 2025 while also shaping the strongest pull on future investment.

By End Use Industry: Hyperscalers Hold the Base, While Platform Developers Extend the Demand Curve

Cloud service providers and hyperscalers accounted for 51.77% of the China HBM market in 2025, reflecting the scale and capital intensity of centralized AI infrastructure buildouts. This segment led because large cloud operators can commit early to accelerator clusters, absorb qualification complexity, and create visibility into demand for suppliers across memory, packaging, and system integration. Their role is especially important when local HBM supply remains constrained, because hyperscalers are often the first buyers able to structure around partial availability and phased deployment. That gave the China HBM market a strong anchor in 2025, even as the broader ecosystem remained uneven in supply readiness. It also explains why procurement concentration stayed high at the top end of the customer base.

Internet platforms and AI model developers are projected to expand at a 26.78% CAGR through 2031, suggesting a broader commercial use beyond centralized training clusters. Reuters reported in March 2026 that ByteDance and Alibaba planned orders for Huawei’s new AI chips after customer testing, which supports the view that demand is broadening into application-led deployment environments. This category grows faster because platform operators are building customer-facing model services that need high-bandwidth memory in distributed inference setups, not only in core training centers. Government, defense, research, academic institutions, enterprise data centers, and telecom operators still matter, but their role is steadier and more policy or use-case specific. The China HBM market is therefore likely to keep its volume base in hyperscale procurement while its next growth wave spreads across service platforms and model deployment ecosystems.

By Application: Training Led Current Demand, While Inference Is Expanding the Use Case

AI model training accounted for 56.46% of the China HBM market in 2025, underscoring the continued concentration of capital spending in foundation model development and core compute clusters. Training led because it requires large, tightly coupled accelerator fleets that consume substantial HBM per card and keep those resources active for long periods. Huawei’s product roadmap reinforced this pattern, with higher-capacity memory designs built for increasingly demanding model workloads.[2]Huawei Technologies, “Ascend 950DT Deployment Update,” Huawei Technologies, huawei.com This made training the primary demand center for the China HBM market in 2025, even though supply remained tight. It also kept purchasing concentrated among a smaller group of well-funded organizations.

AI model inference is projected to grow at a 26.79% CAGR through 2031, which makes it the fastest-expanding application in the forecast period. The growth case is tied to commercialization, because once trained models move into live services, demand shifts from isolated training runs to ongoing, geographically broader deployment. That does not eliminate the importance of HPC, scientific computing, professional graphics, rendering, visualization, network processing, and telecom processing, but it changes the center of growth. Inference creates a wider operational footprint for HBM, especially when services must run continuously and respond in real time. The China HBM market is therefore moving from a training-led demand profile toward a more balanced mix where inference plays a larger commercial role each year.

By Packaging Type: 2.5D Dominates Today, While Fan-Out Represents a Strategic Alternative

2.5D interposer-based packaging captured 84.69% of the China HBM market in 2025, which made it the clear operating standard for commercial deployments. That concentration reflects technical necessity more than vendor preference, because leading HBM architectures still rely on short interconnect paths between memory stacks and logic dies to deliver very high bandwidth. As a result, 2.5D packaging remained central to the China HBM market while domestic suppliers worked to expand qualified capacity and reduce dependence on external benchmarks. The segment’s lead also shows why packaging remains such a sensitive bottleneck, since product readiness depends on proven assembly and testing at scale. In the China HBM industry, control over 2.5D capability is moving closer to control over actual market access.

Fan-out advanced packaging is expected to record a 26.12% CAGR through 2031, which signals that Chinese suppliers are actively building an alternative route where interposer dependency is harder to sustain. This growth does not mean fan-out will quickly displace 2.5D, because the performance demands of high-end accelerators still favor established architectures. It shows that domestic players want a second packaging path that can support more secure, more flexible supply in selected deployments. 3D stacking also remains strategically important, especially for later HBM generations that will depend on more advanced bonding approaches. The China HBM market is therefore likely to keep 2.5D at the center of present demand while using fan-out and deeper stacking programs to reduce future structural dependence.

Geography Analysis

The China HBM market is geographically concentrated by function, with the Yangtze River Delta acting as the leading production and packaging corridor. Within the country, this corridor links Hefei’s memory manufacturing base with Shanghai and Jiangsu's packaging capacity, which gives it the most integrated industrial position. The China HBM market share for this cluster is not stated in the draft, but its strategic role is clear, as major fabrication, back-end, and packaging investments continue to cluster in the same region. This concentration matters because the domestic supply chain still needs tight coordination between memory output, advanced packaging, testing, and accelerator integration.

Shanghai gained additional weight in June 2026 when JCET announced its CNY 7.8 billion (USD 1.15 billion) advanced packaging and testing facility in Lingang, designed for HPC, HBM, and chiplet demand.[3]South China Morning Post Staff, “China’s JCET to Build New Plant in Shanghai to Expand Advanced Chip Packaging,” South China Morning Post, scmp.com Hefei remains important because it anchors CXMT’s DRAM base and sits close to the broader supplier network needed for HBM scaling. Wuhan adds a specialized role through hybrid bonding work tied to future high-stack packaging pathways, giving it strategic relevance even without the same scale today. Shenzhen and the Greater Bay Area contribute more on the demand and design side, as they host major AI chip design activity and downstream system integration. The China HBM market therefore does not spread evenly across the country, and instead follows a pattern where production, packaging, and application demand gather in a few linked hubs.

Policy direction reinforces this concentration. State-backed localization rules continue to favor domestic procurement channels, which means regional clusters that can deliver memory, packaging, and accelerator integration will gain faster commercial traction than stand-alone facilities. The China HBM market also stands apart because it combines strong local demand with a supply base that is still maturing under external constraints. That combination supports continued investment in the same core regions rather than a broad and fragmented geographic spread. As domestic capacity improves, these hubs are likely to capture an even larger operational role in China’s HBM value chain.

Competitive Landscape

The China HBM market remains highly concentrated on the supply side, as a small group of foreign memory manufacturers still shapes effective availability in 2025. Samsung and SK Hynix remained central to higher-generation HBM supply, while Micron’s role remained much smaller due to the combined effects of US controls and earlier Chinese restrictions on its products in critical infrastructure settings. This left the China HBM market with a split structure, where foreign suppliers dominated near-term availability, and domestic firms carried most of the future scale-up narrative. That imbalance explains why competitive positioning is still defined as much by qualification timing and policy fit as by standard cost competition.

CXMT is the most important domestic challenger because it sits at the intersection of China’s supply security objective and commercial memory scaling. Xinhua reported in June 2026 that the company secured approval for a CNY 29.5 billion (USD 4.33 billion) STAR Market IPO, with funds directed toward DRAM expansion and HBM mass-production infrastructure.[4]China Securities Regulatory Commission, “China Greenlights IPO Registration of Major Memory Chipmaker CXMT,” Xinhua, english.news.cn JCET and Tongfu Microelectronics are shaping the market from the packaging side, where qualification speed and capacity depth can decide how quickly domestic HBM reaches customers. JCET’s Shanghai facility announcement in June 2026 was one of the clearest strategic moves in the China HBM market because it directly expanded the local route for advanced packaging delivery. Tongfu’s January 2026 fundraising plan was another important move, since it strengthened the supporting layer of packaging and testing needed for memory and computing products.

Huawei is also changing the competitive structure because it is moving beyond the role of a buyer and deeper into memory architecture design. Its March 2026 launch of the Ascend 950PR with self-developed HBM architecture showed that Chinese AI chip vendors are trying to shape the memory stack more directly, not only select from external supply. Reuters also reported that ByteDance and Alibaba planned orders for Huawei’s new AI chip, which shows how quickly successful qualification can translate into ecosystem momentum. The China HBM market is therefore becoming more layered, but not yet broadly fragmented, because strategic control still sits with a limited set of firms across memory supply, packaging execution, and AI accelerator design.

China HBM Industry Leaders

Samsung Electronics Co., Ltd.

SK hynix Inc.

Micron Technology, Inc.

Semiconductor Manufacturing International Corporation

Tencent Holdings Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: JCET announced plans to invest CNY 7.8 billion (USD 1.15 billion) to construct an advanced packaging and testing facility in Shanghai's Lingang Special Area, with Phase 1 construction targeting completion in the second half of 2028. The facility is purpose-built to meet the HPC, HBM, and chiplet-based heterogeneous integration demands of domestic AI chip customers.

- June 2026: China Securities Regulatory Commission approved CXMT's STAR Market IPO registration. The company plans to raise CNY 29.5 billion (USD 4.33 billion), which would be the second-largest IPO in STAR Market history and the largest A-share IPO of 2026, with proceeds earmarked for DRAM capacity expansion and HBM mass-production infrastructure.

- March 2026: Huawei launched the Atlas 350 accelerator card based on the Ascend 950PR at its China Partner Conference 2026, featuring HiBL 1.0, the company's first self-developed HBM with 112 GB capacity and 1.6 TB/s bandwidth, the first domestic AI chip to integrate internally designed HBM and claiming 2.8x the FP4 compute performance of NVIDIA's H20.

- January 2026: Tongfu Microelectronics announced plans to raise CNY 4.4 billion (USD 620 million) via private placement to expand packaging and testing capacity for memory chips and computing applications, reinforcing its position as China's second-largest OSAT provider and deepening its HBM-related packaging capabilities.

China HBM Market Report Scope

The China HBM market refers to the demand, supply, and adoption of high-bandwidth memory (HBM) solutions in China. The market scope includes HBM products and related applications across key end-user industries, such as artificial intelligence, data centers, high-performance computing, graphics processing, and advanced semiconductor systems.

The China HBM Market Report is segmented by HBM type (HBM2E and Earlier Generations, HBM3, HBM3E, HBM4, and HBM4E), Technology Node (1X and above Legacy Nodes, 1Y Node, 1Z Node, and Advanced Nodes below 1Z), End Use Industry (Cloud Service Providers and Hyperscalers, Internet Platforms and AI Model Developers, Government, Defense, Research, and Academic Institutions, Enterprise Data Centers, Telecommunications Operators and Network Equipment Providers, and Other End Use Industries), Application (AI Model Training, AI Model Inference, HPC and Scientific Computing, Professional Graphics, Rendering, and Visualization, Network and Telecom Processing, and Other Applications) and Packaging Type (2.5D Interposer-Based Packaging, Fan-Out Advanced Packaging, and Hybrid/Next-Generation Advanced Packaging). The Market Forecasts are Provided in Terms of Value (USD).

| HBM2E and Earlier Generations |

| HBM3 |

| HBM3E |

| HBM4 |

| HBM4E |

| 1X and above Legacy Nodes |

| 1Y Node |

| 1Z Node |

| Advanced Nodes below 1Z |

| Cloud Service Providers and Hyperscalers |

| Internet Platforms and AI Model Developers |

| Government, Defense, Research, and Academic Institutions |

| Enterprise Data Centers |

| Telecommunications Operators and Network Equipment Providers |

| Other End Use Industries |

| AI Model Training |

| AI Model Inference |

| HPC and Scientific Computing |

| Professional Graphics, Rendering, and Visualization |

| Network and Telecom Processing |

| Other Applications |

| 2.5D Interposer-Based Packaging |

| 3D Stacking |

| Fan-Out Advanced Packaging |

| By HBM Type | HBM2E and Earlier Generations |

| HBM3 | |

| HBM3E | |

| HBM4 | |

| HBM4E | |

| By Technology Node | 1X and above Legacy Nodes |

| 1Y Node | |

| 1Z Node | |

| Advanced Nodes below 1Z | |

| By End Use Industry | Cloud Service Providers and Hyperscalers |

| Internet Platforms and AI Model Developers | |

| Government, Defense, Research, and Academic Institutions | |

| Enterprise Data Centers | |

| Telecommunications Operators and Network Equipment Providers | |

| Other End Use Industries | |

| By Application | AI Model Training |

| AI Model Inference | |

| HPC and Scientific Computing | |

| Professional Graphics, Rendering, and Visualization | |

| Network and Telecom Processing | |

| Other Applications | |

| By Packaging Type | 2.5D Interposer-Based Packaging |

| 3D Stacking | |

| Fan-Out Advanced Packaging |

Key Questions Answered in the Report

What is the current and forecast size of the China HBM space?

The China HBM market size was USD 240.44 million in 2025, reached USD 301.88 million in 2026, and is forecast to reach USD 943.57 million by 2031 at a 25.60% CAGR.

Which HBM type leads demand in China today?

HBM2E and earlier generations led in 2025 with a 44.17% share, mainly because current deployments still relied on available legacy supply during the transition to newer memory classes.

Which application is growing fastest for HBM in China?

AI model inference is the fastest-growing application, with a projected 26.79% CAGR through 2031, as commercialization expands beyond centralized training clusters.

Why is advanced packaging so important for HBM growth in China?

Packaging is the step that turns memory output into usable commercial product, and 2.5D interposer-based packaging already held 84.69% of demand in 2025.

Which customer group drives the largest share of demand?

Cloud service providers and hyperscalers led with 51.77% of end-use demand in 2025, reflecting the large capital needs of AI training and infrastructure buildouts.

What is the main competitive shift to watch over the next few years?

The key shift is the move from foreign-led effective supply toward a more domestic chain led by CXMT, JCET, Tongfu, and Huawei as memory, packaging, and accelerator design become more integrated.

Page last updated on: