China Frontline Worker Technology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

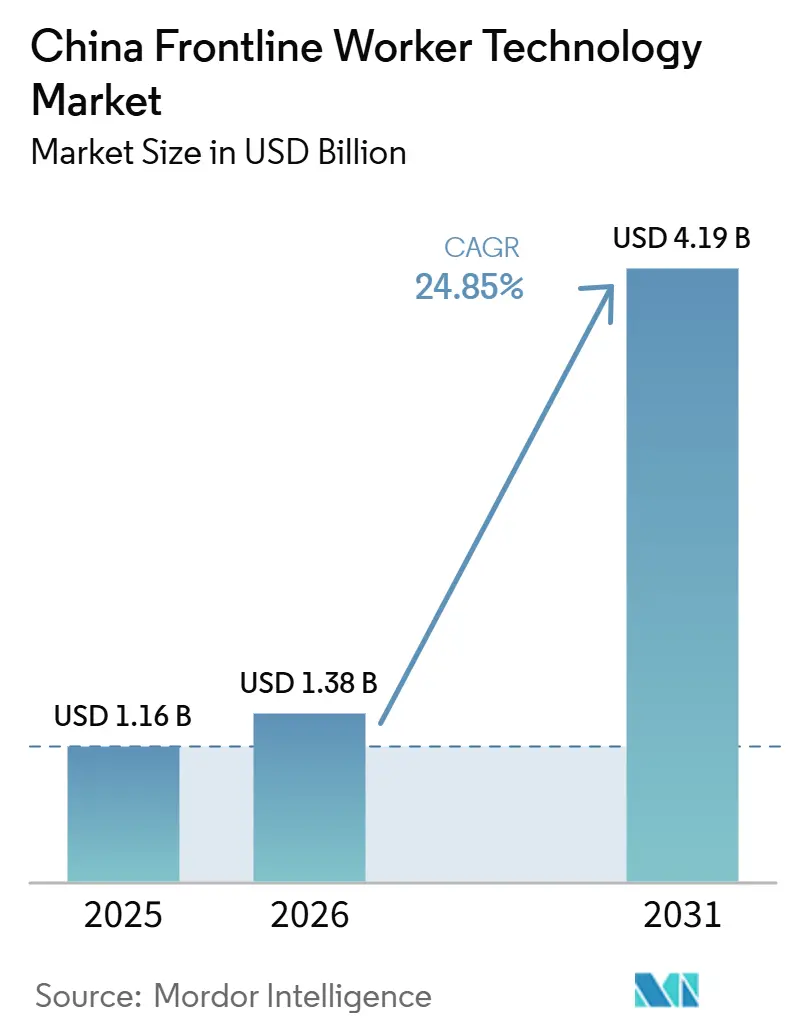

| Base Year Market Size (2025) | USD 1.16 Billion |

| Market Size (2026) | USD 1.38 Billion |

| Market Size (2031) | USD 4.19 Billion |

| Growth Rate (2026 - 2031) | 24.85% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Frontline Worker Technology Market Analysis by Mordor Intelligence

The China frontline worker technology market size is projected to be USD 1.16 billion in 2025, USD 1.38 billion in 2026, and reach USD 4.19 billion by 2031, growing at a CAGR of 24.85% from 2026 to 2031. Growth is being shaped by a tightening labor market, which is pushing employers to raise output through software, automation, and better workforce coordination rather than relying solely on headcount expansion. The policy setting also supports this shift, as industrial upgrading programs are pushing manufacturers, logistics operators, and healthcare systems toward digital tools that can schedule, train, monitor, and engage frontline staff at scale. AI adoption has moved beyond pilot use in China, and that shift is making workforce platforms more valuable because employers now expect real-time planning, predictive staffing, and better visibility into labor productivity. The vendor landscape is becoming more competitive as domestic providers bring locally adapted products, China-compliant cloud infrastructure, and tighter integration with enterprise systems already used by large employers. The next phase of the China frontline worker technology market is likely to be defined by faster SME adoption, stronger demand for compliant cloud deployment, and wider use of worker-facing tools that improve flexibility, retention, and day-to-day communication.

Key Report Takeaways

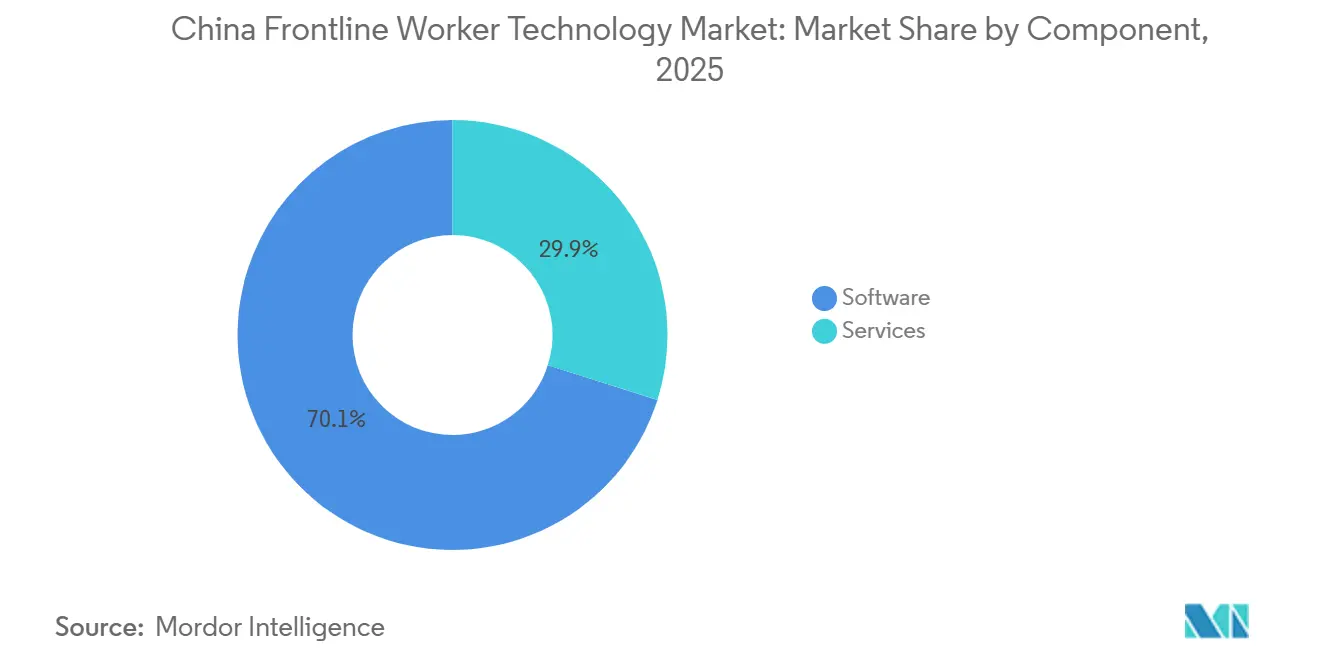

- By component, software accounted for 70.12% of the China frontline worker technology market size in 2025, while services are projected to expand at a 27.18% CAGR through 2031.

- By deployment, cloud-based deployment held 66.84% of the China frontline worker technology market share in 2025 and is projected to expand at a 28.26% CAGR through 2031.

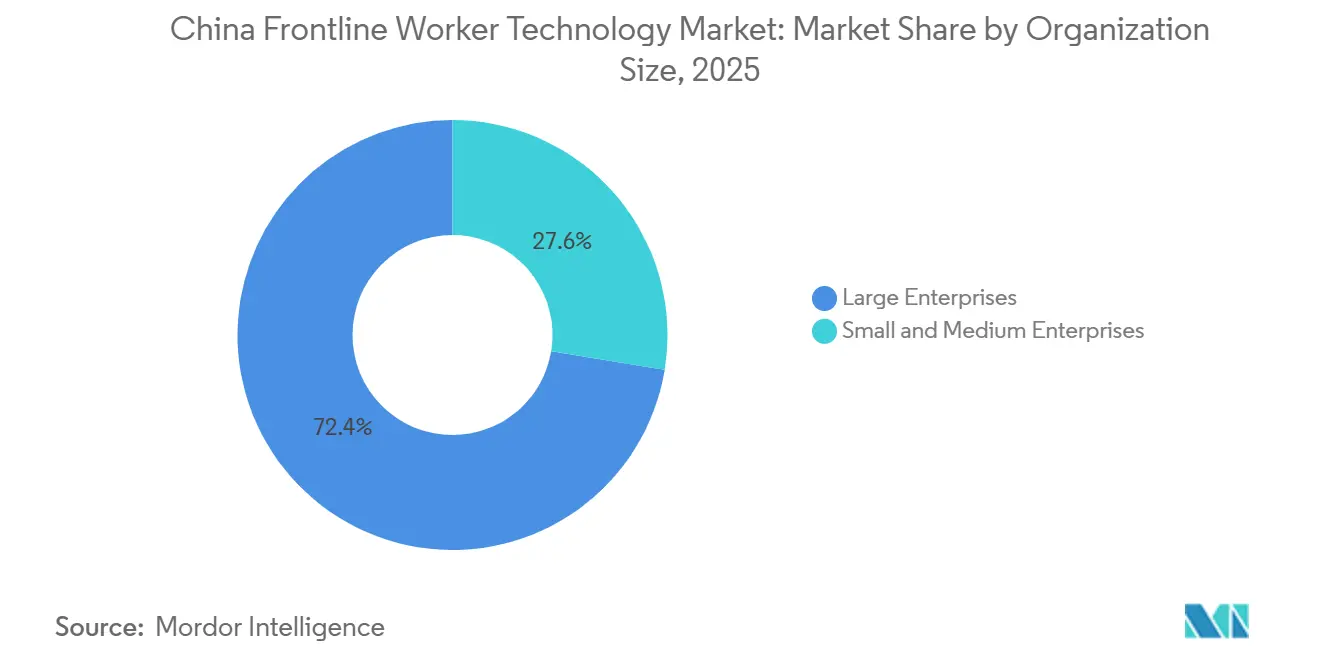

- By organization size, large enterprises captured 72.41% of revenue in 2025, while SMEs are expected to record the fastest growth at a 27.94% CAGR through 2031.

- By application, workforce execution and task management accounted for 25.48% of revenue in 2025, while workforce analytics and performance management are projected to advance at a 29.54% CAGR through 2031.

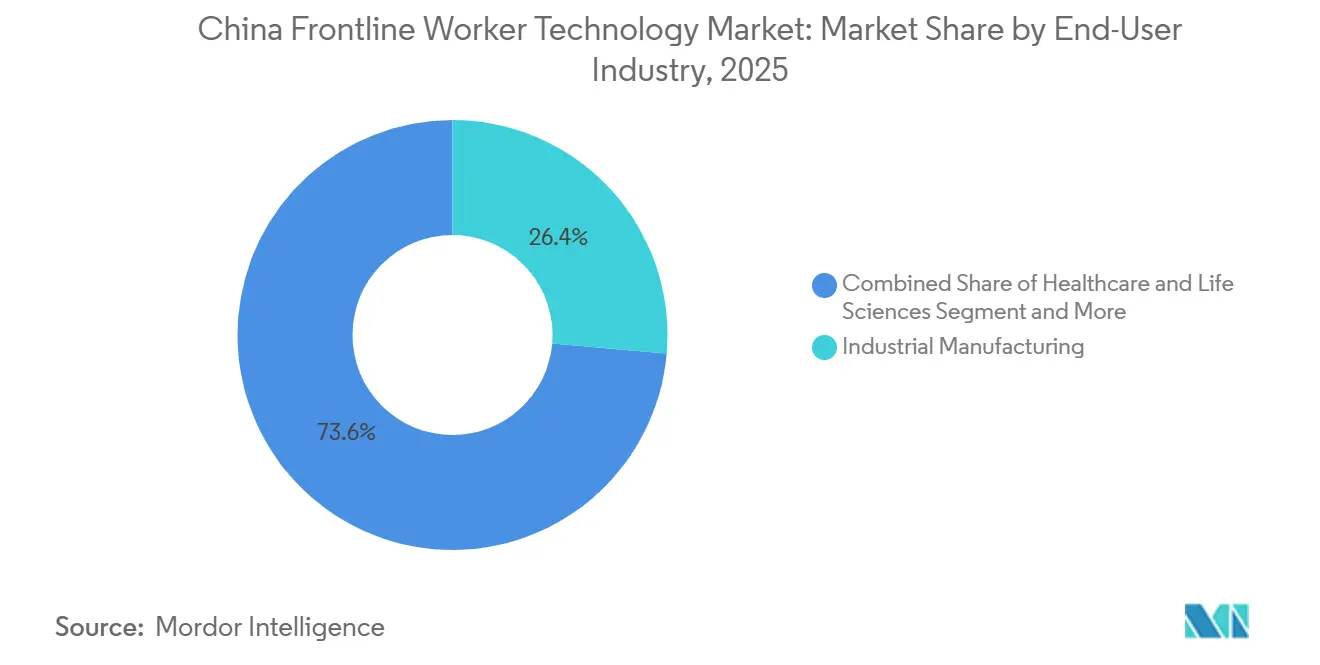

- By end-user industry, industrial manufacturing held 26.37% of revenue in 2025, while healthcare and life sciences are expected to grow at a 29.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China Frontline Worker Technology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mobile-First Digitization of Deskless Workflows | +5.5% | National, with early concentration in Pearl River Delta manufacturing corridors and Yangtze River Delta retail clusters | Short term (≤ 2 years) |

| AI-Led Labor Forecasting and Schedule Optimization | +4.8% | National, with highest intensity in Tier 1 and Tier 2 city manufacturing and logistics hubs | Medium term (2-4 years) |

| Labor-Rule Complexity Across Multi-Site Shift Operations | +4.2% | National, with amplified compliance pressure in Guangdong, Jiangsu, and Shanghai jurisdictions | Short term (≤ 2 years) |

| Unified HR, Payroll, Scheduling, and Communication Stacks | +3.7% | National, with strongest adoption pull among large enterprises operating across multiple provinces | Medium term (2-4 years) |

| Explainable AI and Audit-Ready Scheduling Demand | +2.8% | National, with regulatory influence from the Cyberspace Administration of China expanding into AI governance | Long term (≥ 4 years) |

| Worker-Control Expectations Around Shifts, Pay, and Flexibility | +2.1% | Urban concentrated, especially in Tier 1 and Tier 2 city retail, hospitality, and logistics sectors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Mobile-First Digitization Of Deskless Workflows

The China frontline worker technology market is benefiting from a large deskless labor base that has historically had limited access to enterprise software, which makes mobile-first design the most practical route to mass adoption. Affordable connected devices have reduced the hardware barrier that once slowed deployment across factories, warehouses, stores, and field operations, so software design now matters more than device availability. DingTalk’s deployment at Shandong Weiqiao Group covered 80,000 employees, including production workers with basic formal education, and that example showed that simplified mobile workflows can scale quickly when the interface fits the user environment.[1]DingTalk Global Team, “Shandong’s Top Private Enterprise Brings Artificial Intelligence Into Its Factory in Weifang,” DingTalk Global, dingtalk-global.com Vendors with offline-first architecture are better placed in industrial settings where connectivity can still be uneven across sites, production zones, and logistics yards. Real-time attendance capture, task completion records, and mobile communication are also becoming harder to treat as optional tools, as multi-site employers need more reliable digital records for operational control and labor compliance.

AI-Led Labor Forecasting And Schedule Optimization

The China frontline worker technology market is also being shaped by a clear shift from basic digitization toward AI-backed workforce planning, because employers now expect scheduling software to reduce labor waste and improve staffing precision. GaiaWorks stated that its AI scheduling engine served more than 1,800 enterprise clients across 33 countries and achieved 85% sales-volume prediction accuracy, indicating tangible value for factories, retailers, and service operators that manage high-volume shift patterns.[2]GaiaWorks Team, “GaiaWorks Smart Scheduling, AI Compliance Engine Covering 200+ Labor Regulations,” GaiaWorks, gaiaworks.cn Once labor demand can be forecast with greater accuracy, buyers can justify platform spending through lower overstaffing, fewer missed service windows, and better use of trained workers across shifts. This makes AI scheduling less of a premium add-on and more of a core requirement, especially in sectors where payroll costs move quickly with production volumes or foot traffic. The practical advantage is strongest for vendors that can explain scheduling logic in a way managers, workers, and auditors can all understand, because explainability supports both operational trust and procurement acceptance.

Labor-Rule Complexity Across Multi-Site Shift Operations

China’s labor environment is giving the China frontline worker technology market a durable, compliance-led demand base, as large employers need systems that can handle the varied overtime, rest-day, approval, and record-keeping rules across provinces and cities. Manual scheduling becomes difficult to defend when a business runs several plants, stores, or service sites under different local conditions, and that is raising the value of rule-based automation in day-to-day workforce management. GaiaWorks stated that its compliance engine covered more than 200 active labor regulations, which highlights how broad and frequently updated the local rule environment can be for employers operating at scale. This makes compliance updates a recurring part of the product relationship rather than a one-time implementation task, which strengthens renewal rates for vendors that can keep policy logic current. It also gives domestic providers an edge by allowing them to localize rule engines faster than foreign platforms that rely on heavier customization or slower release cycles.

Unified HR, Payroll, Scheduling, And Communication Stacks

Enterprises in the China frontline worker technology market are moving toward unified platforms because separate tools for HR, payroll, scheduling, approvals, and communication create cost, delays, and fragmented data. The appeal of a single-workspace operating environment is stronger in China because employers and employees are already familiar with mobile-first ecosystems that handle multiple tasks within a single interface. Kingdee reported 20.9% growth in cloud subscription revenue in FY2025, and that momentum reflected stronger demand for integrated cloud tools, including AI HR capabilities that reduce the need for disconnected point solutions.[3]Kingdee International Team, “Kingdee International Announces FY2025 Annual Results, Cloud Subscription Revenue Increased by 20.9%,” Kingdee International, kingdee.com.hk Once buyers move to integrated stacks, the value extends beyond convenience, as shared data improves scheduling quality, attendance accuracy, approval speed, and workforce visibility across sites. This is encouraging both large enterprises and mid-market firms to shorten the old adoption cycle and move directly toward cloud-native platforms with broader built-in functionality.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy Integration Complexity Across HR, Payroll, POS, and EHR | -3.8% | National, most acute in traditional manufacturing and state-owned enterprise sectors with long-tenured legacy systems | Medium term (2-4 years) |

| Workforce Data Privacy and Mobile Cybersecurity Exposure | -2.9% | National, with compliance pressure strongest in Beijing, Shanghai, and Guangzhou | Long term (≥ 4 years) |

| Shared-Device Identity and Digital Access Gaps | -2.1% | National, with highest friction in assembly-line manufacturing and healthcare settings where personal device use is restricted | Medium term (2-4 years) |

| Manager and Worker Distrust of Opaque Scheduling AI | -1.6% | National, most visible in unionized sectors and state-affiliated enterprises | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Legacy Integration Complexity Across HR, Payroll, POS, And EHR

The biggest execution barrier in the China frontline worker technology market remains the technical debt built into legacy systems, especially in manufacturing and healthcare environments, where core operating tools were installed at different times for different functions. Employers often have payroll, ERP, execution, attendance, and scheduling data spread across separate systems, which means a new workforce platform must fit into an already crowded architecture before it can deliver value. This slows rollout, increases implementation costs, and makes deployment harder for mid-sized firms without large internal IT teams or flexible integration budgets. The problem is more pronounced in healthcare because hospital information systems and clinical records often operate within tightly controlled internal environments, limiting real-time data exchange with external scheduling tools. Vendors that bring pre-built connectors to widely used enterprise systems improve their chances, but the long tail of local configurations still extends sales cycles and adds friction to expansion.

Workforce Data Privacy And Mobile Cybersecurity Exposure

Data privacy and device security are a meaningful brake on the China frontline worker technology market because these platforms collect attendance records, location data, shift histories, and sometimes biometric or performance-related information for large populations. Once that data is centralized across many sites and workers, buyers need stronger control over storage, access rights, audit trails, and device-level protection, which raises the bar for vendor selection. China’s personal information protection framework has made workforce data governance a board-level issue for larger employers, and active enforcement has made compliance risk harder to ignore in enterprise procurement. Shared devices create an extra layer of difficulty because session overlap, weak identity controls, and casual hand-offs increase the chance of unauthorized access in factories, hospitals, and depots. Vendors that can show domestic hosting, granular permissions, and audit-ready records are better placed to turn this restraint into a trust advantage, but those safeguards still lengthen evaluation and implementation timelines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Anchors Revenue While Services Scale Fast

Software accounted for 70.12% of revenue in 2025, making it the largest component of the China frontline worker technology market and confirming that buyers continue to direct most spending toward core platforms rather than support layers alone. Enterprises are choosing recurring-license systems because they can combine scheduling, compliance management, analytics, and worker engagement within one managed environment. This buying pattern also reflects a move away from customization-heavy on-premises builds, since buyers want vendors to handle maintenance, rule updates, and AI model improvement within the subscription structure. The software layer matters even more when employers operate many sites, because standardized deployment improves visibility across locations and lowers the risk created by separate local tools. In practical terms, software has become the operating backbone of workforce digitization, while adjacent functions such as training, communication, and performance tracking increasingly sit inside the same platform rather than on separate products.

Services are projected to grow at a 27.18% CAGR through 2031, which shows that the next spending wave in the China frontline worker technology industry will not be limited to software licenses alone. Buyers who adopted foundational systems earlier are now spending more on implementation, integration, change management, and workforce training to capture greater value from data and AI features. This pattern is common in large manufacturers and hospital systems, where deployment success depends on linking the platform with ERP, HR, payroll, and operational data flows across several sites. GaiaWorks introduced an enterprise-grade custom AI framework that allows clients to build human-efficiency AI agents on domestic large language models, reducing some dependence on bespoke external development while still expanding the service opportunity around configuration and rollout. The balance between software and services suggests a market moving from basic adoption to deeper operational use, with service demand rising as employers seek more measurable business outcomes from the installed base.

By Deployment: Cloud Dominance Reinforced By Domestic Data Residency Mandates

Cloud-based deployment accounted for 66.84% of revenue in 2025 and leads forecast expansion at a 28.26% CAGR, placing it at the center of the China frontline worker technology market, both in current demand and future adoption. This dual lead shows that cloud is not only taking most new deployments but also capturing renewal and expansion spending from existing users. Domestic hosting and data residency requirements have supported this trend, as employers seek deployment models that meet local compliance requirements without introducing cross-border data complications. Cloud also shortens rollout time, supports frequent product updates, and enables vendors to push new compliance rules and AI features to many client sites simultaneously. For multi-site operators, that makes cloud deployment easier to justify than local installations that require heavier internal support and slower version management.

Hybrid models continue to serve employers that are not ready for a full migration, especially when payroll records, biometric information, or other sensitive workforce data still reside in local systems. In those cases, businesses can keep selected records on-premises while moving scheduling, communication, and analytics to the cloud, reducing disruption during the transition. On-premises deployments still have a role in some state-linked and heavily controlled environments, but their share of new implementations is under pressure because buyers increasingly value flexibility, scalability, and faster upgrades. The China frontline worker technology market is therefore seeing cloud move from a preferred option to the default architecture for most growth accounts, particularly as domestic providers strengthen their compliant infrastructure and enterprise support. This shift should continue to favor vendors that can combine strong China-based hosting with reliable integration capabilities, as buyers no longer treat compliance and usability as separate purchasing issues.

By Organization Size: Large Enterprises Dominate While SMEs Become The Emerging Growth Engine

Large enterprises accounted for 72.41% of revenue in 2025, giving them a clear lead in the China frontline worker technology market share and reflecting the scale advantages of buyers with thousands of workers across several provinces. These employers face complex labor rules, broader audit exposure, and more urgent needs for standardized scheduling, attendance, payroll coordination, and workforce communication. They also tend to integrate these platforms more deeply with MES, ERP, and HR systems, thereby raising switching costs and making vendor relationships more durable over time. Once a platform is embedded across plants, warehouses, or hospital networks, the cost of migration becomes high enough to support longer renewal cycles and expansion spending. This gives the large enterprise segment a stable revenue base, while also making it the main proving ground for advanced AI and compliance functionality before those tools filter more broadly into the rest of the market.

SMEs are projected to grow at a 27.94% CAGR through 2031, indicating the fastest expansion track within the China frontline worker technology industry as cost barriers and deployment complexity continue to fall. Lower per-seat SaaS pricing and lighter implementation requirements are making modern workforce platforms more practical for companies that once relied on spreadsheets, manual attendance, or basic messaging tools. Provincial and city-led digitalization support has also widened the opportunity set by helping smaller manufacturers and operating businesses fund technology upgrades. China Mobile’s 5G plus AI digitization work for SMEs in Ningbo showed how carrier-backed infrastructure programs are opening a broader pipeline in sectors such as apparel, auto parts, and home appliances.[4]C114 Communications Staff, “Ningbo Mobile 5G+AI Digital Intelligence Empowers SME Quality Improvement,” C114 Communications, c114.com.cn The result is a more balanced demand profile for the China frontline worker technology market, where large accounts still anchor revenue but smaller firms are becoming the main source of new user growth.

By Application: Analytics Leads Growth As Task Execution Holds The Revenue Base

Workforce execution and task management accounted for 25.48% of application revenue in 2025, making it the largest use case and showing that the China frontline worker technology market still rests on operational control at the point of work. Assembly lines, fulfillment centers, field teams, and large service networks need tools that can assign tasks, track completion, and maintain real-time visibility across shifts. These functions are easy for buyers to tie to daily output, which explains why execution remains the revenue foundation even as broader platform capabilities improve. Scheduling and communication tools continue to support this layer by keeping workers informed, aligning managers, and making shift changes visible faster. In many deployments, task management is the entry point that later leads employers toward analytics, engagement, and learning functions once enough workforce data has been captured.

Workforce analytics and performance management are projected to grow at a 29.54% CAGR through 2031, making it the fastest-growing application area as buyers shift their attention from coordination to decision quality. Once employers have digitized attendance, tasks, and schedules, they can use that data to detect attrition risk, labor-cost variance, performance patterns, and staffing gaps. This change matters because workforce software is increasingly being judged on how well it helps managers make better labor decisions, not only on whether it records activity. Learning and knowledge enablement is also receiving more attention as employers look for easier ways to support frontline capability upgrades through mobile access and shorter training loops. The China frontline worker technology market is therefore evolving from workflow digitization toward labor intelligence, with analytics becoming the link between frontline execution and higher-level business planning.

By End-User Industry: Manufacturing Leads By Share As Healthcare Accelerates

Industrial manufacturing accounted for 26.37% of 2025 revenue, giving it the largest end-user position and keeping factory operations at the center of the China frontline worker technology market. Large-scale plants across Guangdong, Jiangsu, Zhejiang, and Shandong continue to need workforce tools that can handle shift complexity, attendance control, compliance logic, and productivity visibility across several production lines. Manufacturing also has a strong incentive to connect labor data with wider industrial digitization efforts because scheduling quality and worker coordination directly affect throughput, quality control, and downtime management. Midea Group’s Jingzhou plant received a world record certification for AI agent factory deployment in 2025, with 14 AI agents across 38 business scenarios, which illustrated how advanced plants are combining workforce tools with broader AI-enabled operating models.[5]Yicai Global Staff, “Chinese Home Appliance Giant Midea Receives World’s First AI Agent Factory Certification,” Yicai Global, yicaiglobal.com That makes manufacturing the clearest current revenue anchor, while also keeping it at the front of product innovation for scheduling, execution, and labor analytics.

Healthcare and life sciences are projected to expand at a 29.08% CAGR through 2031, making it the fastest-growing end-user segment in the China frontline worker technology market, as hospitals and community care systems increase digital adoption. The growth is being supported by the June 2026 directive to embed AI across community health service centers, which raised the importance of workforce coordination, scheduling, and operational support tools in the care system. Xinhua also reported that China was advancing AI-powered digital healthcare to improve efficiency and accessibility, which supports a wider move toward digitally managed clinical workflows and staff deployment. Retail and e-commerce, transportation and logistics, and hospitality remain important demand pools because they combine high employee counts, frequent shift changes, and strong communication needs. Construction and government are earlier adopters, but public digitalization mandates and stricter attendance system requirements are likely to keep them relevant in the next expansion phase.

Geography Analysis

Eastern China remains the most mature part of the China frontline worker technology market, combining dense manufacturing clusters, advanced digital infrastructure, and a high concentration of enterprise buyers. The Yangtze River Delta, including Shanghai, Suzhou, Hangzhou, and Nanjing, offers a strong installed base for scheduling, attendance, communication, and analytics platforms because many employers there operate multiple facilities with large frontline teams. GaiaWorks is headquartered in Suzhou and has supported workforce management for clients such as Nestlé China, which shows how the region connects vendor development with enterprise deployment at scale. Eastern China also benefits from stronger cloud readiness and better connectivity in industrial parks, which support mobile-first deployments across plants and distribution sites. Healthcare digitization in this region is advancing rapidly as large hospital networks respond to workforce-efficiency requirements and broader digital transformation goals.

Southern China is one of the fastest-moving regional demand centers in the China frontline worker technology market because electronics manufacturing, export logistics, retail activity, and hospitality all create large deskless labor pools. Guangdong and the Greater Bay Area place a premium on workforce efficiency because labor costs are higher than in many inland regions, thereby sharpening the return on investment for AI scheduling and improved shift utilization. Shenzhen also adds a connected-device advantage, as its hardware ecosystem supports broader use of handhelds, wearables, and edge devices that can strengthen worker-facing deployments. GaiaWorks used Workday Elevate and SAP HR Connect events in Hong Kong in 2026 to demonstrate Greater Bay Area compliance functionality, highlighting how cross-jurisdictional labor complexity sustains demand for specialized local solutions. The region, therefore, combines strong commercial demand with a practical testing ground for compliant, mobile, and AI-enabled workforce products.

Northern and Central-Western China represent the next broad opportunity zone for the China frontline worker technology market, as public-sector buyers, automotive clusters, and SME digitization programs widen the addressable base. Beijing and Tianjin are important because state-linked and government-adjacent buyers tend to favor domestic, Xinchuang-compliant platforms, which support local vendors with stronger policy alignment. Chongqing, Chengdu, Xi’an, and other inland centers are also gaining relevance as manufacturing and logistics activity spreads beyond the coast and digital transformation programs bring support for smaller enterprises. Xinhua reported in 2026 that China was advancing AI-powered healthcare coverage and efficiency, supporting greater workforce adoption of technology across inland community health systems and public service networks. This means regional growth is no longer limited to coastal demand, as policy support, domestic procurement preferences, and a broader SME pipeline are driving adoption deeper into the national footprint.

Competitive Landscape

The China frontline worker technology market remains moderately concentrated at the top and fragmented across the mid-market, which means no single provider has enough share to dominate every application layer or buyer segment. Global firms such as WorkForce Software, Humanforce, Deputy, Legion Technologies, and Tulip Interfaces maintain strong positions in enterprise-focused deployments, especially where multinational operating models or advanced manufacturing workflows are relevant. At the same time, domestic players such as GaiaWorks and Kingdee are benefiting from local-language interfaces, stronger alignment with Chinese labor rules, and easier integration with China-specific payroll and ERP systems. That mix keeps competition active across software, services, deployment models, and end-user verticals. It also means buyers are comparing vendors not only on features, but also on compliance fit, cloud readiness, implementation burden, and local support depth.

Several strategic patterns are shaping competition in the China frontline worker technology market. ADP completed its acquisition of WorkForce Software in October 2024, strengthening its enterprise workforce management position and giving buyers a broader, single-vendor option for HR and scheduling needs. Kingdee’s FY2025 results showed continued cloud subscription momentum, which supported its push to deepen AI HR capabilities within a broader enterprise software stack. Honeywell launched the CT70 handheld computer in October 2025 with integrated AI processing, 5G, and Wi-Fi 7, demonstrating how device innovation is beginning to complement workforce software in logistics and retail use cases. These moves matter because the competitive field is no longer limited to scheduling software alone; it now includes bundled ecosystems that combine devices, AI, workflow tools, and enterprise integration.

The strongest white-space opportunity appears in SME manufacturing, where many plants still rely on spreadsheets or manual shift planning and need lower-cost tools with limited implementation burden. That opening favors vendors that can deliver simple pricing, fast setup, and enough flexibility to handle local labor rules without a large internal IT team. Domestic platforms have an added advantage when they can train or fine-tune AI functions around local operating language, data-hosting rules, and sector-specific workflows. Compliance credentials are also becoming a stronger moat in healthcare and public-sector procurement, where buyers want proof of data security discipline alongside application performance. Overall, the China frontline worker technology market is likely to remain competitive rather than consolidate quickly, as local regulations, industry diversity, and varying customer maturity levels still leave room for several vendor models to coexist.

China Frontline Worker Technology Industry Leaders

SAP SE

Microsoft Corporation

Honeywell International Inc.

Zebra Technologies Corporation

Huawei Technologies Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Humanforce launched AI-powered Smart Scheduling, an advanced rostering solution that aligns labor demand to real-time forecasts, reducing roster management time by up to 70% and contributing up to a 15% reduction in labor costs.

- May 2026: Axonify announced significant AI enhancements to its frontline enablement platform designed to close the gap between learning and strategy execution for frontline workers, reframing the company's market position from a learning management tool to a unified frontline operations enablement platform.

- January 2026: Tulip Interfaces secured USD 120 million in Series D funding led by Mitsubishi Electric, achieving a valuation of USD 1.3 billion. The strategic alliance with Mitsubishi Electric provides Tulip with direct access to Japan and Asia-Pacific manufacturing customers and distribution channels, expanding its industrial frontline technology footprint.

- January 2026: Legion Technologies launched more than 90 AI workforce innovations, including autonomous workforce decision automation covering forecasting, scheduling, time and attendance, and labor optimization. Legion reported 216% revenue growth in 2025 and now operates in 35 countries.

China Frontline Worker Technology Market Report Scope

The China Frontline Worker Technology Market Report is Segmented by Component (Software and Services), Deployment (Cloud-Based, Hybrid, and On-Premises), Organization Size (Large Enterprises and Small and Medium Enterprises), Application (Employee Communication and Engagement and More), and End-User Industry (Retail and E-Commerce, Industrial Manufacturing, and More). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| Hybrid |

| On-Premises |

| Large Enterprises |

| Small and Medium Enterprises |

| Employee Communication and Engagement |

| Workforce Execution and Task Management |

| Workforce Scheduling and Coordination |

| Learning and Knowledge Enablement |

| Workforce Analytics and Performance Management |

| Safety and Compliance Management |

| Other Applications |

| Retail and E-Commerce |

| Industrial Manufacturing |

| Healthcare and Life Sciences |

| Transportation and Logistics |

| Hospitality |

| Construction |

| Government and Public Administration |

| Other Industries |

| By Component | Software |

| Services | |

| By Deployment | Cloud-Based |

| Hybrid | |

| On-Premises | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Application | Employee Communication and Engagement |

| Workforce Execution and Task Management | |

| Workforce Scheduling and Coordination | |

| Learning and Knowledge Enablement | |

| Workforce Analytics and Performance Management | |

| Safety and Compliance Management | |

| Other Applications | |

| By End-User Industry | Retail and E-Commerce |

| Industrial Manufacturing | |

| Healthcare and Life Sciences | |

| Transportation and Logistics | |

| Hospitality | |

| Construction | |

| Government and Public Administration | |

| Other Industries |

Key Questions Answered in the Report

What is the current and forecast size of the China frontline worker technology market?

The China frontline worker technology market was valued at USD 1.16 billion in 2025, is expected to reach USD 1.38 billion in 2026, and is forecast to reach USD 4.19 billion by 2031 at a 24.85% CAGR.

Which deployment model leads adoption in China frontline worker technology?

Cloud-based deployment leads both current demand and future growth, with 66.84% revenue share in 2025 and a projected 28.26% CAGR through 2031.

Which application area is growing fastest in China frontline worker technology?

Workforce analytics and performance management is the fastest-growing application, with a projected 29.54% CAGR through 2031, as employers shift from basic digitization toward labor intelligence.

Which end-user sector generates the most revenue in China frontline worker technology?

Industrial manufacturing led in 2025 with 26.37% of revenue, supported by multi-line production environments that need scheduling, compliance, and productivity visibility tools.

Why are SMEs becoming more important in China frontline worker technology adoption?

SMEs are projected to grow at a 27.94% CAGR because SaaS pricing is becoming more accessible, implementation is getting simpler, and local digitalization programs are widening the buyer base.

How competitive is the vendor landscape in China frontline worker technology?

The field is moderately concentrated at the top but fragmented overall, with domestic players gaining ground through local compliance strength, while global vendors remain relevant in enterprise and manufacturing deployments.

Page last updated on: