China Finished Vehicle Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

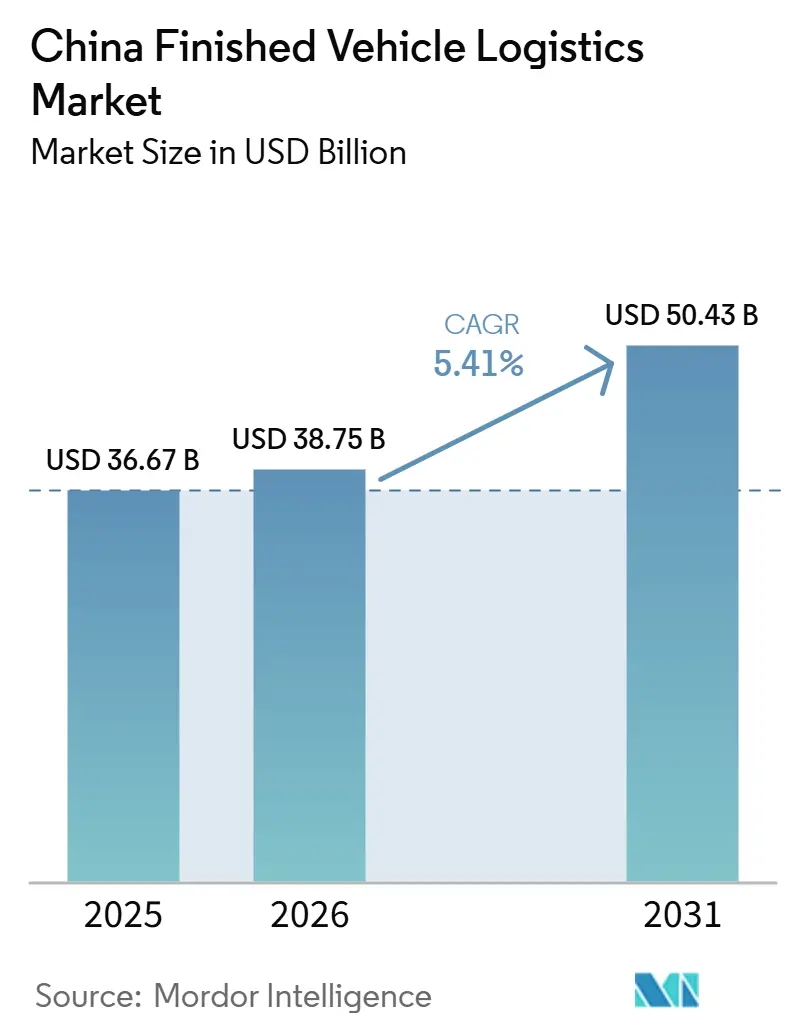

| Base Year Market Size (2025) | USD 36.67 Billion |

| Market Size (2026) | USD 38.75 Billion |

| Market Size (2031) | USD 50.43 Billion |

| Growth Rate (2026 - 2031) | 5.41% CAGR |

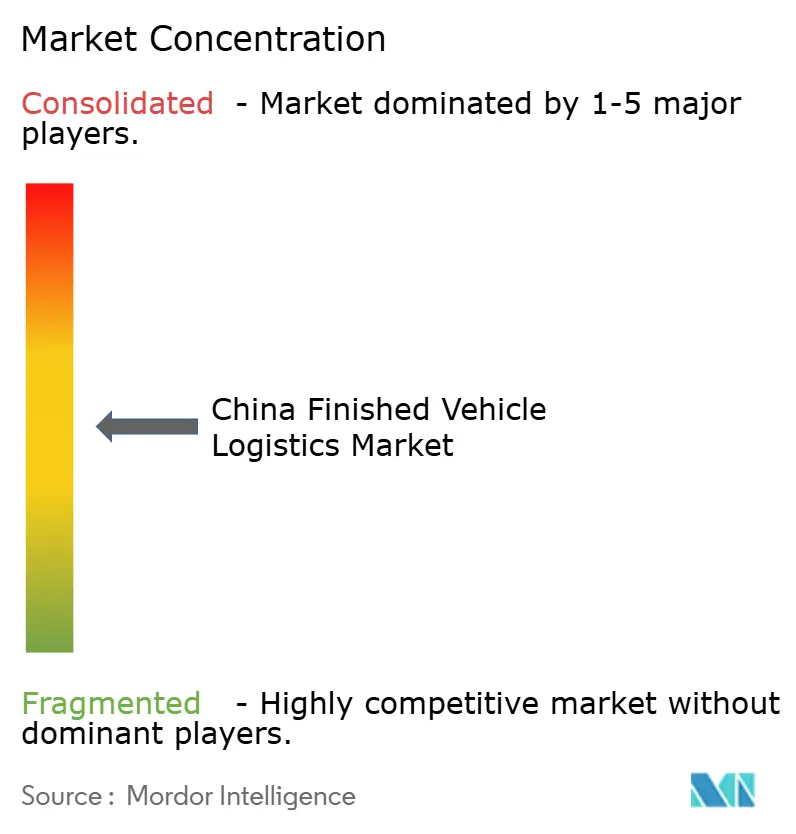

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Finished Vehicle Logistics Market Analysis by Mordor Intelligence

The China finished vehicle logistics market size is projected to expand from USD 36.67 billion in 2025 to USD 38.75 billion in 2026, and reach USD 50.43 billion by 2031, growing at a CAGR of 5.41% from 2026 to 2031.

The China finished vehicle logistics market is being lifted by a wider export footprint, more demanding handling requirements for new energy vehicles, and a steady rise in value-added service content per shipment. Rail-sea coordination, smarter port operations, and expanding customs facilitation are making inland manufacturing clusters more competitive in export logistics and are reducing some of the friction that once favored only coastal hubs. Competition is shifting because OEM-linked logistics arms are taking tighter control of shipping access, while domestic specialists remain strong in rail and dedicated road haulage and global 3PLs are focusing on compliance-heavy and technology-led contracts. The China finished vehicle logistics market is also seeing margin migration away from pure line-haul activity and toward inspection, battery handling, tracking, customs coordination, and yard control, which is changing how providers position themselves for growth. Policy-backed corridor development and continued smart-port investment give the China finished vehicle logistics market a durable operating base, even as carrier bottlenecks, damage liability, and route reconfiguration risk continue to weigh on execution.

Key Report Takeaways

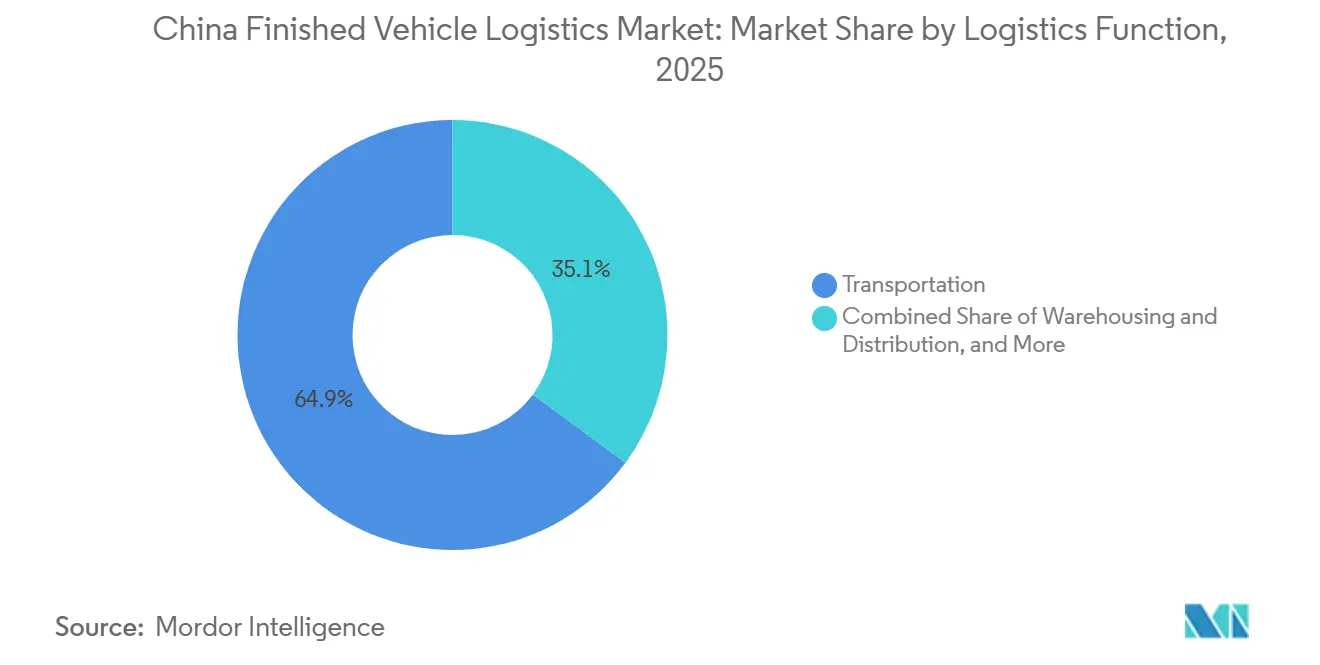

- By logistics function, transportation held 64.87% of the China finished vehicle logistics market share in 2025, while value-added services and others are forecast to expand at a 7.16% CAGR through 2031.

- By destination, domestic logistics held 73.10% of the China finished vehicle logistics market size in 2025, while international logistics is projected to record the fastest growth at a 6.76% CAGR through 2031.

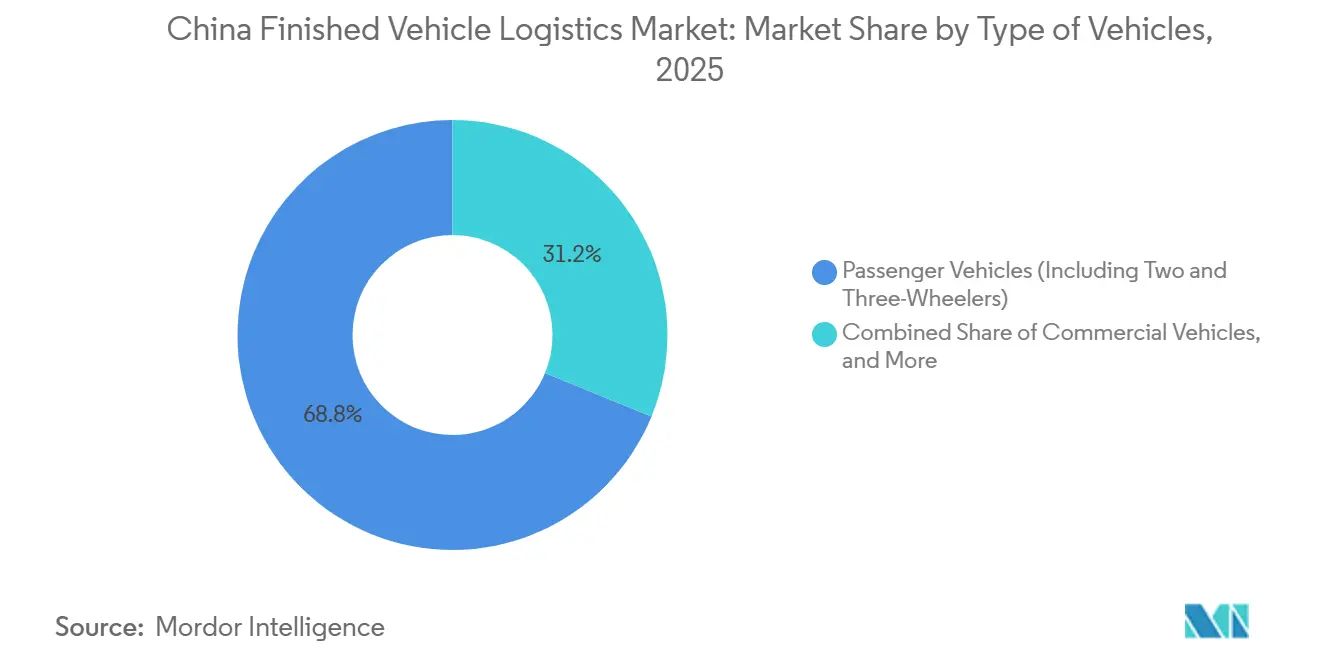

- By type of vehicles, passenger vehicles including two- and three-wheelers accounted for 68.81% of the China finished vehicle logistics market share in 2025 and also recorded the highest projected CAGR at 5.85% through 2031.

- By end-user industry, OEMs held 61.36% of the China finished vehicle logistics market share in 2025, while dealers are forecast to expand at a 6.54% CAGR through 2031.

- By geography, East China accounted for 34.03% of the China finished vehicle logistics market size in 2025, while Southwest China is projected to grow at the fastest CAGR of 6.71% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China Finished Vehicle Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising NEV Exports and Inter-Provincial Vehicle Repositioning | +1.5% | East coast, South, Southwest, inter-provincial corridors from the Yangtze River Delta and Sichuan-Chongqing clusters | Short term (≤ 2 years) |

| Port-Rail-RoRo Integration Across Coastal Export Corridors | +1.0% | East, including Ningbo-Zhoushan and Nantong, South, including Guangzhou Nansha and Shenzhen Xiaomo, and Southwest, including Qinzhou and Beibu Gulf | Medium term (2-4 years) |

| OEM Demand for Damage-Reduction and Real-Time Vehicle Visibility | +0.8% | National, with stronger relevance in East and South export hubs and international terminals | Medium term (2-4 years) |

| Dealer Network Consolidation and Direct-to-Dealer Delivery Optimization | +0.6% | National, with heavier concentration in East and South retail clusters and spillover into Central and Southwest China | Short term (≤ 2 years) |

| Expansion of Digital Yard Management, Gate Automation, and ETA Control Towers | +0.7% | East, especially Yangtze River Delta hubs, and South, especially Guangzhou and Shenzhen terminals | Medium term (2-4 years) |

| Policy Support for Multimodal Freight and Logistics Network Upgrades | +0.9% | National, with faster adoption in Southwest and Northwest corridor nodes | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising NEV Exports and Inter-Provincial Vehicle Repositioning

The China finished vehicle logistics market is increasingly shaped by rising NEV export activity and by the need to reposition finished vehicles between inland production bases and both domestic and export destinations. This is changing the network from a mainly distribution-led system into one that must manage more frequent long-distance balancing moves between factory clusters, staging yards, ports, and dealer points. The operating challenge is stronger because production remains concentrated in a limited number of major manufacturing zones, while demand is spreading across interior provinces and overseas markets. That pattern lifts vehicle handling complexity, planning requirements, and the need for specialized asset deployment across multiple corridors. As a result, the China finished vehicle logistics market is seeing higher logistics value per unit moved, even when transport productivity improves[1]“China Bolsters Regulation of Used Vehicle Exports.” Ministry of Public Security, and General Administration of Customs, cceeccic.org.

Port-Rail-RoRo Integration Across Coastal Export Corridors

The most important infrastructure shift in the China finished vehicle logistics market is the deeper integration of rail, port, and RoRo capacity across export corridors. In April 2025, China opened its first RoRo route from Beibu Gulf Port to Jebel Ali, cutting transit time by 4 to 10 days against conventional routing and improving logistics efficiency by 10% to 15% within the New International Land-Sea Trade Corridor. In January 2026, a rail-sea intermodal freight train loaded with Chongqing-made NEVs departed for Nansha Port and then connected to a vessel bound for the Middle East, showing that inland factories can now plug into regular export chains with fewer breakpoints. Xinhua also reported in June 2025 that China-Europe freight trains were carrying finished vehicles in around 12 days at a logistics cost of around USD 2,000 per vehicle, against 25 to 30 days and around USD 2,500 per vehicle by road, which strengthens the case for high-priority and inland export batches. The China finished vehicle logistics market will benefit as these intermodal links move from pilot corridors into repeatable operating models across a wider set of inland and coastal nodes.

OEM Demand for Damage-Reduction and Real-Time Vehicle Visibility

OEMs are placing more value on damage prevention, location accuracy, and condition monitoring, and this is raising service expectations across the China finished vehicle logistics market. The issue is more important for NEVs because battery safety, state-of-charge control, and traceability requirements add more operational checks than conventional vehicle movements[2]“China’s New EV Battery Safety Standard to Take Effect in July 2026.”gov.cn. Providers are being asked to support tighter service-level commitments through geofencing, real-time ETA visibility, automated exception logging, and better yard sequencing. Shenzhen Xiaomo International Logistics Port has used an IoT-based platform to dispatch vehicles and match berths with parking locations, which points to a more automated model for reducing loading time and handling risk. This is pushing the China finished vehicle logistics market toward contracts that reward proven control and compliance rather than simple transport volume.

Policy Support for Multimodal Freight and Logistics Network Upgrades

Government-backed infrastructure planning remains an important growth base for the China finished vehicle logistics market. Xinhua reported in January 2026 that Chongqing was using rail-sea intermodal transport to move NEVs through Nansha toward Middle East destinations, which shows that public corridor development is already translating into live export flows rather than remaining a policy goal. Xinhua also reported in December 2025 that Chongqing was strengthening its role as an inland NEV export hub through corridor construction, customs support, and better access to global markets. These moves matter because they reduce time loss between factory output and export loading and improve the economics of moving vehicles from interior plants. Over time, that support will keep the China finished vehicle logistics market more geographically balanced, with inland production centers playing a larger role in export logistics than they did in earlier cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Specialized Car-Carrier Capacity Bottlenecks in Peak Export Seasons | -0.7% | East coast export ports, including Shanghai and Ningbo-Zhoushan, South China, including Guangzhou Nansha, and North China, including Tianjin | Short term (≤ 2 years) |

| High Vehicle Damage Exposure in Short-Haul and Yard-to-Yard Movements | -0.5% | National, with greater pressure at East and South processing compounds | Medium term (2-4 years) |

| Toll, Fuel, and Empty-Return Cost Pressure on Domestic Road Transport | -0.4% | National, with stronger pressure on North-South inter-provincial trunk routes and dedicated round-trip car-carrier lanes | Short term (≤ 2 years) |

| Fragmented Regional Operating Standards and Loading Infrastructure Gaps | -0.4% | Northwest, Northeast, and Central China, especially lower-tier logistics zones with limited standardized auto berths | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Specialized Car-Carrier Capacity Bottlenecks in Peak Export Seasons

The China finished vehicle logistics market still faces capacity pressure in peak export periods, even after a wave of vessel additions in 2025 and 2026. The problem is not only fleet size, because berth access, scheduling reliability, and terminal readiness also determine how much vehicle volume can move on time. That means secondary export ports cannot always absorb overflow from the busiest coastal gateways, especially when larger vessels need specific berth depth and handling support. In practice, this keeps export capacity uneven across operators and leaves smaller or less integrated shippers more exposed to quarter-end pressure. The China finished vehicle logistics market, therefore, remains vulnerable to execution bottlenecks whenever export growth outpaces the readiness of port and shipping infrastructure.

High Vehicle Damage Exposure in Short-Haul and Yard-to-Yard Movements

Damage exposure remains a meaningful restraint in the China finished vehicle logistics market, especially in short-haul transfers between factory gates, compounds, processing centers, and ports. NEV shipments raise that exposure because battery-related incidents, loading issues, and condition-monitoring failures can create larger financial and compliance consequences than they do for conventional vehicles. Smart warehousing and automated storage systems can reduce handling risk and lower cost per vehicle, but adoption is still concentrated among larger manufacturers with stronger capital budgets. The result is a two-speed operating environment in which better-equipped providers can document lower damage rates and support stronger audit trails, while smaller operators struggle to match those standards. Over time, this will keep pushing the China finished vehicle logistics market toward more standardized, technology-led handling models[3]“Finished Vehicle Logistics.” Odette and ECG, odette.org .

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Logistics Function: Transportation Dominance Coexists with Value-Added Services Surge

Transportation accounted for 64.87% of the China finished vehicle logistics market share in 2025, which made it the largest functional segment, while value-added services and others are projected to grow at a 7.16% CAGR through 2031. That mix shows that physical movement still anchors the market, even as profit pools start to shift toward services built around the transport leg. Road transport remains the core mode for domestic dealer replenishment and for shorter inter-city and intra-provincial moves. Sea and inland waterways continue to matter for bulk export batches and for linking inland river manufacturing zones with deep-sea terminals.

The China finished vehicle logistics market is gradually rewarding providers that can bundle inspection, damage certification, battery handling, ETA visibility, and customs coordination into a single service offer. Rail still represents a smaller share, but it is becoming more relevant on longer inland routes where cost and time discipline matter more than pure flexibility. Warehousing and distribution are also changing in role, because OEMs now want faster processing and better staging rather than passive vehicle storage. That shift means compounds, pre-delivery inspection, port-side sequencing, and digital yard flow are becoming more central to functional differentiation than simple transport volume alone[4]“Finished Vehicle Logistics.” AIAG, aiag.org/expertise-areas/supply-chain-management/finished-vehicle-logistics.

By Destination: Domestic Primacy Masking a Rapidly Maturing Export Infrastructure

Domestic logistics held 73.10% of the China finished vehicle logistics market size in 2025, while international logistics is forecast to grow at a 6.76% CAGR through 2031. This keeps domestic activity as the base of the market, but it also shows that export-oriented logistics is gaining weight at a faster pace. The domestic segment remained larger because China still supports a vast internal distribution network across coastal and inland retail markets. The international segment, however, is moving beyond a niche export function and into a core growth engine for operators that can manage outbound complexity.

Export logistics is benefiting from corridor upgrades, growing port integration, and wider acceptance of rail-sea handoffs for inland production clusters. Import and inbound flows still matter because they support compound utilization and help reduce directional imbalance at some coastal terminals. A less visible effect is that stronger export deployment can tighten domestic equipment availability when specialized rolling stock or carrier capacity gets pulled toward higher-value overseas routes. Providers that manage outbound and return flow more efficiently will be better placed to protect asset utilization and pricing discipline across the China finished vehicle logistics market.

By Type of Vehicles: Passenger Vehicle NEV Growth Reshapes Handling Standards

Passenger vehicles, including two- and three-wheelers, accounted for 68.81% of the China finished vehicle logistics market size in 2025, and the same segment is projected to expand at a 5.85% CAGR through 2031. That gave passenger vehicles the leading position in both scale and growth within the market. The category remains dominant because passenger vehicle production volumes are high, and because NEV shipments are increasing, the service content required per unit. More documentation, battery monitoring, and condition control are raising the operational bar for providers that handle this segment.

Commercial vehicles remain strategically important because they support different export patterns, customer schedules, and shipment profiles than passenger vehicles do. Off-highway vehicles also contribute, especially where mixed vessel loading and infrastructure-linked export demand support broader cargo combinations. The China finished vehicle logistics market share tied to passenger vehicles is likely to remain high because this segment aligns most closely with China’s large-scale OEM output and export push. At the same time, operators that build strong EV-specific handling capability will have a clearer route to premium accounts within the wider China finished vehicle logistics industry.

By End-user Industry: OEM Centricity Under Pressure from Dealer Model Disruption

OEMs held 61.36% of the China finished vehicle logistics market share in 2025, while dealers are projected to record the fastest CAGR at 6.54% through 2031. This means the market still revolves around OEM contracting power, but dealer-side demand is becoming more important in service design and order execution. Large OEMs continue to shape pricing, service-level expectations, and network configuration because they control shipment volume and route concentration. Even so, dealer demand is becoming more structured and more quality-sensitive as weaker channels exit and stronger groups seek tighter delivery performance.

The practical outcome is that providers are facing more requests for direct-off-wharf delivery, better inventory visibility, and narrower delivery windows. Traditional 4S dealer flows now sit alongside newer delivery endpoints and more flexible retail arrangements, which increases routing complexity in the last stage of the chain. Fleet buyers, rental companies, and public sector users also remain relevant because centralized bulk delivery can offer stable utilization for domestic specialists. The China finished vehicle logistics industry is therefore moving toward a more mixed end-user base in which OEM control remains strong, but downstream service demands influence revenue quality more directly than before.

Geography Analysis

East China held 34.03% of revenue in 2025, which made it the largest regional contributor within the China finished vehicle logistics market. Its strength comes from the Yangtze River Delta, where dense automotive production, strong road and rail links, and major ports create the country’s deepest finished vehicle handling base. The region benefits from the close spacing of factories, compounds, and terminals, which reduces transfer friction and supports better control over dwell time. East China also stays ahead because OEM export operations are concentrated around a relatively mature logistics fabric that can support both domestic redistribution and overseas loading. This gives the China finished vehicle logistics market a strong operational core in the East, even as other regions improve their corridor depth.

South China remains a major export gateway because it supports large NEV flows from Guangdong and has port infrastructure that is already geared toward outward vehicle movement. Shenzhen Xiaomo’s use of IoT-based vehicle dispatch and berth matching shows how South China is trying to raise handling precision and shorten loading cycles. North China also remains important because its manufacturing base and established port system keep it tied to export and domestic redistribution activity. Together, East, South, and North China form the main coastal structure of the China finished vehicle logistics market, with each region serving a different balance of OEM concentration, terminal depth, and route reach. Their combined role will remain central because most large-volume outbound flows still depend on coastal loading efficiency.

Southwest China is projected to grow at a 6.71% CAGR through 2031, which makes it the fastest-expanding geography in the China finished vehicle logistics market. Chongqing’s vehicle export value reached CNY 40.22 billion (USD 5.70 billion) in the first 10 months of 2025, which showed that the inland cluster was already gaining export scale. The region’s rise is closely linked to rail-sea intermodal development, with Xinhua reporting in January 2026 that Chongqing-made NEVs moved by rail to Nansha and then by vessel to the Middle East. Central China, Northeast China, and Northwest China still represent smaller shares, but each has a strategic role through inland distribution, rail gateway access, and border-oriented export corridors. The China finished vehicle logistics market share of these inland and border regions remains lower today, but their corridor function gives them long-term relevance as western and central export flows continue to scale.

Competitive Landscape

The China finished vehicle logistics market is moderately consolidated, with competition shaped by OEM-linked logistics arms, domestic road and rail specialists, and international 3PLs. OEM-captive players hold an advantage in dedicated export support because they can align fleet planning, shipment timing, and vehicle availability more closely with their parent manufacturers. That makes the competitive field tougher for independent operators, especially on routes where export access and vessel coordination are becoming more important than price alone. Domestic specialists still hold defensible positions in inter-provincial road haulage and rail-linked vehicle moves because these segments depend on dense operating networks and local execution discipline. As a result, the China finished vehicle logistics market is not dominated by one model, but by several overlapping capabilities that matter in different corridor types.

Another clear shift is that international providers are no longer competing only on transport scale. They are focusing more on factory-linked logistics, aftermarket control, compliance management, and technology-led visibility. DSV completed its acquisition of Schenker in April 2025, which created a much larger transport and logistics platform and strengthened its ability to serve complex automotive accounts. DHL was selected by NIO in February 2026 as its European finished vehicle aftermarket logistics partner, with an operating model that combines storage, distribution, and customs support through its Automotive Campus in Holtum. Kuehne+Nagel also signed an agreement to support Changan Automobile’s development in Europe, which reflects how cross-border vehicle programs increasingly depend on integrated logistics support rather than isolated transport tasks.

The China finished vehicle logistics market is also being influenced by strategic moves that sit just outside pure finished vehicle line-haul, but still shape competitive reach. Nippon Express launched NX Branded Containers in partnership with SITC in late 2025 and announced the move in early 2026, showing how providers are building broader regional logistics tools that can support automotive and related cargo flows. OEM-linked operators continue to build tighter control over export execution, while global 3PLs try to win where compliance, digital orchestration, and aftermarket support matter most. That means the China finished vehicle logistics market will likely keep moving toward a structure in which scale still matters, but contract quality increasingly depends on visibility, specialization, and corridor integration.

China Finished Vehicle Logistics Industry Leaders

Changjiu Logistics Co., Ltd.

China Railway Special Cargo Logistics Co., Ltd.

Sinotrans Limited

COSCO Shipping Logistics Co., Ltd.

SAIC Motor Transportation and Logistics Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Foton Motor and COSCO Shipping inaugurated their joint venture, Guangzhou Yuanfu Automotive Supply Chain, on March 26. The event coincided with the delivery of an LNG dual-fueled PCTC and the export of 600 Foton pickup trucks to South America. This venture not only creates a controllable maritime supply chain for Foton but also serves as a model for other Chinese OEMs eyeing dedicated ocean capacity.

- March 2026: DSV and NIO cemented a comprehensive logistics partnership at a ceremony in Hefei. This collaboration centers on NIO's advanced manufacturing facilities, marking a pivotal move in DSV's ambition to lead the logistics segment of the smart EV industry, both in China and on the global stage.

- February 2026: NIO selects DHL as European finished vehicle aftermarket logistics partner. Operating from DHL's Automotive Campus in Holtum, Netherlands, DHL manages storage, distribution, and customs clearance for NIO's premium models and Firefly brand across Northwestern Europe, combining DHL Supply Chain, Global Forwarding, and DHL Freight in an integrated automotive campus model.

- February 2026: Nippon Express Holdings launched "NX Brand Containers" in partnership with SITC International Holdings. The initiative expanded NX China's branded container offering on Asian sea lanes, supporting automotive and general cargo flows.

China Finished Vehicle Logistics Market Report Scope

| Transportation | Road |

| Air | |

| Sea and Inland Waterways | |

| Rail | |

| Warehousing and Distribution | |

| Value-added Services and Others |

| Domestic | |

| International | Import/Inbound |

| Export/Outbound |

| Passenger Vehicles (Including Two and Three-Wheelers) |

| Commercial Vehicles |

| Off-Highway Vehicles |

| OEMs |

| Dealers |

| Others (Rental Companies, Fleet leasing companies, Government and Defense Fleets, etc.) |

| North |

| Northeast |

| East |

| Central |

| South |

| Southwest |

| Northwest |

| By Logistics Function | Transportation | Road |

| Air | ||

| Sea and Inland Waterways | ||

| Rail | ||

| Warehousing and Distribution | ||

| Value-added Services and Others | ||

| By Destination | Domestic | |

| International | Import/Inbound | |

| Export/Outbound | ||

| By Type of Vehicles | Passenger Vehicles (Including Two and Three-Wheelers) | |

| Commercial Vehicles | ||

| Off-Highway Vehicles | ||

| By End-user Industry | OEMs | |

| Dealers | ||

| Others (Rental Companies, Fleet leasing companies, Government and Defense Fleets, etc.) | ||

| By Region | North | |

| Northeast | ||

| East | ||

| Central | ||

| South | ||

| Southwest | ||

| Northwest | ||

Key Questions Answered in the Report

What is the 2031 outlook for finished vehicle logistics in China?

The China finished vehicle logistics market is forecast to reach USD 50.43 billion by 2031, rising from USD 38.75 billion in 2026 at a 5.41% CAGR.

Which segment leads by logistics function?

Transportation was the largest segment with 64.87% revenue share in 2025, while value-added services and others are projected to grow the fastest at 7.16% CAGR through 2031.

Is domestic or international logistics growing faster?

Domestic logistics remained larger with 73.10% revenue share in 2025, but international logistics is growing faster with a projected 6.76% CAGR through 2031.

Which vehicle category drives the most demand?

Passenger vehicles, including two- and three-wheelers, led with 68.81% revenue share in 2025 and also posted the highest projected CAGR at 5.85% through 2031.

Which part of China is strongest for this business?

East China led with 34.03% revenue share in 2025 because of its dense production base and port network, while Southwest China is the fastest-growing region at a 6.71% CAGR.

What is changing competition among logistics providers?

Competition is moving away from basic transport alone and toward integrated services such as visibility, compliance, yard control, customs coordination, and aftermarket support.

Page last updated on: