China Electronics Manufacturing Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

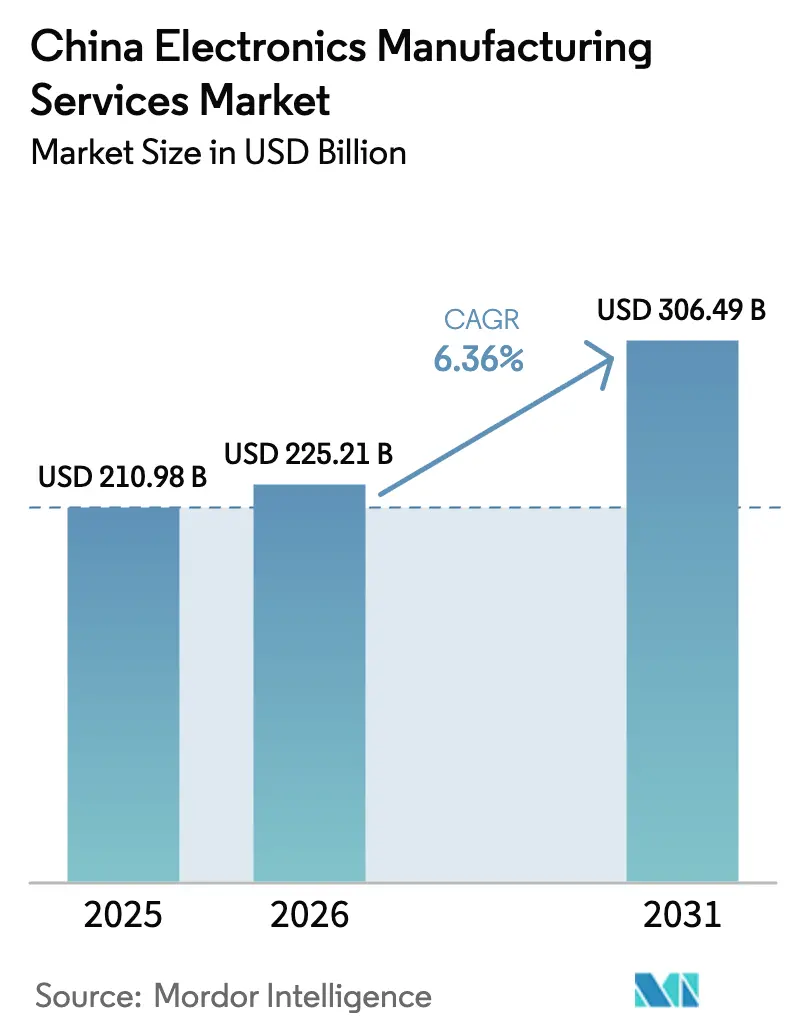

| Base Year Market Size (2025) | USD 210.98 Billion |

| Market Size (2026) | USD 225.21 Billion |

| Market Size (2031) | USD 306.49 Billion |

| Growth Rate (2026 - 2031) | 6.36% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Electronics Manufacturing Services Market Analysis by Mordor Intelligence

China electronics manufacturing services market size in 2026 is estimated at USD 225.21 billion, growing from 2025 value of USD 210.98 billion with projections showing USD 306.49 billion, growing at 6.36% CAGR over 2026-2031. The current expansion is fueled by sovereign technology mandates that prioritize domestic content, rapid capacity additions in high-density interconnect and IC-substrate lines, and a demand pivot from consumer devices toward automotive electronics and humanoid-robot assemblies. Automation is intensifying across every major factory cluster, with more than 30,000 smart factories online by early 2025, embedding collaborative robots, AI-driven optical inspection, and digital twins into PCB, substrate, and box-build workflows. The resulting productivity gains allow top-tier contractors to offset coastal wage inflation that has been rising 8-12% each year. Simultaneously, tight ABF-substrate supply, power-usage quotas, and export controls on sub-7 nm lithography tools are reshaping sourcing strategies, steering the China electronics manufacturing services market toward vertical integration and multi-geography hedging.

Key Report Takeaways

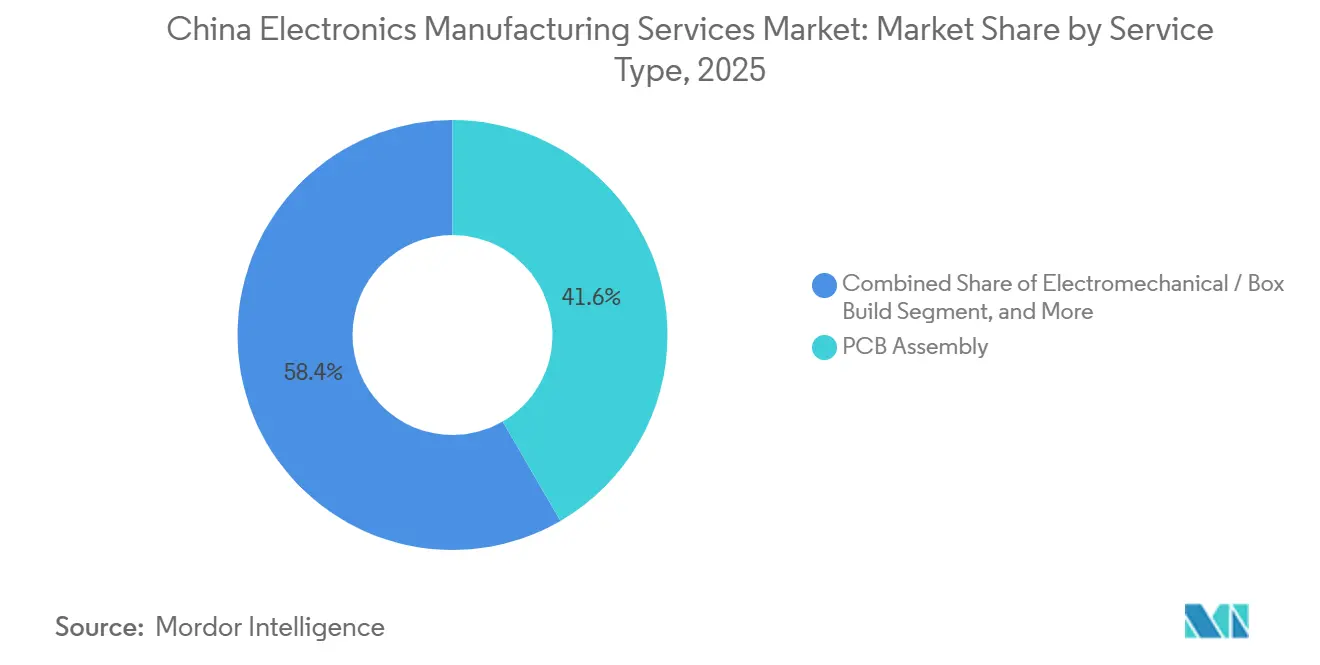

- By service type, PCB Assembly led with 41.63% of the China EMS market share in 2025, while Electromechanical and Box Build services are projected to expand at a 7.39% CAGR through 2031.

- By business model, Contract Manufacturing accounted for 62.19% of the China EMS market share in 2025, whereas Hybrid and Turnkey models are forecast to grow at a 6.89% CAGR through 2031.

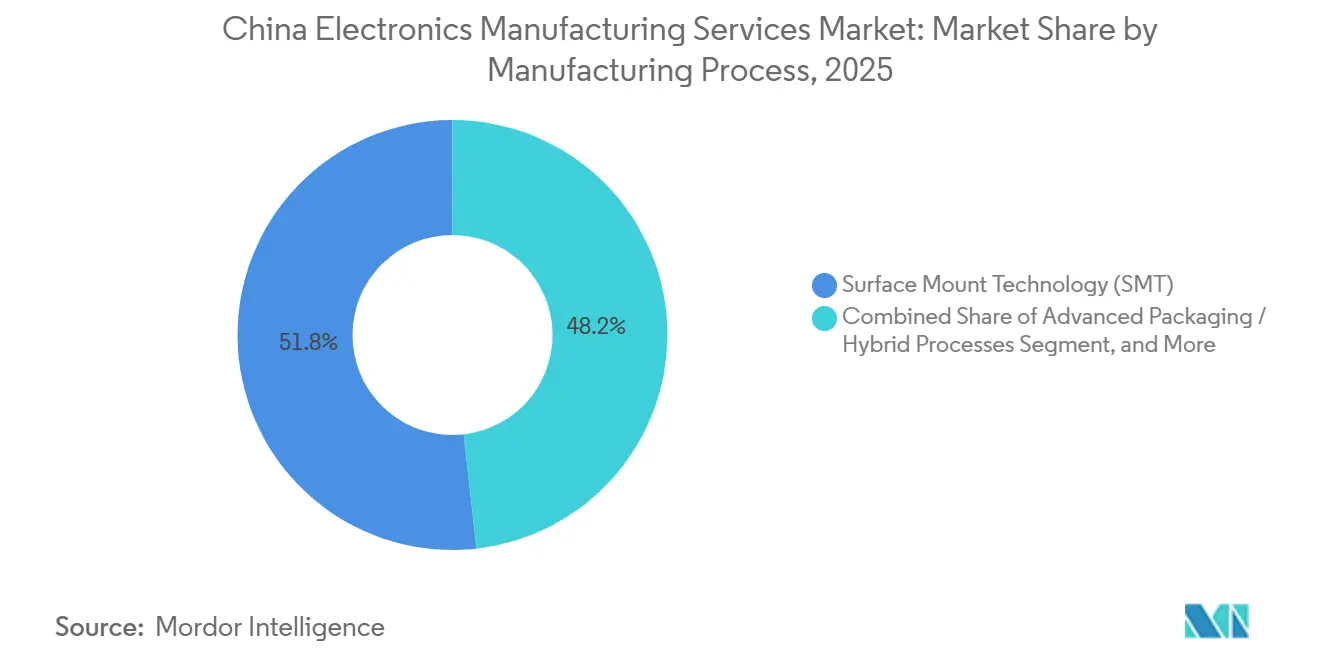

- By manufacturing process, Surface Mount Technology captured 51.78% of the China EMS market share in 2025, while Advanced Packaging and Hybrid Processes are expected to register a 6.94% CAGR over the same period.

- By end-user, Consumer Electronics accounted for 34.66% of the China EMS market share in 2025, yet Automotive electronics are set to advance at an 8.19% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Worldwide, activity is shaped by contributions from multiple countries and regions, with China representing one among them. The global report on electronics manufacturing services market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

China Electronics Manufacturing Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of 5G-Advanced and 6 GHz Device Production | +1.2% | National, with concentration in Guangdong, Jiangsu, Zhejiang clusters | Medium term (2-4 years) |

| Domestic PCB Capacity Upgrade to HDI and Advanced Substrates | +1.4% | National, led by Jiangxi, Guangdong, Jiangsu provinces | Long term (≥ 4 years) |

| Government Incentives for Intelligent Manufacturing Lines | +0.9% | National, early gains in Yangtze River Delta, Pearl River Delta | Medium term (2-4 years) |

| OEM Outsourcing Shift from In-house to ODM Models | +0.8% | National, spillover to Southeast Asia for risk mitigation | Short term (≤ 2 years) |

| Robotics and Humanoid Device Assembly Demand | +0.7% | National, pilot zones in Beijing, Shenzhen, Shanghai | Long term (≥ 4 years) |

| Regional Clusters' Drive for Carbon-Neutral Electronics Plants | +0.5% | National, accelerated in Yangtze River Delta, Pearl River Delta | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of 5G-Advanced and 6 GHz Device Production

China’s early allocation of the 6 GHz band and an ambitious target of 3 million 5G-Advanced base stations by 2027 are already retooling SMT lines for millimeter-wave antenna modules.[1]Ministry of Industry and Information Technology, “5G-Advanced Deployment Roadmap,” miit.gov.cn EMS contractors now integrate tight-impedance RF front-ends and multi-layer flex PCBs, pushing box-build cycle times by 15% while delivering higher average selling prices. Providers with in-house RF test chambers and domestic gallium-nitride substrate supply gain resilience against export-control risks, positioning the China electronics manufacturing services market for premium turnkey contracts.

Domestic PCB Capacity Upgrade to HDI and Advanced Substrates

Investments topping USD 1.1 billion in any-layer HDI and ABF lines have begun easing the 26-30-week substrate bottleneck that constrained AI-server builds in 2024.[2]Zhen Ding Technology, “Annual Report 2024,” zdt.com.tw Mainland plants now support 0.4 mm ball-grid-array pitches, necessary for chiplet architectures, providing EMS operators with locked substrate allocations and margin insulation. Automated optical inspection and X-ray laminography have reduced field-failure rates to below 50 ppm, reinforcing quality leadership in the China electronics manufacturing services market.

Government Incentives for Intelligent Manufacturing Lines

Central and provincial programs reimbursing up to 30% of robot and vision system capex have reduced collaborative robot payback periods to under 18 months.[3]Jiangsu Provincial Government, “Automation Capex Subsidy Program,” jiangsu.gov.cn Mandatory data-interoperability rules also funnel real-time utilization metrics to government dashboards, favoring EMS providers with mature MES layers. Smaller firms facing compliance costs are ceding share, accelerating consolidation in the China electronics manufacturing services market.

OEM Outsourcing Shift from In-House to ODM Models

Smartphone brands outsourced more than 60% of production in 2025, up from 45% three years earlier. ODM contractors shoulder inventory risk but capture design margins on mechanicals, antennas, and thermal systems, lifting EMS gross profit 200-300 basis points. Automotive suppliers are replicating this model for battery-management systems, expanding the total addressable market for China's electronics manufacturing services.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Skilled-Labour Costs in Coastal Provinces | -0.9% | Guangdong, Jiangsu, Zhejiang, Shanghai | Short term (≤ 2 years) |

| Persistent Chip Supply Controls on above 7 nm Tools | -0.7% | National, acute in advanced logic and AI-chip segments | Long term (≥ 4 years) |

| Tight Supply of AI-Grade ABF Substrates | -0.6% | National, spillover to Taiwan and Southeast Asia | Medium term (2-4 years) |

| Power-Usage Quotas in Key Industrial Parks | -0.4% | Guangdong, Jiangsu, Zhejiang industrial zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Skilled-Labor Costs in Coastal Provinces

Average electronics wages in Shenzhen climbed to CNY 110,000 (USD 15,200) in 2024, narrowing China’s cost gap against Malaysia and Vietnam. Leading manufacturers are relocating through-hole insertion and manual inspection to inland provinces such as Henan and Sichuan, where pay scales remain 30% lower, yet this dispersion stretches logistics lead times and complicates just-in-time flows across the China electronics manufacturing services market.

Persistent Chip Supply Controls on above 7 nm Tools

Domestic foundries remain constrained by limited access to EUV lithography, keeping yields on 7 nm lines below 50%. EMS firms consequently redesign boards for mature-node silicon, which expands layer counts and raises thermal load. Dual supply chains, import-based for export products and domestic-based for local brands, reduce economies of scale, weighing on margins in the China electronics manufacturing services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Electromechanical and Box Build Ascend on Humanoid Demand

Electromechanical Assembly and Box Build revenue is growing at 7.39%, outpacing the 6.36% CAGR of the China electronics manufacturing services market. The gain is anchored in multi-stage integration for humanoid-robot frames and automotive battery enclosures. PCB Assembly still delivered 41.63% of 2025 revenue, yet commoditization compresses margins. Tier 1 suppliers run dedicated new-product-introduction hubs that shrink prototype-to-mass-production windows to under 90 days, capturing follow-on contracts and stabilizing the size of the China electronics manufacturing services market for new builds.

Higher-margin Engineering Services covering design-for-manufacturability and failure-mode analysis now accompany every large ODM award. Test and Development Implementation revenues ride the proliferation of Wi-Fi 7 and ultra-wideband modules that demand chamber-level RF validation. Logistics Services integrate inbound sequencing and outbound dropshipping, cutting customer working capital and heightening stickiness. Repair, refurbishment, and end-of-life recycling, though small today, are advancing as extended producer responsibility laws mature, adding optionality to the China electronics manufacturing services market.

By Business Model: Hybrid Turnkey Structures Unlock Design Value

Contract Manufacturing retained a 62.19% share in 2025, but Hybrid and Turnkey structures are growing by 6.89% as OEMs shift engineering and procurement risk. Original Design Manufacturing now dominates the mid-tier smartphone market, enabling Huaqin and Wingtech to capture 15-20% of a device’s BOM as design income. The China electronics manufacturing services market share for turnkey engagements is rising fastest in automotive subsystems, where sourcing complexity and homologation hurdles exceed wage-based cost considerations.

Hybrid deals blend consignment assembly for legacy SKUs with ODM for new categories, smoothing revenue swings and lifting blended gross margins. Providers must carry higher inventories and extend working-capital cycles by 60-90 days, but improved utilization and platform reuse lift return on invested capital. As customers seek supply security, turnkey penetration will keep rising in the China electronics manufacturing services market.

By Manufacturing Process: Advanced Packaging Captures AI Workloads

Surface-mount lines accounted for 51.78% of 2025 process revenue, yet chiplet-ready packages are growing at a 6.94% CAGR, led by any-layer HDI, fan-out wafer-level, and embedded-die substrates. Recent capacity launch in Jiangxi adds 200,000 m² of ABF panels, alleviating server delays triggered by 2024 substrate shortages. The China electronics manufacturing services market for advanced packaging is expanding as EMS plants integrate wafer-level bump, board-level attach, and optical co-package assembly under one roof.

Through-hole technology remains indispensable for industrial drives and automotive power electronics that prioritize ruggedness over miniaturization, accounting for roughly 15% of 2025 revenue. Hybrid processes combining SMT, THT, and wire bonding command premium pricing in medical and automotive builds where ISO 13485 and IATF 16949 compliance are non-negotiable. Mastering such mixed processes cements long-term contracts in the China electronics manufacturing services market.

By End-User: Automotive Electronics Overtakes Smartphones in Growth

Consumer Electronics still provided 34.66% of 2025 EMS revenue, but unit shipments have plateaued as replacement cycles lengthen. Automotive demand, propelled by 9.5 million new-energy vehicle sales in 2024 and expanding at an 8.19% CAGR, is reshaping factory layouts around IP-rated enclosures and functional-safety testing. The China electronics manufacturing services market size advantage emerges in battery-management systems, domain controllers, and infotainment head units that require higher power densities and longer qualification cycles.

Mobile device assembly remains substantial, yet growth shifts toward AI-capable premium tiers. Computers and AI-PCs are trending up, with neural processing units raising average BOM values by 15%. Industrial controls, communication equipment, medical gear, and smart lighting each contribute steady, lower-volatility demand that blends into a balanced customer portfolio for the China electronics manufacturing services market.

Geography Analysis

Three coastal mega-clusters, Pearl River Delta, Yangtze River Delta, and Bohai Rim, generated more than 75% of China electronics manufacturing services market revenue in 2025. Shenzhen and Dongguan alone accounted for 44% as large campuses benefited from Hong Kong logistics and deep supplier pools. Rising wages prompted migration of labor-intensive stages to Henan and Sichuan, where inland subsidies cover up to 20% of automation capex.

The Yangtze River Delta excels in substrates and advanced packaging, hosting Kunshan-Suzhou corridors fed by engineering talent from Fudan and Zhejiang universities. Bohai Rim contributes high-reliability builds for aerospace and defense, leveraging Beijing’s R&D institutions. Western provinces remain peripheral because of logistics lead times, though hydro-powered Sichuan and Chongqing are attracting server and tablet lines with 15% lower energy costs.

Offshore diversification layers onto, rather than replaces, domestic investment. Vietnamese and Indian plants received more than USD 5 billion combined EMS inflows in 2024, yet Foxconn and Luxshare simultaneously expanded Zhengzhou and Kunshan, evidencing a China-plus-one stance that preserves the core supplier ecosystem while meeting customer mandates for geopolitical resilience. This dual-track structure increases capital intensity while keeping the China electronics manufacturing services market at the heart of global electronics value chains.

Mordor Intelligence provides coverage of the electronics manufacturing services market across other key regional markets, including Europe, Asia, and North America, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to Vietnam, India, Germany, United States, Thailand, and Singapore incorporating local coverage and market participation, as required.

Competitive Landscape

The China electronics manufacturing services arena remains moderately concentrated, with the ten largest contractors accounting for roughly 55% of industry revenue. Scale enables these incumbents to secure favorable component pricing, fund robotics and AI inspection deployments, and maintain mid-single-digit operating margins even as commodity contracts tighten. Hon Hai Precision, Luxshare Precision, BYD Electronic, Quanta Computer, Compal Electronics, Pegatron, Wistron, Inventec, Wingtech Technology, and Flex dominate the customer roster, yet no single firm holds an overwhelming position, preserving room for specialized rivals.

Strategic investment increasingly revolves around vertical integration and geographic hedging. Hon Hai committed USD 1 billion to expand its Zhengzhou campus for server and automotive boards, and it is spending an additional USD 500 million in Shenzhen to launch a humanoid-robot line. Luxshare bought Catcher Technology’s metal-chassis assets and opened a USD 330 million Vietnam complex to diversify production risk, while Wingtech is channeling USD 400 million into Nexperia’s silicon-carbide wafers to lock in power-device supply for electric-vehicle programs. Zhen Ding Technology’s USD 1.1 billion substrate plant in Jiangxi illustrates how component capacity moves up the EMS value chain, providing contractors with margin insulation against ABF price swings.

Mid-tier disruptors such as Huaqin Telecom, Longcheer, and Goertek are winning original-design contracts that tier-one providers deem too small, leveraging 90-day prototype cycles and flexible credit terms. Niche specialists focus on medical devices, industrial controllers, and 5G small cells, where ISO 13485 or IATF 16949 certification gates entry and keeps volumes manageable. Technology is the primary differentiator: Foxconn filed more than 1,200 patents on AI defect detection in 2024, whereas smaller firms deploy off-the-shelf vision kits to narrow the gap without heavy R&D. The competitive field is therefore bifurcating into capital-intensive leaders that chase automotive and AI substrates and agile regional players that survive on high-mix, low-volume assemblies, collectively shaping a dynamic but balanced market.

China Electronics Manufacturing Services Industry Leaders

Hon Hai Precision Industry Co., Ltd.

BYD Electronic (International) Company Limited

Luxshare Precision Industry Co., Ltd.

Wingtech Technology Co., Ltd.

Shanghai Huaqin Telecom Technology Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Hon Hai Precision confirmed a USD 500 million expansion of its Shenzhen campus to mass-produce humanoid robots targeting 10,000 units annually by 2027.

- December 2025: Luxshare Precision finished its USD 330 million Vietnam complex, adding 500,000 sq ft of cleanrooms for AirPods and watch modules.

- November 2025: Zhen Ding Technology began volume shipments from its USD 1.1 billion Jiangxi IC-substrate plant, delivering any-layer HDI and ABF panels for AI-server modules.

- October 2025: BYD Electronic secured an USD 800 million multi-year contract to supply battery-management systems and on-board chargers for a European automaker.

China Electronics Manufacturing Services Market Report Scope

The China Electronics Manufacturing Services Market Report is Segmented by Service Type (Electronics Manufacturing Services, Engineering Services, Test and Development Implementation Services, Logistics Services, Other Service Types), Business Model (Contract Manufacturing (CM), Original Design Manufacturing (ODM), Hybrid / Turnkey / Other Business Models), Manufacturing Process (Surface Mount Technology (SMT), Through-Hole Technology (THT), Advanced Packaging / Hybrid Processes), End-user (Mobile Devices, Consumer Electronics, Computer, Industrial, Automotive, Communication, Lighting, Medical, Other End-users). The Market Forecasts are Provided in Terms of Value (USD).

| Electronics Manufacturing Services | PCB Assembly |

| Electromechanical Assembly/Box Build | |

| Prototyping | |

| Other Electronics Manufacturing Services | |

| Engineering Services | |

| Test and Development Implementation Services | |

| Logistics Services | |

| Other Service Types |

| Contract Manufacturing (CM) |

| Original Design Manufacturing (ODM) |

| Hybrid / Turnkey / Other Business Models |

| Surface Mount Technology (SMT) |

| Through-Hole Technology (THT) |

| Advanced Packaging / Hybrid Processes |

| Mobile Devices (Smartphones and Tablets) |

| Consumer Electronics |

| Computer (PCs/Desktop/Laptops) |

| Industrial |

| Automotive |

| Communication |

| Lighting |

| Medical |

| Other End-users |

| By Service Type | Electronics Manufacturing Services | PCB Assembly |

| Electromechanical Assembly/Box Build | ||

| Prototyping | ||

| Other Electronics Manufacturing Services | ||

| Engineering Services | ||

| Test and Development Implementation Services | ||

| Logistics Services | ||

| Other Service Types | ||

| By Business Model | Contract Manufacturing (CM) | |

| Original Design Manufacturing (ODM) | ||

| Hybrid / Turnkey / Other Business Models | ||

| By Manufacturing Process | Surface Mount Technology (SMT) | |

| Through-Hole Technology (THT) | ||

| Advanced Packaging / Hybrid Processes | ||

| By End-user | Mobile Devices (Smartphones and Tablets) | |

| Consumer Electronics | ||

| Computer (PCs/Desktop/Laptops) | ||

| Industrial | ||

| Automotive | ||

| Communication | ||

| Lighting | ||

| Medical | ||

| Other End-users |

Key Questions Answered in the Report

How large is the China electronics manufacturing services market in 2026?

The market generated USD 225.21 billion in 2026 and is projected to reach USD 306.49 billion by 2031.

What CAGR is forecast for China’s EMS sector through 2031?

A compound annual growth rate of 6.36% is expected during 2026-2031.

Which service category is growing fastest inside China’s EMS ecosystem?

Electromechanical and Box Build services are advancing at 7.39% a year, buoyed by automotive electronics and humanoid-robot assembly.

Which end-user segment offers the strongest growth opportunity?

Automotive electronics are expanding at an 8.19% CAGR, benefiting from surging new-energy vehicle production.

How are wage increases affecting EMS providers?

Coastal wage inflation of 8-12% is driving relocation of labor-intensive stages inland and accelerating factory automation investments to preserve margins.

What is the competitive intensity of China’s EMS landscape?

The top 10 firms command roughly 55% of revenue, giving the market a moderate concentration level while leaving room for niche specialists.

Page last updated on: