China Cutting Machine and Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

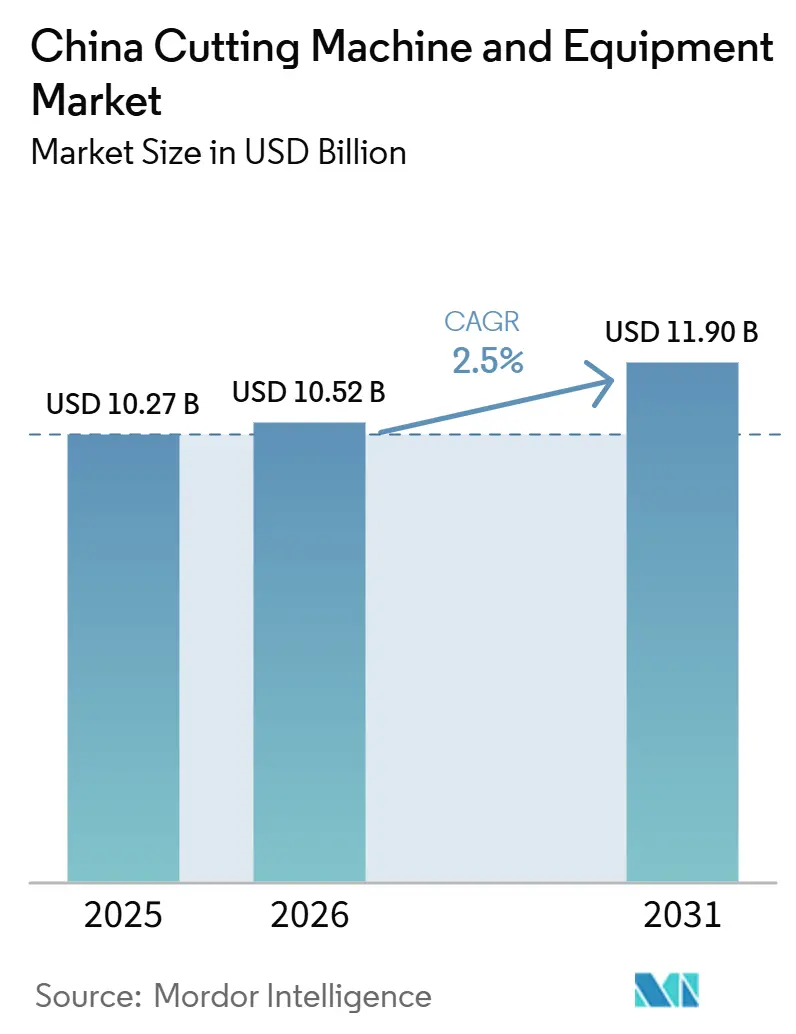

| Base Year Market Size (2025) | USD 10.27 Billion |

| Market Size (2026) | USD 10.52 Billion |

| Market Size (2031) | USD 11.90 Billion |

| Growth Rate (2026 - 2031) | 2.50% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Cutting Machine and Equipment Market Analysis by Mordor Intelligence

The China Cutting Machine and Equipment Market size is expected to grow from USD 10.27 billion in 2025 to USD 10.52 billion in 2026 and is forecast to reach USD 11.90 billion by 2031 at 2.5% CAGR over 2026-2031.

Industry trends suggest that equipment upgrades are becoming an important growth driver alongside new equipment installations, as mid-range fiber laser systems and automated CNC platforms continue to replace lower-value plasma and oxy-fuel machines. China’s manufacturing value-added reached CNY 34.7 trillion (USD 5.0 trillion) in 2025, while equipment manufacturing grew 9.2%, supporting a strong equipment investment base for the market. The standard equipment segment remains highly competitive, while premium segments increasingly favor suppliers with strong technology and service capabilities. The main operating risks remain dependence on imported high-end optical and motion components and a shortage of skilled smart manufacturing workers, with demand for such workers expected to exceed 31 million by 2035, and nearly half of that need is currently unmet. Companies that can localize more core components and pair them with application engineering, automation, and service support are well-positioned to capture a larger share of new spending as the market moves toward higher-precision applications.

Key Report Takeaways

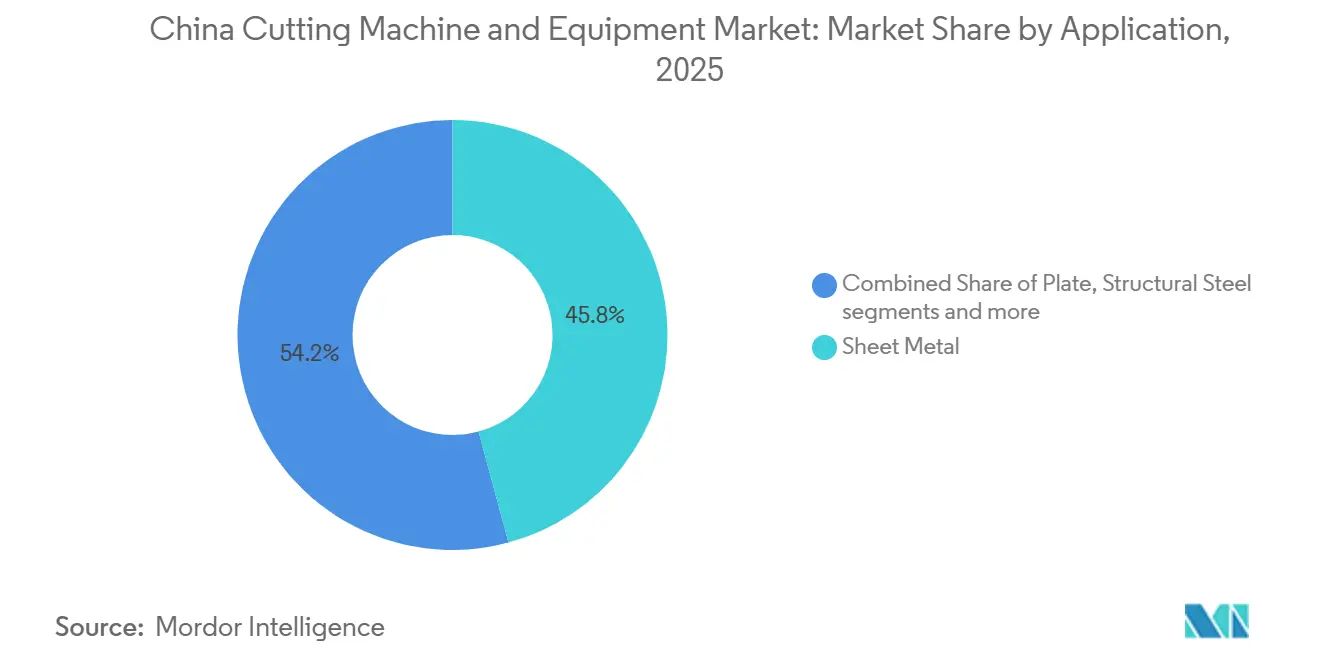

- By application, sheet metal held 45.8% of the China cutting machine and equipment market share in 2025, while structural steel is projected to expand at a 3.2% CAGR through 2031.

- By technology, laser accounted for 47.5% of the China cutting machine and equipment market size in 2025 and is also forecast to grow at the fastest 4.1% CAGR through 2031.

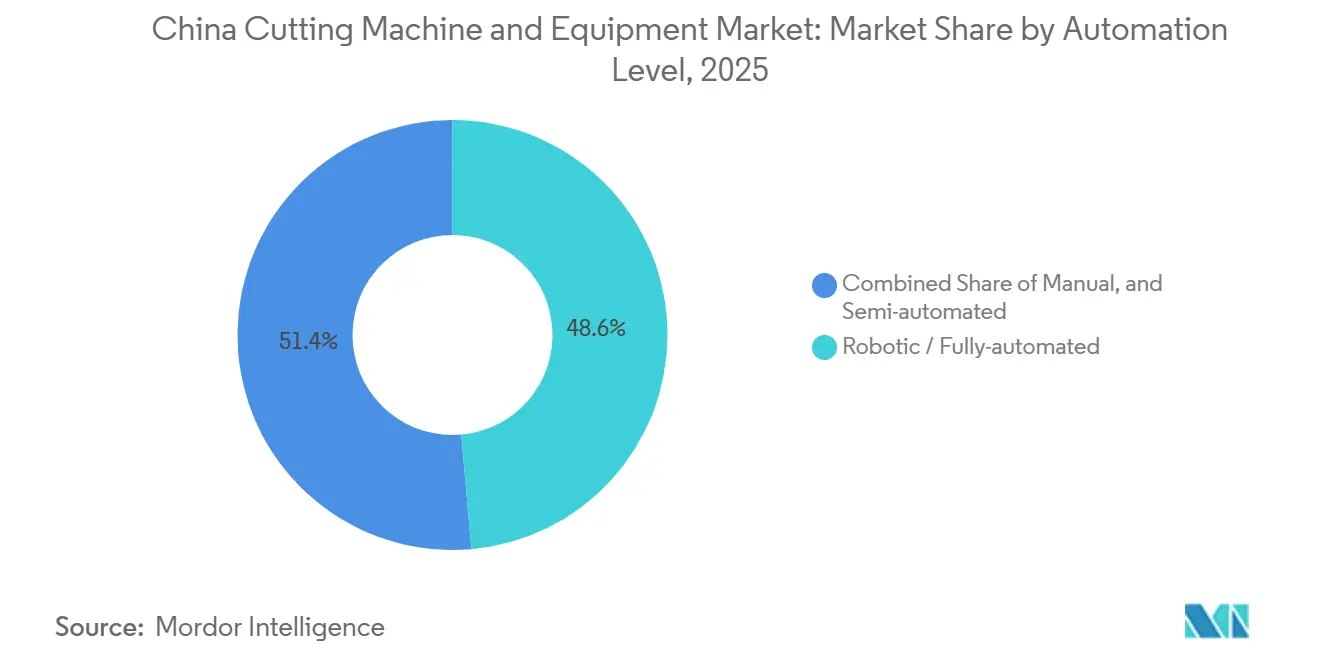

- By automation level, robotic/fully automated segment captured 48.6% of the China cutting machine and equipment market share in 2025 and are projected to advance at a 4.5% CAGR through 2031.

- By end-user industry, automotive accounted for 24.8% of the China cutting machine and equipment market in 2025, while electrical & electronics is expected to record the highest 4.3% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China Cutting Machine and Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of Domestic Manufacturing and Industrial Production | +1.2% | National, with the highest intensity in Jiangsu, Guangdong, Shandong, and Zhejiang | Short term (≤ 2 years) |

| Growth In Automotive, Electronics, and Machinery Industries | +1.0% | Jilin, Hubei, Guangdong for automotive, Jiangsu, and Guangdong for electronics | Short term (≤ 2 years) |

| Increasing Adoption of Automated CNC Cutting Systems | +0.9% | National, with a stronger pull in smart manufacturing zones | Medium term (2-4 years) |

| Rising Demand For Fiber Laser and High-Precision Cutting Technologies | +0.8% | Hubei and the Yangtze River Delta | Short term (≤ 2 years) |

| Government Support for Advanced Manufacturing and Industry Upgrades | +0.7% | National, with early concentration in Beijing, Shanghai, Shenzhen, and Wuhan | Medium term (2-4 years) |

| Growth In Metal Fabrication and Export-Oriented Production | +0.6% | Coastal provinces, including Guangdong, Zhejiang, Fujian, and Jiangsu | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Domestic Manufacturing and Industrial Production

China’s manufacturing base continued to expand in 2025, with value-added output reaching CNY 34.7 trillion (USD 5.0 trillion) and keeping the country in the top global position for the 16th straight year. Industrial output rose 5.9% in 2025, while equipment manufacturing grew 9.2%, indicating that capital goods demand outpaced the broader industrial trend. Industrial robot output increased 28%, and 3D printing equipment output rose 52.5% in 2025, pointing to a broader upstream investment cycle in factory equipment and tooling. More than 8,200 factories had reached advanced-level smart factory certification by the end of 2025 under MIIT’s tiered program, meaning that a larger installed base is now operating with more demanding precision and integration requirements.[1]Ministry of Industry and Information Technology Equipment Industry Development Centre, “2025 Industrial and Informatisation Development Key Targets and Tasks Smoothly Completed,” MIIT-EIDC, miit-eidc.org.cn In practice, this raises replacement demand in the China cutting machine and equipment market, as certified facilities tend to replace older plasma and oxy-fuel lines with fiber laser cells and higher-control CNC systems. This provides a more stable baseline demand for the cutting machine and equipment market.

Growth in Automotive, Electronics, and Machinery Industries

China produced 34.5 million vehicles in 2025, and new energy vehicle sales reached 16.5 million units, up 28.2% year on year, keeping automotive production as one of the largest sources of demand for the China cutting machine and equipment market. Automotive manufacturing value-added rose 11.5% in 2025, while computer, communication, and electronics manufacturing increased 10.6%, both clearly ahead of the broader industrial average. These sectors purchase cutting systems not only for new production lines but also for retrofits within existing plants where tolerance demands have tightened. Battery housings, busbars, motor covers, and power electronics parts require cleaner edges and more repeatable cuts than older plasma systems can usually deliver at scale. Han’s Laser reported 197% growth in its automotive electronics segment in 2025, underscoring the strong overlap between automotive and electronics, which is driving equipment demand. As a result, the market is supported by new manufacturing investments and accelerated replacement of older equipment.

Increasing Adoption of Automated CNC Cutting Systems

The digital transformation plan for the machinery sector, issued in August 2025, calls for the broad adoption of digital and intelligent technologies and targets the build-out of 200 or more excellent-level intelligent factories by 2027.[2]SESEC, “China’s Blueprint for Digital Transformation in Machinery (2025-2030),” SESEC, sesec.eu That policy direction favors automated CNC cutting systems because intelligent factories depend on stable data capture, repeatable path control, and connected production cells. The equipment development update also shows that China completed its 2025 industrial and informatization targets smoothly, which supports the case for continued equipment localization and higher automation intensity. China’s mid-range CNC localization rate rose from 62.6% to 73.5% over the past decade, while the high-end segment remained at around 15% domestic, leaving a large opening for further local upgrading.[3]US-China Economic and Security Review Commission, “Made in China 2025, Evaluating China’s Performance,” USCC, uscc.gov The gap between mid-range success and high-end dependence is important for the China cutting machine and equipment market because it keeps investment focused on better controls, motion systems, and integrated automation. It also means that policy support and procurement preferences are likely to keep pulling buyers toward automated domestic platforms even when technical parity remains incomplete in the top tier.

Rising Demand for Fiber Laser and High-Precision Cutting Technologies

The shift from CO₂ and plasma systems to fiber laser platforms is one of the clearest changes in the China cutting machine and equipment market. In April 2026, Raycus announced large-scale mass production of a 220 kW ultra-high-power industrial continuous fiber laser, with a planned monthly capacity of 50 units, for new energy, aerospace, and shipbuilding applications. This development expands domestic capabilities in applications that previously relied on imported high-performance laser sources. Han’s Laser reported that high-power equipment sales rose 30.5% in 2025, and its general industrial laser equipment segment generated CNY 6.1 billion (USD 871.2 million) in revenue, which confirms that buyers are moving toward higher-value laser systems. China aims to strengthen its position in advanced machine tools by 2035 through continued technological development and localization efforts. This keeps the China cutting machine and equipment market aligned with premium applications where edge quality, speed, and process stability carry more weight than low upfront price alone.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost Of Advanced Laser Cutting Equipment | -0.5% | National, most pronounced in mid-scale job shops and SME metal fabricators | Long term (≥ 4 years) |

| Dependence On Imported High-End Components | -0.4% | National, with import sourcing concentrated in Guangdong, Shanghai, and Beijing logistics hubs | Long term (≥ 4 years) |

| Intense Competition And Price Pressure Among Domestic Manufacturers | -0.3% | National, most severe in Shandong, Jiangsu, and Guangdong, mid-range equipment clusters | Short term (≤ 2 years) |

| Skilled Labor Shortage For Advanced Equipment Operation | -0.3% | National, most acute in the Pearl River Delta and the Yangtze River Delta | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Laser Cutting Equipment

Advanced fiber laser systems still require a significant upfront investment when buyers add motion axes, cutting heads, chillers, software, and automation hardware to build a complete production line. This is especially relevant for small and mid-sized fabricators, as many can justify the productivity gains but still struggle to absorb the initial capital burden in a single purchase cycle. The recent wave of domestic innovation, including the production of ultra-high-power laser sources and increased R&D spending by leading firms, improves local capability but does not remove the cost hurdle for the full system. Buyers in the China cutting machine and equipment market, therefore, continue to closely weigh payback periods, especially as they move from semi-automated lines to fully integrated robotic cells. That slows adoption in the broad middle of the market even while large accounts keep upgrading. It also helps explain why plasma and other lower-cost technologies remain relevant across several heavy-fabrication use cases.

Dependence on Imported High-End Components

China has made significant progress in laser source localization, but the broader optical and motion chain still relies on imported components in the most demanding applications. China has become much stronger in mid-range CNC equipment, while high-end capabilities still lag behind imports from Japan, Germany, and Switzerland. That gap matters for the China cutting machine and equipment market market because aerospace, premium automotive, and medical-grade applications rely on the most stable cutting heads, beam delivery systems, controls, and servo performance. Raycus’ 220 kW launch shows that domestic firms are pushing forward quickly at the source level, but full-system independence still requires broader progress across adjacent precision components. The long-term outlook also implies that closing this gap remains necessary if China is to move its machine tool sector fully into the world’s advanced tier. Until that happens, import controls and supply friction can still slow premium upgrades inside the China cutting machine and equipment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Sheet Metal Anchors Demand While Structural Steel Adds a New Growth Layer

Sheet metal accounted for 45.8% of the China cutting machine and equipment market share in 2025, making it the largest application segment. Vehicle production of 34.5 million units and growth in electronics manufacturing sustain this demand, as both sectors rely on thin- and medium-gauge precision cutting. Sheet metal remains the largest application segment due to its extensive use in export-oriented manufacturing and domestic assembly operations. New energy vehicle platforms further support demand, requiring tighter dimensional control for battery housings, motor covers, and charging hardware, favoring fiber laser systems for edge quality and repeatability. Machine upgrades in existing plants highlight the overlap of replacement, automation, and precision demand, focusing capital spending on faster, more efficient machines with lower scrap rates. This also strengthens suppliers' ability to sell software, service, and automation add-ons.

Structural steel is projected to register the fastest 3.2% CAGR through 2031, supported by rising use in public buildings, infrastructure, and heavy fabrication. Structural steel processing, though a smaller revenue share, is gaining importance as public works, industrial buildings, and heavy fabrication demand prepared beams, sections, and plates. Unlike sheet metal, this segment involves heavier workpieces, application-specific tolerances, and throughput tied to material thickness and project timing, keeping plasma and heavy-plate laser systems relevant. Structural steel broadens the customer base to construction fabricators, shipyards, and energy contractors, diversifying demand despite uneven order patterns. Inland industrial expansion supports this segment, complementing the precision fabrication core by driving growth in heavier industrial work. Suppliers benefit by offering broad product lines for both high-volume sheet work and structural applications.

By Technology: Fiber Laser Leads the Upgrade Cycle While Other Methods Hold Their Niche

Laser accounted for 47.5% of the China cutting machine and equipment market in 2025 and is also the fastest-growing technology segment, with a projected 4.1% CAGR through 2031. This trend indicates a broader shift toward fiber laser systems, driven by greater energy efficiency, lower operating costs, higher precision, and easier integration into automated production lines. Raycus’ April 2026 mass production of a 220 kW industrial continuous fiber laser highlights rising domestic capability in high-power applications. Han’s Laser reported strong momentum in high-power equipment sales in 2025, indicating a shift toward advanced platforms over older machines. High-end laser adoption is reshaping competition, favoring suppliers with proprietary sources, controls, and application support, shifting the focus from machine price to total productivity and reliability. Key demand comes from automotive electronics, battery systems, machinery, and premium fabricated components, where repeatability and speed are critical. Fiber lasers are increasingly replacing CO₂ systems and driving premium pricing in the upper market segment. Laser technology is the fastest-growing and highest-value segment of the market.

Despite this shift, plasma, waterjet, flame, oxy-fuel, and ultrasonic systems remain relevant, maintaining a diverse technology mix. Plasma is preferred for heavy plate and structural work where high-wattage fiber lasers may not justify the cost. Waterjet is suitable for materials unsuitable for thermal cutting, such as composites and specialty alloys. Flame and oxy-fuel systems are vital for thick heavy fabrication where speed and cost outweigh finish quality. By 2035, premium, precision-driven technologies are expected to gain market share, but older technologies will persist in specific use cases. The China cutting machine and equipment market continues to use multiple technologies depending on material type, thickness, and precision requirements. This ensures technical diversity alongside the growing dominance of laser technology.

By Automation Level: Robotic Systems Hold the Lead as Smart Factory Demand Deepens

The robotic/fully automated segment held 48.6% of the China cutting machine and equipment market share in 2025 and is expected to expand at the fastest 4.5% CAGR through 2031. Their lead reflects stronger demand for connected production cells, sensor-based process control, and smart factory compatibility across large manufacturing sites. This trend indicates a shift in Chinese manufacturing toward interconnected, data-driven equipment over isolated workstations. A 28% rise in industrial robot output in 2025 highlights increased automation in handling, assembly, and processing functions. Advanced smart factory development supports this trend, as automated cutting cells integrate better into digital production environments than manual systems. Purchasing decisions now prioritize uptime, labor efficiency, traceability, and integration value, driving demand for machines with loading systems, software-driven nesting, sensor feedback, and consistent process control. Suppliers linking cutting systems to broader factory automation frameworks benefit significantly. Automation increasingly supports productivity, quality consistency, and manufacturing traceability requirements, solidifying the position of fully automated systems and increasing switching costs for vendors with superior software and services.

Semi-automated systems remain vital for mid-sized fabricators needing flexibility across varied job lots and part shapes without fully adopting robotic setups. These fabricators cater to diverse clients, valuing operator discretion and lower capital costs. Manual systems persist in repair work, low-volume job shops, and smaller inland production hubs where simpler equipment aligns with labor models. However, the market increasingly favors automation, driven by smart factory goals, localization, and quality standards. While manual and semi-automated machines retain niche importance, their role in high-end investments is diminishing. The transition varies depending on skills, finances, and application needs, but factories seeking higher throughput and clearer data are moving toward autonomous setups. This shift distinguishes commodity from premium cutting machine and equipment, strengthening vendors that combine hardware with advanced controls, workflow software, and process engineering. Automation has become an increasingly important purchasing criterion for large industrial manufacturers in the China cutting machine and equipment market.

By End-User Industry: Automotive Anchors Current Demand While Electrical and Electronics Expands Fastest

Automotive accounted for 24.8% of the China cutting machine and equipment market in 2025, making it the largest end-user segment. Electrical and electronics is projected to grow at the fastest 4.3% CAGR through 2031, supported by rising demand for precision-cut components in EV electronics, communication equipment, power systems, and data center infrastructure. This trend indicates the rising need for precision-cut components in consumer electronics, EV power electronics, server hardware, thermal systems, and communication equipment. China’s computer, communication, and electronics manufacturing value-added rose 10.6% in 2025, while electrical machinery increased 9.2%, both above the overall industrial pace. The segment also benefits from the fact that many parts are small, quality-sensitive, and produced in high volume, which aligns with the strengths of fiber lasers and automated CNC systems. In the China cutting machine and equipment market, this is one of the segments where machine capability upgrades can be monetized quickly because higher precision and lower rework directly support customer requirements. Han’s Laser reported 197% growth in its automotive electronics segment in 2025, underscoring how quickly this demand base is scaling in practice. The electrical and electronics segment also benefits from proximity to major production clusters in Guangdong, Jiangsu, and other coastal provinces. That concentration supports dense service networks, faster machine commissioning, and quicker process iteration between suppliers and customers. For the China cutting machine and equipment market, this segment is important because it links high precision with sustained production intensity. It is therefore likely to remain one of the most attractive destinations for premium equipment spending.

Automotive remained the anchor end-user segment in 2025, as China’s vehicle output of 34.5 million units created significant demand across body parts, battery housings, brackets, chassis components, and exhaust systems. The shift toward new energy vehicles adds another layer of complexity, as lighter materials and tighter packaging place greater emphasis on precision cutting and process consistency. Metal fabrication job shops and construction-linked buyers create a broad secondary demand layer that keeps overall machine volumes supported, even though these accounts are usually more price-sensitive. Aerospace and defense remain smaller in revenue but are strategically important because they favor the highest-precision tier and sustain demand for advanced domestic capability. The long-term outlook favors premium cutting applications. However, reliance on imported high-end components indicates further opportunities for localization. Shipbuilding, energy, and power also remain meaningful because they support heavy plate and structural applications that do not always follow the same technology path as electronics. The China cutting machine and equipment market, therefore, relies on a broad end-user mix. Still, its value growth is increasingly concentrated in sectors that reward precision, automation, and system integration. That mix makes the market more resilient because it is not tied to one single downstream sector. It also gives suppliers room to specialize by application depth, service model, and technical capability. For the China cutting machine and equipment market, the result is a demand structure in which automotive provides scale, while electronics and adjacent precision sectors drive the strongest upgrade momentum.

Geography Analysis

The China cutting machine and equipment market is geographically concentrated around a small number of manufacturing and technology corridors, with the Yangtze River Delta acting as the premium demand center. Jiangsu, Zhejiang, and Shanghai combine machinery exports, precision electronics, automotive supply chains, and dense supplier ecosystems, which keep average equipment value higher than in many other regions. Nationally, equipment manufacturing value-added rose 9.2% in 2025, and the strongest provincial clusters continue to absorb a large share of that equipment intensity. The machinery digital transformation plan also targets 200 or more excellent-level intelligent factories by 2027, and many of those projects are expected to be concentrated in the most advanced industrial corridors. For the China cutting machine and equipment market, that means the Yangtze River Delta remains the strongest zone for premium laser systems, automated cells, and software-rich equipment packages.

Guangdong and the Pearl River Delta remain another core zone for the China cutting machine and equipment market because of their export-oriented electronics, appliance, and machinery production base. Buyers in this region tend to value fast throughput, changeover flexibility, and reliable service support because product cycles are shorter and customer requirements shift quickly. Wuhan also holds a special position because the optical valley cluster brings together laser source development, system integration, and technical talent in one place, accelerating product iteration for the broader China cutting machine and equipment market. Raycus’ high-power laser milestone and the wider concentration of photonics capabilities in Hubei support that role.

Western and central provinces such as Sichuan, Chongqing, Shaanxi, and Hunan are gaining relevance as industrial investment moves inland and as manufacturers seek lower operating costs with improving logistics. China’s AI-enabled manufacturing initiatives and machinery digital transformation policies support this industrial expansion. This inland shift matters for the China cutting machine and equipment market because it rewards distributors and service partners that establish coverage before demand reaches full scale. It also broadens the market’s geographic base beyond the older coastal clusters, which should make future demand less concentrated in only a few provinces.

Competitive Landscape

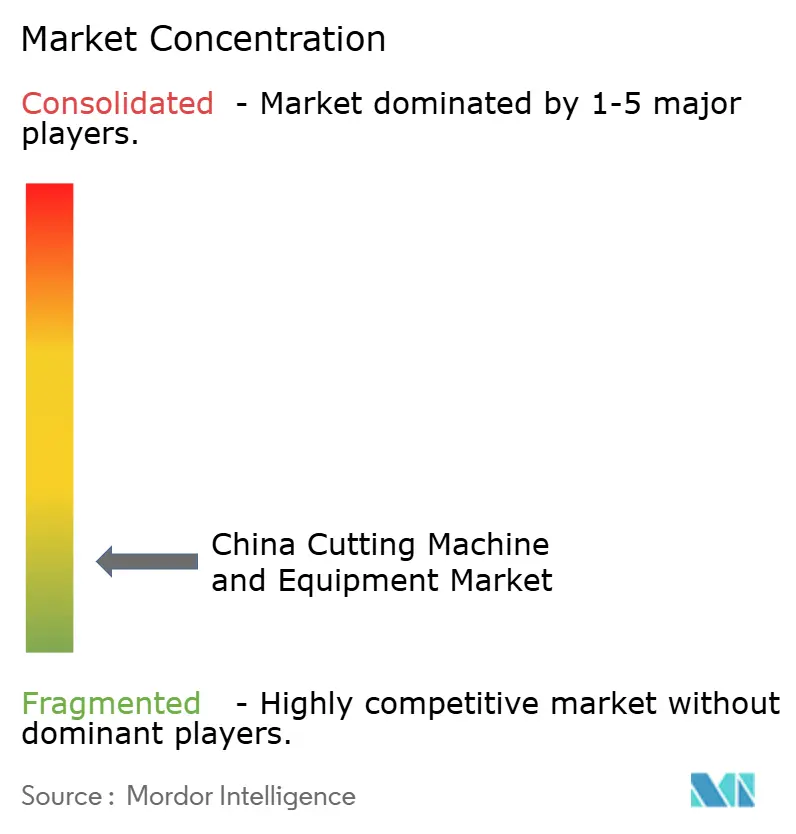

The China cutting machine and equipment market is fragmented, with numerous domestic suppliers competing in the mid-range segment on price, standard configurations, and delivery speed. At the higher end, the China cutting machine and equipment market is becoming more selective, as buyers increasingly prefer vendors that combine laser source capability, controls, software, application engineering, and after-sales support. China’s progress in mid-range localization and continued dependence on imported high-end components support this market split, as they show where local competition is deepest and where technical barriers still matter most. This structure leaves room for large domestic leaders to move upmarket even as smaller firms continue to crowd the entry- and mid-range segments.

Several strategic moves in 2025 and 2026 show how leading firms are trying to widen that gap. Han’s Laser increased R&D spending to CNY 2.1 billion (USD 299.9 million) in 2025, equal to 11.1% of revenue, supporting deeper product development and broader integration capabilities. Raycus began mass production of a 220 kW industrial continuous fiber laser in April 2026, raising the domestic ceiling for high-power applications in the China cutting machine and equipment market. Bodor’s global expansion increases manufacturing scale and strengthens its competitive position in the China cutting machine and equipment market.

Foreign suppliers still play a role in high-precision applications such as aerospace and advanced electronics, where strict quality requirements leave little room for performance variability. Even so, localization goals, domestic standards, and policy-backed digital manufacturing plans are gradually narrowing that opening for the China cutting machine and equipment market. The competitive advantage is therefore shifting toward companies that can meet premium specifications while also demonstrating domestic supply resilience, advanced software capabilities, and responsive after-sales service. In that setting, the China cutting machine and equipment market is likely to remain fragmented in total supplier count but more clearly tiered by technology capability, product quality, and service support.

China Cutting Machine and Equipment Industry Leaders

Han’s Laser Technology Industry Group Co., Ltd.

HGTECH Co., Ltd.

Bodor Laser Co., Ltd.

HSG Laser Co., Ltd.

Jinan G.Weike Science & Technology Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Wuhan Raycus Fiber Laser Technologies has begun mass production of its 220kW ultra-high-power industrial continuous fiber laser, the world's most powerful in its class, with a monthly target of 50 units. The system significantly improves domestic optical supply capabilities and reduces reliance on certain foreign components in high-power cutting applications. This advancement strengthens the domestic capability of Chinese manufacturers in ultra-high-power laser applications.

- April 2026: Bodor Laser has led global laser cutting machine sales for the seventh consecutive year, surpassing 10,000 units in 2025. It remains the only manufacturer to achieve this milestone consistently. The company also expanded manufacturing in Thailand and operates in 180 countries with over 10 overseas subsidiaries and service centers.

- January 2026: Han's Laser releases its full-year 2025 annual report, disclosing record revenue of USD 2.7 billion (CNY 18.7 billion), up 27% year on year, with general industrial laser equipment contributing CNY 6.1 billion (USD 871.2 million). High-power equipment sales grew 30.5%, and new energy equipment sales grew 53.4%, reflecting a surge in cross-sector demand for high-precision laser systems.

China Cutting Machine and Equipment Market Report Scope

The China Cutting Machine and Equipment Market Report is Segmented by Application (Sheet Metal, Plate, Tube & Pipe, Structural Steel, and Others), by Technology (Laser, Plasma, Waterjet, and More), by Automation Level (Manual, Semi-Automated, and Robotic/Fully-automated), and by End-User Industry (Automotive, Aerospace & Defense, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

| Sheet Metal |

| Plate |

| Tube & Pipe |

| Structural Steel |

| Others |

| Laser | Fiber |

| CO₂ | |

| Others | |

| Plasma | High-definition |

| Conventional | |

| Water-Jet | Abrasive |

| Pure | |

| Flame / Oxy-fuel | |

| Ultrasonic & Emerging |

| Manual |

| Semi-automated |

| Robotic / Fully-automated |

| Automotive |

| Aerospace & Defense |

| Electrical & Electronics |

| Construction & Infrastructure |

| Metal-Fabrication Job Shops |

| Shipbuilding |

| Energy & Power |

| Others |

| By Application | Sheet Metal | |

| Plate | ||

| Tube & Pipe | ||

| Structural Steel | ||

| Others | ||

| By Technology | Laser | Fiber |

| CO₂ | ||

| Others | ||

| Plasma | High-definition | |

| Conventional | ||

| Water-Jet | Abrasive | |

| Pure | ||

| Flame / Oxy-fuel | ||

| Ultrasonic & Emerging | ||

| By Automation Level | Manual | |

| Semi-automated | ||

| Robotic / Fully-automated | ||

| By End-User Industry | Automotive | |

| Aerospace & Defense | ||

| Electrical & Electronics | ||

| Construction & Infrastructure | ||

| Metal-Fabrication Job Shops | ||

| Shipbuilding | ||

| Energy & Power | ||

| Others | ||

Key Questions Answered in the Report

What is the outlook for China's cutting machine and equipment in 2031?

The China cutting machine and equipment market is forecast to reach USD 11.90 billion by 2031, rising from USD 10.52 billion in 2026 at 2.50% CAGR.

Which application currently leads demand in China?

Sheet metal processing led with a 45.8% share in 2025, supported by automotive, appliance, electrical enclosure, and battery component production.

Which technology is expanding the fastest?

Laser technology is the fastest-growing segment, with a projected 4.1% CAGR through 2031, driven by precision, energy efficiency, and easier automation.

Why are electrical and electronics buyers becoming more important?

This segment is forecast to grow at a 4.3% CAGR through 2031, driven by high-precision cutting for EV electronics, communication hardware, and dense component manufacturing.

What is the main barrier to wider adoption of advanced systems?

The high upfront system cost remains the biggest practical barrier, especially for smaller fabricators that must fund the full machine, software, and automation package in one go.

What gives leading suppliers an edge in China?

The strongest players combine domestic laser technology, software integration, application engineering, and nationwide service support, which matters more in premium applications.

Page last updated on: