China Customer Data Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

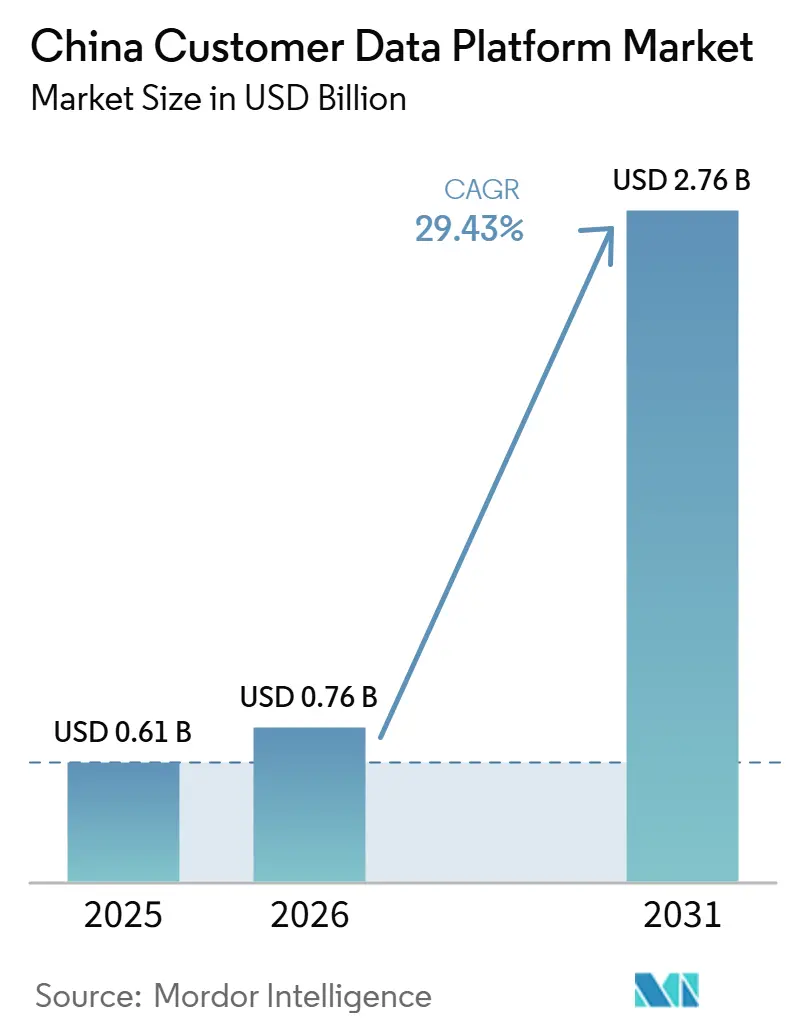

| Base Year Market Size (2025) | USD 0.61 Billion |

| Market Size (2026) | USD 0.76 Billion |

| Market Size (2031) | USD 2.76 Billion |

| Growth Rate (2026 - 2031) | 29.43% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Customer Data Platform Market Analysis by Mordor Intelligence

The China customer data platform market size was USD 0.61 billion in 2025 and is projected to reach USD 2.76 billion by 2031, at a CAGR of 29.43% over 2026-2031. Growth in the China customer data platform market is being shaped by stricter data governance, fragmented customer identities across super apps, and wider use of AI-based customer analytics inside enterprise marketing systems. The market is also moving toward first-party data models because enterprises need stronger consent tracking, cleaner customer records, and better control over how data is activated across sales and marketing channels. Competitive positioning is shifting toward vendors that can support domestic deployment, local cloud partnerships, and direct connectivity with platforms such as WeChat, Alipay, Douyin, and Tmall. Demand is strongest where enterprises need real-time identity resolution, consent management, and campaign execution at scale, which keeps large organizations and digital commerce players at the center of spending. At the same time, the move toward hybrid architectures and more vertical-specific use cases is widening the addressable opportunity across financial services, retail, healthcare, manufacturing, and public sector environments.

Key Report Takeaways

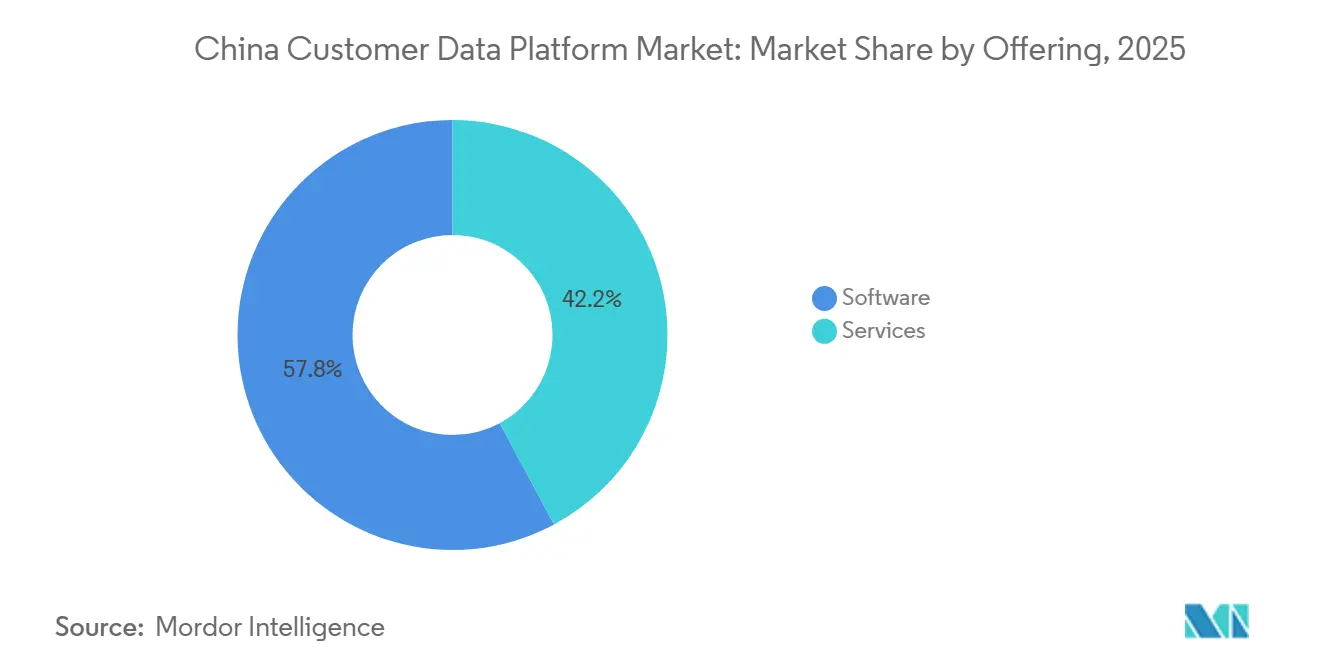

- By offering, software held 57.83% of revenue in 2025, while services scaled with deployment complexity and ongoing optimization demand across the China customer data platform market.

- By deployment mode, cloud remained the leading model in 2025, while hybrid was projected to expand at a 34.91% CAGR through 2031.

- By organization size, large enterprises accounted for 52.69% of revenue in 2025, while small and medium enterprises represented the most significant long-term expansion opportunity as low-code and modular platforms widened adoption.

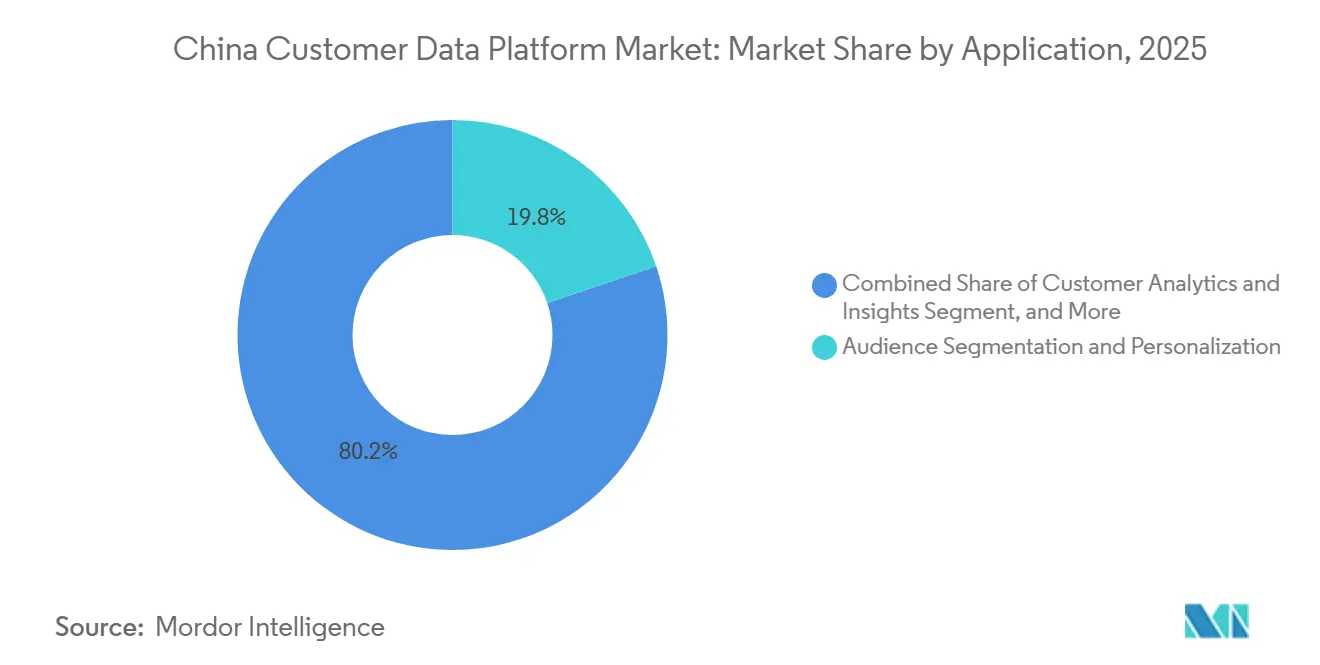

- By application, audience segmentation and personalization remained the largest category in 2025, while customer analytics and insights were projected to advance at a 36.73% CAGR through 2031.

- By end-user industry, retail and e-commerce accounted for 21.37% of revenue in 2025, while BFSI remained the next major demand center because of its scale, compliance requirements, and need for personalized engagement.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China Customer Data Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-Native Real-Time Segmentation | +7.2% | Global, with concentrated impact in Tier-1 Chinese cities including Shanghai, Beijing, and Shenzhen | Medium term (2-4 years) |

| Super-App Data Fragmentation and Identity Resolution | +5.8% | China specific, across all tier cities with strongest effect in coastal e-commerce hubs | Short term (≤ 2 years) |

| PIPL-Driven In-Country Data Residency | +5.5% | National, with concentrated compliance activity in Shanghai, Beijing, and cross-border enterprises | Short term (≤ 2 years) |

| Third-Party Cookie Phaseout and First-Party Data Investment | +3.9% | Global, with faster acceleration in APAC and China | Medium term (2-4 years) |

| Retail Media Monetization and Closed-Loop Customer Graphs | +3.3% | China core, especially Alibaba, JD, and Douyin ecosystems | Medium term (2-4 years) |

| Zero-Copy Warehouse Activation | +2.2% | Global, with early adoption among large enterprises on domestic cloud platforms | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ai-Native Real-Time Segmentation and Next-Best-Action Orchestration

AI-native architecture is pushing the China customer data platform market beyond basic record unification and into active business execution. Vendors are increasingly embedding prediction, recommendation, and workflow automation within the same environment that stores customer data with consent. That shift matters because buyers are no longer evaluating a platform only on storage and integration; they are also judging how quickly it can support churn prevention, repurchase targeting, and campaign refinement. Ping An Group demonstrated the scale of this operating model in 2026, when it said 84% of its business volume was processed through AI-driven automated systems, and that its digital ecosystem served around 90 million monthly active customers.[1]Ping An Group, “Reimagining 250 Million Customer Engagements, Ping An's AI Express Service,” Ping An Group, group.pingan.com In the China customer data platform market, this raises the value of platforms that can connect customer profiles with decision logic, workflow tools, and measurement loops within a single stack. It also strengthens the position of vendors that can localize AI-led use cases around Chinese customer behavior, domestic data rules, and platform-specific interaction patterns.

Social Commerce and Super-App Data Fragmentation Requiring Unified Identity Resolution

The China customer data platform market is expanding because brands in China manage customer identities spread across multiple closed ecosystems. A single consumer can appear under different identifiers across WeChat, Alipay, Douyin, and Tmall, making profile matching a core requirement rather than an optional feature. Weixin Open Platform documentation shows how OpenID and UnionID operate across its ecosystem, which helps explain why identity resolution remains central to platform design.[2]Weixin Open Platform, “User Management, UnionID Documentation,” Weixin Open Platform, developers.weixin.qq.com WeChat Mini Programs continue to act as a major source of consented behavioral data, while Alipay added new data touchpoints after launching its AI-powered assistant Abao in June 2026. South China Morning Post also reported that Douyin, WeChat, and Xiaohongshu were reshaping marketing rules in 2026, which supports the case for stronger customer graph capabilities in the China customer data platform market. This environment favors vendors that maintain certified local connectors and can unify customer activity across multiple walled gardens.

China Pipl-Driven in-Country Data Residency Requirements

Data residency rules have become a direct buying factor in the China customer data platform market, as enterprises now face a more formal compliance framework for personal information. Legal guidance published for 2026 described how the revised Cybersecurity Law aligned more closely with the Personal Information Protection Law and the Data Security Law, which made data governance obligations more coordinated and more visible in procurement.[3]Chambers and Partners, “Data Protection and Privacy 2026, China,” Chambers and Partners, practiceguides.chambers.com The certification regime for cross-border provision of personal information also became effective in January 2026, creating a stricter transfer pathway and raising the cost of moving China-based customer data into global systems. Separate compliance audit rules that took effect in 2025 require organizations processing personal information of more than 10 million individuals to undergo audits every 2 years, which pushed consent logs and traceable governance controls higher on the buying checklist. For the China customer data platform market, this has made domestic deployment and China-resident infrastructure far more important in regulated sectors. International vendors remain relevant, but their position is stronger when they can point to localized cloud arrangements such as Salesforce on Alibaba Cloud.

Third-Party Cookie Phaseout Accelerating First-Party Data Investments

The China customer data platform market is also benefiting from a stronger shift toward first-party data management. Even after Google changed course on some Privacy Sandbox components in late 2025, brands still had to work within privacy limits already set by Apple tracking rules and platform-level restrictions.[4]Consenteo, “Third-Party Cookies in 2026, What Actually Happened After Google's Reversal,” Consenteo, consenteo.com In China, this issue carries added weight because domestic browsers and digital platforms sit outside the Google ecosystem and keep their own customer data rules. China Trading Desk noted in 2026 that app governance changes and platform-side transparency requirements were pushing advertisers and data teams toward first-party audience strategies and cleaner consent chains. That dynamic supports the China customer data platform market because brands need systems that can turn loyalty data, mini-program behavior, and owned-channel signals into addressable customer views. It also makes it harder for enterprises to rely solely on rented audience access, keeping platform investment tied to retention, personalization, and better media efficiency.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration Complexity Across WeChat, E-Commerce, CRM, And Ad-Tech | -3.0% | China specific, with highest friction in Tier-2 and Tier-3 city enterprises with limited IT staffing | Short term (≤ 2 years) |

| Data Localization And Cross-Border Compliance Burden | -2.6% | National, with concentrated impact on multinational enterprises handling cross-border flows | Short term (≤ 2 years) |

| Shortage Of Composable CDP And Reverse-ETL Talent | -2.0% | National, with stronger shortfall in Tier-2 cities and manufacturing-heavy inland provinces | Medium term (2-4 years) |

| Elevated Total Cost Of Ownership For Enterprise-Grade Deployments | -1.7% | Global, with heavier effect on SMEs and mid-market enterprises in China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Integration Complexity Across WeChat, E-Commerce, CRM, and Ad-Tech Stacks

The China customer data platform market still faces a major execution barrier because customer data sits across too many systems with different logic and access rules. Enterprises often need to connect WeChat Work, official accounts, Mini Programs, Tmall stores, JD stores, Douyin shop pages, point-of-sale systems, and internal CRM platforms before they can activate a unified profile. Weixin Open Platform documentation illustrates that even identity handling within a single large ecosystem requires platform-specific understanding, making broader cross-platform unification even harder. This complexity raises implementation cost and slows deployment speed, especially for mid-market users without large internal engineering teams. In the China customer data platform market, vendors that already maintain local connector libraries and China-specific implementation teams are better placed to reduce this friction. The same barrier also creates recurring demand for services, remediation work, and workflow redesign after the initial software purchase.

Data Localization And Cross-Border Transfer Compliance Burden

Cross-border compliance is a constraint in the China customer data platform market because global enterprises often need separate China- and non-China-specific customer data environments. DLA Piper, writing through JD Supra in 2026, described a public penalty for illegal cross-border data transfer activity in 2025, signaling a more active enforcement phase. That enforcement risk raises the cost of maintaining a single global customer view when personal information collected in China may need to remain within a localized instance. The 2026 guidance on China's privacy law and the new certification path both point to a more demanding process for outbound transfers, which makes compliance design part of architecture design. In the China customer data platform market, this tends to slow adoption among mid-sized multinational users because they lack the legal and technical resources available to larger global firms. It also strengthens demand for hybrid and jurisdictionally segregated setups that keep high-value data usable without breaching transfer rules.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Software Leads Revenue While Services Gain Strategic Weight

Software captured 57.83% of the China customer data platform market in 2025, reflecting enterprise preference for packaged platforms that can be configured and updated without rebuilding the underlying system. Buyers increasingly want ready-to-deploy capabilities such as identity stitching, predictive scoring, consent tracking, and audience activation, which keeps software at the center of the spending mix. That pattern is especially evident in the China customer data platform market, where regulated data handling and local connector support both require a stable product architecture. Vendor-managed software also helps enterprises reduce lifecycle complexity when compared with heavily customized internal builds. As a result, the software layer remains the primary revenue driver even when deployment still requires hands-on support.

Services held a smaller share, but their role in the China customer data platform market is becoming more strategic as integration demands increase. Many enterprises need outside support to fix failed rollouts, improve data quality, configure vertical workflows, and operationalize AI-led use cases after the core platform goes live. GrowingIO’s April 2026 capability upgrade, which added multi-entity asset segmentation for property- and vehicle-based grouping, demonstrated that product enhancements often drive service work around data model setup and business rule design. Service revenue also extends beyond implementation because customer journey redesign, consent process tuning, and analytics optimization continue after deployment. This means the China customer data platform industry is not becoming services-led, but service capability remains a clear differentiator for winning and expanding enterprise accounts.

By Deployment Mode: Hybrid Adoption Rises With Governance Demands

Hybrid deployment is the fastest-growing mode in the China customer data platform market and is projected to advance at a 34.91% CAGR through 2031. The appeal of this model lies in its ability to keep sensitive records and consent logs in tightly controlled environments while shifting analytics-intensive tasks to elastic cloud infrastructure. This balance has become more important because many enterprises want performance gains without creating unnecessary exposure around customer data handling. In the China customer data platform market, hybrid architecture also fits organizations that already operate both private and public environments. The model is therefore moving from a niche option into a practical middle path.

Cloud remained the dominant deployment model in 2025, supported by the Alibaba Cloud, Tencent Cloud, and Huawei Cloud ecosystems, which can host localized customer data workloads. Salesforce’s China architecture on Alibaba Cloud is a clear example of how global platforms have adapted to stay relevant in this environment. On-premises deployment still matters in banking, government, and state-owned contexts where internal policy or risk controls limit public cloud use. Even so, the China customer data platform market is moving toward a multi-layered infrastructure, as large enterprises now have more experience running split environments. That shift supports vendors that can offer flexible orchestration across domestic cloud services and internal systems without forcing a full migration in either direction.

By Organization Size: Large Enterprises Hold The Lead While SME Potential Expands

Large enterprises held 52.69% of the China customer data platform market share in 2025, underscoring how strongly scale, data volume, and organizational readiness continue to shape adoption. These buyers entered the market earlier because they faced more urgent needs around customer governance, cross-channel visibility, and enterprise-level automation. Banks, insurers, and top retailers were among the first to invest because fragmented customer data was already affecting service quality and marketing efficiency. In the China customer data platform market, large organizations also had the budget and technical staff needed to absorb long deployment cycles. That combination kept them ahead in both rollout scale and feature depth.

Ping An Group remains one of the clearest examples of this enterprise pattern, with AI-enabled customer engagement serving 250 million retail customers and 90 million monthly active digital users as of early 2026. Small and medium enterprises currently account for a smaller share of the China customer data platform market, but they are becoming more relevant as low-code tools and modular bundles reduce the cost of entry. That change is important because many smaller brands are shifting toward private-domain traffic models built around owned WeChat communities, official accounts, and Mini Programs. Vendors that package easier onboarding and prebuilt WeCom integration are lowering barriers that once confined adoption to the enterprise tier. Over time, this will broaden the user base of the China customer data platform industry, even if revenue remains concentrated among larger accounts in the near term.

By Application: Analytics Growth Builds On An Established Personalization Base

Customer analytics and insights are the fastest-growing application in the China customer data platform market and are projected to rise at a 36.73% CAGR through 2031. This shows that enterprises are moving beyond simple profile unification and looking for tools that can predict behavior, rank audience value, and refine action timing. In practical terms, the application layer is becoming more outcome-focused because buyers want clearer links between customer data and revenue decisions. The China customer data platform market is therefore shifting toward environments where analysis and execution sit much closer together. That favors platforms that can support scoring, recommendation, and performance review within the same operating flow.

Audience segmentation and personalization remained the largest application category in 2025 because Chinese consumers already expect targeted recommendations and lifecycle-based communication across digital channels. Tencent’s enterprise CDP product page shows how customer data, audience selection, journey design, content creation, enterprise WeChat interactions, and analytics are connected within a single product structure. Marketing campaign orchestration is also gaining relevance because buyers want tighter coordination between the customer data layer and delivery systems. Consent and preference management is no longer optional because audit obligations and platform-side transparency requirements keep recordkeeping under scrutiny. As these use cases expand, foundational collection and profile building remain necessary, but they are gradually becoming baseline capabilities rather than the main reason enterprises choose one vendor over another.

By End-User Industry: Retail And E-Commerce Anchor Revenue While Vertical Depth Increases

Retail and e-commerce accounted for 21.37% of the China customer data platform market in 2025, making it the largest end-user segment. This position reflects the intensity of competition across Tmall, JD.com, Douyin Shop, Xiaohongshu, and brand-owned channels, where customer data directly affects targeting, suppression, and loyalty performance. Retail users also have a strong need for closed-loop measurement because they operate across online storefronts, platform media, and offline sales touchpoints. In the China customer data platform market, this keeps commerce-led use cases at the center of product roadmaps. The segment remains the main proving ground for audience activation, journey orchestration, and repeat-purchase programs.

BFSI is the next major demand center because large financial institutions need customer data systems that support personalized engagement, cross-sell, churn prevention, and governance at scale. Ping An’s operating scale shows how far this model has progressed in Chinese financial services. Healthcare and life sciences use similar capabilities for patient engagement and adherence support, though more sensitive data handling often keeps deployment in private or on-premises settings. Industrial manufacturing is also emerging in the China customer data platform market through use cases for after-sales service and dealer networks, while APEX Technologies positions its Nexus CDP for enterprise scenarios that extend beyond traditional retail marketing. This broadening demand base means the market is still led by retail, but future expansion increasingly depends on how well vendors adapt product logic to sector-specific workflows and compliance needs.

Geography Analysis

East China remains the most developed zone in the China customer data platform market because it combines high enterprise density, strong digital commerce activity, and a strong concentration of technology and software decision-makers. Shanghai continues to anchor the mainland presence of many global enterprise software providers, while Hangzhou remains closely linked to Alibaba’s cloud and commerce ecosystem. The region supports some of the most mature deployments because financial institutions, fashion brands, FMCG companies, and major online retailers all operate there at scale. The China customer data platform market is therefore most commercially established in this eastern cluster, where data governance programs tend to be more advanced, and platform adoption is less experimental. Salesforce’s localized structure on Alibaba Cloud also reinforces East China’s role as a base for compliant multinational deployments.

South China is the second major concentration point in the China customer data platform market, with Guangdong, Shenzhen, and Guangzhou benefiting from strong technology, electronics, and cross-border commerce. Tencent has a natural advantage in this region because its enterprise CDP is closely tied to WeChat and WeCom workflows via OneID-based identity linking. This matters because brands in South China often need tighter integration among commerce, service, and communication channels within the Tencent ecosystem. North China, led by Beijing, supports a different deployment profile, shaped more by government, state-owned enterprise, and large financial institution demand. Those projects usually involve longer procurement cycles, stricter internal security controls, and higher demand for private cloud or on-premises setups. As a result, the China customer data platform market shows a clear regional split between commerce-led adoption in the south and governance-led adoption in the north.

Central and western cities such as Chengdu, Wuhan, Xi’an, and Chongqing still account for a smaller share of spending in the China customer data platform market, but their role is growing as infrastructure investment spreads inland. These markets generally begin with simpler use cases, such as customer data collection and segmentation, before moving to real-time activation or predictive analytics. That pattern suggests a maturity gap rather than a lack of demand, because the core business need is already present, but deployment depth is still catching up. The long-term reach of the China customer data platform market will depend on how effectively vendors can deliver simpler, lower-cost, WeChat-native bundles for inland enterprises without losing compliance and integration quality.

Competitive Landscape

The China customer data platform market has a dual structure comprising domestic-native vendors and localized global players. Domestic companies such as Sensors Data, GrowingIO, Convertlab, APEX Technologies, Shuyun, and HYPERS AI are better aligned with local platform behavior, domestic cloud environments, and China-specific data handling needs. Their advantage is strongest where enterprises need direct connectivity with WeChat, Alipay, Douyin, and local commerce systems. Global vendors such as Salesforce, Oracle, SAP, and Tealium still compete in the China customer data platform market, but they are strongest in large organizations that already use international ERP or CRM systems. That gives the competitive field a layered profile rather than a winner-takes-all structure.

One visible strategy has been localization through infrastructure partnerships. Salesforce’s China Customer 360 setup on Alibaba Cloud shows how global vendors are adapting architecture and hosting arrangements to remain eligible for mainland deployments. Another strategy has been feature expansion tied to sector use cases, as shown by GrowingIO’s April 2026 upgrade for asset-based customer grouping in real estate and automotive environments. Tealium’s CloudStream launch in 2025 pointed to a different route, with zero-copy activation serving as a technical differentiator for enterprises seeking less data duplication across warehouses and engagement layers. Domestic leaders have also used expansion partnerships, including HKBN Enterprise Solutions becoming the exclusive telecom distribution partner for Sensors Data in Hong Kong and Macao in December 2025. These moves show that competition in the China customer data platform market is being shaped by localization, product depth, and channel reach.

White-space opportunity remains important because not every buyer group is fully served. BFSI-grade consent orchestration with audit-ready workflow depth remains a premium niche in the China customer data platform market, especially where compliance records must be both operational and reviewable. Composable architectures are attracting the attention of larger enterprises that want more control over warehouse-native data and lower long-term dependence on a single software layer. Vertical modules for healthcare, manufacturing, and government are also expanding the field, as general-purpose functionality is not always sufficient for regulated workflows. Overall, the China customer data platform market remains competitive and active, but the strongest players are those that can combine local platform engineering, compliant deployment models, and usable business applications into a single offering.

China Customer Data Platform Industry Leaders

Adobe Inc.

Salesforce, Inc.

Oracle Corporation

SAP SE

Twilio Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: Sensors Data released its New Three-Year Product Strategy for the AI Era and launched Sensors AI 1.0, an agentic AI platform for enterprise growth workflows. The platform embeds scenario-specific agents covering churn recall, member repurchase, advertising conversion optimization, and new customer conversion into CDP-connected business processes, compressing month-long planning cycles to minute-level agent collaborations.

- June 2026: Alipay launched its AI-powered assistant Abao in invitation-only testing, marking the platform's most significant redesign and its full shift toward AI-driven service delivery. The launch creates new structured first-party data streams across payments, service bookings, and daily financial interactions that will require CDP vendors to build certified Abao data connectors.

- April 2026: GrowingIO released a major capability upgrade to its CDP platform, introducing multi-entity asset segmentation enabling property and vehicle asset-based customer grouping for real estate and automotive industry clients. The upgrade extended CDP utility beyond traditional consumer marketing use cases into asset-lifecycle management.

- January 2026: China's revised Cybersecurity Law took effect, elevating administrative fines to up to CNY 10 million for severe data violations, explicitly integrating the cybersecurity regime with PIPL and the Data Security Law into a coordinated three-pillar national data governance framework.

China Customer Data Platform Market Report Scope

The China customer data platform market refers to the ecosystem of software and associated services that enable organizations in China to collect, unify, and manage customer data from multiple touchpoints into a single, persistent database. These platforms are designed to break down data silos, creating comprehensive customer profiles that can be leveraged for advanced audience segmentation, personalized marketing campaigns, customer journey orchestration, and predictive analytics. The market encompasses cloud, on-premises, and hybrid deployment models tailored to the operational needs of large and small and medium enterprises across sectors such as retail, BFSI, healthcare, and IT. By integrating robust consent and preference management capabilities, CDPs help Chinese businesses navigate and comply with stringent local data protection regulations, such as the Personal Information Protection Law (PIPL), while enhancing customer experience, driving brand loyalty, and improving overall marketing return on investment.

The China Customer Data Platform Market Report is Segmented by Offering (Software, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Customer Data Collection and Profile Unification, Audience Segmentation and Personalization, Marketing Campaign and Customer Journey Orchestration, Customer Analytics and Insights, Consent and Preference Management, and Other Applications), and End-User Industry (Retail and E-Commerce, BFSI, Healthcare and Life Sciences, IT and Telecom, Media and Entertainment, Industrial Manufacturing, Government and Public Administration, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization |

| Marketing Campaign and Customer Journey Orchestration |

| Customer Analytics and Insights |

| Consent and Preference Management |

| Other Applications |

| Retail and E-Commerce |

| BFSI |

| Healthcare and Life Sciences |

| IT and Telecom |

| Media and Entertainment |

| Industrial Manufacturing |

| Government and Public Administration |

| Other End-User Industries |

| By Offering | Software |

| Services | |

| By Deployment Mode | Cloud |

| On-Premises | |

| Hybrid | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Application | Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization | |

| Marketing Campaign and Customer Journey Orchestration | |

| Customer Analytics and Insights | |

| Consent and Preference Management | |

| Other Applications | |

| By End-User Industry | Retail and E-Commerce |

| BFSI | |

| Healthcare and Life Sciences | |

| IT and Telecom | |

| Media and Entertainment | |

| Industrial Manufacturing | |

| Government and Public Administration | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the size outlook for the China customer data platform market?

The China customer data platform market was valued at USD 0.61 billion in 2025 and is projected to reach USD 2.76 billion by 2031, at a CAGR of 29.43% over 2026-2031.

Which deployment model is growing fastest in China?

Hybrid deployment is growing the fastest, with a projected CAGR of 34.91% through 2031 because it balances local control of sensitive data with scalable cloud analytics.

Which application area is expanding most quickly?

Customer analytics and insights is the fastest-growing application, with a projected CAGR of 36.73% through 2031 as enterprises move from data unification to predictive and action-oriented use cases.

Which end-user group leads spending?

Retail and e-commerce led spending with a 21.37% revenue share in 2025 because customer data directly affects personalization, loyalty, and closed-loop measurement across commerce channels.

Why are local vendors strong in this space?

Local vendors are strong because they offer deeper integrations with WeChat, Alipay, Douyin, and domestic cloud platforms, along with deployment models that fit China’s compliance requirements.

What is the biggest challenge for new adopters?

Integration complexity remains the main challenge because enterprises often need to unify customer data across super apps, e-commerce platforms, CRM systems, and internal records before activation becomes effective.

Page last updated on: