China Cold Storage Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

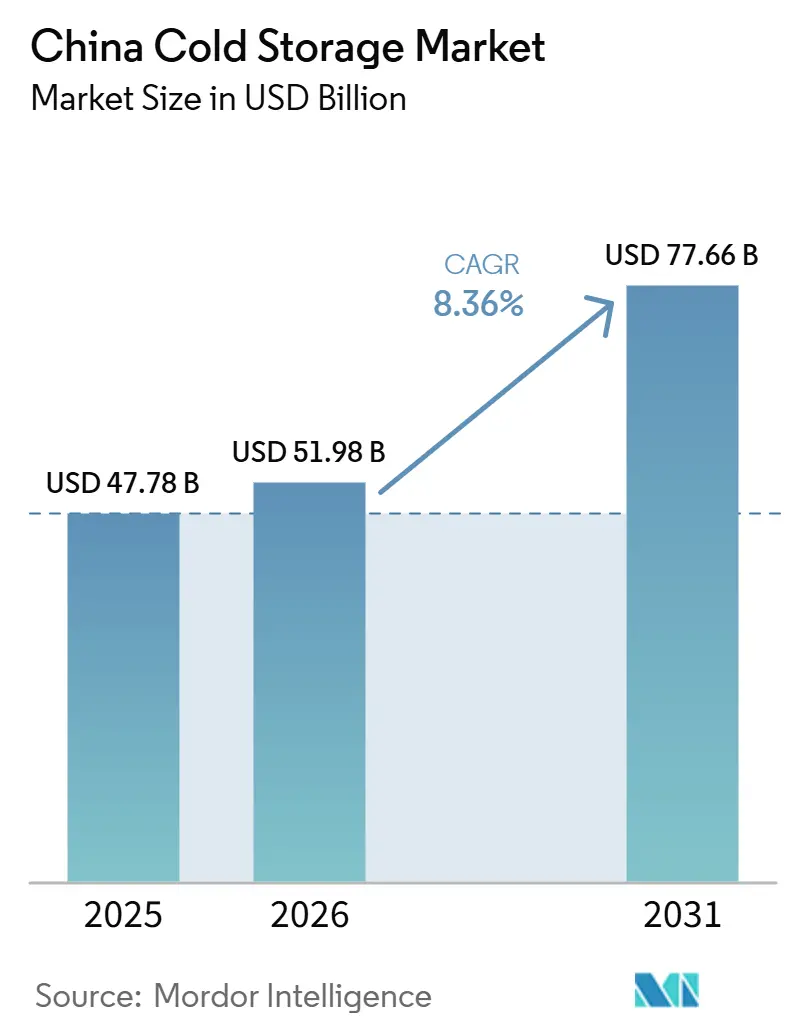

| Base Year Market Size (2025) | USD 47.78 Billion |

| Market Size (2026) | USD 51.98 Billion |

| Market Size (2031) | USD 77.66 Billion |

| Growth Rate (2026 - 2031) | 8.36% CAGR |

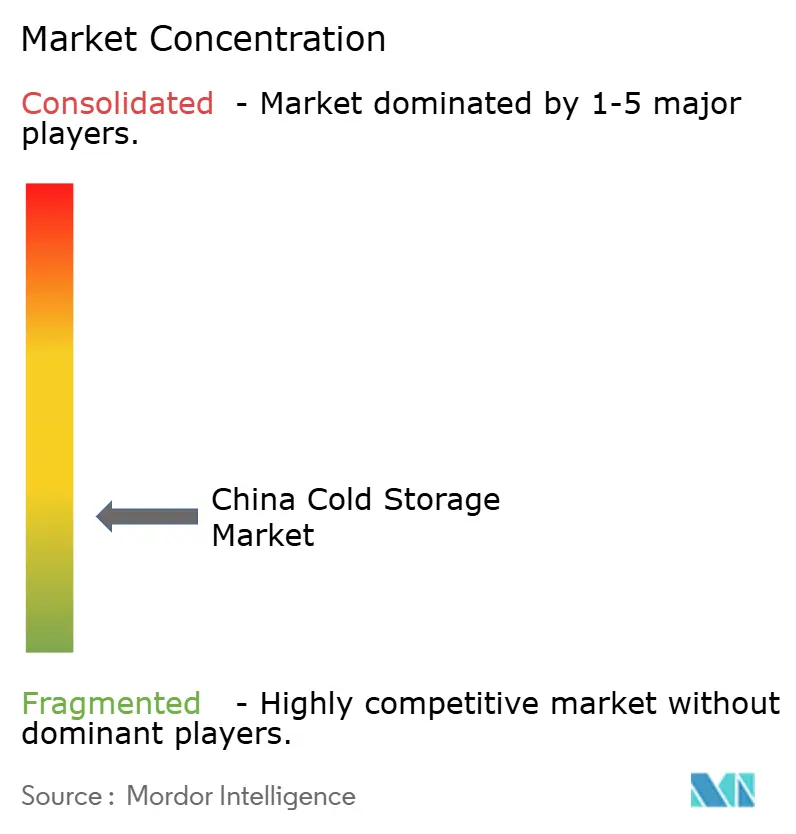

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

China Cold Storage Market Analysis by Mordor Intelligence

The China cold storage market size was valued at USD 47.78 billion in 2025 and is projected to grow to USD 51.98 billion in 2026 and reach USD 77.66 billion by 2031, growing at a CAGR of 8.36% from 2026 to 2031.

Demand in the China cold storage market is now coming from a broader mix of food retail, biologics, premium convenience foods, and last-mile urban fulfillment, lifting the value of higher-specification storage beyond its capacity needs. The China cold storage market is also being shaped by stronger public investment in backbone logistics bases, county-level cold chain coverage, and low-carbon upgrades, which is shifting competition toward operators that can fund compliance and engineering upgrades at scale. Urban grocery delivery, instant retail, and tighter service windows are changing the preferred facility model in the China cold storage market from large, outer-ring warehouses to a mix that includes smaller, more distributed chilled nodes closer to dense residential areas. Competition is becoming more uneven because national operators are investing in automation, validated pharmaceutical lanes, and longer-term energy strategies, while smaller regional operators remain more exposed to electricity costs, land pressure, and rising technical standards. The China cold storage market, therefore, continues to offer room for expansion. Still, the clearest gains are moving toward higher-value segments, expanding the inland network, and developing facilities that combine storage, traceability, and reliable temperature control in a single service model.

Key Report Takeaways

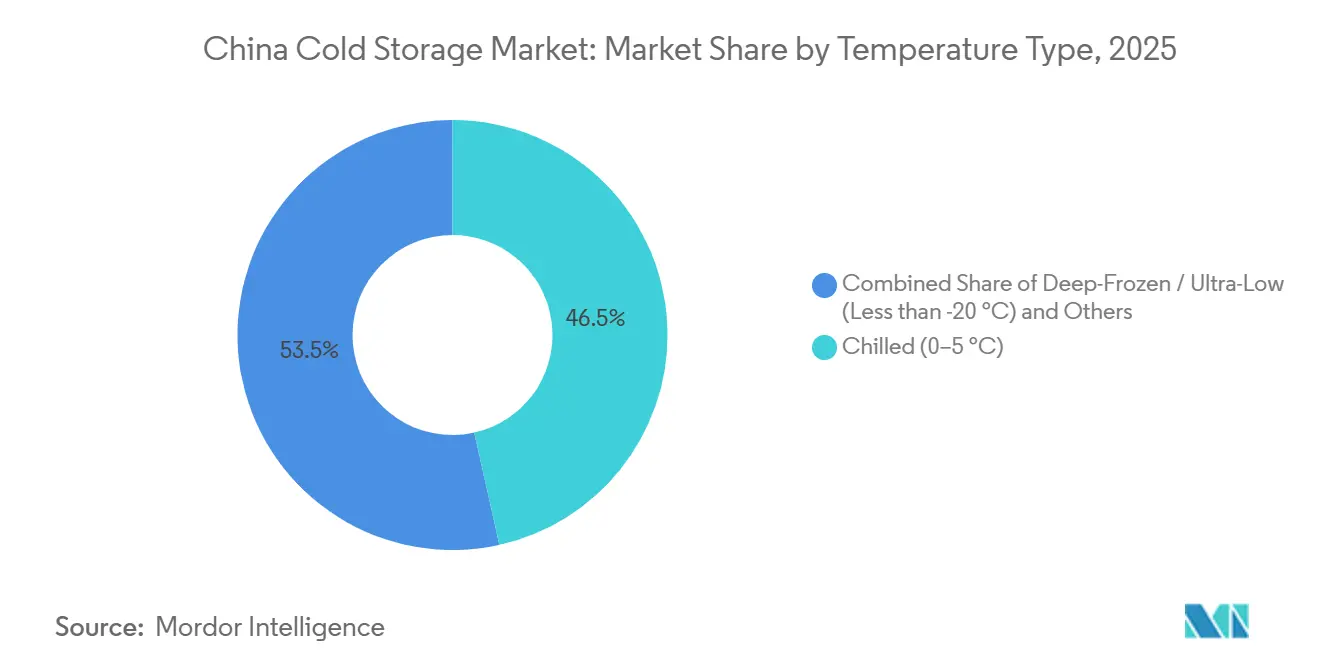

- By temperature type, chilled (0–5 °C) held 46.51% of the China cold storage market share in 2025, while deep-frozen/ultra-low (less than -20 °C) is forecast to grow at a 13.62% CAGR through 2031.

- By automation level, conventional facilities accounted for 83.02% share of the China cold storage market size in 2025, while automated cold stores are projected to expand at a 16.36% CAGR through 2031.

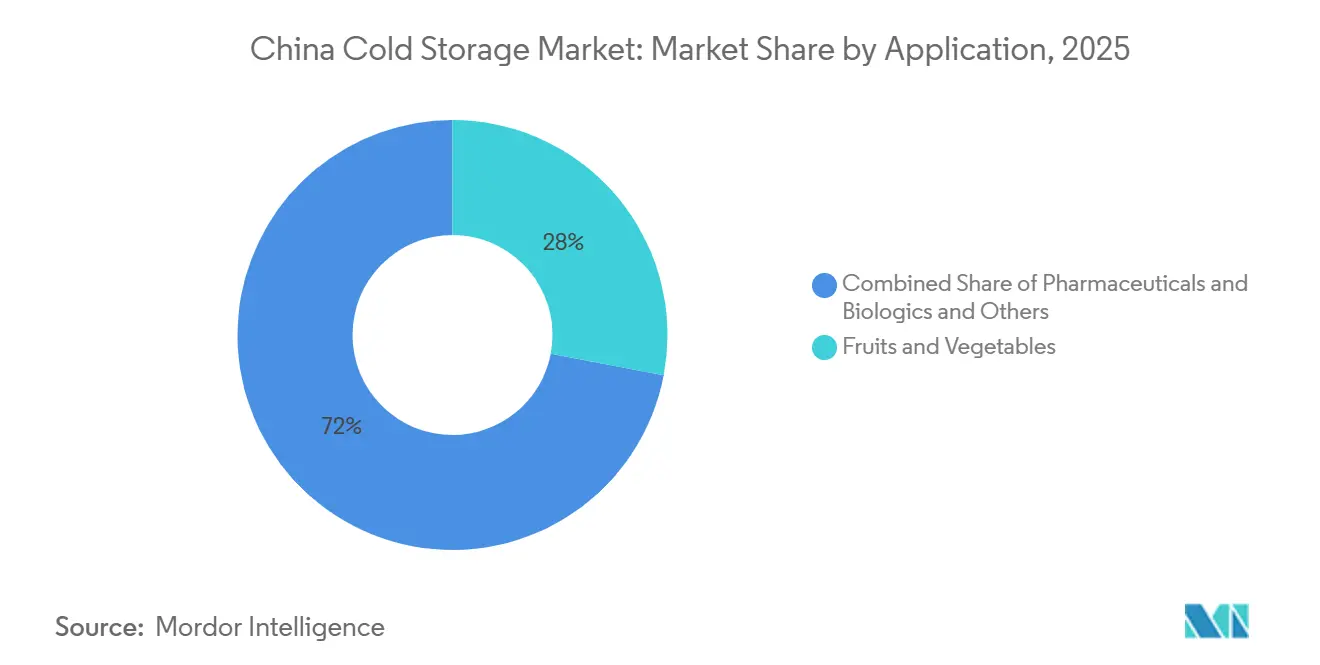

- By application, fruits and vegetables accounted for 28% of the China cold storage market size in 2025, while pharmaceuticals and biologics are expected to advance at a 16.68% CAGR through 2031.

- By geography, the East region led with 30.11% of the China cold storage market share in 2025, while the South region is set to record the highest CAGR of 12.47% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China Cold Storage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion Of Online Grocery And Fresh E-Commerce | +2.0% | National, concentrated in East, South, and Tier-1 and Tier-2 cities | Short term (≤ 2 years) |

| Rising Pharmaceutical And Biologics Cold Chain Demand | +1.8% | East and South, especially Jiangsu, Zhejiang, and Guangdong | Medium term (2-4 years) |

| Government-Led Cold Chain Infrastructure Investment | +1.7% | National, with faster gains in Central, Southwest, and Northwest | Medium term (2-4 years) |

| Rising Demand For Premium Frozen And Ready-To-Eat Foods | +0.9% | East and South, especially the Yangtze River Delta and Pearl River Delta | Short term (≤ 2 years) |

| Automation Adoption In High-Density Urban Logistics Hubs | +0.8% | East and South, especially Beijing, Shanghai, Guangzhou, and Shenzhen | Medium term (2-4 years) |

| Export-Oriented Compliance For Seafood And Processed Food | +0.5% | East, Northeast, and South coastal export hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expansion Of Online Grocery And Fresh E-Commerce

Fresh e-commerce penetration reached 48.6% in 2025, while China’s urbanization rate reached 67.2%, which kept a large consumer base within reach of dense urban delivery networks in the China cold storage market. The same pattern is pushing operators to place more chilled inventory inside or near residential clusters because short delivery windows now matter as much as bulk storage capacity for many food categories. Micro-fulfillment hubs are changing the sizing logic of the China cold storage market because distributed 500- to 2,000-m² nodes can serve urban demand more efficiently than relying solely on distant mega sites. This shift is creating pressure on standard-specification assets in outer industrial parks, where supply is easier to add but access to fast urban demand is weaker. It also supports greater investment in software-enabled inventory visibility, routing, and replenishment, as city-level cold chain performance is now closely tied to response speed and location quality, not just pallet volume.

Rising Pharmaceutical And Biologics Cold Chain Demand

The China cold storage market is seeing stronger demand from pharmaceutical and biologics customers that need tighter validation, higher traceability, and better temperature discipline than conventional food-grade storage usually provides. The national standard GB/T 46204-2025 increased the traceability burden upon its October 2025 implementation, strengthening the position of operators that already run validated processes and digital temperature monitoring systems. Demand is also shifting toward ultra-low-temperature lanes for biologics, mRNA-related handling, and advanced therapy logistics, which is narrowing the field of providers able to serve premium contracts. As a result, the China cold storage market is moving toward higher-quality revenue by facilities that combine compliant storage, validated handling, and dependable last-mile service for healthcare customers.

Government-Led Cold Chain Infrastructure Investment

Government-backed network building remains one of the clearest supports for the China cold storage market because more than 100 national backbone cold chain logistics bases were completed ahead of schedule by early 2026. The policy focus is now shifting from basic network coverage to higher-quality, greener operations and more county-level infrastructure, favoring operators that can fund retrofits and standardized facility design. The Ministry of Agriculture and Rural Affairs also expanded county eligibility for agricultural cold chain support in late 2025, which is helping connect inland production areas to more dependable temperature-controlled storage and transport links. This support matters because post-harvest loss reduction, rural logistics coverage, and product quality preservation all depend on storage access beyond the coastal provinces. It is also improving the long-term shape of the China cold storage market by shifting investment toward inland nodes, greener vehicle fleets, and stricter procurement standards for low-carbon logistics service providers.

Automation Adoption In High-Density Urban Logistics Hubs

Automation is gaining importance in the China cold storage market because urban logistics operators face tight land supply, labor challenges in sub-zero work, and shorter delivery service windows. JD Logistics opened a 120,000 m² multi-temperature automated center in Suzhou in April 2025, designed to serve five climate zones and support 24-hour coverage across 200 cities. A cold chain park case cited by People’s Daily showed an 18% reduction in merchant transport costs and a 90% vehicle load rate after data-driven operational upgrades, underscoring why automation is becoming a service quality tool rather than just a labor-saving measure. A Keslon project in Hunan also showed materially higher space utilization and transfer efficiency in a fully automated, low-temperature environment, which helps explain why the China cold storage market is delivering stronger returns to operators that can invest in dense, software-led facility models[1]Source: Keslon, “Case of a Large-Scale Fully Automated Stacker Cold Storage Project in Xiangtan,” Keslon, keslon.com.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Land And Electricity Costs In Core Logistics Corridors | -0.8% | East and South, especially Shanghai, Guangzhou, and Shenzhen | Long term (≥ 4 years) |

| Fragmented Operator Base And Uneven Cold Chain Standardization | -0.7% | National, with higher severity in Central, Southwest, and Northwest | Medium term (2-4 years) |

| Skilled Labor Shortages For Automation, Maintenance, And Quality Assurance | -0.5% | National, with the highest pressure in the western provinces | Medium term (2-4 years) |

| Grid Reliability And Carbon Compliance Pressure On Energy-Intensive Facilities | -0.6% | North and Central inland areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Land And Electricity Costs In Core Logistics Corridors

Energy and land remain major cost limits in the China cold storage market because refrigerated facilities are more power-intensive than standard warehouses, and core logistics corridors continue to see pricing pressure on industrial sites. This issue is most visible around Shanghai, Guangzhou, and Shenzhen, where the economics of older facilities are weaker if operators have not invested in green refrigerants, solar support, or better energy management. Smaller operators are under the most pressure because they often lack the capital needed for retrofits that could lower recurring utility exposure and reduce future compliance risk. Developers are therefore moving some new projects toward satellite cities and second-ring industrial zones, where land is cheaper even if transport distances become longer. The result is that profitability in the China cold storage market depends more on site selection, energy efficiency, and customer mix than on storage scale alone[2]China National Standards Bureau. "GB/T 46204-2025: Requirements for Traceability Management of Drug Cold Chain Logistics." October 2025. .

Fragmented Operator Base And Uneven Cold Chain Standardization

The China cold storage market still has a sharp split between national operators with broad technical capability and a large number of local providers that compete mainly on price. That imbalance is more severe in central and western provinces, where service reliability remains less consistent, and enterprise customers stay more cautious when awarding large multi-site contracts. Standards finalized in 2025 and moving into implementation from 2026 are raising the threshold for safe transport, traceability, and facility management, which should force more upgrades and exits among undercapitalized operators. Even so, consolidation is unlikely to be immediate because asset trading remains uneven and many regional businesses still operate around local customer relationships rather than scalable national systems. This keeps the China cold storage market open, but it also slows the pace at which buyers can rely on a uniform quality standard nationwide.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Temperature Type: Deep-Frozen Demand Reshapes Facility Mix

Chilled (0–5 °C) storage accounted for 46.51% of China cold storage market share in 2025, making it the largest temperature segment by value. That position came from the large flow of fresh produce, dairy, chilled meat, and ready-to-sell food items moving through East and South China distribution networks. Chilled assets are important for throughput and network density, but they often serve food retail contracts with lower margins than more specialized low-temperature applications. Frozen storage remains central for processed meat, imports, and central kitchen supply because longer dwell times and more predictable throughput support steadier operating patterns in the China cold storage market.

Deep-frozen/ultra-low (-20 °C or lower) storage is projected to grow at a 13.62% CAGR through 2031, making it the fastest-expanding temperature segment in the China cold storage market. This demand is coming from both biologics handling and premium seafood or ice cream imports, which require more stable sub-zero performance than conventional food storage. Operators that entered this segment earlier are better placed because ultra-low chambers require more capex, tighter monitoring, and stronger engineering discipline than standard frozen rooms. The China cold storage industry is therefore seeing a clearer divide between volume-heavy chilled infrastructure and higher-yield ultra-low assets that serve fewer but more demanding customers.

By Automation Level (Storage): Conventional Base Narrows As AS/RS Economics Improve

Conventional facilities accounted for 83.02% of the China cold storage market share in 2025, indicating that the installed base still reflects the rapid build-out phase of earlier years. Many of these assets were built when fast deployment mattered more than dense automation, especially for basic food logistics across expanding urban corridors. Their large footprint does not fully reflect current investment direction, as labor costs, food safety requirements, and service-level demands have all risen. Conventional operators now face pressure from both automated national networks and e-commerce-led stocking models that bypass many generic storage sites in the China cold storage market.

Automated cold stores are forecast to expand at a 16.36% CAGR through 2031, which is more than double the pace of the overall China cold storage market. The shift is being supported by falling equipment economics, stronger domestic manufacturing of AS/RS systems, and better returns from high-density sites in expensive urban logistics zones. The Xiangtan automated project cited by Keslon showed 3 times higher space utilization and 60% higher transfer efficiency than a comparable manual facility, which helps explain the commercial logic behind new capex decisions. The China cold storage industry is therefore moving toward automation as a practical response to labor exposure, traceability needs, and urban real estate constraints rather than as a narrow technology upgrade.

By Application: Pharmaceutical Segment Elevates Revenue Quality

Fruits and vegetables accounted for 28% of the China cold storage market size in 2025, making it the largest application segment by value. The segment reflects China’s scale in fresh produce production and its growing trade links with Southeast Asia, Australia, and South America for perishables that need dependable temperature control. Meat and Poultry remained another major use case, supported by imported volumes routed through bonded cold stores in Qingdao, Tianjin, and Shanghai. Fish and seafood also matter because import and export compliance is tightening, which raises the value of well-managed bonded cold storage in the China cold storage market.

Pharmaceuticals and biologics are projected to grow at a 16.68% CAGR through 2031, making it the fastest-growing application in the China cold storage market. This application carries better pricing because customers need validated handling, stronger chain-of-custody control, and dependable last-mile delivery for temperature-sensitive products. Vaccines and clinical trial materials create an even tighter niche because the temperature range can extend to cryogenic handling, which only a limited number of operators can support. The China cold storage market is therefore improving in terms of revenue quality as more operators move from volume-led food contracts toward technically demanding healthcare and specialty-materials businesses.

Geography Analysis

The East region led the China cold storage market, accounting for 30.11% in 2025. It remained the country’s strongest regional base for dense consumer demand, bonded import flows, and pharmaceutical manufacturing activity. This position comes from the Shanghai and Ningbo port corridor, the large consumer base across the Yangtze River Delta, and the presence of strong pharmaceutical clusters in Jiangsu and Zhejiang. East China also benefits from a mature multi-layer network that combines large multi-temperature parks, bonded facilities, and smaller urban nodes for fast food delivery. North China remains important because Beijing anchors administrative demand, and nearby agricultural zones support steady cold chain use across grain, meat, and broader food distribution systems. The China cold storage market in the South also benefits from Greater Bay Area trade links and cross-border refrigerated flows connected to Hong Kong and Guangdong.

The South region is projected to grow at a 12.47% CAGR through 2031, making it the fastest-growing geography in the China cold storage market. Growth is supported by the Pearl River Delta’s diverse manufacturing base, strong ready-to-eat meal demand, and seafood import activity through Guangzhou’s Nansha port. Shenzhen Agricultural Products Group signed a land-use agreement in May 2025 and committed CNY 306.56 million (USD 42.6 million) to land for a new import center in Nansha, indicating ongoing capital inflows into southern cold-chain capacity[3]MarketScreener. "Shenzhen Agricultural Power Group Agreed to Acquire Shenzhen Zhenchu Supply Chain Co. Ltd. for CNY 27.5 Million." March 26, 2025.. The Northeast remains important for frozen-food processing and seafood handling, but it also faces pressure from land and utility costs in key corridors. South China, therefore, stands out as the clearest near-term regional growth engine in the China cold storage market because it combines consumption, trade, and investment momentum in one corridor.

Central and Southwest China represent the clearest policy-led expansion zones in the China cold storage market because the backbone cold chain base development is attracting more investment inland. Sinotrans committed CNY 2.8 billion (USD 389 million) in March 2025 to 15 new cold chain parks across central and western provinces, signaling a deliberate push to connect inland production hubs with coastal consumption centers more efficiently. The Northwest remains the smallest and least-served region. Still, subsidies for agricultural cold chain infrastructure and a broader domestic dairy base are improving the medium-term case for selective investment. Regional performance in the China cold storage market will therefore remain uneven, but the strongest incremental upside now sits outside the most mature coastal clusters.

Competitive Landscape

The China cold storage market is less consolidated at the upper end, with the top 5 operators accounting for less than 40% of market value in 2025, while hundreds of smaller firms still serve local customers across standard storage segments. This structure creates a two-speed market where scale operators compete through national reach, automation, and compliance, while regional firms often rely on proximity and price. China Merchants Americold Holdings and Sinotrans are using a network strategy built around multi-temperature parks, large project pipelines, and long-term operating discipline in the China cold storage market. JD Logistics and SF Cold Chain are competing more through technology visibility, speed commitments, and integrated warehouse and transport management systems that improve execution consistency. Pharmaceutical-capable facilities also hold a stronger position because validated operations create higher switching costs and more stable customer relationships than standard food-only contracts.

JD Logistics opened its 120,000 m² multi-temperature automated center in Suzhou in April 2025, strengthening its ability to combine speed, automation, and national coverage in the China cold storage market. China Merchants Americold Holdings also secured CNY 3.5 billion (USD 487 million) in January 2025 to develop 20 GDP-compliant cold stores by 2027, with a focus on biologics and pharmaceutical logistics. Sinotrans committed CNY 2.8 billion (USD 389 million) in March 2025 to add 15 inland cold chain parks designed for rail-road interchange operations[4]Hkexnews. Sinotrans Ltd., Half-Year Report 2025 Management Discussion and Analysis. August 26, 2025. . These moves show that the most credible expansion models in the China cold storage market combine capacity growth with either automation depth, pharmaceutical readiness, or inland network positioning.

White space still exists in county-level nodes, bonded ultra-low facilities, and integrated storage services for central kitchen and food service chains. Operators with stronger digital systems are also gaining ground because predictive maintenance, IoT-based temperature visibility, and real-time inventory positioning improve uptime and customer confidence. This shifts the basis of competition in the China cold storage market away from asset ownership alone and toward service quality that can be measured and audited. Even with this shift, the presence of many regional firms means pricing pressure will remain visible in conventional storage, especially outside the highest-value pharmaceutical and automated niches.

China Cold Storage Industry Leaders

-

China Merchants Americold Holdings Co., Ltd.

-

JD Logistics, Inc.

-

SF Cold Chain (SF Holding)

-

Sinotrans Ltd.

-

Xianyi Holdings Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Nichirei Corporation announced the acquisition of 51% stakes in PT Mega Indo Logistik and PT Mega Internasional Sejahtera, Indonesia, consolidating the group's ASEAN cold chain network in the region's largest economy by GDP. The deal, scheduled to close in June 2026, is part of Nichirei's strategy to build a pan-ASEAN temperature-controlled logistics network amid compressing domestic Japanese cold-chain margins.

- January 2026: SF Holding signed a subscription agreement with J&T Express, issuing approximately 225.9 million H-shares at HKD 36.74 (USD 4.69) per share and raising approximately HKD 8.299 billion (USD 1.07 billion). The transaction deepens SF Holding's footprint in cross-border e-commerce logistics and broadens SF Cold Chain's last-mile delivery reach across Southeast Asia.

- June 2025: JD Logistics deployed 500,000 new reusable cold chain delivery boxes for fresh products on World Environment Day. Each reuse cycle is estimated to cut carbon emissions by 850 grams, targeting a lifecycle carbon reduction of 127,000 tons across the fleet.

- May 2025: Shenzhen Agricultural Products Group signed a land use agreement with Guangzhou municipal authorities for a plot in Nansha District, committing CNY 306.56 million (USD 42.6 million) for land to develop a food and agricultural products import center in the Greater Bay Area, including cold storage and value-added processing capabilities.

China Cold Storage Market Report Scope

| Chilled (0–5 °C) |

| Frozen (-18–0 °C) |

| Ambient |

| Deep-Frozen / Ultra-Low (Less than -20 °C) |

| Conventional Facilities |

| Automated Cold Stores (AS/RS, Robotics) |

| Fruits and Vegetables |

| Meat and Poultry |

| Fish and Seafood |

| Dairy and Frozen Desserts |

| Bakery and Confectionery |

| Ready-to-Eat Meals |

| Pharmaceuticals and Biologics |

| Vaccines and Clinical Trial Materials |

| Chemicals and Specialty Materials |

| Other Perishables |

| North |

| Northeast |

| East |

| Central |

| South |

| Southwest |

| Northwest |

| By Temperature Type | Chilled (0–5 °C) |

| Frozen (-18–0 °C) | |

| Ambient | |

| Deep-Frozen / Ultra-Low (Less than -20 °C) | |

| By Automation Level (Storage) | Conventional Facilities |

| Automated Cold Stores (AS/RS, Robotics) | |

| By Application | Fruits and Vegetables |

| Meat and Poultry | |

| Fish and Seafood | |

| Dairy and Frozen Desserts | |

| Bakery and Confectionery | |

| Ready-to-Eat Meals | |

| Pharmaceuticals and Biologics | |

| Vaccines and Clinical Trial Materials | |

| Chemicals and Specialty Materials | |

| Other Perishables | |

| By Region | North |

| Northeast | |

| East | |

| Central | |

| South | |

| Southwest | |

| Northwest |

Key Questions Answered in the Report

What is the projected value of the China cold storage sector by 2031?

The China cold storage market is forecast to reach USD 77.66 billion by 2031 from USD 51.98 billion in 2026, growing at an 8.36% CAGR over 2026 to 2031.

Which application is expanding the fastest in China cold storage?

Pharmaceuticals and biologics are the fastest-growing application, with a projected 16.68% CAGR through 2031, well above the overall market pace.

Which region leads the cold storage demand in China?

The East region led with a 30.11% share in 2025, driven by high consumption, strong port infrastructure, and pharmaceutical manufacturing clusters.

Why are automated facilities gaining traction in China?

Automated cold stores are projected to grow at a 16.36% CAGR as operators seek better space utilization, more reliable low-temperature handling, and stronger traceability in urban logistics hubs.

What is the biggest challenge for cold storage operators in China?

High land and electricity costs in major logistics corridors remain a major challenge, especially for smaller operators that cannot easily fund energy and compliance upgrades.

How concentrated is the competitive landscape in China cold storage?

The top five operators accounted for less than 40% of the market value in 2025, while hundreds of smaller firms continued to serve local customers across standard storage segments.

Page last updated on: