China Co-Living Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

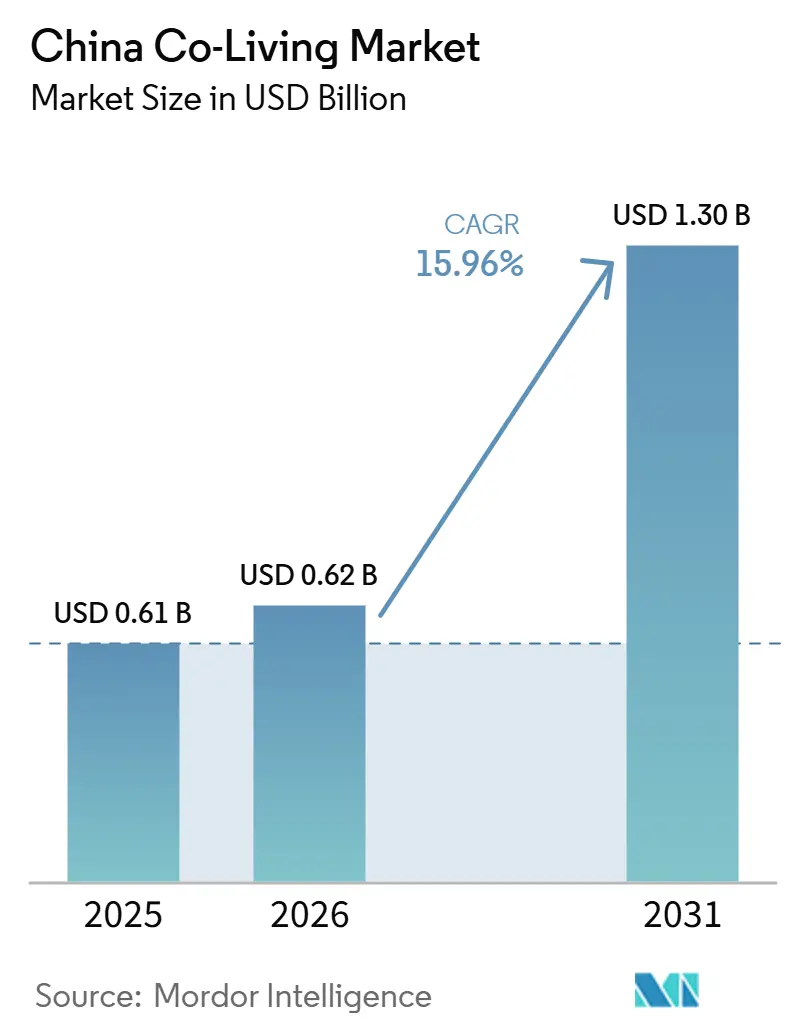

| Base Year Market Size (2025) | USD 0.61 Billion |

| Market Size (2026) | USD 0.62 Billion |

| Market Size (2031) | USD 1.30 Billion |

| Growth Rate (2026 - 2031) | 15.96% CAGR |

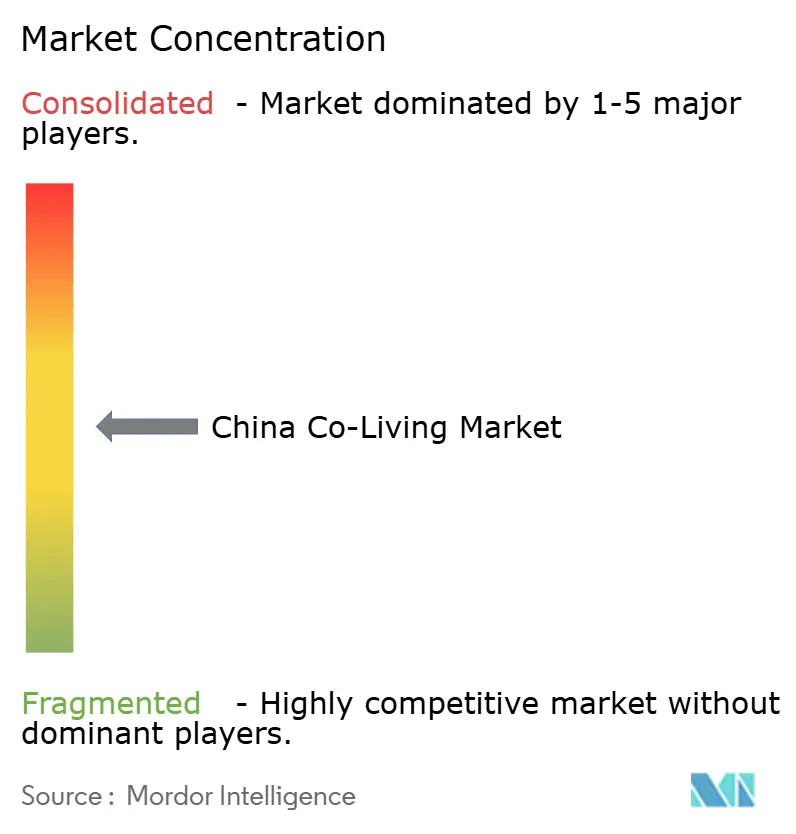

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Co-Living Market Analysis by Mordor Intelligence

The China Co-Living Market size was valued at USD 0.61 billion in 2025 and is estimated to grow from USD 0.62 billion in 2026 to reach USD 1.30 billion by 2031, at a CAGR of 15.96% during the forecast period (2026-2031).

The China co-living market is expanding amid continued urban concentration, with China’s urbanization rate reaching 67.9% in 2025, keeping rental demand concentrated in large cities where ownership remains out of reach for many younger households. The addressable renter base also remains deep because policymakers stated in May 2026 that 250 million urban residents still lacked local household registration, which keeps demand tilted toward formal rental formats rather than public ownership channels. The State Council’s Housing Rental Regulations, effective from September 15, 2025, reduced an important source of uncertainty by establishing a national framework for tenant rights, contract registration, and operator accountability, providing larger licensed operators with a clearer path for expansion. At the same time, weakness in the ownership market is pushing more household formation into rental, while government-backed affordable rental supply is pressuring low-end pricing and forcing private operators to move toward higher-quality products and lighter balance sheets. That combination is creating a China co-living market in which revenue growth increasingly depends on compliance, service quality, and management capability rather than on simple asset accumulation.

Key Report Takeaways

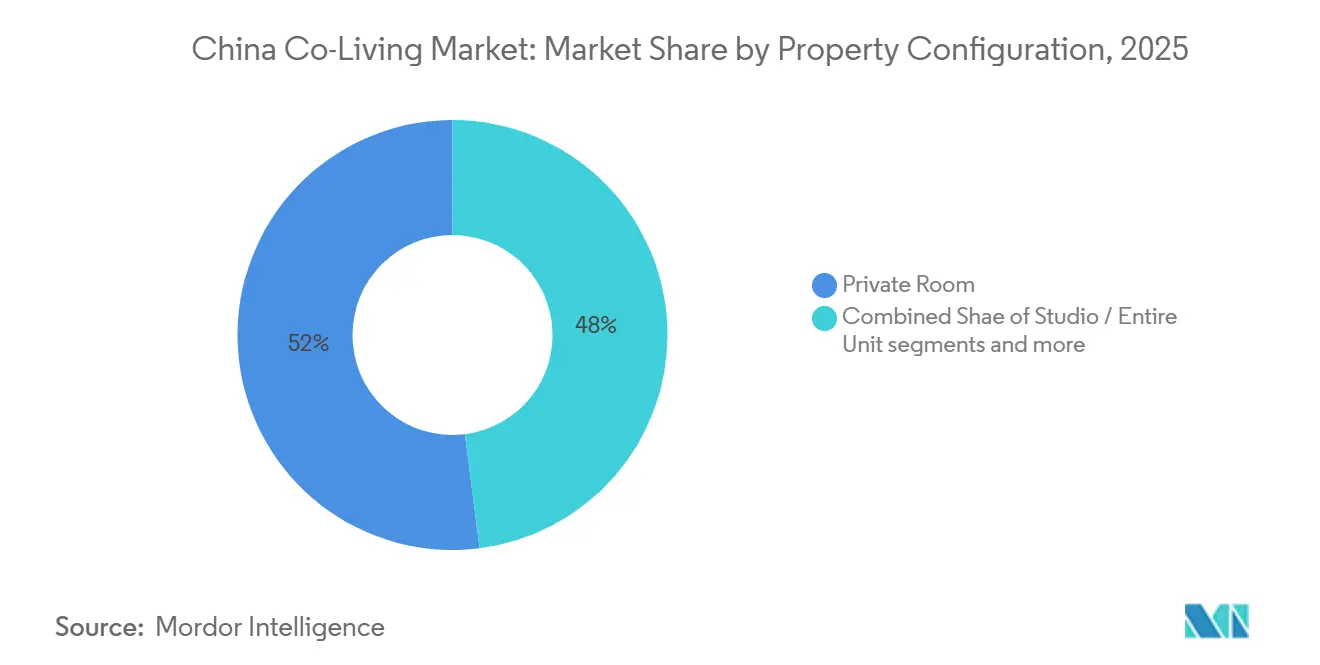

- By property configuration, private rooms held 52% of the China co-living market share in 2025, while studio / entire unit is forecast to expand at a 16.50% CAGR through 2031.

- By business model, asset-light master lease / lease arbitrage held 46% share in 2025, while asset-light management agreement recorded the highest projected CAGR at 16.90% through 2031.

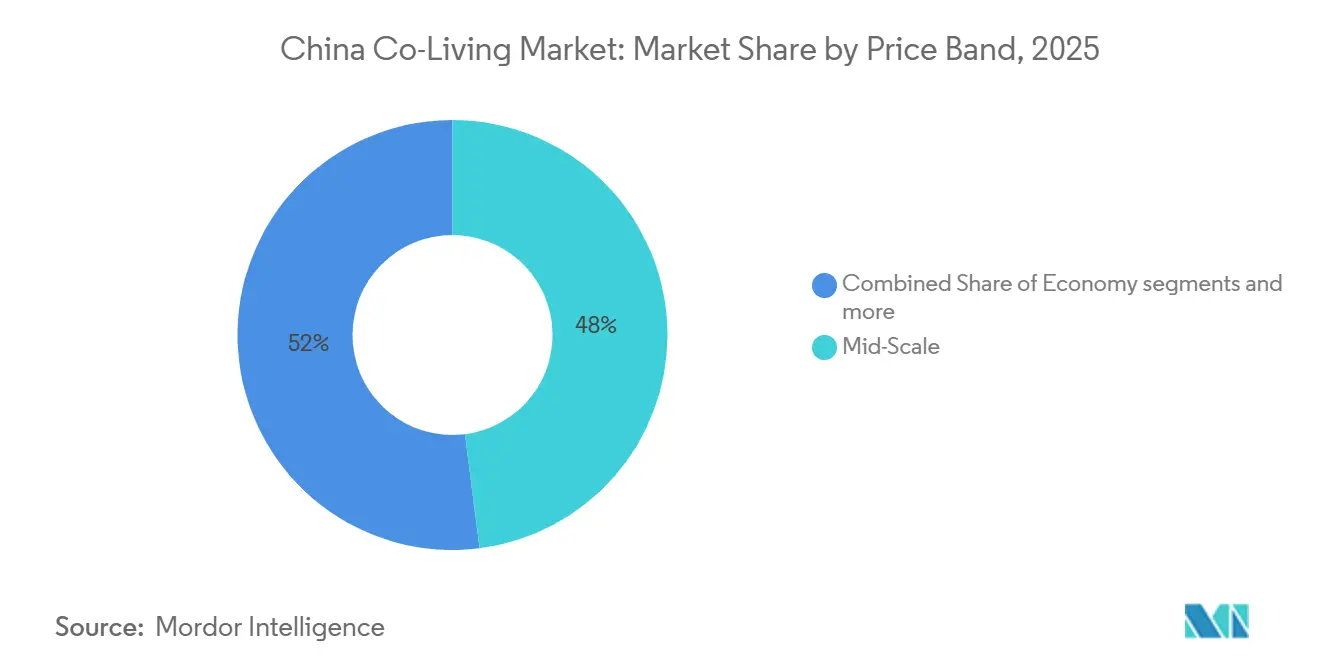

- By price band, mid-scale accounted for 48% of the China co-living market size in 2025, while premium / luxury is advancing at a 17.30% CAGR through 2031.

- By end user, students led with 53% share in 2025, while working professionals are projected to grow at a 17.50% CAGR through 2031.

- By city, Beijing held 28% share in 2025, while Shanghai is forecast to expand at a 17.90% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China Co-Living Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Housing Prices and Rental Affordability | +3.0% | Beijing, Shanghai, Shenzhen, and Tier-1 core cities | Medium term (2-4 years) |

| Rapid Urbanization and Migrant Workforce Growth | +2.5% | National, with concentrated gains in Beijing, Shanghai, Shenzhen, and Guangzhou | Short term (≤ 2 years) and Medium term (2-4 years) |

| Growing Young Professional and Graduate Population | +2.5% | National, with faster momentum in Tier-1 and new Tier-1 cities | Medium term (2-4 years) |

| Government Support for Rental Housing | +2.0% | National, with early gains concentrated in Beijing, Shanghai, Shenzhen, and Guangzhou | Short term (≤ 2 years) and Medium term (2-4 years) |

| Redevelopment of Underutilized Urban Properties | +1.5% | Beijing, Shanghai, Guangzhou, with spillover to Tier-2 cities | Medium term (2-4 years) |

| Growing Demand for Flexible Rental Housing | +1.5% | Tier-1 cities, with spillover to Chengdu and Hangzhou | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Housing Prices and Rental Affordability

Housing affordability remains the central demand support for the China co-living market in Tier-1 cities because home purchase costs still sit well above what many younger workers can absorb even after the 2023 to 2025 correction cycle. The China co-living market also remains attractive because institutionally managed projects in Beijing and Shanghai held occupancy near 90% in early 2025 even as broader rents softened, which shows that professionally run rental products continue to draw demand during weaker pricing conditions. This pattern matters because demand strength is most durable in the same cities where ownership is least attainable. Rent pressure has therefore not reduced the role of co-living, but has instead pushed tenants to look for better value within managed formats. That keeps Beijing, Shanghai, Shenzhen, and Guangzhou at the center of China co-living market demand and supports continued product differentiation across private rooms, studios, and quality-certified mid-scale assets.

Rapid Urbanization and Migrant Workforce Growth Drive Co-Living Demand

China’s migrant worker population reached 301.15 million in 2025, up by 1.42 million from the prior year, which keeps a very large share of urban housing demand tied to mobile renters rather than settled owners. Average monthly income for out-of-province workers rose to CNY 5,774 (USD 794) in 2025. Yet, this income level still leaves Tier-1 city housing unaffordable for many workers without a shared or managed rental solution. The China co-living market benefits from this mismatch because it offers a formal rental format that sits between informal shared housing and full private apartments. Policy discussion in May 2026 around extending public services to 250 million unregistered urban residents also points to a continued push toward better-regulated rental living rather than a reduced need for private operators. As a result, operators with strong compliance systems are positioned to capture tenants who would otherwise remain in unlicensed or fragmented rental arrangements.

Growing Young Professional and Graduate Population Expands Occupancy

More than 12.22 million graduates entered China’s labor market in 2025, keeping the graduation season a major demand trigger for the China co-living market in large employment hubs. Academic research published in 2025 also showed that first-tier city graduates face a clear mismatch between entry-level incomes and housing costs, making co-living a practical first housing option after graduation. The demand base is now broadening beyond first-time renters, as tenants aged 30 and above accounted for more than 50% of institutional rental tenants in 2025, signaling a longer-staying renter population. That shift changes product expectations toward privacy, better service, and layouts suited to couples or small families rather than only single occupants. It also explains why operators that can support flexible leases and quality upgrades are capturing a larger share of the China co-living market than those still built around a purely transient tenant base.

Government Support for Rental Housing Encourages Co-Living Development

Policy support has become a direct growth lever for the China co-living market since the People’s Bank of China and the National Financial Regulatory Administration issued guidance on housing rental finance in February 2024. That framework pushed lenders toward dedicated rental products and widened the path for infrastructure Real Estate Investment Trust (REIT) financing, which improved access to long-term capital for compliant operators. Invesco’s 2025 review also noted that the rental housing REIT price index rose 31% in 2024, making rental housing the only real estate sub-sector in China to record cap rate compression that year. The State Council’s Housing Rental Regulations, added in September 2025, established a national legal framework that strengthened the operating advantage of licensed providers over informal landlords. The result is a clearer investment runway for the China co-living market, as regulation and financing are now moving in the same direction.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Property Acquisition and Operating Costs Increase Development Expenses | -2.0% | Beijing, Shanghai, Shenzhen, and Guangzhou | Long term (≥ 4 years) |

| Regulatory Uncertainty Across Cities Delays Market Expansion | -1.5% | National, most pronounced in Tier-2 and Tier-3 cities | Medium term (2-4 years) |

| Competition from Traditional Rental Apartments Limits Co-Living Adoption | -1.5% | National | Short term (≤ 2 years) and Medium term (2-4 years) |

| Low Consumer Acceptance in Lower-Tier Cities Restricts Market Growth | -1.0% | Tier-3 and Tier-4 cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Property Acquisition and Operating Costs Increase Development Expenses

Cost pressure remains a meaningful restraint because the master lease model has become much harder to defend once rents began to fall in 2025, leaving operators with lease obligations set at earlier peak levels. Shanghai’s centralized apartment rents fell from CNY 195.6 (USD 26.9) per square meter per month in 2021 to CNY 149.6 (USD 20.6) per square meter per month in 2025, highlighting the earnings risk of rent arbitrage strategies when occupancy falls below break-even levels. Purpose-built projects also require large capital commitments, as shown by the Invesco Real Estate and Ziroom venture in Beijing with an expected total investment of RMB 1.2 billion (USD 165 million). Those thresholds narrow the field of companies that can add quality supply in premium locations, and they slow expansion for independent operators. The China co-living market, therefore, grows fastest where institutional capital, policy support, and experienced operating teams already overlap.

Regulatory Uncertainty Across Cities Delays Market Expansion

National regulations have improved, but local implementation still varies sharply across cities, limiting how quickly the China co-living market can scale beyond the main gateways. Shanghai’s conversion policy is one of the clearest examples because it allows commercial buildings to shift to rental use under a 15-year operating structure without additional land premium payments, a flexibility that most smaller cities still do not offer. Operators in second- and third-tier locations still face uneven licensing, less clarity on shared-occupancy standards, and weaker access to financing tools tied to institutional rental assets. This keeps the China co-living market concentrated in Beijing, Shanghai, Shenzhen, and Guangzhou, even though renter demand is spreading more widely across urban China. It also favors larger operators with stronger legal and government affairs capacity, as they can more easily absorb compliance costs than smaller local players.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Configuration: Private Rooms Anchor Revenue as Studio / Entire Units Build Share

Private Room configurations held 52% of the China co-living market share in 2025, making them the main revenue driver across the configuration mix. This lead reflects a simple preference for privacy in a shared living setting, especially among tenants seeking a lower-cost option without sacrificing personal space. Shared Room products still matter at the entry level because they serve students and recent migrants who are more sensitive to monthly rent than to layout quality. At the same time, the China co-living market is moving beyond a purely low-cost proposition because studio / entire unit formats are projected to grow at a 16.50% CAGR through 2031. That growth is tied to a broader renter profile that increasingly includes older professionals and small family units.

The shift is already visible in transaction patterns: 3-bedroom entire-unit deals in key cities rose 15% quarter over quarter in the first half of 2026[1]China Urban Housing Rental Think Tank and Ziroom Research Institute, “2026 H1 Long-Term Rental Market Semi-Annual Report,” NetEase News, 163.com. That increase suggests that family-compatible or privacy-led demand is not confined to traditional apartment rentals, but is also feeding into the product logic of managed co-living. Shared room supply faces the greatest pressure from subsidized affordable rental housing, as public units directly compete on price in the lowest tier. Private room products sit in a more defensible middle position because they balance affordability, convenience, and personal control better than either open dorm-style formats or higher-priced private units. Operators are responding by adding smart access, app-based services, and more consistent maintenance standards to private rooms and entire-unit products, which helps defend occupancy and reduce churn even when broader rents are soft.

By Business Model: Asset-Light Management Agreements Displace Asset-Heavy Structures

Asset-light master lease / lease arbitrage held a 46% share in 2025, indicating it remained the largest business model in the China co-living market even as its risk profile worsened. That model expanded quickly in earlier years because operators could scale without buying assets, but it also left them exposed when market rents stopped rising. The weakness became clearer in 2025, as rent deflation compressed margins while lease commitments remained fixed, limiting operators' earnings flexibility with large leased portfolios. In contrast, the asset-light management agreement is projected to grow at a 16.90% CAGR through 2031, making it the fastest-moving model in the market. That growth reflects a wider operator shift toward fee income and away from direct rent-cycle exposure.

The economics of the model are attractive because operators can earn 20% to 30% of rental revenue as a management fee while avoiding the balance-sheet burden of long-term lease liabilities. Mofang’s joint venture with Shanghai Huayi Holdings Group Co. Ltd. showed how this approach works in practice, with the state entity holding the asset and the private company handling operations. This split between public ownership and private management is important because affordable rental housing expansion is both a competitive threat at the low end and a direct source of management contracts. Asset-heavy own-develop-operate structures are also drawing renewed interest, but mainly through institutional partnerships such as the Invesco Real Estate and Ziroom platform rather than through standalone operator expansion. Even so, 3- to 5-year contract terms create continuity risk, suggesting the China co-living market is likely to reward operators with stronger long-cycle performance records over those relying solely on rapid footprint growth.

By Price Band: Mid-Scale Commands Volume as Premium / Luxury Decouples from the Market

Mid-scale held a 48% share in 2025, making it the largest price band in the China co-living market, as it aligns most closely with the budgets of urban working renters. The segment sits between subsidized economy supply and higher-service premium stock, giving it a broad customer base across younger professionals and longer-stay tenants. Premium / luxury is still the fastest-growing price tier, with a 17.30% CAGR through 2031, indicating that growth is not coming only from low-rent demand. The China co-living market for premium / luxury is expanding as a larger 30-plus renter base places greater value on privacy, reliable operations, and branded living standards. That preference also raises the value of technology integration and better tenant services in higher-priced properties.

Demand resilience at the top end has held up better than the broader rent cycle, as institutionally managed properties in Beijing and Shanghai maintained occupancy rates of 90% to 91% in early 2025, even as general rents declined. Economy co-living faces the most direct competition from subsidized rental housing, and 84% of the new centralized apartment supply in 2025 came from affordable rental projects priced below market alternatives. That pricing gap narrows the room for private operators to compete purely on cost in the lowest tier. Mid-scale, therefore, remains the volume anchor because it serves tenants priced out of ownership and premium stock who are still seeking more stability than informal rentals can provide. Premium / luxury, by contrast, is becoming the clearest path for operators seeking stronger margins and less exposure to state-backed pricing pressure.

By End User: Student Base Sustains Volume While Working Professionals Drive Mix

Students accounted for 53% of the China co-living market in 2025, making them the largest end-user group by volume. Their importance is linked to the annual flow of graduates into major city labor markets, and more than 12.22 million graduates entered the labor force in 2025. This seasonal demand supports occupancy around educational and employment clusters, especially in Beijing, Shanghai, and Shenzhen, where rental competition is strongest. Working professionals, however, are projected to grow at a 17.50% CAGR through 2031, making them the fastest expanding end-user segment in the China co-living market. That faster growth shows how the sector is shifting from a temporary graduate solution toward a longer-duration urban housing format.

Product design is changing alongside that renter mix, as operators move away from dormitory-style shared rooms toward private rooms, studio, and family-compatible layouts. The 2025 Shanghai Youth Renting Trend Report found that more than 70% of young Shanghai renters lived with partners, children, or parents, which supports the case for more flexible unit formats rather than single-occupant products alone. This matters because operators who remain too narrowly focused on single young tenants risk missing a larger, more stable renewal base. Working professionals usually renew more consistently and show less vacancy sensitivity than students, thereby improving revenue visibility. Students still provide important intake volume, but the quality of earnings in the China co-living market is increasingly shaped by older renters who want convenience, privacy, and dependable service over longer stays.

Geography Analysis

Beijing accounted for 28% of the China co-living market size in 2025 and remains the clearest example of institutional depth in the sector. The city had 243 operational co-living projects and nearly 116,000 units at the end of 2025, with average rents of CNY 121 (USD 16.6) per square meter per month and an occupancy rate of 91%[2]JLL China, “Investment Opportunities in Rental Housing, 15th Five-Year Plan Outlook,” JLL China, joneslanglasalle.com.cn. That occupancy level shows that quality-managed stock is still attracting tenants, even in a softer national rental market. Bulk investment transactions totaling RMB 3.1 billion (USD 426.4 million) across 3 deals in 2025 confirmed that Beijing continues to attract global capital into rental housing projects. New supply remains concentrated in outer districts such as Chaoyang, Fengtai, and Daxing, reflecting land cost constraints within the core urban ring.

Shanghai is the fastest-growing city in the China co-living market, with a projected 17.90% CAGR through 2031 and the largest supply base among major gateway cities. The city had 695 projects and nearly 330,000 units at the end of 2025, with average rents of CNY 113 (USD 15.5) per square meter per month. Bulk transaction volume reached RMB 8.24 billion (USD 1.13 billion) in 2025, more than 2.6 times Beijing’s total and underscoring Shanghai’s role as the main institutional investment hub. The city’s talent inflow remained strong between 2021 and 2025, widening the future renter base for institutional housing. Its commercial building conversion policy is also creating a new supply channel from underused office assets, giving Shanghai an advantage in expanding managed rental stock without waiting for new land supply.

Shenzhen and Guangzhou form the Pearl River Delta hub of the China co-living market, with Shenzhen’s centralized co-living supply reaching 281,000 units in the first quarter of 2026, the second largest among China’s 8 core cities. Shenzhen’s renter mix is shaped by technology employment, which supports a stronger demand for premium and mid-scale housing than in many other cities. Guangzhou is using commercial-to-rental conversion policies to add supply, while its employment base keeps demand broad in affordable and mid-scale formats. Beyond the 4 gateway cities, Chengdu, Hangzhou, Suzhou, and other new Tier-1 markets are entering a more quality-focused development phase, with transaction growth in the first half of 2026 indicating that new demand centers are emerging outside the traditional core.

Competitive Landscape

The China co-living market is moderately consolidated, with a leading group of operators strengthening their positions through scale, institutional partnerships, and diversified operating models. Vanke’s Port Apartment and Longfor’s Guanyu remain the leading brands, and the top 30 operators managed 1.98 million rooms at the end of 2025, up 13% year on year[3]China Real Estate Association, “2025 China Housing Rental Industry Monitoring Report, Mid-Year Edition,” China Real Estate Association, fangchan.com. State-owned enterprises also expanded their presence, accounting for more than 20% of the top 30 operators in 2025, reflecting the growing importance of policy-backed capital and government participation in market expansion. As a result, larger operators benefit from stronger financing capabilities, broader land access, and greater operating scale than smaller competitors.

Leading companies are increasingly shifting toward asset-light expansion, institutional collaboration, and professional management services. In February 2025, Invesco Real Estate and Ziroom established Izara Holdings to invest in and operate rental housing assets across China, launching a 1,500-room project in Beijing with a total investment of RMB 1.2 billion (USD 165 million). Mofang Living formed a management agreement joint venture with Shanghai Huayi Holdings Group Co. Ltd., highlighting the industry's transition from traditional lease-arbitrage models toward fee-based management services. Meanwhile, Vanke's Port Apartment reported 273,000 managed long-term rental apartments during the first half of 2025, including more than 130,000 affordable rental units and partnerships with over 6,200 corporate clients. These developments demonstrate how institutional partnerships and scalable operating platforms are reinforcing the competitive positions of leading operators.

Technology, compliance, and operational efficiency are becoming increasingly important competitive differentiators across the China co-living market. Larger operators continue to invest in digital tenant management, standardized maintenance, and portfolio-wide compliance systems, strengthening their ability to secure contracts from institutional and public-sector asset owners. The expansion of affordable rental housing REITs since 2022 has further improved financing and capital recycling opportunities for established operators. While regional and niche providers continue to compete in specific markets, the China co-living market is expected to remain moderately consolidated, with competitive advantages increasingly driven by institutional partnerships, operational capability, access to capital, and technology-enabled management rather than portfolio size alone.

China Co-Living Industry Leaders

Ziroom

Danke Apartment

Mofang Living

Anxin Apartment

Tujia Coliving

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: China Rongtong Real Estate disclosed that its long-term rental brand "Rongyu" had expanded to 19 cities nationally as of Q1 2026, with total housing supply, including units under construction and in operation, surpassing 20,000. Average occupancy across operating projects held above 90%, with the Wuhan Jianghan Road property specifically recording a dynamic occupancy rate above 90% and a resident satisfaction score of 95%. The disclosure marks a significant capacity milestone for a centrally backed state enterprise operator.

- May 2026: Xinhua Net and Ziroom Research Institute jointly released the 2026 China Urban Long-term Rental Market Development Blue Book in Beijing, the sector's first comprehensive structural review under China's Housing Rental Regulations (implemented September 2025). Key findings include approximately 80% of China's 260 million renters now accept tenancies of five or more years; renters aged 30 and above exceeded 50% of institutional housing occupants for the first time in 2025; and over 70% of tenants now co-rent with family members, marking a decisive demand shift from transient shared accommodation toward family-grade, quality-focused co-living.

- September 2025: China’s Housing Rental Regulations (State Council Order No. 812, issued July 16, 2025) took effect on September 15, 2025, establishing the first comprehensive national legal framework for the residential rental sector. The regulations mandate contract registration, set occupancy density standards, and place the national supervisory authority with the Ministry of Housing and Urban-Rural Development (MOHURD).

China Co-Living Market Report Scope

The China Co-Living Market Report is Segmented by Property Configuration (Studio / Entire Unit, Private Room, and Shared Room), Business Model (Asset-Light Master Lease / Lease Arbitrage and More), Price Band (Economy, Mid-Scale, and Premium / Luxury), End User (Students, and Working Professionals), and Region (Beijing, Shanghai, Shenzhen, Guangzhou, and Rest of China). The Market Forecasts are Provided in Terms of Value (USD).

| Studio / Entire Unit |

| Private Room |

| Shared Room |

| Asset-Light Master Lease / Lease Arbitrage |

| Asset-Light Management Agreement |

| Asset-Heavy Own-Develop-Operate |

| Economy |

| Mid-Scale |

| Premium / Luxury |

| Students |

| Working Professionals |

| Beijing |

| Shanghai |

| Shenzhen |

| Guangzhou |

| Rest of China |

| By Property Configuration | Studio / Entire Unit |

| Private Room | |

| Shared Room | |

| By Business Model | Asset-Light Master Lease / Lease Arbitrage |

| Asset-Light Management Agreement | |

| Asset-Heavy Own-Develop-Operate | |

| By Price Band | Economy |

| Mid-Scale | |

| Premium / Luxury | |

| By End User | Students |

| Working Professionals | |

| By City | Beijing |

| Shanghai | |

| Shenzhen | |

| Guangzhou | |

| Rest of China |

Key Questions Answered in the Report

What is the current outlook for China co-living demand through 2031?

The sector is projected to grow from USD 0.62 billion in 2026 to USD 1.30 billion by 2031 at a 15.96% CAGR, supported by urban renter growth, stronger regulation, and rising demand for formal managed housing.

Which tenant group drives the largest volume in China co-living?

Students remained the largest end-user group with 53% share in 2025, supported by the annual entry of more than 12.22 million graduates into urban labor markets.

Which business model is gaining the most traction in managed rental housing in China?

Management agreement is the fastest-growing model at a 16.9% CAGR through 2031 because it allows operators to earn fee income without taking direct rent-cycle risk on long lease liabilities.

Why are Beijing and Shanghai so important for this space?

Beijing held 28% share in 2025, while Shanghai is the fastest-growing city at 17.90% CAGR, and both cities combine deep renter demand with stronger policy support and institutional capital access.

Page last updated on: