China Automotive Reed Sensors/Switches Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

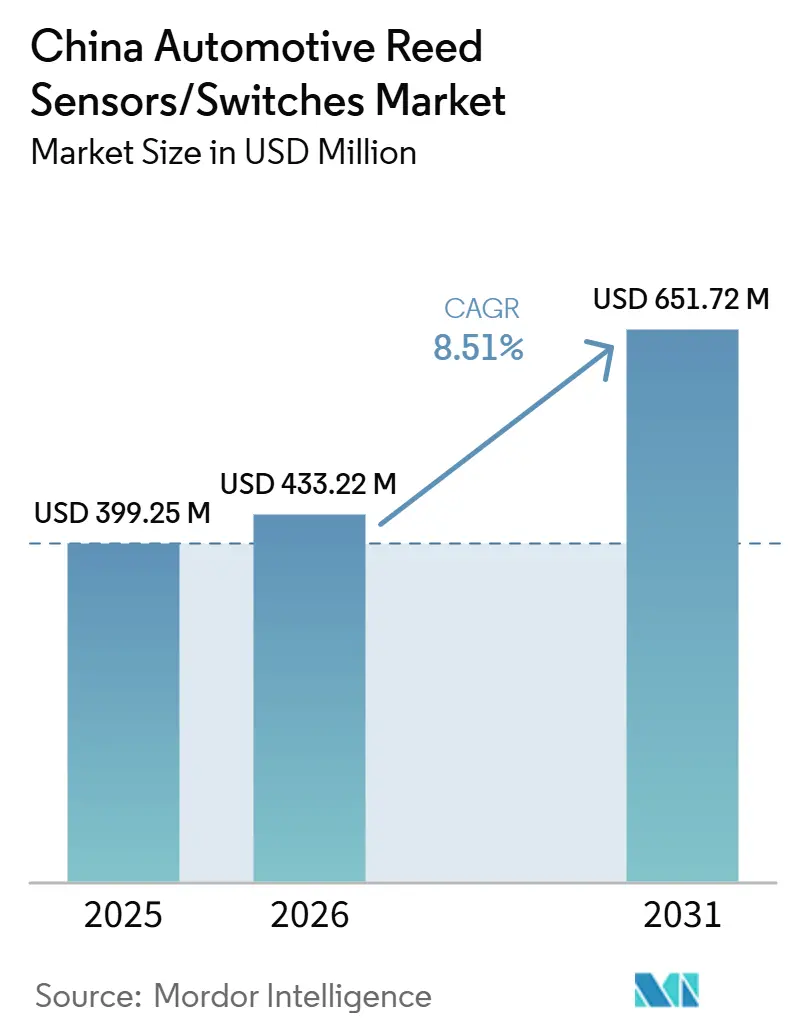

| Base Year Market Size (2025) | USD 399.25 Million |

| Market Size (2026) | USD 433.22 Million |

| Market Size (2031) | USD 651.72 Million |

| Growth Rate (2026 - 2031) | 8.51% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

China Automotive Reed Sensors/Switches Market Analysis by Mordor Intelligence

The China Automotive Reed Sensors/Switches Market size is expected to increase from USD 399.25 million in 2025 to USD 433.22 million in 2026 and reach USD 651.72 million by 2031, growing at a CAGR of 8.51% over 2026-2031. China is the world's largest automotive market by unit volume and the most advanced large market in vehicle electrification. These two structural factors directly expand the addressable demand for automotive reed sensors and switches across multiple vehicle subsystems. High vehicle production volumes sustain baseline demand in body electronics. At the same time, rapid electrification increases sensing density per vehicle, particularly in battery safety loops, charge-port detection, high-voltage interlock paths, and charging-related interfaces. Compared with markets with a higher share of internal combustion engine vehicles, China's product mix inherently supports more magnet-based sensing points per vehicle.

Alongside vehicle electrification, China's charging ecosystem has scaled rapidly, reinforcing downstream demand for charging-related sensing components. The large installed base of public and private charging piles increases the need for reliable detection and safety mechanisms within charging equipment and vehicle-side interfaces. Reed sensors and switches are commonly used in connector engagement detection, access-door monitoring, and safety-state verification, supporting sustained growth in charging-adjacent applications as infrastructure density increases.

Policy support remains a critical stabilizing factor for demand. The extension of new energy vehicle purchase tax incentives through 2027 improves volume visibility for OEMs and suppliers and supports continued penetration of electrified platforms. This policy continuity strengthens the medium-term outlook for battery- and charging-related sensing points, ensuring that growth in reed sensors and switches is supported not only by market scale but also by regulatory alignment with long-term electrification objectives[1]"China’s auto output, sales both reach new heights in 2024," China Daily (Xinhua), chinadaily.com.cn..

Key Report Takeaways

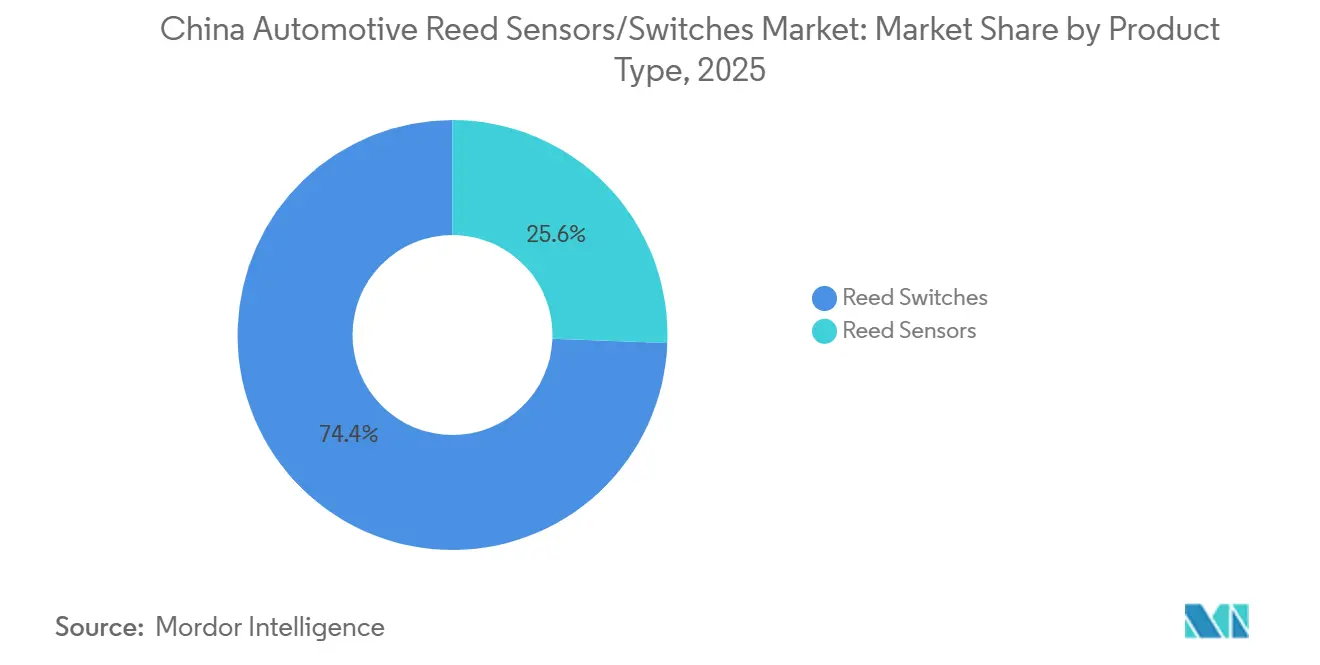

- By product type, reed switches led in 2025 with 74.37%, while reed sensors are projected to grow fastest during 2026–2031 at a 10.27% CAGR.

- By application, body electronics led in 2025 with 45.16%, while battery and charging systems are projected to grow fastest during 2026–2031 at a 13.97% CAGR.

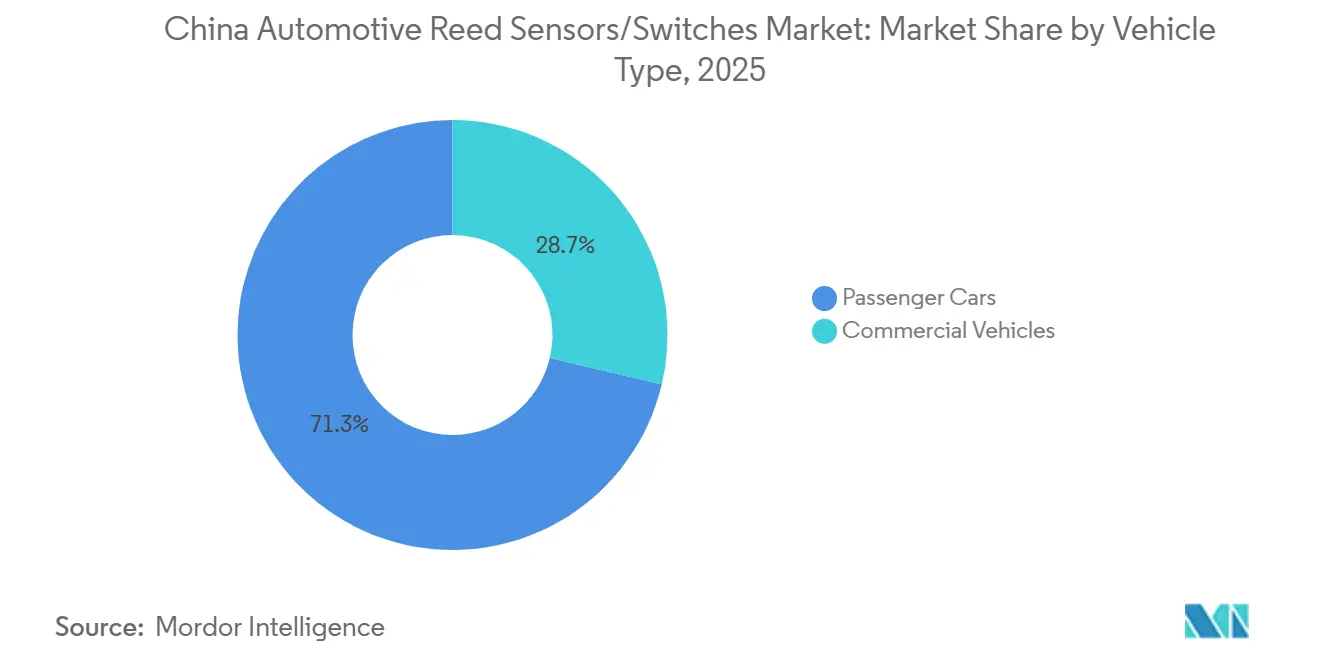

- By vehicle type, passenger cars led in 2025 with 71.28%, while commercial vehicles are projected to grow fastest during 2026–2031 at a 9.67% CAGR.

- By sales channel, OEMs led in 2025 at 78.34% and are projected to remain the fastest-growing channel during 2026–2031, with a 9.07% CAGR.

- By propulsion type, internal combustion engine vehicles led in 2025 with 63.27%, while battery electric vehicles are projected to grow fastest during 22026–2031 at a 14.97% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China Automotive Reed Sensors/Switches Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| NEV Penetration And Scale | +1.7% | National (Tier-1/2 Cities Lead) | Short term (≤ 2 years) |

| Charging Infrastructure Expansion | +1.2% | Urban + Expressway Networks | Short term (≤ 2 years) |

| OEM Platform Design-Ins | +1.0% | National | Short term (≤ 2 years) |

| Passenger Vehicle Volume Base | +0.8% | National | Medium term (2-4 years) |

| EV Supply Chain Localization | +0.7% | Coastal + Industrial Provinces | Medium term (2-4 years) |

| Module Density And Integration | +0.5% | OEM/Tier Programs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High NEV Penetration Increasing EV-Associated Sensing Points

China’s high NEV penetration increases the number of sensing points per vehicle, particularly across battery systems and high-voltage subsystems. NEV architectures typically require additional state-detection nodes for safety loops and operational readiness, including pack cover status, service disconnect detection, charge-port state detection, and high-voltage interlock confirmation. This increases the addressable demand for sensors and switches used for binary open/closed and presence/absence detection.

The scale of NEV penetration also matters from a sourcing standpoint. As NEVs represent a larger share of new vehicle sales, EV-linked sensing moves from niche to high-volume platform design. This supports wider standardization of EV subsystem sensing points and increases recurring demand for component suppliers aligned with battery and charging applications [2]"China extends preferential purchase tax policy for NEVs," State Taxation Administration (Xinhua via STA site), chinatax.gov.cn..

Rapid Charging Infrastructure Expansion Supporting Charging Ecosystem Demand

China’s charging infrastructure build-out supports NEV adoption by improving charging availability and usability. Expanding public and private charging points increases the installed base of charging equipment and vehicle-side interfaces that rely on detection and safety switching. This supports demand for sensing solutions for connector engagement detection, access-door monitoring, and safety interlocks associated with charging operations.

Charging infrastructure expansion also increases component pull-through beyond vehicles. Higher utilization and wider coverage support growth in charging hardware deployments, and these systems typically include safety-state monitoring nodes for enclosure access, connector presence, and operational status. This reinforces battery and charging systems as the highest-growth application area for reed sensors and switches over the forecast period.

Large Vehicle Production Base Sustaining High-Volume Electronics Demand

China’s vehicle market scale sustains a large, recurring demand base for automotive electronics, including body electronics and control modules. High production volumes translate into great aggregate demand for sensors and switches used in closures, latches, seat mechanisms, door and hood status detection, and other body-control functions. These applications are present across ICE and NEV platforms, supporting stable baseline demand.

In addition, high model proliferation and frequent platform updates increase the number of electronics-rich variants in production. As OEMs expand feature content across segments, the number of sensing nodes per vehicle increases, supporting continued demand for simple, reliable state-detection solutions in body electronics and related modules.

NEV Policy Support Supporting EV Demand Resilience

Policy continuity supports demand stability for NEVs and reduces short-term volatility for suppliers planning capacity and sourcing programs. Purchase incentive structures and extended policy timelines sustain NEV volumes, which in turn support the installed base of EV battery and charging sensing points. This strengthens the demand foundation for components linked to electrification, including safety-state and interlock-related sensing nodes.

Policy support also reinforces OEM commitment to NEV platform expansion. With clearer demand expectations, OEMs and Tier-1 suppliers can sustain investment in EV architectures and supply chain localization. This improves the predictability of EV-linked component demand and supports multi-year sourcing programs for sensors and switches.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Solid-State Sensor Substitution | -1.2% | National | Medium term (2-4 years) |

| OEM Cost-Down Pressure | -1.0% | National | Medium term (2-4 years) |

| Overcapacity And Price Erosion | -0.8% | Key Manufacturing Provinces | Short term (≤ 2 years) |

| Platform Consolidation Reducing Part Counts | -0.6% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Substitution by Semiconductor Magnetic Sensors in Some Applications

In several vehicle subsystems, semiconductor-based magnetic sensing technologies can replace reed-based solutions, particularly where continuous measurement, diagnostic capability, or tighter ECU integration is required. As vehicle architectures adopt more centralized computing and software-defined features, OEMs may standardize Hall or TMR solutions in selected nodes to support signal conditioning and diagnostics within IC-based systems.

This substitution pressure does not eliminate the use of reed switches across all applications. However, it can reduce penetration in areas where OEMs require continuous sensing or enhanced diagnostic functions, particularly in advanced electrified platforms. Supplier positioning, therefore, depends on application fit, cost targets, and the level of diagnostic capability required by the platform.

Intense Price Competition Compressing Component ASPs and Margins

China's automotive market is highly competitive, and aggressive pricing pressure is pushing OEMs and Tier-1 suppliers toward rapid cost-reduction roadmaps. This typically increases dual-sourcing, accelerates localization, and compresses component average selling prices. Even when unit demand grows, value capture for component suppliers can be limited if pricing pressure outpaces content growth.

This restraint is particularly relevant in high-volume vehicle segments where cost targets are tightly controlled, and sourcing decisions prioritize scale and pricing. Component suppliers must therefore compete on both cost and reliability while maintaining automotive-grade quality and delivery performance in a market characterized by rapid product cycles and high procurement intensity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Reed Switches Lead Today; Reed Sensors Expand Faster

Reed switches are the largest product type in China’s automotive reed sensors/switches market, with a 74.37% market share in 2025. Their leadership is driven by broad deployment in high-volume automotive modules, where binary-state detection is required with high reliability and low cost. Reed switches remain widely used in body electronics and distributed vehicle functions, where sealed magnetic actuation provides consistent performance under vibration, temperature variation, and long duty cycles.

Reed sensors are projected to grow at the fastest rate, registering a CAGR of 10.27% during the forecast period. Faster growth reflects increasing OEM and Tier-1 preference for packaged and overmolded sensor assemblies that improve mounting consistency and manufacturing efficiency. In parallel, the expansion of EV subsystems favors sensor formats specified as module-ready components rather than discrete elements, thereby supporting broader adoption of reed sensors in compact and integration-intensive applications.

By Application: Body Electronics Anchor Demand; Battery and Charging Systems Lead Growth

Body electronics constitute the largest application segment, accounting for 45.16% in 2025. China’s large vehicle production base and high feature penetration across passenger vehicle segments sustain significant volumes of state detection related to closures and access. Applications such as doors, trunk and hood latches, seat mechanisms, and comfort modules remain present across nearly all vehicle platforms, anchoring demand for reed sensors and switches.

Battery and charging systems are projected to grow at the fastest pace, registering a CAGR of 13.97% during 2026–2031. Growth is supported by the continued expansion of China’s EV ecosystem, which increases sensing requirements related to charge-port detection, connector engagement, high-voltage interlocks, pack cover status, service disconnects, and other safety-state monitoring functions. These EV-specific architectures increase sensing density per vehicle, supporting above-average growth for reed-based solutions in these subsystems.

By Vehicle Type: Passenger Cars Dominate; Commercial Vehicles Grow Faster

Passenger cars represent the largest vehicle type segment, with a market share of 71.28% in 2025. This reflects China’s high passenger-vehicle volumes and the rapid adoption of electronics-rich architectures across trim levels. Passenger vehicles also account for a large share of electrification uptake, reinforcing both baseline and growth demand for reed sensors and switches across body electronics and EV-adjacent modules.

Commercial vehicles are projected to grow at a faster rate, registering a CAGR of 9.67% during the forecast period. Faster growth is supported by increasing electronics penetration in trucks and buses, along with selective electrification in urban delivery, public transport, and fleet applications. These platforms introduce additional sensing points per vehicle, even though absolute volumes remain smaller than those of passenger cars.

By Sales Channel: OEMs Dominate and Remain the Primary Growth Engine

OEMs represent the dominant sales channel, accounting for 78.34% in 2025. They are also projected to be the fastest-growing channel, registering a CAGR of 9.07% during 2026–2031. This indicates that demand for reed sensors and switches in China is primarily design-in-driven, with components specified at the platform and module levels and scaled through vehicle production and new-model launches.

The aftermarket continues to play a role in replacement demand, particularly for body electronics modules and serviceable switch assemblies. However, market data indicates that the majority of incremental growth will continue to be driven by OEM-led sourcing programs rather than replacement-driven channels.

By Propulsion Type: ICE Leads Current Volume; BEVs Expand the Fastest

Internal combustion engine vehicles remain the largest propulsion segment, with a market share of 63.27% in 2025. This reflects the still-large installed base and ongoing production volumes of ICE vehicles, which continue to rely on reed sensors and switches for body electronics and conventional control applications.

Battery electric vehicles are projected to register the fastest growth, with a CAGR of 14.97% during 2026–2031. This growth aligns with BEV architectures, introducing additional sensing requirements in battery packs, charging systems, and high-voltage safety circuits. Continued scaling of BEV penetration positions battery electric vehicles as the key propulsion-linked growth driver for reed sensors and switches in China over the forecast horizon.

Geography Analysis

Demand for automotive reed sensors and switches in China is concentrated in regions with the highest vehicle production output and the most developed automotive supply chains. Major automotive manufacturing hubs and adjacent Tier-1 and Tier-2 supplier clusters drive OEM-led demand, as reed solutions are typically engineered into modules and sourced through factory-fit supply chains. These regions benefit from higher platform throughput, faster model refresh cycles, and greater electronics integration, which collectively increase the number of sensing points per vehicle and support large-volume procurement.

Demand growth is stronger in provinces and metropolitan areas with higher NEV penetration and denser charging infrastructure. Higher adoption of battery-electric vehicles and plug-in hybrids increases sensing requirements for battery and charging subsystems, including high-voltage safety interlocks and charging-interface monitoring.

As charging coverage expands across urban networks and intercity corridors, demand for EV-related sensing is broadening beyond early-adopter regions. Meanwhile, body-electronics demand remains widely distributed nationwide, supported by China's large installed vehicle base and service ecosystem.

Competitive Landscape

Competition in China's automotive reed sensors and switches market is shaped by vehicle platform cycle scale and speed, strong localization expectations across the automotive electronics supply chain, and aggressive cost reduction targets driven by intense price competition.

Suppliers capable of delivering automotive-grade reliability at scale while offering miniaturized form factors, such as SMD-compatible solutions, are better positioned to secure sustained sourcing programs.

At the technology level, suppliers increasingly maintain broad portfolios spanning reed, Hall-effect, and tunneling magnetoresistance (TMR) sensing technologies. This multi-technology approach allows suppliers to retain share when OEMs adjust sensing architectures or standardize alternative solutions for specific applications. The ability to support high-volume programs, meet localization requirements, and compete on cost remains central to competitive positioning in China's automotive sensing market.

China Automotive Reed Sensors/Switches Industry Leaders

-

Littelfuse Inc.

-

Standex Electronics

-

Coto Technology

-

PIC GmbH

-

Honeywell International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Government-reported data indicated that China had 11.43 million charging piles by the end of September 2024, supporting the build-out of the charging ecosystem tied to EV growth and EV subsystem component demand.

- February 2024: Standex announced it closed the acquisition of Sanyu Switch, expanding its reed-based switching portfolio and strengthening its electronics platform across Asian manufacturing/supply networks.

China Automotive Reed Sensors/Switches Market Report Scope

Automotive reed sensors/switches are magnetically actuated switching/sensing components used to detect position, proximity, presence, or limit states in vehicle systems. Reed switches typically use hermetically sealed contacts inside a glass capsule actuated by a magnetic field, while reed sensors generally package the reed element into application-ready formats (SMD housings, molded packages, or cabled/connectorized sensors) suited to automotive module integration.

The scope includes segmentation by Product Type (Reed Switches and Reed Sensors), Application (Body Electronics, Battery and Charging Systems, Powertrain & Drivetrain, Safety & Security Systems, and Others), Vehicle Type (Passenger Cars and Commercial Vehicles), Sales Channel (OEMs and Aftermarket), Propulsion Type (Internal Combustion Engine (ICE) Vehicles, Hybrid Electric Vehicles (HEV), Plug-in Hybrid Electric Vehicle (PHEV), Battery Electric Vehicles (BEV), and Fuel Cell Electric Vehicles (FCEV)). The market forecasts are provided in terms of value (USD).

| Reed sensors |

| Reed switches |

| Engine and Powertrain Systems |

| Body Electronics |

| Safety and Security Systems |

| Infotainment and Comfort Systems |

| Transmission and Braking Systems |

| Battery and Charging Systems |

| Other Applications |

| Passenger Cars |

| Commercial Vehicles |

| OEMs |

| Aftermarket |

| Internal Combustion Engine (ICE) Vehicles |

| Hybrid Electric Vehicles (HEV) |

| Plug-in Hybrid Electric Vehicle (PHEV) |

| Battery Electric Vehicles (BEV) |

| Fuel Cell Electric Vehicles (FCEV) |

| By Product Type | Reed sensors |

| Reed switches | |

| By Application | Engine and Powertrain Systems |

| Body Electronics | |

| Safety and Security Systems | |

| Infotainment and Comfort Systems | |

| Transmission and Braking Systems | |

| Battery and Charging Systems | |

| Other Applications | |

| By Vehicle Type | Passenger Cars |

| Commercial Vehicles | |

| By Sales Channel | OEMs |

| Aftermarket | |

| By Propulsion Type | Internal Combustion Engine (ICE) Vehicles |

| Hybrid Electric Vehicles (HEV) | |

| Plug-in Hybrid Electric Vehicle (PHEV) | |

| Battery Electric Vehicles (BEV) | |

| Fuel Cell Electric Vehicles (FCEV) |

Key Questions Answered in the Report

What is the current value of the China automotive reed sensors/switches market?

It stands at USD 399.25 million in 2025 and is projected to reach USD 651.72 million by 2031 (8.51% CAGR).

Which product type leads the China market today?

Reed switches lead with 74.37% in 2025 due to broad design-in across high-volume vehicle modules.

Which application is growing the fastest and why?

Battery and charging systems are growing fastest (13.97% CAGR, 2026-2031) as electrification increases sensing points in EV subsystems.

Which propulsion type will expand the quickest through 2031?

Battery electric vehicles grow fastest (14.97% CAGR,2026-2031) as BEV penetration lifts EV-associated sensing demand.

Which sales channel dominates demand in China?

OEMs dominate with 78.34% in 2025 because most components are specified at the platform/module level.

Page last updated on: