Market Overview

| Study Period | 2020 - 2030 |

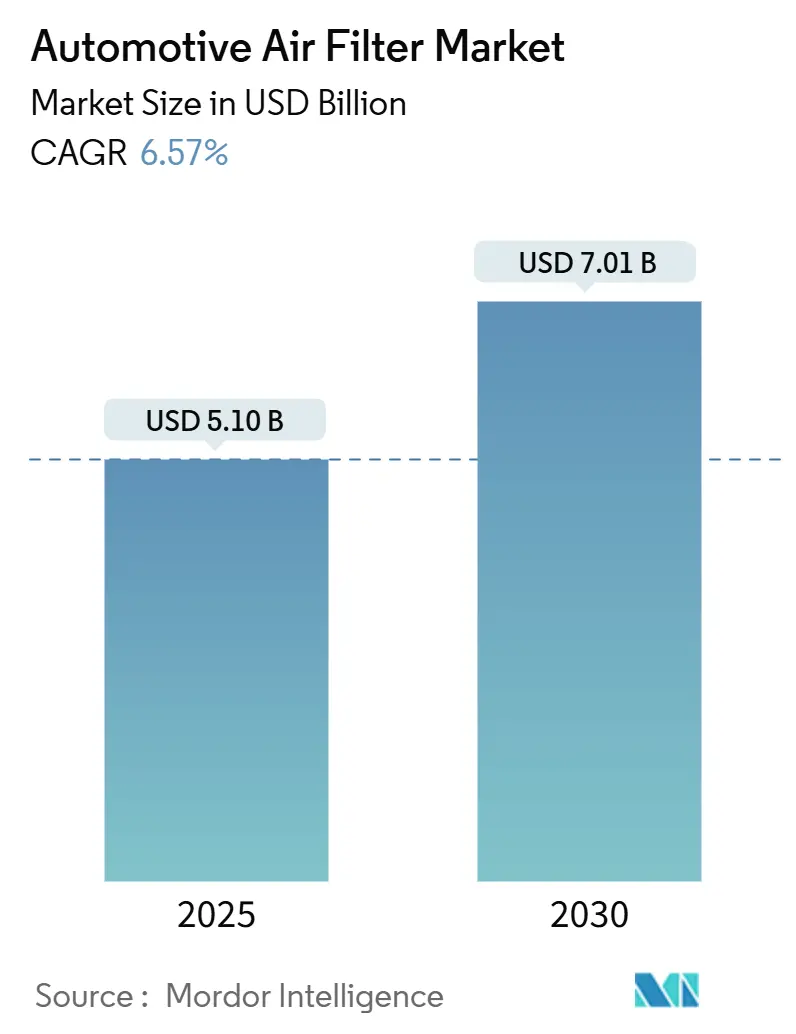

| Market Size (2025) | USD 5.10 Billion |

| Market Size (2030) | USD 7.01 Billion |

| Growth Rate (2025 - 2030) | 6.57% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Air Filter Market Analysis by Mordor Intelligence

The automotive air filtration market size stands at USD 5.10 billion in 2025 and is forecast to reach USD 7.01 billion by 2030, advancing at a 6.57% CAGR. Tightening emission norms in Europe, North America, and key Asian economies, together with consumer attention to in-cabin air quality, sustain a robust demand pipeline. Original equipment manufacturers (OEMs) increasingly specify high-efficiency particulate air (HEPA) systems and electrostatic nano-fiber media to comply with Euro 7, EPA 2027–2032 multi-pollutant standards, and Bharat Stage VI rules. Electric-vehicle (EV) platforms amplify the opportunity because battery thermal systems and silent cabins highlight filtration performance differences. At the same time, aftermarket distributors leverage predictive maintenance data to position premium replacement filters, countering the lengthening service intervals delivered by synthetic media.

Key Report Takeaways

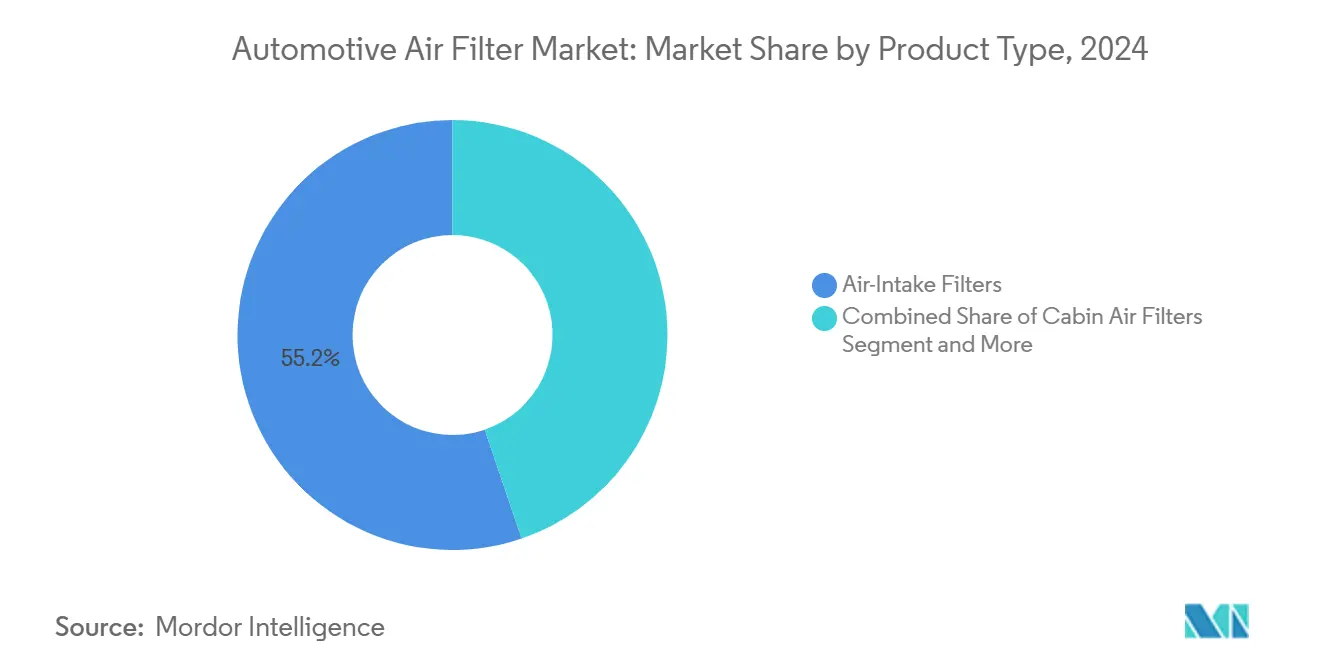

- By product type, air-intake filters led the automotive air filtration market with 55.21% of the share in 2024, whereas cabin filters are projected to record the fastest 9.21% CAGR to 2030.

- By filter media, cellulose retained 44.18% revenue share in 2024; nano-fiber and HEPA media are poised to expand at 11.48% CAGR, the highest among all materials.

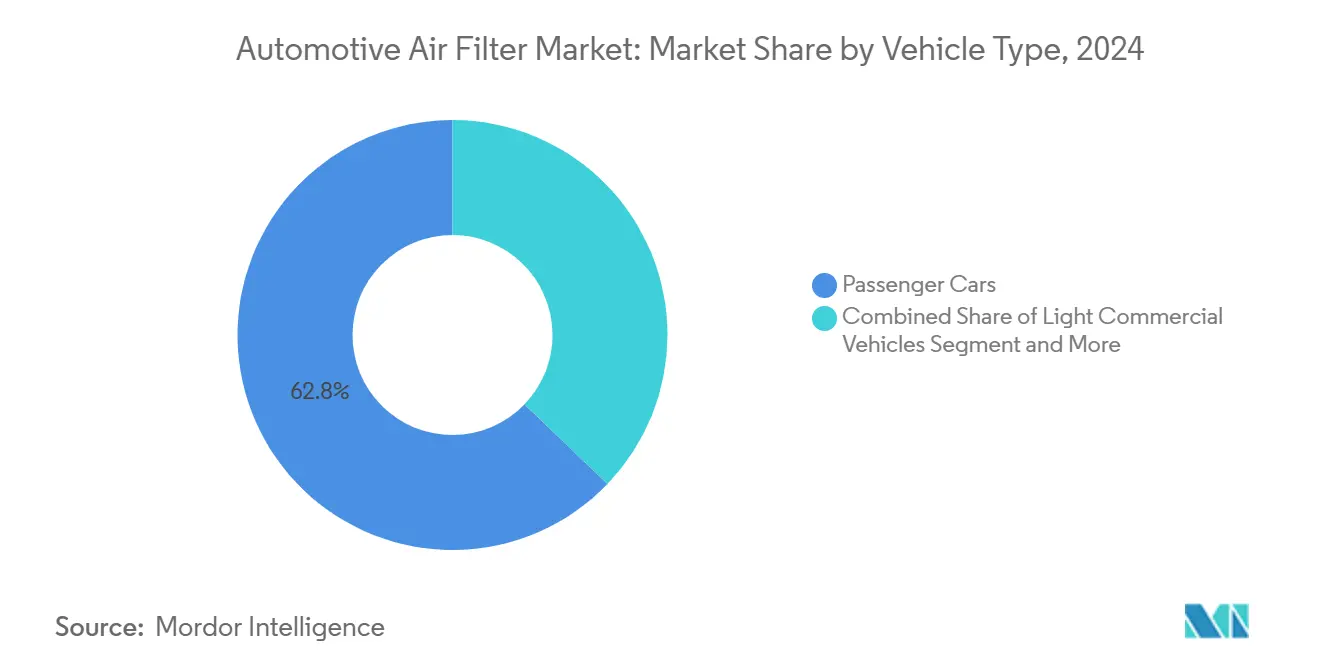

- By vehicle type, passenger cars held 62.82% of the automotive air filtration market size in 2024, while light commercial vehicles are set to grow at a 5.97% CAGR through 2030.

- By sales channel, the aftermarket commanded 58.97% revenue share in 2024 and is anticipated to lead the market with 6.23% CAGR during the forecast period.

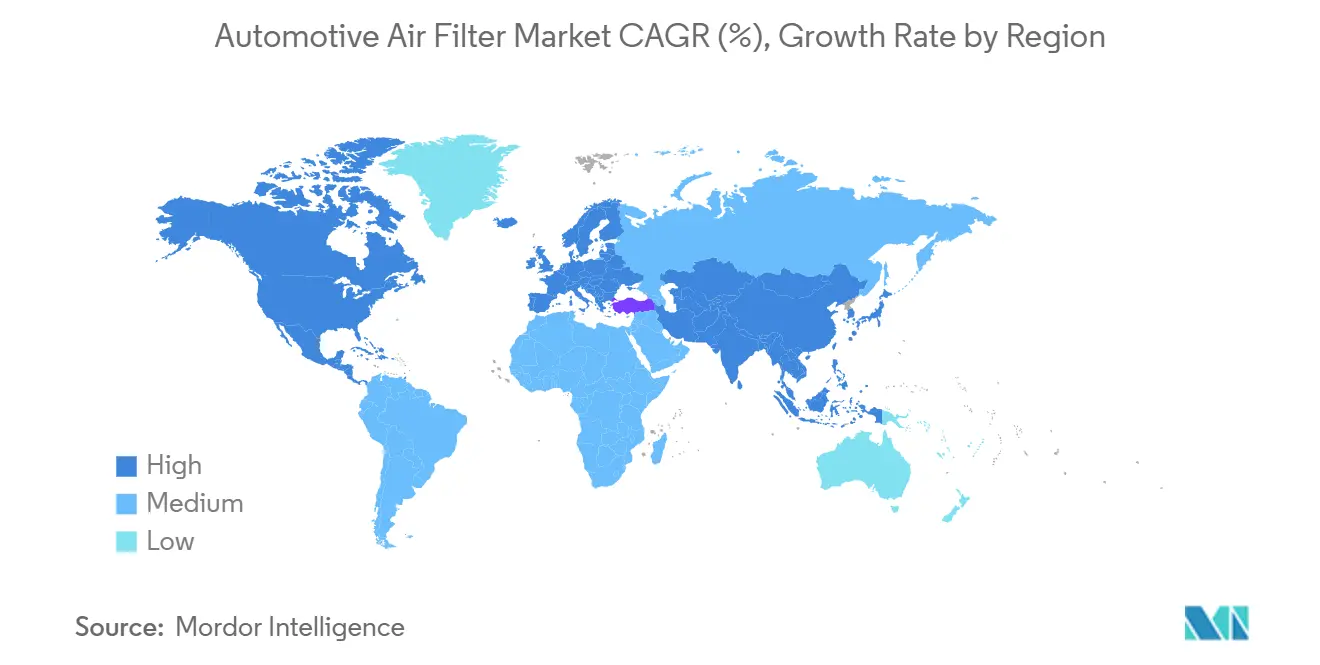

- By geography, Asia-Pacific accounted for 38.75% of the automotive air filter market share in 2024 and is expected to post the quickest 6.41% regional CAGR through 2030.

Global Automotive Air Filter Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Point Impact on Market CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict emission & in-cabin air-quality mandates | +1.8% | Global, with EU and North America leading | Medium term (2-4 years) |

| Growing global vehicle parc & service-interval mileage | +1.2% | Global, concentrated in APAC and emerging markets | Long term (≥ 4 years) |

| Consumer health awareness in high-pollution megacities | +0.9% | APAC core, spill-over to MEA urban centers | Short term (≤ 2 years) |

| HEPA-grade filters adopted by EV & premium OEM platforms | +0.7% | North America & EU, expanding to APAC premium segment | Medium term (2-4 years) |

| Sensor-activated smart HVAC filtration modules | +0.5% | Global, early adoption in premium vehicles | Long term (≥ 4 years) |

| Predictive fleet-maintenance algorithms driving filter turnover | +0.4% | North America & EU commercial fleets | Medium term (2-4 years) |

Source: Mordor Intelligence

Strict Emission & In-Cabin Air-Quality Mandates

Regulatory convergence across major automotive markets creates unprecedented demand for advanced filtration technologies that address engine protection and cabin air quality. The EU's Euro 7 regulation introduces particulate emissions limits from tire and brake wear for the first time, requiring filtration systems to capture particles beyond traditional exhaust emissions.[1]"Euro 7: The new emission standard for light- and heavy-duty vehicles in the European Union," International Council on Clean Transportation, theicct.org. This regulatory expansion coincides with the EPA's Tier 4 standards mandating gasoline particulate filters for vehicles achieving 0.5 mg/mi PM emissions, fundamentally altering the filtration value proposition from an optional comfort feature to a regulatory compliance necessity. Cambodia's adoption of Euro 6/VI standards by 2030 demonstrates regulatory harmonization extending beyond developed markets, creating global scale opportunities for filtration suppliers. The regulatory timeline compression forces OEMs to accelerate filtration technology integration, with compliance deadlines creating artificial demand spikes that benefit suppliers with ready-to-deploy solutions. California's Advanced Clean Cars II program mandating 100% zero-emission vehicle sales by 2035 paradoxically increases filtration demand as EVs require sophisticated cabin air management systems to maintain battery thermal efficiency.

Growing Global Vehicle Parc & Service-Interval Mileage

The expanding global vehicle fleet, particularly in emerging markets, creates sustained aftermarket demand that outpaces new vehicle production growth rates. Extended service intervals, driven by synthetic lubricant adoption and improved engine durability, paradoxically increase filtration system stress as filters must perform longer between replacements while maintaining efficiency standards. This dynamic benefits premium filter manufacturers who can command higher margins for extended-life products that meet OEM specifications. Fleet operators increasingly recognize the benefits of premium filtration for total cost of ownership, with predictive maintenance algorithms enabling condition-based replacement schedules that optimize filter utilization while preventing premature engine wear. The shift toward mobility-as-a-service models intensifies filter replacement frequency as commercial vehicles accumulate higher annual mileage than private passenger cars, creating a more predictable and lucrative replacement cycle for aftermarket suppliers.

Consumer Health Awareness in High-Pollution Megacities

Urban air quality deterioration in major metropolitan areas drives consumer willingness to pay premium prices for advanced cabin filtration systems. Hyundai's introduction of Fine Dust Indicator technology, which displays real-time air quality measurements, transforms cabin air filtration from an invisible commodity to a visible value proposition. This consumer awareness creates market segmentation opportunities where premium vehicles justify HEPA-grade filtration systems as standard equipment while aftermarket suppliers target health-conscious consumers in high-pollution regions. The correlation between air quality index readings and filtration system sales creates predictable demand patterns that enable suppliers to optimize inventory and pricing strategies. CabinAir's technology removes 10 times more PM2.5 particles than standard filters, demonstrates how quantifiable health benefits translate into competitive differentiation and premium pricing power. Regional air quality variations create geographic arbitrage opportunities where suppliers can command higher margins in pollution-prone markets while maintaining cost-competitive positions in cleaner environments.

HEPA-Grade Filters Adopted by EV & Premium OEM Platforms

Electric vehicle manufacturers leverage cabin air quality as a key differentiator, with HEPA-grade filtration becoming standard equipment in premium EV segments. The absence of engine noise in EVs makes HVAC system operation more noticeable, creating consumer expectations for whisper-quiet, high-efficiency filtration systems that maintain performance without generating objectionable noise levels. MANN+HUMMEL's development of filtration solutions specifically for electrified drive systems, including coolant particle filters and cooling air particle filters for battery systems, demonstrates how EV architecture creates new filtration applications beyond traditional cabin and engine air cleaning. Tesla's introduction of bioweapon defense mode, utilizing medical-grade HEPA filtration, establishes consumer expectations that premium EVs should provide hospital-level air purification capabilities. This positioning strategy enables EV manufacturers to justify higher vehicle prices while creating sustained aftermarket revenue streams from specialized filter replacements that command premium pricing due to their advanced specifications and lower production volumes.

Restraints Impact Analysis

| Restraint | (~) % Point Impact on Market CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Long-life synthetic media extending replacement intervals | -0.8% | Global, concentrated in premium vehicle segments | Medium term (2-4 years) |

| Volatile non-woven & activated-carbon prices | -0.6% | Global manufacturing hubs, particularly Asia-Pacific | Short term (≤ 2 years) |

| Sealed "lifetime" cabin-filter modules in luxury EVs reduce aftermarket | -0.5% | North America & EU luxury EV segments | Long term (≥ 4 years) |

| Energy/weight penalty of ultra-high-efficiency media in BEVs | -0.3% | Global EV markets, concentrated in premium segments | Medium term (2-4 years) |

Source: Mordor Intelligence

Long-Life Synthetic Media Extending Replacement Intervals

Advanced synthetic filter media technologies paradoxically constrain market growth by extending service intervals beyond traditional replacement cycles. Nano-fiber coating technologies, such as Hollingsworth & Vose's NANOWEB system, enhance depth filtration and pulse-cleaning capabilities, enabling filters to maintain efficiency longer while reducing replacement frequency. This technological advancement creates a classic innovator's dilemma where superior product performance reduces total addressable market size by decreasing replacement frequency. Premium vehicle manufacturers increasingly specify long-life filtration systems as standard equipment to reduce maintenance costs and improve customer satisfaction scores, inadvertently constraining aftermarket revenue potential. The trend toward "lifetime" sealed cabin filter modules in luxury EVs eliminates aftermarket replacement opportunities entirely, forcing suppliers to capture higher margins during OEM fitment rather than relying on recurring aftermarket sales. Iran's Behran Filter Company, receiving the first "Nano Namad" license for nanotechnology-based car air filters, demonstrates how emerging markets are leapfrogging to advanced filtration technologies that extend service intervals.[2]"Granting Nano Namad license to an industrial company for nanotechnology-based car air filters," Iran Nanotechnology Innovation Council, en.nano.ir. Filter manufacturers must balance technological advancement with business model sustainability, potentially requiring shift toward subscription-based maintenance services or value-added monitoring systems that generate recurring revenue streams independent of physical filter replacement frequency.

Volatile Non-Woven & Activated-Carbon Prices

Raw material price volatility creates margin pressure across the filtration supply chain, with activated carbon and non-woven media costs fluctuating based on petroleum prices and global supply chain disruptions. Concentrating activated carbon production in specific geographic regions creates supply security risks that automotive suppliers must hedge through inventory management or alternative sourcing strategies. New recycling technologies that reduce activated carbon replacement costs by 50% offer potential relief from price volatility while supporting sustainability objectives.[3]"New technology halves cost of recycling activated carbon for removing harmful substances," National Research Council of Science and Technology, techxplore.com. However, the automotive industry's stringent quality requirements and long validation cycles limit suppliers' ability to rapidly adopt alternative materials or suppliers in response to price fluctuations. Energy costs associated with activated carbon regeneration create additional cost pressures, particularly in regions with high electricity prices or carbon taxation policies. Suppliers with vertically integrated manufacturing capabilities or long-term raw material contracts maintain competitive advantages during periods of price volatility, while smaller players face margin compression that may force market consolidation.

Segment Analysis

By Product Type: Cabin Filters Drive Premium Growth

Air-intake filters command 55.21% market share in 2024, reflecting their universal application across all vehicle types and mandatory replacement cycles driven by engine protection requirements. However, cabin air filters emerge as the growth catalyst with 9.21% CAGR through 2030, propelled by consumer health awareness and regulatory mandates for in-cabin air quality improvement.

Bosch's introduction of FILTER+pro cabin air filters with antimicrobial layers effective against viruses, bacteria, and allergens demonstrates how traditional suppliers innovate to capture premium pricing in the cabin filtration segment. The convergence of air quality regulations and consumer health consciousness creates sustained demand for cabin filtration upgrades, with OEMs increasingly specifying HEPA-grade systems as standard equipment in premium vehicle segments. Air-intake filters maintain steady demand driven by engine protection requirements, though growth rates lag cabin filters due to mature technology and established replacement cycles. The electrostatic and nano-fiber segments represent the industry's technological frontier, where suppliers command premium pricing for advanced particle capture capabilities that exceed traditional media performance.

Note: Segment shares of all individual segments available upon report purchase

By Filter Media: Nano-Fiber Technologies Lead Innovation

Cellulose retained a 44.18% share in 2024 because it is inexpensive and well-understood by manufacturers. The automotive air filtration market size for nano-fiber and HEPA media is projected to expand at 11.48% CAGR, a clear indicator that premium, high-efficiency media sets the innovation pace.

Nanofiber layers add depth loading and high dust-holding capacity while maintaining low restriction, a critical benefit for engine performance and HVAC energy efficiency. Suppliers integrate proprietary nano-coatings into traditional substrates to create differentiated SKUs with significant price premiums. Activated-carbon producers invest in recycling technology to combat feedstock price swings, reinforcing the dual performance and sustainability value proposition demanded by automakers and regulators.

By Vehicle Type: Commercial Segments Show Resilience

Passenger cars generated 62.82% revenue in 2024, driven by global scale and diversified product mixes. Light commercial vehicles, catalyzed by e-commerce logistics, grow at 5.97% CAGR, the fastest among all vehicle categories. Fleet operators favor premium filters that extend engine life and support predictive maintenance schedules, producing dependable repeat business.

Commercial vehicles run higher annual mileage, accelerating replacement frequency despite longer-life media. OEMs now specify dual-stage filtration—coarse pre-separators plus fine cabin HEPA elements—to safeguard driveline components and driver health. Suppliers such as UFI build new facilities dedicated to commercial and new-energy vehicle filters to meet specialized requirements. Strict uptime metrics in logistics fleets make filtration a small-cost, high-impact maintenance item, underpinning aftermarket resilience.

Note: Segment shares of all individual segments available upon report purchase

By Sales Channel: Aftermarket Maintains Revenue Leadership

The aftermarket captured 58.97% revenue in 2024 and is projected to hold its lead through 2030 at a 6.23% CAGR. Consumers and fleets value flexibility in selecting performance upgrades, and digital marketplaces simplify access to premium brands. Donaldson’s 12.6% 2024 aftermarket sales jump underscores the segment’s profitability. The automotive air filtration market size for OEM fitment is growing more slowly, but integration of HEPA and sensor-ready modules into factory packages elevates average content per vehicle.

Replacement-driven demand allows aftermarket players to roll out tailored SKUs with region-specific pollutant claims. Strategic e-commerce investments, such as Doc’s Diesel’s USD 4 million Ohio distribution center, expand direct-to-fleet reach. OEM channels still matter for volume and early exposure of new technology to consumers. Vehicle manufacturers increasingly negotiate lifecycle filter programs with suppliers, bundling the first two or three replacements into warranty packages, subtly shifting aftermarket share toward authorized parts networks.

Geography Analysis

Asia-Pacific’s 38.75% share in 2024 is backed by China’s EV surge and India’s Bharat Stage VI norms. The region is anticipated to grow with a 6.41% CAGR during the forecast period. Local suppliers collaborate with global brands to secure advanced media licenses, while cost-efficient manufacturing plants in China, Thailand, and Vietnam feed worldwide demand. Australia’s adoption of Euro 6d-equivalent tailpipe limits further widens the regulatory addressable market.

Euro 7’s inclusion of non-exhaust particles in Europe opens niches for tire-wear capture devices and brake-dust filters. German OEMs spearhead HEPA and sensor integration, often co-engineering with suppliers such as MANN+HUMMEL. Hengst's Romanian plant shows that Eastern Europe’s cost base attracts new capacity. Consumers associate advanced filtration with wellness and environmental responsibility, supporting premium pricing.

The EPA’s 2027–2032 rules in North America guarantee sustained demand for high-efficiency engine-air and cabin systems. California’s zero-emission vehicle mandate stimulates demand for EV-specific thermal-management filters. Hanon Systems’ Ontario EV compressor plant signals supplier investment to serve growing regional EV output. Well-developed aftermarket logistics and strong do-it-yourself cultures ensure rapid uptake of performance upgrades.

Competitive Landscape

Industry concentration is low, as the market has the presence of several OEM and aftermarket companies. MANN+HUMMEL deploys predictive filter-life algorithms linked to vehicle telematics, moving toward service-as-a-software models. Bosch’s FILTER+pro, certified against viruses and allergens, positions the brand at the health-oriented end of the spectrum.

Hengst accelerates inorganic growth through acquisitions of Main Filter and Bosch Rexroth’s hydraulic unit, enhancing its industrial and off-highway breadth. CabinAir captures premium niches by guaranteeing tenfold PM2.5 removal without recirculation, an attractive specification for luxury EV OEMs. Donaldson leverages a diversified media portfolio and an omnichannel distribution model to protect margins across cyclical swings.

Investment funds target filtration assets for their steady aftermarket cash flow. In February 2025, Apollo Fund X invested fresh capital in Tenneco’s Clean Air division, aiming to scale innovation pipelines in particulate management. Suppliers who marry proprietary media science with digital monitoring stand to consolidate share as regulatory and consumer trends converge on demonstrable filtration outcomes.

Automotive Air Filter Industry Leaders

-

MANN+HUMMEL GmbH

-

Freudenberg & Co. KG

-

MAHLE GmbH

-

Robert Bosch GmbH

-

DENSO Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- February 2025: Tenneco announced strategic investment from Apollo Fund X to accelerate growth in Clean Air and Powertrain divisions, with transaction completion expected in Q2 2025. This investment strengthens Tenneco's market position and operational capabilities following its 2022 acquisition by Apollo.

- February 2025: Filtration Technology Corporation expanded manufacturing headquarters by 55,000 square feet to meet growing demand for filtration solutions, including advanced manufacturing equipment.

- July 2024: Hengst Filtration opened a new 15,000 square meter plant in Balș, Romania, producing filters for cleaning appliances and power tools.

Global Automotive Air Filter Market Report Scope

An automotive air filter is a crucial component in a vehicle's intake system that prevents dust, debris, and contaminants from entering the engine. It ensures a clean air supply, promoting optimal engine performance and longevity while also enhancing fuel efficiency and reducing harmful emissions.

The automotive air filter market has been segmented into type (air intake filters and cabin air filters), vehicle type (passenger cars and commercial vehicles), and geography (North America, Europe, Asia-Pacific, and the Rest of the World).

The report offers market size and forecasts for all the above segments in terms of value (USD).

| By Product Type | Air-Intake Filters | ||

| Cabin Air Filters | |||

| Hybrid / Electrostatic Nano-fiber Filters | |||

| Electrically-enhanced (ePM1) Filters | |||

| By Filter Media | Cellulose | ||

| Synthetic/Melt-blown | |||

| Activated-Carbon Composite | |||

| Nano-fiber/HEPA Grade | |||

| By Vehicle Type | Passenger Cars | ||

| Light Commercial Vehicles | |||

| Medium and Heavy Commercial Vehicles | |||

| By Sales Channel | OEM Fitment | ||

| Aftermarket | |||

| By Geography | North America | United States | |

| Canada | |||

| Rest of North America | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia & New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | GCC Countries | ||

| Turkey | |||

| South Africa | |||

| Rest of Middle East and Africa | |||

By Product Type

| Air-Intake Filters |

| Cabin Air Filters |

| Hybrid / Electrostatic Nano-fiber Filters |

| Electrically-enhanced (ePM1) Filters |

By Filter Media

| Cellulose |

| Synthetic/Melt-blown |

| Activated-Carbon Composite |

| Nano-fiber/HEPA Grade |

By Vehicle Type

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

By Sales Channel

| OEM Fitment |

| Aftermarket |

By Geography

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia & New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC Countries |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How big is the Automotive Air Filter Market?

The Automotive Air Filter Market size is expected to reach USD 5.10 billion in 2025 and grow at a CAGR of 6.59% to reach USD 7.01 billion by 2030.

What is the current Automotive Air Filter Market size?

In 2025, the Automotive Air Filter Market size is expected to reach USD 5.10 billion.

What is the current size of the automotive air filtration market?

The market is valued at USD 5.10 billion in 2025 and is projected to reach USD 7.01 billion by 2030 on a 6.59% CAGR.

Which product type is growing fastest?

Cabin air filters post the highest 9.2% CAGR thanks to rising consumer focus on in-cabin health and stricter air-quality rules.

Why are HEPA filters gaining popularity in vehicles?

HEPA and nano-fiber filters meet new regulatory particulate limits and satisfy motorists’ demand for hospital-grade cabin

What impact do long-life synthetic media have on market growth?

They extend service intervals, reducing replacement frequency and shaving 0.8 percentage points off the CAGR forecast.

Page last updated on: July 7, 2025