Chile Corrugated Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

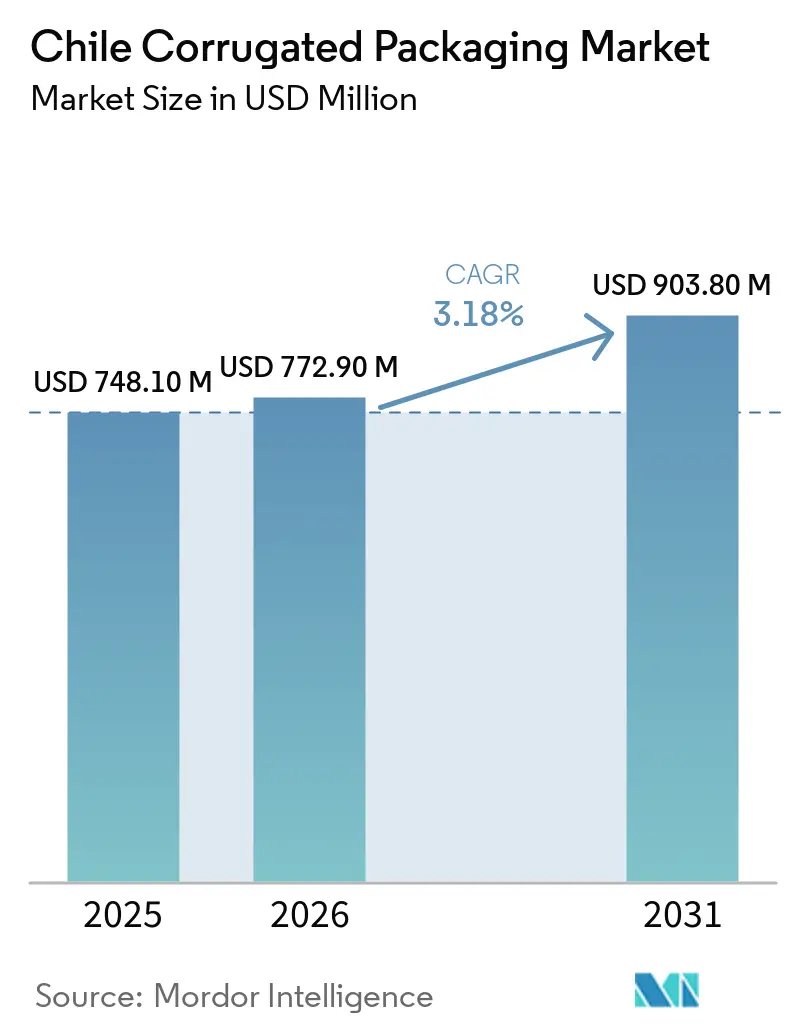

| Base Year Market Size (2025) | USD 748.10 Million |

| Market Size (2026) | USD 772.90 Million |

| Market Size (2031) | USD 903.80 Million |

| Growth Rate (2026 - 2031) | 3.18% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chile Corrugated Packaging Market Analysis by Mordor Intelligence

The Chile corrugated packaging market size is expected to increase from USD 772.9 million in 2026 to USD 903.8 million by 2031, growing at a CAGR of 3.18% over 2026-2031. Modest expansion comes from rising e-commerce volumes, export-driven fresh-produce demand, and stronger enforcement of Chile’s Extended Producer Responsibility (EPR) law. Growth is moderated by recovered-fiber price swings, freight bottlenecks in the south, and import-linked cost inflation on virgin linerboard. Integrated producers leverage scale and recycling assets to offset higher fiber costs, while mid-tier converters add servo-controlled die cutters and inkjet modules to win short-run jobs. Near-term demand clusters in Santiago, Valparaíso, Maule, and O’Higgins, yet decentralizing fulfillment centers are steering incremental box consumption toward Bío-Bío and Araucanía, widening the addressable footprint of the Chile corrugated packaging market.

Key Report Takeaways

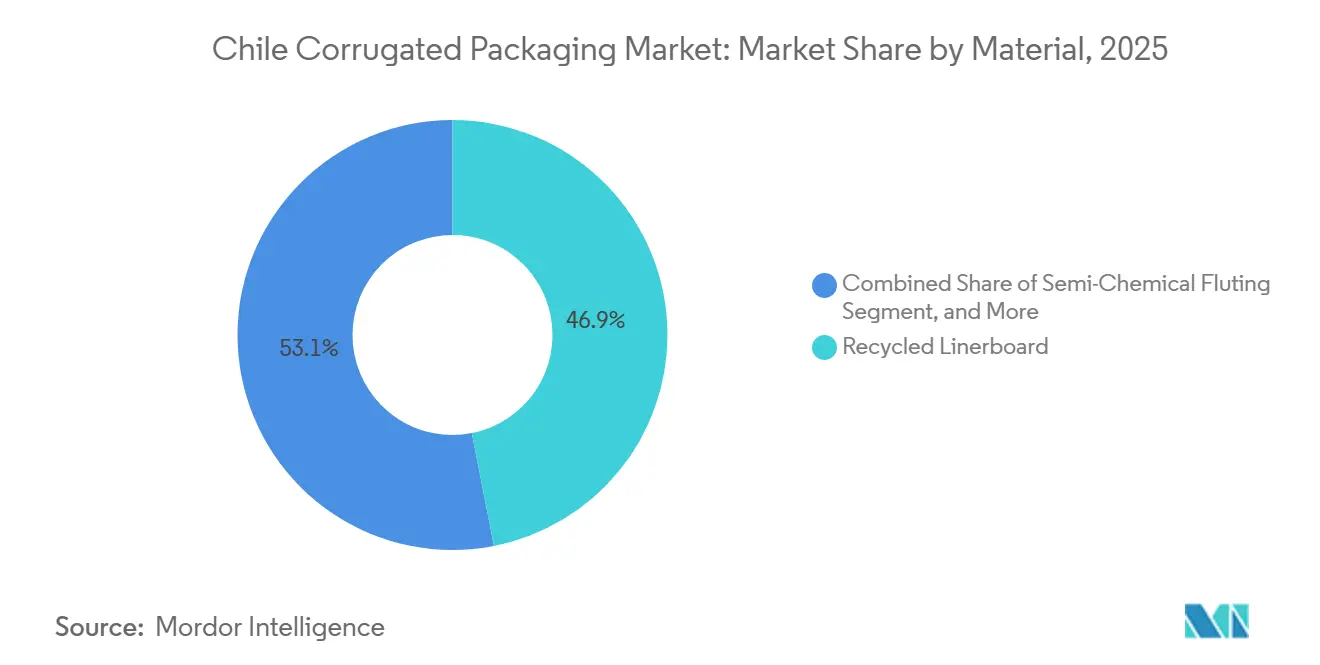

- By material, recycled linerboard captured 46.91% of the Chile corrugated packaging market share in 2025.

- By flute type, B flute captured 31.61% of the Chile corrugated packaging market share in 2025.

- By packaging type, the Chile corrugated packaging market size for the point-of-purchase displays segment is forecast to advance at a 5.12% CAGR through 2031.

- By wall type, single-wall captured 54.58% of the Chile corrugated packaging market share in 2025.

- By printing technology, the Chile corrugated packaging market size for the digital inkjet segment is forecast to advance at a 5.02% CAGR through 2031.

- By end-user, fresh food and produce captured 29.26% of the Chile corrugated packaging market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Chile Corrugated Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising E-commerce Shipment Volumes | +0.80% | Santiago, Valparaíso, Concepción | Short term (≤ 2 years) |

| Growth in Chile's Export-Oriented Fresh Produce Sector | +0.70% | Maule, O’Higgins, Valparaíso | Medium term (2-4 years) |

| Regulatory Push for Recyclable Packaging | +0.50% | National | Medium term (2-4 years) |

| Consumer Preference for Sustainable Materials | +0.40% | Urban centers nationwide | Long term (≥ 4 years) |

| Automation Adoption in Box Converting Lines | +0.30% | Major converters | Medium term (2-4 years) |

| Supply-Chain Resilience Investments Post-Pandemic | +0.20% | National, spillover south | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising E-Commerce Shipment Volumes

MercadoLibre processed more than 1 million parcels per week in 2025, with 15% same-day and 80% sub-48-hour delivery rates, prompting the standardization of lightweight, regular-slotted containers that flow smoothly through automated pick-and-pack lines.[1]Mercado Libre, “Nuevo centro de almacenamiento en San Pedro de la Paz,” mercadolibre.com Same-day service relies on regional hubs in Colina and San Pedro de la Paz, which multiply box turns and increase demand for high-stacking E flute cartons sized for parcel lockers. CorreosChile’s 90 million-parcel throughput, coupled with the opening of last-mile centers across Coquimbo and Los Lagos, sustains nationwide demand for corrugated packaging in Chile. Mobile commerce drives preference for easy-open tear strips that reduce return repacks, encouraging converters to incorporate micro-perforation and crash-lock bases. Volume visibility helps integrated mills lock in multi-year linerboard contracts, insulating them from spot-price hikes.

Growth in Chile’s Export-Oriented Fresh Produce Sector

Chile shipped 625,208 tons of cherries in 2024-25 and targets 670,000 tons in 2025-26, equal to roughly 134 million five-kilogram boxes bound chiefly for Chinese ports on 20-day voyages. Moisture-resistant triple-wall cartons with water-repellent coatings preserve structural integrity at 95% relative humidity, stimulating specialty-grade demand within the Chile corrugated packaging market. Table grapes add 62.2 million 8.2 kg boxes a year, each requiring vivid varietal graphics that digital inkjet can produce without plates. Converters position corrugators near Maule orchards to curb freight, reinforcing regional cluster economies. Traceability barcodes requested by China Customs necessitate inline variable-data print, bolstering inkjet installations.

Regulatory Push for Recyclable Packaging

EPR Law 20.920 obliges producers to achieve a 57% cardboard collection rate by 2026, rising to 70% by 2034, with penalties for non-compliance exceeding USD 8 million.[2]Sustainable Packaging Middle East and Africa, “Chile proposes regulatory changes to strengthen packaging EPR implementation,” sustainabilitymea.com Obligatory monthly declarations through the pollutant register intensify audits and raise the compliance premium on documented recycled fiber. Three producer-responsibility organizations manage collection, yet early audits revealed a 45% declaration shortfall in 2025, accelerating demand for converters that guarantee fiber provenance. Virgin linerboard retains niches, but brand owners now list recycled-content thresholds in tender documents, deeply embedding circular metrics in procurement across the Chile corrugated packaging industry.

Consumer Preference for Sustainable Materials

Law 21.368 mandates 15% recycled content in plastic bottles by 2025, spotlighting paper-based formats as environmentally aligned substitutes. Urban consumers value curbside recyclability, prompting retailers to switch from plastic-molded displays to corrugated point-of-purchase units. CMPC’s 100% recycled Liner Cordillera grades supply brand owners with on-pack sustainability cues that resonate at checkout. Social media unboxing videos further legitimize fiber over plastics, steering even cosmetics brands toward litho-laminated E flute gift packs in the Chile corrugated packaging market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Recovered Paper Prices | -0.40% | National | Short term (≤ 2 years) |

| Competition from Flexible Plastic Packaging | -0.30% | Processed foods, personal care | Medium term (2-4 years) |

| Logistics Bottlenecks in Southern Chile | -0.20% | Aysén and Magallanes | Medium term (2-4 years) |

| Capital-Intensive Nature of Corrugator Upgrades | -0.10% | Small and mid-tier converters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Recovered Paper Prices

South American OCC prices swung sharply in 2024, squeezing converters lacking integrated recycling plants. Chilean-peso depreciation inflated import costs for virgin kraft linerboard, narrowing gross margins. CMPC’s Puente Alto facility processes 700 tonnes of recovered fiber daily, buffering price spikes, yet smaller plants depend on spot bales that fluctuate monthly. EPR-mandated recovery should ease supply tension, but uneven municipal sorting keeps bale quality inconsistent, forcing mills to over-specify furnish or slow machine speeds, both of which dampen profitability in the Chile corrugated packaging market.

Logistics Bottlenecks in Southern Chile

Aysén and Magallanes' average freight costs of USD 650 per kilometer are about 40% above Santiago's, because sparse populations limit backhauls and winter storms delay maritime links 30% of the time. The government’s Plan de Zonas Extremas earmarks USD 1.6 billion for 54 projects, yet most roads and port upgrades will only come onstream after 2029, prolonging high buffer-stock requirements.[3]Chile Infrastructure Portal, “Plan de Zonas Extremas 2025-2035 project list,” chileinfra.cl Converters often ship flat blanks from Santiago, then erect boxes onsite, adding handling stages that offset material savings. High logistics friction curbs local demand growth and constrains the southern slice of the Chile corrugated packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Linerboard Extends Its Lead

Recycled linerboard captured 46.91% of the Chile corrugated packaging market share in 2025 and is projected to outpace virgin grades at 4.11% CAGR through 2031. CMPC’s closed-loop system covers curbside collection, papermaking, and box conversion, enabling the firm to internalize EPR compliance and monetize fiber twice. Smaller mills sign long-term fiber agreements with RESIMPLE, accepting premium bale prices to ensure compliance with documentation requirements. Virgin Kraft linerboard remains crucial where moisture and print fidelity trump cost, notably in cherry and salmon exports that use wax-replacement coatings. Specialty barrier liners coated with starch-based dispersions are emerging for seafood shippers seeking plastic-free ice boxes, incrementally expanding the Chilean corrugated packaging market.

Chilean brand owners increasingly demand life-cycle assessment data in procurement bids, driving mills to publish cradle-to-gate carbon disclosures. Recycled content above 70% wins tie-breaks, nudging converters to dial back virgin top sheets in favor of high-brightness recycled liners. Mills responded by upgrading optical sorters and de-inking lines to raise brightness by 4 points, minimizing ink show-through and enabling full-bleed graphics without virgin overlamination.

By Flute Type: E Flute Surges on Last-Mile Optimization

B flute retained 31.61% share in 2025 thanks to its cushioning-to-cost balance, yet parcel-carrier dimensional tariffs accelerate E flute’s 4.56% CAGR by trimming carton height and shipping weight. Urban micro-fulfillment centers favor E flute mailers that nest eight deep on sortation trays, maximizing belt throughput. Converters retrofit corrugators with servo gap-adjust systems and electronic adhesive metering to prevent paper nip crush on slender flutes, a capital outlay many small plants delay, widening the service gap.

F flute mirrors E flute’s growth from a low base in premium cosmetics and VR headset boxes that demand photo-quality litho lamination. C flute remains preferred for produce export trays where cross-stack compression outvalues cube savings. SUN Automation Group’s BX Motion Pro, capable of toggling between E, B, and double-wall configurations in under 60 seconds, allows high-mix scheduling without downtime penalties.[4]SUN Automation Group, “BX Motion Pro product sheet,” sunautomation.com Efficient changeovers attract contract packers that run fluctuating SKUs for promotion-driven fast-moving consumer goods, swelling the total job count per shift.

By Packaging Type: Displays Ride Omnichannel Momentum

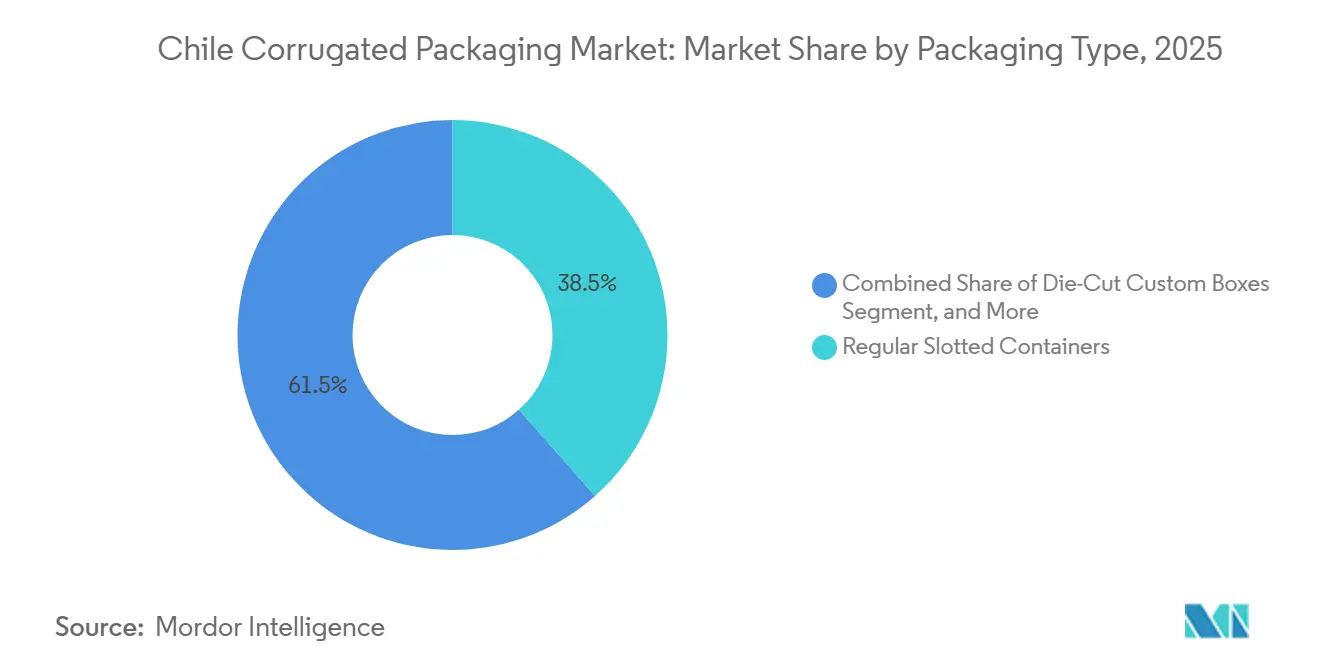

Regular slotted containers commanded 38.46% share in 2025, anchoring volume across produce, industrial, and parcel delivery. Yet point-of-purchase displays will generate the highest 5.12% CAGR as supermarkets adopt shelf-ready packaging that migrates seamlessly from pallet to aisle endcap. Box designers integrate perforated knock-outs, allowing cartons to become instant dump bins, slicing shelf-facing setup time by 30%. Die-cut custom boxes flourish in subscription cosmetics, where distinctive unboxing drives social engagement, justifying higher tooling costs.

Folding cartons split the difference between paperboard and corrugated, serving over-the-counter drugs that must display mandated star symbols and narcotics legends per 2024 health authority guidance AZ.CL. Pallet boxes often triple-wall handle 1-ton loads of copper concentrate sacs headed to Antofagasta ports. Other formats, like produce bins with integrated ice-drain channels, surface in salmon logistics, underscoring the Chile corrugated packaging market’s pivot from plastic crates to fiber.

By Wall Type: Triple-Wall Supports Long-Haul Exports

Single-wall accounted for 54.58% of shipments in 2025 as e-commerce volumes soared, but triple-wall advances at 4.66% CAGR by securing perishable exports on 28-day Asia routes. Triple-wall boxes, 16 mm thick, survive 45 stacking cycles in refrigerated holds without deformation, mitigating cherry bruising losses worth USD 130 per metric ton. Double-wall remains the mainstay for wine and processed foods, balancing cost and compression.

SUN Automation equipment runs single- through triple-wall on one line, improving machine uptime. Integrated damp-proof coatings extend carton life in high-humidity containers, allowing firms to retire polyethylene liners and comply with EPR’s 75% re-entry rule. Retailers are now piloting reusable triple-wall bulk shippers that return folded, suggesting downstream circular loops may curb virgin box demand while raising specialty board penetration.

By Printing Technology: Inkjet Gains for Variable Data

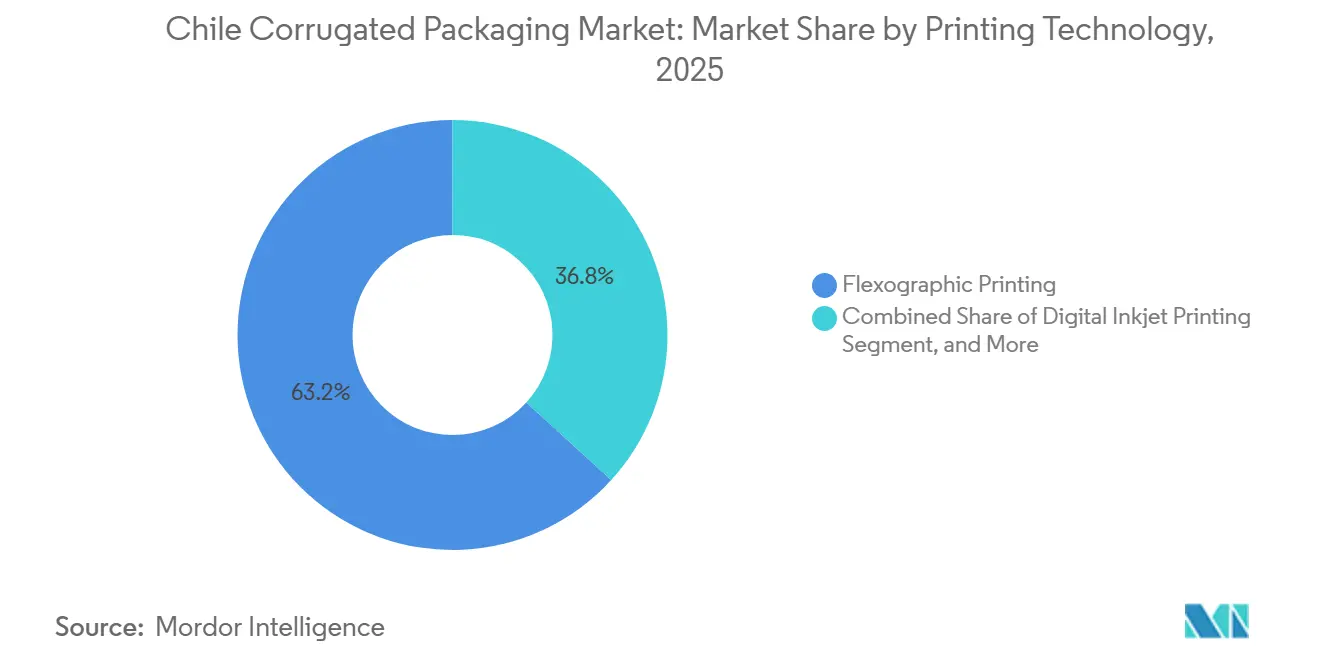

Flexography held a 63.22% share in 2025, powered by rotary die-cutters that reached 12,000 sheets per hour, delivering the lowest cost per unit beyond 10,000 impressions. Digital inkjet climbs at 5.02% CAGR as SKU proliferation, seasonal campaigns, and EPR traceability drive variable printing. Four-color single-pass inkjet heads can now be integrated adjacent to flexo decks, allowing converters to lay down base graphics and then overprint serialized QR codes in a single run.

Litho-lamination still anchors luxury perfume and boutique electronics, though its setup labor deters short runs. Screen printing occupies a shrinking niche for opaque metallic inks on promotional displays. CORFO’s credit line for Industry 4.0 upgrades reimburses up to 40% of digital press capex, accelerating adoption among mid-tier plants and broadening service offerings within the Chile corrugated packaging market.

By End-User Industry: E-Commerce Fulfillment Commands Growth

Fresh food and produce accounted for 29.26% of 2025 revenue, providing corrugators with steady, harvest-linked baseloads that ensure plant utilization runs near 90% during peak months. E-commerce fulfillment centers, however, record the swiftest 5.94% CAGR, galvanized by MercadoLibre’s USD 135 million Colina expansion that doubles warehouse space to 200,000 m² by late 2026. Apparel, small electronics, and nutraceuticals flow through automated sorters demanding precision-scored mailers compatible with robotic erectors.

Processed foods and beverages keep mid-single-digit growth tied to population gains and channel shifts toward club stores. Electrical goods require foam-free assembled inserts made from die-cut corrugated, aligning with national plastic-reduction targets. Personal care entrepreneurs deploy subscription boxes with high-gloss varnish and influencer co-branding, spurring demand for litho-laminated E flute. Pharmaceutical volume is limited, yet heightened serialization regulation pushes orders toward inkjet-capable converters, adding profitable short-run work to press schedules.

Geography Analysis

Santiago Metropolitan Region, Valparaíso, and O’Higgins house over two-thirds of Chile corrugated packaging market demand, blending population density, port access, and agribusiness clusters. Maule supplies 42.9% of cherry acreage, generating peak box volumes each November-February harvest. Fulfillment decentralization is nudging box flows southward; MercadoLibre’s San Pedro de la Paz hub enables same-day service for 1 million shoppers, fostering micro-run custom packaging near Bío-Bío orchards.

Northern mining centers in Antofagasta and Atacama add bulky chemical and spare-parts traffic, yet long drayage from Santiago mills inflates delivered cost, inviting on-site box plants attached to smelters. Southern Aysén and Magallanes remain limited by freight rates 40% above central benchmarks and 30% weather-related shipment delays, constraining the Chile corrugated packaging market’s penetration despite salmon hatchery demand. Government Road Plan 2025-2035 promises 235 km of Carretera Austral pavement and a USD 37 million expansion of Puerto Chacabuco, but box makers anticipate minimal relief before 2029, thereby sustaining reliance on central plants shipping flat blanks.

Integrated producers cluster near Puente Alto recycling flows and Lampa corrugators to maximize turnaround of recovered fiber. However, provincial incentives may catalyze satellite sheet feeders in Araucanía, spreading asset bases and enhancing responsiveness as south-bound e-commerce volumes climb.

Competitive Landscape

Three vertically integrated groups, CMPC, Smurfit Westrock, and Forestal y Papelera Concepción, command the bulk of the Chilean corrugated packaging market. CMPC runs 260,000 tonnes of corrugating paper, 520,000 tonnes of boxboard, and processes 700 tonnes of recovered fiber daily, enabling cradle-to-carton control. Smurfit Westrock’s South America unit posted USD 2.1 billion net sales and a 23% margin in 2025 after shuttering 600,000 tonnes of high-cost global capacity and wringing USD 400 million in synergies. Forestal y Papelera Concepción focuses on specialty produce bins, leveraging regional farmer ties.

International Paper’s exit in 2026 opened white space quickly seized by Corrupac, which now operates plants in Graneros, Pudahuel, and San Bernardo, scaling to challenge incumbents in retail-ready cartons. Smaller converters face capital-stretch upgrades for inkjet and servo die cutters; many pivot to niche point-of-purchase displays and micro-run e-commerce inserts, where service trumps scale.

R&D targets barrier topcoats to replace waxed produce cartons and win salmon and grape accounts. CMPC pilots water-repellent triple-wall grades, while Smurfit WestRock tests starch-based dispersion barriers that are repulpable and align with EPR thresholds. Compliance capability differentiates suppliers; integrated mills track bale provenance through blockchain modules, which producer-responsibility organizations recognize during audits, giving them bid headroom over non-integrated rivals.

Chile Corrugated Packaging Industry Leaders

Empresas CMPC S.A.

Smurfit Westrock plc

International Paper Company

Mondi plc

Georgia-Pacific LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Coipsa’s Corrupac closed the acquisition of International Paper’s Graneros plant after antitrust clearance, consolidating regional capacity and expanding its footprint to five corrugators.

- February 2026: The Ministry of the Environment issued proposals to optimize EPR execution, targeting capacity misalignment and procurement inefficiency ahead of strict 2026 enforcement.

- February 2026: Smurfit Westrock reported USD 2.1 billion South America net sales for 2025 with a 23% adjusted EBITDA margin, citing synergy capture and capacity rationalization.

- November 2025: MercadoLibre launched a 30,000-SKU regional hub in San Pedro de la Paz to enable same-day delivery for 1 million central-south users.

Chile Corrugated Packaging Market Report Scope

The Chile Corrugated Packaging Market report encompasses a comprehensive analysis of fiber-based and polymer-based corrugated materials used for the containment, protection, and transport of goods across diverse industrial and retail sectors. The market refers to the industry that produces multi-layered boards, typically consisting of a fluted medium sandwiched between linerboards, designed to provide high strength-to-weight ratios and crush resistance for secondary and tertiary packaging.

The Chile Corrugated Packaging Market Report is Segmented by Material (Virgin Kraft Linerboard, Recycled Linerboard, Corrugating Medium, Semi-Chemical Fluting, and Other Materials), Flute Type (A Flute, B Flute, C Flute, E Flute, and F Flute), Packaging Type (Regular Slotted Containers, Die-Cut Custom Boxes, Folding Cartons, Point-of-Purchase Displays, Pallet Boxes, and Other Packaging Types), Wall Type (Single-Wall, Double-Wall, Triple-Wall, and Single Face), Printing Technology (Flexographic Printing, Digital Inkjet Printing, Litho-Lamination, Screen Printing, and Other Printing Technologies), End-User Industry (Processed Foods, Fresh Food and Produce, Beverages, Electrical Products, Personal Care and Cosmetics, E-commerce Fulfillment Centers, Pharmaceuticals, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Kraft Linerboard |

| Recycled Linerboard |

| Corrugating Medium |

| Semi-Chemical Fluting |

| Other Materials |

| A Flute |

| B Flute |

| C Flute |

| E Flute |

| F Flute |

| Regular Slotted Containers |

| Die-Cut Custom Boxes |

| Folding Cartons |

| Point-of-Purchase Displays |

| Pallet Boxes |

| Other Packaging Types |

| Single-Wall |

| Double-Wall |

| Triple-Wall |

| Single Face |

| Flexographic Printing |

| Digital Inkjet Printing |

| Litho-Lamination |

| Screen Printing |

| Other Printing Technologies |

| Processed Foods |

| Fresh Food and Produce |

| Beverages |

| Electrical Products |

| Personal Care and Cosmetics |

| E-commerce Fulfillment Centers |

| Pharmaceuticals |

| Other End-User Industries |

| By Material | Virgin Kraft Linerboard |

| Recycled Linerboard | |

| Corrugating Medium | |

| Semi-Chemical Fluting | |

| Other Materials | |

| By Flute Type | A Flute |

| B Flute | |

| C Flute | |

| E Flute | |

| F Flute | |

| By Packaging Type | Regular Slotted Containers |

| Die-Cut Custom Boxes | |

| Folding Cartons | |

| Point-of-Purchase Displays | |

| Pallet Boxes | |

| Other Packaging Types | |

| By Wall Type | Single-Wall |

| Double-Wall | |

| Triple-Wall | |

| Single Face | |

| By Printing Technology | Flexographic Printing |

| Digital Inkjet Printing | |

| Litho-Lamination | |

| Screen Printing | |

| Other Printing Technologies | |

| By End-User Industry | Processed Foods |

| Fresh Food and Produce | |

| Beverages | |

| Electrical Products | |

| Personal Care and Cosmetics | |

| E-commerce Fulfillment Centers | |

| Pharmaceuticals | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current value of the Chile corrugated packaging market?

The Chile corrugated packaging market size is valued at USD 772.90 million in 2026 and is projected to reach USD 903.80 million by 2031.

Which segment is growing fastest within Chile's corrugated packaging sector?

E-commerce fulfillment centers are expanding at a 5.94% CAGR through 2031 due to rapid parcel growth and new regional warehouses.

Why is recycled linerboard gaining share in Chile?

Strict EPR targets, corporate sustainability commitments, and integrated recovery systems are steering material choice toward high recycled-content grades.

How are Chilean converters managing short print runs?

Many have added digital inkjet modules that cut setup to under one minute and enable variable-data graphics without plates.

What logistics challenges affect southern Chile?

Sparse populations, harsh weather, and limited road infrastructure lift freight costs about 40% above Santiago levels, slowing market penetration.

Which regulations most influence packaging design in Chile?

EPR Law 20.920 drives recyclability, while health-authority labeling rules dictate pharmaceutical secondary-pack design specifics.

Page last updated on: