Cesium Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

| Growth Rate | 2.00% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

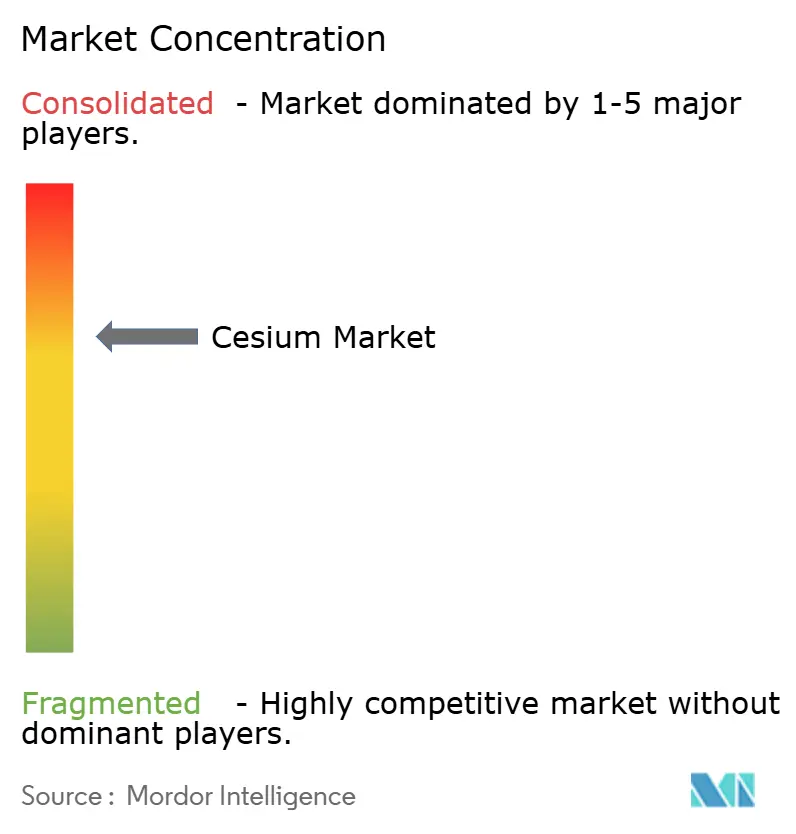

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cesium Market Analysis by Mordor Intelligence

The Cesium Market size is estimated at 3.32 kilotons in 2026, and is expected to reach 4.33 kilotons by 2031, at a CAGR of 5.43% during the forecast period (2026-2031). Rising high-pressure high-temperature (HPHT) drilling activity, fast-growing 5G and future 6G infrastructure, and new medical-imaging uses are expanding demand even as the pipeline of primary pollucite ore remains thin. Vertically integrated suppliers have reacted by raising prices in 2024 while locking in multiyear contracts with drilling-service companies to secure scarce feedstock. Asia-Pacific leads both consumption and processing because China refines the bulk of global cesium salts, and Japan dominates precision-electronics applications. In North America and Europe, offshore HPHT completions and defense programs sustain a stable demand base but expose buyers to a single-supplier risk centered on Sinomine and Albemarle.

Key Report Takeaways

- By product type, cesium compounds captured 73.45% of the cesium market share in 2025, and they are expanding at a 6.02% CAGR to 2031.

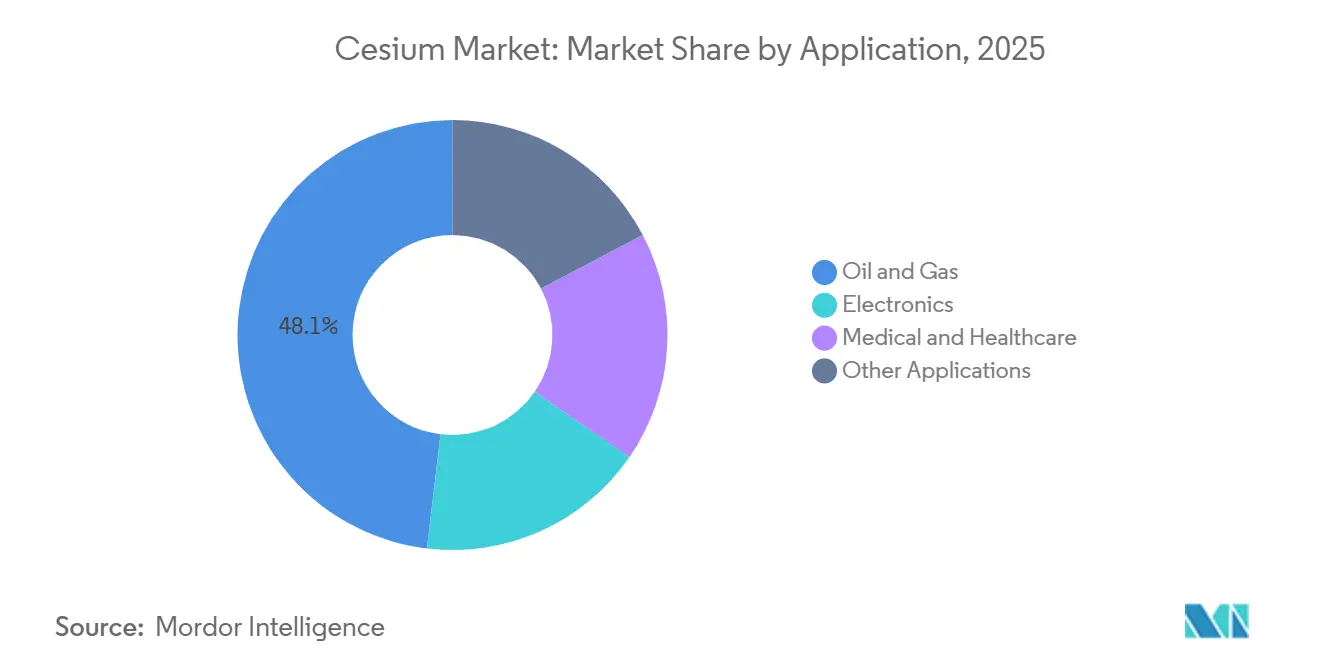

- By application, oil and gas accounted for 48.11% of the cesium market size in 2025, while it is advancing at a 6.12% CAGR through 2031.

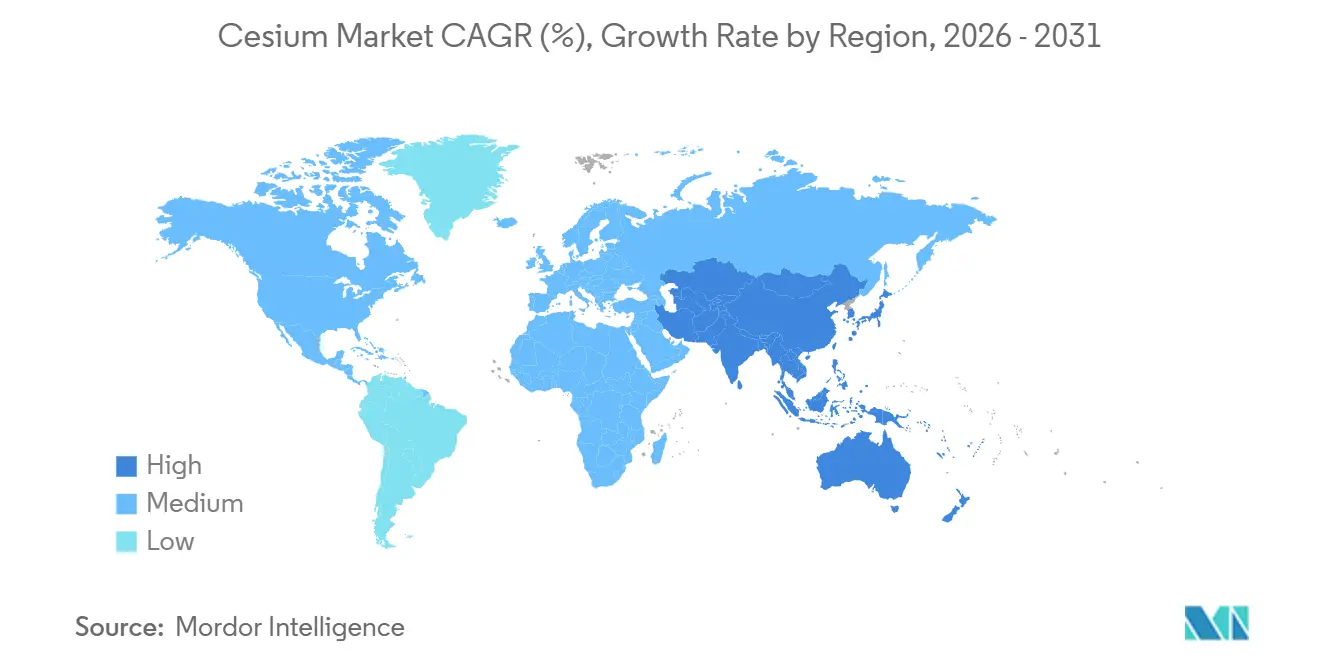

- By geography, Asia-Pacific held 43.86% of the cesium market share in 2025 and is forecast to post the fastest 6.56% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cesium Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging use of cesium-formate fluids in ultra-deep HPHT wells | +1.8% | Global, with concentration in North Sea, Gulf of Mexico, offshore Brazil, West Africa | Medium term (2–4 years) |

| Proliferation of 5G/6G networks requiring ultra-stable cesium clocks | +1.2% | APAC core (China, South Korea, Japan), spill-over to North America and EU | Short term (≤ 2 years) |

| Growing demand for Cs-based scintillators in advanced medical imaging | +0.9% | North America and EU (hospital capex cycles), emerging in APAC tier-1 cities | Medium term (2–4 years) |

| Rise of mini-Cs atomic clocks for autonomous and defense UAV fleets | +0.7% | North America (DoD programs), EU (defense modernization), select APAC markets | Long term (≥ 4 years) |

| Pilot-scale extraction of cesium from lepidolite tailings in Africa | +0.5% | Africa (Namibia, Zimbabwe, DRC), with processed salts exported globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Use of Cesium-Formate Fluids in Ultra-Deep HPHT Wells

Cesium-formate brines, with high densities and minimal formation damage, have emerged as the go-to completion fluid for reservoirs exceeding 20,000 psi[1]Schlumberger, “Cesium Formate Brine Enables Successful Completion,” Slb.com. Operators in the North Sea, Gulf of Mexico, and Brazil have demonstrated that they can recover the cost of these fluids within a year, thanks to preserved formation integrity and enhanced lifetime recovery. The global inventory of cesium-formate is limited, and the supply is tightening as the demand for deeper wells grows. In response, Sinomine has established dedicated recovery bases in Aberdeen and Bergen, and has tied long-term supply contracts to Brent oil futures. These strategic moves not only safeguard profit margins but also create barriers for new competitors in the HPHT service chain, solidifying Sinomine's dominance in the cesium market.

Proliferation of 5G/6G Networks Requiring Ultra-Stable Cesium Clocks

Telecom operators are increasingly replacing rubidium oscillators with cesium atomic clocks, which can maintain GPS-free accuracy for an extended period. This shift is largely driven by the need for sub-microsecond synchronization, a requirement for 5G coordinated multipoint transmission. Vodafone Turkey's 2024 deployment is just one example of a trend that's rapidly gaining momentum in China, South Korea, and the United States. While optical lattice clocks have achieved greater accuracy than cesium in laboratory settings, the regulatory metrology still recognizes the SI second based on the 9.19 GHz cesium-133 transition. As long as standards bodies uphold this definition, cesium's dominant position—and the market for cesium—remains firmly established.

Growing Demand for Cs-Based Scintillators in Advanced Medical Imaging

In a 2024 study published on ArXiv, researchers highlighted a significant leap in quantum yield for terbium-doped cryogenic CsI. This advancement allows for PET image quality at just half the cost of the traditional lutetium-yttrium oxyorthosilicate detectors. Faced with budget constraints, hospitals across North America and Europe are now extending the lifecycles of their scanners to 12–15 years. This shift has created a strong incentive to transition to the more affordable CsI modules. Meanwhile, thallium-doped CsI(Tl) has solidified its dominance in security X-ray arrays, thanks to its 540 nm emission, which perfectly aligns with the sensitivity of silicon photodiodes. While the bottleneck in supply isn't due to crystal growth, it lies in sourcing high-purity cesium iodide feedstock. This critical feedstock is a specialty of only a select few refiners located in China, Germany, and Japan. Although the bulk demand for cesium remains modest, the stringent purity requirements carve out a substantial profit margin within the industry.

Rise of Mini-Cs Atomic Clocks for Autonomous and Defense UAV Fleets

Thanks to DARPA's advancements in its chip-scale atomic clock (CSAC) program, power consumption has been reduced and the size shrunk. This miniaturization allows for seamless integration into Reaper and Gray Eagle UAVs, which operate in areas where GPS navigation is unavailable. Each SA.45s unit requires cesium metal. While the tonnage may seem minor, its significance lies in the purity and export-license considerations. Given that production takes place in defense-approved cleanrooms across the U.S. and EU, even slight disruptions in supply necessitate expensive inventory buffers. This specialized segment of the cesium market, insulated from broader commodity fluctuations, commands premium pricing.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited number of commercially active pollucite mines | -1.1% | Global, with primary impact on North America and EU supply chains | Short term (≤ 2 years) |

| Tight export controls on strategic alkali metals | -0.6% | China (export source), North America and EU (import destinations) | Medium term (2–4 years) |

| Volatile pricing due to by-product dependence on Li supply | -0.8% | Global, with acute impact on African by-product projects and Asia-Pacific processors | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Limited Number of Commercially Active Pollucite Mines

In 2024, the absence of a continuously operating primary pollucite mine compelled the demand for cesium salts—used outside of drilling fluids—to depend on existing inventories and sporadic outputs from Tanco. Despite Sinomine's leadership, Tanco has opted for batch processing over continuous operations, hinting at either subpar ore grades or challenging processing economics given the current price levels. With global reserves of cesium oxide (Cs₂O) showing no significant discoveries since the early 2000s, aerospace and defense sectors have begun stockpiling high-purity cesium carbonate and metal. This move has not only heightened their working-capital demands but also dampened the demand's elasticity in the cesium market.

Tight Export Controls on Strategic Alkali Metals

China's December 2023 regulations on rare-earth-processing technology set a precedent for potential future restrictions on cesium salts. This is particularly true for iodide and metal grades, which find applications in defense optics and clocks[2]Ministry of Commerce PRC, “Regulations on Export Controls,” Mofcom.gov.cn. Meanwhile, Russia's broader stance on resource nationalism, albeit with less emphasis on cesium, hints at a tightening geopolitical landscape. The EU's Critical Raw Materials Act added cesium to its monitoring list. This move is expected to increase compliance costs and extend lead times for European importers. Furthermore, the cesium industry is already divided into restricted and unrestricted channels due to defense-end-use verification. This segmentation diminishes fungibility and heightens supply risk premiums.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Compounds Scale With Industrial Uses While Metal Serves Niche Precision Needs

The cesium market size for compounds stood equals to 73.45% of total volume, and is forecast to grow at 6.02% through 2031. Formate brines lead this segment, while carbonate supports pharmaceutical catalysis and high-refractive-index glass. Iodide and bromide cater to scintillator and infrared-optics markets. The metal segment commands premium margins as purity levels increase. Although each CSAC unit requires only small amounts of metal, defense buyers are willing to pay significantly higher prices compared to commodity salts, insulating this sub-segment from broader market fluctuations.

As global infrastructure and healthcare spending rise, the demand for cesium compounds—driven by HPHT drilling, specialty glass, and medical imaging—is set to continue. While metal demand will see episodic growth aligned with defense procurement and telecom upgrades, it won't alter the overall tonnage balance. Other cesium derivatives like hydroxide, fluoride, and antimonide will remain niche players, catering to etching chemistry and photocathodes, collectively making up a minor portion of the market. Thus, vertical integration into both cesium compounds and metal emerges as the most reliable strategy against demand fluctuations in the industry.

By Application: Oil and Gas Provides Baseline Volume While Electronics and Medical Devices Accelerate Growth

Oil and gas represented 48.11% of the cesium market size in 2025, expanding at a 6.12% CAGR as operators push farther into pre-salt Brazil, the Lower Tertiary Gulf of Mexico, and deepwater West Africa. While recycling loops reclaim most of the cesium formate per well, the remaining loss still drives demand for fresh salts annually, solidifying baseline demand. Although electronic applications—like atomic clocks, photocathodes, and ion propulsion—consume smaller tonnages, their significance for supply-chain security is paramount. With Vodafone Turkey launching 5G in 2024 and China testing 6G, the demand for ultra-high-purity salts is on a steady ascent.

Medical applications, particularly cesium iodide scintillators, are reaping benefits as hospitals lean towards cost-effective detectors and extended scanner lifecycles. Each PET or SPECT system may only need a small amount of CsI, but the emphasis on purity ensures a high value share compared to volume. Other uses, such as the budding perovskite solar cells and catalytic processes, complete the spectrum and could gain prominence if they overcome stability challenges. These evolving dynamics are broadening the cesium market's horizons, diminishing its historical dependence on drilling fluids, yet underscoring the demand for ultra-pure supplies.

Geography Analysis

Asia-Pacific accounted for 43.86% of the cesium market share in 2025 and is anticipated to log the fastest 6.56% CAGR to 2031. China, boasting the world's largest refinery cluster, adeptly transforms pollucite sourced from Canada and Zimbabwe into carbonate, iodide, and ultra-dry formate. Meanwhile, Japan's specialized producers, spearheaded by GODO SHIGEN and Iwatani, not only cater to domestic electronics with atomic-clock-grade salts but also export their surplus to North America and Europe. South Korea's nationwide 5G Advanced upgrade amplifies the regional demand for cesium oscillators. Concurrently, Chinese offshore explorations in the South China Sea bolster the demand for formate. However, a looming concern is the pending export-license frameworks, which may redirect high-purity cesium to prioritize domestic aerospace and telecom needs.

North America and Europe, while mature, represent a market cluster of strategic significance. Western refining of cesium metal and its specialty compounds finds a cornerstone in Albemarle’s Langelsheim plant in Germany. The Lower Tertiary HPHT wells in the Gulf of Mexico and the aging high-pressure reservoirs of the North Sea guarantee a steady offtake of formate. Yet, both regions find themselves heavily reliant on upstream ore supplied by Sinomine. In the U.S., defense sectors are stockpiling cesium metal for CSAC programs, even if it means accepting longer lead times and incurring higher purity-assurance costs. Across the Atlantic, European importers face challenges with the traceability mandates of the EU Critical Raw Materials Act. While these mandates extend procurement cycles, they might also set the stage for a revival of North American pollucite operations, especially if prices surpass a critical threshold.

While the Rest of the World currently plays a modest role, its potential is undeniably strategic. In Brazil’s pre-salt fields, Petrobras and its partners are tapping into formate brines for depths surpassing 7,000 m, signaling a demand that could stretch through 2030. West Africa's deepwater activities, though swayed by oil-price fluctuations, hint at a promising long-term trajectory as infrastructure continues to develop. However, Africa's potential as a cesium supplier is closely tied to a rebound in lithium prices. Projects in lepidolite-rich regions of Namibia, Zimbabwe, and the DRC are banking on higher lithium values to make cesium co-processing viable. Without this price recovery, these nations remain on the periphery as prospective suppliers, leaving the global cesium market heavily concentrated in a select few producing locales.

Competitive Landscape

The cesium market is moderately consolidated. Strategic moves focus on feedstock security and downstream specialization. White-space entry remains difficult because new producers must secure ore, master hazardous refining, and win export-license approvals, a trifecta that consumes capital and time. Potential disruptors could emerge from African lithium miners if lithium prices rebound, yet co-processing complexity and capital intensity raise hurdles. Optical lattice clock technology using strontium or ytterbium is not yet commercially ready, so cesium’s regulatory incumbency protects current leaders, reinforcing the high-concentration profile of the cesium market.

Cesium Industry Leaders

Albemarle Corporation

Sinomine Resource Group Co., Ltd.

GODO SHIGEN Co., Ltd.

Iwatani Corporation

Suvchem

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Albemarle Corporation prepaid CAD 5 million to Power Metals for cesium-oxide concentrate offtake from the Case Lake project in Ontario, Canada.

- March 2025: Patriot Battery Metals announced the discovery of a sizable cesium zone at its CV13 pegmatite within the Shaakichiuwaanaan property in Quebec.

Global Cesium Market Report Scope

Cesium (Cs), a soft and silvery-gold alkali metal, remains liquid close to room temperature and exhibits high reactivity. This high-value material plays a pivotal role in industries that demand precise timing, specialized drilling fluids, and advanced imaging technologies.

The cesium market is segmented by product type, application, and geography. By product type, the market is segmented into cesium metal, cesium compounds, and other product types. By application, the market is segmented into oil and gas, electronics, medical and healthcare, and other applications. The report also covers the market size and forecasts across North America, Europe, Asia-Pacific, and the rest of the world. For each segment, the market sizing and forecasts have been done based on revenue (Tons).

| Cesium Metal |

| Cesium Compounds |

| Other Product Types |

| Oil and Gas |

| Electronics |

| Medical and Healthcare |

| Other Applications |

| North America |

| Europe |

| Asia-Pacific |

| Rest of the World |

| By Product Type | Cesium Metal |

| Cesium Compounds | |

| Other Product Types | |

| By Application | Oil and Gas |

| Electronics | |

| Medical and Healthcare | |

| Other Applications | |

| By Geography | North America |

| Europe | |

| Asia-Pacific | |

| Rest of the World |

Key Questions Answered in the Report

What is the forecast volume for global cesium demand by 2031?

It is expected to reach 4.33 kilo tons, reflecting a 5.43% CAGR over 2026–2031, from 3.32 kilo tons in 2026.

Which region is poised to grow fastest in cesium consumption?

Asia-Pacific is projected to record a 6.56% CAGR, driven by Chinese refining capacity and expanding 5G infrastructure.

Why are cesium-formate brines critical in HPHT drilling?

They combine densities up to 2.3 g/cm³ with minimal formation damage, making them the only viable fluid for pressures above 20,000 psi.

What new application areas support future cesium demand?

Autonomous-vehicle navigation using chip-scale atomic clocks and cost-efficient cesium-iodide PET scanners offers incremental high-purity demand streams.

Page last updated on: