Central Precocious Puberty Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.82 Billion |

| Market Size (2031) | USD 2.56 Billion |

| Growth Rate (2026 - 2031) | 8.53% CAGR |

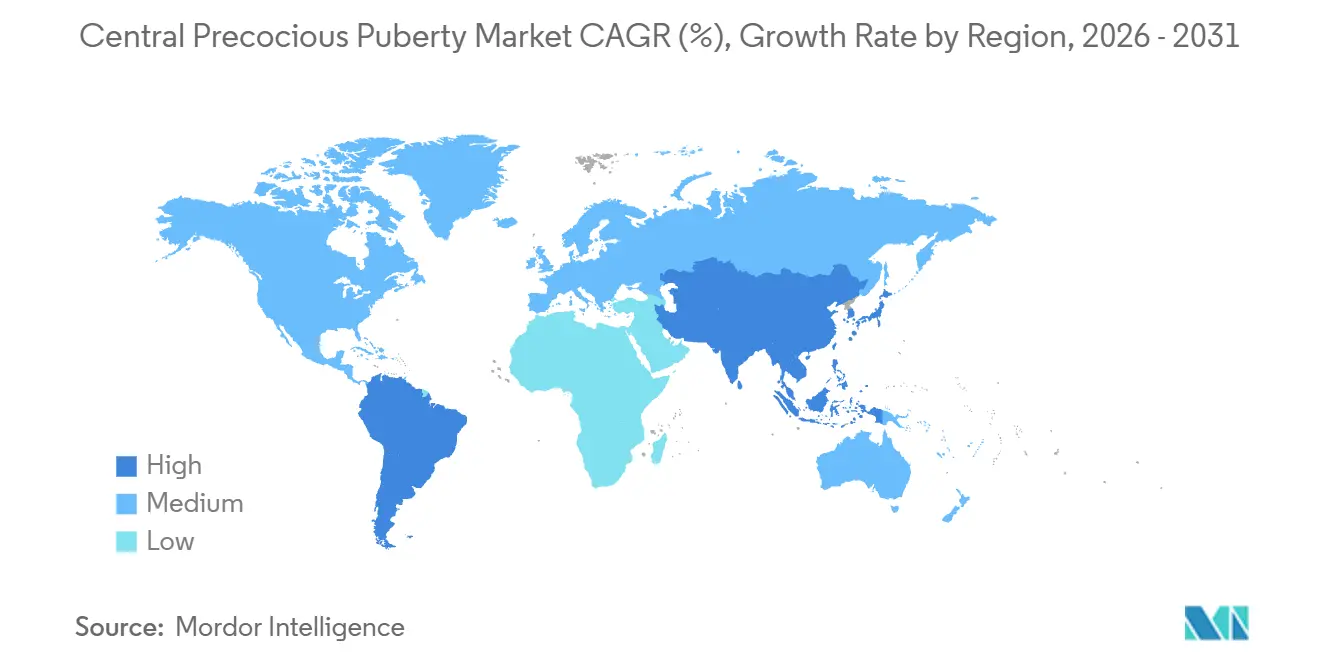

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

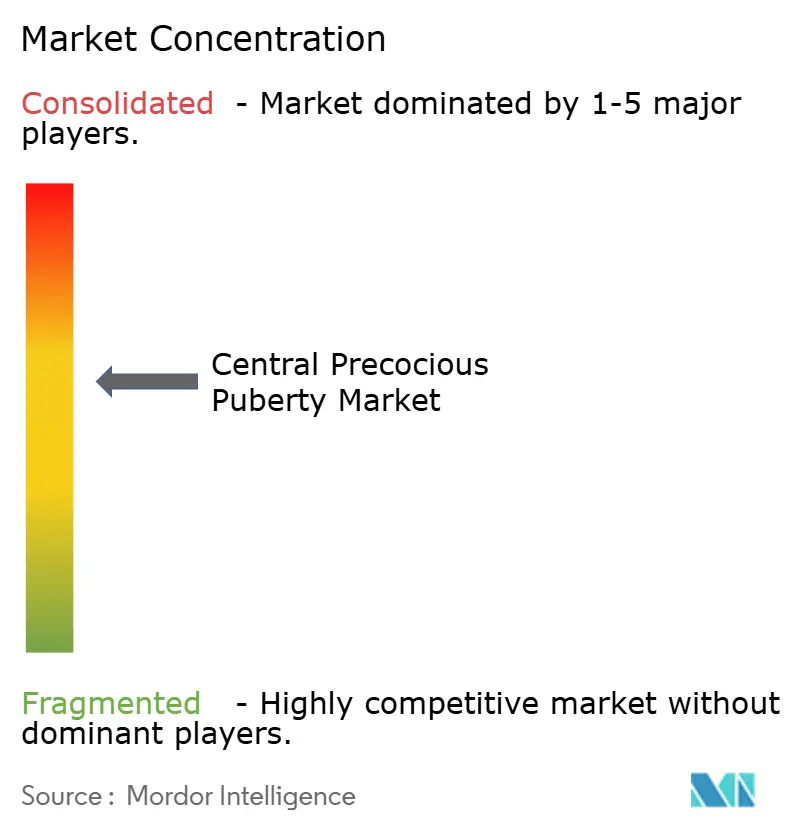

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Central Precocious Puberty Market Analysis by Mordor Intelligence

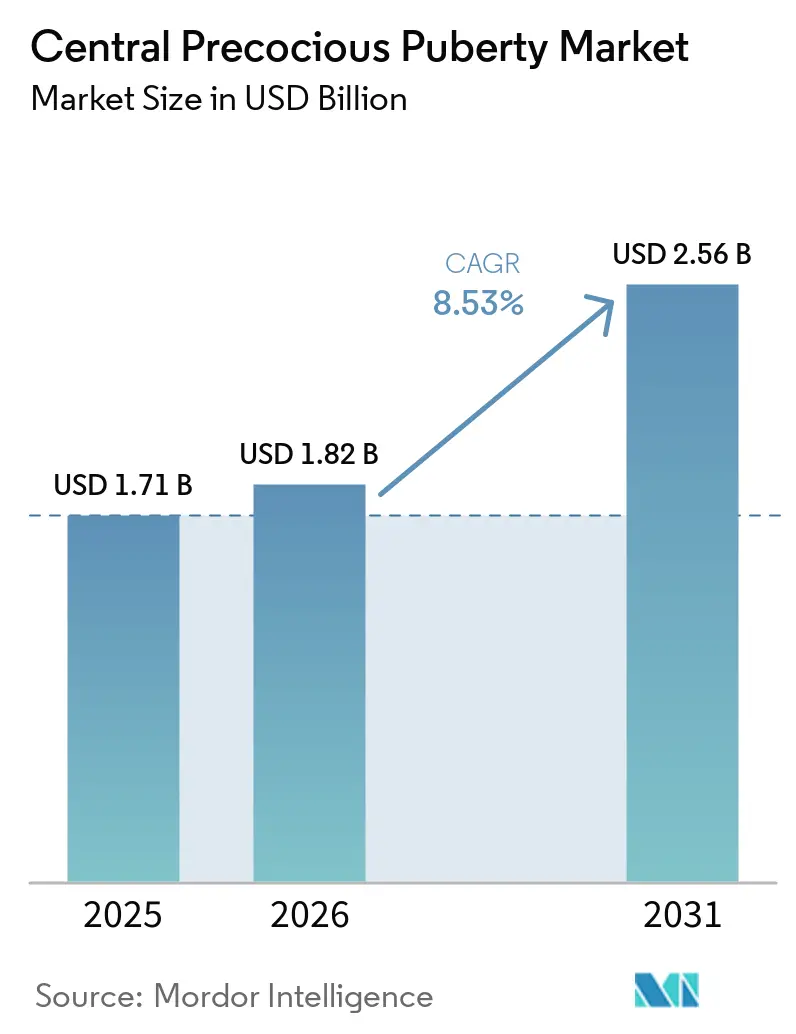

The Central Precocious Puberty Market size is expected to increase from USD 1.71 billion in 2025 to USD 1.82 billion in 2026 and reach USD 2.56 billion by 2031, growing at a CAGR of 8.53% over 2026-2031.

Demand is rising as clinicians diagnose earlier with ultrasensitive LH assays and standardized cut-offs that shorten testing pathways in routine practice. Payer criteria updates in the United States are broadening access to long-acting GnRH analogs, which is shifting prescribing to semiannual and investigational annual dosing formats that improve adherence and clinic flow. At the same time, the central precocious puberty market is adapting to supply fragility in biodegradable microsphere injectables, as documented shortages in major markets underscore the need for diversified manufacturing. Competitive focus is tilting from molecule novelty to delivery platforms, with six-month depots consolidating share and first annual triptorelin formulations moving through late-stage trials, setting the tone for the next phase of the central precocious puberty market.

Key Report Takeaways

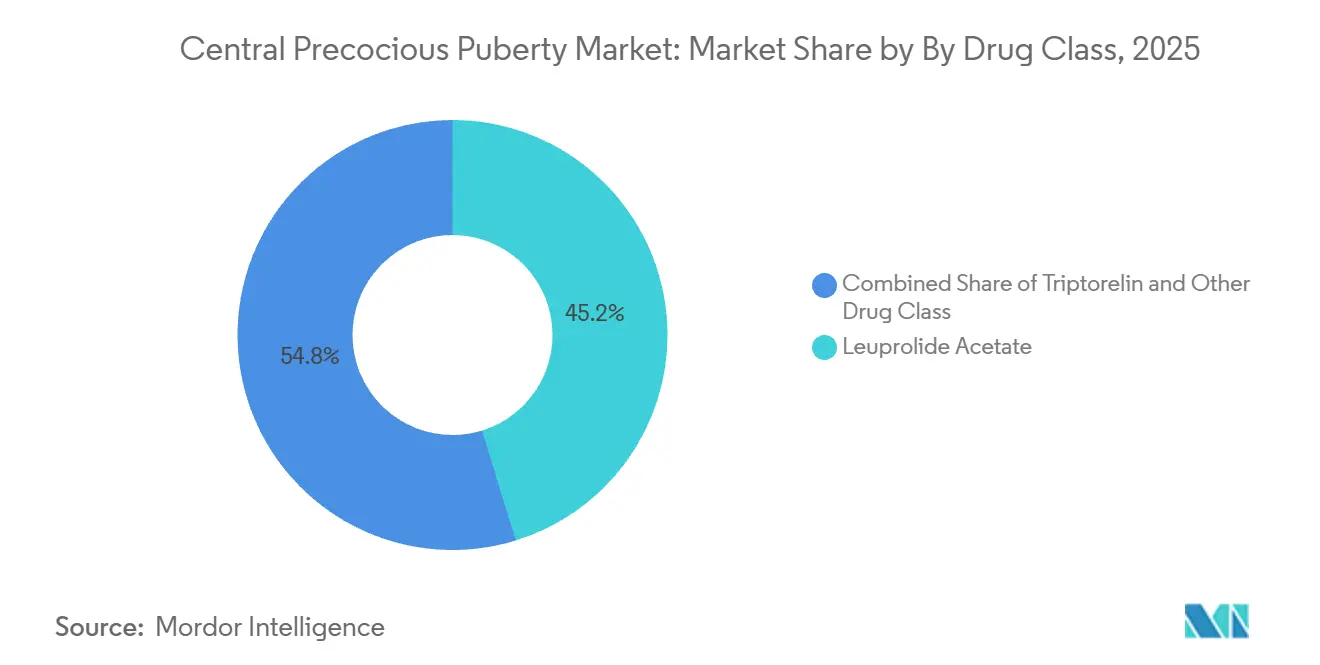

By drug class, leuprolide acetate led with 45.24% revenue share in 2025, while triptorelin is projected to expand at a 7.49% CAGR through 2031.

By distribution channel, hospital pharmacies held 40.12% share in 2025, while online pharmacies are forecast to grow at a 7.88% CAGR to 2031.

By geography, North America accounted for 43.11% in 2025, while the Asia-Pacific is set to grow at 8.24% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Central Precocious Puberty Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Incidence Linked to Pediatric Obesity & Endocrine-Disruptor Exposure | +1.8% | Global, concentrated in North America & Europe | Medium term (2-4 years) |

| Uptake Of Long-Acting GnRH-Analog Depots & Implants | +2.1% | Global, with early gains in United States, Germany, South Korea | Medium term (2-4 years) |

| Wider Reimbursement Expanding Treatment Access | +1.3% | North America & EU core, spill-over to APAC | Long term (≥ 4 years) |

| Improved Ultrasensitive LH Assays Boosting Early Diagnosis | +0.9% | Global, adoption highest in United States, Netherlands, China | Short term (≤ 2 years) |

| Tele-Endocrinology Platforms Increasing Specialist Reach | +0.7% | National, with early gains in United States rural areas | Long term (≥ 4 years) |

| Pipeline Oral GnRH Antagonists Promising Needle-Free Therapy | +0.6% | Global, pending pediatric PK/PD data | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence Linked to Pediatric Obesity & Endocrine-Disruptor Exposure

Childhood obesity is linked to faster activation of the hypothalamic pituitary gonadal axis, and reported CPP prevalence in girls with obesity reached 48% versus 8.73% in normal-weight cohorts[1]“Endocrine Consequences of Childhood Obesity,” Frontiers in Endocrinology. Elevated leptin and kisspeptin signaling appear to contribute to earlier thelarche and menarche in these populations, which sustains a steady inflow of patients into the central precocious puberty market. Low-dose endocrine-disrupting chemical mixtures also correlate with gut microbiome changes, including reported decreases in Lactobacillus of 40% in human studies and 58% in rodent models. Modeling work suggested that gut-brain axis mediators explained 68% of internal variance for early puberty risk at low experimental doses, which raises long-horizon incidence expectations independent of access to care. As regulators continue to reassess exposure limits for endocrine-active substances, care pathways for earlier screening and treatment are likely to remain a planning priority for the central precocious puberty market.

Uptake Of Long-Acting GnRH-Analog Depots & Implants

Six-month depot formats are reducing visit frequency and improving adherence, supported by Phase III data showing 94% of pediatric patients on leuprolide mesylate 42 mg achieved LH suppression below 4 mIU/mL at Week 24 with statistical significance. Annual dosing is moving closer, with a 12 month triptorelin formulation completing Phase III enrollment across multiple countries and targeting a 2026 U.S. filing. As families reduce clinic visits relative to monthly schedules, indirect costs and school or work absences also fall, which supports steady adherence over multi-year courses of therapy in the central precocious puberty market. Manufacturing precision for uniform PLGA microspheres remains a limitation in scaling supply, which concentrates risk and makes single-site interruptions more consequential for patient access [2]Medicine Supply Notification, Triptorelin Acetate Gonapeptyl Depot 3.75 mg,” Community Pharmacy England. These delivery platform shifts are now core to competitive strategies, since pharmacologic mechanisms across GnRH agonists are similar and differentiation hinges on interval, consistency, and product logistics in the central precocious puberty market.

Wider Reimbursement Expanding Treatment Access

U.S. payer criteria have broadened coverage, with policies that list Fensolvi 45 mg every 24 weeks, Lupron Depot Ped at approved intervals, Supprelin LA 50 mg annually, Synarel nasal spray, and Triptodur 22.5 mg every 24 weeks for CPP when clinical and laboratory criteria are met. These policies accept third-generation or ultrasensitive LH assays and use LH detection thresholds below 0.2 mIU/L for confirmation, which streamlines qualifying documentation for prior authorization. Quantity limits have been aligned to dosing intervals, including one kit per 24 weeks for Fensolvi and one implant per year for Supprelin LA, which has clarified renewal timing for care teams and families. The net effect is fewer administrative cycles between endocrinology practices and plans, which reduces delays to start or continue therapy in the central precocious puberty market. While coverage terms are improving, total therapy costs can still limit uptake in lower-income settings, which keeps access uneven across regions of care in the central precocious puberty market.

Improved Ultrasensitive LH Assays Boosting Early Diagnosis

Diagnostic workflows are becoming more precise, with a study validating that a single LH draw at 60 minutes after triptorelin stimulation can diagnose HPG axis activation in girls, using optimal cut-offs of 4.45 IU/L in overweight precocious pubertal girls and 4.20 IU/L in pubertal girls. Pairing basal LH with DHEAs has shown high discriminative performance for CPP prediction with an AUC of 0.973, which supports reduced reliance on multi hour stimulation testing in many clinics. These gains help clinicians act earlier to prevent accelerated bone age and compromised adult height, which strengthens the care pathway in the central precocious puberty market. Shorter, clearer protocols also lower the burden on families and laboratories, which shortens the time between first specialist contact and treatment initiation. Laboratory quality frameworks such as ISO 15189 are helping harmonize assay performance, which stabilizes test interpretation and downstream treatment decisions in the central precocious puberty market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Annual Therapy Cost in Low-Income Regions | -0.8% | MEA, South America, rural APAC | Long term (≥ 4 years) |

| Limited CPP Awareness Among Primary-Care Physicians | -0.6% | Global, most acute in MEA and South America | Medium term (2-4 years) |

| Safety Concerns: Bone-Density Loss & Intracranial Hypertension | -0.4% | Global | Short term (≤ 2 years) |

| Supply-Chain Gaps for Biodegradable Microsphere Injectables | -0.5% | Europe, North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Supply-Chain Gaps for Biodegradable Microsphere Injectables

Documented shortages of depot triptorelin in the United Kingdom from March 2025 through January 2026 illustrate the fragility of PLGA microsphere supply lines, with Tier 2 disruption status underscoring the medium impact on patients and providers. Concentrated manufacturing and complex particle engineering increase the chance that a single facility issue can affect many clinics at once in the central precocious puberty market. Parallel availability of alternative GnRH analogs during this period mitigated some of the access risks, yet switching can complicate scheduling and monitoring across health systems. These events highlight the operational value of multi-product formularies and cross-training among pharmacy teams, which reduces friction when shortages arise. The underlying dynamic supports strategic investments that diversify sources and build redundancy for critical components in the central precocious puberty market.

Limited CPP Awareness Among Primary-Care Physicians

Referral delays persist when early signs are misattributed to weight-related pseudopubertal changes rather than HPG axis activation, which pushes first specialist visits beyond an optimal treatment window in some cases. Standardized algorithms and CME-driven refreshers have improved baseline recognition in higher resource settings, yet awareness remains uneven where pediatric endocrinology training pipelines are limited. These gaps can slow time to diagnostic confirmation, heighten family uncertainty, and reduce the likelihood of initiating timely GnRH analog therapy in the central precocious puberty market. Structured triage protocols and simple checklist tools can reduce watch-and-wait decisions in borderline cases when used alongside assay-based confirmation. The result is more consistent care escalation at the primary care and specialist interface, which raises the share of eligible children who receive guideline-supported therapy in the central precocious puberty market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Leuprolide Dominates, Yet Triptorelin’s Depot Edge Drives Faster Growth

Leuprolide acetate secured 45.24% of the central precocious puberty market share in 2025, reflecting the depth of the Lupron Depot franchise across multiple dosing intervals. Triptorelin is projected to grow at a 7.49% CAGR through 2031 as semiannual formulations and the first annual injectable candidate advance, which is consistent with provider preferences for longer intervals and streamlined clinic schedules in the central precocious puberty market. Histrelin, delivered as a surgically implanted 50 mg device, faced revenue pressure in late 2024 as payers shifted to injectable depots and families weighed the trade-offs of minor procedures versus office-based injections. Nafarelin nasal spray continues to serve a narrow group of patients who require a non-injectable route, although its frequent dosing reduces suitability for many families in the central precocious puberty market. Across these options, choice is shaped by dosing cadence, predictability of LH suppression at interval endpoints, and the ease of coordinating refills and visits across busy pediatric practices.

In late 2025, a six-month leuprolide mesylate formulation met its primary endpoint in Phase III pediatric CPP with 94% LH suppression at Week 24, which would add a third semiannual leuprolide option if approved[3]Foresee Pharmaceuticals, “CASPPIAN Phase 3 Study Meets Primary Efficacy Endpoint”. Portfolio breadth that spans one month to six months has helped incumbents retain brand familiarity among pediatric endocrinologists, although longer-acting products are capturing more starts and switches as care teams aim to reduce missed doses in the central precocious puberty market. Annual triptorelin would extend that logic further by compressing the visit schedule to a single implant-style appointment per year if outcomes prove noninferior, which could shift share from quarterly and semiannual regimen. Evidence reviews also suggest interest in combination care, where GnRH analogs with growth hormone can improve height outcomes in select cases, although costs and monitoring needs limit widespread use in the central precocious puberty industry.

By Distribution Channel: Hospital Pharmacies Lead, Online Channels Surge on Payer Mandates

Hospital pharmacies accounted for 40.12% of distribution in 2025, reflecting integrated models where pediatric endocrinology clinics coordinate ordering, storage, and administration for depot injectables. Online specialty pharmacies are forecast to grow at a 7.88% CAGR through 2031 as payer networks steer high-cost therapies into mail-order channels with dedicated counseling and logistics teams for temperature-sensitive products in the central precocious puberty market. Retail channel volumes are smaller since limited distribution programs and payer contracts often bypass traditional chains, which concentrates dispensing among specialty providers that can manage benefits verification and delivery scheduling. Aligning refill cycles to dosing windows, especially for six-month depots, reduces the risk of lapse and improves on-time administration in the central precocious puberty market. Hospital-affiliated outpatient infusion centers and pediatric day hospitals remain important for new starts and for patients who require observation due to comorbidities.

As coverage criteria and quantity limits stabilize, online and specialty channels have scaled clinical services such as injection education, adherence outreach, and coordination of prior authorization renewals, which help busy clinics reduce administrative burden. Provider choice across channels is shaped by product availability, local practice settings, and the need for physical administration, which still anchors many patients to in-person care in the central precocious puberty industry. The centralization of specialty dispensing simplifies cold chain handling but can create single-point dependencies that are sensitive to supply interruptions, which reinforces the value of contingency plans at the clinic and payer levels. As online platforms refine pediatric support services, the balance between convenience and clinical oversight continues to evolve in the central precocious puberty market.

Geography Analysis

North America retained 43.11% of the central precocious puberty market share in 2025, supported by broad coverage in major plans, clear testing criteria, and multiple long-acting GnRH analogs available to pediatric endocrinologists. U.S. payer policies have specified accepted assay types, thresholds for LH results, and quantity limits aligned to dosing intervals, which improves predictability in treatment approvals and renewals for families and providers. In Canada, a six-month 45 mg leuprolide strength received approval in late 2025, adding to the set of long-acting options across North America and reinforcing the role of extended intervals in routine practice in the central precocious puberty market. Clinicians are also responding to safety signals emerging in the literature, including a meta-analysis that observed higher PCOS risk in treated girls relative to untreated cohorts, which is informing counseling and follow-up discussions with families. The regional ecosystem of specialty pharmacies, children’s hospitals, and payer formularies supports timely care, even as supply stewardship remains important in the central precocious puberty market.

Asia Pacific is the fastest-growing region at an expected 8.24% CAGR from 2026 to 2031, helped by increasing diagnostic capacity, expanding specialist coverage, and rising awareness among families seeking early interventions. A comprehensive meta-analysis that aggregated studies across China, South Korea, and Thailand reflected active clinical research and a growing base of patients entering care pathways, with efficacy influenced by age at onset and timeliness of initiation. As longer-acting formats scale globally, providers in APAC are prioritizing dosing intervals that match clinic resources and family preferences, which supports steady adoption in the central precocious puberty market. Multi-country pediatric trials for annual triptorelin underscore the region’s increased participation in late-stage development and signal the demand for delivery models that minimize clinic visits while preserving suppression targets. Continued investments in lab infrastructure and teleconsult coverage are expected to improve referral pathways and reduce diagnostic delays in the central precocious puberty market.

Europe shows steady adoption at mid single-digit growth, anchored by established pediatric endocrinology centers, HTA processes, and country-level reimbursement frameworks that support long-acting GnRH analogs. Ipsen reported strong 2025 performance across therapeutic areas and guided to sustained margin strength in 2026, which reflects underlying demand for rare disease assets and the capability to maintain supply at scale. Supply monitoring remains a regional focus following U.K. notifications of triptorelin depot shortages that persisted into early 2026, which highlighted the need for contingency stocks and alternative regimens during constrained periods in the central precocious puberty market. In the Middle East and Africa and in South America, access is evolving from smaller bases as specialty pharmacy networks, diagnostic capacity, and public payer coverage expand at different speeds, which keeps the share modest but rising in the central precocious puberty market.

Competitive Landscape

Competition is centered on delivery innovation rather than new pharmacologic targets, since GnRH agonists share a mechanism and comparable effects on LH suppression when delivered consistently. In late 2025, a six-month 45 mg leuprolide strength received approval in Canada, reinforcing the trend toward extended dosing intervals and validating development strategies that focus on convenience and adherence. A six-month leuprolide mesylate candidate reported Phase III success, while an annual triptorelin formulation completed Phase III enrollment across the Americas, positioning sponsors to compete on once or twice per year schedules in the central precocious puberty market. Endo’s 2024 results showed pressure on the histrelin implant business, consistent with the shift away from surgical placement in favor of office-based injectables in the central precocious puberty market.

Ecosystem participants are also preparing for potential needle-free options. Oral GnRH antagonists already suppress gonadotropins in adults, and sponsors continue to gather pharmacokinetic and pediatric tolerability data that could open new routes if regulators accept dosing paradigms for younger patients. If pediatric approvals arrive, daily adherence will become a central determinant of outcomes, which would alter the balance of factors providers weigh when comparing annual or semiannual depots to tablets in the central precocious puberty market. In parallel, combination therapy with growth hormone has shown added height gains in select cases, although real-world adoption is tempered by cost and monitoring requirements.

Capabilities in complex injectables are expanding among generics and specialty manufacturers, as reflected by approvals in other long-acting depot categories that rely on uniform microsphere production. A 2025 U.S. approval for a long-acting risperidone by a generic sponsor showcased particle control expertise and a platform designed for biodegradable microspheres, which signals potential for broader competition if regulatory pathways and clinical equivalence requirements for depot GnRH analogs become clearer. Strategic messaging from large-cap incumbents in 2026 continues to emphasize investment in R&D scale and manufacturing resilience, which supports supply continuity and product life cycle extensions in the central precocious puberty market. As companies prioritize interval length, predictable suppression, and reliable delivery, the central precocious puberty market is likely to remain focused on platform execution and access expansion rather than on new mechanisms over the near term.

Central Precocious Puberty Industry Leaders

Pfizer Inc.

AbbVie Inc.

AstraZeneca plc

Endo Pharmaceuticals Inc.

Ferring Pharmaceuticals

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Foresee Pharmaceuticals announced that its Phase III CASPPIAN trial for FP 001 42 mg met the primary efficacy endpoint, with 94% of CPP patients achieving serum LH suppression below 4 mIU/mL at Week 24 with P = 0.0005, and plans to file an NDA by mid 2026.

- November 2025: Debiopharm completed enrollment in the Phase III LIBELULA trial evaluating Debio 4326, a 12-month extended-release triptorelin formulation for pediatric CPP across the United States, Argentina, Brazil, Chile, and Mexico, with a U.S. regulatory submission targeted in 2026.

- November 2025: AbbVie received Health Canada approval for Lupron Depot 45 mg at a six month dosing interval for advanced prostate cancer, expanding the product’s approved strengths that also include CPP among indications.

- April 2025: Anthem published updated medical drug clinical criteria for GnRH analogs in non-oncologic indications, including CPP, accepting ultrasensitive LH assays and aligning quantity limits to dosing intervals.

Global Central Precocious Puberty Market Report Scope

| Leuprolide Acetate |

| Triptorelin |

| Histrelin |

| Nafarelin |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class | Leuprolide Acetate | |

| Triptorelin | ||

| Histrelin | ||

| Nafarelin | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the size and growth outlook for the central precocious puberty market through 2031?

The central precocious puberty market size is USD 1.82 billion in 2026 and is projected to reach USD 2.56 billion by 2031 at a 7.08% CAGR over 2026-2031.

Which therapy class currently leads the central precocious puberty market?

Leuprolide acetate leads by revenue with 45.24% in 2025, while triptorelin is the fastest growing class to 2031 as longer dosing intervals gain traction.

Which distribution channels are expanding fastest for CPP treatments?

Online specialty pharmacies are the fastest-growing channel with a projected 7.88% CAGR to 2031, while hospital pharmacies remain the largest share at 40.12% in 2025.

Which region leads and which is growing fastest in CPP?

North America leads with 43.11% in 2025, and Asia Pacific is the fastest-growing region with an expected 8.24% CAGR through 2031.

What clinical or policy shifts are shaping the central precocious puberty market now?

Ultrasensitive LH assays are streamlining diagnosis, and U.S. payers have aligned coverage and quantity limits to long-acting dosing intervals, which supports wider access and predictable renewals.

What pipeline advances could change patient experience in CPP?

The most notable advances are six-month depots with strong LH suppression data and the first annual triptorelin in Phase III, which together could reduce clinic visits and improve adherence if approvals are secured.

Page last updated on: