Central and Eastern Europe Global Capability Centers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

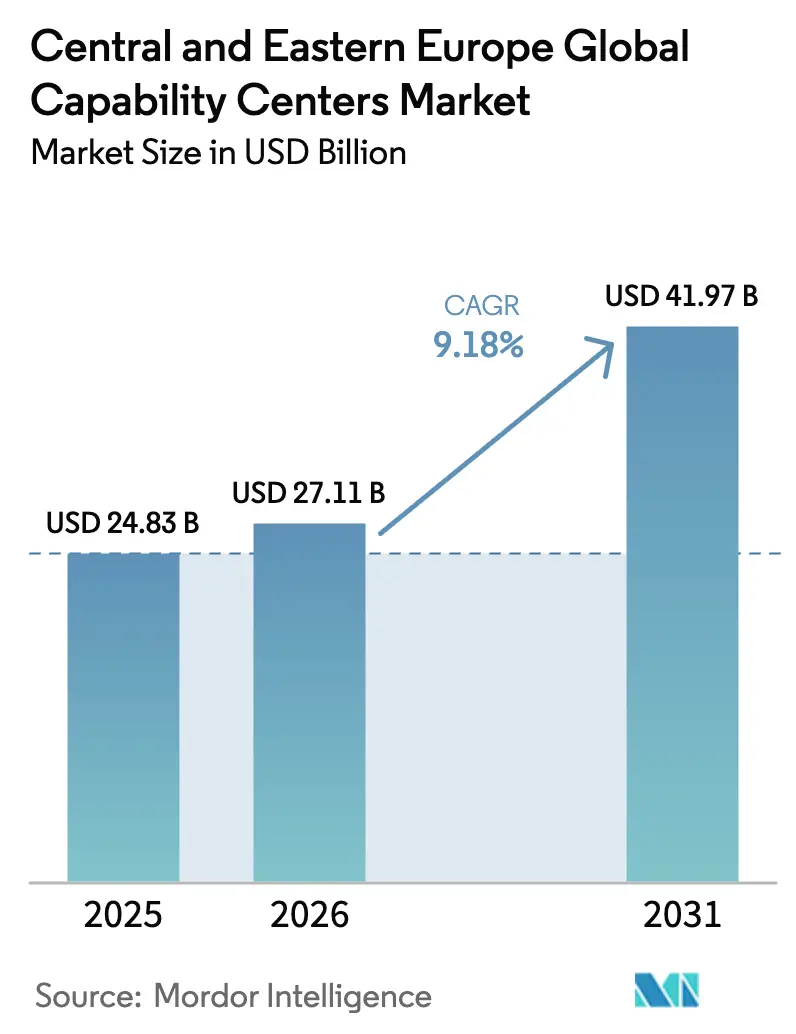

| Base Year Market Size (2025) | USD 24.83 Billion |

| Market Size (2026) | USD 27.11 Billion |

| Market Size (2031) | USD 41.97 Billion |

| Growth Rate (2026 - 2031) | 9.18% CAGR |

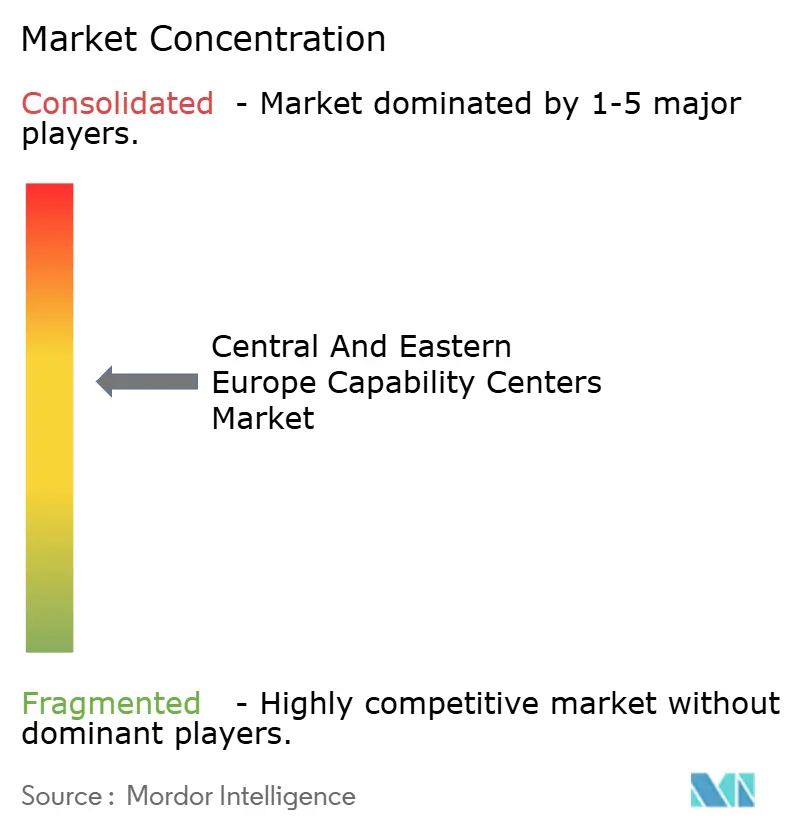

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Central and Eastern Europe Global Capability Centers Market Analysis by Mordor Intelligence

The Central and Eastern Europe Global Capability Centers Market size was valued at USD 24.83 billion in 2025 and estimated to grow from USD 27.11 billion in 2026 to reach USD 41.97 billion by 2031, at a CAGR of 9.18% during the forecast period (2026-2031). The expansion reflects sizable near-shore demand from Western Europe, strong governmental support for digital transformation, and accelerating adoption of artificial intelligence across knowledge processes. Service providers benefit from a cost-to-quality advantage that persists despite wage inflation in Tier-1 cities, while European Union funding of EUR 134 billion (USD 147.4 billion) under the Recovery and Resilience Facility upgrades regional digital infrastructure.[1]European Commission, “Recovery Plan for Europe,” COMMISSION.EUROPA.EU Growing engineering requirements from automotive original-equipment manufacturers, widespread cloud migration, and the resilience imperative triggered by supply-chain shocks continue to attract fresh corporate footprints to secondary Polish, Czech, and Romanian cities. Multilingual talent and European time-zone proximity further reinforce the CEE value proposition, enabling productivity gains of 15-25% when generative AI tools scale across customer service, software development, and compliance functions.

Key Report Takeaways

- By function, Business Process Management held 48.12% of the Central and Eastern Europe Global Capability Centers market share in 2025, while Information Technology and Digital Services are expected to expand at a 9.54% CAGR through 2031.

- By engagement model, the captive segment commanded 57.85% of the 2025 revenue base; hybrid Build-Operate-Transfer (BOT) deployments registered the fastest growth at a 9.96% CAGR to 2031.

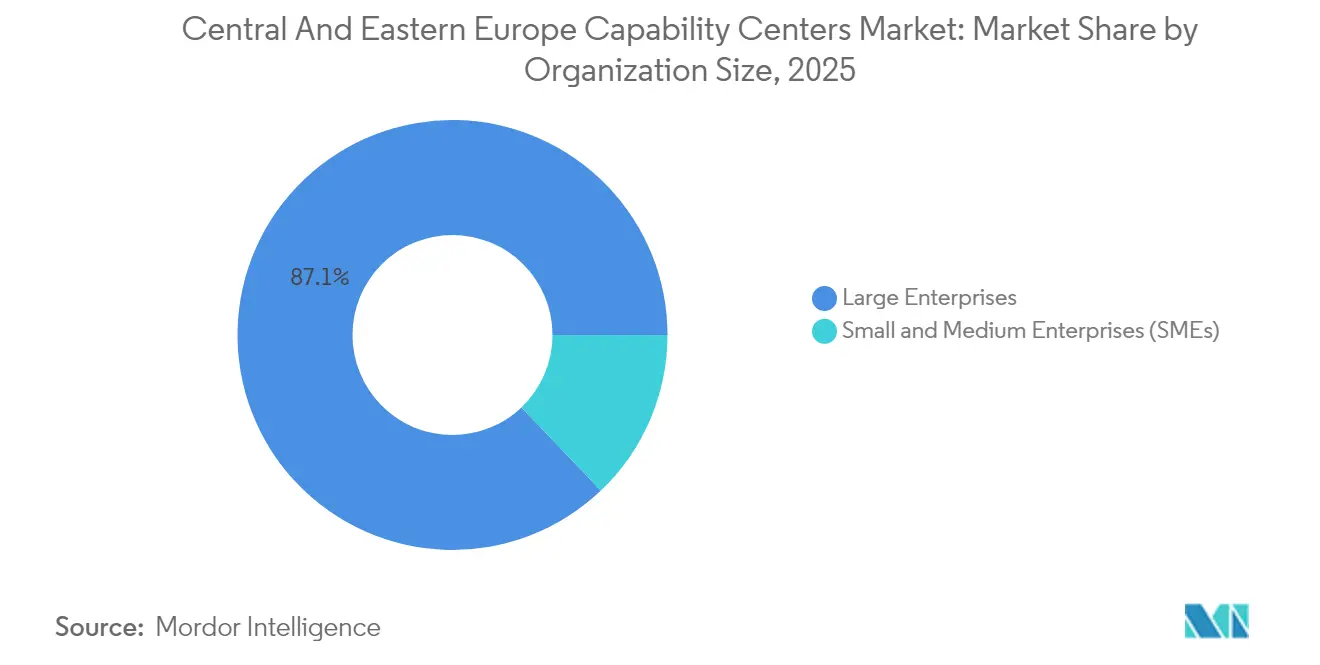

- By organization size, large enterprises accounted for 87.12% of the 2025 demand; however, Small and Medium Enterprises are poised for an 10.74% CAGR through 2031.

- By industry vertical, Banking, Financial Services, and Insurance led with 36.02% revenue share in 2025, whereas Manufacturing, Automotive, and Industrial activities are forecast to accelerate at a 9.82% CAGR.

- By country, Poland secured 53.88% of the total revenue in 2025; Romania is projected to have the highest CAGR at 9.94% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Central and Eastern Europe Global Capability Centers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising near-shore demand from Western Europe | +2.1% | Poland, the Czech Republic, Romania, and Hungary | Medium term (2-4 years) |

| GenAI-enabled productivity leap in multilingual talent hubs | +1.8% | Poland, Romania, Ukraine, Czech Republic | Short term (≤ 2 years) |

| Cost-to-quality advantage versus Western Europe and North America | +1.5% | Entire CEE region | Long term (≥ 4 years) |

| EU funds accelerating digital and green transformation projects | +1.2% | EU member states in CEE | Medium term (2-4 years) |

| De-risking global footprints via Europe-friendly time zones | +0.9% | Poland, the Czech Republic, Hungary, and Slovakia | Long term (≥ 4 years) |

| Shift from BPO to knowledge-intensive engineering centers | +0.7% | Poland, Romania, Ukraine, Czech Republic | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Near-Shore Demand From Western Europe

Western European companies continue to relocate technology and business support work to nearby Central and Eastern European locations, where salaries remain at least 60% lower than in Frankfurt or London, while cultural alignment and European Union regulations remain intact. The trend accelerated after 2020-2022 logistics disruptions exposed offshore vulnerabilities, prompting German automotive groups to open 47 engineering hubs across Poland and the Czech Republic in 2024.[2]German Federal Ministry for Economic Affairs and Climate Action, “Electric-Vehicle Engineering Investments,” BMWK.DE Access to 180,000 new STEM graduates every year further strengthens the case for complex software and hardware projects. Engineering centers in Wroclaw, Brno, and Katowice now handle electric-vehicle software, battery management, and autonomous-driving algorithms that were once developed in Western Europe.

GenAI-Enabled Productivity Leap In Multilingual Talent Hubs

Generative AI applications rolled out across capability centers raise coding throughput by 35-40% and automate up to 70% of routine help-desk inquiries. In 2024, technology firms invested USD 2.8 billion in Polish AI infrastructure, positioning Warsaw as a regional machine-learning hotbed.[3]Polish Investment and Trade Agency, “AI Infrastructure Investments,” PAIH.GOV.PL Multilingual linguists, typically fluent in three or four European languages, train conversational agents that power cross-border banking and e-commerce support. Microsoft’s USD 1 billion allocation to new cloud zones in Poland and Google’s 40% workforce expansion at the Warsaw AI Center signal a shift from purely transactional work toward value-creating innovation that draws on deep natural language and data science expertise.

Cost-to-Quality Advantage Versus Western Europe And North America

Even with rising wages, senior software engineers in Warsaw earn USD 45,000-65,000, far below USD 120,000-180,000 in Frankfurt or London, while comparable outcomes are achieved on agile sprints, security audits, and cloud migrations. Real-estate costs follow a similar pattern: prime Prague offices cost USD 25-35 per m² monthly, versus USD 80-120 in Paris, which lowers total operating costs by 50-60%. CEE governments invest 4.8% of GDP in higher education, above the EU average, and sponsor continuous-learning vouchers that keep engineering talent current on cybersecurity, DevOps, and cloud-native frameworks.

EU Funds Accelerating Digital And Green Transformation Projects

The European Union has earmarked EUR 59 billion (USD 64.9 billion) for digital upgrades in Central and Eastern European member states. Poland alone is securing EUR 23.9 billion (USD 26.29 billion) and is pledging 21% to 5G rollout, sovereign cloud, and national cybersecurity fabrics. Improved connectivity and low-latency networks shorten deployment cycles for advanced analytics platforms housed inside regional capability centers. Romania allocates EUR 1.8 billion (USD 1.98 billion) for public-service digitization, which is distributed to private vendors specializing in enterprise resource planning, document management, and citizen identity protection.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying wage inflation in Tier-1 CEE cities | -1.4% | Warsaw, Prague, Bucharest, Budapest | Short term (≤ 2 years) |

| Chronic talent leakage to Western Europe | -1.1% | Poland, Romania, Hungary, Czech Republic | Medium term (2-4 years) |

| Geopolitical volatility near the Ukraine conflict zone | -0.8% | Poland, Romania, Hungary, Slovakia | Medium term (2-4 years) |

| Real-estate supply bottlenecks in top tech hubs | -0.6% | Warsaw, Prague, Bucharest, Krakow | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Intensifying Wage Inflation In Tier-1 CEE Cities

Salary growth of 10-12% per year in Warsaw, Prague, and Bucharest narrows the historical labor arbitrage gap, putting pressure on profit margins for both captives and third-party providers. Talent shortages, in some niches, demand exceeds supply by as much as 40%, trigger bidding wars and driving compensation closer to Western European benchmarks. Many investors respond by opening satellites in Gdańsk, Wrocław, and Cluj-Napoca; however, these locations face constrained office space and smaller university pipelines that limit center scalability.

Chronic Talent Leakage To Western Europe

Freedom of movement within the European Union enables the steady migration of seasoned engineers to higher-paying markets. Germany alone hired 89,000 Polish workers in 2024, with 35% of them possessing advanced technology skills.[4]German Federal Employment Agency, “Worker Migration Statistics,” ARBEITSAGENTUR.DE This drain affects mid-career specialists, the backbone of delivery leadership, leading to succession-planning challenges and higher onboarding costs for capability centers. Employers counter with retention bonuses, stock-purchase programs, and sponsored postgraduate education, but the outflow remains a structural headwind.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Function / Capability: Digital Acceleration Reshapes Service Mix

Business Process Management retained 48.12% of the Central and Eastern Europe Global Capability Centers market share in 2025, underscoring the region’s strong track record in multilingual finance, procurement, and human resources processing. Transactional excellence initially built the investor base, but cloud adoption and platform modernization have redirected incremental spending toward software engineering, cybersecurity, and data analytics. The Information Technology and Digital Services stream, projected to grow at a 9.54% CAGR through 2031, now absorbs budget from European cloud migrations, agile product roadmaps, and enterprise natural language engines. Engineering teams in Krakow develop microservices for global e-commerce majors, while Romanian specialists craft regulatory-compliant fintech modules in accordance with the European Parliament's AI Act.

The functional shift toward higher-value work carries revenue premiums of 40-60% relative to traditional BPO rates, cushioning providers against wage escalation. The Central and Eastern Europe Global Capability Centers market size for engineering services is expected to expand faster than any other capability bucket, as automotive, pharmaceutical, and medical technology clients relocate innovation labs to access domain-focused PhDs at a competitive cost. Captive design houses operated by Microsoft, SAP, and Oracle codify best practices and deepen local vendor ecosystems that supply DevOps automation, model-risk validation, and quality assurance toolchains.

By Engagement Model: Flexibility Drives Hybrid Adoption

In 2025, captives delivered 57.85% of all services, cementing their role in safeguarding intellectual property and ensuring rigorous compliance for regulated sectors. Established banks and telecom carriers maintain a preference for wholly owned sites staffed by 500-5,000 employees across Poland and the Czech Republic. Even so, the Build-Operate-Transfer pathway accelerates at 9.96% CAGR, reflecting mid-market adoption of phased approaches that temper upfront capital commitments. Under this model, an experienced vendor launches a center, operates it according to agreed-upon service-level metrics, and transfers ownership after two to three years. Success stories such as Nordea’s 1,500-person technology hub in Gdynia demonstrate how the arrangement reduces ramp-up risk while preserving long-term cost optimization.

Hybrid configurations also attract Small and Medium Enterprises seeking a foothold in the Central and Eastern Europe Global Capability Centers market without building standalone legal entities. Vendors structure modular governance frameworks and compliance playbooks that shorten onboarding to fewer than 90 days and facilitate future captive takeovers once scale thresholds are reached.

By Organization Size: Enterprise Dominance With SME Momentum

Large multinational corporations generated 87.12% of 2025 revenue, propelled by complex multi-domain programs that rely on enterprise-grade security controls and global process ownership. Mega centers in Warsaw, Krakow, and Prague often span finance, procurement, legal, and engineering activities under one roof, leveraging economies of scale in facility management, training, and vendor contracting. These players also pilot emerging technologies, such as synthetic data generation for model training, before rolling them out to other regions within their network.

Small and Medium Enterprises, however, are expected to register an 10.74% CAGR through 2031, illustrating that democratized cloud platforms and shared-service constructs lower participation barriers. Pay-as-you-grow subscription models enable SMEs to access cybersecurity operations, DevSecOps toolchains, and multilingual customer analytics without incurring fixed real estate obligations. Regional providers curate service catalogs that bundle public-cloud resell, near-real-time language translation, and governance dashboards tailored to firms with fewer than 1,000 employees.

By Industry Vertical: BFSI Leads, Manufacturing Gains Speed

At a 36.02% revenue share, Banking, Financial Services, and Insurance remains the dominant vertical, fortified by European Union regulations on anti-money laundering, data privacy, and capital adequacy that demand continuous compliance support. Capability centers in Krakow and Sofia handle Know-Your-Customer (KYC) adjudication, credit scoring model validation, and instant payment reconciliation for pan-European banks. Simultaneously, Manufacturing, Automotive, and Industrial projects expand at a 9.82% CAGR as electric-vehicle platforms, predictive-maintenance analytics, and digital twin simulations migrate from German headquarters to near-shore engineering bases. Volkswagen’s Prague software unit, set to employ 2,000 engineers by 2026, exemplifies the strategic pivot from mechanical to software-defined automotive systems.

Life sciences, retail, and energy domains also turn to Central and Eastern Europe Global Capability Centers to supplement scarce domain talent and meet sovereignty requirements for sensitive research data. Strong science faculties and affordable specialized labs in Ljubljana, Brno, and Debrecen reinforce the region’s appeal for Good Laboratory Practice-compliant digital trials.

Geography Analysis

Poland captured 53.88% of the revenue in 2025, reflecting two decades of cumulative investment in business services ecosystems, modern highways, and a domestic population of 38 million that fuels deep talent pools. Warsaw and Kraków remain anchor sites, although Gdańsk, Wrocław, and Poznań now absorb secondary expansions amid rising wages in capital cities. Incentives under the Polish Investment Zone grant corporate income tax relief of up to 70% for digital projects located in emerging economic districts, lowering total ownership costs and promoting geographic dispersion.

Romania is projected to post a leading 9.94% CAGR through 2031, driven by competitive salary benchmarks, subsidy packages for technology exporters, and a robust pipeline of software engineers graduating from Cluj-Napoca and Iasi each year. Bucharest already hosts over 150 multinationals, while secondary metropolitan areas nurture specialty clusters: Cluj-Napoca for automotive embedded code, Timisoara for hardware design, and Iasi for multilingual fintech support. Latin-based language skills enable seamless expansion into Spanish, Italian, and French customer bases.

Czech Republic, Hungary, Slovakia, and Bulgaria round out the core Central and Eastern Europe Global Capability Centers market, together delivering finance hubs for Austrian banks, analytics labs for Scandinavian retailers, and cybersecurity centers for telecom majors. The Baltic states capitalize on advanced e-government infrastructure, while Croatia and Slovenia court high-value niche engineering projects related to renewable energy and marine technology.

Competitive Landscape

The Central and Eastern Europe Global Capability Centers market remains moderately concentrated, with the top 10 providers accounting for a significant share of revenue, leaving ample room for regional specialists and emerging cloud-native boutiques. Scale leaders, such as EPAM Systems, Luxoft, and SoftServe, leverage extensive delivery networks and established enterprise relationships across the banking and automotive verticals. Each invests aggressively in proprietary data platform accelerators, autonomous driving toolkits, and DevSecOps pipelines to defend premium pricing. Private-equity inflows of USD 3.2 billion in 2024 accelerated consolidation, funding bolt-on acquisitions that expand geographic footprints and vertical domain depth.

Technology leadership stands as the pivotal differentiator. Providers race to achieve ISO 27001, SOC 2, and forthcoming EU AI governance certifications that assure clients of rigorous data stewardship. EPAM’s USD 460 million acquisition of Neoris expanded its manufacturing domain solutions, while Luxoft opened a 400-seat automotive lab in Prague to strengthen its autonomous driving portfolio. Mid-tier firms counter by emphasizing niche expertise, such as near-real-time embedded coding for MedTech devices, and faster decision cycles compared with multinational giants. In response, captives increasingly partner with multiple local vendors to diversify risk, tap specialized skills, and catalyze innovation sprints.

Strategic initiatives also include talent-upskilling consortiums with universities, cross-border rotational programs for knowledge retention, and shared innovation labs that incubate AI proof-of-concepts under client co-financing. These activities embed providers more deeply into client transformation roadmaps, driving multi-year contract renewals and higher total contract value.

Central and Eastern Europe Global Capability Centers Industry Leaders

EPAM Systems Inc.

Luxoft Holding Inc.

SoftServe Inc.

N-iX LLC

GlobalLogic Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Microsoft announced a USD 1.2 billion expansion of its Polish cloud infrastructure, establishing a new Azure region in Gdansk and adding 800 AI engineers in Warsaw.

- August 2025: EPAM Systems closed the USD 180 million purchase of Romanian firm Zitec, onboarding 1,200 fintech and e-commerce specialists.

- July 2025: Google increased Warsaw engineering headcount by 600, allocating USD 150 million to YouTube platform localization.

- June 2025: Luxoft opened a 400-person automotive engineering center in Prague in partnership with the Czech Technical University.

Central and Eastern Europe Global Capability Centers Market Report Scope

The scope of the global capability center study for the market segmentation by the Function/Capability for (i) Information Technology (IT) and Digital Services segment is limited to Software Development, Cloud and Infrastructure Management, Cybersecurity, Data Analytics and AI/ML; (ii) Engineering / ER&D segment is limited to Product Design and Testing, Embedded Systems, Digital Twin / Simulation; (iii) Business Process Management (BPM) segment is limited to Finance and Accounting, HR, Payroll and Talent Management, Procurement, Customer Service; and (iv)Knowledge Process Outsourcing (KPO) segment is limited to Market Research and Insights, Risk and Compliance, Legal and Regulatory Support, Strategy and Consulting Support. Similarly, for segmentation by the Engagement Model, scope for (i) Hybrid Build-Operate-Transfer (BOT) is limited to Joint Venture / Strategic Partnership and Virtual Captive Model. The rest of the segment scope is as specified for the listed segment.

| Information Technology (IT) and Digital Services |

| Engineering / ER&D |

| Business Process Management (BPM) |

| Knowledge Process Outsourcing (KPO) |

| Captive (Self-Build) / In-House |

| Build-Operate-Transfer (BOT) |

| Hybrid Build-Operate-Transfer (BOT) |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| Banking, Financial Services, and Insurance (BFSI) |

| Telecom and IT |

| Healthcare and Life Sciences |

| Manufacturing, Automotive and Industrial |

| Retail and Consumer Goods |

| Other Industry Verticals |

| Poland |

| Romania |

| Czech Republic |

| Hungary |

| Slovakia |

| Bulgaria |

| Ukraine |

| Estonia |

| Latvia |

| Lithuania |

| Croatia |

| Slovenia |

| Rest of Central and Eastern Europe |

| By Function / Capability | Information Technology (IT) and Digital Services |

| Engineering / ER&D | |

| Business Process Management (BPM) | |

| Knowledge Process Outsourcing (KPO) | |

| By Engagement Model | Captive (Self-Build) / In-House |

| Build-Operate-Transfer (BOT) | |

| Hybrid Build-Operate-Transfer (BOT) | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises (SMEs) | |

| By Industry Vertical | Banking, Financial Services, and Insurance (BFSI) |

| Telecom and IT | |

| Healthcare and Life Sciences | |

| Manufacturing, Automotive and Industrial | |

| Retail and Consumer Goods | |

| Other Industry Verticals | |

| By Country | Poland |

| Romania | |

| Czech Republic | |

| Hungary | |

| Slovakia | |

| Bulgaria | |

| Ukraine | |

| Estonia | |

| Latvia | |

| Lithuania | |

| Croatia | |

| Slovenia | |

| Rest of Central and Eastern Europe |

Key Questions Answered in the Report

What is the projected value of the Central and Eastern Europe Global Capability Centers market in 2031?

The market is forecast to reach USD 41.97 billion by 2031.

Which functional segment is growing fastest within regional capability centers?

Information Technology and Digital Services is expected to advance at a 9.54% CAGR through 2031, driven by the adoption of cloud and AI technologies.

Why are Western European enterprises shifting work to Central and Eastern Europe?

They seek cost savings exceeding 60% while retaining cultural compatibility, regulatory alignment, and European time-zone convenience.

Which country is expected to post the highest growth rate through 2031?

Romania leads with a projected CAGR of 9.94%, supported by competitive wages and government incentives.

How is generative AI impacting the productivity of the capability center?

The deployment of GenAI increases coding throughput by up to 40% and automates 70% of routine support queries, resulting in overall productivity gains of 15-25%.

Page last updated on: