Cationic Starches Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.89 Billion |

| Market Size (2031) | USD 2.33 Billion |

| Growth Rate (2026 - 2031) | 4.27% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

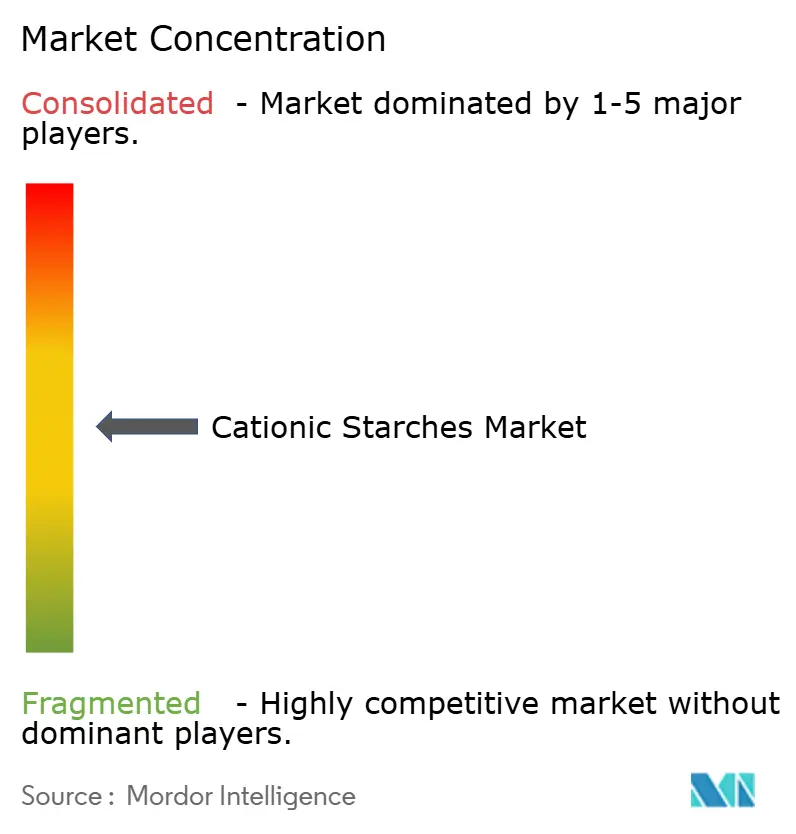

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cationic Starches Market Analysis by Mordor Intelligence

The cationic starches market size is expected to grow from USD 1.82 billion in 2025 to USD 1.89 billion in 2026 and is forecast to reach USD 2.33 billion by 2031 at 4.27% CAGR over 2026-2031. The cationic starches market is being supported by steady packaging and paperboard demand, because paper mills continue to depend on wet-end additives that improve retention, drainage, and sheet strength. The cationic starches market is also benefiting from higher recycled fiber use, since recycled furnishes carry more anionic material and often require higher starch dosage per tonne of paper output. Food processors are adding support to the cationic starches market as they keep reformulating for cleaner labels, better texture, and stable performance across convenience food categories. Over the longer term, the cationic starches market is gaining another layer of demand from pharmaceutical tablet formulations, where modified starch excipients are valued for binding, disintegration, and controlled release functions.

Key Report Takeaways

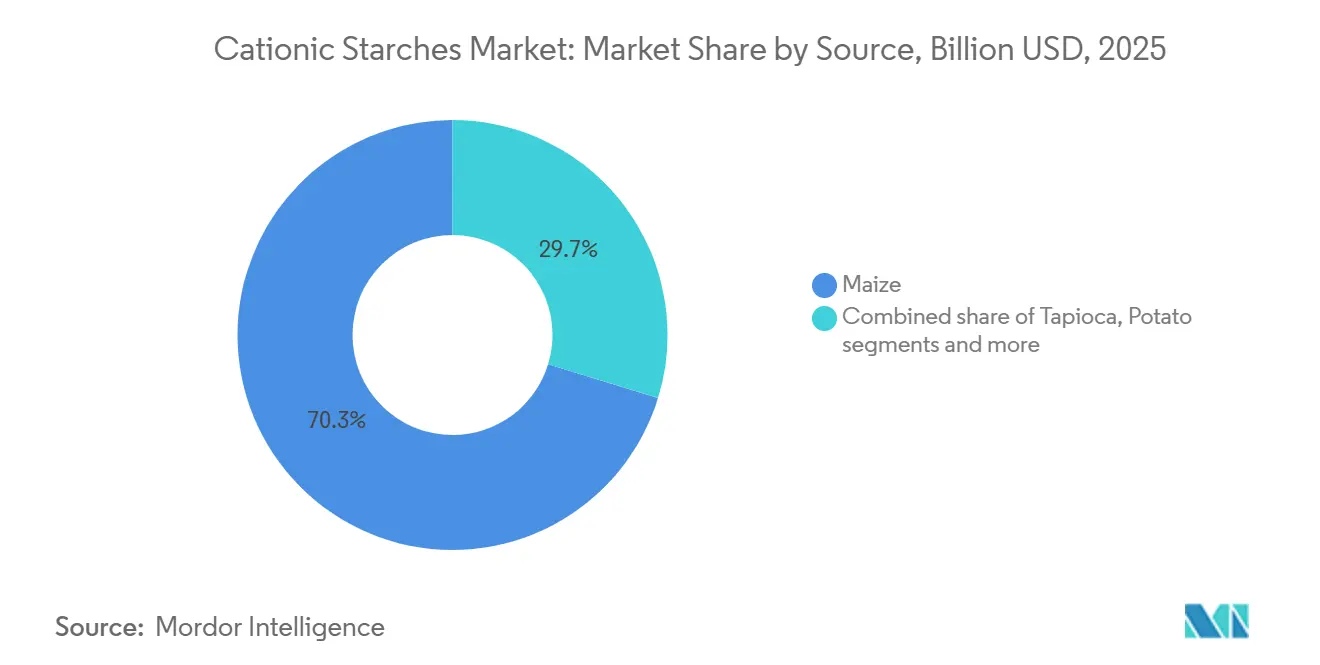

- By source, maize held 70.26% of the market in 2025, while potato is forecast to expand at a 5.46% CAGR through 2031.

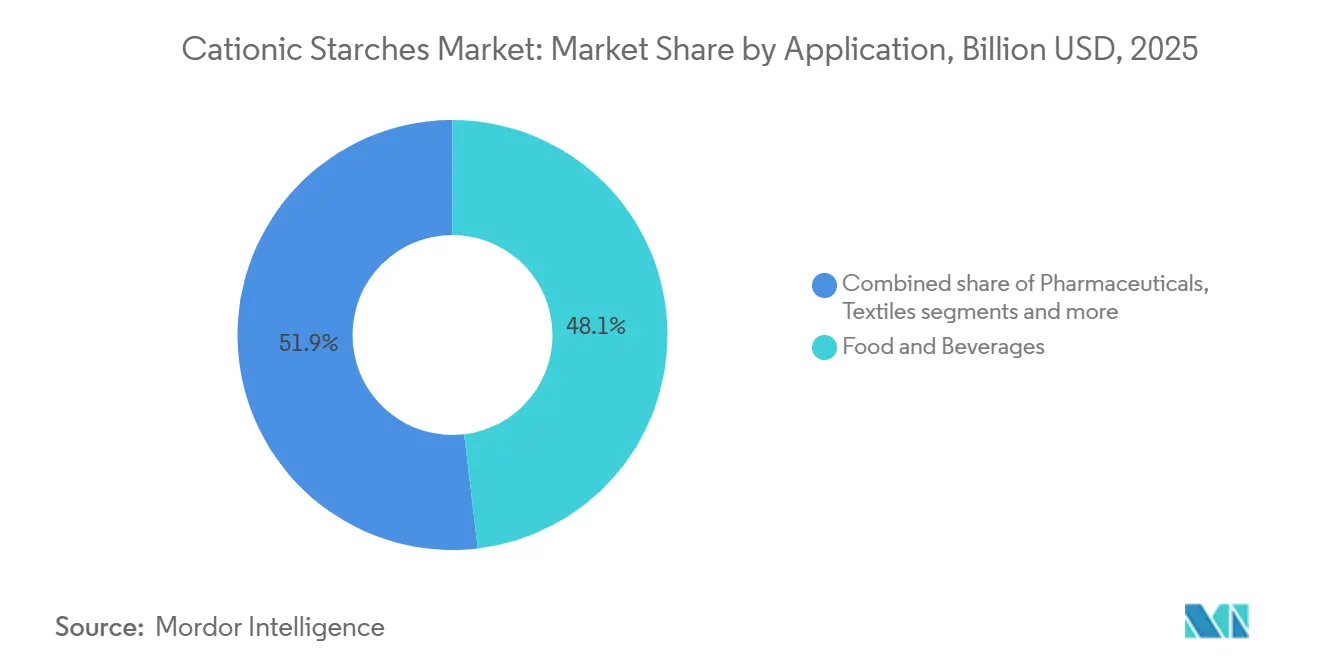

- By application, food and beverage accounted for 48.12% share of the cationic starches market size in 2025, while pharmaceuticals are projected to grow at a 5.25% CAGR through 2031.

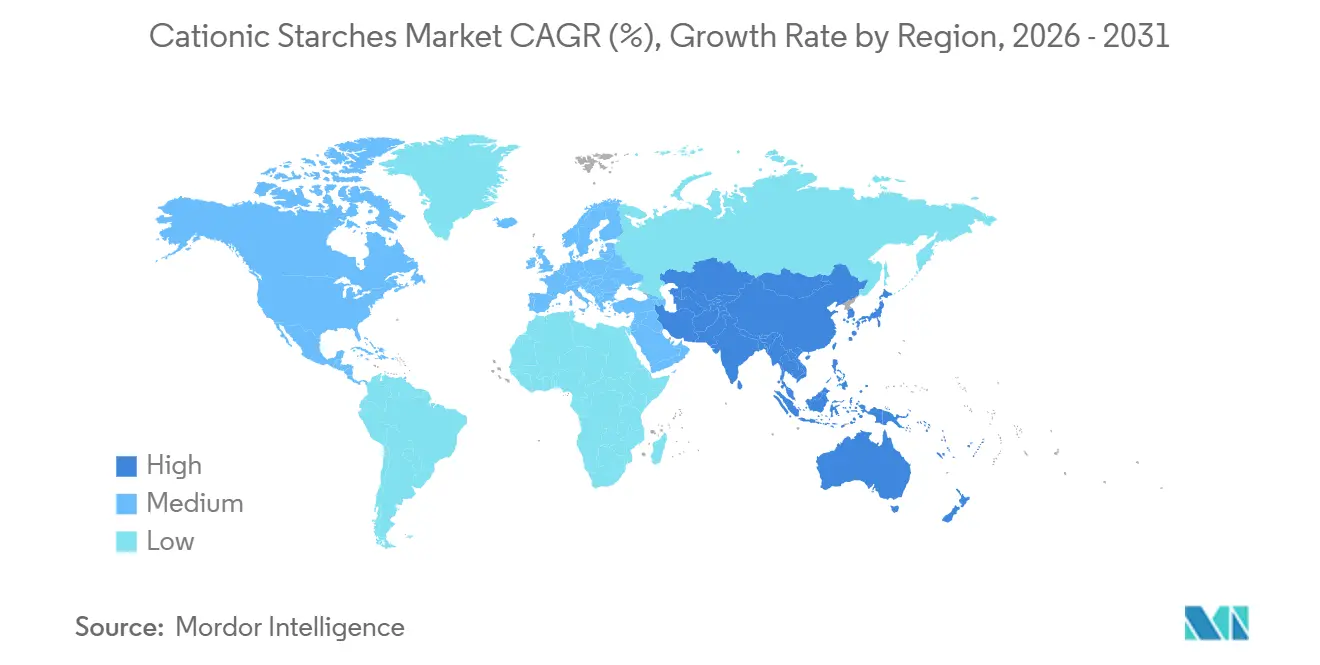

- By geography, North America held 34.11% of cationic starches market share in 2025, while Asia-Pacific is expected to record the fastest growth at a 5.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cationic Starches Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand from the paper and paperboard industry | +1.2% | Global, strongest in North America, Asia-Pacific, and Europe | Short term (≤ 2 years) |

| Increasing adoption in textile sizing and finishing applications | +0.7% | Asia-Pacific core, with spillover to South America | Medium term (2-4 years) |

| Growing demand for clean-label texture-enhancing ingredients | +0.6% | North America and Europe, with emerging relevance in Asia-Pacific | Medium term (2-4 years) |

| Expanding demand for functional food ingredients with improved stability | +0.5% | Global, strongest in North America and Western Europe | Medium term (2-4 years) |

| Technological advancements in starch modification processes | +0.4% | Global, led by the Europe, North America, and China | Long term (≥ 4 years) |

| Growth of pulp and paper manufacturing in emerging economies | +0.5% | Asia-Pacific, South America, and the Middle East and Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand from the paper and paperboard industry

The paper sector remains the largest demand center shaping the cationic starches market, but this relationship extends beyond paper volume growth. Paper mills that increase recycled fiber content often face higher anionic charge in the furnish, which raises the need for cationic starch to maintain retention and drainage performance within operating targets. According to the FAO, global paper and paperboard production reached 423 million tonnes in 2024, a 4% increase compared to 2023[1]Source: Food and Agriculture Organization, “Forest product data”, fao.org. This growth reflects rising demand for packaging, tissue, and specialty paper products, all of which use cationic starch to improve paper strength, retention, drainage, and printability. Ingredion’s February 2025 investment announcement for Cedar Rapids highlighted continued demand from packaging and papermaking customers for specialty industrial starches that offer strength, biodegradability, and recyclability benefits. For the cationic starches market, this trend keeps paper and packaging demand important for both scale and value addition.

Increasing adoption in textile sizing and finishing applications

The increasing adoption of cationic starch in textile sizing and finishing applications is a significant driver of the cationic starches market. Cationic starch is widely used as a sizing agent to improve yarn strength, reduce breakage during weaving, and enhance production efficiency by minimizing friction between fibers. In textile finishing, it provides improved fabric stiffness, smoothness, dye affinity, and print quality while contributing to better dimensional stability. Growing demand for high-quality apparel, technical textiles, and home furnishings is encouraging manufacturers to adopt performance-enhancing and sustainable textile chemicals. In addition, cationic starch is biodegradable and derived from renewable resources, making it an attractive alternative to synthetic sizing agents amid tightening environmental regulations. As textile producers increasingly prioritize cost-effective, eco-friendly, and high-performance finishing solutions, the consumption of cationic starch in textile processing is expected to continue rising throughout the forecast period.

Growing demand for clean-label texture-enhancing ingredients

The growing demand for clean-label texture-enhancing ingredients is becoming a key driver of the cationic starches market, particularly in the food and beverage industry. Consumers are increasingly seeking products formulated with recognizable, naturally derived ingredients while avoiding artificial additives and synthetic stabilizers. This shift is encouraging food manufacturers to incorporate starch-based ingredients that improve texture, viscosity, stability, and mouthfeel without compromising clean-label positioning. According to research by the CBI, Ministry of Foreign Affairs, clean-label products are projected to account for more than 70% of product portfolios during 2025 and 2026, up significantly from 52% in 2021[2]Source: CBI Ministry of Foreign Affairs, “Which trends offer opportunities”, cbi.eu, highlighting the accelerating industry transition toward transparent ingredient formulations. As a naturally sourced and renewable ingredient, starch aligns well with these evolving consumer preferences and regulatory expectations.

Expanding demand for functional food ingredients with improved stability

The cationic starches market is also gaining support from processed food categories that require better heat stability, freeze-thaw performance, and texture retention than native starches can provide. Ready meals, instant noodles, sauces, dairy alternatives, and retort products depend on ingredients that can withstand industrial processing stress and maintain acceptable texture after distribution. Research published in 2024 on cationic-acetylated glutinous rice starch showed improved texture stability and viscosity retention compared to single modification routes, supporting the development of more advanced food-grade solutions. This is important for the cationic starches market because customers seek not only thickening power but also processing consistency and shelf-life support. Suppliers that can translate starch chemistry into stable product performance have a clearer path to premium positioning in the cationic starches market. Therefore, application development capabilities remain important when competing for higher-value food contracts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict food safety regulations governing modified starch ingredients | -0.4% | Europe and North America, with spillover to export oriented Asia-Pacific producers | Medium term (2-4 years) |

| Volatility in corn, potato, and tapioca starch prices | -0.5% | Global, most acute in commodity paper and textile grades | Short term (≤ 2 years) |

| Limited adoption in regions with low industrialization | -0.3% | Sub-Saharan Africa and parts of South and Southeast Asia | Long term (≥ 4 years) |

| High production and chemical modification costs | -0.5% | Global, with a heavier effect on smaller regional producers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in corn, potato, and tapioca starch prices

Raw material cost volatility remains a direct restraint on the cationic starches market, as maize, potato, and tapioca starches depend on agricultural supply chains influenced by weather, energy prices, and currency movements. Maize presents the highest exposure, as the leading source segment depends on global corn balances and faces competing demand from food, feed, and fuel applications. When grain costs rise rapidly, participants in the cationic starches market cannot pass on these increases evenly, as paper and textile applications often remain highly price sensitive. Large integrated suppliers can reduce part of this pressure through broader sourcing networks and trading capabilities, while smaller specialty producers typically have fewer hedging options and limited flexibility to protect margins. This dynamic creates an uneven competitive effect in the cationic starches market, where scale helps companies absorb volatility, while regional players face sharper cost pressures. It also slows investment in differentiation, as producers facing raw material pressure tend to prioritize throughput and contract retention over new product development.

Strict food safety regulations governing modified starch ingredients

Food additive oversight remains a key restraint on the cationic starches market, particularly in Europe and North America, where documentation standards are stringent and product changes can take time. Under the current EU food additive framework, category-specific rules, labeling requirements, and the need for clear technical justification continue to shape the use of modified starch[3]Source: European Commission, “COMMISSION REGULATION (EU) 2025/2058”, eur-lex.europa.eu. Producers serving food applications in the cationic starches market must manage product performance, dossier quality, traceability, and reformulation risk. These requirements place a greater burden on smaller suppliers that lack dedicated regulatory teams or extensive customer support resources. As a result, compliance requirements can strengthen the scale advantages of multinational starch suppliers, even when their products are not the lowest-cost options. While these factors do not stop growth in the cationic starches market, they limit the number of suppliers that can compete effectively in regulated food applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Maize's Command Masks a Structural Shift Toward Specialty Origins

Maize dominated the cationic starches market by source, accounting for 70.26% of the total market share in 2025. Its leadership is primarily attributed to the abundant global availability of maize, well-established cultivation, and its cost-effective processing into starch. Maize-based cationic starch offers consistent quality, high purity, and excellent cationization efficiency, making it the preferred raw material for paper manufacturing, wastewater treatment, textiles, and adhesives. The extensive industrial infrastructure supporting corn wet milling further strengthens its commercial viability and ensures stable supply across major consuming regions. In addition, continuous improvements in starch modification technologies have enhanced the functional performance of maize-derived cationic starch, reinforcing its adoption in diverse industrial applications.

Potato is projected to be the fastest-growing source segment, expanding at a CAGR of 5.46% through 2031. The increasing demand for specialty starches with superior viscosity, binding, and film-forming properties is driving the adoption of potato-derived cationic starch across multiple industries. Potato starch possesses naturally large granules and a higher amylopectin content, enabling improved water retention and enhanced functionality in paper coating, textiles, and specialty industrial formulations. Growing interest in sustainable and renewable raw materials is also encouraging manufacturers to diversify beyond conventional maize-based starches, particularly in regions with strong potato production.

By Application: Food and Beverage Concentration Conceals Pharmaceutical Upside

Food and beverage emerged as the largest application segment in the cationic starches market, accounting for 48.12% of the total market share in 2025. The segment's dominance is driven by the extensive use of cationic starches as stabilizers, thickeners, binders, and texture-enhancing agents in a wide range of processed food and beverage products. Manufacturers increasingly rely on these modified starches to improve product consistency, moisture retention, shelf life, and processing efficiency while meeting evolving consumer quality expectations. Rising consumption of convenience foods, ready-to-eat meals, dairy products, bakery items, and beverages continues to support robust demand for functional starch ingredients worldwide.

Pharmaceuticals are projected to be the fastest-growing application segment, registering a CAGR of 5.25% through 2031. Growth is fueled by the increasing use of cationic starches as excipients, tablet binders, disintegrants, and controlled drug delivery materials in pharmaceutical formulations. The expansion of the global pharmaceutical industry, coupled with rising investments in innovative drug development and advanced dosage technologies, is creating greater demand for high-performance starch derivatives. Cationic starches are valued for their biocompatibility, biodegradability, and ability to enhance the stability and controlled release of active pharmaceutical ingredients.

Geography Analysis

North America held 34.11% of the cationic starches market share in 2025, making it the largest regional base in the current structure of demand. The region benefits from a strong paper and packaging network, broad corn availability, and integrated starch supply chains that support both standard and specialty grades. The United States remains central to the cationic starches market, as it combines large paper products consumption with a major domestic feedstock base and strong industrial processing capacity. Canada supports the market through pulp and tissue manufacturing, while Mexico offers incremental growth linked to industrial expansion and supply chain relocation. Traceability and sustainable sourcing expectations from large consumer goods companies also help North American suppliers defend higher-value positions in the cationic starches market.

Europe remains important to the cationic starches market due to its concentrated base of specialty suppliers with strong positions in potato-based starch and regulated end uses. Demand in the region depends less on volume expansion and more on compliance, sustainability expectations, and the ability to meet precise application requirements in food and pharmaceuticals. Current EU food additive rules maintain strict formulation discipline, giving established suppliers an advantage when customers need technical support and dependable documentation. Germany, France, and the United Kingdom remain key demand centers, while Eastern Europe offers a more active outlook for capacity additions and industrial growth than some mature Western European markets.

Asia-Pacific is the fastest-growing region in the cationic starches market, with a projected CAGR of 5.78% through 2031. China remains the largest demand anchor in the region, supported by its broad containerboard, tissue, and food processing base. India is emerging as the fastest-accelerating national opportunity, driven by paper capacity additions, a large textile export platform, and growing pharmaceutical manufacturing. Southeast Asia also remains important, as Vietnam, Bangladesh, and Thailand continue to add textile and industrial starch demand amid regional manufacturing shifts. South America and the Middle East and Africa still account for smaller shares of the cationic starches market, but both regions are building a stronger base through packaging growth, food diversification, and industrial development. As a result, the cationic starches market is steadily shifting eastward, although North America still holds the largest current share.

Competitive Landscape

The cationic starches market is moderately consolidated globally. However, it remains fragmented when commodity paper, textile, and regional supply relationships are considered. Cargill, Ingredion, Roquette, Tate & Lyle, and Avebe lead the cationic starches market in areas where application support, modification know-how, and control over upstream sourcing are critical. These companies hold the strongest positions in pharmaceutical excipients, premium food grades, and more technical paper applications, where product consistency often outweighs the lowest price. At the same time, regional suppliers in Asia continue to compete effectively in commodity grades, preventing the cationic starches market from becoming highly concentrated.

Capital investment remains one of the clearest indicators of how large companies are defending their positions in the cationic starches market. Ingredion’s planned USD 50 million investment in Cedar Rapids in February 2025 targets specialty industrial starch capacity for packaging and papermaking customers, indicating a direct response to end-use demand rather than a general capacity expansion. Cargill’s Baupte modernization also shows how operational upgrades tied to efficiency and emissions can strengthen long-term competitiveness in the cationic starches market without relying solely on pricing strategies.

Technology differentiation is becoming a stronger dividing line within the cationic starches market. Tate & Lyle’s FY2026 update indicates continued innovation spending and the rollout of a proprietary generative AI tool for technical teams, highlighting faster formulation response as a competitive asset. Smaller European specialists, such as Emsland-Stärke, Novidon, and similar players, remain relevant because traceability, non-GMO positioning, and regulatory confidence continue to matter in pharmaceutical and clean-label niches. As a result, the cationic starches market rewards both scale and specialization, depending on the application and customer set.

Cationic Starches Industry Leaders

Cargill, Incorporated

Tate & Lyle PLC

Ingredion Incorporated

Roquette Frères S.A.

Archer Daniels Midland Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Roquette inaugurated a starch and polyol pilot center at its Lianyungang facility in China. The 1,000-square-meter center integrates physicochemical analysis, lab-scale research, and pilot-scale transformation into a single platform. This setup enables faster co-development with Chinese food, beverage, dairy, and specialty nutrition customers and shortens the time to market for modified starch applications.

- February 2026: Tate & Lyle rolled out a proprietary generative AI tool, trained on its technical and scientific libraries, to its applications, solutions, and technical services teams. The tool enables faster formulation responses for starch-based customer solutions and complements the company’s GBP 86 million innovation investment in FY2026.

- February 2025: Ingredion Incorporated announced a USD 50 million investment in its Cedar Rapids, Iowa, facility to modernize and expand specialty industrial starch production for packaging and papermaking customers seeking functional strength, biodegradability, and recyclability performance.

Global Cationic Starches Market Report Scope

Cationic starch is a chemically modified starch in which positively charged (cationic) functional groups are introduced into the starch molecule. The cationic starches market is segmented into source, application and geography. Based on the source, the market is segmented into maize , wheat , potato , tapioca and others. Based on application, the market is segmented into food and beverage, pharmaceutial, personal care and cosmetics, textile, animal feed, paper and corrugating and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle-East and Africa. For each segment, the market sizing and forecasting have been done in value terms (USD).

| Maize |

| Wheat |

| Potato |

| Tapioca |

| Others |

| Food and Beverage |

| Pharmaceutials |

| Personal Care and Cosmetics |

| Textile |

| Animal Feed |

| Paper and Corrugating |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Source | Maize | |

| Wheat | ||

| Potato | ||

| Tapioca | ||

| Others | ||

| By Application | Food and Beverage | |

| Pharmaceutials | ||

| Personal Care and Cosmetics | ||

| Textile | ||

| Animal Feed | ||

| Paper and Corrugating | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the expected size of the cationic starches market by 2031?

The cationic starches market is forecast to reach USD 2.33 billion by 2031, rising from USD 1.89 billion in 2026 at a 4.27% CAGR.

Which application leads current demand for cationic starches?

Food and beverage led demand with 48.12% of total value in 2025, supported by thickening, stabilization, and texture needs across processed foods.

Which source segment is growing the fastest?

Potato is the fastest growing source, with a projected 5.46% CAGR through 2031, supported by premium pharmaceutical excipient demand.

Why does the paper sector remain important for suppliers?

Paper and paperboard mills use cationic starch to improve retention, drainage, and strength, and higher recycled fiber content often increases dosage needs per tonne.

Which region offers the strongest growth outlook through 2031?

Asia-Pacific has the fastest regional growth outlook with a 5.8% CAGR, supported by paper capacity additions, textile demand, and pharmaceutical manufacturing growth.

Page last updated on: