Casting And Splinting Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

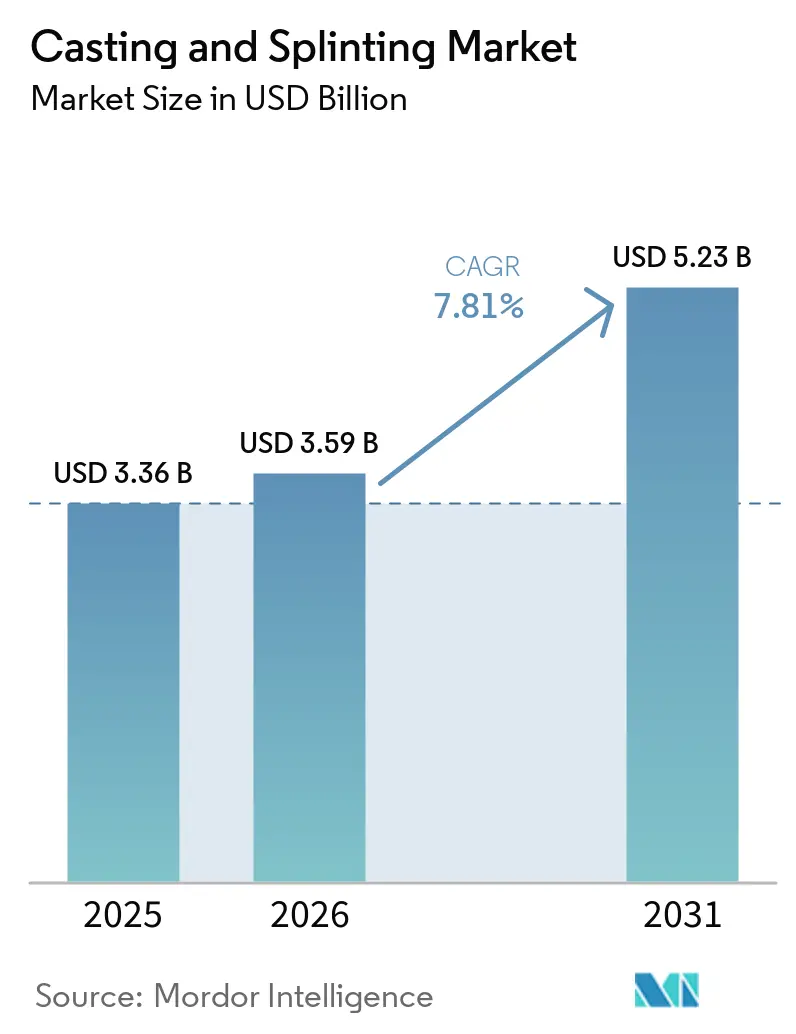

| Market Size (2026) | USD 3.59 Billion |

| Market Size (2031) | USD 5.23 Billion |

| Growth Rate (2026 - 2031) | 7.81% CAGR |

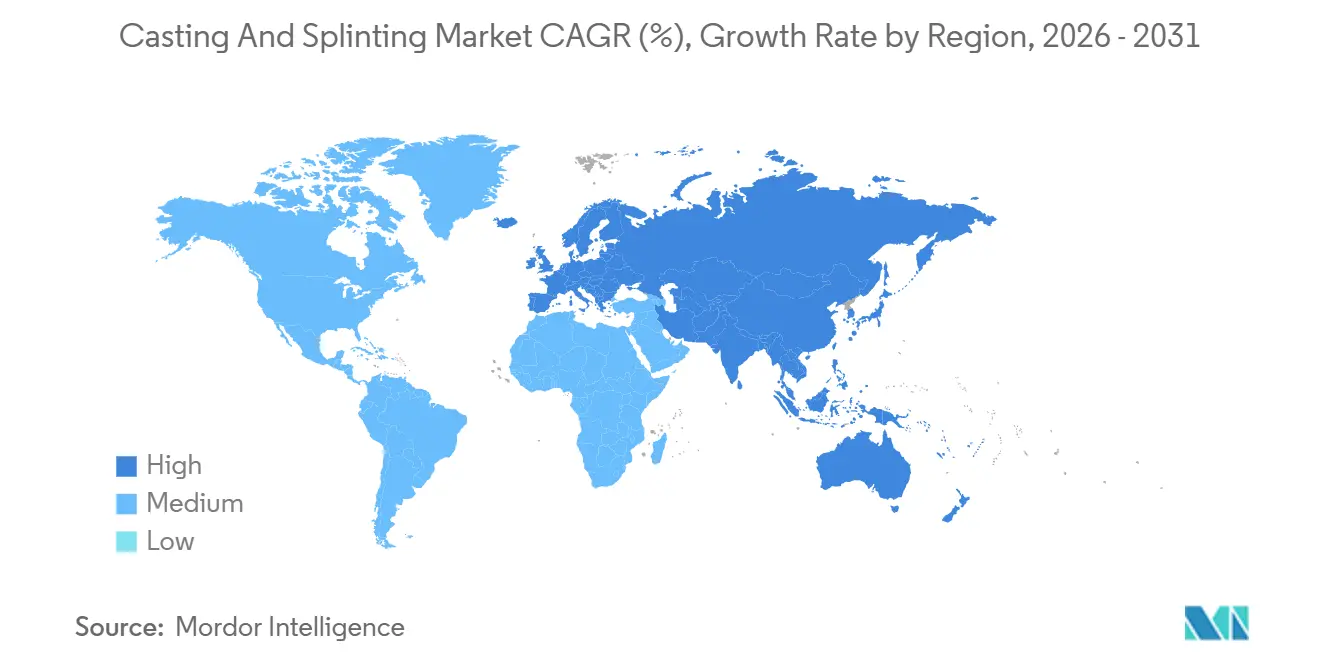

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Casting And Splinting Market Analysis by Mordor Intelligence

The Casting And Splinting Market size is projected to be USD 3.36 billion in 2025, USD 3.59 billion in 2026, and reach USD 5.23 billion by 2031, growing at a CAGR of 7.81% from 2026 to 2031.

Demand momentum strengthens as aging-related fragility fractures, outpatient migration, and material innovation drive consistent use of immobilization solutions across acute, post-operative, and rehabilitation settings. In 2026, providers prioritize lightweight synthetics and thermoformable systems that streamline same-day discharge and support functional treatment protocols. Advances in 3D scanning, additively manufactured splints, and water-friendly liners create premium-priced SKUs that offset input-cost volatility and pricing pressure in commodity SKUs. Vendors consolidate workflow value with digital ordering portals and inventory automation that reduce stock-outs and improve charge capture. Regional trajectories diverge as North America benefits from outpatient reimbursement alignment while Asia-Pacific advances faster on the back of urban trauma volumes and broader access to fracture stabilization.

Key Report Takeaways

- By geography, North America led with 45.64% share in 2025, while Asia-Pacific is projected to grow at an 8.31% CAGR over 2026-2031.

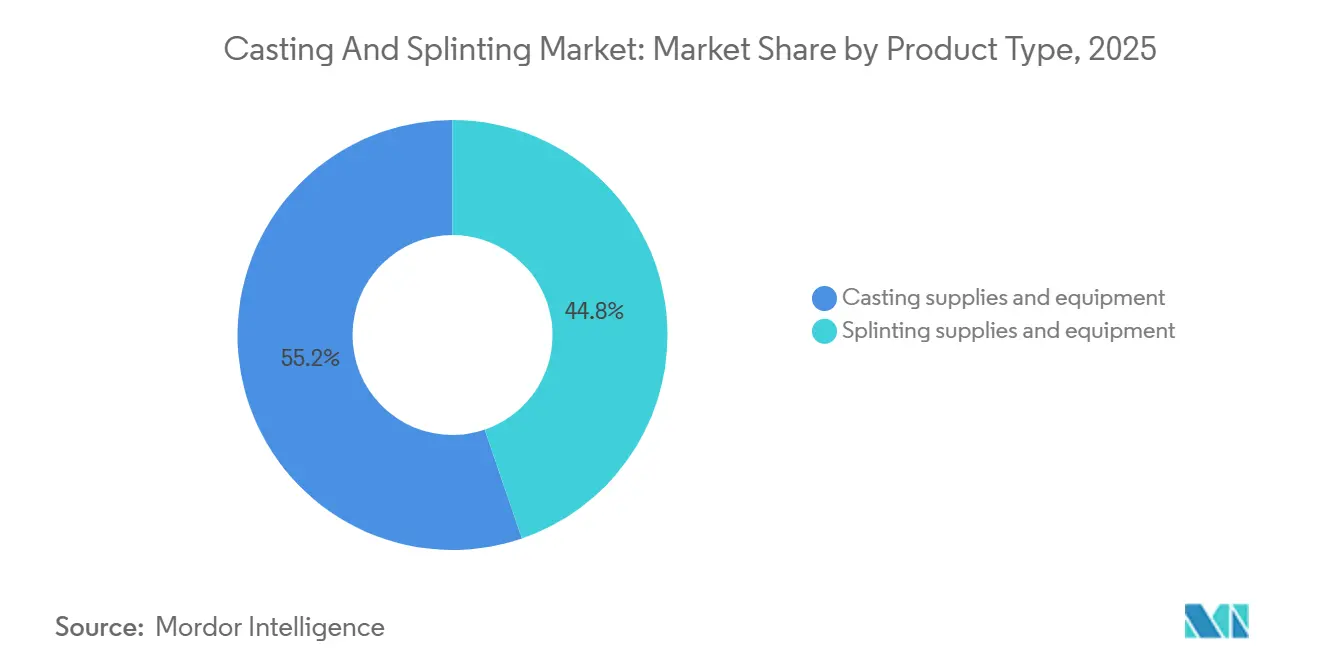

- By product type, casting supplies and equipment held 55.23% share in 2025, while splinting supplies and equipment is projected to advance at an 8.56% CAGR through 2031.

- By material, fiberglass or synthetic polyurethane accounted for 45.15% share in 2025, while thermoplastic is forecast to grow at an 8.65% CAGR during 2026-2031.

- By application, fracture management captured 58.56% revenue in 2025, while sports injuries is projected to record the fastest growth at a 9.19% CAGR to 2031.

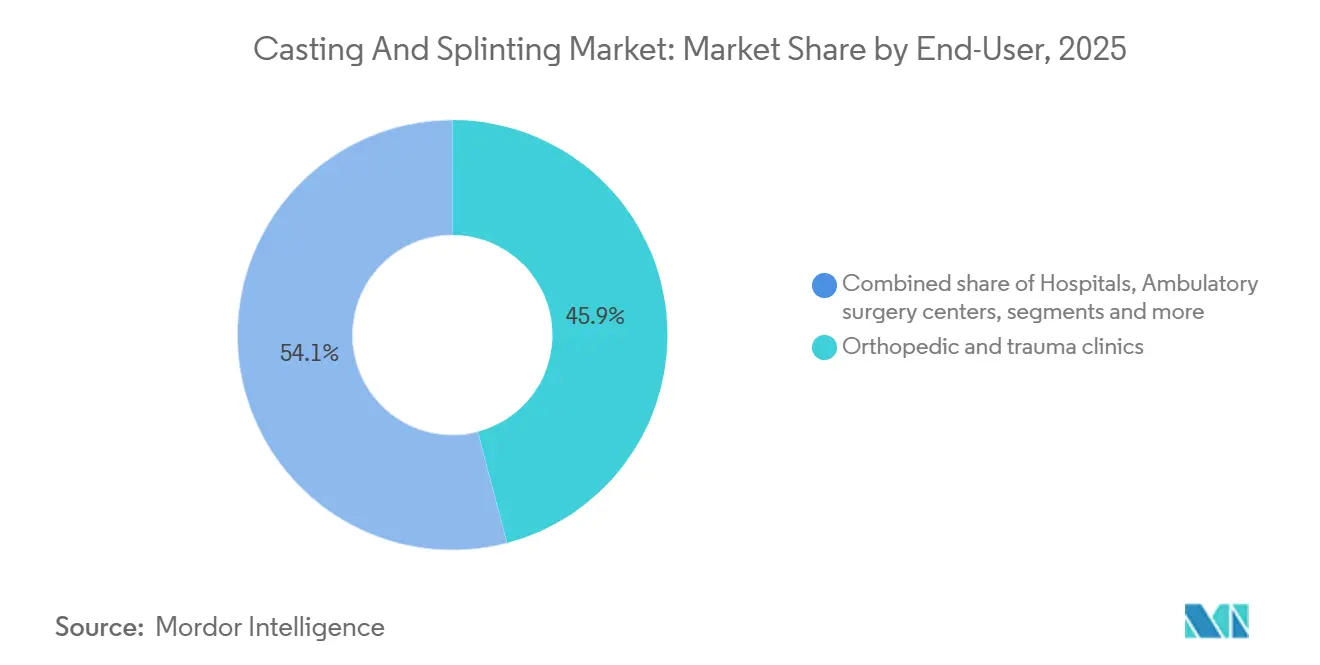

- By end-user, orthopedic and trauma clinics represented 45.90% of 2025 sales, and this setting is expected to post an 8.61% CAGR over 2026-2031.

- By distribution channel, direct-to-provider accounted for 55.64% share in 2025, while e-commerce is expected to achieve an 8.89% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Casting And Splinting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging-related fragility fractures sustaining demand | +2.1% | Global, with early gains in North America, Western Europe, and Japan; accelerating in China as population ages | Long term (≥ 4 years) |

| Rising trauma and road injuries elevating fracture burden | +1.5% | APAC core (India, Southeast Asia), spill-over to MEA and South America | Medium term (2-4 years) |

| Shift to outpatient/ASC and urgent care workflows | +1.8% | North America & EU, with gradual adoption in APAC urban centers | Medium term (2-4 years) |

| Material innovation toward lightweight fiberglass and thermoformable systems | +1.2% | Global, led by North America and Western Europe in commercialization | Short term (≤ 2 years) |

| Digital/3D scanning and additive manufacturing enable custom immobilization | +0.9% | North America, Western Europe; pilot adoption in APAC metro hospitals | Medium term (2-4 years) |

| Water-friendly, hygiene-focused liners improving adherence | +0.8% | Global, with premium uptake in North America, EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aging-Related Fragility Fractures Sustaining Demand

Health systems are responding to sustained increases in fragility fractures by expanding non-operative pathways that emphasize conservative care for stable injuries in older adults. Wrist and forearm fractures in seniors often transition to casting and splinting when surgery is not indicated, reinforcing recurring demand for immobilization devices in outpatient and rehabilitation settings. Post-hip fracture care creates downstream need for protective orthoses and boots during recovery, extending immobilization use beyond the acute event. European payers have moved to standardize fast-track fracture clinics, a model that is diffusing to major Asian urban centers where geriatric cohorts are expanding. Heightened attention to prevention and care pathways for fragility events underscores continuous utilization of casting and splinting products within integrated musculoskeletal care. Ongoing WHO guidance on fragility fracture prevention and management continues to shape service models and resource allocation in orthopedic care[1]World Health Organization, “Fragility fractures,” WHO, who.int.

Shift to Outpatient, ASC, and Urgent Care Workflows

The United States counted 12,294 ambulatory surgery centers by early 2025 with orthopedic services embedded across more than one third of sites, and outpatient settings handled the large majority of surgical procedures by that time. Payment policy alignment supports this shift as ASCs gain steady reimbursement updates that favor same-day discharge workflows and streamlined supply chains. Providers increasingly adopt lightweight, low-exotherm synthetic casting systems that cure quickly and support rapid ambulation within narrow observation windows. Inventory strategies favor prepackaged kits and dedicated SKUs that simplify ordering, storage, and coding, which raises mix toward higher-margin products. Workflow digitization further accelerates adoption, as platforms like MotionMD help tie specific immobilization SKUs to appropriate billing codes and documentation within the episode of care.

Digital/3D Scanning and Additive Manufacturing Enable Custom Immobilization

Point-of-care 3D scanning using smartphone depth cameras and handheld scanners now generates accurate limb geometries within minutes that design tools convert into printable files for custom orthoses. Production runs on polymer printers yield lightweight, ventilated constructs that reduce skin complications and improve comfort compared to traditional full-circumference casts. Clinical evidence in pediatrics has shown improved alignment, lower pain scores, and higher functional outcomes for 3D-printed splints compared with plaster controls in recent trials. These devices also enable removable, adjustable care pathways that align with early mobilization protocols and patient hygiene preferences. Premium pricing for personalized orthoses is gaining payer acceptance as reductions in cast changes and complication-related revisits can offset higher unit costs when considering total episode economics.

Material Innovation Toward Lightweight Fiberglass and Thermoformable Systems

Material science is improving mechanical properties at lower weights, supporting thinner-gauge orthoses that maintain stiffness and resist impact in daily use. Long-fiber thermoplastics are advancing with antimicrobial additives and flexural performance that enables substitution for heavier reinforcements in select applications. European molders piloted bio-based thermoplastics for non-load-bearing splints in 2025, aligning with hospital sustainability goals embedded in public procurement criteria. Polyester-based casting tapes with low-tack resins help reduce dust during cast removal, improving the working environment for clinical staff. Collectively, these shifts favor materials that support speed, hygiene, and comfort while maintaining clinical effectiveness across immobilization protocols.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory exposure to diisocyanates in polyurethanes | -0.9% | EU core (Germany, France, Italy); ripple effects in UK, EFTA nations | Short term (≤ 2 years) |

| Complications/skin issues push substitutions to functional bracing | -0.6% | Global, with higher incidence in humid climates (Southeast Asia, Gulf states) | Medium term (2-4 years) |

| Pricing pressure and limited differentiation in commodity SKUs | -0.7% | Global, most acute in price-sensitive public tenders (India, Brazil, Eastern Europe) | Long term (≥ 4 years) |

| Polymer and logistics volatility impacting input costs | -1.3% | Global supply chains; acute in import-dependent markets (Middle East, sub-Saharan Africa) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Regulatory Exposure to Diisocyanates in Polyurethanes

New EU exposure limits for monomeric diisocyanates in polyurethane processing introduce tighter controls on workplace air quality and handling procedures, prompting manufacturing reformulation and additional training obligations. Facilities must adapt ventilation, implement continuous monitoring, and refresh worker education on defined intervals as the limits phase into full enforcement. These requirements add costs that are harder to pass through for low-ASP, high-volume consumables, creating margin pressure on standard casting tapes. European suppliers are accelerating development of diisocyanate-free alternatives and moving to water-based dispersions, while advancing MDR certifications to preserve access in regulated tenders. Communication from industry publications has highlighted the harmonized exposure thresholds and timelines across the EU that are now shaping procurement and product design decisions.

Polymer and Logistics Volatility Impacting Input Costs

Petrochemical volatility since 2025 has raised spot prices for core feedstocks, with periodic surges in resin and glass-fiber costs affecting landed costs for casting tapes and splinting systems. Government interventions in some countries, including targeted subsidies to stabilize naphtha inputs, have helped manufacturers temper cost pass-through in priority sectors. Shifts in global tariffs on medical devices have required recalibration of supply routes and sourcing mixes to maintain service levels while managing cash-conversion cycles and inventory risk in long-haul shipping lanes. Glass-fiber price upticks in both Europe and Asia near the end of 2025 added to the bill of materials for fiberglass-based consumables. To protect profitability under volatility, top suppliers are using indexed contracts tied to published polymer and energy benchmarks that enable periodic price adjustments within defined bands while sharing risk with healthcare providers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Removable Splints Gain as Functional Protocols Diffuse

Casting supplies and equipment held 55.23% of revenue in 2025 as clinicians adopt functional treatment where stability permits. Hospitals maintain steady utilization of rigid casts for displaced fractures and immediate post-operative stabilization, which anchors the installed base of casting tools and accessories. Splinting gains traction for ambulatory care pathways that require adjustability, hygiene, and faster return to light activity. Clinics also emphasize ergonomic cast cutters and dust extraction accessories to reduce particulate exposure during removal. The casting and splinting market continues to shift mix toward prepackaged splinting kits and color-coded materials that standardize workflows across high-volume sites.

Splinting supplies and equipment are projected to grow at 8.56% CAGR during 2026-2031. Prefabricated fiberglass and thermoplastic splints capture a leading share within splinting due to ease of application and lower setup times in outpatient and urgent care clinics. Night splints for common repetitive strain conditions benefit from coverage policies that support home use and remote guidance. Malleable aluminum foam splints retain a role in emergency medical kits where simplicity and reusability matter. The casting and splinting market aligns product design with coding and documentation tools that help providers secure appropriate reimbursement for each immobilization episode. As functional bracing philosophies diffuse, the product mix within the casting and splinting market favors removable systems that maintain protection while enabling monitored motion.

By Material: Thermoplastics Ascend on Clinic Remoldability

Fiberglass or synthetic polyurethane accounted for 45.15% of revenue in 2025. A January 2024 article in BMC Musculoskeletal Disorders highlighted a groundbreaking biobased polyester cast. This innovative cast not only matches the stability of traditional fiberglass casts but also enhances patient satisfaction, all while being more eco-friendly and safer. In the study, 100 patients were randomly assigned via sealed envelopes to one of two groups: the biobased polyester cast group (using MEDlite Thermo Casting Tape from Taipei Smart Materials, Taipei, Taiwan) or the fiberglass cast group (utilizing Scotchcast from 3M Health Care, Maplewood, Minnesota, U.S.). Each group comprised 50 patients. Traditional synthetic casts often contain harmful components such as isocyanates, which can lead to skin issues, including itching, redness, and dryness. This novel biobased cast is crafted from a newly developed, nontoxic, and biodegradable copolymer. This copolymer, named poly(ethylene sebacate-co-ethylene adipate) (PESA), is synthesized from the green resource sebacic acid and is copolymerized with ethylene glycol, trimesic acid, aminocaproic acid, and adipic acid. Notably, animal studies have indicated that skin exposure to such chemical allergens can trigger asthmatic responses.

Low-temperature thermoplastics are the fastest-growing material at an 8.65% CAGR for 2026-2031 due to chairside remoldability. Thermoplastics soften in warm-water or controlled-heat setups and allow clinicians to fine-tune fit without complete reapplication. In regions with sustainability mandates, qualified bio-based thermoplastic formulations have begun to appear in non-load-bearing devices, supported by molder certifications and hospital procurement criteria. Polyester-based tapes with low-tack resins emphasize lower dust during saw removal and improved radiolucency, which is valued in pediatric follow-up imaging. The casting and splinting market shows ongoing preference for materials that reduce skin complications, odor, and maceration, while maintaining adequate rigidity in daily wear.

Plaster of Paris remains relevant for budget-constrained settings where acquisition cost and supply simplicity guide product selection. Aluminum splints serve specialized use cases that benefit from reusability and quick field application. Thermoplastic adoption gains momentum in markets where regulation around diisocyanates encourages alternatives and where clinics invest in small-form heating equipment. The casting and splinting market accommodates both incumbent fiberglass tapes and expanding thermoplastic lines, as buyers weigh per-roll cost against adjustability, patient comfort, and clinic throughput. As suppliers roll out next-generation composites and antimicrobial additives, material choice continues to diversify, which sustains competitive differentiation[2]XeniaEditor Marketing, “HM UPGRADE | High-Performance Thermoplastic Composites,” Xenia Materials, xeniamaterials.com.

By Application: Sports Injuries Outpace Base Fracture Growth

Fracture management captured 58.56% of 2025 revenue, with larger lower-extremity casts supporting higher per-case revenue due to longer immobilization durations. Acute sprains and strains hold a meaningful share, with ankle injuries often managed via functional bracing to speed recovery and preserve mobility for daily activities. Sports injuries are projected to post the fastest growth at a 9.19% CAGR for 2026-2031 as organized sport participation and return-to-play protocols reinforce demand for protective and adjustable supports. U.S. emergency department data over a recent decade shows a sizeable burden of sports-related upper-extremity cases, which aligns with the expanding need for removable splints and protective gear in rehabilitation. The casting and splinting market supports this shift with brace designs that maintain alignment while permitting stepwise increases in controlled motion.

Post-operative immobilization follows steady growth trends as minimally invasive procedures advance and outpatient care pathways shorten inpatient stays. Pediatric populations benefit from options that improve comfort and adherence, including lighter materials and hygienic liners that enable bathing. In markets with formal athletic programs, hinged and adjustable designs help bridge immobilization with progressive rehabilitation goals. The casting and splinting market continues to blend rigid stabilization for acute phases with transition devices that enable early function under clinician guidance. Evidence that links fewer skin issues and improved functional scores to advanced designs will likely deepen adoption where payers reward outcomes.

By End-User: Orthopedic Clinics Capitalize on Integrated Care Models

Orthopedic and trauma clinics represented 45.90% of 2025 sales and are projected to grow at 8.61% CAGR through 2031 on the strength of integrated on-site imaging, casting suites, and fast specialist access. Hospitals are working through the effects of outpatient migration that shifts many lower-acuity fracture cases into clinic, urgent care, or ASC settings. Ambulatory surgery centers continue to expand procedure volumes, which supports demand for post-procedure splinting kits that enable rapid turnover and infection-control compliance. Rehabilitation and therapy clinics apply removable supports to reinforce early mobilization under supervised care plans. The casting and splinting market adapts product form factors for staff efficiency, patient comfort, and consistent charge capture across diverse ambulatory sites.

In home-care settings, caregiver-friendly designs with easy closures and instructions align with remote follow-up and app-based check-ins. Clinics adopt digital inventory tools and training portals from suppliers to standardize application techniques and reduce waste. EU MDR guidance on reprocessing of single-use products nudges select pilot programs toward reusable thermoplastic splints where validation is feasible, though broader adoption remains limited due to liability and sterilization constraints. As end-users pursue throughput and adherence, the casting and splinting market emphasizes devices that simplify fit and follow-up without sacrificing protective function. Vendor education and workflow consulting complement offerings and help sustain product differentiation.

By Distribution Channel: E-Commerce Disrupts Legacy Distributor Markups

Direct-to-provider channels accounted for 55.64% in 2025, reflecting large hospitals and orthopedic groups that negotiate volume contracts and use vendor-managed inventory programs. These sites often deploy RFID-enabled systems and analytics to automate replenishment and align SKUs with procedure coding and reimbursement. Distributor networks continue to serve regions where direct coverage is uneconomical and where local regulatory navigation is valuable for in-country registrations. E-commerce is the fastest-growing route with an 8.89% CAGR expected for 2026-2031 due to 24/7 ordering, transparent comparisons, and integrated invoicing. The casting and splinting market also benefits from proprietary B2B portals that bundle sizing tools, clinical videos, and subscription discounts to improve retention.

Hybrid channel models let suppliers maintain scale in developed markets while relying on local partners in countries that require import licensing and specialized customs clearance. Companies with broad international footprints illustrate this approach by balancing direct sales and channel partners across continents. As online platforms experiment with white-glove regulatory services, traditional distributor value propositions face pressure where digital workflow support can close historical gaps. The casting and splinting market continues to spread ordering volume across direct, dealer, and online routes to optimize service levels by geography and account type. Channel innovation remains a lever for improving margins and smoothing supply variability in high-turnover environments.

Geography Analysis

North America held 45.64% of revenue in 2025 on the strength of outpatient alignment, broad ASC penetration, and fast adoption of premium immobilization technologies that secure coverage under value-based care. The region’s outpatient infrastructure rests on 12,294 ASCs in the United States by 2025 and a high share of procedures performed outside inpatient settings, which channel fracture care toward same-day stabilization options. Providers deploy custom 3D-printed splints and water-friendly liner systems to improve comfort and adherence in pediatric and adult cases. Clinic and ASC focus on speed supports uptake of low-exotherm synthetics that set quickly, enabling discharge within short observation windows. Regional consolidation among hospitals has shifted some trauma volumes while intensifying emphasis on inventory automation and coding accuracy to defend margins. Changes in professional sport injury profiles during 2025 illustrate how safety policy can influence case mix, with some lower-extremity injuries reduced under updated rules. The casting and splinting market in North America continues to emphasize supply reliability, patient comfort, and clean documentation across ambulatory pathways.

Asia-Pacific is projected to grow at an 8.31% CAGR over 2026-2031 as urbanization raises trauma incidence and as universal coverage programs expand access to stabilization beyond tertiary hubs. China’s aging cohort accelerates fragility volumes, while India and Southeast Asia advance district-level access to fracture care through broader funding and referral networks. Pilots of pediatric 3D-printed splints in leading Japanese centers have reported favorable functional outcomes, reinforcing premium-tier interest where clinical acceptance aligns with customization benefits. Government support in select markets has aimed to stabilize petrochemical inputs and ensure consistent availability of resins necessary for casting tapes. In lower-resource environments across the broader region, plaster maintains a role due to cost and supply continuity, while fiberglass adoption rises with improvements in distribution. The casting and splinting market balances product portfolios across APAC to reflect both premium customization and volume-led consumables.

Europe faces dual pressures from regulatory changes and trade frictions that influence material selection and export dynamics for suppliers. New EU diisocyanate exposure limits require investments in compliance, catalyze resin reformulations, and influence tender specifications that shape product choice for casting tapes. Import tariffs on medical devices in some export markets since 2025 have nudged suppliers to adjust logistics routes or rebalance production footprints to mitigate cost exposure. In France, reimbursement policies sustain use of removable splints for common ankle injuries encountered over a lifetime, maintaining steady demand for functional solutions. Spain and Italy continue to rely on public-tender formularies that reward lowest unit costs, which preserves a role for plaster alongside lighter synthetics. European suppliers emphasize MDR certifications and sustainability credentials as differentiators while extending digital portals to streamline ordering and training for hospitals and clinics. The casting and splinting market in Europe reflects a balance of compliance-driven product evolution and steady utilization in high-volume trauma and orthopedic pathways.

Competitive Landscape

The casting and splinting market remains moderately fragmented, with a group of global suppliers supported by a long tail of regional converters and private labels that serve local formularies and public tenders. Product portfolios span fiberglass casting tapes, removable thermoplastic systems, protective bracing, and accessories that support application, removal, and follow-up. Companies reinforce competitive positions through integration of coding and billing software that links SKU usage to reimbursement, enhancing provider economics and strengthening vendor selection criteria. Workflow training, stocking programs, and clinical education portals further differentiate vendor offerings. The casting and splinting market also rewards suppliers that pair consumables with digital portals and reliable logistics, as ordering convenience and product availability weigh heavily in ASC and clinic purchasing decisions.

Enovis reported USD 1.14 billion in Prevention & Recovery segment revenue in 2025 and continued to invest in margin expansion through higher-value bracing and integrated software support for charge capture in the U.S. and abroad. Essity launched the Actimove Manus Air wrist brace in 2025, targeting faster application and water-resistant performance, and recorded positive organic growth in its Medical Solutions division for the year. Lohmann & Rauscher secured MDR certifications across core portfolios and signaled a transition toward diisocyanate-free formulations to align with evolving EU regulatory expectations. The casting and splinting market continues to see supplier investments in product speed, hygiene, and adjustability, consistent with outpatient and home-care adoption patterns.

Customization and digitization form a clear innovation axis, with smartphone-based scanning, cloud-based design tools, and additive manufacturing workflows enabling patient-specific orthoses in select sites. Partners in the design-to-print chain have deployed scalable tools and factory-certified workflows to supply orthopedic networks with consistent quality. Material science advances in composites and thermoplastics provide the stiffness-to-weight gains and impact resistance needed for thinner-gauge devices that improve comfort and adherence. International suppliers with hybrid routes to market demonstrate how direct and distributor models can coexist as companies address regulatory filings and customs needs across diverse geographies. The casting and splinting market remains focused on consistent clinical outcomes, clean documentation, and supply dependability as purchasing groups evaluate vendor performance across the full episode of care.

Casting And Splinting Industry Leaders

Enovis (DJO/Exos/Aircast/ProCare),

Essity (Delta-Cast/Ortho-Glass)

Solventum (Scotchcast, post-3M spinoff)

Lohmann & Rauscher (Cellona/Cellacast)

Medline Industries

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Xenia Materials launched its HM Upgrade technology, integrating high-modulus carbon fibers into thermoplastic composites to achieve 15% increases in tensile modulus and flexural strength, plus up to 20% improvements in impact resistance, without increasing material density. Available across Xenia's XECARB family and compatible with polymer matrices including PA66, PA6, PP, PPA, and various polyamides, this innovation addresses demand for thinner-gauge orthoses that maintain structural rigidity, critical for improving patient comfort and adherence in long-duration immobilization protocols (6-12 weeks for distal radius fractures). The technology targets aerospace, motorsport, and demanding industrial applications, with medical orthotic segments positioned as a strategic growth adjacency.

- September 2025: Lohmann & Rauscher strengthened its European market presence through a strategic investment in the Portuguese medical device company ADA Group, having successfully completed the acquisition of 49% of ADA Group shares with strategic cooperation effective retroactively from January 1, 2025, following merger control approval. This move enhances L&R's delivery capability and geographic footprint across Southern Europe, positioning the company to capture growing demand for orthopedic consumables in Iberian and Mediterranean markets where public-hospital tenders increasingly favor EU-domiciled suppliers to mitigate currency and logistics risk.

Global Casting And Splinting Market Report Scope

As per the report’s scope, orthopedic professionals utilize casting and splinting techniques to stabilize fractures and support injured soft tissues, such as ligaments and tendons, by restricting movement. Casts provide a fully encircling rigid support, while splints offer a partially wrapping device, often employed initially to accommodate swelling. The casting and splinting market is segmented by product type, material, application, end-user, distributional channel, and geography.

By product type, the market is segmented into casting supplies & equipment and splinting supplies & equipment. Casting supplies & equipment is further segmented into casting tapes, plaster casts, cast cutters, and tools & accessories. Splinting supplies & equipment is segmented into prefabricated fiberglass/plaster, thermoplastic sheets/rolls, aluminum foam, and night splints. By material, the market is segmented into fiberglass/synthetic polyurethane, plaster of paris, thermoplastic (low-temp), polyester fabric, and aluminum (splints).

By application, the market is segmented into fracture management, acute sprains and strains, postoperative immobilization, pediatric fracture care, and sports injuries. Fracture management is further segmented into upper extremity and lower extremity. By end-user, the market is segmented into hospitals, orthopedic & trauma clinics, ambulatory surgery centers, rehab/ot/pt clinics, and home care. By distribution channel, the market is segmented into direct to providers, distributor/dealer, and e-commerce.By geography, the market is segmented as North America, Europe, Asia-Pacific, Middle-East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| Casting supplies & equipment | Casting tapes |

| Plaster casts | |

| Cast cutters | |

| Tools & accessories | |

| Splinting supplies & equipment | Prefabricated fiberglass/plaster |

| Thermoplastic sheets/rolls | |

| Aluminum foam | |

| Night splints |

| Fiberglass/synthetic polyurethane |

| Plaster of Paris |

| Thermoplastic (low-temp) |

| Polyester fabric |

| Aluminum (splints) |

| Fracture management | Upper extremity |

| Lower extremity | |

| Acute sprains and strains | |

| Postoperative immobilization | |

| Pediatric fracture care | |

| Sports injuries |

| Hospitals |

| Orthopedic & trauma clinics |

| Ambulatory surgery centers |

| Rehab/OT/PT clinics |

| Home care |

| Direct to providers |

| Distributor/Dealer |

| E-commerce |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Casting supplies & equipment | Casting tapes |

| Plaster casts | ||

| Cast cutters | ||

| Tools & accessories | ||

| Splinting supplies & equipment | Prefabricated fiberglass/plaster | |

| Thermoplastic sheets/rolls | ||

| Aluminum foam | ||

| Night splints | ||

| By Material | Fiberglass/synthetic polyurethane | |

| Plaster of Paris | ||

| Thermoplastic (low-temp) | ||

| Polyester fabric | ||

| Aluminum (splints) | ||

| By Application | Fracture management | Upper extremity |

| Lower extremity | ||

| Acute sprains and strains | ||

| Postoperative immobilization | ||

| Pediatric fracture care | ||

| Sports injuries | ||

| By End-User | Hospitals | |

| Orthopedic & trauma clinics | ||

| Ambulatory surgery centers | ||

| Rehab/OT/PT clinics | ||

| Home care | ||

| By Distribution Channel | Direct to providers | |

| Distributor/Dealer | ||

| E-commerce | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the casting and splinting market’s current size and growth outlook?

The casting and splinting market size is USD 3.59 billion in 2026 and is projected to reach USD 5.23 billion by 2031 at a 7.81% CAGR.

Which region leads and which grows fastest in casting and splinting?

North America led with 45.64% share in 2025, while Asia-Pacific is projected to grow at an 8.31% CAGR over 2026-2031.

Which product segments are leading and expanding in casting and splinting?

Casting supplies and equipment led with 55.23% share in 2025, while splinting supplies and equipment is projected to post an 8.56% CAGR through 2031.

How are materials evolving in casting and splinting?

Fiberglass or synthetic polyurethane held 45.15% share in 2025, while low-temperature thermoplastics is the fastest-growing material at an 8.65% CAGR due to remoldability and workflow fit.

What end-users and channels are shaping demand in casting and splinting?

Orthopedic and trauma clinics accounted for 45.90% of 2025 sales and are projected to grow at 8.61% CAGR, while e-commerce is the fastest-growing channel at 8.89% CAGR.

What innovations are changing patient and provider experience in casting and splinting?

Smartphone-based 3D scanning, additively manufactured custom splints, and water-friendly liners are improving comfort, adherence, and discharge speed, with clinical trials reporting better alignment and functional outcomes for 3D-printed solutions.

Page last updated on: