Cardiopulmonary Exercise Testing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.63 Billion |

| Market Size (2031) | USD 2.71 Billion |

| Growth Rate (2026 - 2031) | 10.74% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cardiopulmonary Exercise Testing Market Analysis by Mordor Intelligence

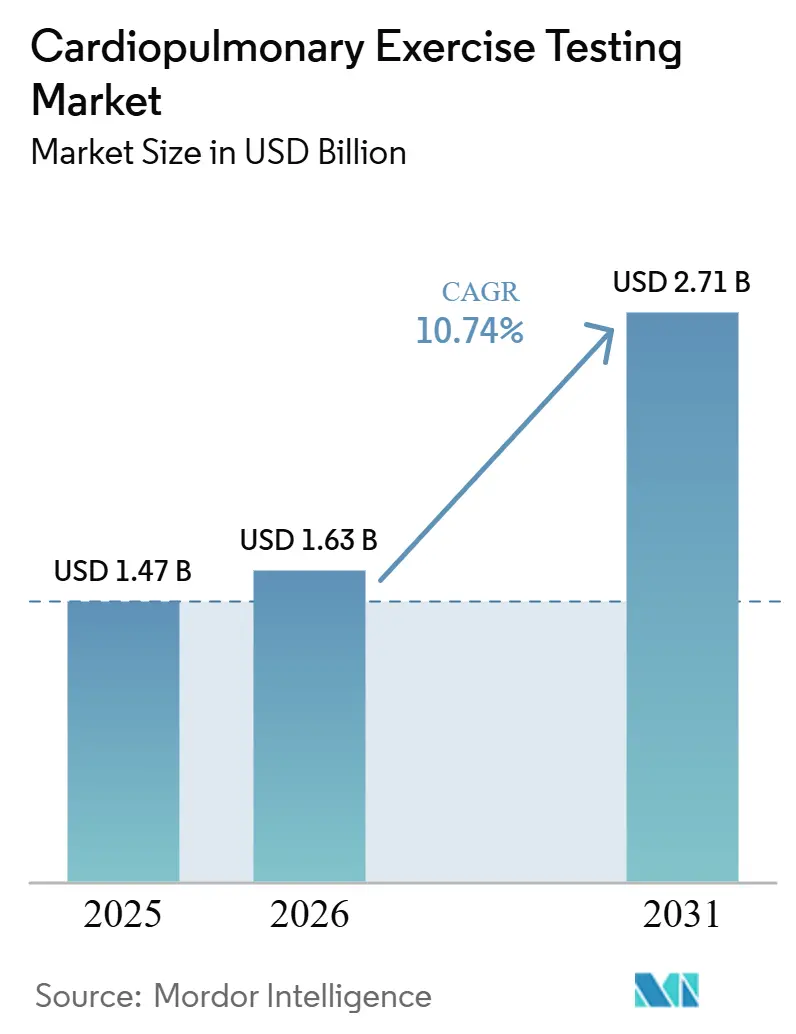

The Cardiopulmonary Exercise Testing Market size was valued at USD 1.47 billion in 2025 and is estimated to grow from USD 1.63 billion in 2026 to reach USD 2.71 billion by 2031, at a CAGR of 10.74% during the forecast period (2026-2031).

The cardiopulmonary exercise testing market is benefiting from a larger patient base that needs structured functional assessment, as cardiovascular diseases caused 19.2 million deaths in 2023 and accounted for 1 in 3 global deaths, which keeps pressure on health systems to use objective evaluation tools more often. The cardiopulmonary exercise testing market is also gaining support from formal care pathways because peak VO₂ and ventilatory efficiency measures are now used more directly in pre-operative assessment, rehabilitation follow-up, and pulmonary hypertension monitoring, which broadens demand beyond one-time diagnosis. Another support for the cardiopulmonary exercise testing market comes from software-led interpretation, as automated threshold detection and structured reporting help facilities use CPET without depending only on a small pool of specialists. Competitive activity in the cardiopulmonary exercise testing market is moving toward integrated workflows, compact device formats, and modular platforms that allow hospitals and specialist clinics to match testing complexity with patient volume and available staff. The cardiopulmonary exercise testing market also has room to expand in outpatient and community settings, but the pace of adoption still depends on training depth, reimbursement clarity, and the ability of providers to absorb equipment and service costs over time.

Key Report Takeaways

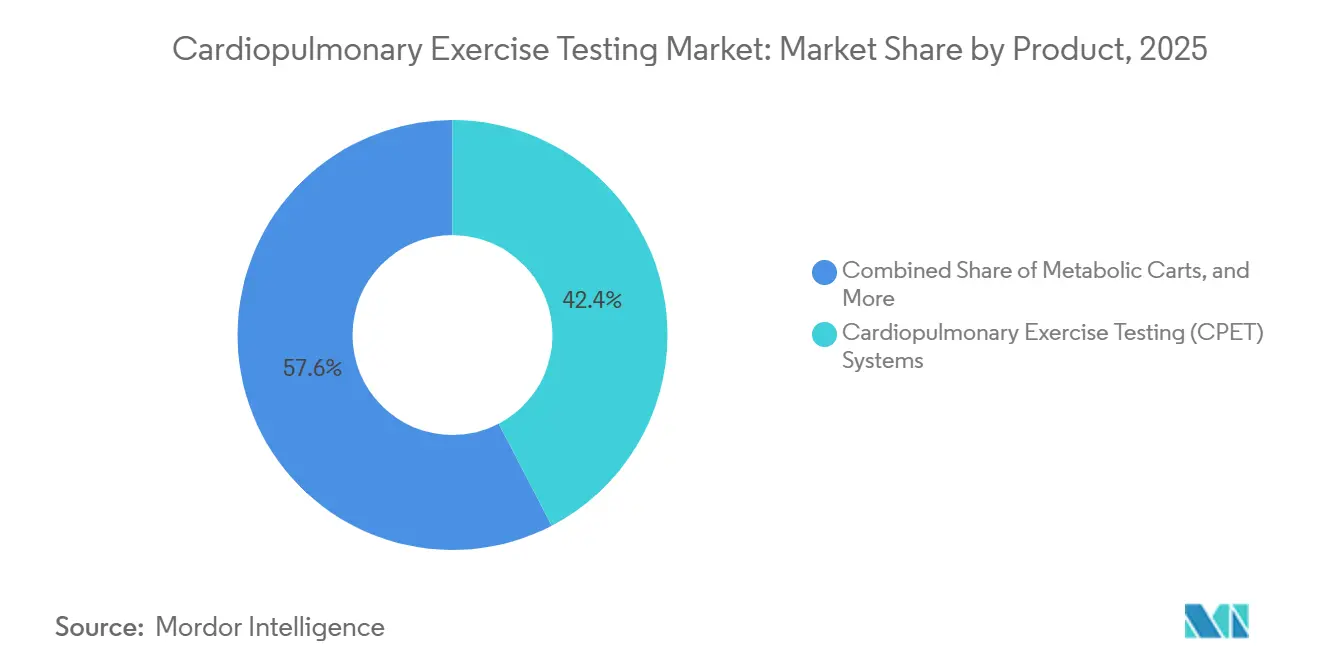

- By product, CPET systems led with 42.37% revenue share in 2025, while metabolic carts are forecast to expand at an 11.34% CAGR through 2031 in the cardiopulmonary exercise testing market.

- By application, clinical diagnostics held 43.68% share in 2025, while pulmonary rehabilitation is projected to grow at an 11.89% CAGR through 2031.

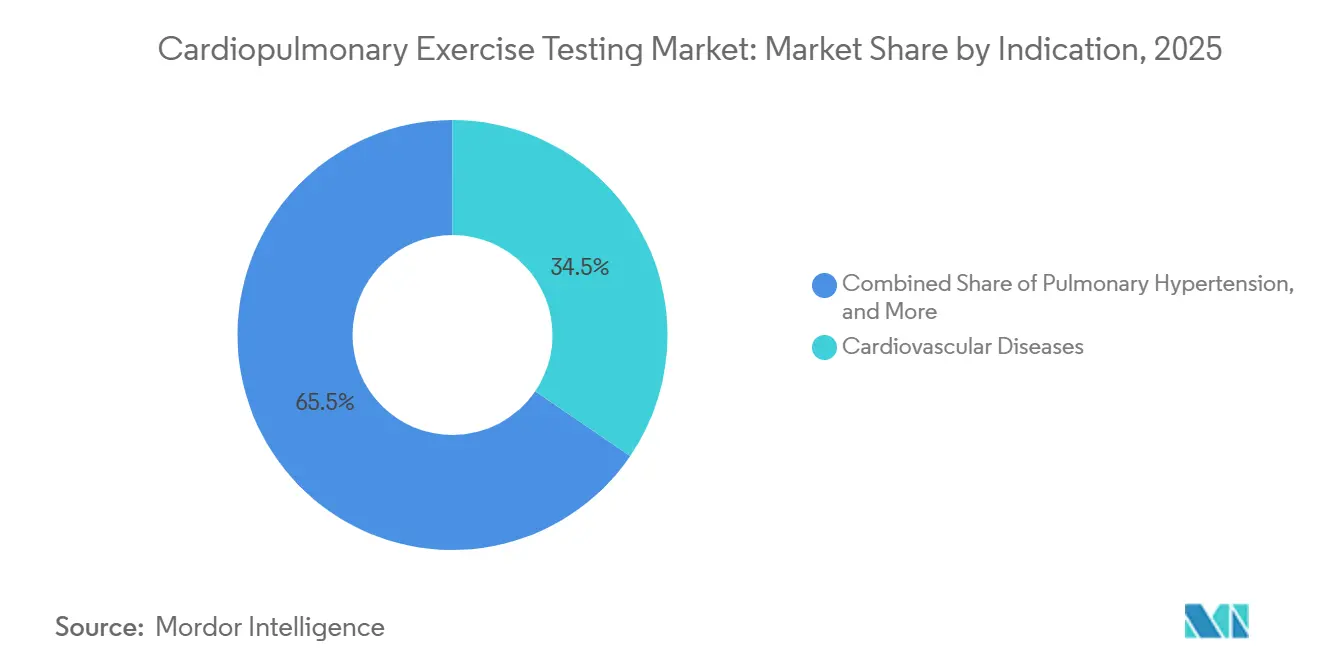

- By indication, cardiovascular diseases accounted for 34.52% share in 2025, while pulmonary hypertension is expected to record the highest CAGR at 12.56% through 2031 in the cardiopulmonary exercise testing market.

- By end user, hospitals accounted for 53.41% share of the cardiopulmonary exercise testing market size in 2025, while specialty cardiology and pulmonology clinics are forecast to advance at a 13.28% CAGR through 2031.

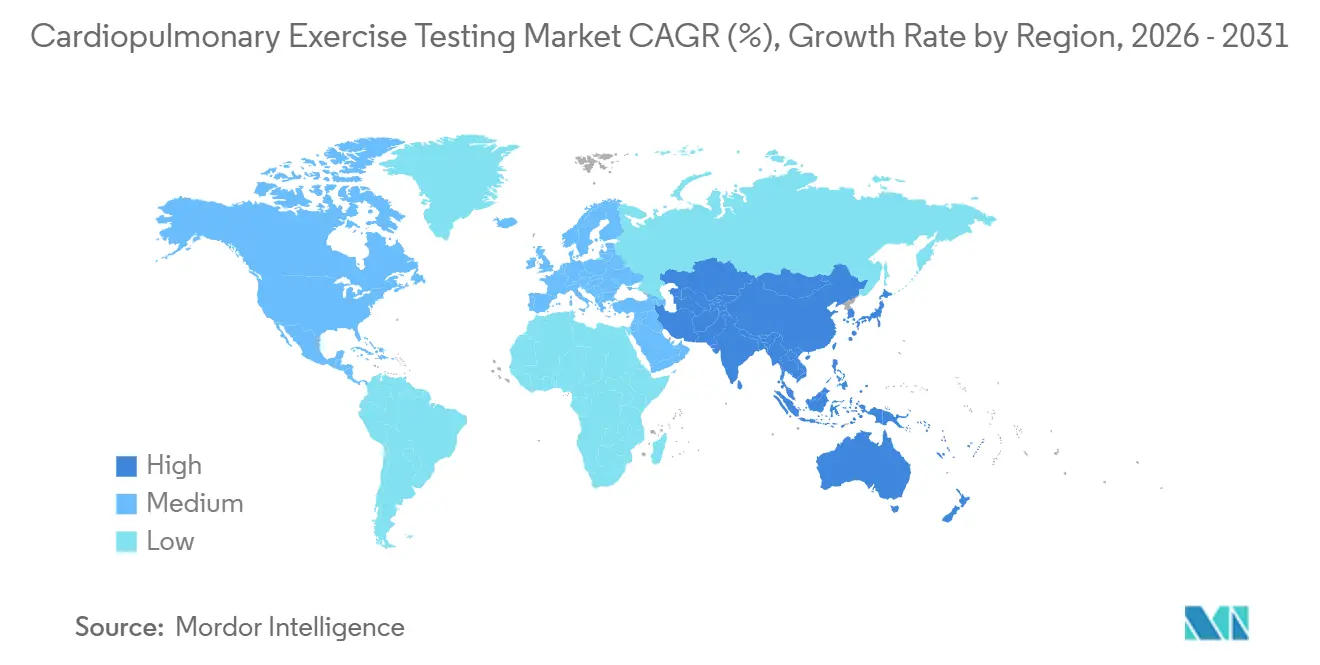

- By geography, North America held 38.46% of the cardiopulmonary exercise testing market share in 2025, while Asia-Pacific is projected to expand at a 14.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cardiopulmonary Exercise Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Burden of Cardiovascular and Respiratory Disease | +2.1% | Global, most acute in South and East Asia, Sub-Saharan Africa | Long term (≥ 4 years) |

| Expansion of Pre-Operative Risk Stratification Use Cases | +1.8% | North America and Western Europe, spill-over to APAC tertiary centers | Medium term (2-4 years) |

| Shift Toward Objective Exercise-Based Functional Assessment | +1.5% | North America and EU, early adoption in ANZ | Medium term (2-4 years) |

| Artificial Intelligence Assisted Test Interpretation | +1.4% | Global, fastest in North America and East Asia | Short term (≤ 2 years) |

| Portable and Compact CPET Adoption in Outpatient Settings | +1.2% | North America, Western Europe, urban APAC | Medium term (2-4 years) |

| Reimbursement Backing for Specialty Diagnostic Testing in Mature Markets | +1.0% | North America and Western Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Cardiovascular and Respiratory Disease

The cardiopulmonary exercise testing market sits at the point where cardiovascular and respiratory disease management now overlap more often in routine care. The World Health Organization reported 19.8 million cardiovascular disease deaths in 2022, equal to 32% of all global deaths, and more than three-quarters of those deaths occurred in low and middle-income countries, which still leaves substantial room for CPET expansion where penetration is low.[1]World Health Organization, “Cardiovascular Diseases (CVDs),” The American Heart Association’s 2025 statistical update also showed that growing absolute incidence and better survival are extending the number of patients who need long-term functional monitoring instead of only acute treatment.[2]American Heart Association, “2025 Heart Disease and Stroke Statistics, A Report of US and Global Data,” This matters for the cardiopulmonary exercise testing market because more patients now live long enough to require repeated assessment of exercise tolerance, ventilatory response, and treatment recovery across several care settings. The same pattern supports follow-up demand in cardiac rehabilitation, where exercise prescription depends on measurable physiologic thresholds instead of generalized activity plans. A 2025 study in the European Journal of Preventive Cardiology found that patients with at least a 5% gain in VO₂ peak after 1 year of phase III rehabilitation had better composite outcomes, which strengthens the case for serial testing rather than a single baseline evaluation.[3]European Journal of Preventive Cardiology, “The Role of Phase 3 Cardiac Rehabilitation in Boosting Peak VO2 and Predicting Clinical Success,”

Expansion of Pre-Operative Risk Stratification Use Cases

The cardiopulmonary exercise testing market is also being supported by the wider use of CPET in surgical risk assessment at large hospitals and academic centers. A 2025 systematic review in the British Journal of Anesthesia Open found that submaximal CPET measures, especially the VE/VCO₂ slope, were independently linked to early postoperative complications across abdominal cancer populations, and values above 38 were tied to higher complication risk after esophageal cancer surgery.[4]“Preoperative Submaximal Cardiopulmonary Exercise Testing and Its Association With Early Postoperative Complications,” A separate 2025 study in PLOS Digital Health used machine learning on preoperative CPET data and showed that cardiorespiratory fitness variables can reveal nonlinear risk thresholds that are not captured through static clinical measures alone. These findings are widening the role of the cardiopulmonary exercise testing market from selected high-risk cases to more standardized use in thoracic, abdominal, and oncologic surgical pathways. The demand effect is not limited to full maximal testing because shorter protocols are also becoming more practical for presurgical clinics with heavy throughput. A 2025 JMIR Perioperative Medicine feasibility study showed that an 18-minute submaximal CPET protocol was technically reliable and acceptable in a high-volume clinic, with 96% of older adults reporting tolerable exertion, which lowers workflow barriers for broader use.

Artificial Intelligence Assisted Test Interpretation

Artificial intelligence is becoming one of the clearest near-term supports for the cardiopulmonary exercise testing market because interpretation remains a major staffing bottleneck. A 2026 study in npj Digital Medicine showed that the Oxynet deep learning framework identified gas exchange and ventilatory thresholds with performance comparable to expert visual review across more than 1,200 CPET files. That matters because threshold detection is one of the most specialized parts of CPET interpretation, and automation reduces the dependence on a small number of trained readers. A 2025 European Respiratory Society Congress presentation also found that GPT-based interpretation showed promising accuracy in identifying normal CPET results, which is particularly relevant for practices that do not have an in-house CPET specialist. The cardiopulmonary exercise testing market, therefore, has a clearer path into community hospitals, remote rehabilitation programs, and general cardiology clinics that could not previously support complex interpretation. Commercial software models are reinforcing that shift, as Medibyt’s CPETwise and other cloud-based tools point to a model where interpretive capability can be delivered separately from deep on-site expertise.

Portable and Compact CPET Adoption in Outpatient Settings

The cardiopulmonary exercise testing market is also expanding through smaller hardware formats that fit outpatient and rehabilitation workflows more easily than traditional lab installations. COSMED’s Quark CPET platform combines breath-by-breath gas exchange analysis with an optional mixing chamber in a compact format designed for clinical use, while the Q-NRG Max extends measurement toward hybrid clinical and performance applications. Vyaire Medical’s Vyntus CPX metabolic cart, distributed through Jaeger, is designed to connect with GE HealthCare’s CardioSoft ECG, which allows one unit to cover both CPET and ECG needs and reduces space and equipment duplication in lower-volume settings. This matters for the cardiopulmonary exercise testing market because smaller clinics and outpatient centers can enter the category without the same footprint required by older systems. Even so, hardware availability alone does not ensure utilization, especially in health systems with technician shortages and uneven protocol familiarity. A 2025 national survey from Saudi Arabia found that the lack of trained technicians remained as important a barrier as equipment availability, which shows that device miniaturization must be matched by operator training and standardized practice to create real throughput gains.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Cost of CPET Equipment and Service Contracts | -2.3% | Global, most acute in MEA, South America, and emerging APAC | Long term (≥ 4 years) |

| Need for Specialized Training and Standardized Protocol Adherence | -1.6% | Global, most acute in emerging markets and community hospitals | Medium term (2-4 years) |

| Limited Reimbursement Depth in Emerging Healthcare Systems | -1.2% | MEA, South America, South and Southeast Asia | Long term (≥ 4 years) |

| Workflow Complexity in Low-Volume Clinical Settings | -0.8% | Community hospitals and low-volume outpatient practices globally | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of CPET Equipment and Service Contracts

The cardiopulmonary exercise testing market still faces a meaningful adoption barrier because a full CPET laboratory setup requires a large upfront investment. The input draft states that integrated systems combining a metabolic cart, calibrated ergometer, 12-lead ECG, and software can cost USD 50,000 to USD 150,000 per installation, and annual service contracts can add another 10% to 15% to ownership costs. That burden slows purchasing in community and secondary hospitals, especially where administrators compare CPET with other capital needs that appear more urgent or serve broader patient volumes. The restraint is stronger in low and middle-income countries because thin reimbursement and limited equipment financing make it harder to justify long payback periods. Ongoing calibration, sensor replacement, and mask or mouthpiece consumables also raise the total cost of ownership and create budget pressure in public systems operating under fixed diagnostic tariffs. This slows replacement cycles as well, which means older installed systems stay in use longer and newer platforms enter the cardiopulmonary exercise testing market more gradually.

Need for Specialized Training and Standardized Protocol Adherence

The cardiopulmonary exercise testing market also remains constrained by the need for trained operators and consistent interpretation standards. Professional bodies such as the American Thoracic Society, the European Respiratory Society, and the Association for Respiratory Technology and Physiology have already published detailed practice guidance, but routine implementation is still uneven across facilities. A UK national survey published in PMC reported that 31.7% of hospitals without CPET cited lack of staff as a barrier, and among hospitals that tried and failed to establish services, 91.7% cited difficulty securing finance for trained personnel. A 2025 Journal of Arrhythmia study reached a similar conclusion in Japan, where low implementation was linked more to systemic under-resourcing than to lack of physician awareness. The effect on the cardiopulmonary exercise testing market is larger than staffing alone because inconsistent protocols reduce the reproducibility of CPET variables across centers, which weakens benchmarking, multi-site research, and AI model development. Quality frameworks such as the ARTP statement and ISO calibration standards provide a basis for consistency, but uptake is still voluntary in many settings, and that leaves performance uneven from one institution to the next.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Hospital Labs Anchor Revenue While Portable Carts Capture Growth

CPET systems held 42.37% of global product revenue in 2025, which kept them as the leading product group within the cardiopulmonary exercise testing market. Their lead reflects the fact that hospitals still prefer integrated platforms that combine gas exchange analysis, ergometers, ECG capability, and interpretation software in a single clinical setup. These systems remain the reference standard for diagnostic depth and are widely used in heart failure prognosis, transplant workup, pulmonary hypertension management, and other guideline-based use cases. The product mix also shows how strongly hospital cardiology and pulmonology labs continue to shape purchasing patterns in the cardiopulmonary exercise testing market. GE HealthCare’s CASE platform update with CardioSoft technology, presented at ACC 2025, reflects the direction of this category because buyers increasingly want digital workflow integration and direct compatibility with hospital information systems.

Metabolic carts are projected to expand at an 11.34% CAGR from 2026 to 2031, which makes them the fastest-growing product group in the cardiopulmonary exercise testing market. Their faster growth reflects demand from outpatient rehabilitation programs, specialist clinics, and diagnostic centers that want leaner configurations than full laboratory systems. ECG and blood pressure monitoring systems remain more standardized products, but they still benefit from mandatory integration in most CPET workflows and continue to support recurring revenue through consumables and software-linked functionality. The broader “others” group, which includes wearable metabolic monitors, remote spirometry accessories, and pulse oximetry modules, remains smaller but strategically relevant as sensor-fusion models develop across the cardiopulmonary exercise testing market. Regulation is also shaping product choices because most CPET gas analyzers in the United States fall under FDA device classification rules in 21 CFR Part 868, while the CMS billing update to Article A56784 affects how hospitals align reimbursable pulmonary stress testing configurations with procurement plans.

By Application: Rehabilitation Displaces Research as the High-Growth Category

Clinical diagnostics accounted for 43.68% share of the cardiopulmonary exercise testing market size in 2025, which kept it as the largest application area. That position reflects CPET’s role as a leading tool in evaluating unexplained dyspnea, classifying heart failure severity, and assessing coronary artery disease in hospital cardiology practice. These use cases generate large testing volumes because they sit close to referral hubs and established specialist pathways. Pre-operative assessment also holds an important share because thoracic surgery and major abdominal oncology programs are using standardized CPET workup more often before complex procedures. Research remains smaller in volume, but it still supports premium device configurations and advanced software demand because sponsored studies require detailed protocols, structured outputs, and reproducible measurements.

Pulmonary rehabilitation is projected to grow at an 11.89% CAGR from 2026 to 2031, making it the fastest-expanding application in the cardiopulmonary exercise testing market. Its rise reflects formal rehabilitation guidance for COPD, heart failure, and post-COVID functional limitation, where exercise prescription is stronger when based on measured physiologic thresholds rather than generic endurance plans. A 2025 BMC Cardiovascular Disorders study found that CPET-guided exercise training improved peak VO₂, anaerobic threshold, and METS in heart failure patients after acute myocardial infarction who received sacubitril or valsartan therapy. That result matters because it supports a combined model in which pharmacotherapy and rehabilitation monitoring reinforce each other over repeated care episodes. The cardiopulmonary exercise testing market therefore benefits from rehabilitation demand differently than from pre-operative assessment, since repeated follow-up creates more durable testing utilization than a single diagnostic event.

By Indication: Pulmonary Hypertension Redefines CPET’s Diagnostic Role

Cardiovascular diseases accounted for 34.52% share in 2025, which made them the largest indication group in the cardiopulmonary exercise testing market. This remains the category’s core because coronary artery disease evaluation, heart failure staging, and cardiac rehabilitation monitoring are already embedded in established clinical pathways. High testing frequency and more stable reimbursement in mature health systems have helped this indication-based approach remain durable even as new use cases emerge. Heart failure is especially important because serial peak VO₂ assessment influences decisions on device therapy eligibility and cardiac transplant listing in major centers. Respiratory diseases form the second-largest indication cluster, supported by COPD staging and pulmonary function assessment in high-burden populations across East and South Asia.

Pulmonary hypertension is forecast to record a 12.56% CAGR from 2026 to 2031, which makes it the fastest-growing indication in the cardiopulmonary exercise testing market. Its growth is tied to a stronger evidence base that positions CPET as a preferred non-invasive tool for detecting early pulmonary vascular dysfunction and monitoring treatment response. A 2025 European Respiratory Journal study found that CPET variables such as oxygen pulse and VE/VCO₂ slope had prognostic value comparable to invasive hemodynamic measures in pulmonary arterial hypertension. A 2026 BMJ Respiratory Research study also showed that combining submaximal CPET parameters with echocardiography improved prognostic assessment in PH-COPD beyond resting hemodynamics alone. The remaining indications, including obesity, metabolic syndrome, and post-COVID condition, are still emerging but they widen the future scope of the cardiopulmonary exercise testing market as protocols become more standardized.

By End User: Hospitals Retain Volume Dominance as Clinics Lead Growth

Hospitals captured 53.41% of end-user demand in 2025, which gave them the leading position in the cardiopulmonary exercise testing market. Their dominance reflects the equipment intensity of full CPET laboratories and the concentration of referral volume from cardiology, pulmonology, and thoracic surgery departments in acute care settings. Large academic and tertiary hospitals continue to anchor the premium tier because they buy high-specification systems that can support AI interpretation, multi-protocol testing, and broad ECG capability. Hospital buyers also tend to place more value on interoperability, centralized data storage, and service reliability because CPET often sits within wider diagnostic pathways. Diagnostic centers held the second-largest share in 2025, and their role is important where hospital waiting times are long or in-house testing capacity is rationed.

Specialty cardiology and pulmonology clinics are forecast to expand at a 13.28% CAGR from 2026 to 2031, which makes them the fastest-growing end-user group in the cardiopulmonary exercise testing market. This rise is linked to semi-portable and portable systems that fit tighter staffing and space conditions without removing core testing capability. Defined reimbursement pathways in mature markets also make the return case easier for outpatient specialist settings than it was in earlier deployment cycles. MGC Diagnostics’ Meridian Series launch in November 2025 directly targets this part of the cardiopulmonary exercise testing market because the platform spans routine spirometry through full CPET in both full-cart and compact tabletop formats. The remaining end-user group, including ambulatory surgical centers and sports medicine facilities, is smaller today but it shows how gas-exchange based performance assessment is broadening beyond traditional hospital walls.

Geography Analysis

North America accounted for 38.46% of the cardiopulmonary exercise testing market share in 2025, which kept the region in the leading position. The region benefits from a dense base of academic cardiology and pulmonology programs, broad familiarity with exercise-based diagnostics, and stronger payer coverage across hospital and outpatient settings. The United States remains the regional anchor because several major platform developers, including GE HealthCare, MGC Diagnostics, SunTech Medical, and Masimo, are based there and support local product visibility, service capacity, and workflow innovation. Canada is emerging as a secondary growth market because aging demographics and health technology assessment activity are improving the case for broader cardiopulmonary monitoring. Mexico remains slower to develop because insurance coverage is more fragmented, and specialist CPET infrastructure is still concentrated in major urban centers.

Europe is the second-largest regional bloc in the cardiopulmonary exercise testing market, supported by strong healthcare infrastructure and established reimbursement pathways for cardiopulmonary diagnostics. Germany holds a solid position because of its statutory insurance depth and the domestic presence of SCHILLER AG and CORTEX Biophysik, while the United Kingdom sustains high institutional testing volumes through NHS pre-operative assessment networks that are tied to surgical outcomes initiatives. Even within Europe, utilization is not uniform, and a 2026 survey from the Portuguese Society of Cardiology showed that access gaps and insufficient residency training still limit fuller adoption despite mature infrastructure. The EU Medical Device Regulation timeline also affects distributor and OEM strategy because next-generation systems with software and AI modules require careful compliance planning before wider rollout.

Asia-Pacific is projected to expand at a 14.62% CAGR from 2026 to 2031, which makes it the fastest-growing region in the cardiopulmonary exercise testing market. China and India are driving that pace through hospital capacity expansion and stronger integration of cardiopulmonary diagnostics into national non-communicable disease programs. Japan is technically advanced, but a Journal of Arrhythmia study found that only 21% of facilities had introduced CPET equipment, and staffing limitations remained a key brake on utilization even where devices were available. South Korea and Australia add depth to regional growth because both have established cardiology networks and expanding outpatient rehabilitation infrastructure. The Middle East and Africa remain smaller in absolute size, but GCC countries are investing in tertiary care capacity and Saudi data showed a 14.1% increase in utilization versus 2 decades earlier even as equipment cost and technician shortages persisted. South America is still at an earlier stage, with adoption concentrated in large private hospital networks and research institutions in cities such as São Paulo, Buenos Aires, and Bogotá, while public sector uptake remains tied to budget cycles and reimbursement gaps.

Competitive Landscape

The cardiopulmonary exercise testing market is moderately consolidated at the top, with GE HealthCare, Philips, COSMED, SCHILLER AG, and MGC Diagnostics holding a strong position in premium institutional procurement. Their advantage comes from broad product portfolios, established hospital relationships, service infrastructure, and the ability to connect CPET into larger cardiology and pulmonary workflows. Even so, the cardiopulmonary exercise testing market is not closed because mid-tier specialists such as CORTEX Biophysik, Ergoline, Medisoft, Cardioline, and Geratherm Medical remain active through protocol customization, ergometer flexibility, and regional service depth. GE HealthCare’s wider cardiology strategy is especially notable because the company said in 2025 that it had led FDA AI-enabled device authorizations for 3 consecutive years with 85 total authorizations, which suggests that its CPET approach sits inside a broader software and diagnostics platform rather than a stand-alone hardware model. That platform logic matters because hospitals increasingly prefer vendors that can link stress testing, ECG data, imaging, and downstream monitoring in one connected environment.

The main open spaces in the cardiopulmonary exercise testing market are AI interpretation for low-specialist settings, portable metabolic monitoring for home-based rehabilitation, and workflow integration for providers with fragmented clinical IT systems. Danaher’s USD 9.9 billion acquisition of Masimo, completed in June 2026, is strategically important because it brings continuous non-invasive monitoring capabilities into a broader diagnostics group and could improve how pulse oximetry and related monitoring functions are integrated into future CPET setups. This kind of move can reshape competition in the cardiopulmonary exercise testing market even without launching a new cart immediately, because adjacent monitoring assets influence product design, bundled selling, and post-acute use cases. Regional contenders such as Allengers Medical Systems in India and Innomed Medical in Hungary also retain room to grow because they compete on local pricing, regulatory familiarity, and distributor networks that are difficult for global OEMs to match cost-effectively.

Recent product and operating moves show that competition in the cardiopulmonary exercise testing market is increasingly practical rather than purely headline driven. GE HealthCare’s March 2025 CASE update focused on better workflow integration and on-demand ECG access, which speaks directly to the needs of cardiology departments that want faster data movement and less manual handling. MGC Diagnostics responded in November 2025 with the Meridian Series, which used a modular design to cover facilities ranging from large hospitals to specialty clinics and therefore widened its reach across different testing volumes. SCHILLER’s January 2026 completion of building acceptance for its new ERGOSANA facility added a manufacturing and service signal to the competitive picture because delivery capacity and support responsiveness remain important in this category. Taken together, these actions show that leading companies are competing through software integration, deployment flexibility, and service readiness, while smaller firms still have space where regional distribution and price sensitivity matter more than ecosystem breadth.

Cardiopulmonary Exercise Testing Industry Leaders

Cardinal Health

GE HealthCare

Halma plc

Koninklijke Philips N.V.

Nihon Kohden Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Danaher Corporation completed its acquisition of Masimo Corporation in an all-cash transaction valued at approximately USD 9.9 billion. Masimo, a leading specialty diagnostics provider of pulse oximetry and AI-enabled patient monitoring, becomes a standalone operating company within Danaher's Diagnostics segment. The deal integrates Masimo's continuous non-invasive monitoring technology, including SpO₂ and hemodynamic parameters relevant to CPET monitoring, into a larger diagnostics portfolio, materially shifting the competitive positioning in exercise and cardiopulmonary monitoring.

- February 2026: Danaher announced a definitive agreement to acquire Masimo Corporation for USD 180 per share in cash, representing a total enterprise value of approximately USD 9.9 billion, including assumed indebtedness. The transaction was unanimously approved by both boards and cleared shareholder vote in May 2026, with the deal closing in June 2026.

- January 2026: SCHILLER completed building acceptance for its new ERGOSANA facility, marking a significant operational expansion. The new location is expected to enhance manufacturing and service capacity for SCHILLER's cardiovascular diagnostic and CPET product lines across European markets.

Global Cardiopulmonary Exercise Testing Market Report Scope

As per the scope of the report, cardiopulmonary exercise testing (CPET) is a diagnostic assessment that measures how the heart, lungs, and muscles respond to physical exertion. It combines respiratory gas analysis with exercise protocols (usually treadmill or cycle ergometer) to evaluate oxygen uptake, carbon dioxide output, and ventilatory efficiency. CPET provides an integrated view of cardiovascular and pulmonary function, helping clinicians diagnose unexplained breathlessness, assess exercise tolerance, and guide treatment planning in cardiopulmonary diseases.

The cardiopulmonary exercise testing (CPET) market is segmented by product, application, indication, end user, and geography. By product, the market is segmented into cardiopulmonary exercise testing (CPET) systems, metabolic carts, ECG & blood pressure monitoring systems, and others. By application, the market is segmented into clinical diagnostics, pre-operative assessment, research applications, pulmonary rehabilitation, and others. By Indication, the market is segmented into cardiovascular diseases, respiratory diseases, heart failure, pulmonary hypertension, and others. By end user, the market is segmented into hospitals, diagnostic centers, specialty cardiology & pulmonology clinics, and others. The geography segment is further divided into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market size and forecasts in value (USD) for the above segments.

| Cardiopulmonary Exercise Testing (CPET) Systems |

| Metabolic Carts |

| ECG & Blood Pressure Monitoring Systems |

| Others |

| Clinical Diagnostics |

| Pre-operative Assessment |

| Research Applications |

| Pulmonary Rehabilitation |

| Others |

| Cardiovascular Diseases |

| Respiratory Diseases |

| Heart Failure |

| Pulmonary Hypertension |

| Others |

| Hospitals |

| Diagnostic Centers |

| Specialty Cardiology & Pulmonology Clinics |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Cardiopulmonary Exercise Testing (CPET) Systems | |

| Metabolic Carts | ||

| ECG & Blood Pressure Monitoring Systems | ||

| Others | ||

| By Application | Clinical Diagnostics | |

| Pre-operative Assessment | ||

| Research Applications | ||

| Pulmonary Rehabilitation | ||

| Others | ||

| By Indication | Cardiovascular Diseases | |

| Respiratory Diseases | ||

| Heart Failure | ||

| Pulmonary Hypertension | ||

| Others | ||

| By End User | Hospitals | |

| Diagnostic Centers | ||

| Specialty Cardiology & Pulmonology Clinics | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected size of the cardiopulmonary exercise testing market by 2031?

The cardiopulmonary exercise testing market is projected to reach USD 2.71 billion by 2031, up from USD 1.63 billion in 2026, at a 10.74% CAGR over 2026 to 2031.

Which product group leads current revenue in cardiopulmonary exercise testing?

CPET systems led product revenue with a 42.37% share in 2025 because hospitals still prefer integrated setups that combine gas analysis, ECG, ergometry, and software in one platform.

Which application is expanding fastest in cardiopulmonary exercise testing?

Pulmonary rehabilitation is the fastest-growing application with an 11.89% CAGR through 2031, supported by wider use of CPET-guided exercise prescription in COPD, heart failure, and post-COVID care.

Which end users are driving the next wave of demand?

Hospitals remained the largest end users with a 53.41% share in 2025, while specialty cardiology and pulmonology clinics are growing fastest at a 13.28% CAGR as portable and modular systems become easier to deploy.

Which region is growing fastest for cardiopulmonary exercise testing?

Asia-Pacific is the fastest-growing region with a 14.62% CAGR through 2031, driven by hospital capacity expansion in China and India and wider integration of cardiopulmonary diagnostics into chronic disease programs.

What is holding wider CPET adoption back?

The main barriers are high capital cost, ongoing service and consumable expense, and limited access to trained staff who can run and interpret tests consistently across care settings.

Page last updated on: