Cardiac Cryoablation Device Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

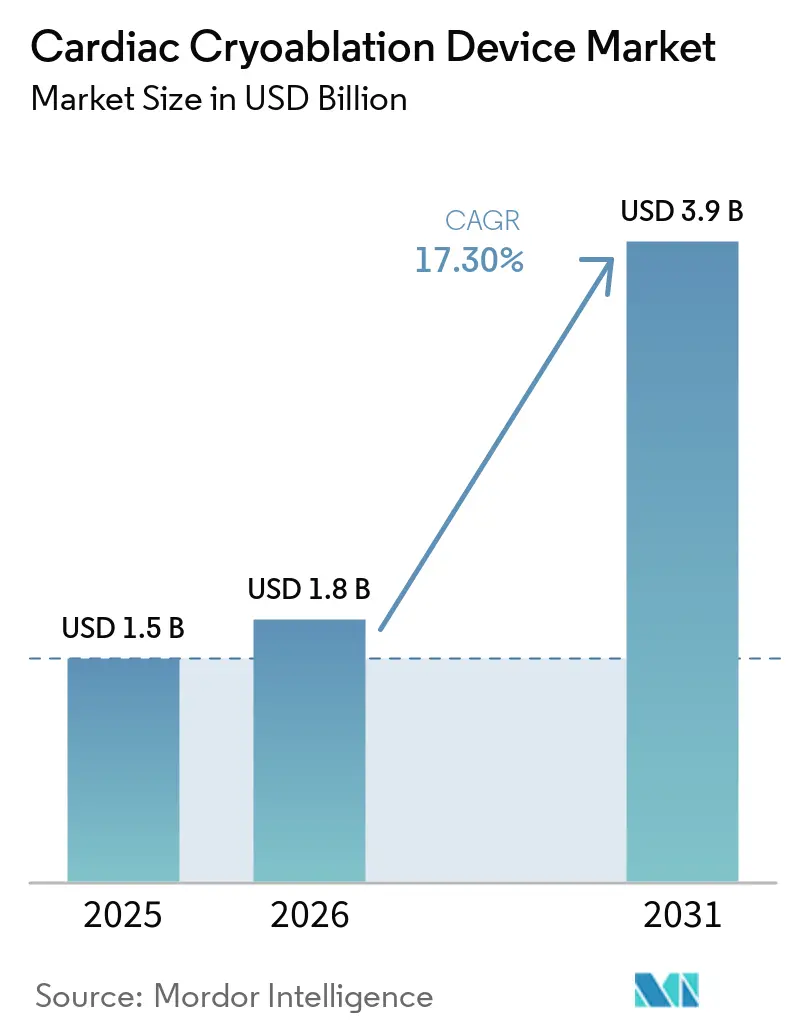

| Market Size (2026) | USD 1.8 Billion |

| Market Size (2031) | USD 3.9 Billion |

| Growth Rate (2026 - 2031) | 17.30% CAGR |

| Fastest Growing Market | Europe |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cardiac Cryoablation Device Market Analysis by Mordor Intelligence

The Cardiac Cryoablation Device Market size is projected to be USD 1.5 billion in 2025, USD 1.8 billion in 2026, and reach USD 3.9 billion by 2031, growing at a CAGR of 17.30% from 2026 to 2031.

A confluence of reimbursement liberalization, technology upgrades such as expandable cryoballoons, and early-intervention clinical evidence is lifting procedure volumes even as pulsed field ablation (PFA) raises near-term substitution risk. Regulatory actions, especially the 2026 U.S. Ambulatory Surgical Center (ASC) payment rule, are steering simple atrial fibrillation (AF) cases into outpatient venues, while ultra-low-temperature cryo is opening a ventricular tachycardia (VT) niche that standard −88 °C balloons cannot reach. Liquid-nitrogen systems from Chinese entrants are adding price and sustainability dynamics, and installed console footprints in tertiary hospitals are being defended through incremental workflow refinements that cut procedure time and device exchanges. Competitive positioning now turns on how quickly vendors can blend mapping, cryo, and PFA on a single platform without losing the single-shot reproducibility that originally differentiated cryoablation.

Key Report Takeaways

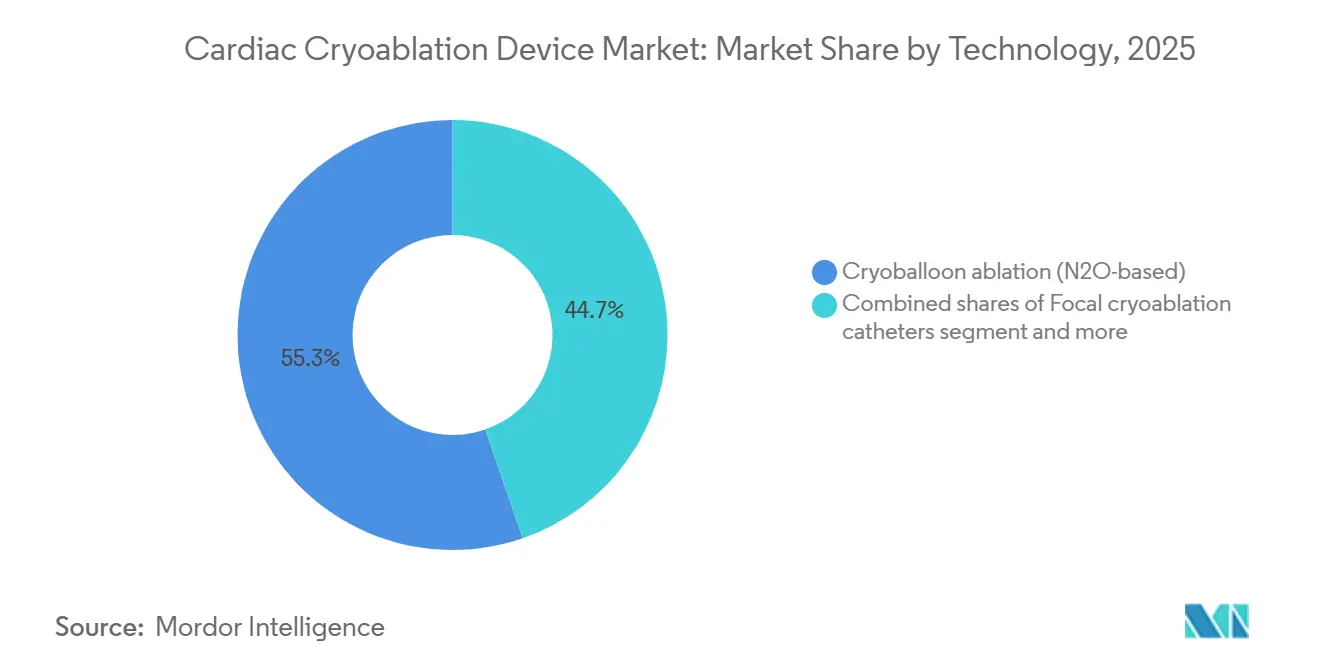

- By technology, nitrous-oxide cryoballoons led with 55.30% of the cardiac cryoablation device market share in 2025, while ultra-low-temperature cryo is forecast to grow at a 17.95% CAGR to 2031.

- By product, catheters and balloons accounted for 62.18% share of the cardiac cryoablation device market size in 2025 and are advancing at a 17.86% CAGR through 2031.

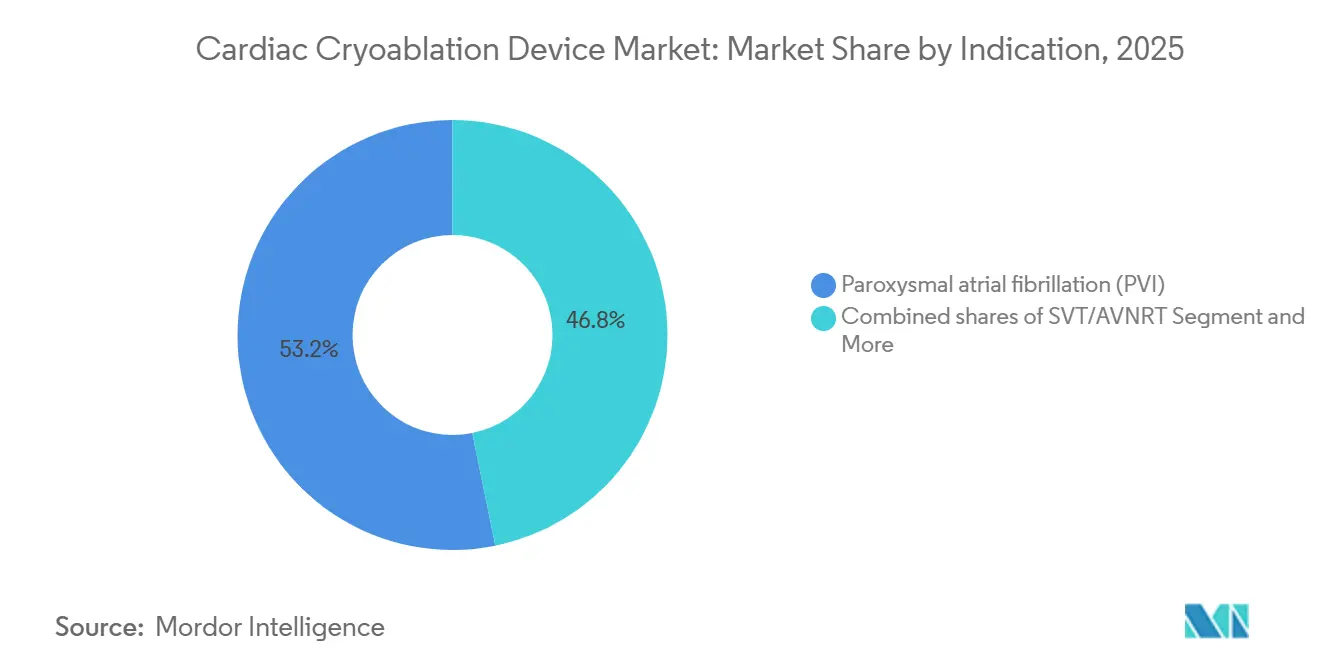

- By indication, paroxysmal AF accounted for 53.18% of revenue in 2025, whereas VT ablation is projected to expand at a 17.81% CAGR through 2031.

- By end user, tertiary hospitals held 57.18% share in 2025, while ASCs recorded the highest forecast CAGR at 17.88% to 2031.

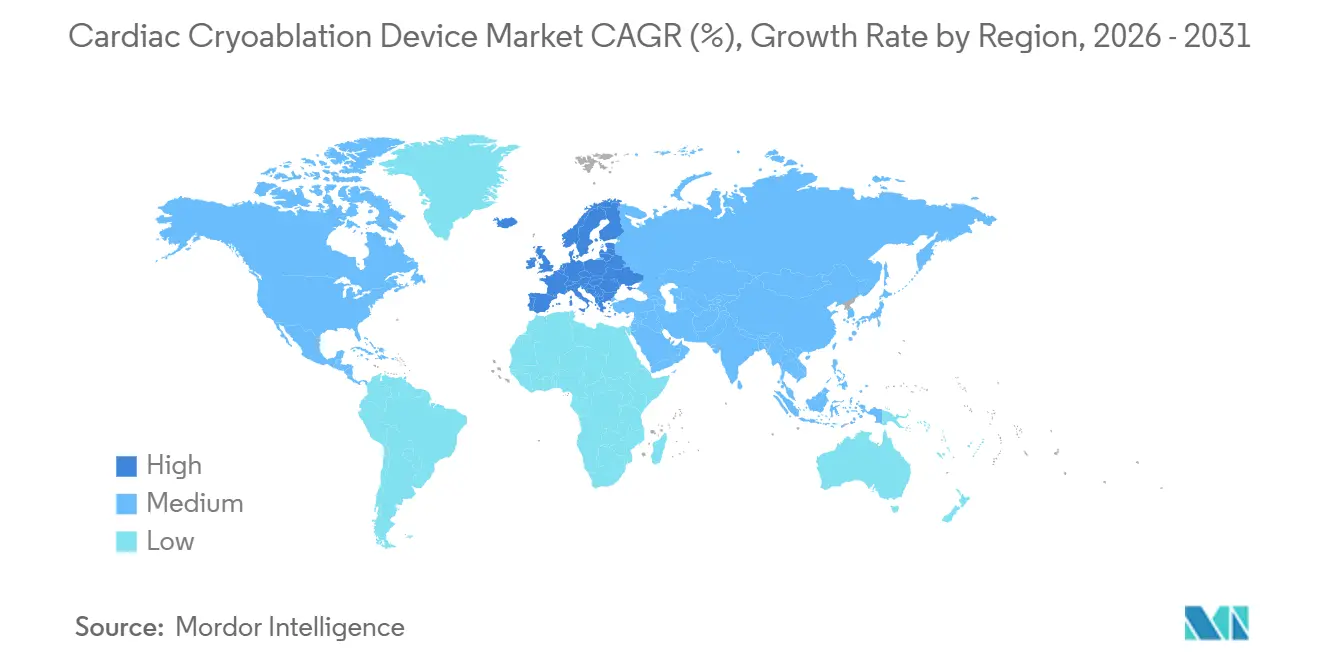

- By geography, North America dominated with 46.17% share in 2025, yet Europe is set to outpace all regions with a 17.76% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cardiac Cryoablation Device Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ASC coverage, outpatient shift in the U.S. | +3.2% | United States, Canada pilot programs, select EU payers | Short term (≤ 2 years) |

| First-line ablation evidence, earlier care | +4.1% | North America, Western Europe, Japan | Medium term (2-4 years) |

| New cryo system approvals, console growth | +2.8% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Single-shot workflow efficiency | +1.9% | High-volume EP centers worldwide | Short term (≤ 2 years) |

| VT opportunity from ultra-low-temperature | +2.5% | Initially North America and Europe | Long term (≥ 4 years) |

| China entrants, price and sustainability | +2.0% | China with spillover to cost-sensitive emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

ASC Coverage and Outpatient Shift in the United States

The November 2025 CMS final rule moved comprehensive AF ablation code CPT 93656 onto the ASC list with a USD 24,532 facility payment, eclipsing the inpatient tariff and catalyzing an outpatient surge. Cryoballoon procedures average 122 minutes, compared with 160 minutes for radiofrequency (RF), reducing overtime and aligning with ASC throughput models [1]Heart Rhythm Journal Editorial Board, “FREEZE Cohort Simulation Study,” heartrhythmjournal.com. Early 2026 scheduling data show ASCs booking two additional cryo cases per lab per day, expanding ASC revenue at a projected 17.88% CAGR. Canadian provinces and several Western European payers are piloting similar day-case AF pathways, hinting at an export of a North American playbook.

First-Line Ablation Evidence and Earlier Intervention

FDA first-line clearance for the Arctic Front Advance balloon, together with STOP-AF First and EARLY-AF results showing 75-82% arrhythmia-free survival, shifted ablation from salvage to upfront care [2]U.S. Food and Drug Administration, “Medtronic POLARx FIT Cryoablation System Decision Summary,” fda.gov. Younger, structurally intact atria yield higher single-procedure durability, trimming costly repeat interventions and pulling forward demand. A 2024 German cost-utility model pegged incremental cost-effectiveness at EUR 1,037 per QALY, well below regional willingness-to-pay thresholds, reinforcing payers’ openness to ablation early in the pathway.

New Cryo System Approvals and Installed Base Expansion

Boston Scientific’s February 2026 FDA nod for POLARx FIT introduced an expandable 28–31 mm balloon that cuts catheter exchanges, a refinement that delivered 96% event-free survival at 12 months in the FROZEN-AF IDE trial. With more than 25,000 global cases logged before the U.S. launch, the platform is positioned to erode Medtronic’s long-held console dominance. Parallel CE-mark supplements and Japanese approvals are expanding the global fleet, with console placements rising in ASCs despite an up-front cost of USD 150,000-200,000.

Workflow Efficiency and Reproducibility of Single-Shot Cryo

Simulation studies from Germany’s FREEZE cohort show cryoballoon overtime days at 25.7% versus 70.7% for RF, translating into lean staffing and predictable lab scheduling. Uniform lesion creation with time-to-isolation dosing has narrowed operator-to-operator variability, boosting cross-credentialing and favoring multi-site health-system adoption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PFA substitution risk for AF ablation | -4.8% | North America, Western Europe | Short term (≤ 2 years) |

| Safety events (esophageal injury, PNP) | -1.7% | Global with heightened U.S. and EU oversight | Medium term (2-4 years) |

| FDA real-world evidence mandates | -1.2% | United States with knock-on effects for CE-mark aspirants | Medium term (2-4 years) |

| Under-utilization of surgical ablation | -0.9% | Community cardiac surgery centers worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

PFA Substitution Risk for AF Ablation

The January 2025 NEJM SINGLE SHOT CHAMPION trial reported 37.1% recurrence for PFA versus 50.7% for cryo, propelling hospitals to fast-track PFA console buying even at 23% higher device cost [3]The New England Journal of Medicine, “Single Shot Champion Trial Results,” nejm.org. U.S. physician surveys indicate PFA penetration climbing toward 68% of AF ablations in 2026, tightening the window for cryo vendors to defend share. Europe mirrors the trend as CE-cleared PFA catheters demonstrate zero esophageal injury in 17,000-plus real-world cases, sharpening medico-legal contrast with cryo.

Safety Events (Esophageal Injury, Phrenic Nerve Palsy) and IFU Updates

Cryo’s phrenic nerve palsy (PNP) incidence stands near 2%, with nearly half of them persisting beyond 12 months, prompting 2024 FDA IFU revisions that cut freeze time from 240 s to 180 s and require continuous diaphragmatic stimulation. Although atrio-esophageal fistula risk remains far lower than with RF, PFA’s zero-injury track record is shifting posterior-wall lesion preference. Both U.S. and EU regulators now require post-market clinical follow-up for Class III cryo catheters, extending launch timelines and increasing evidence-generation costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: N₂O Cryoballoon Defends Volume While Ultra-Low-Temperature VT Gains Traction

In 2025, nitrous oxide cryoballoon systems accounted for 55.30% of the cardiac cryoablation device market share, anchored by Medtronic’s decade-old console-based system that enables reproducible single-shot pulmonary vein isolation. The cardiac cryoablation device market for cryoballoon technology is expected to grow steadily as ASCs acquire consoles for paroxysmal AF workflows. Ultra-low-temperature cryo for VT, operating at −196 °C, is projected to log the fastest 17.95% CAGR, opening a new revenue lane for underserved structural heart disease populations.

Console makers are layering incremental software and integrated mapping to hold off PFA cannibalization. Chinese liquid-nitrogen balloons bring sustainability branding that resonates with hospital “green OR” committees. Focal cryo catheters retain niche utility for supraventricular tachycardia, yet their modest volume, coupled with RF’s contact-force advances, limits upside. Surgical cryo remains guideline-endorsed but under-penetrated, held back by operating-room workflow inertia and cross-clamp penalties.

By Product: Catheters/Balloons Drive Revenue as Consoles Follow ASC Build-Out

Catheters and balloons accounted for 62.18% of 2025 revenue and will continue to outpace consoles at a 17.86% CAGR, as procedure growth directly scales consumable pull-through. Expandable balloons such as POLARx FIT reduce device exchanges, adding economic and ergonomic value. The cardiac cryoablation device market size attached to console sales will rise in tandem with ASC migration, though capital budgets remain sensitive to uncertainty around multi-energy platforms. Ancillary sheaths and mapping catheters are increasingly bundled into single reimbursement codes, compressing stand-alone pricing but cementing vendor lock-in.

Disposable scavenging hoses, pressure lines, and sterile sleeves generate predictable but low-margin revenue; environmental scrutiny of nitrous oxide exhaust may spur additional redesigns of accessories. Integrated platforms that align cryo data feeds with external 3-D mapping systems lower cognitive load for electrophysiologists and are likely to shape future product roadmaps.

By Indication: Paroxysmal AF Anchors Volume, VT Is the Growth Spark

Paroxysmal AF constituted 53.18% of 2025 turnover and, supported by first-line approvals, remains the backbone of procedure volume. Durable single-shot outcomes in minimally remodeled atria sustain high lab throughput. VT ablation, leveraging ultra-low-temperature depth, is forecast to post a 17.81% CAGR as clinical data mature; the cardiac cryoablation device market size for VT could approach the persistent AF segment by decade’s end if reimbursement codes are secured. Persistent AF use cases face stiffer PFA rivalry given larger lesion sets and safety advantages on the posterior wall.

Supraventricular tachycardia and atrioventricular nodal re-entry tachycardia remain niche, addressed by small-diameter focal probes. Their low complexity and established RF solutions can cryo-expand but provide stable, repeatable volumes in pediatric and young-adult populations, where cryo’s lower AV-block risk carries weight.

By End User: ASC Channel Accelerates Under New CMS Economics

Tertiary hospitals still generated 57.18% of 2025 spend, leveraging comprehensive EP ecosystems, hybrid OR suites, and multidisciplinary VT programs. Nonetheless, ASCs are set to be the fastest risers, with a 17.88% CAGR, as the 2026 rule equalizes payments and rewards efficient single-shot workflows. The cardiac cryoablation device market share attributable to ASCs could reach one-third by 2031 if payer pilots in Canada and Western Europe institutionalize day-case models.

Community hospitals remain volume participants for straightforward paroxysmal cases but lack staff depth for complex VT or mapping-intensive persistent AF. Purchasing behavior bifurcates accordingly: ASCs often adopt single-energy cryo consoles, whereas academic centers lean toward multi-energy stacks integrating cryo, RF, and PFA to handle a broader lesion portfolio.

Geography Analysis

North America delivered 46.17% of 2025 revenue, buoyed by CMS’s outpatient ruling and Medtronic’s entrenched console fleet. U.S. labs are fast-tracking ASC conversions, aided by predictable cryo timings that fit half-day blocks. Canadian adoption is constrained by provincial budgetary variances; specialist centers in Ontario and Quebec show momentum, yet cross-country uniformity is absent. Mexico lags due to private-payer dominance and limited EP infrastructure.

Europe is the fastest-growing region at a 17.76% CAGR. Early CE-mark access to POLARx FIT and supportive cost-effectiveness data from Germany and the U.K. have kept cryo competitive even as PFA enters. Germany’s workflow modeling demonstrates tangible staffing efficiencies, while the U.K.’s National Health Service weighs higher device cost against lower re-ablation rates. Southern European markets expand on the back of regional cardiac network programs, although reimbursement heterogeneity tempers the pace.

Asia-Pacific presents a mixed landscape. Japan, with PMDA approvals for both paroxysmal and persistent AF indications, serves as a global launch pad for incremental balloon refinements. China’s newly approved liquid-nitrogen systems inject price and eco-credential competition, widening access in tier-2 cities. Australia and South Korea display steady tertiary-hospital demand, but ASC infrastructure is nascent. India and much of Southeast Asia remain constrained by cash-pay models, limiting penetration to urban referral centers.

Competitive Landscape

The competitive arena is moderately concentrated. Medtronic retains the largest installed base, yet Boston Scientific’s POLARx FIT is eroding share by solving anatomical fit challenges without catheter swaps. AtriCure dominates surgical cryo but reported a revenue dip in minimally invasive cardiac ablation as PFA siphons off catheter cases. Johnson & Johnson’s global ablation supremacy is tempered by a temporary Varipulse trial pause, offering cryo a brief defensive window. Chinese entrants are carving out eco-friendly value propositions through liquid-nitrogen coolant and cost advantages, while Adagio Medical is pioneering ultra-low-temperature VT therapy with FDA Breakthrough Device momentum.

Strategically, incumbents are bundling mapping and ablation into unified consoles to blunt PFA encroachment. Philips and Abbott supply mapping systems that interface seamlessly with cryo consoles, fostering ecosystem stickiness. Regulatory tightening around post-market evidence and sustainability assessments may favor diversified players with deep compliance infrastructure. Success through 2031 will hinge on defending paroxysmal AF volume in ASCs, monetizing VT expansion, and integrating cryo within multi-energy architectures before PFA achieves irreversible dominance.

Cardiac Cryoablation Device Industry Leaders

Medtronic Plc

Boston Scientific Corporation

AtriCure, Inc.

Abbott Laboratories

Koninklijke Philips N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Abbott gained CE-Mark clearance for the TactiFlex Duo ablation catheter, giving European clinicians another tool for restoring a normal heartbeat in patients with difficult-to-treat arrhythmias.

- January 2026: Medtronic secured its own CE Mark for the Sphere-360 pulsed-field ablation catheter, underscoring the company’s plan to blend years of cryotherapy experience with the emerging non-thermal energy source favored for fast, tissue-selective cardiac procedures.

- April 2025: Adagio Medical earned U.S. FDA Breakthrough Device designation for its vCLAS cryoablation system, a therapy designed to quickly freeze and disable the short circuits that trigger life-threatening ventricular tachycardia.

Global Cardiac Cryoablation Device Market Report Scope

As per the scope of the report, a cardiac cryoablation device is a specialized medical tool used to treat heart rhythm disorders, most commonly atrial fibrillation (AFib), by delivering extreme cold to disable the heart tissue that generates irregular electrical signals. Unlike traditional radiofrequency ablation, which uses heat, these devices utilize a refrigerant—typically nitrous oxide to freeze the targeted tissue to temperatures as low as -30 degrees Celsius to -80 degrees Celsius.

The cardiac cryoablation device market is segmented by technology, product, indication, end user, and geography. By technology, the market is segmented into Cryoballoon ablation (N2O-based), Focal cryoablation catheters, Surgical cryoablation (probes/clamps; N2O/Argon), and Ultra-low-temperature cryo for VT (emerging). By end users’ industry, the market is segmented into cryoablation catheters/balloons, cryo consoles/generators, steerable sheaths/introducers, inner-lumen circular mapping catheters, and ancillary disposables. By indication, the market is segmented into paroxysmal atrial fibrillation, persistent atrial fibrillation, SVT/AVNRT, and ventricular tachycardia. By end users, the market is segmented into tertiary/academic hospitals & EP labs, community hospitals, and ambulatory surgery centers (ASC)

Geographically, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Cryoballoon ablation (N2O-based) |

| Focal cryoablation catheters |

| Surgical cryoablation (probes/clamps; N2O/Argon) |

| Ultra-low-temperature cryo for VT (emerging) |

| Cryoablation catheters/balloons |

| Cryo consoles/generators |

| Steerable sheaths/introducers |

| Inner-lumen circular mapping catheters (cryo workflows) |

| Ancillary disposables |

| Paroxysmal atrial fibrillation (PVI) |

| Persistent atrial fibrillation (PVI-centric) |

| SVT/AVNRT (focal cryo) |

| Ventricular tachycardia (ULTC) |

| Tertiary/academic hospitals & EP labs |

| Community hospitals |

| Ambulatory surgery centers (ASC) |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology | Cryoballoon ablation (N2O-based) | |

| Focal cryoablation catheters | ||

| Surgical cryoablation (probes/clamps; N2O/Argon) | ||

| Ultra-low-temperature cryo for VT (emerging) | ||

| By Product | Cryoablation catheters/balloons | |

| Cryo consoles/generators | ||

| Steerable sheaths/introducers | ||

| Inner-lumen circular mapping catheters (cryo workflows) | ||

| Ancillary disposables | ||

| By Indication | Paroxysmal atrial fibrillation (PVI) | |

| Persistent atrial fibrillation (PVI-centric) | ||

| SVT/AVNRT (focal cryo) | ||

| Ventricular tachycardia (ULTC) | ||

| By End User | Tertiary/academic hospitals & EP labs | |

| Community hospitals | ||

| Ambulatory surgery centers (ASC) | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the market size of cardiac cryoablation devices market in 2025?

The Cardiac Cryoablation Device Market size is projected to be USD 1.5 billion in 2025, USD 1.8 billion in 2026, and reach USD 3.9 billion by 2031, growing at a CAGR of 17.30% from 2026 to 2031.

Which product type contributes the most revenue?

Catheters and balloons generated 62.18% of 2025 sales and remain the leading revenue driver, as every procedure consumes a new disposable.

Will pulsed field ablation displace cryo in atrial fibrillation?

PFA penetration is expected to reach 68% of U.S. AF ablations in 2026, yet cryo retains a cost and console-availability edge in many ASCs, preserving share in paroxysmal cases.

What fuels the surge in ventricular tachycardia procedures?

Ultra-low-temperature systems that create 8-10 mm transmural lesions address thick ventricular scar tissue, delivering a forecast 17.81% CAGR in VT-specific revenue.

Page last updated on: