Carboxytherapy Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

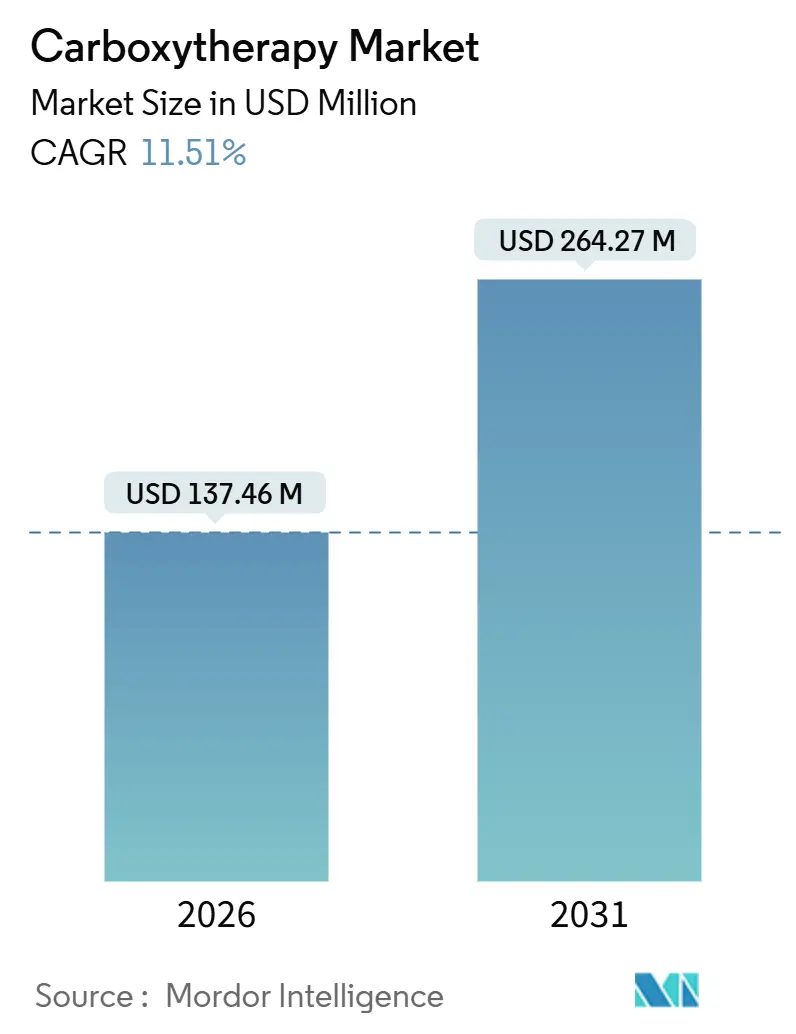

| Market Size (2026) | USD 137.46 Million |

| Market Size (2031) | USD 264.27 Million |

| Growth Rate (2026 - 2031) | 11.51% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Carboxytherapy Market Analysis by Mordor Intelligence

The Carboxytherapy Market size is estimated at USD 137.46 million in 2026, and is expected to reach USD 264.27 million by 2031, at a CAGR of 11.51% during the forecast period (2026-2031).

Elevated post-pandemic demand for minimally invasive care, mounting clinical evidence for diabetic wound healing, and a visible preference for portable delivery systems are reshaping the competitive field. Growth also stems from Gen Z’s early adoption of aesthetic procedures in Asia-Pacific, regulatory tailwinds that shorten trial timelines in China, and hospital initiatives to lower Scope 3 emissions through low-carbon medical gases. Competitive pressure from fractional lasers and radiofrequency microneedling is intensifying, so manufacturers emphasize lower downtime, bundled treatment packages, and AI-driven dose personalization to widen practitioner appeal. Portable units, value-based reimbursement for angiology indications, and sustainability-linked gas supply contracts are the three most actionable opportunities for stakeholders in the carboxytherapy market.

Key Report Takeaways

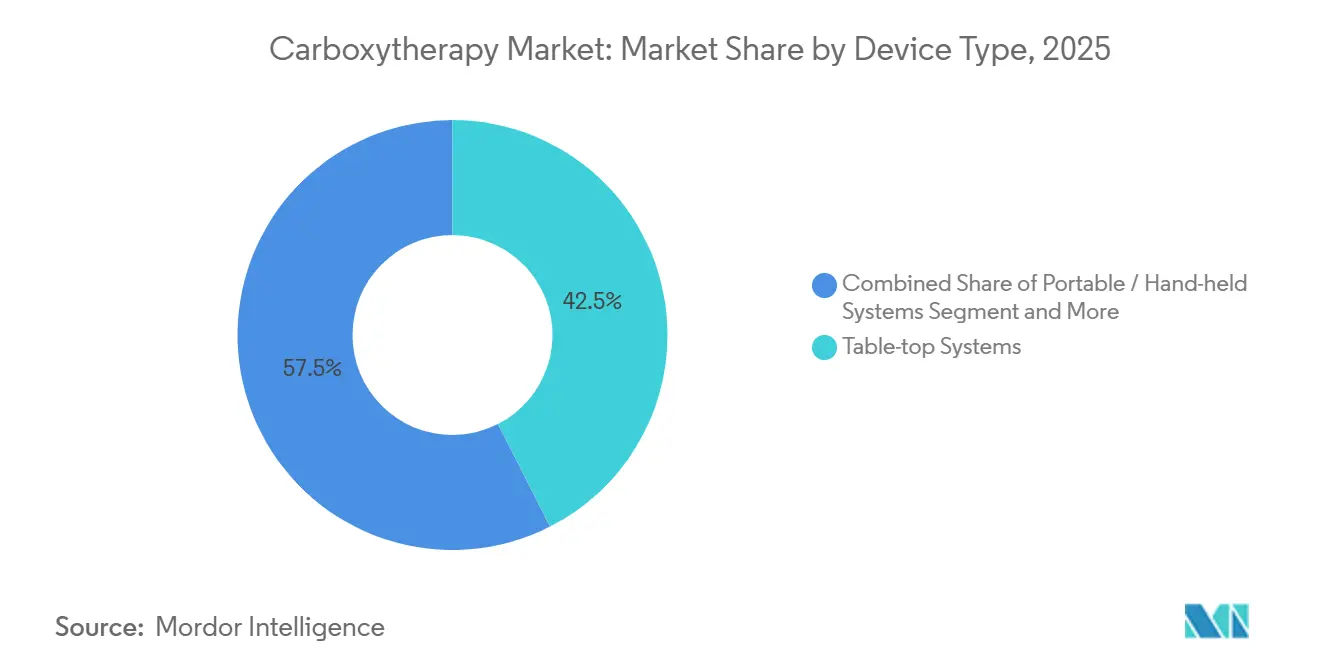

- By device type, table-top systems held 42.55% of carboxytherapy market share in 2025 while portable units are forecast to expand at a 13.25% CAGR through 2031.

- By application, aesthetic medicine captured 54.23% of the carboxytherapy market size in 2025 whereas angiology indications are advancing at a 14.15% CAGR between 2026-2031.

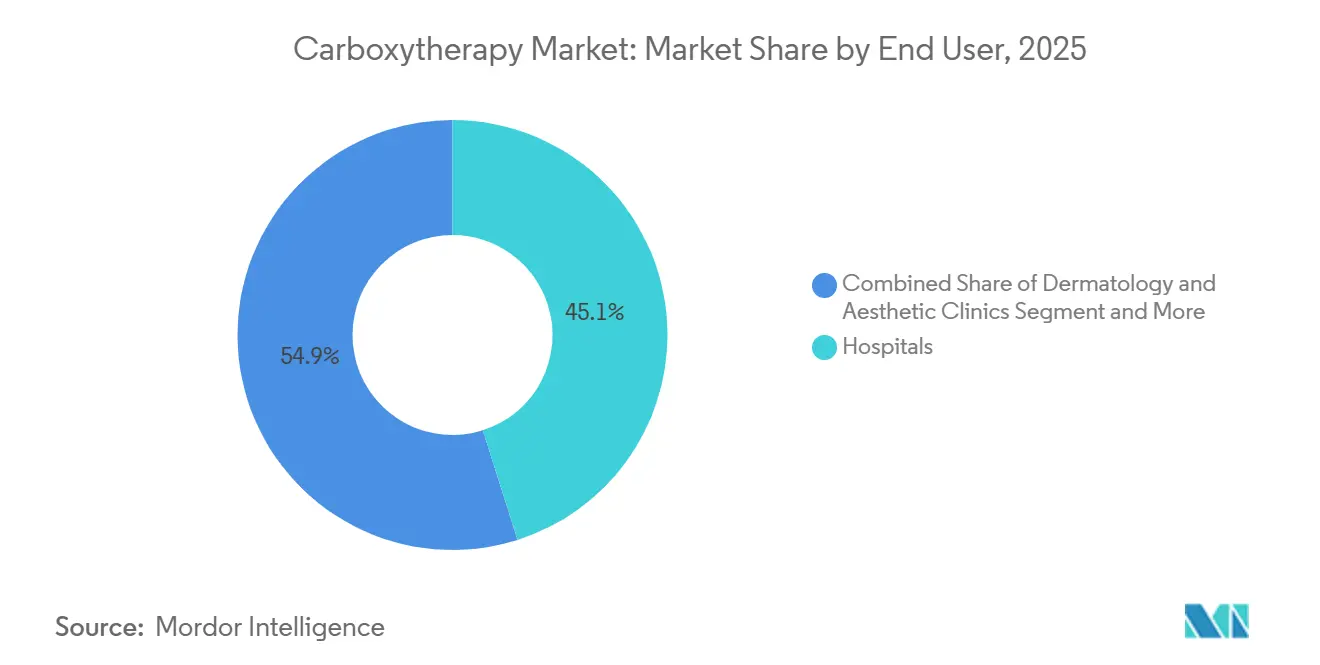

- By end user, hospitals generated 45.15% of 2025 revenue but wellness and beauty centers are set to grow at a 13.51% CAGR through 2031.

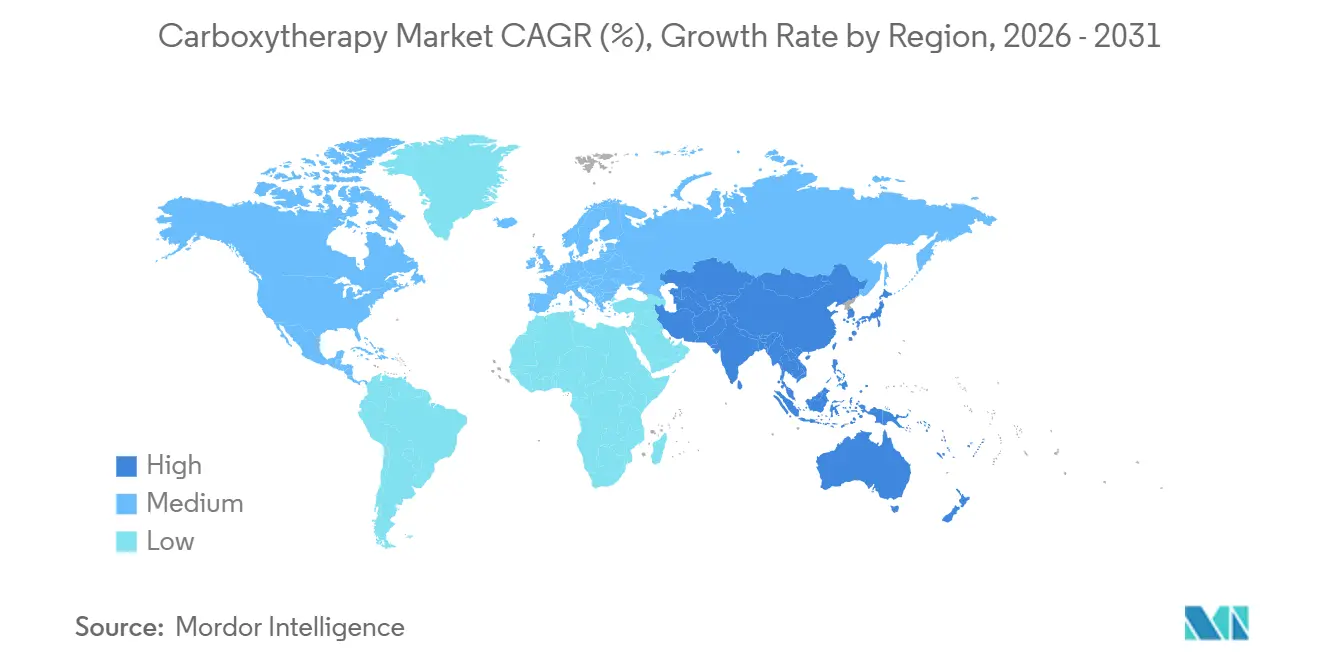

- By geography, North America led with 36.15% of 2025 revenue, and Asia-Pacific is projected to rise at a 12.51% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Carboxytherapy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Non-Invasive Aesthetic Procedures Post-COVID-19 | +2.3% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Rapid Adoption of Portable / Hand-Held CO₂ Devices | +1.8% | Asia-Pacific, Middle East, South America | Medium term (2-4 years) |

| Technological Advances in Micro-Needle and Automated Dosing | +1.5% | North America, European Union, Japan | Medium term (2-4 years) |

| Rising Anti-Aging Demand from the 40-65 Cohort | +2.1% | Global, marked in GCC and Europe | Long term (≥ 4 years) |

| Emerging Angiology Use-Cases | +2.4% | European Union, select Asia-Pacific | Long term (≥ 4 years) |

| AI-Enabled Dose Personalization | +1.4% | North America, European Union, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Non-Invasive Aesthetic Procedures Post-COVID-19

Elective procedure bookings rebounded sharply after travel restrictions eased, and carboxytherapy market participants capitalized on office-based treatments that require no general anesthesia. Saudi Arabia’s Vision 2030 health investments, coupled with a population where 63% are under 30, boost clinic volumes, while monthly beauty spend among Gulf women creates upsell potential for bundled packages[1]Vision 2030, “Healthcare Pillar Progress Update,” vision2030.gov.sa. In Western markets, social media showcases short-recovery procedures, prompting millennials to sample carboxytherapy between facial filler sessions. Clinics therefore position CO₂ therapy as a maintenance step that preserves results from neuromodulators. Across the United States, loyalty programs that pair carboxytherapy with skin-care subscriptions further cut churn and push lifetime value upward. The trend cements a durable demand floor for the carboxytherapy market.

Rapid Adoption of Portable/Hand-Held CO₂ Devices

Lower-priced portable units such as CarboMed Bluetooth and Carboxy-Pen remove a USD 10,000-30,000 cap-ex hurdle for small practices. Wellness tourism hubs in Thailand and South Korea rely on these devices to serve hotel-based clinics that rotate across resort chains. Bluetooth connectivity enables cloud logging, which satisfies emerging tele-supervision rules in Australia and Canada. Device-as-a-service leasing further de-risks entry for spa operators, ensuring that a wider provider base fuels steady cartridge demand. The portability shift therefore enlarges the total addressable carboxytherapy market.

Technological Advances in Micro-Needle & Automated Dosing

Automated flow control halves adverse events tied to manual pressure variation, a finding echoed in peer-reviewed dermatology audits. Micro-needle arrays deliver gas through painless channels, appealing to patients who fear injections. Patent activity in the United States and South Korea shows a pipeline of AI-assisted systems that adjust flow based on tissue impedance. Alma Lasers linked its Alma IQ software to carboxytherapy prototypes in 2025, giving multi-site chains a uniform protocol update mechanism[2]Alma Lasers, “Investor Presentation May 2025,” almalasers.com. Collectively, these upgrades cut operator training hours and broaden provider eligibility, thus accelerating the carboxytherapy market growth trajectory.

Rising Anti-Aging Demand from the 40-65 Cohort

As life expectancy increases, older consumers seek treatments that avoid the downtime of ablative lasers. Carboxytherapy stimulates microcirculation and collagen remodeling, making it a logical mid-tier solution between cosmeceuticals and surgery. Spending power in the 40-65 bracket is strongest in the United States and Western Europe, so clinics bundle CO₂ sessions with photobiomodulation to optimize skin texture. L’Oréal’s 2024 minority stake in Galderma demonstrates the merging of topical and in-office care paths, a convergence that the carboxytherapy market can leverage through cross-promotion. The demographic wave ensures sustained demand through 2031.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Hurdles & Heterogeneous Approvals | -1.6% | European Union, Japan, Brazil, China | Medium term (2-4 years) |

| High Capital Cost & Need for Trained Operators | -1.2% | Emerging Asia, South America, Middle East | Short term (≤ 2 years) |

| Competition from Fractional Lasers & RF Microneedling | -1.4% | North America, Europe, select Asia-Pacific | Short term (≤ 2 years) |

| CO₂ Cylinder Supply-Chain & Sustainability Concerns | -0.9% | Global, acute in South America and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Hurdles & Heterogeneous Device Approvals

The European Union requires sterile single-use consumables and rigorous post-market surveillance for non-medical injectables under Regulation 2022/2346. Brazil’s ANVISA demands Portuguese labeling plus a domestic legal representative, adding expense for foreign entrants. Japan’s PMDA still classifies invasive devices as Class III, so companies must submit detailed clinical dossiers. China shortened trial clearance to 30 days but stepped up manufacturing audits. Multi-country launches therefore stall unless firms run parallel regulatory teams, which weighs on smaller innovators and moderates overall carboxytherapy market expansion.

High Capital Cost & Need for Trained Operators

Table-top consoles cost up to USD 30,000, and emerging-market clinics struggle with financing. Portable models solve part of the problem but cannot match hospital throughput. Additionally, systematic reviews highlight adverse events when untrained staff exceed pressure thresholds. Mandatory certification courses in Germany and South Korea raise onboarding cost, steering solo estheticians to alternative modalities. Until price-per-treatment falls or leasing spreads further, budget sensitivity restrains uptake, especially outside tier-one cities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Portable Units Accelerate Multi-Site Expansion

Portable units drove a 13.25% CAGR forecast for 2026-2031, while table-top consoles maintained a 42.55% 2025 revenue share. The carboxytherapy market size for portable units is projected to double by 2031 as chain spas in Bangkok and Seoul lease Bluetooth-enabled guns that record every dose for compliance logs. Table-top systems remain staples in teaching hospitals where automated calibration allows back-to-back wound-care sessions. Still, hospitals are beginning to pilot hybrid fleets, pairing one high-throughput console with several satellite pens to serve overflow demand without facility expansion.

Device manufacturers now bundle cartridges, sterile tubing, and micro-needle tips into subscription kits that guarantee consumable revenue. Suppliers also preload treatment protocols for cellulite, under-eye circles, and vascular ulcers, reducing reliance on in-house trainers. As Brazilian notification pathways classify many portable systems as Class II, time-to-market shortens to roughly six months, expanding Latin American presence. Within Europe, stricter single-use requirements offset some cost advantages but enhance safety credentials, thus preserving provider confidence. Together, these trends embed portable platforms deeper into the carboxytherapy market.

By Application: Angiology Broadens Reimbursable Horizons

Angiology indications are forecast to grow at 14.15% through 2031 and may overtake aesthetics by revenue mid-decade. Health-economic models in France show limb-salvage savings of EUR 7,400 per patient when carboxytherapy accelerates ulcer closure. Payers in Germany and Japan now reimburse up to four sessions per chronic wound case, lifting hospital adoption. Conversely, aesthetic medicine keeps a sizeable foothold, accounting for 54.23% of the 2025 carboxytherapy market share, driven by cellulite and periorbital pigment reduction procedures.

Medical evidence for stretch-mark remodeling and alopecia remains limited, so device makers allocate R&D budgets to combination protocols that include hypochlorous acid and LED phototherapy. Clinics that serve both cosmetic and wound-care patients cross-utilize equipment to maximize utilization rates. Social media remains a potent demand catalyst on the aesthetic side, while peer-reviewed data underpins medical reimbursement narratives. The dual-track strategy cushions revenue volatility when discretionary spending wanes, reinforcing the carboxytherapy market.

By End User: Wellness Centers Outpace Hospitals

Wellness and beauty centers are on pace to post a 13.51% CAGR over 2026-2031, shrinking hospitals’ dominance. Portable guns priced under USD 2,000 allow day spas in Dubai and Jakarta to add CO₂ sessions without complex licensing. Pre-loaded dosing apps help non-medical staff meet safety thresholds, although regulatory bodies in the European Union still mandate remote physician supervision for invasive depth settings. Meanwhile, hospitals protect their niche by emphasizing reimbursable vascular cases and adopting table-top systems that process multiple limbs simultaneously.

Dermatology clinics balance both segments by offering package deals: aesthetic skin-polish sessions between wound-healing visits. Medical tourism operators in Thailand bundle carboxytherapy with recovery spa stays, leveraging low procedural cost to attract overseas clients. Home-use devices remain experimental because most jurisdictions classify gas injection as medical, not cosmetic. Unless consumer regulators recalibrate risk definitions, home penetration will stay minimal, keeping clinic foot traffic central to the carboxytherapy market revenue pool.

Geography Analysis

North America generated 36.15% of 2025 revenue, with insurers slowly evaluating coverage for diabetic ulcer applications. The U.S. FDA’s growing familiarity with gas-based modalities accelerates 510(k) clearances, but competition from RF microneedling means clinics scrutinize return on investment. Canada’s smaller population but high aesthetic spend per capita offers steady demand, while Mexican border clinics tap affluent U.S. travelers seeking lower procedure fees.

Asia-Pacific grows at a 12.51% CAGR, driven by China’s RMB 311.5 billion medical aesthetics sector, where non-surgical services hold a 38% share. South Korea handled 1.17 million foreign medical tourists in 2024, many booking combination laser and CO₂ packages. Japan’s PMDA dual-track review demands domestic clinical data, so early-mover Japanese firms leverage local studies to gain first approval. India’s rising middle class, coupled with a fast-expanding private hospital network, presents a medium-term upside once training pipelines mature.

Europe enforces strict MDR rules, inflating compliance cost but assuring product safety. Germany and France deploy carboxytherapy in university hospitals for vascular research, whereas Spain and Italy focus on aesthetic packages for inbound tourists. In the Gulf Cooperation Council, Saudi Arabia’s youth demographic and Vision 2030 healthcare build-out stimulate clinic openings. Latin America remains price-sensitive; Brazil’s ANVISA classification raises entry barriers, but high demand for cellulite treatment sustains core volumes. Africa’s adoption lags due to gas supply constraints, although South African luxury spas pilot portable devices tested under Europe’s CE mark.

Competitive Landscape

The field is moderately fragmented. Top five manufacturers together control significant percentage of global revenue. Alma Lasers leverages its Alma IQ platform to integrate dose analytics across multi-application consoles, while Air Liquide partners with device firms to supply low-carbon cylinders, converting sustainability into a buy-signal for hospital procurement teams. Alvi Prague and AAMS World disrupt incumbents by selling sub-USD 500 Bluetooth-enabled guns with app-based flow charts, grabbing share in fast-growing spa channels.

Patent filings show an uptick in AI-assisted micro-needle arrays that optimize depth in real time. L’Oréal’s dermatology alliance points to a future where topical cosmeceuticals and in-office CO₂ sessions form unified treatment plans. On the medical side, randomized controlled trials in Europe anchor payer negotiations, and firms able to co-fund studies win faster formulary placement. Sustainability now shapes bids, so SIAD Group’s recovered-gas portfolio gains preference in public tenders[3]SIAD Group, “Annual Report 2025,” siad.eu. Regional regulatory expertise becomes a must-have capability, favoring larger players able to sustain multi-jurisdiction project teams.

Carboxytherapy Industry Leaders

DTA Medical

Cosmo Pro

Carbossiterapia Italiana

Beijing Jontelaser Technologies

Alvi Prague

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Lumisque hosted Carboxy Couture during Paris Couture Fashion Week to position CO₂Lift as a premium adjunct for runway models.

- February 2025: Air Liquide stated its ECO ORIGIN line cut more than 10,000 tonnes of CO₂ across 120 hospitals, enhancing its standing with carbon-focused procurement teams.

Global Carboxytherapy Market Report Scope

As per the scope of the report, carboxytherapy is a non-surgical treatment that involves the injection of carbon dioxide (CO₂) gas into the skin or subcutaneous tissue. It is used to improve skin elasticity, reduce the appearance of cellulite, diminish stretch marks, and treat certain types of scars by stimulating blood flow and collagen production.

The segmentation for the carboxytherapy market by device type includes table-top systems, portable/hand-held systems, standalone/mobile units, and consumables & accessories. By application, the market is segmented into aesthetic medicine, dermatology (chronic wounds, psoriasis), angiology (peripheral vascular diseases), orthopedics & rheumatology, and others. The aesthetic medicine segment is further segmented into cellulite reduction, skin rejuvenation/anti-aging, stretch-mark reduction, dark under-eye circles, alopecia/hair regrowth, body contouring/fat reduction. By end user, the segmentation includes hospitals, dermatology & aesthetic clinics, wellness & beauty centers/spas, home-care settings, and other end users. By geography, the market is divided into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The Market Forecasts are Provided in Terms of Value (USD).

| Table-top Systems |

| Portable / Hand-held Systems |

| Standalone / Mobile Units |

| Consumables & Accessories |

| Aesthetic Medicine | Cellulite Reduction |

| Skin Rejuvenation / Anti-Aging | |

| Stretch-mark Reduction | |

| Dark Under-Eye Circles | |

| Alopecia / Hair Regrowth | |

| Body Contouring / Fat Reduction | |

| Dermatology (Chronic Wounds, Psoriasis) | |

| Angiology (Peripheral Vascular Diseases) | |

| Orthopedics & Rheumatology | |

| Others |

| Hospitals |

| Dermatology & Aesthetic Clinics |

| Wellness & Beauty Centers / Spas |

| Home-care Settings |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Device Type | Table-top Systems | |

| Portable / Hand-held Systems | ||

| Standalone / Mobile Units | ||

| Consumables & Accessories | ||

| By Application | Aesthetic Medicine | Cellulite Reduction |

| Skin Rejuvenation / Anti-Aging | ||

| Stretch-mark Reduction | ||

| Dark Under-Eye Circles | ||

| Alopecia / Hair Regrowth | ||

| Body Contouring / Fat Reduction | ||

| Dermatology (Chronic Wounds, Psoriasis) | ||

| Angiology (Peripheral Vascular Diseases) | ||

| Orthopedics & Rheumatology | ||

| Others | ||

| By End User | Hospitals | |

| Dermatology & Aesthetic Clinics | ||

| Wellness & Beauty Centers / Spas | ||

| Home-care Settings | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What was the global revenue for the carboxytherapy market in 2026?

It reached USD 137.46 million and is on track to more than double by 2031.

Which device category is expanding fastest?

Portable and hand-held units are growing at a 13.25% CAGR through 2031, outpacing table-top consoles.

Which application shows the strongest growth outlook?

Angiology indications such as peripheral vascular disease and diabetic wound care are projected to rise at 14.15% CAGR.

Why is Asia-Pacific considered a high-potential region?

China's large Gen Z consumer base, South Korea's medical tourism inflow, and streamlined Chinese regulatory timelines push regional growth to 12.51% CAGR.

How are sustainability demands affecting carboxytherapy providers?

Hospital buyers favor suppliers of low-carbon medical gases, prompting firms like Air Liquide to launch ECO ORIGIN cylinders that cut emissions by 70%.

What competitive advantage do AI-enabled devices offer?

Real-time dose personalization reduces operator variability, lowers retreatment rates, and provides remote update capabilities for multi-clinic chains.

Page last updated on: