Capillary Electrophoresis Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

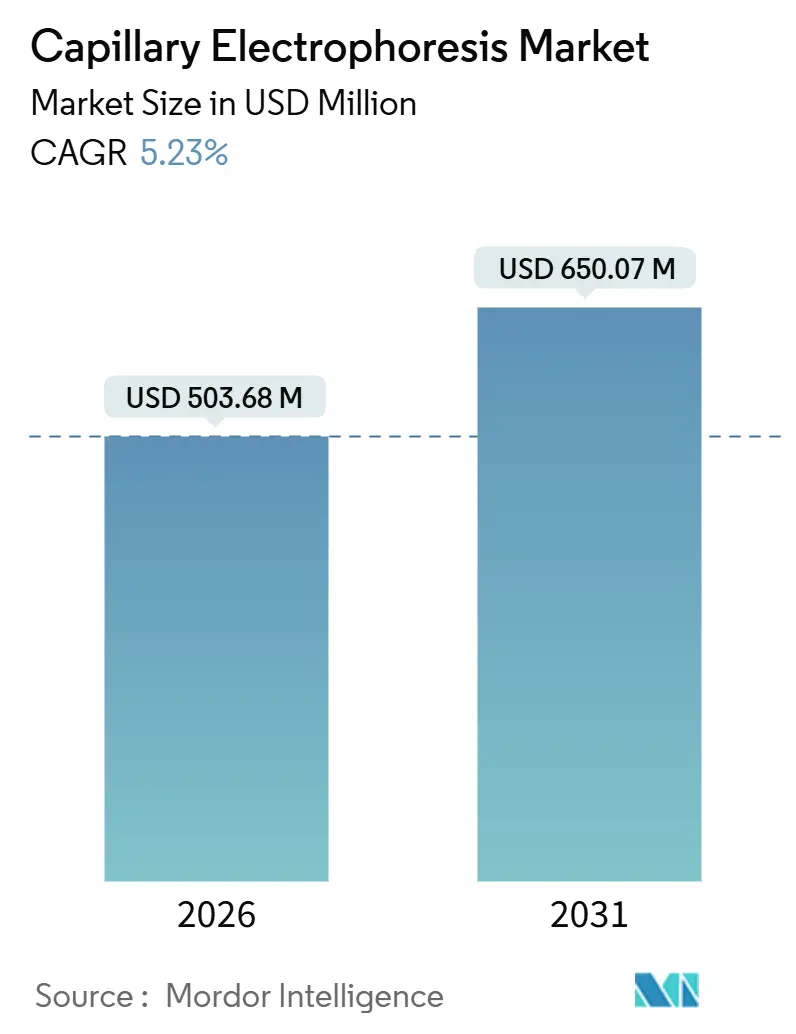

| Market Size (2026) | USD 503.68 Million |

| Market Size (2031) | USD 650.07 Million |

| Growth Rate (2026 - 2031) | 5.23% CAGR |

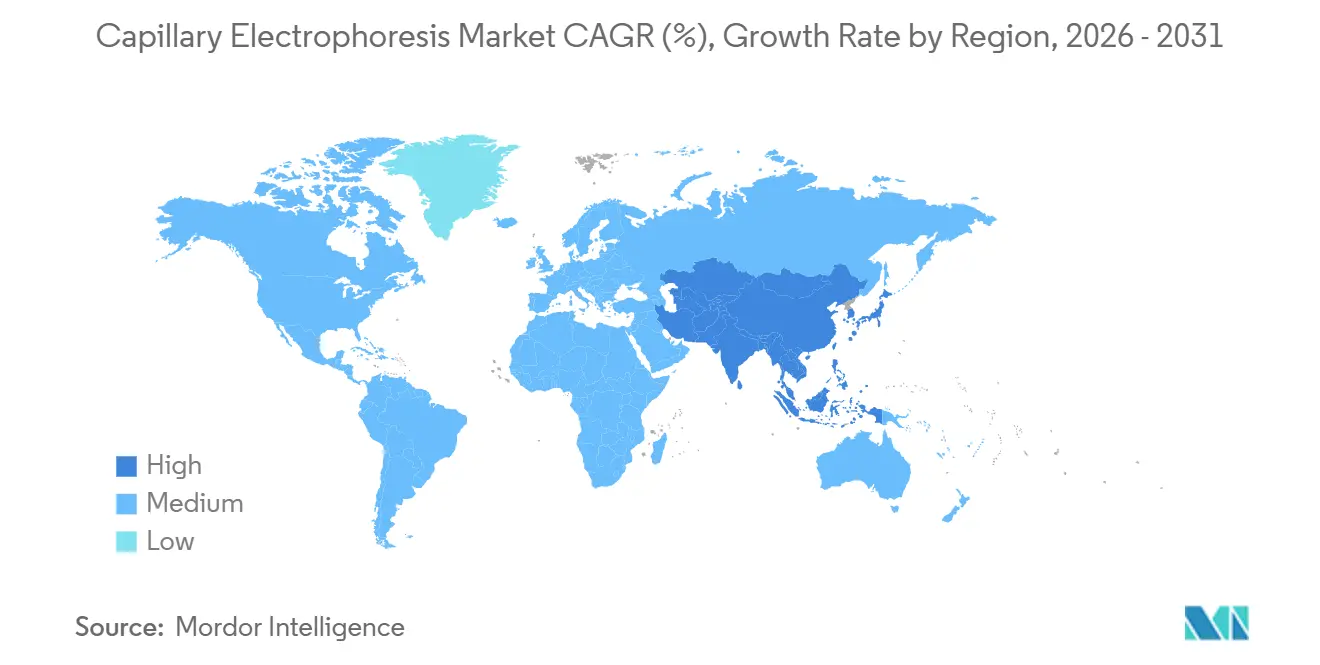

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Capillary Electrophoresis Market Analysis by Mordor Intelligence

The Capillary Electrophoresis Market size is estimated at USD 503.68 million in 2026, and is expected to reach USD 650.07 million by 2031, at a CAGR of 5.23% during the forecast period (2026-2031).

This expansion underscores a strategic shift from routine analytical separations toward high-value niches where speed, resolution, and minimal sample consumption outweigh cost advantages offered by liquid chromatography. Pharmaceutical and biotechnology companies continue to anchor demand, especially for monoclonal-antibody charge-variant profiling and oligonucleotide purity testing under tighter ICH Q6B oversight.[1]International Council for Harmonisation, “ICH Q6B Specifications: Test Procedures and Acceptance Criteria for Biotechnological/Biological Products,” ICH, ich.org Simultaneously, contract research organizations (CROs) are capturing outsourced bioanalytical workloads, amplifying the capillary electrophoresis market footprint across global hubs. Regulatory acceptance, such as FDA endorsement of CE-based purity assays for gene therapies and EMA approval of capillary isoelectric focusing under the IVDR, has validated the platform’s fit-for-purpose status in both therapeutics and diagnostics. North America dominates revenue, yet Asia-Pacific’s fast-track biosimilar filings and EU pesticide-residue rules are unlocking fresh adoption vectors that sustain momentum despite premium instrument pricing.

Key Report Takeaways

- By product type, automatic systems led with 39.64% revenue share in 2025, while consumables are advancing at an 8.38% CAGR through 2031.

- By mode, capillary gel electrophoresis commanded 35.37% of the capillary electrophoresis market share in 2025; capillary electrochromatography is projected to gain at a 9.47% CAGR to 2031.

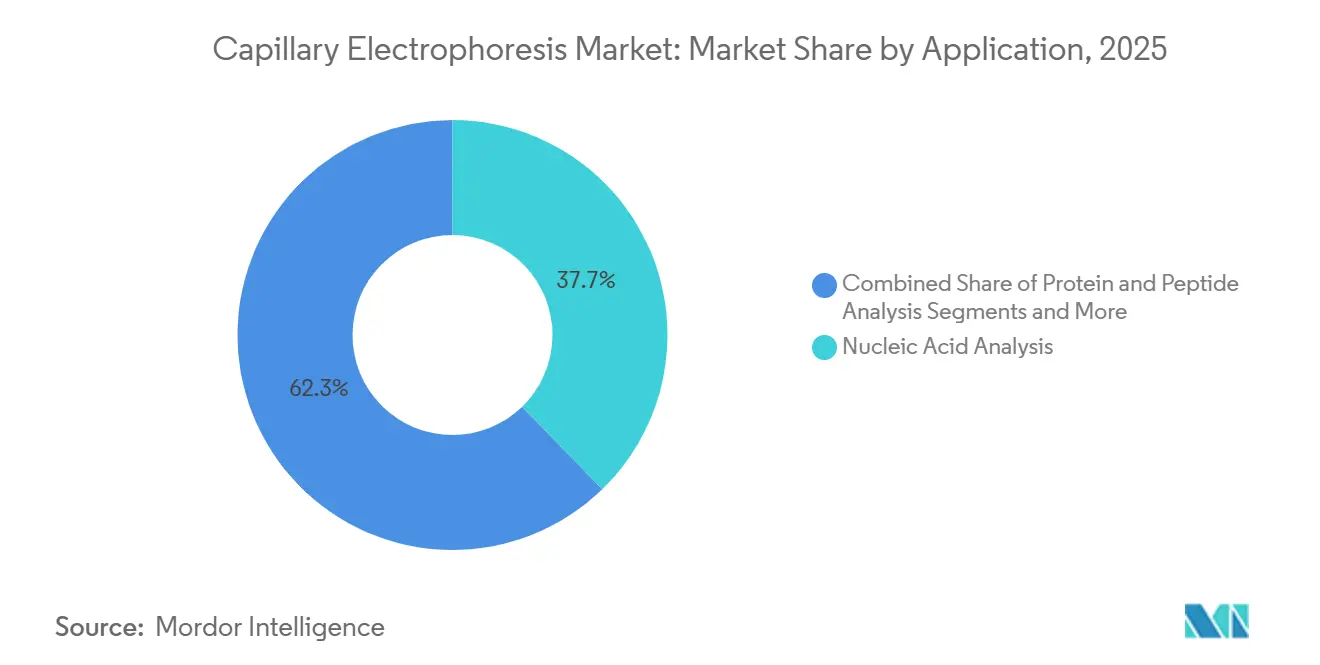

- By application, nucleic-acid analysis accounted for 37.73% share of the capillary electrophoresis market size in 2025, whereas environmental and food-safety testing is accelerating at an 8.62% CAGR through 2031.

- By end-user, pharmaceutical and biotech firms held 43.64% of 2025 revenue; CROs record the highest projected CAGR at 8.34% through 2031.

- By geography, North America held 36.26% of the capillary electrophoresis market share in 2025, while Asia-Pacific is forecast to post the fastest 7.89% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Capillary Electrophoresis Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration of CE with mass spectrometry for high-resolution proteomics & metabolomics | +1.2% | North America & Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Miniaturized and microfluidic CE enabling point-of-care and field diagnostics | +0.8% | Global, early adoption in North America & Asia-Pacific | Long term (≥4 years) |

| Automation demand from pharma/biotech for high-throughput screening | +1.4% | North America & Europe, spillover to Asia-Pacific | Short term (≤2 years) |

| Rising genomics and NGS fragment-analysis workloads | +1.0% | Global, concentrated in North America & Asia-Pacific | Medium term (2-4 years) |

| Improved capillary coatings and reagents boosting reproducibility | +0.9% | Global | Short term (≤2 years) |

| Expansion of CE into environmental and food-safety niches | +0.7% | Europe & Asia-Pacific, emerging in North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Integration of CE With Mass Spectrometry for High-Resolution Proteomics & Metabolomics

Coupling capillary electrophoresis to mass spectrometry transforms separations into discovery engines that reveal co-migrating isoforms and low-abundance metabolites invisible to UV detection. A 2024 Nature Scientific Reports study showed nano-CE-MS delivered 10-fold sensitivity gains for plasma peptidome profiling.[2]Cheng Jiang, “Nano-Capillary Electrophoresis–Mass Spectrometry Enables Deep Plasma Peptidome Profiling,” Nature Scientific Reports, nature.com Pharmaceutical developers use CE-MS to characterize antibody-drug conjugate heterogeneity, while clinical metabolomics labs quantify neurotransmitters in cerebrospinal fluid without pre-concentration. FDA biosimilar guidance favors orthogonal techniques, and CE-MS offers charge-state resolution unavailable with ion-exchange chromatography. Emerging single-cell metabolomics also relies on pico-liter CE-MS injections that preserve cellular heterogeneity.

Miniaturized & Microfluidic CE Enabling Point-of-Care and Field Diagnostics

Shrinking CE onto microfluidic chips detaches the platform from bulky hardware, creating rapid-test pathways for resource-limited settings. Agilent’s 2024 ProteoAnalyzer uses disposable cartridges that deliver protein-purity results in under 30 minutes, aligning with cell-therapy release timelines. Portable CE instruments quantify nitrates and heavy metals onsite for environmental regulators.[3]U.S. Environmental Protection Agency, “Portable Capillary Electrophoresis for On-Site Water Quality Monitoring,” EPA, epa.govHowever, chip-to-chip coating variability introduces migration-time drift that complicates ISO 17025 accreditation.

Automation Demand From Pharma/Biotech for High-Throughput Screening

High batch volumes in biologics manufacturing drive investment in multi-capillary instruments such as SCIEX’s BioPhase 8800, which runs 96 samples unattended and integrates seamlessly with 21 CFR Part 11 electronic records. Contract research organizations leverage automated platforms to shorten method-development cycles and offset skilled-labor shortages, a key differentiator in winning outsourced projects.

Rising Genomics & NGS Fragment-Analysis Workloads

Next-generation sequencing relies on CE-based fragment sizing to predict clustering efficiency and detect adapter dimers. Clinical genomics labs use CE analyzers to validate exome-library molarity before pooling, preventing sample under-representation. mRNA vaccine production employs capillary-gel electrophoresis for transcript integrity checks, and CE confirms CRISPR editing accuracy when Sanger sequencing lacks sensitivity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High instrument acquisition & maintenance costs versus HPLC/LC-MS alternatives | -0.9% | Global, acute in price-sensitive emerging markets | Short term (≤2 years) |

| Shortage of CE-skilled personnel in emerging markets | -0.6% | Asia-Pacific, Middle East & Africa, Latin America | Medium term (2-4 years) |

| Regulatory uncertainty for CE-based LDTs in clinical diagnostics | -0.5% | North America, spillover to Europe | Medium term (2-4 years) |

| Supply-chain fragility for specialty capillaries & coated consumables | -0.4% | Global, concentrated risk in Asia-Pacific hubs | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

High Instrument Acquisition & Maintenance Costs Versus HPLC/LC-MS Alternatives

Entry-level CE platforms cost USD 50,000–150,000, overlapping with UHPLC, yet owning CE incurs recurrent capillary and buffer expenses that can exceed HPLC mobile-phase costs by 20%–30%. Budget-sensitive CROs in India and China hesitate to adopt CE because method-transfer complexity erodes operating margins.

Shortage of CE-Skilled Personnel in Emerging Markets

Few university curricula cover electrokinetic theory, leaving labs to invest six-to-12 months in on-the-job training. A 2024 ANVISA audit showed 25% of CE-based submissions required revalidation due to operator errors. Vendor workshops mitigate gaps but cost up to USD 5,000 per attendee, an impediment for small labs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Consumables Outpace Automation Investments

Automatic systems contributed 39.64% of 2025 revenue, reflecting widespread adoption in pharmaceutical QC suites, yet the capillary electrophoresis market size for consumables is projected to expand at 8.38% CAGR because every instrument requires multiple capillary swaps each quarter, alongside proprietary buffer kits that sustain vendor lock-in. Software and services, though smaller, benefit from FDA’s 21 CFR Part 11 mandate for electronic batch records, driving upgrades to compliant data-management platforms.

Recurring consumable demand underpins vendor razor-and-blade strategies. ProteoAnalyzer microfluidic cartridges, priced at USD 15–20 per sample, eliminate cross-contamination but elevate assay costs—an acceptable trade-off in cell-therapy manufacturing where time-to-release is critical. Semi-automatic instruments attract budget-constrained academia, though variability in manual injections limits throughput to 40 daily samples, compared with 96-plus in fully-automated systems.

By Mode of Capillary Electrophoresis: CEC Gains as Hybrid Techniques Mature

Capillary gel electrophoresis maintained 35.37% of 2025 revenue, rooted in DNA-fragment and SDS-protein assays, but capillary electrochromatography is forecast to post the fastest growth at 9.47% CAGR as labs seek chiral separations without nano-HPLC complexity. Meanwhile, micellar electrokinetic chromatography fills the neutral-analyte gap by leveraging surfactant micelles, although method optimization challenges confine adoption to research settings.

Capillary zone electrophoresis remains the workhorse, appreciated for MS compatibility, while capillary isoelectric focusing persists in monoclonal-antibody charge-variant mapping. Technology convergence is accelerating: vendors now prototype capillary electrophoresis–ion mobility hybrids targeting ultra-complex samples, suggesting further mode diversification beyond 2030.

By Application: Environmental Testing Surges Amid Regulatory Mandates

Nucleic-acid analysis held 37.73% of 2025 revenue, yet environmental and food-safety testing is projected to grow at 8.62% CAGR on the back of EU glyphosate limits and PFAS monitoring demands. Protein and peptide analysis remains the second-largest segment, buoyed by biosimilar comparability studies that favor CE-SDS over size-exclusion HPLC due to superior resolution.

Fragment analysis underpins forensic STR profiling and agricultural genotyping, while clinical diagnostics—chiefly hemoglobin A1c and hemoglobinopathy testing—maintains steady uptake. Forensic toxicology laboratories continue to value 10-minute capillary-zone electrophoresis screens that satisfy court turnaround deadlines without compromising analytical rigor.

By End-User: CROs Capitalize on Outsourcing Wave

Pharmaceutical and biotechnology companies generated 43.64% of 2025 revenue, but CROs are set to outpace all other segments with an 8.34% CAGR through 2031 as sponsors shift risk-laden method development to specialists. Clinical labs remain stable, with CE adoption constrained by reimbursement ceilings, while academic institutes drive foundational CE-MS and microfluidics research that feeds commercial pipelines.

CRO expansion hinges on preferred-pricing agreements and data-integration services that streamline sponsor interactions. Instrument vendors nurture this channel through bundled reagent contracts and co-marketing, reinforcing a virtuous cycle of outsourcing growth.

Geography Analysis

North America led with 36.26% of 2025 revenue, anchored by FDA endorsement of CE assays for gene-therapy purity and NIH grants fueling single-cell metabolomics. Canada’s regulatory alignment and Mexico’s export-driven manufacturing bolster regional demand, though market maturation tempers growth.

Asia-Pacific is the fastest-growing geography at a 7.89% CAGR, spurred by China’s accelerated biosimilar approvals that mandate CE-based orthogonal data. India’s contract manufacturers scale automated platforms to secure global projects, while Japan leverages domestic vendors such as Shimadzu to support local pharmaceutical giants.

Europe benefits from IVDR-driven reproducibility standards that favor CE. Germany and France spearhead adoption, whereas the United Kingdom’s post-Brexit reagent-validation requirements introduce friction. Southern Europe and emerging Eastern European markets lag due to fiscal constraints, yet academic centers in Switzerland and Scandinavia drive CE-MS innovation.

Middle East & Africa and South America are smaller, fragmented markets where high import tariffs and talent shortages moderate adoption, although GCC modernization programs and ANVISA biosimilar guidelines spotlight niche growth pockets.

Competitive Landscape

Competitive intensity is moderate, but consumables remain less consolidated, giving niche coating specialists room to differentiate. SCIEX’s vertical integration of capillary production secures supply stability, while Agilent’s OpenLab CDS unifies CE, LC-MS, and GC data streams for regulated labs.

Product innovation clusters around throughput and miniaturization. Patent filings in 2024–2025 emphasized microfluidic designs, novel coatings, and CE-ion mobility couplings. Disruptors such as ProteinSimple’s imaged CIEF challenge incumbents by shrinking analysis times to under 10 minutes. Supply-chain fragility for specialty capillaries catalyzes selective M&A as larger players acquire coating vendors to insulate against disruptions.

Capillary Electrophoresis Industry Leaders

Thermo Fisher Scientific

Merck KGaA

Agilent Technologies

Danaher

Bio-Rad Laboratories

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Mirabo Biotechnology and CMP Scientific formed a partnership to co-develop an automated CE-MS solution for antibody clipping variants, creating the first end-to-end closed-loop workflow that links high-precision detection with AI-driven molecular redesign.

- March 2025: Thermo Fisher launched the Applied Biosystems SeqStudio Flex Dx Genetic Analyzer, an IVDR-compliant CE platform tailored for modern clinical labs.

- February 2024: Sysmex and Hitachi High-Tech agreed to co-develop capillary electrophoresis sequencer-based genetic-testing systems aimed at lowering costs and broadening clinical access.

Global Capillary Electrophoresis Market Report Scope

Capillary electrophoresis (CE) employs high-voltage electric fields to swiftly and efficiently separate ionic species, proteins, and DNA in a narrow capillary tube, all based on their charge-to-size ratio. This technique stands out for its high efficiency and low sample consumption.

The Capillary Electrophoresis Market Report is segmented by Product Type, Mode, Application, End User, and Geography. By Product Type, the market is segmented into Automatic Systems, Semi-automatic Systems, Consumables, and Software & Services. By Mode, the market is segmented into CZE, CGE, MEKC, CIEF, and CEC. By Application, the market is segmented into Nucleic Acid, Protein, Fragment Analysis, Clinical Diagnostics, Forensic, and Environmental. By End User, the market is segmented into Pharma/Biotech, Clinical Labs, Academic, and CROs. By Geography, the market is segmented into North America, Europe, Asia-Pacific, MEA, and South America. The market report also covers the estimated market sizes and trends across major regions globally. Market Forecasts are Provided in Terms of Value (USD).

| Automatic Systems |

| Semi-automatic Systems |

| Consumables (Capillaries, Reagents) |

| Software & Services |

| Capillary Zone Electrophoresis (CZE) |

| Capillary Gel Electrophoresis (CGE) |

| Micellar Electrokinetic Chromatography (MEKC) |

| Capillary Isoelectric Focusing (CIEF) |

| Capillary Electrochromatography (CEC) |

| Nucleic Acid Analysis (DNA, RNA, mRNA) |

| Protein & Peptide Analysis |

| Fragment Analysis & Genotyping |

| Clinical Diagnostics (HbA1c, Hemoglobinopathies, TDM) |

| Forensic & Toxicology Testing |

| Environmental & Food Safety Testing |

| Pharmaceutical & Biotechnology Companies |

| Clinical & Diagnostic Laboratories |

| Academic & Research Institutes |

| Contract Research Organizations (CROs) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Automatic Systems | |

| Semi-automatic Systems | ||

| Consumables (Capillaries, Reagents) | ||

| Software & Services | ||

| By Mode of Capillary Electrophoresis | Capillary Zone Electrophoresis (CZE) | |

| Capillary Gel Electrophoresis (CGE) | ||

| Micellar Electrokinetic Chromatography (MEKC) | ||

| Capillary Isoelectric Focusing (CIEF) | ||

| Capillary Electrochromatography (CEC) | ||

| By Application | Nucleic Acid Analysis (DNA, RNA, mRNA) | |

| Protein & Peptide Analysis | ||

| Fragment Analysis & Genotyping | ||

| Clinical Diagnostics (HbA1c, Hemoglobinopathies, TDM) | ||

| Forensic & Toxicology Testing | ||

| Environmental & Food Safety Testing | ||

| By End-User | Pharmaceutical & Biotechnology Companies | |

| Clinical & Diagnostic Laboratories | ||

| Academic & Research Institutes | ||

| Contract Research Organizations (CROs) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value for capillary electrophoresis solutions by 2031?

The segment is expected to reach USD 650.07 million by 2031, expanding at a 5.23% CAGR.

Which product category is set to post the quickest revenue growth?

Consumables are forecast to grow at an 8.38% CAGR as recurring demand for capillaries and proprietary reagents rises across installed instruments.

Why are contract research organizations investing heavily in capillary electrophoresis platforms?

Sponsors increasingly outsource complex bioanalytical method development, helping CROs secure an 8.34% CAGR through 2031 while freeing internal capacity for drug developers.

How do recent EU pesticide regulations influence environmental testing uptake?

Stricter residue limits for polar metabolites, especially glyphosate, are accelerating CE adoption because the technique delivers sub-10-minute separations without extensive solvent use.

Which analytical mode is projected to expand fastest over the next five years?

Capillary electrochromatography is poised to grow at a 9.47% CAGR as hybrid electrophoretic-chromatographic selectivity attracts labs handling chiral compounds.

What level of market concentration characterizes leading vendors?

The top five suppliers hold around 60% share, resulting in a moderate concentration score of 6, with room for niche coating and reagent innovators to gain ground.

Page last updated on: