Canada Timber Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

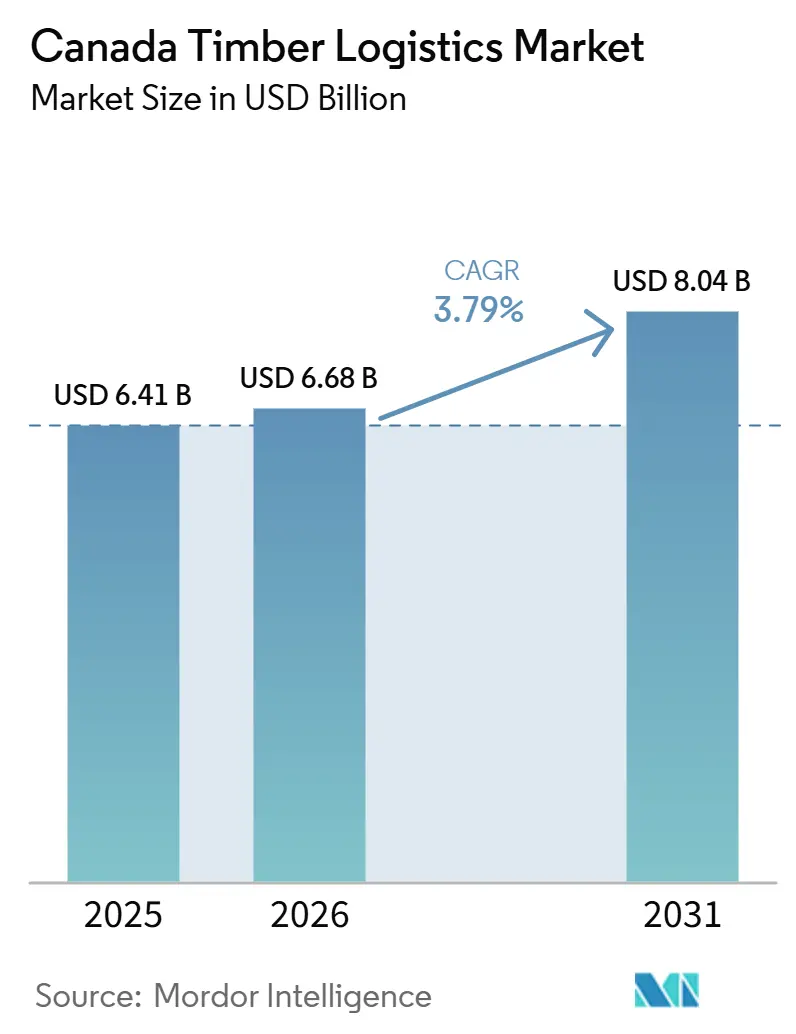

| Base Year Market Size (2025) | USD 6.41 Billion |

| Market Size (2026) | USD 6.68 Billion |

| Market Size (2031) | USD 8.04 Billion |

| Growth Rate (2026 - 2031) | 3.79% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Timber Logistics Market Analysis by Mordor Intelligence

The Canada timber logistics market size was valued at USD 6.41 billion in 2025 and estimated to grow from USD 6.68 billion in 2026 to reach USD 8.04 billion by 2031, at a CAGR of 3.79% during the forecast period 2026-2031.

The Canada timber logistics market is being reshaped by changes in export routes, the wider use of rail and intermodal freight, and tighter chain-of-custody expectations, which now influence how carriers, terminals, and shippers organize freight flows. United States countervailing and anti-dumping duties averaged 35.2% in 2025, and a 10% Section 232 tariff applied from October 2025 added further pressure on traditional cross-border lumber lanes, increasing the need to redirect volumes toward domestic and Asian destinations. That shift does not reduce logistics activity in a simple way, because longer routes, more handling points, and added port dependence increase spend per shipment and push the Canada timber logistics market toward more complex service models. Competitive advantage in the Canadian timber logistics market is therefore shifting toward operators that can combine corridor access, dependable capacity, digital documentation, and flexible multimodal execution under a single customer relationship.

Key Report Takeaways

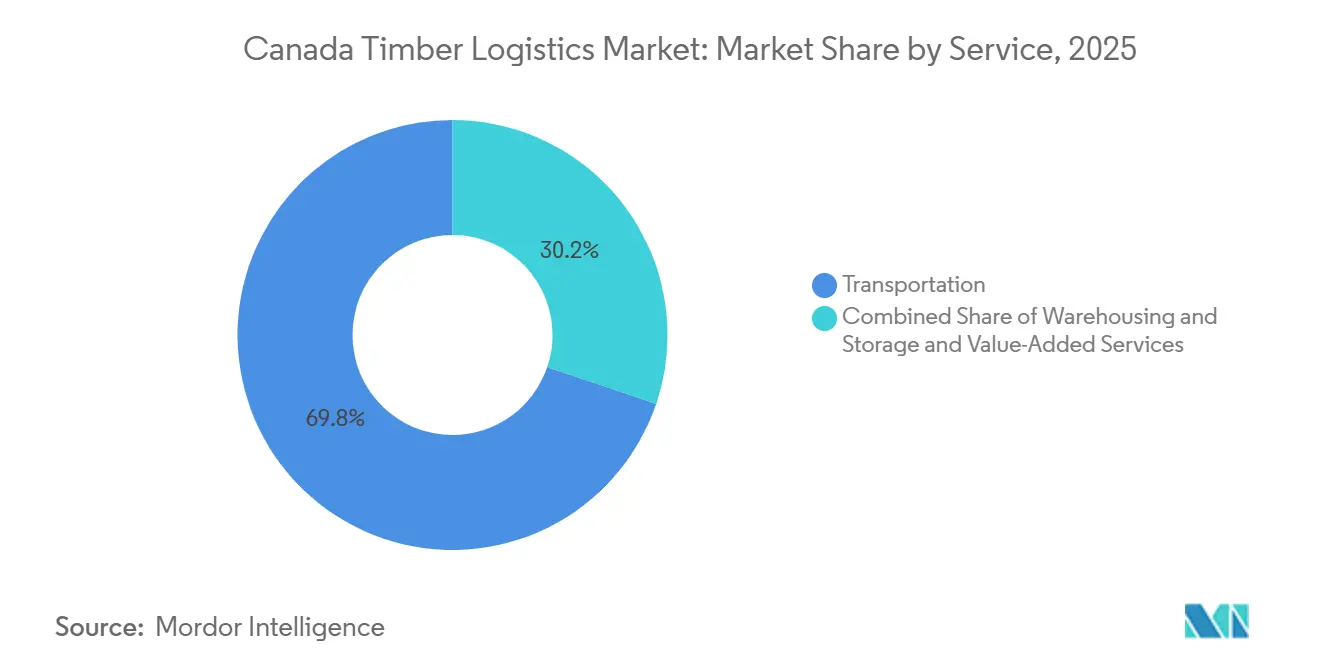

- By service, transportation held 69.81% share of the Canada timber logistics market size in 2025, while value-added services are forecast to expand at a 5.03% CAGR through 2031.

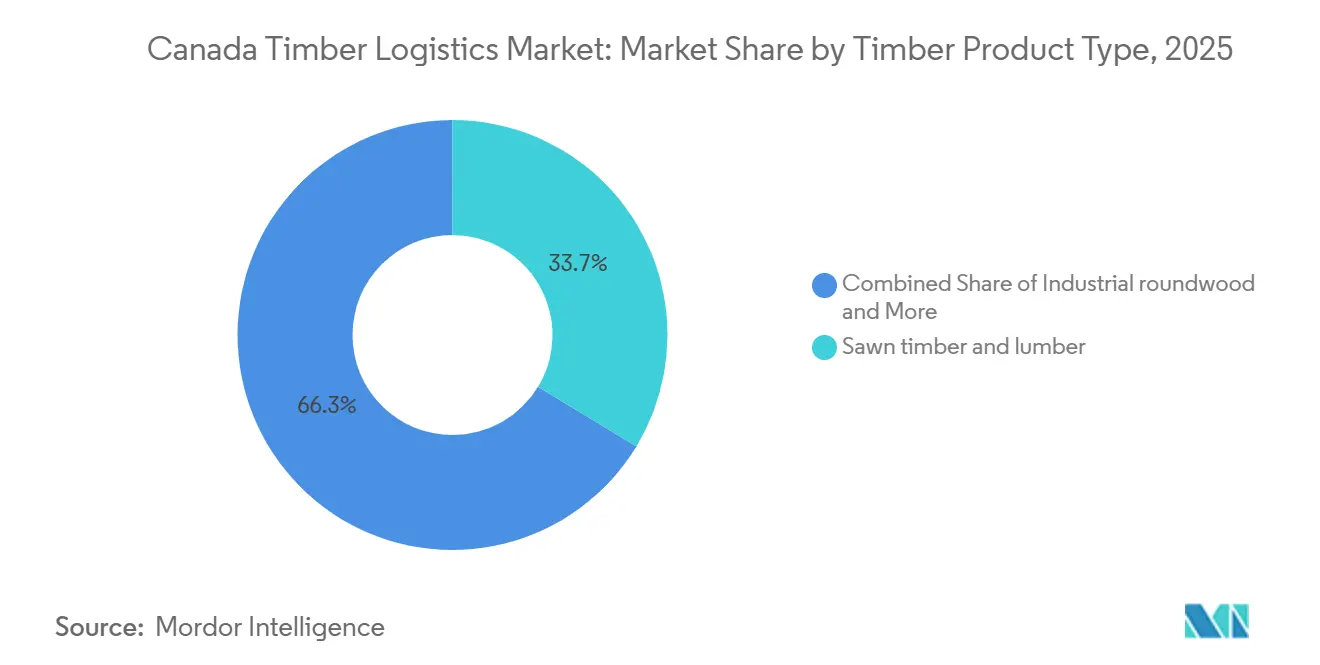

- By timber product type, sawn timber and lumber led with 33.67% market share in 2025, while engineered wood products are projected to grow at a 4.44% CAGR through 2031.

- By end-use industry, construction and infrastructure accounted for 51.03% of revenue in 2025, while the energy and biomass segment is expected to grow at a 4.24% CAGR through 2031.

- By geography, Western Canada held 40.53% of the Canada timber logistics market share in 2025, while Central Canada is forecast to expand at a 3.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Canada Timber Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Export Flow of Canadian Softwood and Pulpwood | +1.1% | Western Canada, Atlantic Canada, with spillover to Central Canada port corridors | Medium term (2-4 years) |

| Expansion of Forestry-Adjacent Industrial Hubs | +0.5% | Western Canada, especially Alberta Heartland, and Central Canada | Long term (≥ 4 years) |

| Rising Demand for End-to-End Timber Visibility and Chain-of-Custody Compliance | +0.4% | Global, with the strongest pull in British Columbia, Quebec, and Ontario | Short term (≤ 2 years) |

| Greater Use of Intermodal and Rail-Based Timber Movements | +0.6% | Western Canada to national ports and Central Canada corridors | Medium term (2-4 years) |

| Growth in Harvest Scheduling Optimization and Digital Dispatching | +0.3% | National, with early gains in British Columbia, Ontario, and Quebec | Short term (≤ 2 years) |

| Higher Demand for Weather-Resilient Winter Road and Remote Area Logistics | +0.3% | Northern Canada and remote British Columbia and Alberta corridors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Export Flow of Canadian Softwood and Pulpwood

The combined effect of countervailing duties, anti-dumping duties, and Section 232 measures has changed Canadian timber trade flows in a structural way, as export frictions with the United States now affect route design as much as final demand[1]RBC Economics, “Decades of Trade Disputes Reshape Canada’s Softwood Lumber Sector,” RBC, rbc.com. This has pushed producers to look more closely at Asian markets, domestic building programs, and more value-added production, broadening the range of destinations the Canada timber logistics market must serve. Longer export paths through Pacific gateways require more coordination between mills, truckers, rail carriers, terminals, and ocean shipping schedules, so logistics intensity rises even when physical tonnage does not increase at the same pace. The federal decision announced in December 2025 to work with railways to cut interprovincial lumber freight rates by 50% from Spring 2026 shows that transport costs have become a policy issue rather than solely a private operating issue. As a result, the Canada timber logistics market is seeing stronger demand for port-side staging, better vessel coordination, and more consistent origin-to-destination shipment control than the older United States-focused road model required.

Greater Use of Intermodal and Rail-Based Timber Movements

Canadian intermodal volumes reached a record level in April 2025, up 2.8% year over year, supporting the case for a larger rail role in the Canada timber logistics market[2]Statistics Canada, “The Daily, Railway Carloadings, April 2025,” Statistics Canada, statcan.gc.ca. Rail investment in Canada reached CAD 4.5 billion (USD 3.3 billion) in 2024, including track renewal, ties, and added capacity on corridors linked to major export gateways. Those network upgrades matter for timber because long-haul forest product lanes become more competitive when rail can handle heavier and more reliable flows into Vancouver and other terminal systems. The federal lumber freight initiative announced for Spring 2026 also strengthens the economic case for shifting selected corridors away from full reliance on roads toward combined truck-and-rail solutions. For the Canada timber logistics market, this means transportation providers that can connect forest pickup, terminal transfer, and linehaul rail service are likely to capture more of the higher-value freight relationships.

Rising Demand for End-to-End Timber Visibility and Chain-of-Custody Compliance

The European Union Deforestation Regulation required large operators and traders to comply by December 30, 2025, and smaller enterprises by June 30, 2026, meaning documentation has a direct effect on freight eligibility. That requirement means a shipment needs a traceable digital record from forest origin through transport movements to the final delivery point, rather than only basic proof at the shipping stage. Remsoft’s logistics tools are designed to synchronize load documentation across drivers, mills, and forest owners in near real time, which shows how digital paperwork is becoming part of the freight offer itself. Canada’s updated Group Chain of Custody eligibility criteria, expanded in 2025, widened the pool of smaller and mid-sized enterprises that now need transport partners with compatible systems. This gives larger logistics providers in the Canadian timber logistics market an advantage by allowing them to bundle haulage, traceability, and certification support into a single service package for exporters and mills.

Growth in Harvest Scheduling Optimization and Digital Dispatching

The Canada timber logistics market is placing greater emphasis on dispatch accuracy and harvest scheduling because driver scarcity and uneven raw material flows now pose direct production risk for mills. In May 2026, West Fraser Timber and Kodiak AI launched a pilot that deploys Kodiak Driver technology on Alberta resource roads to improve timber hauling consistency in a difficult labor environment. IBM and Polytechnique Montréal also launched a two-year program that combines digital twins, multi-objective optimization, machine learning, and quantum-enabled decision support for the forest supply chain. These tools can reduce avoidable empty miles, improve harvest planning, and tighten dispatch timing across widely dispersed forest operations that otherwise lose time through manual coordination. As adoption rises, the Canada timber logistics market should see better fleet utilization and more stable fiber movement in corridors where labor and road access conditions remain uneven.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Seasonality and Weather Disruption Across Remote Forest Corridors | -0.7% | Northern Canada and remote British Columbia and Alberta corridors | Short term (≤ 2 years) |

| High Diesel, Labor, and Equipment Maintenance Costs | -0.8% | National, with the sharpest pressure in British Columbia, Alberta, and Northern Canada | Medium term (2-4 years) |

| Truck Capacity Constraints in Peak Harvest and Export Windows | -0.5% | Western Canada and Central Canada | Short term (≤ 2 years) |

| Road Weight, Permitting, and Provincial Transport Compliance Complexity | -0.4% | National, with fragmented rules across Quebec, Ontario, and British Columbia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Diesel, Labor, and Equipment Maintenance Costs

Cost pressure remains a clear brake on the Canada timber logistics market because specialized forestry fleets operate in harsher conditions than standard freight fleets and cannot rotate equipment as easily across easier lanes. Labor pressure adds to that burden, as the sector has already seen material job losses in British Columbia's logging and sawmilling activities between December 2024 and December 2025[3]Vancouver Sun, “Employment Statistics Highlight Tough Times in B.C.’s Forestry Sector,” Vancouver Sun, vancouversun.com. Maintenance needs are structurally higher on remote resource roads, where rutting, icing, and limited service support shorten equipment life and increase the risk of downtime. That combination narrows margins for forest carriers and makes fleet expansion less attractive for new entrants that might otherwise add capacity. Even when freight demand is present, the Canadian timber logistics market cannot convert that demand into scalable capacity if operators remain cautious about hiring, asset replacement, and corridor commitments.

Seasonality and Weather Disruption Across Remote Forest Corridors

Climate variability is altering the operating calendar in the Canada timber logistics market because winter road access remains essential for many northern and remote forest corridors. In some Ontario corridors, winter road seasons have shrunk from an average of 77 days to as few as 28, sharply reducing the window for bulk fiber movement[4]Canada’s National Observer, “Driving the Ice Road, A Journey along a Community’s Disappearing Lifeline,” Canada’s National Observer, nationalobserver.com. The 2025 to 2026 season also saw late freezes and temperature swings of 20 °C or more in parts of the North, forcing operators to change load limits and schedules in real time. When short winter access periods overlap with peak shipment needs, mills and harvest operators can face long delivery delays, weakening confidence in time-sensitive supply arrangements. Federal support for long-horizon road solutions, including CAD 45 million (USD 32.6 million) in Budget 2024 for a Pikangikum First Nation highway connection, shows that this issue has no quick operational fix.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Transportation Volumes Underpin Revenue, Value-Added Services Lead Growth

Transportation accounted for 69.81% of the Canada timber logistics market share in 2025, confirming that physical movement from the harvest point to the mill or port remains the core revenue pool across the national network. Road transport remains the leading sub-segment within transportation because resource roads and dispersed forest sites still require truck access for pickup, short-haul movement, and mill delivery. Rail is most important on long-haul bulk corridors, especially when Western Canadian mills need to connect large outbound volumes to Vancouver and Prince Rupert export systems. Waterway and multimodal operations remain smaller, but they remain strategically relevant in coastal British Columbia and in export chains where a truck-only model no longer aligns with route economics.

Value-added services are projected to grow at a 5.03% CAGR from 2026 to 2031, making them the fastest-growing service category in the Canada timber logistics market. Growth is coming from digital tracking, chain-of-custody support, export compliance packaging, and documentation services that shippers increasingly want integrated into the transport contract. This changes buying behavior because mills and exporters now place greater value on fewer service handoffs and clearer audit trails throughout the freight process. The federal plan to reduce interprovincial lumber freight rates from Spring 2026 should also support more rail conversion inside the Canada timber logistics industry, while keeping transportation as the main revenue anchor and letting higher-margin support services grow around it.

By Timber Product Type: Sawn Lumber Anchors Volume, Engineered Wood Products Redefine Value Density

Sawn timber and lumber accounted for 33.67% of the Canada timber logistics market size in 2025, reflecting their central role in Canadian housing supply chains and in export-oriented forest product shipments. It remains the largest product category because it combines high shipment frequency with a broad customer base across domestic construction, cross-border trade, and offshore orders. Industrial roundwood, logs, and pulpwood streams remain closely tied to mill supply chains and therefore react quickly to changes in forest access, road conditions, and harvest timing. Pellets and briquettes serve a smaller base, but they are important for export logistics because they depend on rail staging, bulk storage, and coordination with tidewater terminals.

Engineered wood products are projected to expand at a 4.44% CAGR through 2031, making them the fastest-growing timber product category within the Canada timber logistics market. Federal procurement support for Canadian-made engineered wood products and IFIT-backed manufacturing investment are helping move this category from a niche freight stream toward a more mainstream one. This matters for logistics because engineered wood usually carries a higher value per shipment and needs more controlled handling, more reliable delivery windows, and better scheduling accuracy. The result is a steadier mix upgrade for the Canada timber logistics market, even as conventional lumber routes remain exposed to tariff-related volatility.

By End-Use Industry: Construction Demand Moderates, Energy and Biomass Emerges as a Faster-Growing Outlet

Construction and infrastructure commanded 51.03% of the Canada timber logistics market share in 2025, so building-related freight remained the largest source of end-use demand in the Canadian timber logistics market. CMHC expects new home construction to decline from 259,000 units in 2025 to 247,000 in 2026, and then to 223,000 in 2028, suggesting a softer near-term pace for residential timber movement. That moderation is most relevant in Ontario and British Columbia, where affordability pressures are weighing on new housing activity and, in turn, on some downstream demand for building materials. Pulp and paper, furniture, and packaging provide a more stable shipment base because they rely less on short-term housing momentum and more on recurring manufacturing and domestic consumption patterns.

Energy and biomass are projected to grow at a 4.24% CAGR through 2031, making this the fastest-growing end-use channel in the Canadian timber logistics market. Canada’s role as a wood pellet supplier to Asian utilities is supporting demand for specialized bulk handling, covered storage, and export-oriented rail-to-port movement. Compared with housing-linked timber flows, biomass shipments are less exposed to mortgage affordability cycles and can give carriers a useful outlet when residential construction cools. This makes biomass a balancing demand stream for the Canada timber logistics industry, especially in corridors that already connect inland production sites with coastal export infrastructure.

Geography Analysis

Western Canada held a 40.53% share of the Canadian timber logistics market in 2025, reflecting British Columbia's dominance in softwood production and Alberta's growing role in biomass and engineered wood manufacturing. British Columbia’s Interior remained a major source of softwood exports, and the disruption caused by United States tariffs has increased the importance of Vancouver and Prince Rupert corridors for rerouted flows. That shift is increasing reliance on rail staging, terminal coordination, and intermodal planning across the western portion of the Canada timber logistics market. In Alberta, the Sturgeon Terminal expansion, backed by a CAD 100 million (USD 72.3 million) loan, is expected to add 3,700 railcar storage and staging spaces by late 2026, strengthening the region’s handling capacity for chips, pellets, fiber, and other forest-linked loads.

Central Canada is projected to grow at a 3.92% CAGR through 2031, which makes it the fastest-expanding regional segment in the Canada timber logistics market. Quebec’s export-oriented pulp and paper base and Ontario’s rising interest in mass timber construction support a broader and more diversified freight base than in some single-product corridors. Ontario’s CN network includes Sarnia, Windsor, and Fort Erie among Canada’s top rail export crossings, providing shippers with strong access to both United States routes and domestic intermodal networks. That network density supports route flexibility and can reduce disruption when one corridor faces congestion or rate pressure. The IBM and Polytechnique Montréal initiative also points to rising investment in planning intelligence across Central Canadian forestry networks before a fuller freight recovery cycle takes hold.

Atlantic Canada and Northern Canada are smaller segments, but each has a distinct role in the Canada timber logistics market. In Atlantic Canada, the October 2025 Section 232 tariff pushed some New Brunswick producers to absorb USD 60 to USD 100 per load in broker and rerouting costs when a Maine pulp mill stopped taking imports. The federal government also invested CAD 2.8 million (USD 2 million), in February 2026 across seven Atlantic forestry innovation projects that include export diversification work tied to certification, logistics, and sustainability needs for non-United States. markets. Northern Canada remains the hardest operating environment because winter road interruptions and low Mackenzie River water levels have repeatedly narrowed the annual logistics window for remote communities and harvest operations.

Competitive Landscape

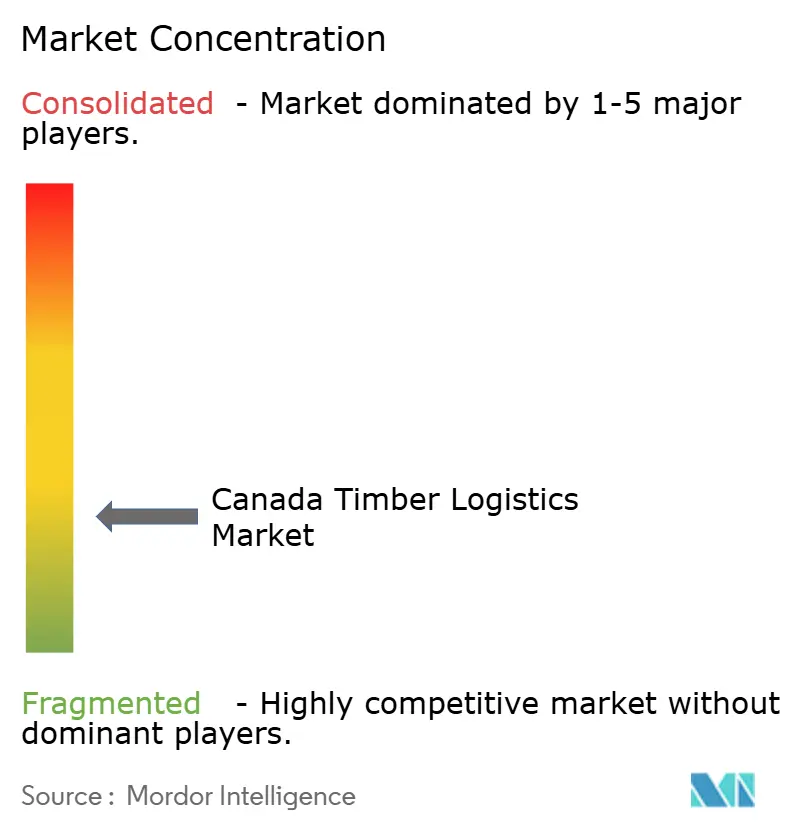

The Canada timber logistics market is fragmented among trucking operators and specialized forest service providers, keeping local competition active across many haulage lanes. Its upper layer is more concentrated because CN and CPKC dominate long-haul rail and intermodal movements that matter most for export corridors and large-volume forest products. That means competition is shaped less by simple price cutting and more by corridor access, network depth, asset availability, and the ability to connect truck pickup with rail and terminal service. It also leaves space for regional operators that understand remote roads, seasonal access rules, and northern operating conditions better than general freight carriers do.

Consolidation remains a visible strategy in the Canadian timber logistics market because scale helps operators spread equipment, labor, and compliance costs across more corridors and customers. In May 2026, Cando Rail & Terminals completed its acquisition of Savage Rail, which expanded its first-mile and last-mile rail operating services and terminal footprint across Canada and the United States. In February 2026, Mullen Group acquired the remaining 70% of Thrive Fluid Management Group, extending its position in northern Alberta industrial corridors that overlap with timber-linked freight demand. In May 2026, West Fraser Timber and Kodiak AI also launched an autonomous hauling pilot in Alberta, which shows that technology is becoming part of competitive positioning rather than a side project. Together, these moves show that network reach, corridor control, and operating technology are becoming more important than standalone linehaul capacity in the Canada timber logistics market.

Compliance is becoming another competitive filter because export-facing shippers increasingly need transport partners that can support traceability and chain-of-custody requirements without extra handoffs. Carriers that can provide auditable digital records across the full trip are better placed to win longer-term contracts with larger mills and exporters. Smaller carriers can still compete in local and remote haulage, but many will need partnerships with rail providers, terminals, or digital platforms to keep access to larger freight programs. The result is that the Canada timber logistics market is likely to remain fragmented in trucking while becoming harder to enter in export-oriented, intermodal, and compliance-heavy niches.

Canada Timber Logistics Industry Leaders

Canadian National Railway Company

Canadian Pacific Kansas City

Mullen Group Ltd.

Canada Cartage Logistics Solutions Inc.

TFI International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Cando Rail & Terminals completed the acquisition of Savage Rail from Savage Enterprises, LLC, establishing itself as North America's market leader in first and last-mile rail operating services and terminal infrastructure, with a significantly expanded footprint across the United States and Canada. The transaction positions Cando to serve forest product and industrial commodity flows across an enlarged multi-terminal network.

- May 2026: West Fraser Timber and Kodiak AI announced a pilot deployment of Kodiak's autonomous Driver technology for log hauling on remote resource roads in Alberta, targeting the industry-wide driver shortage and improving the consistency of raw material supply to mills. The first phase will transport timber from forest sites to a West Fraser Alberta processing facility.

- February 2026: Mullen Group Ltd. acquired the remaining 70% of Thrive Fluid Management Group Ltd., effective February 1, adding fluid management logistics capabilities adjacent to Northern Alberta timber and energy corridors, with the broader acquisition strategy expected to drive record 2026 group revenues.

- December 2025: The Government of Canada announced that it would work with Canadian railways to reduce interprovincial freight rates for lumber and steel by 50%, beginning in Spring 2026, as part of a broader package of measures.

Canada Timber Logistics Market Report Scope

| Transportation | Road |

| Rail | |

| Waterway | |

| Multimodal | |

| Warehousing and Storage | |

| Value-Added Services |

| Industrial roundwood / logs |

| Fuelwood & biomass |

| Sawn timber & lumber |

| Engineered wood products |

| Pulpwood, chips, and fibre |

| Pellets and briquettes |

| Other Timber Types |

| Construction & Infrastructure |

| Pulp & Paper Industry |

| Furniture Manufacturing |

| Packaging Industry |

| Energy & Biomass Industry |

| Other End-Use Industries |

| Western Canada (West Coast & Prairie provinces) |

| Central Canada |

| Atlantic Canada |

| Northern Canada |

| By Service | Transportation | Road |

| Rail | ||

| Waterway | ||

| Multimodal | ||

| Warehousing and Storage | ||

| Value-Added Services | ||

| By Timber Product Type | Industrial roundwood / logs | |

| Fuelwood & biomass | ||

| Sawn timber & lumber | ||

| Engineered wood products | ||

| Pulpwood, chips, and fibre | ||

| Pellets and briquettes | ||

| Other Timber Types | ||

| By End-Use Industry | Construction & Infrastructure | |

| Pulp & Paper Industry | ||

| Furniture Manufacturing | ||

| Packaging Industry | ||

| Energy & Biomass Industry | ||

| Other End-Use Industries | ||

| By Geography | Western Canada (West Coast & Prairie provinces) | |

| Central Canada | ||

| Atlantic Canada | ||

| Northern Canada |

Key Questions Answered in the Report

What is the projected value of Canada timber logistics by 2031?

The Canada timber logistics market is forecast to reach USD 8.04 billion by 2031 from USD 6.68 billion in 2026, reflecting a 3.79% CAGR over 2026 to 2031.

Which service category contributes the most revenue in Canada timber logistics?

Transportation remains the largest service category, accounting for 69.81% of revenue in 2025 because timber still depends on truck pickup, mill delivery, and port-linked movement.

Which timber product type is growing the fastest in Canada?

Engineered wood products are projected to grow at a 4.44% CAGR through 2031, helped by federal support for Canadian-made engineered wood and new advanced manufacturing capacity.

Why is Western Canada the leading regional contributor?

Western Canada held 40.53% of revenue in 2025 due to British Columbia’s large softwood base, Alberta’s expanding biomass and engineered wood activity, and strong connections to Pacific export corridors.

What is driving more demand for digital tracking in timber transport?

EUDR compliance deadlines and wider chain-of-custody adoption are making auditable shipment records essential, so mills and exporters increasingly want digital traceability bundled with haulage.

What is the main operating challenge for remote timber corridors in Canada?

Shorter winter road seasons and weather volatility are reducing reliable access windows in northern routes, which raises scheduling risk and can delay bulk fiber movement for months.

Page last updated on: