Canada Social Commerce Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

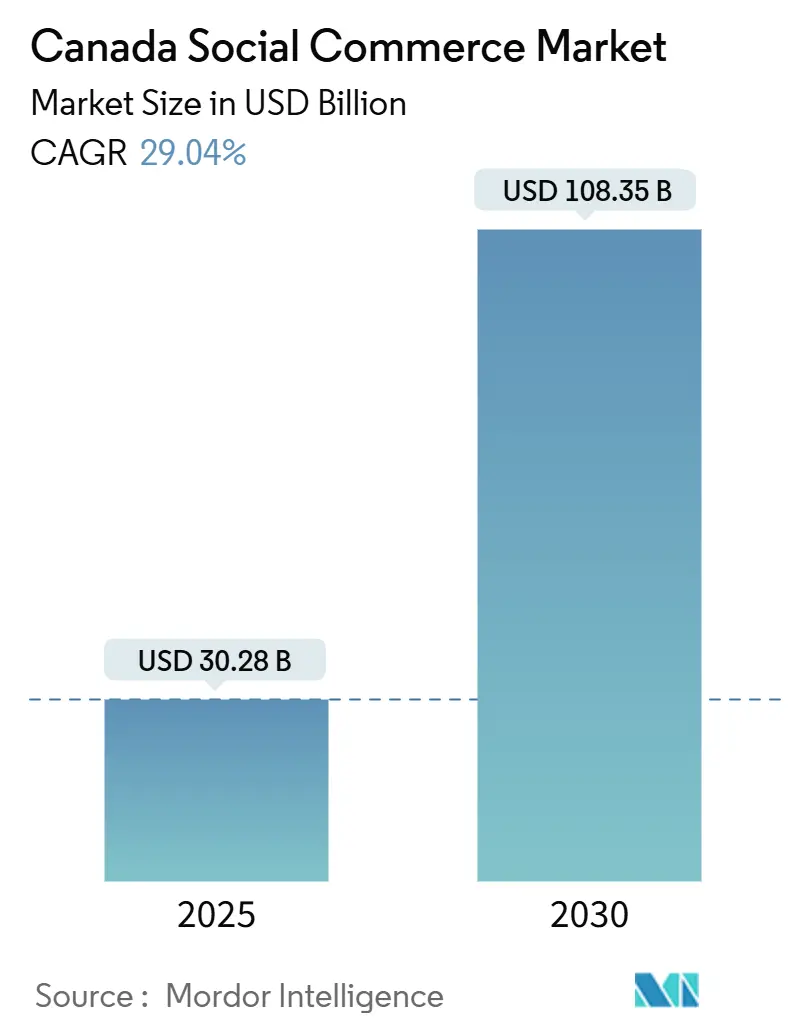

| Market Size (2025) | USD 30.28 Billion |

| Market Size (2030) | USD 108.35 Billion |

| Growth Rate (2025 - 2030) | 29.04% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Social Commerce Market Analysis by Mordor Intelligence

The Canada Social Commerce market size stands at USD 30.28 billion in 2025 and is forecast to reach USD 108.35 billion by 2030, reflecting a robust 29.04% CAGR. Driven by mobile-first shopping habits, video-centric discovery, and streamlined in-app checkout flows, the Canada social commerce market is scaling faster than traditional e-commerce. In 2024, smartphone transactions dominated social purchases, reflecting the growing reliance on mobile devices for commerce. Similarly, video commerce has emerged as a significant channel, emphasizing the shift toward visual and interactive formats in the market. Regulatory measures promoting secure Interac-enabled payments, along with well-established same-day logistics networks spanning from Vancouver to Halifax, provide the necessary infrastructure to support consistent growth in the sector. Competition remains moderate, with Shopify enabling a large number of domestic merchants to establish social storefronts. Meanwhile, global players such as Meta, ByteDance, and Amazon are actively working to integrate creator monetization and streamlined payment solutions.

Key Report Takeaways

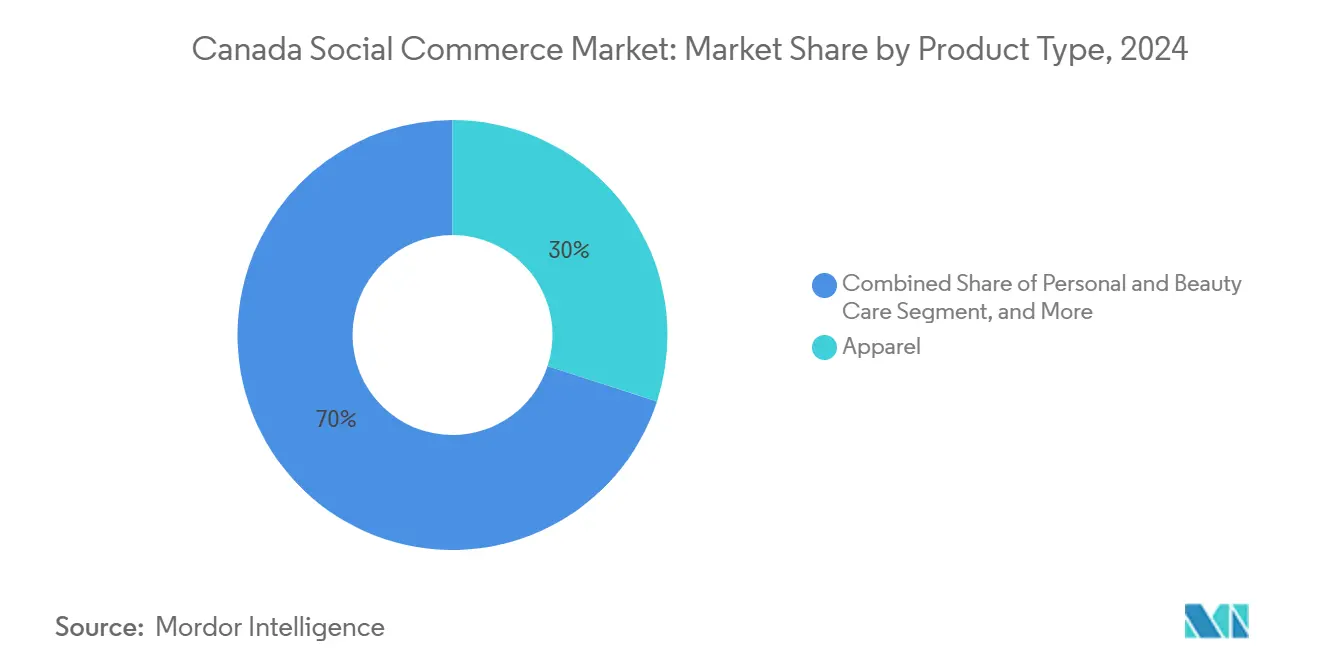

- By product type, apparel led with 29.77% of the Canada social commerce market share in 2024, whereas personal and beauty care is projected to grow at a 29.13% CAGR through 2030.

- By device, smartphone transactions accounted for 91.11% of the Canada social commerce market size in 2024, and this category is forecast to widen at a 29.23% CAGR to 2030.

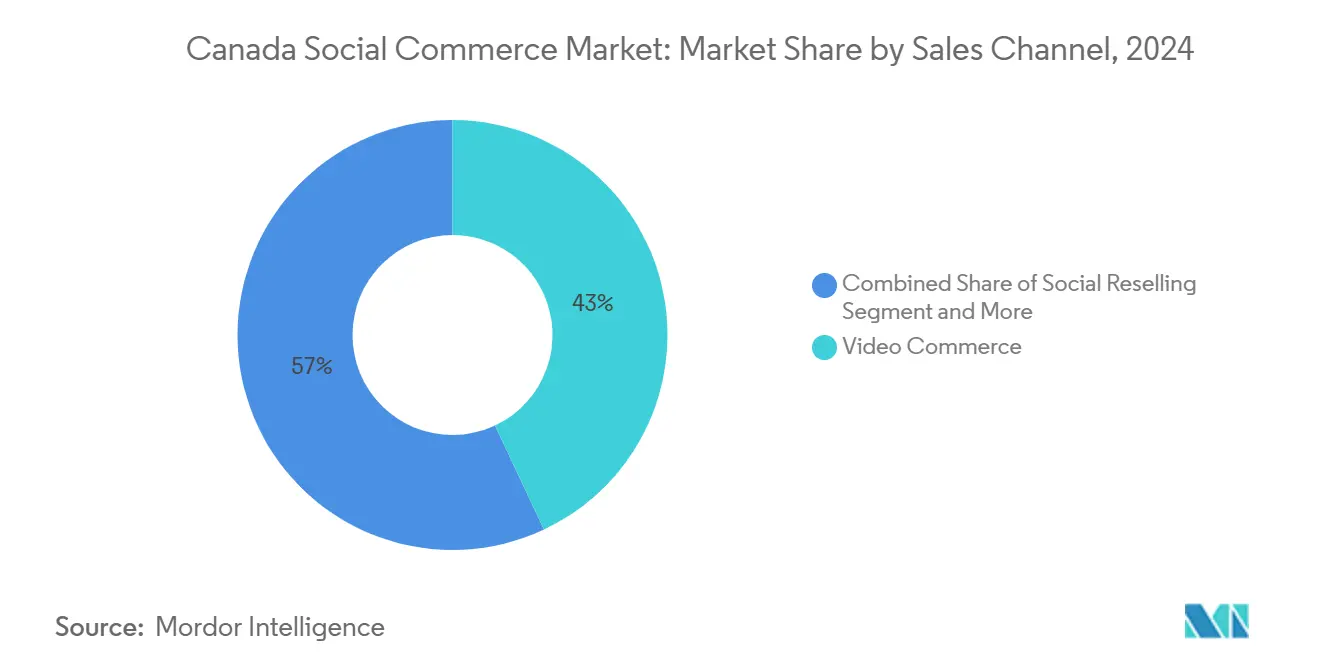

- By sales channel, video commerce captured 43.21% revenue share in 2024, while social reselling is advancing at a 31.01% CAGR through 2030.

Global valuation is built by aggregating outputs from multiple countries and regions, with Canada being one of the contributors. Our global social commerce market size represents that cumulative total.

Canada Social Commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise of in-app check-out features | + 6.2% | National, with early gains in Toronto, Vancouver, Montreal | Medium term (2-4 years) |

| Growth of mobile-first millennials' share of retail spend | + 7.8% | National | Long term (≥ 4 years) |

| Increasing ad-to-purchase conversion tracking by platforms | + 4.1% | National | Short term (≤ 2 years) |

| Expansion of creator-brand partnerships | + 5.3% | National, concentrated in urban centers | Medium term (2-4 years) |

| Canada-wide rollout of Interac-enabled social payments | + 3.7% | National | Short term (≤ 2 years) |

| Cross-border US micro-brands targeting Canada via TikTok | + 2.9% | National, stronger in border provinces | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rise of In-App Checkout Features

Platform-native payment flows have effectively reduced cart abandonment rates, which were previously a significant challenge. For example, Meta's Instagram Checkout, integrated with Canadian processors, has improved completion times compared to traditional browser-based flows.[1]Shopify, “Social Commerce Solutions for Canadian Merchants,” shopify.com Similarly, Apple Pay and Google Pay, when utilized within social apps, enhance conversions by providing users with a familiar interface. Shop Pay, with its streamlined one-click feature, supports Canadian merchants by simplifying impulse purchases of fashion and beauty items, offering a more efficient alternative to older web store processes. Additionally, compliance with the Payment Card Industry Data Security Standard ensures trust and maintains transaction efficiency.

Growth of Mobile-First Millennials' Retail Spend

Millennials aged 28-43 significantly contribute to retail spending and primarily initiate their purchases through mobile devices. Their familiarity with social checkouts is driving growth in Canada's social commerce market. Brands that focus on visual storytelling tailored to this demographic achieve stronger conversion rates. In 2024, Aritzia reported a notable portion of its online revenue originating from referrals via Instagram and TikTok. As Gen Z's earning potential increases, they are expected to further accelerate this trend. Additionally, research from the Bank of Canada indicated widespread adoption of mobile payments among millennials last year.

Increasing Ad-to-Purchase Conversion Tracking

In 2024, Canadian retailers utilizing advanced attribution through Meta's Conversions API and TikTok's Events API enhanced cost-efficiency and improved budget allocation. These tools connect social media impressions directly to completed transactions, enabling marketers to make data-driven budget decisions. Additionally, by integrating first-party data from loyalty programs with platform pixels, retailers are able to implement dynamic pricing and personalized product recommendations while adhering to the privacy requirements introduced by iOS 14.5.

Expansion of Creator-Brand Partnerships

Influencer marketing has transitioned from occasional endorsements to structured revenue-sharing models that align creator incentives with brand objectives. In Canada, mid-tier creators typically earn between CAD 500 and 2,000 per post, while macro-influencers command higher compensation per campaign.[2]Canadian Radio-television and Telecommunications Commission, “Digital Platform Regulations,” crtc.gc.ca In 2024, Shopify Collabs facilitated numerous partnerships across Canada, contributing significantly to sales. Lululemon's ambassador network exemplifies the value of long-term collaboration in driving social commerce revenue.[3]Lululemon, “Ambassador Network Performance,” lululemon.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy tightening under Bill C-27 | -3.8% | National | Short term (≤ 2 years) |

| Counterfeit goods and consumer trust issues | -2.1% | National | Medium term (2-4 years) |

| Rising unit economics for same-day delivery | -1.7% | Urban centers, particularly Toronto, Vancouver | Short term (≤ 2 years) |

| Fragmented provincial sales-tax compliance | -1.4% | National, varying by province | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data-Privacy Tightening Under Bill C-27

Under the Consumer Privacy Protection Act, platforms must secure explicit user consent for data usage beyond essential services. This move aims to limit the detailed targeting that enhances the efficiency of social commerce. Furthermore, platforms are required to adopt 'privacy-by-design' systems and facilitate user-initiated data deletions. Depending on their scale, compliance costs can vary significantly, ranging from CAD 50,000 to CAD 500,000.[4]Parliament of Canada, “Bill C-27 Consumer Privacy Protection Act,” parl.ca While challenges like consent fatigue and diminished ad precision are evident initially, the potential for increased consumer trust could yield substantial long-term benefits.

Counterfeit Goods and Consumer Trust Issues

In 2024, the Royal Canadian Mounted Police (RCMP) observed a significant rise in the seizure of counterfeit items associated with social transactions, impacting buyer confidence.[5]Royal Canadian Mounted Police, “Counterfeit Goods Enforcement Statistics,” rcmp-grc.gc.ca Complaints primarily focused on fashion accessories, electronics, and beauty products, with numerous consumers reporting fraud to federal agencies. Although stricter seller-verification programs increase onboarding costs and may pose challenges for smaller merchants, these measures are considered vital for maintaining the integrity of Canada's social commerce market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Apparel Leads Despite Beauty’s Acceleration

Apparel controlled 29.77% of the Canada social commerce market in 2024, retaining clear leadership thanks to mature supply chains and high visibility on fashion-centric platforms. Personal and beauty care, however, is scaling at a 29.13% CAGR, narrowing the gap as makeup tutorials and skincare routines turn views into purchases within minutes. Sephora's integration with Instagram Shopping has demonstrated higher conversion rates compared to web-only funnels. Accessories are frequently purchased on impulse, while home products are experiencing increased demand, supported by décor influencers showcasing curated spaces on Pinterest. Meanwhile, health supplement vendors operate under strict oversight from Health Canada, prioritizing consumer safety over scalability. In the food and beverage sector, artisanal labels are gaining attention by emphasizing local sourcing through storytelling and adhering to regulations from the Canadian Food Inspection Agency to build consumer trust.

In the coming years, while apparel volumes are expected to grow, the beauty sector's faster growth rate indicates it may surpass apparel in Canada's social commerce market. Brands that integrate creator routines with streamlined purchasing processes are likely to achieve significant advantages. Beyond the leading categories, accessories are expected to retain strong profit margins due to low return rates. Home products are anticipated to leverage AR-enabled visualization to address consumer hesitations regarding high-touch items. Food sellers are positioned to benefit from advancements in same-day cold-chain logistics, while compliant supplement manufacturers are expected to rely on expert-led video content to substantiate product efficacy.

By Device: Smartphone Supremacy Reshapes Commerce

Smartphones generated 91.11% of social commerce purchases last year, reflecting an entrenched mobile-first culture across Canada. The category will register a 29.23% CAGR through 2030, powered by 5G expansion and frictionless mobile wallets. While laptops and desktops remain relevant for conducting detailed research on high-consideration items, their role in the Canadian social commerce market is gradually declining. This shift aligns with the growing preference for AR and AI-driven shopping assistants on handheld devices.

Digital payment platforms integrated into mobile ecosystems are facilitating faster checkouts, streamlining the purchasing process for a significant portion of consumers. Additionally, the practice of discovering products on mobile devices and completing purchases on desktops is becoming less common as social applications continue to enhance their catalog and payment capabilities. This evolution is exerting pressure on traditional web storefronts to adopt the convenience and functionality now prevalent in mobile ecosystems.

By Sales Channel: Video Commerce Transforms Discovery

Video commerce captured 43.21% revenue share in 2024, demonstrating unrivaled effectiveness at linking storytelling to purchase. In Canada, social commerce emphasizes the use of unboxing videos, short-form try-ons, and live Question and Answer sessions. These formats, including livestream events, shoppable Reels, and tutorial clips, enable audiences to observe, inquire, and make purchasing decisions in real-time, effectively supporting products that require demonstration.

Social reselling leads growth with a 31.01% CAGR, propelled by consumer interest in sustainable buying and community validation. Within six months of its launch, Poshmark expanded its user base in Canada. While Instagram Shopping and Facebook Marketplace remain key players in social-commerce, group buying has established a presence, particularly for bulk goods. Additionally, product review platforms enable buyers to assess items thoroughly before making a purchase. This aligns with findings indicating that shoppers often consult multiple sources prior to buying decisions.

Geography Analysis

In 2024, Toronto, Vancouver, and Montreal emerged as key contributors to Canada's social commerce market. These cities feature concentrated populations of millennials and Gen Z, supported by advanced fiber and 5G infrastructure, along with efficient delivery networks capable of same-day service. Vancouver's technology corridor and proximity to Asian brands facilitate cross-border sales, particularly in electronics and fashion, targeting North American consumers.

Quebec enforces French-language consumer protection disclosures and implements distinct sales-tax collection regulations, requiring platforms to incorporate multilingual interfaces and ensure compliance with provincial standards. In British Columbia, sellers must automate tax remittance at checkout to comply with the Provincial Sales Tax. Atlantic Canada, with Halifax at the forefront, is experiencing rapid growth due to investments in broadband infrastructure and an expanding gig-economy workforce that supports last-mile delivery operations.

The northern territories face challenges such as low population density and high shipping costs, though satellite broadband projects are helping to address these issues. The Canadian Radio-television and Telecommunications Commission standardizes content regulations nationwide, while provincial agencies handle dispute resolution, creating a governance structure that balances consumer protection with regional adaptability.

Coverage of the social commerce market by Mordor Intelligence spans a wide geographic footprint, with detailed country-level intelligence for Brazil, India, China, and France, each shaped by local operating conditions.

Competitive Landscape

The Canadian social commerce market is moderately fragmented. Meta utilizes Instagram Shopping and Facebook Marketplace to maintain its position in the category. Shopify provides small and mid-sized businesses with social storefront solutions, enabling smaller merchants to compete effectively. TikTok achieves significant user engagement but faces increased scrutiny due to privacy regulations. Amazon Canada collaborates with TikTok and Instagram to integrate Amazon Pay into influencer content, connecting social discovery with its logistics capabilities.

Lightspeed Commerce integrates point-of-sale data with social platforms to create a seamless experience across physical and digital channels. Established retailers such as Canadian Tire and The Bay leverage loyalty programs in TikTok campaigns, targeting customers who browse in-store and complete purchases online. Patent filings, including Shopify’s 2024 application for “Social Commerce Attribution Systems,” highlight ongoing innovation in tracking and efficiency improvements.

New entrants are focusing on niche segments. Resale platforms like Depop and Poshmark concentrate on secondhand fashion, while local specialists address grocery micro-fulfillment and Indigenous crafts. Platforms with privacy frameworks aligned with the Personal Information Protection and Electronic Documents Act benefit from economies of scale, creating challenges for startups with limited compliance resources.

Canada Social Commerce Industry Leaders

Shopify Inc.

Meta Platforms Inc.

ByteDance Ltd.

Amazon.com Inc.

Pinterest Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Interac introduced social payment APIs, enabling peer-to-peer transfers within major social applications, secured through biometric authentication. The launch of real-time payments by Accept/Pay Global, in collaboration with Interac, represents a notable development for Canada's social commerce market. This initiative supports immediate and secure transactions, improving both consumer trust and operational efficiency. The API-driven solution facilitates fast payouts, payroll, and B2B settlements, which are essential for social commerce platforms that depend on efficient financial processes. By upgrading the payment infrastructure, Canadian merchants are better equipped to operate in the evolving digital economy.

- May 2025: Shopify introduced its enhanced Creator Commerce Platform, incorporating AI-driven recommendations and revenue-sharing tools. This update facilitates automatic payouts to creators and provides real-time analytics. The platform simplifies store creation, utilizes AI-generated theme blocks for design automation, and improves customer engagement through Sidekick, an AI assistant. By addressing technical challenges and enhancing personalization, Shopify supports Canadian merchants in adapting to the evolving social commerce environment, driving advancements in digital retail operations.

- May 2025: Pinterest introduced visual search and merchant verification tools to simplify the discovery and checkout process. By enabling users to shop directly from images and refine searches based on style, color, or occasion, Pinterest aims to enhance personalized shopping experiences. These tools, powered by generative AI, are designed to meet the preferences of Canada’s mobile-focused and fashion-conscious consumers, making social commerce more streamlined. The rollout in Canada supports local merchants and aligns with the increasing adoption of visual-first online shopping.

- September 2024: Amazon Canada has integrated Amazon Pay into TikTok and Instagram, enabling Prime members to make one-click purchases. This integration allows Canadian merchants to display Prime branding and provide real-time delivery estimates within their TikTok advertisements, directing traffic to their websites. By combining Amazon's logistics capabilities with TikTok's reach, this initiative strengthens consumer confidence, improves conversion rates, and supports local sellers in adapting to mobile-focused, video-based shopping environments.

Canada Social Commerce Market Report Scope

The Canada Social Commerce Market Report is Segmented by Product Type (Apparel, Personal and Beauty Care, Accessories, Home Products, Health Supplements, Food and Beverages, Other Product Types), Device (Laptops and Desktops, Smartphone), Sales Channel (Video Commerce, Social Network-Led Commerce, Social Reselling, Group Buying/Team Purchase, and More), and Geography (Canada). The Market Forecasts are Provided in Terms of Value (USD).

| Apparel |

| Personal and Beauty Care |

| Accessories |

| Home Products |

| Health Supplements |

| Food and Beverages |

| Other Product Types |

| Laptops and Desktops |

| Smartphone |

| Video Commerce |

| Social Network-Led Commerce |

| Social Reselling |

| Group Buying / Team Purchase |

| Product Review and Discovery Platforms |

| By Product Type | Apparel |

| Personal and Beauty Care | |

| Accessories | |

| Home Products | |

| Health Supplements | |

| Food and Beverages | |

| Other Product Types | |

| By Device | Laptops and Desktops |

| Smartphone | |

| By Sales Channel | Video Commerce |

| Social Network-Led Commerce | |

| Social Reselling | |

| Group Buying / Team Purchase | |

| Product Review and Discovery Platforms |

Key Questions Answered in the Report

How large is the Canada social commerce market in 2025?

The market is valued at USD 30.28 billion in 2025, with a projected CAGR of 29.04% through 2030.

Which product category is growing fastest on Canadian social platforms?

Personal and beauty care leads growth at a 29.13% CAGR, challenging apparel’s long-time dominance.

What share of Canadian social commerce purchases takes place on smartphones?

Smartphones accounted for 91.11% of transactions in 2024 and their dominance is rising further.

How is video commerce impacting Canadian consumer buying behavior?

Video formats control 43.21% of sales, offering demonstrations and storytelling that convert viewers into buyers.

What legislation is shaping data privacy for social commerce in Canada?

Bill C-27’s Consumer Privacy Protection Act sets strict consent and data portability rules for platforms.

Which regions generate the highest social commerce sales in Canada?

Toronto, Vancouver, and Montreal together produce about 60% of national volume, with Toronto alone at 28%.

Page last updated on: