Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

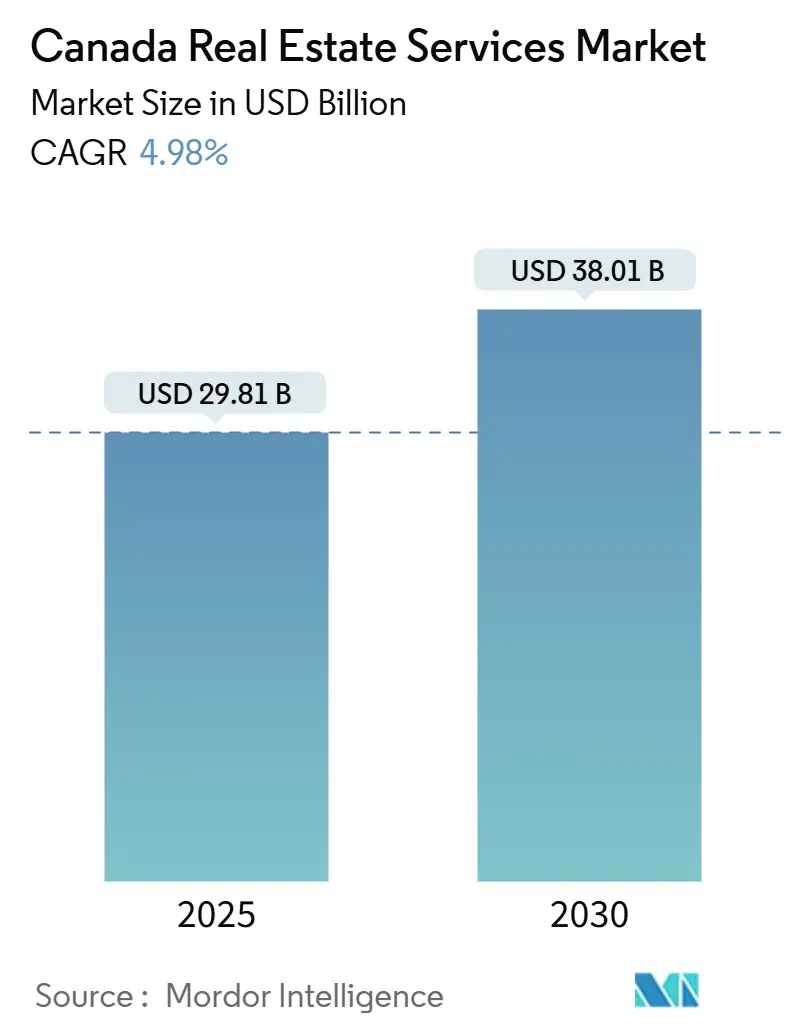

| Market Size (2025) | USD 29.81 Billion |

| Market Size (2030) | USD 38.01 Billion |

| Growth Rate (2025 - 2030) | 4.98% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Real Estate Services Market Analysis by Mordor Intelligence

The Canada real estate services market size stood at USD 29.81 billion in 2025 and is forecast to reach USD 38.01 billion by 2030, advancing at a 4.98% CAGR over the period 2025-2030. Tailwinds from sustained immigration, the institutionalization of rental housing, and rising demand for logistics space underpin this outlook, while elevated borrowing costs and affordability pressures temper short-term deal volumes,. The Bank of Canada’s five rate cuts in 2024, combined with expectations of further easing toward 2.5% by mid-2025, are set to revive brokerage and valuation mandates as financing conditions normalize. Meanwhile, ESG disclosure rules in Toronto and Vancouver, coupled with the Canada Green Building Council’s Zero Carbon Building Standard, enlarge the consulting revenue pool for compliance and retrofit advisory,. Technology adoption—from AI-driven pricing engines to automated lease abstraction—continues to compress transaction timelines and expand margin opportunities for firms that scale digital platforms

Key Report Takeaways

- By property type, residential services led with 56.1% of Canada real estate services market share in 2024, whereas commercial services are set to expand at a 5.66% CAGR through 2030.

- By service, brokerage generated 46.7% of 2024 revenues, but property management is forecast to grow fastest at 5.94% CAGR to 2030.

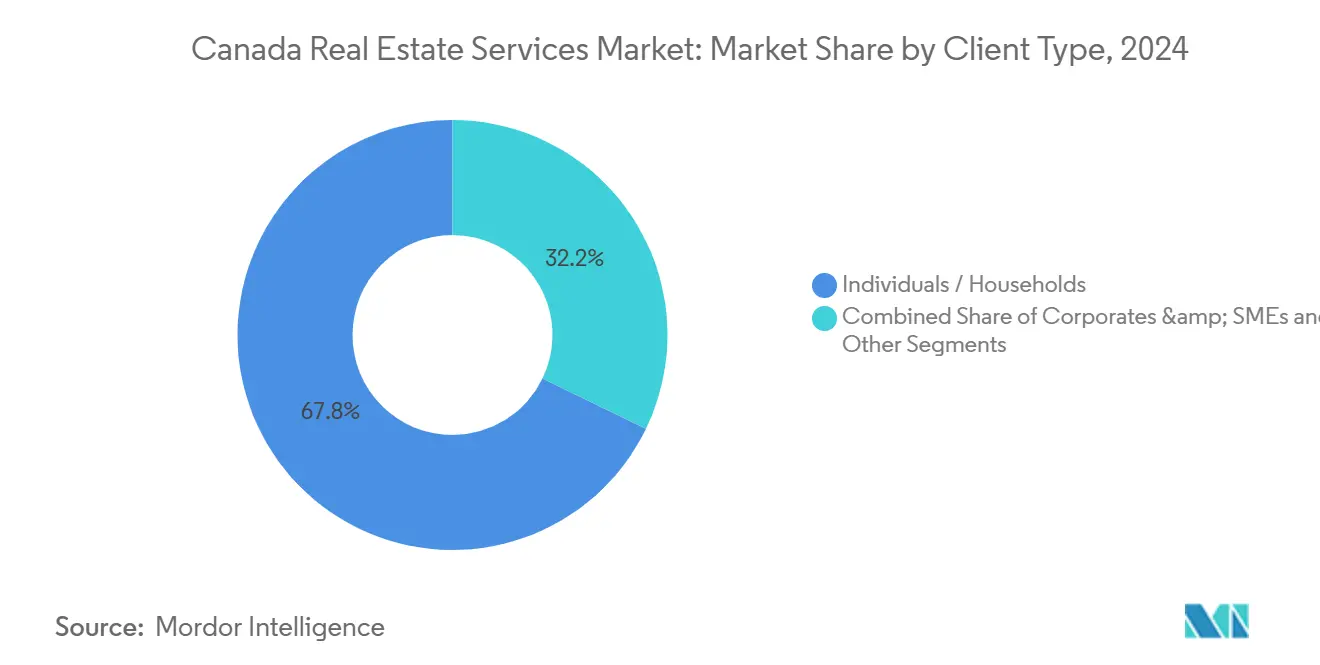

- By client type, individuals and households contributed 67.8% of 2024 turnover, while corporates and SMEs are projected to post a 6.11% CAGR through 2030.

- By geography, Ontario captured 40.1% of 2024 value, yet Alberta is expected to record the highest provincial CAGR at 6.32% to 2030.

Canada Real Estate Services Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Population growth and immigration fueling transactions across residential and rental sectors | +1.2% | Ontario, British Columbia, Alberta | Medium term (2-4 years) |

| Institutionalization of rentals (BTR) and industrial/logistics expanding property management mandates | +1.4% | National, concentrated in major metros | Long term (≥ 4 years) |

| Capital recycling, recapitalizations, and asset repositioning boosting advisory and valuation work | +0.9% | Ontario and British Columbia urban cores | Medium term (2-4 years) |

| Data/analytics and proptech adoption enhancing brokerage productivity | +0.7% | Toronto, Vancouver, Calgary tech hubs | Short term (≤ 2 years) |

| ESG, energy retrofits, and compliance driving consulting and monitoring services | +0.6% | Toronto, Vancouver, Montreal | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Population Growth and Immigration Fueling Transactions Across Residential and Rental Sectors

Canada’s revised immigration plan still targets 395,000 new permanent residents in 2025, keeping population growth above historic norms and sustaining demand for both home purchases and rentals[1]Government of Canada, “Supplementary Immigration Levels Plan 2025-2027,” canada.ca. Net international migration remained robust through mid-2024, even as student visa rules tightened, shifting rental demand toward family-oriented multi-family units. Household formation continues to cluster in Ontario, British Columbia, and Alberta, supporting brokerage pipelines and expanding property management mandates. Scotiabank Economics notes that absolute population additions, while moderating from pandemic peaks, remain sufficient to underpin steady transaction activity. This demographic momentum is expected to offset some affordability-driven softness in first-time buyer segments through the forecast window.

Institutionalization of Rentals (BTR) and Industrial/Logistics Expanding Property Management Mandates

Institutional investors now own up to 30% of Canada’s purpose-built rental stock, accelerating the professionalization of property management[2]Canadian Human Rights Commission, “Financialization of Rental Housing in Canada,” chrc-ccdp.gc.ca. CMHC recorded a 61% year-over-year rise in multi-unit insurance approvals in Q2 2024, signaling a deep pipeline of build-to-rent projects that will require scaled operating platforms. Canadian Apartment Properties REIT alone deployed USD 211 million into acquisitions in December 2025, exemplifying capital’s pivot to rental housing. On the commercial side, national industrial inventory reached 2.06 billion sq ft by Q2 2025, with almost 20 million sq ft under construction, cementing long-term demand for warehouse and logistics management services. The convergence of BTR and logistics trends positions property management as the fastest-growing revenue stream across the Canada real estate services market.

Capital Recycling, Recapitalizations, and Asset Repositioning Boosting Advisory and Valuation Work

Tight credit conditions in 2024 prompted institutional owners to shed non-core holdings and recapitalize prime assets, heightening demand for valuation and transaction advisory. Avison Young’s February 2024 recapitalization underscores the strategic repositioning sweeping mid-tier advisory firms. Morguard REIT booked USD 48 million in fair-value losses during H1 2024, spurring extensive mark-to-market studies and asset-disposition analyses. Office-to-residential conversions in downtown Toronto and Vancouver require feasibility, zoning, and construction-monitoring expertise, further enlarging advisory mandates. These dynamics create recurring consulting revenues as owners navigate complex regulatory, capital-stack, and use-conversion challenges.

Data/Analytics and Proptech Adoption Enhancing Brokerage Productivity

AI-driven valuation engines, virtual tours, and automated e-sign solutions are compressing deal timelines and expanding agent capacity. JLL’s Falcon AI automates lease abstraction and cash-flow modeling, allowing brokers to handle larger pipelines with lean support teams. Wahi partners with the Vector Institute to generate instant property valuations, challenging legacy appraisal workflows. Real Brokerage upgraded its Leo AI assistant in October 2024 with natural-language contract drafting, reducing administrative burden and compliance risk. Proptech penetration remains uneven across the Canada real estate services market, leaving ample white space for digital platforms that integrate seamlessly with provincial MLS systems.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High interest rates and affordability headwinds suppressing deal volumes and brokerage revenues | -1.1% | Ontario, British Columbia, Quebec | Short term (≤ 2 years) |

| Limited new supply and tighter underwriting shrinking pipelines for leasing and investment sales | -0.7% | Toronto, Vancouver, Ottawa | Medium term (2-4 years) |

| Talent shortages and rising operating costs squeezing mid-sized firms’ margins | -0.5% | Major metros nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Interest Rates and Affordability Headwinds Suppressing Deal Volumes and Brokerage Revenues

The Bank of Canada lifted its policy rate to 5.0% in early 2024 before easing to 3.25% by December; nonetheless, mortgage rates stayed well above pre-pandemic norms, muting buyer activity. Toronto recorded 67,610 home sales in 2024, only a 2.6% uptick from 2023, even as listings swelled 16.4%, putting pressure on prices and commissions. RBC Economics calculates that servicing a median-priced Toronto home now requires annual household income exceeding USD 144,000, sidelining many first-time buyers. CMHC continues to flag overvaluation risks, signaling potential price adjustments that could further delay buyer re-engagement. Although further rate cuts are expected by mid-2025, the recovery in consumer confidence and transaction velocity is likely to lag.

Limited New Supply and Tighter Underwriting Shrinking Pipelines for Leasing and Investment Sales

Developers pared back starts in 2024 as lenders demanded higher pre-leasing thresholds and equity cushions. Industrial vacancy climbed to 5.5% nationally by Q2 2025, with Montreal at 7.7%, reflecting speculative projects launched during the e-commerce boom now facing softer tenant demand. In residential, condominium completions outpaced presales, forcing banks to order blanket appraisals to close at lower valuations, thereby postponing distress but curbing new project pipelines[3]Parliamentary Budget Officer, “Housing Supply Analysis,” pbo-dpb.ca. The Real Estate Institute of Canada warns that zoning bottlenecks and labor shortages will continue to limit new deliveries, constraining future leasing and sales inventories. Thin supply reduces fee-earning opportunities for service providers dependent on fresh inventory.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Type: Commercial Momentum Surpasses a Dominant Residential Base

Residential services commanded 56.1% of the Canada real estate services market share in 2024 as single-family and multi-family transactions anchored brokerage and property management revenue . Immigration-led population gains, particularly in Ontario and British Columbia, kept resale listings liquid, while a 61% surge in multi-unit insurance approvals signaled robust rental-housing pipelines. The institutionalization of build-to-rent portfolios is funnelling contracts toward scaled property managers such as FirstService, whose residential division posted double-digit revenue growth in 2024. Despite headwinds from mortgage affordability, sustained household formation and the upcoming policy-rate down-cycle are projected to stabilize transaction counts, preserving residential’s absolute lead in the Canada real estate services market.

Commercial services are forecast to post a 5.66% CAGR through 2030, outpacing residential on the back of logistics and industrial demand. National industrial stock hit 2.06 billion sq ft by Q2 2025, with 19.65 million sq ft under construction, driving leasing, valuation, and facilities-management mandates. Office services remain in flux as landlords explore conversions; Morguard REIT’s USD 17.9 million write-down in Q2 2024 illustrates the valuation volatility fueling advisory demand. Retail assets anchored by necessity-based tenants maintain stable management fees, while hospitality and mixed-use properties tap ESG consulting as owners chase LEED and Zero-Carbon certification. These dynamics collectively reinforce commercial’s ascent within the Canada real estate services market.

By Service: Property Management Accelerates Ahead of Brokerage Dominance

Brokerage retained a 46.7% revenue share in 2024, reflecting its central role in residential resale and commercial leasing. Elevated interest rates curbed deal flow, but platform innovations such as JLL’s Falcon AI and Real Brokerage’s Leo assistant are improving agent productivity and compressing cycle times,. The Canada real estate services market size tied to brokerage transactions is expected to regain momentum once rate normalization bolsters borrower capacity in 2026.

Property management is projected to expand at a 5.94% CAGR to 2030, the fastest among all service lines CAPREIT’s USD 211 million acquisition spree in 2025 exemplifies institutional investors’ reliance on third-party operators to manage dispersed BTR portfolios. On the industrial front, warehouses exceeding 100,000 sq ft require specialized maintenance, dock scheduling, and safety compliance that mid-tier managers are racing to provide. The Canada real estate services market size for property management is expected to climb steadily alongside rental-housing deliveries and logistics absorption.

Valuation and consulting revenues are also rising as owners seek ESG certifications and navigate recapitalizations. Avison Young’s recapitalization enhanced capacity to handle complex appraisal assignments for corporates repositioning under-performing assets. Other ancillary services—project management, energy auditing, and carbon-tracking—are expanding in tandem with retrofit financing programs from the Canada Infrastructure Bank, weaving ESG advisory into core service bundles.

By Client Type: Corporates and SMEs Lead Growth While Households Remain Core

Individuals and households generated 67.8% of 2024 revenue, underlining the pivotal role of residential resale and rental management in the Canada real estate services market TRREB forecasts 76,000 Toronto home transactions in 2025 as lower rates revive upper-income demand, sustaining commission pools. Persistent rental tightness, driven by immigration inflows, guarantees stable fee income for multi-family property managers across the GTA and Lower Mainland.

Corporates and SMEs are set to record a 6.11% CAGR through 2030, reflecting rising demand for valuation, ESG advisory, and capital-recycling support. Office-to-residential conversions in Toronto and Vancouver illustrate the complex zoning and feasibility studies corporates increasingly outsource to multidisciplinary advisors. JLL’s Falcon AI deployment in Canada allows corporate real-estate teams to centralize portfolio analytics, widening the addressable advisory market. As tenant expectations evolve toward net-zero and wellness-certified space, SMEs require guidance on retrofit financing, further lifting consulting billings.

Others—principally institutional investors and public bodies—remain a smaller slice but are expanding via affordable-housing initiatives and infrastructure-linked developments. CHRC estimates institutional ownership of purpose-built rentals will continue to climb, ensuring specialist mandates for ESG-aligned asset management.

Geography Analysis

Ontario accounted for 40.1% of 2024 revenue, anchored by Toronto’s deep transaction pool and diverse asset mix The province benefits from steady immigration, high-value commercial deals, and a regulatory push toward emissions disclosure that generates advisory fees. Industrial vacancy in the Greater Toronto Area reached 5.0% in Q2 2025, with 7.46 million sq ft underway, pointing to a potential short-term supply glut but long-run service opportunities in lease-up and facilities management. Ottawa supplements provincial growth through stable government tenancy and expanding tech employment that underpins office leasing.

Alberta is projected to grow fastest at a 6.32% CAGR through 2030, driven by energy-sector recovery and competitive housing affordability Calgary logged 1.025 million sq ft of positive industrial absorption in Q2 2025, signaling healthy logistics demand amid Western Canadian supply-chain diversification. Brokerages in the province are early adopters of AI tools, as shown by Virtuo’s partnership with Royal LePage Benchmark covering over 200 agents, which is expected to enhance operating efficiency and capture share in the expanding Canada real estate services market. Edmonton’s 5.9% industrial vacancy and robust construction pipeline support sustained property management and leasing assignments.

British Columbia’s Vancouver market balances luxury residential softness with persistent industrial tightness, reporting 3.9% warehouse vacancy in Q2 2025. Emissions-reporting requirements parallel to Toronto’s add compliance-advisory demand, while constrained land supply keeps industrial rents elevated, supporting asset-management fees. Quebec’s Montreal wrestles with 7.7% industrial vacancy and negative absorption, but language-specific regulations provide local brokerages with a moat against national competitors, maintaining fee integrity. The rest of Canada, including Atlantic provinces and the Prairies, generates modest volumes yet offers stable residential markets and resource-linked industrial deals that round out national service portfolios.

Competitive Landscape

Competition in the Canada real estate services market is moderate, with global full-service firms CBRE, Colliers, and JLL vying against residential franchises RE/MAX, Royal LePage, and Century 21. Commercial market share concentration favors the multinationals, which leverage cross-border client relationships and proprietary data platforms to secure large advisory and leasing mandates. Residential brokerage remains fragmented, comprising thousands of agents under franchise umbrellas that collectively handle the bulk of resale transactions.

Technology is the key battleground for differentiation. JLL’s Falcon AI streamlines lease-analysis workflows, while Wahi’s flat-fee, AI-assisted listing model compresses traditional commission structures, pressuring incumbents to match digital convenience. Real Brokerage’s Real Wallet integrates payment processing and lending referrals, capturing ancillary revenue and deepening agent stickiness. Regional consolidation intensified as RealServus absorbed StreetCity Realty in Ontario, and Coldwell Banker Momentum bought Action Plus Realty to build scale economies in compliance, marketing, and technology,.

ESG advisory capacity is emerging as a competitive differentiator. Firms investing in ISO 14001 and LEED accreditation stand to monetize Toronto’s emissions-reporting mandates and CaGBC’s zero-carbon certification pathway. FirstService’s property-management arm highlights the appeal of steady, contract-based income streams, especially as build-to-rent portfolios expand. Advisory outfits such as Avison Young fortify balance sheets to pursue capital-recycling mandates, underscoring the convergence of capital-markets expertise and sustainability consulting.

Canada Real Estate Services Industry Leaders

CBRE

Colliers

JLL

RE/MAX

Royal LePage

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Canadian Apartment Properties REIT invested USD 211 million in multi-family acquisitions, amplifying demand for third-party property management.

- November 2025: myAbode acquired FirstList, merging digital listing tech with full-service brokerage to enhance agent productivity.

- July 2025: Virtuo and Royal LePage Benchmark partnered to deploy AI valuation tools across 200+ Alberta agents.

- June 2025: RealServus bought StreetCity Realty, adding 170 Ontario agents and expanding its residential footprint.

Canada Real Estate Services Market Report Scope

By Property Type

| Residential | Single-Family |

| Multi-Family | |

| Commercial | Office |

| Retail | |

| Logistics | |

| Others |

By Service

| Brokerage Services |

| Property Management Services |

| Valuation Services |

| Others |

By Client Type

| Individuals / Households |

| Corporates & SMEs |

| Others |

By Province

| Ontario |

| Quebec |

| British Columbia |

| Alberta |

| Rest of Canada |

| By Property Type | Residential | Single-Family |

| Multi-Family | ||

| Commercial | Office | |

| Retail | ||

| Logistics | ||

| Others | ||

| By Service | Brokerage Services | |

| Property Management Services | ||

| Valuation Services | ||

| Others | ||

| By Client Type | Individuals / Households | |

| Corporates & SMEs | ||

| Others | ||

| By Province | Ontario | |

| Quebec | ||

| British Columbia | ||

| Alberta | ||

| Rest of Canada | ||

Key Questions Answered in the Report

How large is the Canada real estate services market in 2025?

The market is valued at USD 29.81 billion in 2025.

What CAGR is projected for Canada real estate services through 2030?

The market is forecast to grow at a 4.98% CAGR between 2025 and 2030.

Which service line is expected to grow fastest?

Property management is projected to post a 5.94% CAGR to 2030, driven by build-to-rent and logistics demand.

Which province will likely see the highest growth?

Alberta is forecast to lead with a 6.32% CAGR thanks to energy-sector recovery and strong industrial absorption.

Why are ESG services gaining traction?

Municipal emissions-reporting rules and the CaGBC Zero Carbon Standard require ongoing audits, certifications, and retrofit consulting.

What key technology trend is reshaping brokerage operations?

AI platforms like JLL’s Falcon and Wahi’s valuation engine automate analysis and compress transaction timelines.

Page last updated on: