Canada Nicotine Pouches Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

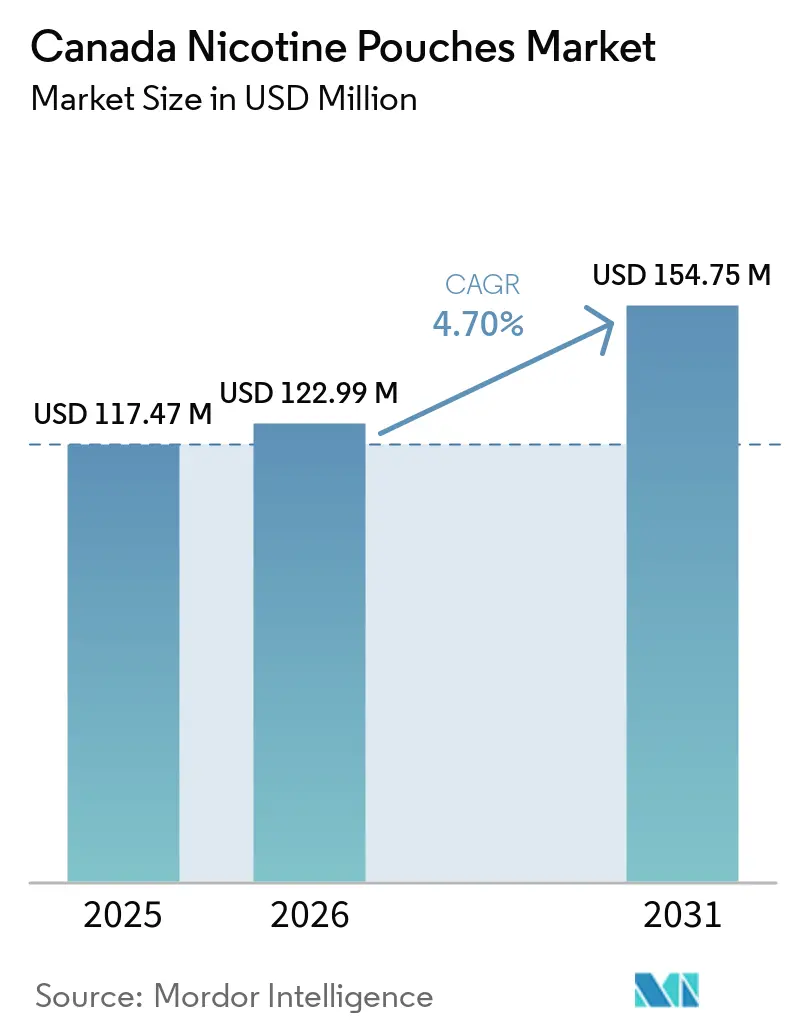

| Base Year Market Size (2025) | USD 117.47 Million |

| Market Size (2026) | USD 122.99 Million |

| Market Size (2031) | USD 154.75 Million |

| Growth Rate (2026 - 2031) | 4.70% CAGR |

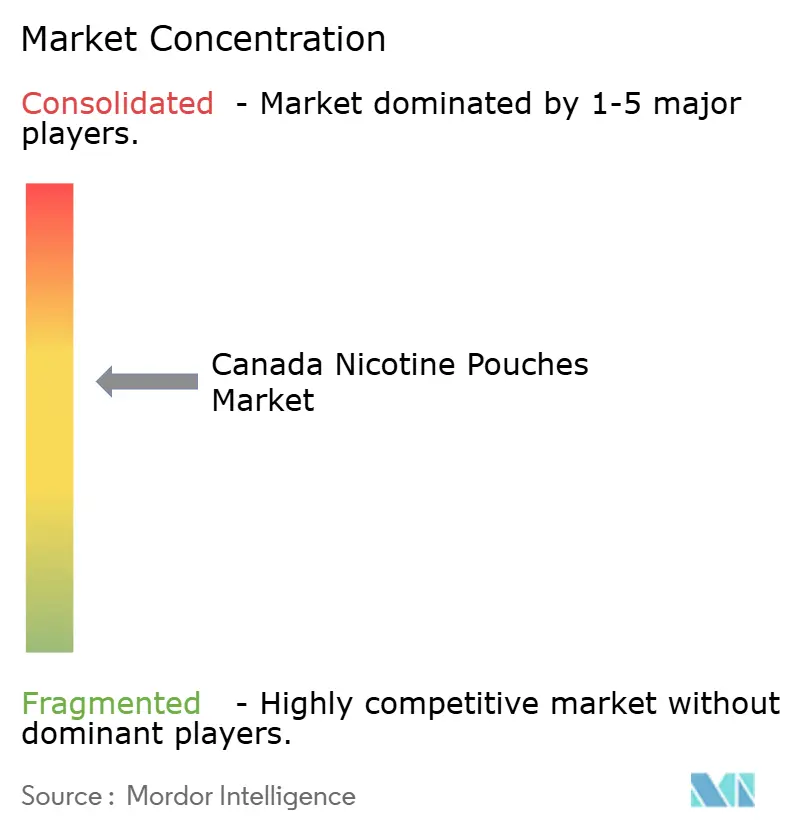

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Nicotine Pouches Market Analysis by Mordor Intelligence

The Canada nicotine pouches market size is projected to be USD 117.47 million in 2025, USD 122.99 million in 2026, and reach USD 154.75 million by 2031, growing at a CAGR of 4.70% from 2026 to 2031. The Canada nicotine pouches market is undergoing a regulatory transition in which legal access remains narrow, even as the category gains greater medical legitimacy under the Food and Drugs Act. Health Canada's August 2024 order reduced near-term retail availability by limiting sales to behind-the-counter, but the same rule also positioned authorized nicotine pouches as cessation-oriented products rather than general retail nicotine items. Smoking prevalence in Canada continued to decline in 2024, yet the number of adults still trying to quit kept the demand base relevant for regulated nicotine replacement formats. The market also faces a policy contradiction: restricted legal access has coincided with the spread of unauthorized products and a rise in cigarette sales. The January 2026 clarification that nicotine buccal pouches at 4 milligrams or less can be sold as non-prescription natural health products is likely to support more license applications, a broader authorized assortment, and more active competition in the Canada nicotine pouches market before 2031.

Key Report Takeaways

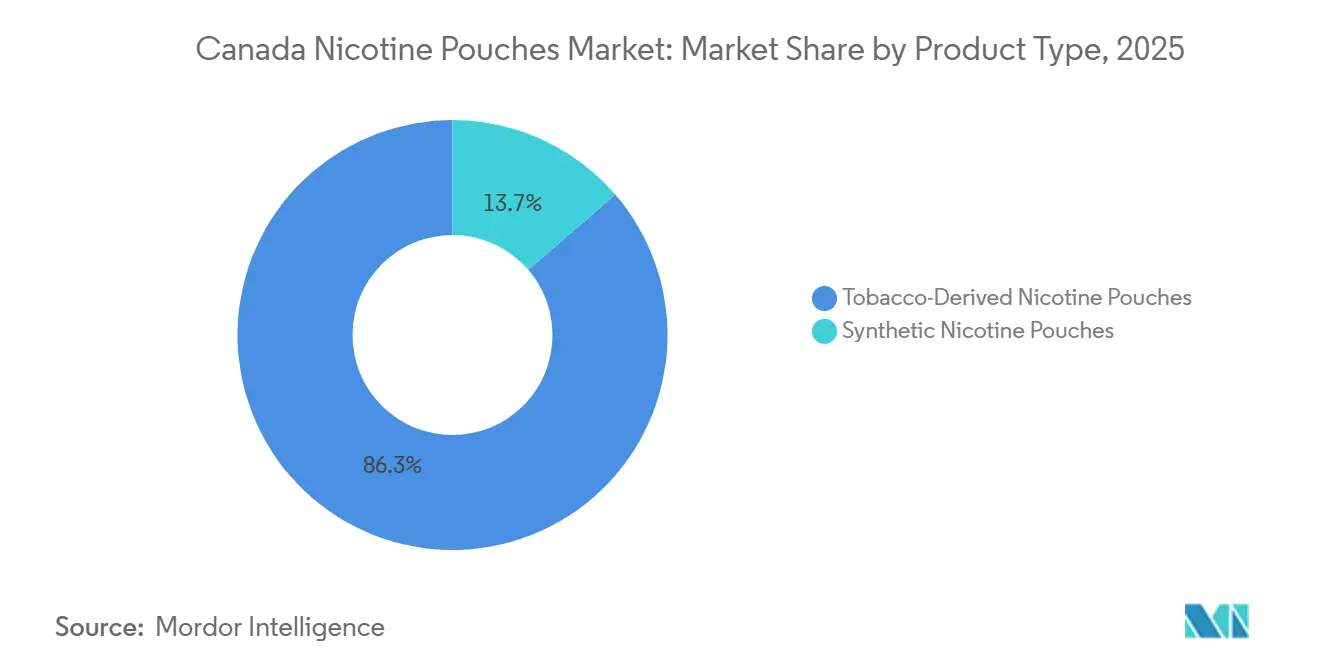

- By product type, tobacco-derived nicotine pouches held 86.34% of the Canada nicotine pouches market in 2025.

- By flavor type, the Canada nicotine pouches market for unflavored pouches is expected to grow at a CAGR of 5.68% from 2026 to 2031.

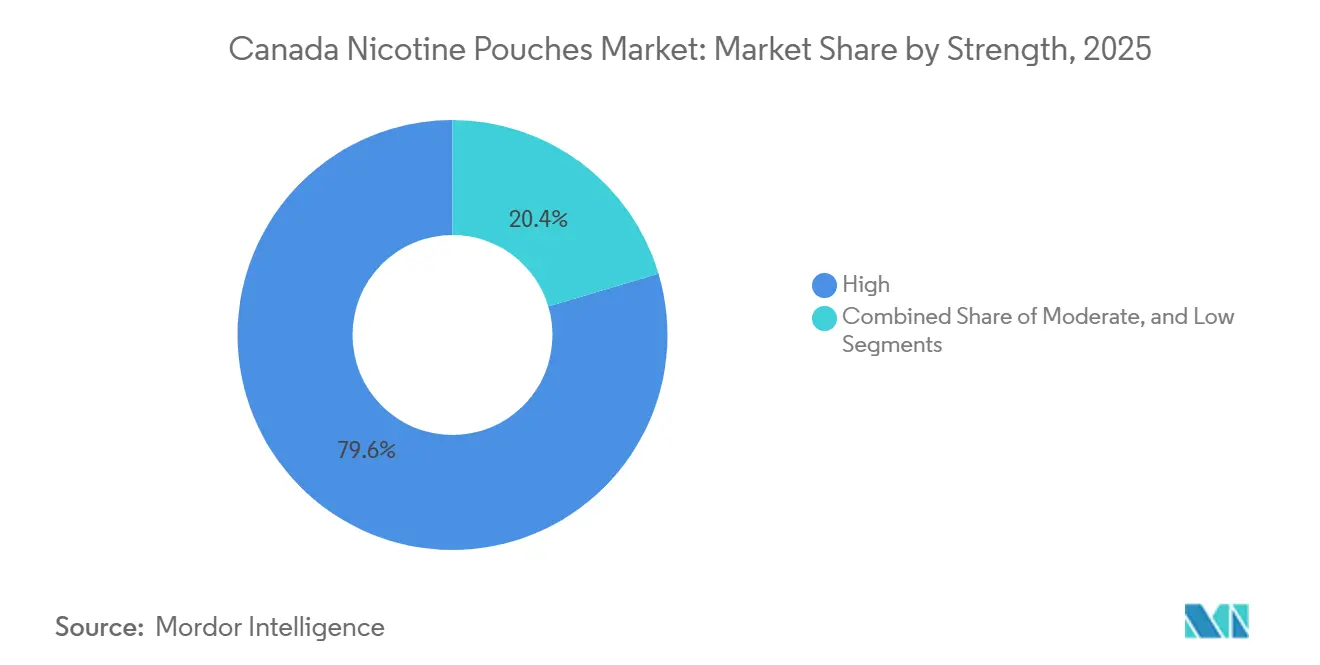

- By strength, high pouches captured 79.61% of the Canada nicotine pouches market in 2025.

- By distribution channel, the Canada nicotine pouches market for offline is expected to grow at a CAGR of 5.63% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Canada Nicotine Pouches Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smoking Cessation Demand and Tobacco Harm-Reduction Positioning | +1.8% | National, with the strongest uptake in Ontario and British Columbia, where pharmacy infrastructure is densest | Medium term (2-4 years) |

| Discreet Smoke-Free Nicotine Consumption in Restricted Settings | +1.1% | National, particularly in high-density urban centers with extensive smoke-free bylaws | Short term (≤ 2 years) |

| Product Innovation in Pouch Materials, Moisture Systems, And Nicotine Delivery | +0.8% | National, pipeline realization is dependent on Health Canada license throughput timelines | Long term (≥ 4 years) |

| Growth In Consumer Preference for Tobacco-Free Oral Alternatives | +0.6% | National | Medium term (2-4 years) |

| Pharmacy Channel Credibility for Quit-Intent Adult Users | +0.4% | National, particularly reinforced in Quebec, where pharmacy-only NRT sales predated the federal order | Short term (≤ 2 years) |

| Potential Conversion from Unauthorized High-Strength Use to Regulated Low-Dose Formats | +0.3% | National, with Alberta and convenience-store-dense urban markets as the primary conversion pools | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Smoking Cessation Demand and Tobacco Harm-Reduction Positioning

Authorized nicotine pouches hold a distinct place in the Canadian nicotine pouches market because Health Canada regulates them under the Food and Drugs Act rather than the Tobacco and Vaping Products Act, which gives compliant products a medical and cessation-focused position that unauthorized products do not have. Health Canada's January 2026 tobacco strategy report stated that 25% of Canadians who tried to quit in 2024 used nicotine replacement products, and it also noted that combining a nicotine patch with a short-acting nicotine replacement product can sharply improve quit success.[1]Health Canada, “Guidance on Additions to the List of Nicotine Replacement Therapy Dosage Forms, Overview,” Health Canada, canada.ca That framework matters for the Canada nicotine pouches market because pouches can fit as a short-acting option alongside other nicotine replacement therapies during quit attempts. The same Health Canada report confirmed that 300,000 Canadians quit smoking in 2024 and that tobacco use among adults had fallen to 11%, which supports a durable but regulated demand pool for cessation products. Demand in this part of the market is therefore tied less to casual trial and more to adults with an active intent to reduce or quit smoking, which improves the quality of demand, even if the legal buyer pool remains narrower than in more open retail systems. That pattern supports measured growth in the Canada nicotine pouches market, even while the category remains closely supervised by regulators and pharmacists.

Discreet Smoke-Free Nicotine Consumption in Restricted Settings

A second demand driver in the Canada nicotine pouches market is the product's ability to deliver nicotine without smoke, vapor, or visible use, which gives it a practical role in settings where smoking and vaping are not allowed. A 2026 scoping review found that discreet use and portability were among the most common reasons consumers adopted oral nicotine pouches, suggesting a use case that sits alongside cessation rather than replacing it. This matters for the Canada nicotine pouches market because some adults may use pouches in workplaces, travel settings, or public spaces where combustible and vaping products are not practical. That situational demand can widen the addressable audience beyond consumers who are fully committed to quitting, even if those users still rely on cigarettes or other nicotine products at other times. The present legal model does not fully capture that demand, because pharmacy-only access creates more friction than a general retail purchase for an occasional or situational user. As a result, discreet consumption supports the Canada nicotine pouches market on the demand side, while the authorized channel still limits how much of that demand turns into legal sales.

Product Innovation in Pouch Materials, Moisture Systems, and Nicotine Delivery

The Canada nicotine pouches market is also influenced by ongoing work in faster release systems, improved moisture control, and more stable nicotine delivery designs, all of which can help future applicants differentiate themselves without changing the broad regulatory intent. Fertin Pharma's published 2025 patent application described a non-tobacco pouched product that used a reduced-fill composition to enhance nicotine release, with some formulations reaching more than 90% release within 30 minutes. Nicoventures Trading Limited filed a December 2025 patent for a nicotine-polymer complex that combined freebase and protonated nicotine forms to deliver a more controlled 30 to 60 minute release pattern and better storage stability. Those developments matter in the Canada nicotine pouches market because Health Canada's review process places weight on safety, efficacy, quality, and a clear dosage form profile for nicotine replacement therapies. New entrants are therefore likely to compete on formulation performance and compliance quality rather than on broad flavor ranges or wide retail placement. Over time, better delivery systems could help the Canada nicotine pouches market add more licensed SKUs and reduce its dependence on a very small authorized assortment.

Growth In Consumer Preference for Tobacco-Free Oral Alternatives

The Canada nicotine pouches market also benefits from a broader shift toward tobacco-free oral formats, even though Canada's legal market remains much more restrictive than those in the leading Nordic markets. A 2026 JMIR study covering more than 19 million e-commerce orders in Sweden and Norway found that nicotine pouch volume share passed traditional snus by 2025, with Sweden rising from 5% to 55% and Norway from 22% to 56% over the study period. That evidence does not transfer directly to Canada, but it does show that oral nicotine substitution can move from niche status to mainstream relevance when the product format is available and understood by consumers. A 2026 narrative review in Internal and Emergency Medicine further stated that switching smokers to nicotine pouches can reduce toxic substance exposure to levels close to those seen after smoking cessation, which strengthens the clinical case for authorized products in the Canada nicotine pouches market. That clinical framing is important because the Canadian nicotine pouch market is expanding within a harm-reduction debate, rather than as a normal, convenience-driven consumer category.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pharmacy-Only Access and Behind-The-Counter Purchase Friction | -1.5% | National, most acute in rural, remote, and northern regions with sparse pharmacy coverage | Short term (≤ 2 years) |

| Mint-and-Menthol Flavor Limits Constraining Adult Trial and Retention | -0.9% | National, particularly suppressive for adult smokers seeking behavioral substitution cues from flavor variety | Medium term (2-4 years) |

| Illicit High-Strength Online and Convenience-Store Supply Distorting the Legal Market | -0.6% | National, concentrated in Alberta, and convenience-store-dense urban markets | Short term (≤ 2 years) |

| Slow Label, Packaging, and License-Change Cycles Limiting Legal Assortment Agility | -0.4% | National, most acute for manufacturers managing multi-SKU portfolios with pending license amendments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Pharmacy-Only Access and Behind-The-Counter Purchase Friction

The largest restraint on the Canada nicotine pouches market is the pharmacy-only model, which requires behind-the-counter sales and removes the product from normal convenience retail access. Health Canada's 2026 tobacco strategy report showed that tobacco use remained much higher in the territories and among lower-income groups, yet these are the same areas where pharmacy coverage can be thinner and less convenient for routine access. Imperial Tobacco Canada stated in August 2025 that pharmacists absorbed close to 1,000,000 hours of additional administrative burden in the first year after the order, suggesting the authorized channel has become both more operationally demanding and more restricted. That friction can slow transactions, limit stocking interest, and reduce access for adult smokers who might otherwise try a regulated product. The model does improve credibility with consumers who reach a pharmacist, but that benefit is not evenly distributed across the country. In practical terms, the Canada nicotine pouches market remains constrained by a legal channel that is designed for controlled access rather than broad consumer availability.

Mint-and-Menthol Flavor Limits Constraining Adult Trial and Retention

Flavor restrictions are another major brake on the Canada nicotine pouches market because legal products can only be sold in mint and menthol variants under the current order. The market still showed a 57.48% share for flavored products in 2025, which indicates that sensory preference continues to shape adult purchasing even within a narrow two-flavor system. A 2025 medRxiv study found that post-ban nicotine pouch formulations may rely on synthetic sensory additives such as WS-3 to create cooling effects in mint-compliant products, suggesting manufacturers are trying to preserve differentiation even when official flavor naming is restricted. That means regulatory limits may change product chemistry and marketing rather than fully remove sensory differences from the category. It also means product developers in the Canadian nicotine pouches market must spend more effort on release profiles, moisture systems, and compliance language because open flavor variety is not available as a growth lever in Canada. As long as those limits remain in place, legal product trial and repeat adoption are likely to grow more slowly than they would in a broader adult-flavor environment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Regulatory Approval Timing Sustaining a Concentrated Category

Tobacco-derived nicotine pouches held 86.34% of the market value in 2025, and that share effectively reflected the Canada nicotine pouches market structure at a time when Health Canada had confirmed only 2 licensed pouch products by August 2025. The category was therefore shaped less by open consumer choice and more by what had already cleared the regulatory pathway for legal sale. Tobacco-derived products had a practical advantage because assessors could compare them with existing nicotine replacement formats, such as lozenges and gums, when reviewing applications. That helped keep the authorized Canada nicotine pouch market concentrated on products that already matched a familiar review logic and an established evidence base.

Synthetic nicotine pouches are projected to grow at a 5.13% CAGR from 2026 to 2031, and that makes them the fastest-moving product type in the Canada nicotine pouches market size discussion, even though they started from a much smaller base. Scientific and commercial work in Europe and the United States shows that synthetic nicotine formulations and nicotine analogs are advancing even when regulatory systems remain unsettled. That matters in Canada because future entrants are likely to use alternative nicotine sources as part of a cleaner, more differentiated filing strategy under the natural health product route. Nicoventures' December 2025 patent filing showed that major tobacco groups are already building release systems that could support new filings beyond today's narrow authorized shelf. Within the Canada nicotine pouches industry, that points to future competition being decided by application quality and formulation performance rather than by brand scale alone.

By Flavor Type: Narrow Legal Variety Leaving Room for Unflavored Growth

Unflavored nicotine pouches are projected to expand at a 5.68% CAGR from 2026 to 2031, making them the fastest-growing flavor segment in the Canada nicotine pouches market. That outlook looks unusual beside global experience, but it fits Canada's legal setting, where some adults may prioritize nicotine delivery and a clinical feel over taste variety. It also aligns with the likely behavior of new applicants, who may see unflavored SKUs as easier to defend under youth-appeal rules and a cessation-focused regulatory lens. In that sense, unflavored products can grow without displacing flavored demand, because they serve a different buyer need within the authorized Canada nicotine pouches market.

Flavored pouches still accounted for 57.48% of the Canadian nicotine pouch market in 2025, even though legal flavor options were limited to mint and menthol. That result shows that taste remains a meaningful part of purchase behavior even when choice is tightly constrained. A 2025 medRxiv analysis found that post-ban products may still use sensory chemistry to create distinct cooling experiences within compliant mint positioning, suggesting the effective product spread is broader than label names alone imply.[2]Natalia Peraza et al., “Pre- and Post-Flavor Ban Oral Nicotine Pouches, A Chemical, Sensory, and Young Adult Appeal Analysis,” medRxiv, medrxiv.org That makes flavored products likely to remain the larger tier through 2031, while unflavored products grow as a more clinical and defensible option for adult cessation users. Within the Canada nicotine pouches industry, flavor strategy is therefore tied to regulation as much as to consumer preference.

By Strength: The 4mg Cap Pushing Demand Toward the Legal Ceiling

High-strength pouches captured 79.61% of the Canada nicotine pouch market in 2025, and that result needs to be read in the context of Health Canada's January 2026 clarification that pouches containing 4 milligrams or less can be sold as non-prescription natural health products. In Canada, the high-strength tier differs from that in more open international markets, because the legal ceiling already compresses the upper end of the authorized range. CBC News reported in December 2025 that unauthorized products containing up to 15mg per pouch were being sold in Canadian corner stores, indicating that demand for stronger products existed outside the legal channel. That dynamic kept the legal Canada nicotine pouches market centered near the maximum dose that could still fit the non-prescription pathway.

Moderate-strength pouches are projected to grow at the fastest rate, with a 6.05% CAGR from 2026 to 2031, suggesting a broader role for step-down use as the category develops. Health Canada's cessation framing supports that pattern because nicotine replacement products are often used in staged reduction rather than as a one-step switch. JAMA Network Open published evidence in 2025 showing that nicotine pouches generally deliver nicotine more slowly and often at lower peak levels than cigarettes, which supports a role for moderate strengths among lighter or more transition-focused users. Low-strength products remain the smallest tier, but they could gain relevance if the authorized assortment expands and pharmacist-led step-down guidance becomes more common in the Canada nicotine pouches market. Taken together, the strength mix shows a market that is being shaped by dosage rules as much as by end-user preference.

By Distribution Channel: Pharmacies Remaining the Core of Legal Sales

Offline channels held 67.42% share in 2025, and that outcome was largely a legal effect rather than a clear consumer preference signal. The Canada nicotine pouches market was pushed into physical pharmacies after SOR/2024-169 ended broad convenience and gas-station sales for authorized products. Quebec and British Columbia had already moved earlier on pharmacy integration, which gave those provinces a more established pharmacist-patient routine once the federal rules took effect. As more products move through review, physical pharmacies are likely to remain the leading legal route because the compliance model still centers on professional oversight and controlled purchase conditions.

Online sales account for the rest of the Canada nicotine pouches market, but only pharmacy-operated websites can participate under the current framework, and they must involve a pharmacist or supervised person in the transaction. That rule provides the channel with a compliance safeguard, but it also makes the model more costly and less seamless than typical e-commerce. Health Canada reported more than 300 enforcement actions since August 2024 against unauthorized nicotine pouch products, which shows that illicit online and retail supply remains a real competitor to the legal channel. The result is a Canada nicotine pouches market where legal distribution remains highly controlled even as unauthorized sellers continue to operate with broader reach and less friction.

Geography Analysis

The Canada nicotine pouches market is national in regulation, but its commercial results differ across provinces because access, pharmacy practice, and enforcement conditions are not uniform. Quebec and British Columbia entered the post-August 2024 period with a stronger pharmacy-based integration model for nicotine replacement products, which helped them adapt more quickly to the federal framework. That early alignment matters because the current legal market depends heavily on pharmacist interaction and behind-the-counter storage. Youth demand has not disappeared under stricter provincial settings, and media reporting in Quebec and nationally has shown that unauthorized products continue to reach consumers outside the authorized system. Quebec also adds a bilingual labeling requirement under SOR/2024-169, which creates an extra compliance step that larger national operators can handle more easily than smaller applicants.

Ontario remains central to the Canada nicotine pouches market because it has the largest absolute pool of adult smokers and the broadest urban pharmacy network. Large urban areas in Ontario are better positioned to support compliant purchases, pharmacist counseling, and repeat legal access than smaller, more remote markets. At the same time, Health Canada's 2026 report showed much higher tobacco use in the territories and persistent disparities among lower-income groups, which highlights a mismatch between need and legal access. That gap limits how far the Canada nicotine pouches market can penetrate outside the better-served pharmacy catchments that dominate legal sales today.

Western Canada presents a different geographic pattern because the demand story is closely tied to channel conflict and unauthorized supply. Imperial Tobacco Canada said in August 2025 that 500 million illegal pouches were sold nationally in the first year after the order, and it linked that period with a 2.8% rise in cigarette sales, which points to real substitution leakage away from the legal category.[3]Imperial Tobacco Canada, “One Year Later, Ottawa's Nicotine Pouch Order Fuels Illicit Boom, Hurts Smokers Trying to Quit,” Newswire, newswire.ca That problem is especially relevant in markets where convenience channels have traditionally been important for nicotine purchases and where pharmacy access is less convenient. The Canada nicotine pouches market therefore faces a regional access problem as much as a national regulatory problem. If future policy changes ease distribution without changing product standards, the largest provincial upside would likely appear first in areas where legal access is now the weakest and unauthorized availability is already visible.

Competitive Landscape

The Canada nicotine pouches market remained tightly concentrated in the authorized tier through 2025 because entry depended on Health Canada's natural health product licensing process and only a very small number of products had cleared that route. That licensing system acts as a structural entry barrier because companies must show safety, efficacy, quality, and a compliant dosage form before legal sale is allowed. Imperial Tobacco Company Ltd., through Zonnic distribution, held the dominant authorized position in the Canadian nicotine pouches market during 2025 because its product was the first to secure legal presence and national awareness within the regulated channel. That position gave it an advantage in pharmacy relationships, compliance readiness, and consumer familiarity, even though overall category discovery remained limited by the narrow legal assortment. The result was a Canada nicotine pouches market where legal competition stayed muted even as interest in the category grew.

The main strategic moves from larger companies have centered on product science, intellectual property, and regulatory positioning rather than aggressive retail expansion. Nicoventures Trading Limited, a British American Tobacco subsidiary, filed a December 2025 patent for a nicotine-polymer complex designed to extend release duration and improve stability, which signals a clear pipeline strategy for future product filings. Fertin Pharma's May 2025 patent application described a precision-release pouch architecture that aimed for faster nicotine release through reduced fill composition, which is another example of differentiation built around delivery performance.[4]Fertin Pharma A/S, “A Pouched Product,” Patent Application, patents-review.com Imperial Tobacco Canada also used its August 2025 one-year review to push for broader authorized points of sale, showing that distribution access itself has become a competitive issue alongside product development.

White space in the Canada nicotine pouches market is still defined by two gaps, a thin moderate-to-low strength range and limited access outside dense pharmacy networks. That leaves room for entrants that can build a compliant product around faster release, better stability, or a more credible step-down profile for adult cessation use. Sesh Products US Inc. showed that adjacent oral nicotine replacement formats can still find a route into Canada, which signals that the legal assortment can widen even beyond the traditional tobacco groups. At the same time, unauthorized imports and illegal retail sales continue to complicate competition because they offer higher strengths and easier access than the legal system allows. Competitive progress in the Canada nicotine pouches market will therefore depend on which companies can navigate Health Canada's pathway quickly while also building products that feel meaningfully different within a narrow legal framework.

Canada Nicotine Pouches Industry Leaders

Philip Morris International Inc.

Imperial Brands plc

JT International SA

Swisher International, Inc.

Turning Point Brands, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Health Canada published Delivering Results: Advancing Canada's Tobacco Strategy, confirming that approximately 300,000 Canadians quit smoking in 2024 and establishing that 3% of those quitters used tobacco-free nicotine pouches, a measurable baseline signaling the category's nascent but growing role in national cessation efforts.

- January 2026: Health Canada revised the Prescription Drug List to formally clarify that nicotine buccal pouches containing 4 milligrams or less of nicotine per dosage unit are non-prescription natural health products, resolving an ambiguity in the regulatory qualifier language and providing a clearer licensing pathway for new product applicants.

- December 2025: Nicoventures Trading Limited, a British American Tobacco subsidiary, filed patent WO2025253338A1 disclosing a nicotine-polymer complex that combines freebase and protonated nicotine forms for modulated 30-60-minute release profiles, improving craving relief duration and storage stability over a 1-12-month shelf-life window.

- August 2025: Imperial Tobacco Canada published a one-year review of the ministerial order's impact, estimating approximately 500 million illegal pouches had entered the Canadian market in 12 months, citing a 2.8% concurrent rise in cigarette sales, and formally requesting that Zonnic's authorized point of sale be extended to front-of-counter pharmacy locations and adult tobacco retail environments.

Canada Nicotine Pouches Market Report Scope

The scope of the report covers the analysis of the nicotine pouches market in Canada. Nicotine pouches are oral products that contain nicotine but do not include tobacco leaf or stem. These pouches are placed between the gum and lip, offering a smokeless and spit-free alternative to traditional tobacco products. The study examines market trends, growth drivers, challenges, and opportunities, providing insights into the competitive landscape and consumer preferences within the forecast period.

The Canada Nicotine Pouches Market Report is Segmented by Product Type (Tobacco-Derived Nicotine Pouches, and Synthetic Nicotine Pouches), Flavor Type (Unflavored Nicotine Pouches, and Flavored Nicotine Pouches), Strength (Low, Moderate, and High), and Distribution Channel (Online, and Offline). The Market Forecasts are Provided in Terms of Value (USD).

| Tobacco-Derived Nicotine Pouches |

| Synthetic Nicotine Pouches |

| Unflavored Nicotine Pouches |

| Flavored Nicotine Pouches |

| Low |

| Moderate |

| High |

| Online |

| Offline |

| By Product Type | Tobacco-Derived Nicotine Pouches |

| Synthetic Nicotine Pouches | |

| By Flavor Type | Unflavored Nicotine Pouches |

| Flavored Nicotine Pouches | |

| By Strength | Low |

| Moderate | |

| High | |

| By Distribution Channel | Online |

| Offline |

Key Questions Answered in the Report

What is the size of the Canada nicotine pouches market?

The Canada nicotine pouches market reached USD 117.47 million in 2025, stood at USD 122.99 million in 2026, and is projected to reach USD 154.75 million by 2031 at a 4.70% CAGR.

What is driving demand for nicotine pouches in Canada?

Demand is being supported by smoking cessation use, harm-reduction positioning, and discreet use in smoke-free settings, although legal access remains tightly controlled through pharmacies.

Which product type leads legal sales in Canada?

Tobacco-derived nicotine pouches led with an 86.34% share in 2025 because the authorized market remained concentrated around a very limited number of licensed products.

Which flavor and strength segments are growing fastest?

Unflavored pouches are projected to grow at a 5.68% CAGR through 2031, while moderate-strength pouches are expected to expand at a 6.05% CAGR over the same period.

Why are pharmacies so important for this category?

Current federal rules require authorized products to be sold behind pharmacy counters or through pharmacy-operated websites with pharmacist involvement, which makes pharmacies the main legal gateway.

What is the biggest competitive challenge for authorized brands?

The biggest challenge is the gap between strict legal access and the ease of unauthorized availability, especially for higher-strength products that continue to circulate in convenience stores and online channels.

Page last updated on: