Canada Global Capability Centers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

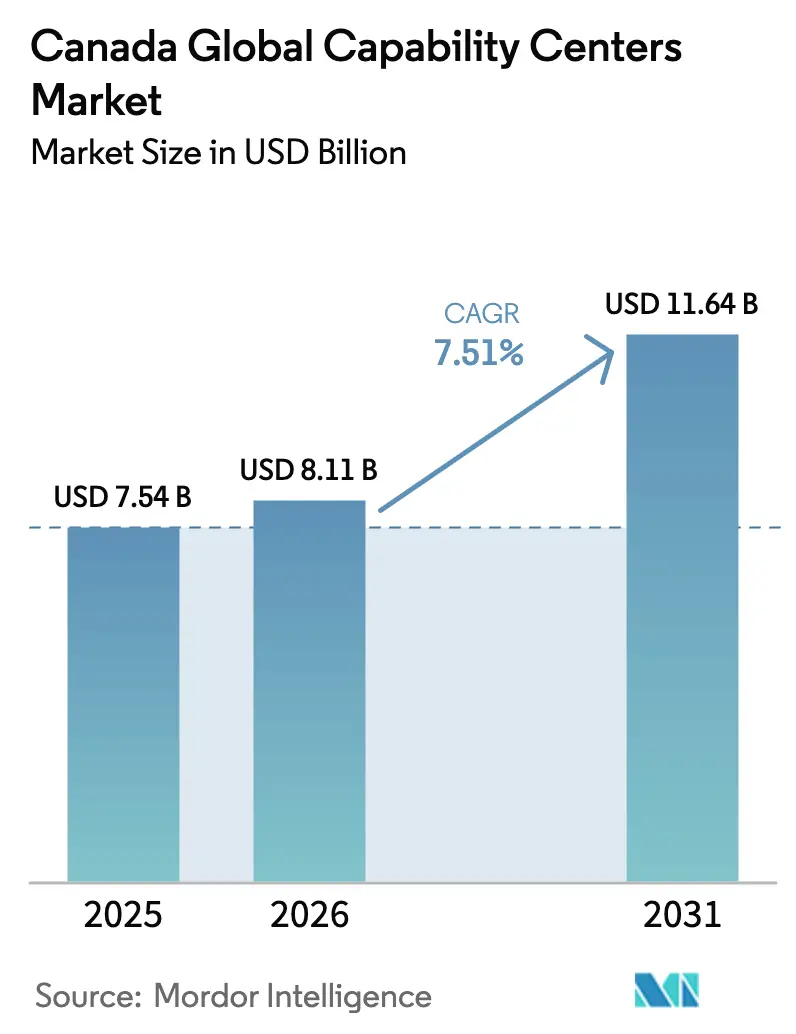

| Base Year Market Size (2025) | USD 7.54 Billion |

| Market Size (2026) | USD 8.11 Billion |

| Market Size (2031) | USD 11.64 Billion |

| Growth Rate (2026 - 2031) | 7.51% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Global Capability Centers Market Analysis by Mordor Intelligence

The Canada Global Capability Centers market size was valued at USD 7.54 billion in 2025 and estimated to grow from USD 8.11 billion in 2026 to reach USD 11.64 billion by 2031, at a CAGR of 7.51% during the forecast period (2026-2031). Robust government incentives for digital innovation hubs, the appeal of near-time collaboration with the United States headquarters, and access to a multicultural bilingual workforce are driving expansion. Regulatory scrutiny around cross-border data transfers is steering regulated industries toward Canadian delivery sites that assure data sovereignty. The intensification of investments by technology giants in Toronto, Vancouver, and Montreal validates Canada’s nearshore attractiveness, while emerging tech corridors in Alberta and Ontario diversify the geographic footprint of the Canada Global Capability Centers market. Competition for senior digital talent and comparatively higher salary costs versus traditional offshore locations temper near-term growth, but do not offset the strategic rationale for Canadian centers.

Key Report Takeaways

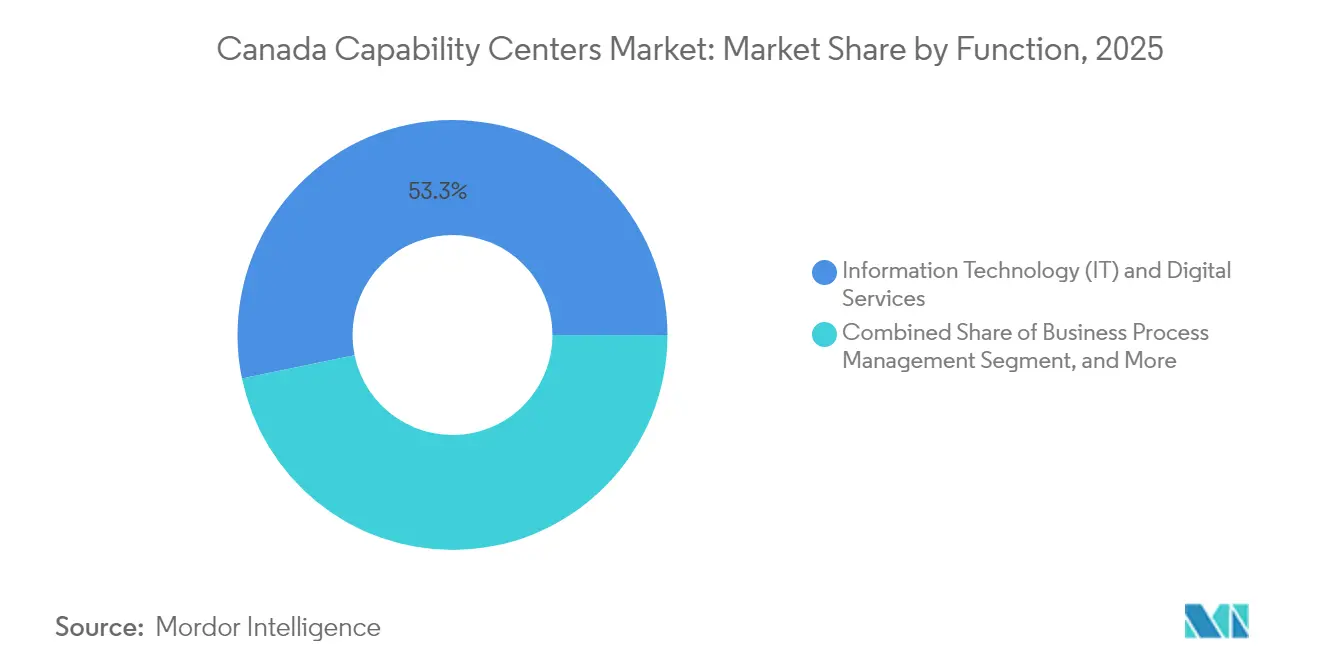

- By function and capability, information technology and digital services led the Canada Global Capability Centers market, accounting for a 53.25% share in 2025, while knowledge process outsourcing posted the fastest growth trajectory, at a 7.63% CAGR through 2031.

- By engagement model, captive operations held 62.74% of the Canada Global Capability Centers market size in 2025, and hybrid build-operate-transfer arrangements are projected to expand at an 8.12% CAGR during 2026-2031.

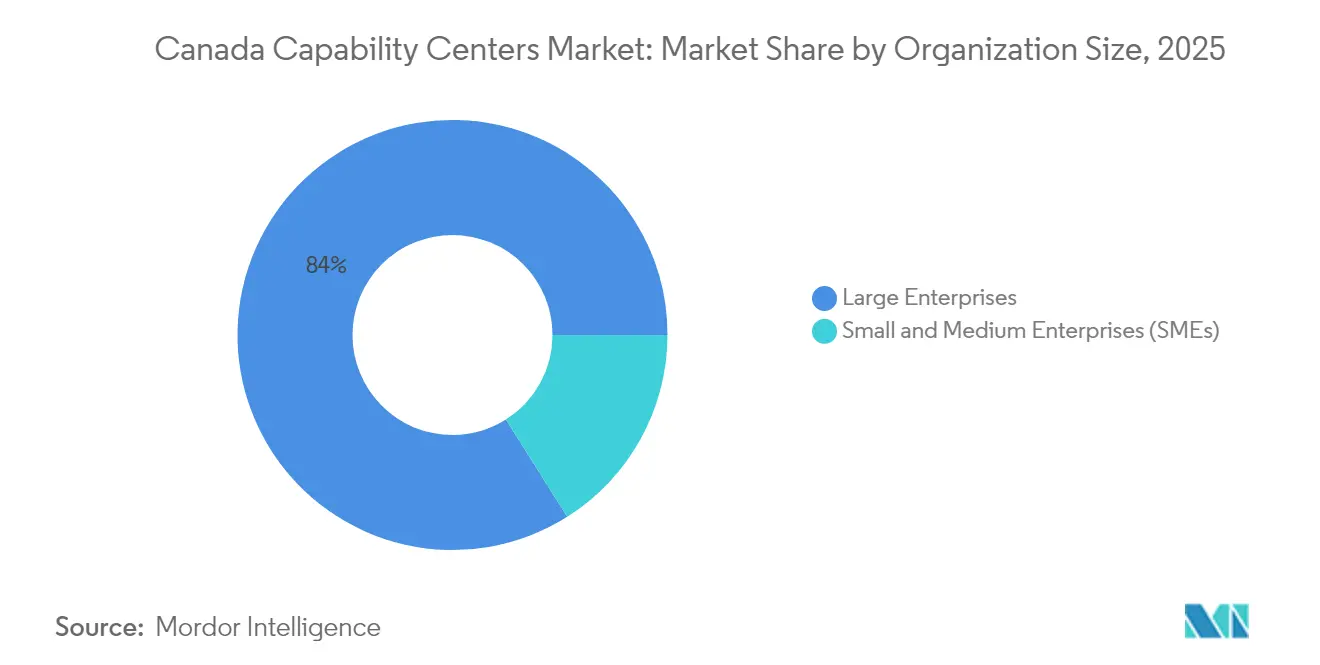

- By organization size, large enterprises accounted for 83.96% of the Canada Global Capability Centers market share in 2025, whereas small and medium enterprises are forecast to grow at a 9.02% CAGR to 2031.

- By industry vertical, banking, financial services, and insurance captured a 34.41% revenue share in 2025, while the healthcare and life sciences sector is projected to advance at an 7.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Global Capability Centers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for Nearshore Time-Zone Alignment with the United States | +2.1% | National, with concentrations in Toronto, Vancouver, and Montreal | Medium term (2-4 years) |

| Government Incentives for Digital Innovation Hubs | +1.8% | National, with provincial variations in Quebec, Ontario, and Alberta | Long term (≥ 4 years) |

| Access to Multicultural, Bilingual Talent Pool | +1.5% | National, with emphasis on Toronto, Vancouver, and Montreal corridors | Long term (≥ 4 years) |

| Rising Cross-Border Data Residency Requirements | +1.3% | National, with regulatory focus on the BFSI and Healthcare sectors | Medium term (2-4 years) |

| Canada-U.S. Critical Technologies Collaboration Roadmap | +0.9% | National, with emphasis on AI and semiconductor hubs | Long term (≥ 4 years) |

| Surge in Climate-Tech Funding Driving Green Global Capability Center Mandates | +0.8% | National, with a concentration in clean energy provinces | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Demand for Nearshore Time-Zone Alignment with the United States

Real-time collaboration across the same working day eliminates the twelve-hour handoff delays that characterize traditional offshore models. Canada Global Capability Centers join live meetings, provide immediate customer support, and synchronize agile sprints with United States teams, which improves productivity and reduces project cycle time. Amazon’s decision to staff more than 8,500 corporate and technology employees across Toronto and Vancouver illustrates how multinational firms leverage proximity to embed Canadian sites inside global delivery networks.[1]Amazon Staff, “Check Out The Latest Developments at Amazon's Vancouver and Toronto Tech Hubs,” aboutamazon.ca Financial institutions place a premium on concurrent collaboration because regulatory reporting cut-offs demand instant data validation and sign-off. As enterprises trade pure labor arbitrage for speed and quality advantages, the Canada Global Capability Centers market captures mandates that once defaulted to Asia-Pacific locations.

Government Incentives for Digital Innovation Hubs

Federal and provincial programs lower the entry costs for both foreign investors and Canadian scale-ups. The Canadian Sovereign AI Compute Strategy commits CAD 2 billion (USD 1.58 billion) through 2030 to expand domestic AI compute capacity and fund the AI Compute Challenge. Quebec provided CAD 48 million (USD 37.92 million) for the Ax-C Montreal hub, with private partners led by Google Cloud adding CAD 5.25 million (USD 4.15 million). Alberta’s AI Data Centers Strategy targets CAD 100 billion (USD 79 billion) in private investment over five years to attract hyperscale facilities. These layered incentives reduce setup time, subsidize infrastructure, and enhance the value proposition for hosting high-compute workloads in Canada.

Access to Multicultural Bilingual Talent Pool

Immigration-friendly policies combined with a diverse domestic workforce deliver language and cultural fluency across major global markets. One-third of Canada’s tech labor force identifies as Asian, and the share of women in technical roles is rising, broadening the available talent base.[2]CBRE, “Tech-30 2024: Measuring the Tech Industry's Impact on U.S. and Canadian Office Markets,” cbre.com Infosys’s pledge to create 8,000 Canadian jobs and its partnerships with fourteen universities prove how Canada Global Capability Centers scale quickly by tapping both newcomers and local graduates. Bilingual proficiency in English and French enables centers in Quebec to serve francophone markets without incurring additional localization costs.

Rising Cross-Border Data Residency Requirements

Privacy legislation in Canada, coupled with sector-specific mandates such as the Office of the Superintendent of Financial Institutions Technology and Cyber Risk guidelines, pushes regulated enterprises to keep customer information within national borders. Microsoft’s CAD 680 million (USD 537.2 million) investment in Quebec's data infrastructure, combined with IBM’s multi-zone cloud region in Montreal, provides Canada Global Capability Centers with compliant hosting options, thereby reducing legal risk and latency. As penalties for non-compliance escalate worldwide, companies are increasingly opting for onshore or nearshore environments that simplify audits and certifications.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher Average Salary Cost vs. Traditional Offshore Locations | -1.2% | National, with premium costs in Toronto, Vancouver | Short term (≤ 2 years) |

| Intensifying Competition for Senior Digital Talent in Toronto and Vancouver | -0.8% | Toronto and Vancouver metropolitan areas | Medium term (2-4 years) |

| Delays in Work-Permit Processing for Foreign Specialists | -0.6% | National, affecting all major tech centers | Short term (≤ 2 years) |

| Scarcity of Large-Floorplate, Class-A Office Spaces in Emerging Tech Corridors | -0.4% | Secondary markets outside Toronto, Vancouver, and Montreal | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Higher Average Salary Cost vs. Traditional Offshore Locations

Canadian software engineers earn significantly more than their peers in India or the Philippines, so labor no longer underpins the business case in isolation. Although wages remain 46% lower than those in comparable roles in the United States, payroll still represents the largest cost element for Global Capability Centers. Operators offset the premium through productivity gains, lower travel overhead, and reduced rework associated with cultural misalignment. As Centers of Excellence replace routine tasks, companies measure value by speed-to-market and quality rather than headline hourly rates.

Intensifying Competition for Senior Digital Talent in Toronto and Vancouver

Technology giants and start-ups often recruit from the same finite pool of leadership talent, which can lead to increased compensation and a higher risk of attrition. Amazon’s 79,000 square-foot Toronto expansion and its new Vancouver tower have accelerated the scramble for principal engineers and product managers.[3]Evan Duggan, “Amazon to grow Toronto tech hub, open Vancouver office North Tower,” renx.ca Canada's Global Capability Centers diversify to Montreal, Calgary, and emerging corridors, but senior specialists remain clustered in the largest metropolitan areas, where lifestyle amenities and professional networks converge. Firms respond with equity grants, internal academies, and distributed team structures to smooth demand spikes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Function / Capability: IT Services Backbone Faces Knowledge Work Upshift

Information technology and digital services remained the anchor in 2025, generating 53.25% of the Canada Global Capability Centers market share. Mature service catalogs covering application maintenance, cloud migration, and cybersecurity continue to renew multi-year contracts, anchoring operating margins for incumbents. Yet, knowledge process outsourcing is accelerating at a 7.63% CAGR to 2031 as enterprises transfer analytics, regulatory reporting, and domain-specific research to Canada, where cultural proximity and language proficiency reduce context-setting cycles. In this shift, the Canada Global Capability Centers market size for knowledge-led mandates is projected to outpace traditional IT budgets over the forecast horizon.

A rise in applied-AI projects indicates how knowledge work is scaling. Scale AI directed CAD 96 million (USD 75.84 million) toward twenty-two industry collaborations in 2024, creating applied research pipelines that Canada Global Capability Centers can leverage for fast-track proofs of concept. Engineering and R&D hubs in Ottawa and Montreal collaborate with parent-company labs in the United States, leveraging synchronized time zones for daily stand-ups. As a result, value metrics now emphasize design velocity and intellectual property creation rather than ticket closures, heralding a strategic repositioning of Canadian centers in global portfolios.

By Engagement Model: Captive Control Balanced with Hybrid Flexibility

Captive formats accounted for 62.74% of the Canada Global Capability Centers market size in 2025, reflecting corporate desires for tight stewardship of data and processes. Firms often choose this route when intellectual property risks surpass the cost benefits of outsourcing. However, the hybrid build-operate-transfer model is forecast to grow at an 8.12% CAGR through 2031 as businesses seek phased ownership that mitigates entry friction. Under this structure, a specialist partner establishes the site, recruits staff, and hands over operations once key performance indicators stabilize.

Ericsson’s CAD 634.8 million (USD 501.5 million) incremental spend across Ottawa and Montreal R&D labs demonstrates how hybrid arrangements utilize government and academic alliances to augment internal capacity. The rapid permit processing through the Global Skills Strategy, which targets two-week approvals, further mitigates the risks associated with hybrid rollouts for niche skill sets. Over time, enterprises treat hybrids as strategic options, toggling between self-managed and partner-managed phases to match project cycles and capital allocation preferences.

By Organization Size: Enterprise Scale Paves the Way for SME Uptake

Large corporations controlled 83.96% of the Canada Global Capability Centers market share in 2025, owing to sizable transformation budgets and seasoned global sourcing teams. These players absorb early-stage costs for compliance audits, office build-outs, and cross-border governance frameworks. Their presence also seeds supplier ecosystems, from facilities management to cloud hosting, which later benefits smaller entrants.

Small and medium-sized enterprises, although nascent, are projected to deliver the highest growth at a 9.02% CAGR. Cloud-native platforms and managed service orchestrators reduce fixed infrastructure costs, allowing mid-market firms to orchestrate design, support, and analytics from Canada at a modest scale. Clio’s CAD 900 million (USD 711 million) fundraising round underscores how Canadian scale-ups are now reaching valuation thresholds that support multi-function centers serving overseas users. Provincial funding streams, such as Ontario’s Critical Industrial Technologies Program, which supports cybersecurity sandboxes, further level the playing field for SMEs seeking to internationalize quickly.

By Industry Vertical: BFSI Stays Dominant While Healthcare Rises

Banking, financial services, and insurance generated 34.41% of Canada's Global Capability Centers market revenue in 2025, leveraging Canada’s regulatory alignment with U.S. frameworks and the strict data residency mandates that shape cross-border financial flows. Centers in Toronto and Montreal house anti-money laundering operations, model validation, and real-time trading support, tasks where latency and compliance risks converge. The vertical’s maturity offers reference architectures that newer industries emulate.

Healthcare and life sciences show the strongest momentum, advancing at an 7.92% CAGR through 2031. IBM and government partners committed CAD 187 million (USD 147.73 million) to reinforce semiconductor assembly and testing for medical applications, ensuring a secure domestic supply for compute-heavy clinical workloads. Canada Global Capability Centers in this sector absorb regulatory affairs, pharmacovigilance, and digital therapeutics support, capitalizing on Health Canada’s proximity for faster approvals. Manufacturing, automotive, and clean-energy segments follow, often integrating climate-tech mandates bolstered by the forthcoming Wonder Valley hyperscale park in Alberta.

Geography Analysis

Toronto anchors the national footprint, supported by the country’s deepest financial services cluster and a steady inflow of STEM graduates from the University of Toronto and adjacent institutions. Amazon, IBM, and major banks collectively employ thousands in the downtown core, solidifying a self-reinforcing ecosystem that fuels the continuous expansion of the Canada Global Capability Centers market. Vancouver ranks second, its Pacific orientation aligning with Asia-Pacific business hours, an advantage for firms managing follow-the-sun DevOps or gaming pipelines. Vancouver’s talent draw is strong, but rising housing costs necessitate supplemental hiring in nearby Fraser Valley cities.

Montreal’s ascent is rooted in decades of public investment in artificial intelligence, spearheaded by institutions such as MILA, and a bilingual workforce serving francophone clients in Europe and Africa. Quebec’s tax credits and funding programs lower effective operating costs, offsetting higher French-language compliance requirements. Microsoft’s and Google’s cloud multimodal regions provide the hyperscale backbone that underpins data residency for life sciences and public sector workloads.

Beyond the big three metros, Calgary and Edmonton are leveraging their legacy energy sector engineering expertise to pivot toward digital twin and clean-tech applications. Alberta’s AI Data Centers Strategy and hyperscale facilities north of Calgary reduce latency for Western Canada operations while offering meaningful cost arbitrage over Toronto and Vancouver rents. Ottawa, home to federal agencies and telecom innovators, benefits from Ericsson’s R&D expansion, positioning the region as a hub for secure network technology. Waterloo and Halifax offer university-linked feeder locations, enabling companies to attract early-career talent before they relocate to larger cities. Together, these corridors broaden the Canada Global Capability Centers market beyond traditional urban anchors, enhancing resilience to localized talent or real-estate volatility.

Competitive Landscape

The market is moderately fragmented, with Indian IT services majors, United States-headquartered consultancies, and Canadian niche specialists competing for wallet share. Tata Consultancy Services, Infosys, and Wipro extend their established client relationships to Canadian nearshore footprints, leveraging common toolchains for seamless multishore delivery. North American consultancies, including the Big Four, differentiate on cultural alignment and boardroom access, providing integrated advisory and operational execution services. Local specialists carve vertical niches, particularly in health data stewardship and clean-energy analytics.

Technology modernization sets the battleground. Providers channel capital into proprietary AI accelerators, robotics process automation, and cybersecurity solutions, such as the uOttawa-IBM facility, which provides customers with sandbox access to test zero-day responses without affecting production systems.[4]IBM Canada, “Ontario Centre of Innovation, IBM Canada and uOttawa Announce a Strategic Partnership,” canada.newsroom.ibm.com Government immigration pathways that promise two-week visa processing offer early-mover advantages to firms that master the nuances of compliance. Meanwhile, talent scarcity drives continued mergers and acquisitions as players acquire boutique firms to secure specialized teams in quantum, generative AI, and semiconductor design.

White-space opportunities proliferate in regulated verticals where domain knowledge creates switching costs. Providers offering turnkey solutions that embed compliance artifacts into delivery workflows capture premium pricing despite wage inflation. In parallel, climate-aligned mandates are driving demand for centers that manage carbon accounting and optimize renewable assets, utilizing Alberta’s forthcoming hyperscale compute grids. Across segments, success hinges on moving up the value chain from labor-based billing to outcome-based contracts that tie fees to business impact.

Canada Global Capability Centers Industry Leaders

Tata Consultancy Services Canada Inc.

Accenture Inc.

IBM Canada Ltd.

Cognizant Technology Solutions Canada, ULC

Capgemini Canada Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: AXL unveiled a USD 15 million venture studio that will cultivate 50 artificial intelligence start-ups in Canada over the next five years. Working alongside NVIDIA, AMD, and Microsoft, the studio offers high-performance compute power and technical expertise, further deepening the AI talent and infrastructure supporting Canadian Global Capability Centers.

- August 2025: CGI purchased Apside, a France-based IT consulting firm with Canadian operations, for CAD 229.9 million (USD 169.4 million). The deal added about 2,400 professionals worldwide and broadened CGI’s digital transformation and cloud delivery capabilities across Europe and Canada.

- August 2025: OpenText and TELUS announced a Canadian Sovereign Cloud partnership that will go live in September 2025. The service will provide secure, regulation-compliant cloud environments for domestic enterprises and government agencies, meeting stringent data-residency requirements.

- June 2025: The Ax.c innovation hub officially opened in Montreal, backed by CAD 48 million in public funding and CAD 5.25 million from partners, including Google Cloud and Bell. The site offers shared AI infrastructure and collaboration space for both start-ups and established firms, reinforcing Quebec’s position as an AI center of excellence.

Canada Global Capability Centers Market Report Scope

The scope of the global capability center study for the market segmentation by the Function/Capability for (i) Information Technology (IT) and Digital Services segment is limited to Software Development, Cloud and Infrastructure Management, Cybersecurity, Data Analytics and AI/ML; (ii) Engineering / ER&D segment is limited to Product Design and Testing, Embedded Systems, Digital Twin / Simulation; (iii) Business Process Management (BPM) segment is limited to Finance and Accounting, HR, Payroll and Talent Management, Procurement, Customer Service; and (iv)Knowledge Process Outsourcing (KPO) segment is limited to Market Research and Insights, Risk and Compliance, Legal and Regulatory Support, Strategy and Consulting Support. Similarly, for segmentation by the Engagement Model, scope for (i) Hybrid Build-Operate-Transfer (BOT) is limited to Joint Venture / Strategic Partnership and Virtual Captive Model. The rest of the segment scope is as specified for the listed segment.

| Information Technology (IT) and Digital Services |

| Engineering / ER&D |

| Business Process Management (BPM) |

| Knowledge Process Outsourcing (KPO) |

| Captive (Self-Build) / In-House |

| Build-Operate-Transfer (BOT) |

| Hybrid Build-Operate-Transfer (BOT) |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| Banking, Financial Services, and Insurance (BFSI) |

| Telecom and IT |

| Healthcare and Life Sciences |

| Manufacturing, Automotive and Industrial |

| Retail and Consumer Goods |

| Other Industry Verticals |

| By Function / Capability | Information Technology (IT) and Digital Services |

| Engineering / ER&D | |

| Business Process Management (BPM) | |

| Knowledge Process Outsourcing (KPO) | |

| By Engagement Model | Captive (Self-Build) / In-House |

| Build-Operate-Transfer (BOT) | |

| Hybrid Build-Operate-Transfer (BOT) | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises (SMEs) | |

| By Industry Vertical | Banking, Financial Services, and Insurance (BFSI) |

| Telecom and IT | |

| Healthcare and Life Sciences | |

| Manufacturing, Automotive and Industrial | |

| Retail and Consumer Goods | |

| Other Industry Verticals |

Key Questions Answered in the Report

How large is the Canadian Global Capability Centers market in 2026?

It is estimated at USD 8.11 billion, with a forecast to reach USD 11.64 billion by 2031.

What is the expected growth rate of Canadian Canada Global Capability Centers through 2031?

The market is projected to grow at a 7.51% CAGR over the 2026-2031 period.

Which functions dominate Canadian Global Capability Centers today?

Information technology and digital services contribute 53.25% of revenue, though knowledge process outsourcing is scaling fastest at a 7.63% CAGR.

Why are companies choosing Canada over traditional offshore locations?

Near-time collaboration with U.S. teams, strong data sovereignty compliance, and generous innovation incentives outweigh higher wages.

Which provinces offer the most attractive incentives for Global Capability Centers?

Quebec, Ontario, and Alberta provide the strongest packages, including AI-compute grants, tax credits, and expedited visa programs.

Which industry vertical is growing fastest within Canadian Global Capability Centers?

The healthcare and life sciences sector is advancing at an 7.92% CAGR, thanks to stringent data residency rules and a vibrant life sciences ecosystem.

Page last updated on: