Canada Frontline Worker Technology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 0.75 Billion |

| Market Size (2026) | USD 0.88 Billion |

| Market Size (2031) | USD 2.45 Billion |

| Growth Rate (2026 - 2031) | 22.70% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Frontline Worker Technology Market Analysis by Mordor Intelligence

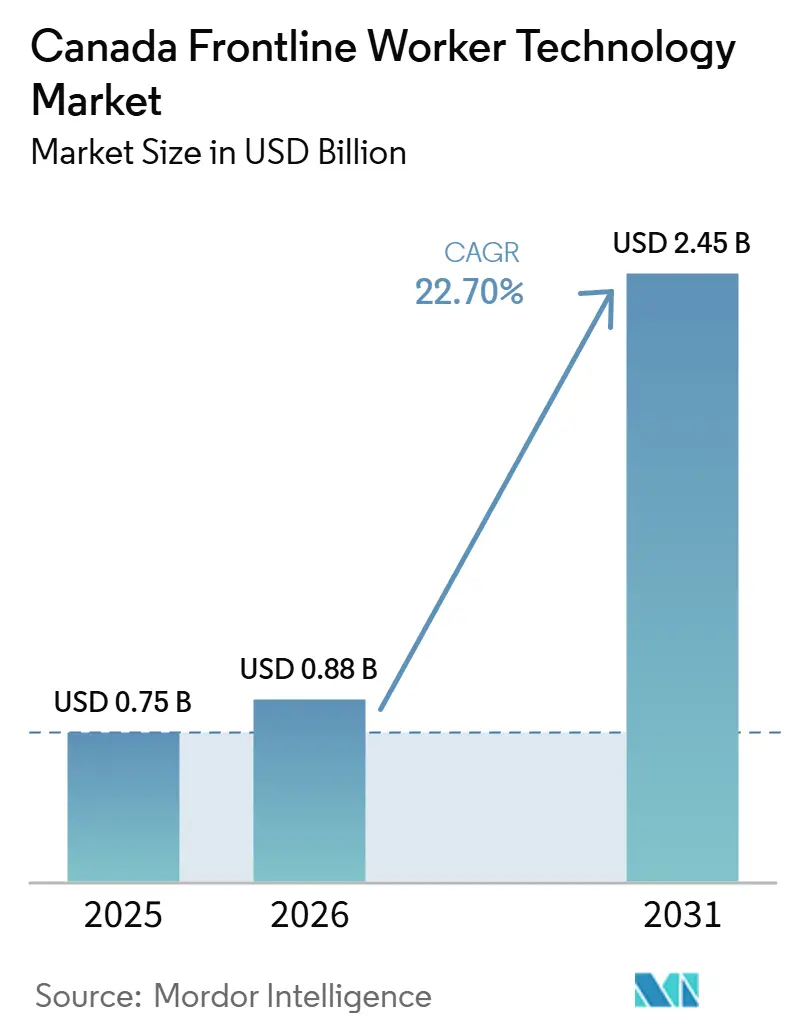

The Canada frontline worker technology market size is projected to be USD 0.75 billion in 2025, USD 0.88 billion in 2026, and reach USD 2.45 billion by 2031, growing at a CAGR of 22.70% from 2026 to 2031. The Canada frontline worker technology market is expanding as employers across retail, healthcare, logistics, and construction move more daily work onto mobile platforms built for deskless teams. A long period of lower technology spending on frontline employees is now giving way to stronger adoption of mobile-first tools, AI-assisted workflows, and connected communication systems that fit non-desk settings. Rising labor costs, staffing shortages, and the operational cost of manual scheduling errors are pushing employers to replace reactive processes with more consistent workforce planning and execution. The Canada frontline worker technology market is also being shaped by software-led business models, cloud deployment, and modular SaaS pricing, which have widened adoption beyond the largest enterprises. Integration complexity with older HR, ERP, and POS systems still slows some projects, and security reviews remain a necessary step, but the overall demand backdrop remains favorable.

Key Report Takeaways

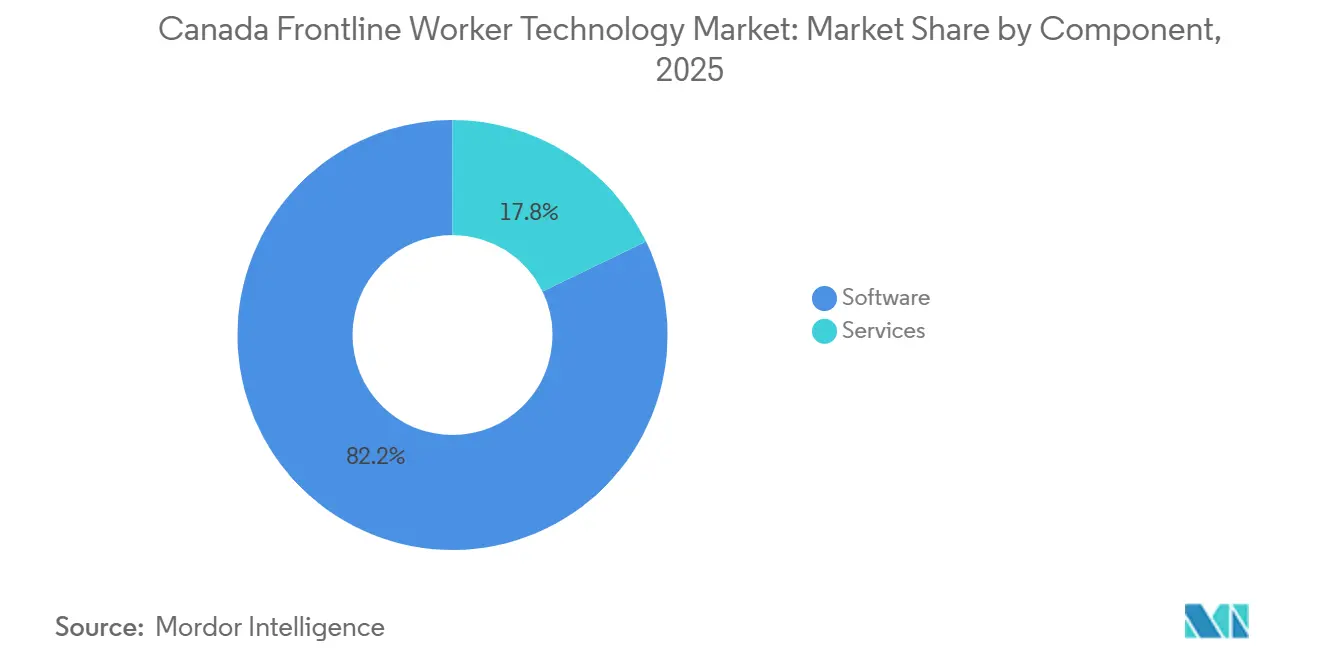

- By component, software held 82.16% of the Canada frontline worker technology market share in 2025, while services is projected to expand at a 25.84% CAGR through 2031.

- By deployment, cloud-based deployment accounted for 81.28% share of the Canada frontline worker technology market size in 2025 and is projected to grow at a 23.31% CAGR through 2031.

- By organization size, large enterprises held a 70.42% share in 2025, while small and medium enterprises are projected to record the fastest CAGR of 24.68% through 2031.

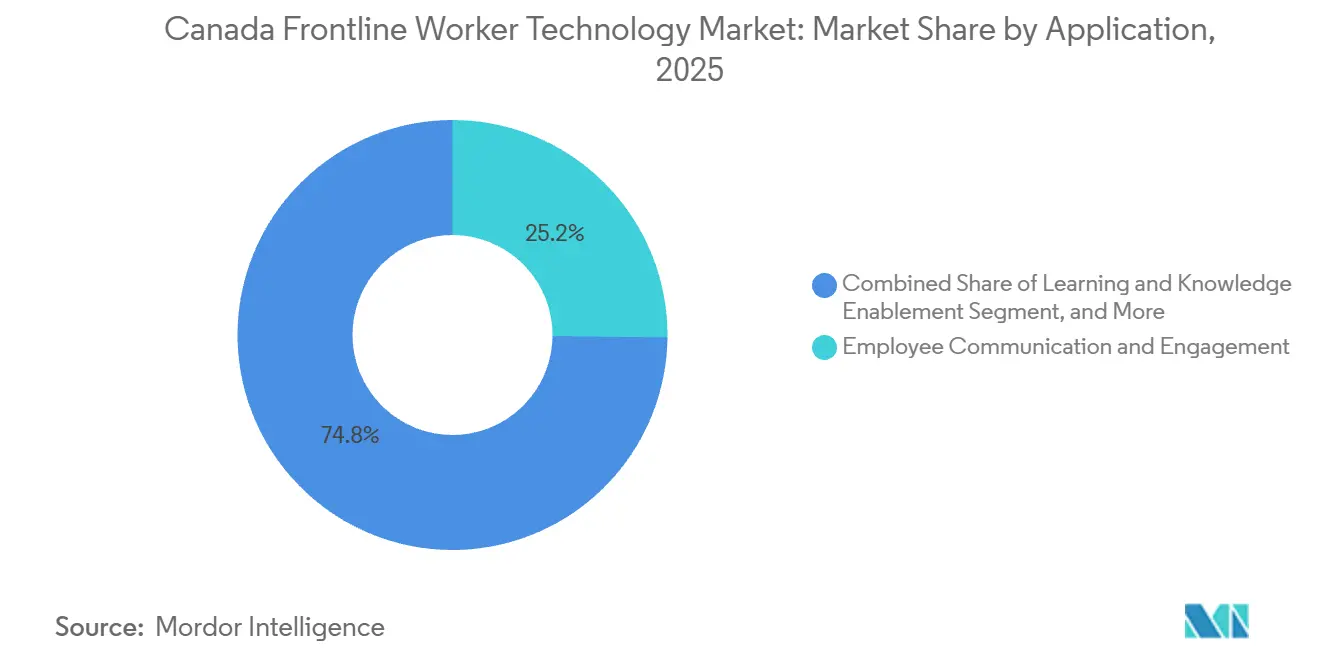

- By application, employee communication and engagement held a 25.18% share in 2025, while workforce analytics and performance management is projected to expand at a 26.12% CAGR through 2031.

- By end-user industry, retail and e-commerce held a 27.36% share in 2025, while healthcare and life sciences is projected to advance at a 25.96% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Canada Frontline Worker Technology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Need for Real-Time Frontline Workforce Visibility | +4.8% | National, with peak demand in Ontario manufacturing corridor, British Columbia logistics, and Alberta energy | Short term (≤ 2 years) |

| AI-Enabled Scheduling and Labor Forecasting Adoption | +4.2% | National, with early commercial gains in Ontario, British Columbia, and Quebec | Medium term (2-4 years) |

| Mobile-First Digitization of Deskless Workflows | +3.5% | National, accelerating in remote construction, northern logistics, and rural healthcare delivery | Short term (≤ 2 years) |

| Convergence of HR, Payroll, and Communication Stacks | +2.8% | National, led by large multi-site retailers and healthcare systems | Medium term (2-4 years) |

| Compliance Pressure from Provincial Labor and Privacy Rules | +2.1% | Quebec-led, with spill-over to British Columbia and Alberta, and a compliance factor for federally regulated employers | Medium term (2-4 years) |

| Audit-Ready Workforce Decisioning and Explainable Automation | +1.6% | National, concentrated in healthcare, financial services, and public administration | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Need for Real-Time Frontline Workforce Visibility

Real-time visibility has become the strongest demand trigger in the Canada frontline worker technology market because employers want fewer blind spots across attendance, task execution, and shift performance. The buying discussion is moving away from pure cost control and toward continuity, margin protection, and better coordination across multi-site operations. That change matters because it shortens the path from operational pain to purchase approval in the Canada frontline worker technology market. Zebra Technologies expanded this visibility theme in June 2026 when it introduced a machine vision ecosystem with on-device AI, real-time locationing, and jam detection for manufacturing environments.[1]Zebra Technologies Corporation, “Transforming Manufacturing Workflows: Zebra Technologies Unveils Machine Vision Ecosystem at Automate 2026,” Zebra Technologies, zebra.com The offer shows that buyers increasingly expect a connected stack rather than isolated tools, which supports wider platform adoption in the Canada frontline worker technology market. As a result, vendors that tie device activity, task status, and workflow analytics together are in a stronger position to win expansion contracts.

AI-Enabled Scheduling and Labor Forecasting Adoption

AI-based scheduling is moving from selective testing to everyday use in the Canada frontline worker technology market as employers look for better labor matching and less manual roster work. The key gap is not simple access to AI, but how well AI is built into the actual workflow used by frontline managers and workers. That makes embedded design more valuable than stand-alone analytics in the Canada frontline worker technology market. WorkJam reinforced this direction in January 2026 when it released a major platform update with AI agents placed directly inside task verification and audit workflows. The same shift was visible in June 2025 when WorkJam expanded its collaboration with Google Cloud around frontline AI agents. In the Canada frontline worker technology market, this kind of embedded AI is likely to raise daily use because it reduces the need for managers to move between separate systems.

Mobile-First Digitization of Deskless Workflows

Mobile-first digitization continues to widen the reach of the Canada frontline worker technology market because frontline work often happens away from desks, fixed terminals, and stable office routines. The commercial value rises further when devices can support offline work, image capture, and on-device processing in field conditions. Zebra’s TC501 and TC701 mobile computers, introduced in 2026 as part of its broader frontline AI push, were positioned around this shift toward real-time frontline execution at the device level. Getac added to the same direction in June 2026 with the ZX80W and ZX80W-EX rugged Windows 11 tablets for transport, logistics, and industrial settings. These launches matter because they strengthen the field hardware base that supports software adoption in the Canada frontline worker technology market. They also make mobile workflow tools more practical in remote construction, logistics, and service environments.

Convergence of HR, Payroll, and Communication Stacks

The move toward unified workforce platforms is reshaping the Canada frontline worker technology market because employers want fewer vendors and simpler operations. Scheduling, payroll, communication, task tracking, and staffing are increasingly being purchased as connected functions rather than separate software layers. That raises switching costs and gives established platforms more room to grow inside existing accounts in the Canada frontline worker technology market. Dayforce moved in this direction in September 2025 when it expanded Dayforce Flex Work to include vendor management, on-demand staffing, and agency network capabilities in a mobile-first interface. WorkJam’s June 2025 Google Cloud expansion also supported stack convergence by bringing AI capability into the same system used for scheduling and frontline execution. In the Canada frontline worker technology market, this kind of platform bundling supports higher retention because finance, HR, and operations all become tied to the same workflow layer.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration Complexity with Legacy HR, ERP, and POS Systems | -2.8% | National, most acute in mid-market retail, manufacturing, and public sector across Ontario and Quebec | Short term (≤ 2 years) |

| Mobile Cybersecurity and Workforce Data Privacy Risks | -2.3% | National, with elevated exposure in Quebec and British Columbia, and regulatory influence on federally regulated employers | Medium term (2-4 years) |

| Shared Device Identity and Access Management Gaps | -1.5% | National, concentrated in retail, healthcare, and hospitality where shared-device workflows are standard | Medium term (2-4 years) |

| Worker Resistance to Opaque Scheduling Automation | -1.0% | National, most pronounced in unionized manufacturing and public sector environments in Ontario and Quebec | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Integration Complexity with Legacy HR, ERP, and POS Systems

Integration complexity remains the most persistent deployment barrier in the Canada frontline worker technology market because many employers still run older HR, ERP, and POS environments. The problem becomes harder as organizations grow because each added legacy system creates more dependencies, more testing, and longer implementation timelines. That leaves some of the largest frontline employers facing the biggest rollout barriers in the Canada frontline worker technology market. WorkJam addressed this issue in October 2025 through its FastTrack Program for qualifying UKG Pro Workforce Management customers, using pre-configured bi-directional connectors to speed deployment. The launch shows that vendors now treat faster integration as a product feature rather than only a service step. In the Canada frontline worker technology market, that response is important because delayed implementation can weaken the business case even when the frontline need is clear.

Mobile Cybersecurity and Workforce Data Privacy Risks

Security and privacy concerns continue to slow some purchases in the Canada frontline worker technology market, especially where shared devices and regulated worker data are part of daily operations. This issue is strongest in settings such as healthcare, hospitality, and retail, where several workers may use the same endpoint during a single day. Quebec’s Law 25 has made privacy assessments and clearer disclosure a more active part of technology deployment decisions, which adds weight to security design in the Canada frontline worker technology market.[2]Gouvernement du Québec, “Projets de Transcription Par Intelligence Artificielle - Professionnels de la Santé,” Gouvernement du Québec, quebec.ca The result is that cybersecurity is no longer a secondary feature set, but a screening condition before contracts move ahead. Vendors that can show stronger identity control, auditability, and governance are likely to face fewer objections during procurement. That is especially true when scheduling, communication, and worker records all sit on the same platform.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Platform Economics Reshape Revenue Mix

Software held 82.16% of revenue in 2025, which kept the software layer at the center of the Canada frontline worker technology market. Buyers are favoring platforms that combine scheduling, communication, task management, and analytics inside one subscription because that reduces tool sprawl and makes rollout easier across large frontline teams. This pattern also supports recurring revenue models, which remain one of the defining commercial features of the Canada frontline worker technology market. WorkJam’s June 2025 expansion with Google Cloud showed how software providers are continuing to add AI features to protect product depth and raise platform value over time. That product direction keeps the software segment ahead of hardware-only offers in day-to-day workforce operations.

Services is projected to expand at a 25.84% CAGR through 2031, making it the fastest-growing component in the Canada frontline worker technology market. The reason is practical, because implementation, integration, change management, and ongoing support still require meaningful hands-on work. As platform deployments become more complex across provinces, sites, and legacy systems, services remain tied to successful adoption rather than optional add-ons. This has pushed vendors to keep more service capability close to the platform so they can protect customer relationships and reduce execution risk. In the Canada frontline worker technology industry, the balance between software scale and service depth is likely to remain important as adoption spreads beyond early large-enterprise buyers.

By Deployment: Cloud Consolidates While Hybrid Keeps Strategic Relevance

Cloud-based deployment captured 81.28% share in 2025, and cloud also represents the fastest-growing model with a 23.31% CAGR through 2031. That combination shows that the Canada frontline worker technology market is still deep in migration rather than nearing deployment maturity. Cloud remains attractive because multi-site employers need centralized updates, common visibility, and simpler administration across frontline locations. The Canada frontline worker technology market size for cloud-based deployment is being reinforced by the operational need to connect workers, managers, and central teams without relying on local infrastructure. This model also fits subscription pricing and faster feature delivery, which support broader adoption across sectors.

Hybrid and on-premises options still matter because some organizations want tighter control over data location, internal governance, or union-sensitive attendance records. This is especially relevant in healthcare, public administration, and multi-province operations where compliance and internal policy can shape architecture choices. Quebec’s regulatory environment has strengthened the case for careful deployment design rather than a one-model approach. As a result, vendors that offer hybrid readiness are better placed to serve the full Canada frontline worker technology market rather than only the least regulated accounts. In practice, a credible local strategy now depends on cloud strength with enough flexibility to support selective local control.

By Organization Size: SME Adoption Broadens the User Base

Large enterprises held a 70.42% share in 2025, which reflected the early concentration of spending among employers with larger budgets and dedicated IT support. For years, that made the Canada frontline worker technology market more accessible to national retailers, larger health systems, logistics groups, and other scaled employers. Large organizations also had a stronger reason to invest because multi-site scheduling, communication, and compliance problems carried a wider financial effect. Their early adoption helped define the feature set now expected across the Canada frontline worker technology market. It also created the installed base that incumbent vendors are working to defend.

Small and medium enterprises are projected to grow at a 24.68% CAGR through 2031, which marks the fastest pace among organization sizes. Modular SaaS pricing, mobile-native interfaces, and quicker deployment models have lowered the entry barrier that once limited adoption to larger firms. This is widening the addressable demand pool in the Canada frontline worker technology market, especially in retail, hospitality, and construction. Quebec-based Agendrix reflects this opening because its offer is closely aligned with scheduling and time management needs for smaller Canadian employers. Faster go-live timelines also make SME demand commercially appealing because revenue can be recognized sooner and expansion paths can develop from a smaller initial contract base.

By Application: Analytics Gains Ground as Engagement Stays Foundational

Employee communication and engagement held a 25.18% share in 2025, which made it the largest application in the Canada frontline worker technology market. That leadership reflects a basic operating need, because frontline workers often do not have reliable access to corporate email or internal desktop systems. Communication tools are therefore serving as a first adoption point for many employers that later add scheduling, task execution, or analytics. WorkJam’s Manufacturing Connect launch in December 2025 directly targeted this gap in industrial settings, where bulletin boards and disconnected channels still limited frontline information flow.[3]WorkJam, “WorkJam Launches Manufacturing Connect to Re-Engage Disconnected Frontline Employees,” PRWeb, prweb.com Communication remains foundational because other workflow tools are harder to scale when the worker connection layer is weak.

Workforce analytics and performance management is projected to grow at a 26.12% CAGR through 2031, making it the fastest-growing application. Employers want frontline activity to translate into measurable attendance, execution, and productivity views that senior management can actually use. This is shifting the Canada frontline worker technology market away from basic coordination alone and toward stronger decision support. The Canada frontline worker technology market size for workforce analytics and performance management is benefiting from the push to connect operational events with business outcomes, even when those tools are sold as part of larger platforms. Vendors that combine analytics with scheduling and task execution are likely to hold an advantage because buyers prefer fewer data handoffs and less reconciliation work.

By End-User Industry: Retail Leads While Healthcare Expands Fastest

Retail and e-commerce held the largest end-user share at 27.36% in 2025, keeping this segment at the front of the Canada frontline worker technology market. High turnover, complex multi-location scheduling, and rising service expectations keep workforce coordination under constant pressure in retail settings. That operating environment continues to support the adoption of communication, scheduling, and task verification tools across the Canada frontline worker technology market. Zebra’s January 2026 retail frontline AI launch showed how vendors are tailoring product depth for store operations, inventory verification, and worker communication. Retail’s large installed workforce base is likely to keep it central to vendor strategy over the forecast period.

Healthcare and life sciences is projected to grow at a 25.96% CAGR through 2031, which makes it the fastest-growing end-user segment. Staffing pressure, audit needs, and shift accuracy are pushing employers in this area toward tighter digital coordination. Staffy Health’s biometric shift check-in launch in July 2025 showed how workforce identity and compliance can be built directly into frontline workflow tools. Quebec also supported digital uptake through its AI scribe program for frontline primary care providers in 2025-2026. Construction and industrial operations are also moving forward, as shown by Crewscope’s February 2026 deployment with EllisDon on the Toronto Western Hospital expansion project.

Geography Analysis

Ontario and British Columbia remain the main deployment centers within the Canada frontline worker technology market because both provinces combine strong employer density with large frontline workforces. Ontario has a broad mix of retail, logistics, and manufacturing demand, which keeps scheduling, safety reporting, and task verification use cases active across multiple sectors. British Columbia adds strength through port logistics, healthcare, and public service employment, which gives vendors a diversified customer base. In 2026, these two provinces will continue to drive the largest share of new platform rollouts and expansion activity within the Canada frontline worker technology market. Their importance also shapes vendor road maps because product depth in compliance, mobile execution, and multi-site visibility tends to be tested first in these higher-volume provincial markets.

Quebec stands apart in the Canada frontline worker technology market because regulation and local software capability both play a larger role there. Law 25 has made privacy assessment, disclosure, and deployment governance more visible in enterprise buying decisions. That setting gives an advantage to suppliers that already build local compliance requirements into the product rather than leaving them to later configuration. Quebec’s healthcare system also moved forward with AI-supported workflows in 2025-2026 through the provincial AI scribe allocation for frontline primary care providers. The province’s French-language requirement adds another layer, because strong bilingual support is often necessary for broader rollout success.

Alberta represents a distinct growth pocket in the Canada frontline worker technology market because energy, construction, and field service settings need rugged, mobile-first tools. Getac’s 2025 and 2026 rugged device launches fit this profile and support deployment in physically demanding work environments. The Atlantic provinces are smaller and more dispersed, but they still matter as cloud pricing and simpler deployment models improve access for smaller employers. Northern and remote communities remain an early-stage opportunity, yet they could widen the addressable footprint of the Canada frontline worker technology market as connectivity and field-ready hardware improve.

Competitive Landscape

The Canada frontline worker technology market remains moderately fragmented, with strength divided between hardware incumbents and software specialists. Zebra Technologies, Honeywell International, and Panasonic Connect have strong standing on the device side through established rugged mobility and field deployment relationships. On the software side, WorkJam, Dayforce, and Agendrix remain prominent names in frontline workflow, scheduling, and communication. Larger HCM vendors are also pressing more deeply into frontline use cases, which keeps the Canada frontline worker technology market competitive across both new accounts and installed-base defense. This split structure means buyers often compare software depth, deployment flexibility, and device compatibility at the same time rather than treating them as separate decisions.

Recent company moves show how vendors are widening their reach inside the Canada frontline worker technology market. Dayforce partnered with WorkWhile in June 2026 to connect flexible hourly staffing with compliance, scheduling, and payroll infrastructure, which extends its reach into contingent workforce management. Honeywell launched Performance+ for Guided Work in January 2026, which added another software-oriented layer to its frontline execution offering.[4]Honeywell International Inc., “Honeywell Launches New Performance+ for Guided Work to Enable Faster, Smarter Supply Chain Operations,” Honeywell, honeywell.com Panasonic Connect introduced the TOUGHBOOK 56 in 2026 for field workers in construction, public safety, utilities, and enterprise settings. These moves show that competition is no longer limited to hardware replacement cycles and now depends more on workflow relevance and software expansion.

AI is becoming a sharper point of differentiation in the Canada frontline worker technology market because vendors are placing intelligence inside frontline execution rather than outside it. WorkJam’s January 2026 release is a good example because AI agents were built directly into audit and task flows rather than presented as a separate reporting layer. Zebra’s retail and manufacturing announcements in 2026 followed a similar direction by linking frontline decision support with the device and workflow layer. This leaves room for smaller specialists that solve shared-device identity, field coordination, or sector-specific compliance needs better than broader platforms. At the same time, the Canada frontline worker technology market still rewards vendors that can connect devices, software, and support in one credible operating model.

Canada Frontline Worker Technology Industry Leaders

Zebra Technologies Corporation

Honeywell International Inc.

Axonify Inc.

Panasonic Holdings Corporation

Legion Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: WorkWhile and Dayforce announced a strategic partnership to deliver flexible hourly workforce management for leading enterprises, combining WorkWhile's on-demand staffing marketplace with Dayforce's compliance, scheduling, and payroll infrastructure. The partnership extends Dayforce's Canadian frontline reach into contingent workforce management, where shift-flexible worker pools are increasingly central to operational planning in retail and logistics.

- June 2026: Zebra Technologies unveiled a Machine Vision Ecosystem at Automate 2026, including the TC501 and TC701 mobile computers and an AI-driven Jam Detection solution designed to prevent unnecessary conveyor shutdowns in manufacturing environments. The launch extended Zebra's AI-equipped frontline hardware portfolio into warehouse automation, a segment with significant Canadian industrial exposure across Ontario and British Columbia.

- June 2026: Getac Technology Corporation launched the ZX80W and ZX80W-EX 8-inch fully rugged Windows 11 tablets built on ARM architecture, targeting transport and logistics, defense, and industrial environments with fanless, power-efficient design. Availability is scheduled for July 2026, expanding Getac's rugged device options for Canadian field deployments where weight and battery life are primary constraints.

- April 2026: Panasonic Connect North America launched the TOUGHBOOK 56 rugged laptop for field workers in construction, public safety, utilities, and enterprise sectors. Built on an "Engineered for Motion" design philosophy, the device supports three simultaneous wired LAN connections (1 Gb, 2.5 Gb, and 10 Gb) and up to 24 hours of battery life with hot-swappable batteries.

Canada Frontline Worker Technology Market Report Scope

The Canada frontline worker technology market comprises software platforms, connected applications, and associated services designed to digitally enable deskless and field-based employees across industries such as retail, industrial manufacturing, healthcare, transportation and logistics, hospitality, construction, and the public sector. These solutions improve frontline productivity, communication, task execution, workforce coordination, learning, operational visibility, safety, and compliance by integrating mobile devices, wearable technologies, artificial intelligence (AI), Internet of Things (IoT) sensors, cloud platforms, and enterprise business systems. The market includes revenue from software subscriptions and licenses, as well as professional and managed services supporting deployment, integration, customization, training, and ongoing support.

The Canada Frontline Worker Technology Market Report is segmented by Component (Software, and Services), Deployment Mode (Cloud-Based, Hybrid, and On-Premises), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Employee Communication and Engagement, Workforce Execution and Task Management, Workforce Scheduling and Coordination, Learning and Knowledge Enablement, Workforce Analytics and Performance Management, Safety and Compliance Management, and Other Applications), and End-user Industry (Retail and E-Commerce, Industrial Manufacturing, Healthcare and Life Sciences, Transportation and Logistics, Hospitality, Construction, Government and Public Administration, and Other Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| Hybrid |

| On-Premises |

| Large Enterprises |

| Small and Medium Enterprises |

| Employee Communication and Engagement |

| Workforce Execution and Task Management |

| Workforce Scheduling and Coordination |

| Learning and Knowledge Enablement |

| Workforce Analytics and Performance Management |

| Safety and Compliance Management |

| Other Applications |

| Retail and E-Commerce |

| Industrial Manufacturing |

| Healthcare and Life Sciences |

| Transportation and Logistics |

| Hospitality |

| Construction |

| Government and Public Administration |

| Other Industries |

| By Component | Software |

| Services | |

| By Deployment | Cloud-Based |

| Hybrid | |

| On-Premises | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Application | Employee Communication and Engagement |

| Workforce Execution and Task Management | |

| Workforce Scheduling and Coordination | |

| Learning and Knowledge Enablement | |

| Workforce Analytics and Performance Management | |

| Safety and Compliance Management | |

| Other Applications | |

| By End-User Industry | Retail and E-Commerce |

| Industrial Manufacturing | |

| Healthcare and Life Sciences | |

| Transportation and Logistics | |

| Hospitality | |

| Construction | |

| Government and Public Administration | |

| Other Industries |

Key Questions Answered in the Report

What is the size outlook for the Canada frontline worker technology market?

The Canada frontline worker technology market was valued at USD 0.75 billion in 2025, stands at USD 0.88 billion in 2026, and is forecast to reach USD 2.45 billion by 2031 at a 22.70% CAGR.

Which deployment model leads adoption in Canada?

Cloud-based deployment led with an 81.28% share in 2025 and is also the fastest-growing deployment model, with a projected 23.31% CAGR through 2031.

Which end-user segment is growing the fastest?

Healthcare and life sciences is the fastest-growing end-user segment, with a projected CAGR of 25.96% through 2031, supported by staffing pressure and stronger audit needs.

Why are employers adopting frontline platforms more quickly now?

Employers are responding to labor shortages, higher labor costs, scheduling errors, and the need for better real-time visibility across frontline operations.

What is the biggest barrier to wider rollout?

Integration with older HR, ERP, and POS systems remains the most persistent barrier because it extends implementation timelines and increases deployment risk.

Which application area offers the strongest growth opportunity?

Workforce analytics and performance management is projected to grow the fastest at a 26.12% CAGR through 2031 as employers want frontline activity translated into measurable business metrics.

Page last updated on: