Canada Customer Data Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

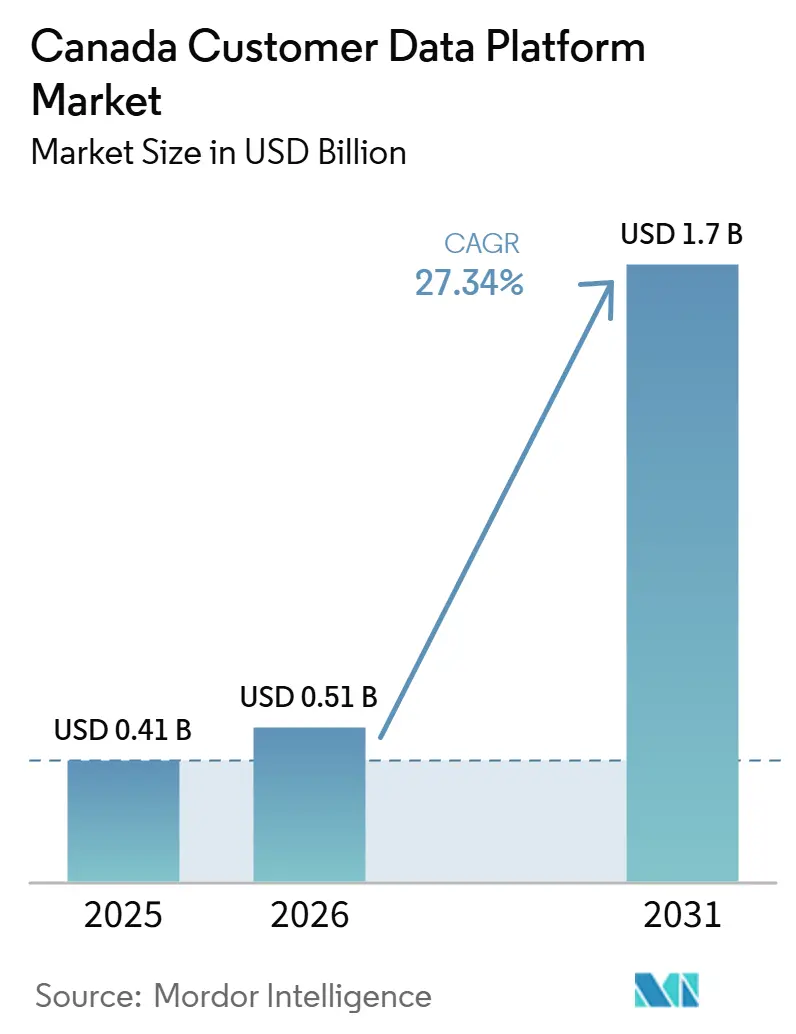

| Base Year Market Size (2025) | USD 0.41 Billion |

| Market Size (2026) | USD 0.51 Billion |

| Market Size (2031) | USD 1.7 Billion |

| Growth Rate (2026 - 2031) | 27.34% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Customer Data Platform Market Analysis by Mordor Intelligence

The Canada customer data platform market size was valued at USD 0.41 billion in 2025 and is projected to reach USD 1.70 billion by 2031, at a CAGR of 27.34% during 2026-2031. Growth is being shaped by a broader move away from third-party data and toward first-party data strategies across Canadian enterprises. AI-led personalization is also changing what buyers expect, because the platform is now judged by how quickly it can turn customer data into action across digital and assisted touchpoints. Privacy and consent governance have become central buying criteria, especially for companies that operate across multiple provinces and need a governed data layer for customer records. Competition is splitting between large suite vendors that sell broad ecosystems and composable vendors that let enterprises work on top of existing cloud data environments. This leaves the Canada customer data platform market with strong room for expansion, but it also keeps implementation quality, identity resolution, and data readiness at the center of vendor selection.

Key Report Takeaways

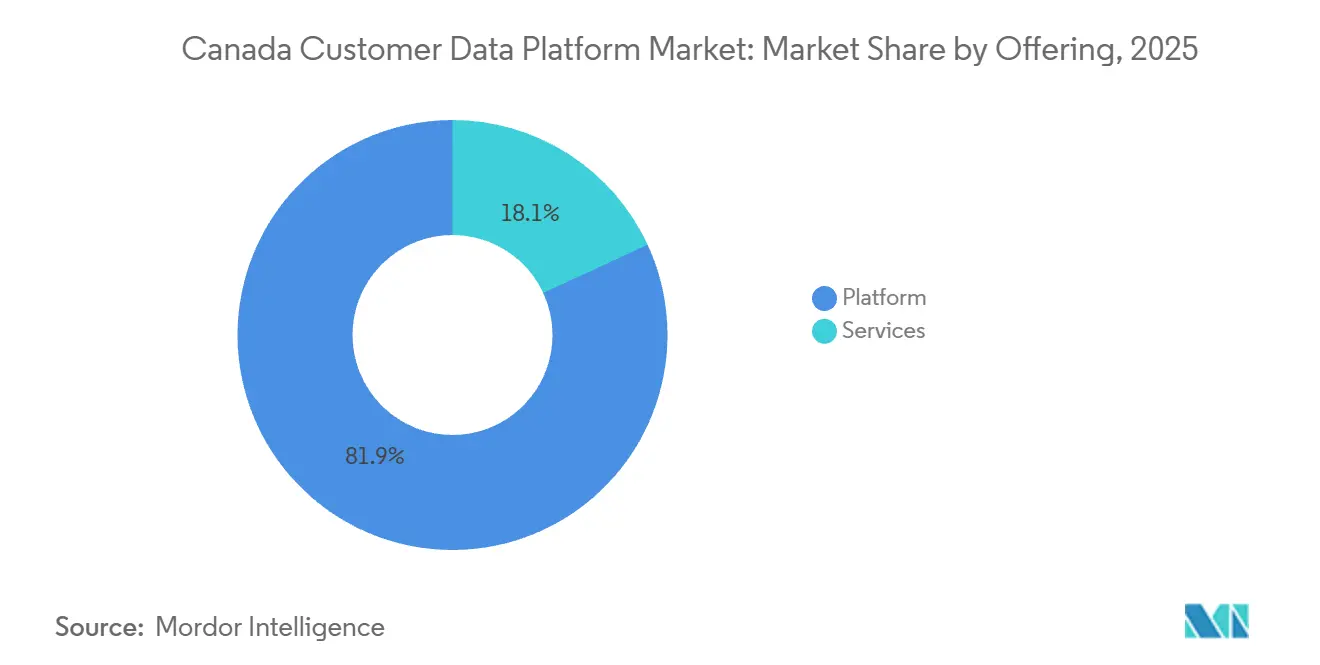

- By offering, Platform held 81.90% revenue share in 2025, while Services is projected to expand at a 30.62% CAGR through 2031.

- By deployment mode, Cloud held 69.41% revenue share in 2025, while Hybrid is projected to grow at a 31.54% CAGR through 2031.

- By organization size, Large Enterprises held 69.84% of the Canada customer data platform market share in 2025, while SMEs recorded the highest projected CAGR at 30.16% through 2031.

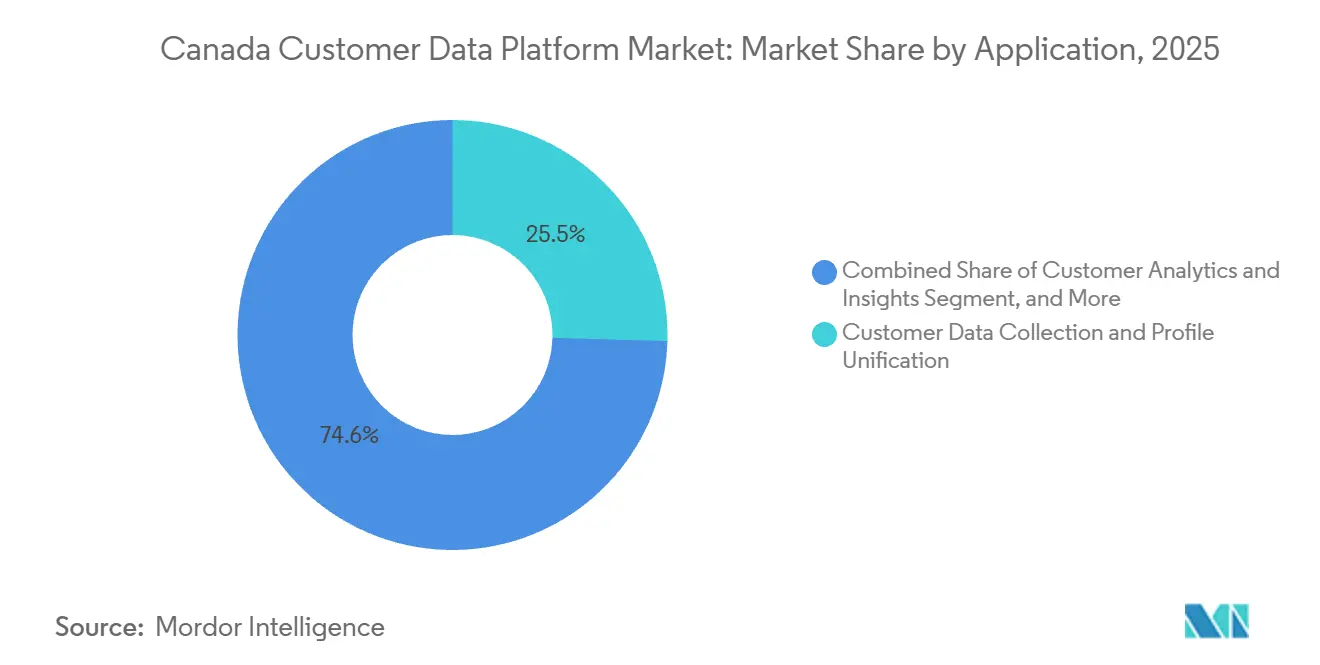

- By application, Customer Data Collection and Profile Unification accounted for 25.45% share of the Canada customer data platform market size in 2025, while Customer Analytics and Insights is projected to advance at a 32.68% CAGR through 2031.

- By end-user industry, BFSI held 22.30% share of the Canada customer data platform market size in 2025, while Healthcare and Life Sciences is projected to grow at a 32.36% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Canada Customer Data Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-Enabled Personalization and Next-Best-Action Use Cases | +5.2% | Global, concentrated early gains in Ontario and British Columbia technology corridors | Short term (≤ 2 years) |

| Need for Unified Customer Profiles | +4.8% | National, highest intensity in Ontario and Quebec large-enterprise clusters | Medium term (2-4 years) |

| Rising Demand for Real-Time Customer Activation | +4.3% | Global, accelerated uptake in Canadian retail, BFSI, and telecom verticals | Short term (≤ 2 years) |

| Privacy-First Identity Resolution Requirements | +3.8% | National, early compliance pressure in Quebec and federally regulated sectors | Medium term (2-4 years) |

| Expansion of First-Party Data Strategies | +3.2% | Global, extending across all Canadian provinces as third-party data deprecation advances | Medium term (2-4 years) |

| Warehouse-Native CDP Adoption in Complex Enterprise Stacks | +2.6% | National, early gains in Ontario financial services and Alberta energy enterprises | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI-Enabled Personalization and Next-Best-Action Use Cases

AI-led personalization is moving from an optional use case to a core operating requirement in the Canada customer data platform market. Canadian Tire scaled its MOSaiC platform across Canadian Tire, Mark's, and SportChek in February 2026 after a successful 2025 pilot, combining Triangle Rewards data with real-time behavioral signals and more than 1,000 customer life occasions for merchandising and promotion decisions. That shift changes the value test for CDPs, because enterprises now want activation speed and automated decisioning instead of simple profile storage. Adobe strengthened this direction in April 2026 when it introduced CX Enterprise Coworker across Real-Time CDP, Customer Journey Analytics, and Journey Optimizer to support agentic orchestration in live customer workflows.[1]Adobe Inc., “Adobe Announces General Availability of Real-Time CDP Collaboration for Brands to Jointly Drive Ad Performance in a Privacy-First Landscape,” Adobe News, news.adobe.com As a result, Canadian buyers are placing more weight on reasoning depth, next-best-action support, and orchestration quality during platform evaluations. This also favors vendors that can link customer data, analytics, and activation inside one environment instead of treating them as separate layers.

Need For Unified Customer Profiles

The need for a unified customer view continues to support steady CDP spending across large Canadian enterprises. Fragmentation across CRM, e-commerce, contact center, loyalty, and branch systems still prevents many organizations from building a dependable profile at scale. CIBC launched CIBC CRTeX in October 2025 to support near-real-time engagement across online, mobile, contact centers, and banking centers, showing how major financial institutions are rebuilding data layers before expanding activation use cases. This pattern keeps CDP demand tied to foundational data work, not only to campaign execution. It also means delayed investment can carry a wider cost, because analytics and AI outputs weaken when customer events remain duplicated or disconnected. For vendors, the Canada customer data platform market increasingly rewards those that can support identity resolution and sequencing across the full customer stack.

Rising Demand for Real-Time Customer Activation

Real-time customer activation is pushing enterprises away from batch models and toward streaming architectures. Tealium launched its AI Partner Ecosystem in April 2026 with more than 1,300 integrations, linking real-time context capture with model invocation and downstream activation in governed workflows. Bloomreach deepened the same direction in June 2026 through its CustomerLake integration with Databricks, which runs identity resolution, segmentation, and activation where the data already sits. These models reduce latency and trim the duplication that older CDP designs often created. Retail and e-commerce operators are setting the early pace because flash promotions and fast offer changes depend on immediate customer response. The same expectation is spreading into banking, healthcare, and telecom, where response speed is becoming part of service quality rather than only a marketing metric.

Privacy-First Identity Resolution Requirements

Privacy-first identity resolution is now a practical requirement for national deployments in the Canada customer data platform market. The Office of the Privacy Commissioner of Canada highlighted the growing importance of consent, accountability, and data rights in its 2024-2025 annual reporting, reinforcing the need for governed handling of customer records across the country. Quebec's Loi 25 has already made audit trails, explicit consent, and strong control over personal data more central to enterprise design choices. Adobe's Real-Time CDP Collaboration reached general availability in February 2025 with privacy-safe first-party data collaboration features, showing how consent-aware design has moved into mainstream product positioning. National enterprises face added complexity because they must align federal obligations with provincial rules within one operating model. Vendors that can propagate consent and control data use at the platform layer are, therefore, better placed to win complex deployments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Integration Complexity Across Legacy MarTech and CRM Stacks | -3.4% | National, highest friction in Ontario large-enterprise financial services and retail sectors | Long term (≥ 4 years) |

| Data Quality and Identity Fragmentation Issues | -2.8% | Global, concentrated risk in multi-brand retail and BFSI organizations operating nationally | Medium term (2-4 years) |

| Enterprise Concerns Over Compliance and Consent Governance Costs | -2.1% | National, acute pressure in Quebec and federally regulated BFSI and healthcare sectors | Medium term (2-4 years) |

| Skills Shortage in CDP Architecture and Activation Workflows | -1.6% | National, talent competition most acute in Greater Toronto Area and Vancouver technology markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Integration Complexity Across Legacy Martech and CRM Stacks

High integration complexity still slows adoption across legacy enterprise environments. Many Canadian financial services and telecom organizations run stacks assembled over many years, with data held in systems that were never built for event streaming or live orchestration. In practice, CDP programs often begin with fewer source systems than originally planned, which narrows the value visible to business teams during the early phases. That smaller initial scope can slow wider rollout, because buyers want proof of return before connecting more channels and datasets. The issue is not only technical, because integration also affects operating models, governance, ownership, and service delivery roles across marketing, data, and IT teams. In the Canada customer data platform market, vendors that reduce setup friction and offer stronger implementation support are therefore better positioned to expand account value over time.

Data Quality and Identity Fragmentation Issues

Data quality and identity fragmentation continue to limit platform performance even after deployment begins. Duplicate records, incomplete event histories, and mismatched identifiers weaken the unified profile that buyers expect from a CDP. The CDP Institute reported that composable and warehouse-native CDP vendors grew employment faster than traditional packaged vendors in the second half of 2025, which reflects a wider market response to these persistent data architecture challenges.[2]CDP Institute, “CDP Institute Industry Update, June-December 2025,” CDP Institute, cdpinstitute.org Many Canadian enterprises now start with remediation work before full activation, which adds time and cost to the project. This shifts the discussion from software selection alone to data readiness, governance, and internal process discipline. Buyers who underestimate upstream cleanup can therefore reach production more slowly and see weaker personalization outcomes than planned.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Platform Dominates, Services Momentum is Accelerating

The Platform segment held 81.90% share of the Canada customer data platform market in 2025, which shows that licensed software remained the core buying unit for enterprise customers. Buyers still anchor spending in the layer that manages identity graphs, segmentation logic, and activation connectors. This gives platform vendors a central role in enterprise architecture, because the software becomes the system that ties data capture to action across channels. The Canada customer data platform industry also benefits from this pattern because platform purchases often pull services, cloud, and partner spending behind them. In national accounts, software decisions are closely tied to compliance needs, integration depth, and fit with existing enterprise systems.

The Services segment is projected to expand at a 30.62% CAGR during 2026-2031, which makes it the fastest-growing part of the offering mix. That pace reflects the amount of implementation, integration, and advisory work needed before enterprises can use AI-led activation in live environments. Salesforce strengthened this service-heavy model in June 2026 when it expanded its Databricks partnership around Data 360 and zero-copy data workflows, further blending platform economics with data integration and AI enablement work. Ongoing reviews around consent architecture, data flows, and operating governance also keep service demand elevated after the initial rollout.

By Deployment Mode: Cloud Leads, Hybrid Architectures are Scaling Fast

Cloud held 69.41% share of the Canada customer data platform market in 2025, supported by the lower friction of SaaS delivery and the native links that major hyperscalers offer to leading CDP products. This mode remains attractive for enterprises that want faster rollout cycles and more predictable subscription spending. It also fits organizations that need easier scaling for customer analytics, segmentation, and orchestration across many digital touchpoints. On-premises demand still exists in regulated use cases where data residency and internal control carry more weight than deployment speed. That keeps deployment choice tied to industry needs rather than to a single architecture preference.

Hybrid deployment is projected to grow at a 31.54% CAGR during 2026-2031, which makes it the fastest-scaling model in the Canada customer data platform market. Enterprises are using this approach to keep sensitive customer records in controlled environments while running activation and analytics workloads across cloud services. The CDP Institute's January 2026 update showed continued momentum for composable and warehouse-native vendors, which supports the view that hybrid design is moving into the mainstream enterprise standard. As a result, vendors that can support zero-copy models, flexible data placement, and governed interoperability are gaining relevance in complex accounts.

By Organization Size: Large Enterprises Anchor Revenue, While SMEs Gain Ground

Large enterprises held 69.84% of the Canada customer data platform market share in 2025, reflecting their scale, data volume, and ability to fund long implementation cycles. These buyers usually manage several customer systems, brands, or channels at once, which makes unified identity and activation more valuable. Their deployments also involve custom orchestration logic and tighter control over security, governance, and integration sequencing. This keeps the largest contracts concentrated among vendors that can support enterprise-grade delivery across software and services. In the Canada customer data platform market, large accounts also shape vendor road maps because their requirements extend beyond campaign execution into enterprise data design.

SMEs are projected to grow at a 30.16% CAGR during 2026-2031 as SaaS-native products and simpler user interfaces lower the barrier to adoption. This growth is supported by demand for packaged solutions that can deliver useful activation without a large in-house data engineering team. Quebec-focused providers such as Comulead and CentrixOne show that smaller organizations also want local hosting, bilingual interfaces, and compliance-friendly operating models that global platforms do not always provide well. That opening gives domestic providers a credible route into the SME segment, even while global vendors continue to lead the largest enterprise accounts.

By Application: Profile Unification Anchors Demand, While Analytics Leads Growth

Customer Data Collection and Profile Unification accounted for 25.45% share of the Canada customer data platform market size in 2025, which kept it as the foundational application area. Enterprises continue to start here because unreliable identity resolution weakens every downstream workflow. The persistence of fragmented records across channels means many buyers still need stronger ingestion, matching, and deduplication before they can scale advanced use cases. This segment stays central because it supports not only marketing workflows but also broader service and compliance needs. In the Canada customer data platform industry, profile unification remains the step that determines whether later analytics and journey tools can perform consistently.

Customer Analytics and Insights is projected to grow at a 32.68% CAGR during 2026-2031, making it the fastest-growing application in the mix. Demand is rising because enterprises want propensity modeling, churn prediction, and lifetime value scoring to feed directly into automated decisioning. Bloomreach tied this trend to execution in June 2026 when it extended AI personalization across email, web, and other channels through its CustomerLake integration with Databricks.[3]Bloomreach Inc., “Bloomreach Deepens Partnership With Databricks, Extending AI Personalization Across Email, Web, and More Through New CustomerLake Integration,” Bloomreach, bloomreach.com Consent and Preference Management is also becoming more important, because privacy obligations are turning governed data use into a direct procurement issue across regulated sectors.

By End-User Industry: BFSI Anchors Volume, While Healthcare and Life Sciences are Rising Fastest

BFSI held 22.30% share of the Canada customer data platform market size in 2025, which made it the largest end-user segment. Banks and other financial institutions can justify CDP spending through both personalization and compliance-related use cases. The same governed customer layer that improves engagement also supports Know Your Customer-related workflows and more consistent control over customer information. CIBC's October 2025 launch of CRTeX showed how major institutions are building near-real-time engagement engines across digital and assisted channels on top of rebuilt client data foundations. This combination keeps BFSI spending resilient even when deployments require heavier governance and integration work.

Healthcare and Life Sciences is projected to expand at a 32.36% CAGR during 2026-2031, making it the fastest-growing vertical in the Canada customer data platform market. Growth is tied to the need to unify clinical, patient engagement, and operational records under stronger interoperability requirements. Retail and E-Commerce and IT and Telecom remain meaningful contributors because they rely on CDPs for loyalty, retention, and omni-channel activation across large customer bases. Government, Media and Entertainment, and Industrial Manufacturing remain earlier-stage adopters, but their use cases are broadening as service personalization and privacy-by-design expectations mature.

Geography Analysis

Ontario and British Columbia account for the largest concentration of Canada customer data platform market activity, with Ontario leading enterprise deployment volume and British Columbia serving as a strong secondary base for cloud-native adoption. Ontario's position comes from the Greater Toronto Area's dense mix of banks, telecom carriers, and retail headquarters that have the scale to fund large customer data programs. RBC's ATOM foundation model illustrated this scale in 2025 by supporting fraud detection and digital personalization on financial data infrastructure that can process up to 10 billion transactions per minute. British Columbia benefits from a technology base that is more comfortable with cloud-first deployment and faster iteration cycles. Across both provinces, privacy expectations still require enterprises to pair activation goals with governed data handling and strong internal controls.

Quebec forms a distinct operating environment within the Canada customer data platform market because Loi 25 has made consent, audit trails, and local data handling more prominent in vendor evaluation. Rosecape positioned its Montreal-based platform around Canadian hosting and Loi 25 compliance, showing how local providers are using sovereignty and language fit as competitive tools.[4]Rosecape, “La Plateforme Rosecape, Intelligence De Données Souveraine Pour Les PME Canadiennes,” Rosecape, rosecape.ca The result is a split pattern where large enterprises often buy global platforms and then add local governance layers, while smaller organizations more actively compare domestic and bilingual alternatives. Comulead and CentrixOne also reflect this demand for Quebec-focused data and customer management tools that align with French-language operating needs. Alberta and the Prairie provinces remain a smaller pool of demand, but adoption is growing in energy, retail, and agriculture programs that use customer analytics for targeting and demand sensing.

Atlantic Canada and the northern territories remain early-stage adoption zones, with demand tied more closely to public sector digital service work and healthcare digitization. Talent availability affects all regions, but it is a larger constraint outside Toronto and Vancouver where smaller specialist pools extend implementation timelines and raise external service costs. Quebec faces an added challenge because bilingual CDP architects and activation specialists are harder to source for programs that must align language needs with privacy requirements. These regional differences do not change the national growth story, but they do shape how quickly enterprises can move from procurement to full activation.

Competitive Landscape

The Canada customer data platform market shows moderate concentration at the top end, where Adobe, Salesforce, Oracle, Microsoft, and SAP hold the strongest positions in large enterprise accounts. Their advantage comes from installed application ecosystems, embedded AI features, and the ability to support broad delivery programs across software and services. Adobe strengthened this position in April 2026 when it launched CX Enterprise Coworker across Real-Time CDP, Customer Journey Analytics, and Journey Optimizer. Salesforce reinforced its own enterprise data strategy in June 2026 through an expanded Databricks partnership that connected Data 360 with federated and zero-copy workflows.[5]Salesforce Inc., “Salesforce and Databricks Build the Shared Foundation for Human and AI Agent Work,” Salesforce, salesforce.com These moves show that the main battle is shifting from stand-alone CDP functions to broader control over customer data, AI orchestration, and switching costs.

A second tier of vendors, including Tealium, Bloomreach, Lytics, Acquia, and ActionIQ under Uniphore, is competing through composable design and stronger fit with existing warehouse environments. This group appeals to enterprises that want identity resolution and segmentation to run where data already resides instead of moving it into a separate proprietary layer. Bloomreach's June 2026 CustomerLake announcement highlighted this model by pushing identity resolution and activation directly onto the Databricks lakehouse. Uniphore's December 2024 acquisition of ActionIQ and Infoworks also pointed to continued consolidation around zero-data and zero-copy architectures. This competitive split gives the Canada customer data platform market room for both full-suite leaders and specialized challengers.

White space remains visible in the Quebec SME segment, where bilingual support, domestic hosting, and local compliance design still matter more than global brand reach. Healthcare is another opening because patient data unification and clinical governance needs do not map neatly onto marketing-led CDP designs. Niche vendors such as Flybits can still compete when they bring strong vertical fit and consent-aware architecture for regulated environments. Even so, the direction of competition still favors vendors that can combine customer data management, AI activation, and flexible architecture within one buying decision.

Canada Customer Data Platform Industry Leaders

Adobe Inc.

Salesforce, Inc.

Twilio Inc.

Tealium Inc.

Treasure Data, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Bloomreach announced on June 16, 2026, its role as a launch partner for Databricks CustomerLake, a new agentic CDP that runs identity resolution, segmentation, and activation directly on the Databricks lakehouse, eliminating data duplication. Bloomreach's Loomi AI agent, trained on over 12 years of e-commerce interaction data, extends CustomerLake for real-time personalized execution across email, web, and SMS channels.

- June 2026: Adobe announced on June 22, 2026, accelerated agentic AI adoption through expanded partnerships with leading global agencies, including dentsu, Havas, Omnicom, Publicis, Stagwell, and WPP, standardizing on CX Enterprise and co-developing outcome-driven customer experience solutions that leverage Adobe Real-Time CDP for AI-powered audience activation.

- April 2026: Salesforce and Google Cloud announced an expanded partnership on April 22, 2026, at Cloud Next '26, enabling AI agents to execute end-to-end workflows across both platforms through zero-copy integration between Salesforce Data 360 and Google BigQuery, reducing data movement latency in CDP activation pipelines.

- April 2026: Adobe unveiled CX Enterprise Coworker on April 21, 2026, an agentic AI solution built on MCP and A2A open standards, integrating with Real-Time CDP, Customer Journey Analytics, and Journey Optimizer to enable autonomous, real-time customer experience management within existing enterprise engagement workflows.

Canada Customer Data Platform Market Report Scope

The Canada Customer Data Platform (CDP) market comprises software platforms and associated services that collect, unify, manage, and activate customer data from multiple online and offline sources to create persistent, unified customer profiles. These platforms enable organizations to deliver personalized, privacy-compliant, and omnichannel customer experiences through capabilities such as identity resolution, audience segmentation, real-time data activation, customer journey orchestration, analytics, and consent management.

The Canada Customer Data Platform Market Report is Segmented by Offering (Platform, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and SMEs), Application (Customer Data Collection and Profile Unification, Audience Segmentation and Personalization, Marketing Campaign and Customer Journey Orchestration, Customer Analytics and Insights, Consent and Preference Management, and Other Applications), End-User Industry (Retail and E-Commerce, BFSI, Healthcare and Life Sciences, IT and Telecom, Media and Entertainment, Industrial Manufacturing, Government and Public Administration, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Platform |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| SMEs |

| Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization |

| Marketing Campaign and Customer Journey Orchestration |

| Customer Analytics and Insights |

| Consent and Preference Management |

| Other Applications |

| Retail and E-Commerce |

| BFSI |

| Healthcare and Life Sciences |

| IT and Telecom |

| Media and Entertainment |

| Industrial Manufacturing |

| Government and Public Administration |

| Other End-User Industries |

| By Offering | Platform |

| Services | |

| By Deployment Mode | Cloud |

| On-Premises | |

| Hybrid | |

| By Organization Size | Large Enterprises |

| SMEs | |

| By Application | Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization | |

| Marketing Campaign and Customer Journey Orchestration | |

| Customer Analytics and Insights | |

| Consent and Preference Management | |

| Other Applications | |

| By End-User Industry | Retail and E-Commerce |

| BFSI | |

| Healthcare and Life Sciences | |

| IT and Telecom | |

| Media and Entertainment | |

| Industrial Manufacturing | |

| Government and Public Administration | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the size and growth outlook for the Canada customer data platform market?

The Canada customer data platform market was valued at USD 0.41 billion in 2025 and is projected to reach USD 1.70 billion by 2031 at a 27.34% CAGR during 2026-2031.

Which end-user group leads spending in Canada?

BFSI led with a 22.30% share in 2025, supported by demand for both personalization and governed customer data management.

Which application is growing the fastest?

Customer Analytics and Insights is projected to grow at a 32.68% CAGR through 2031, driven by demand for propensity models, churn prediction, and automated decisioning.

Why are hybrid deployments gaining traction?

Hybrid deployments are projected to grow at a 31.54% CAGR because enterprises want to keep sensitive data in controlled environments while using cloud tools for activation and analytics.

Why are services expanding faster than software in this space?

Services are projected to grow at a 30.62% CAGR because CDP rollouts often require integration, advisory, consent design, and operating model support after the software purchase.

What makes Quebec different from other parts of Canada?

Quebec places heavier emphasis on consent, audit trails, domestic hosting, and bilingual support, which creates stronger openings for local providers alongside global vendors.

Page last updated on: