Canada CRM Marketing Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

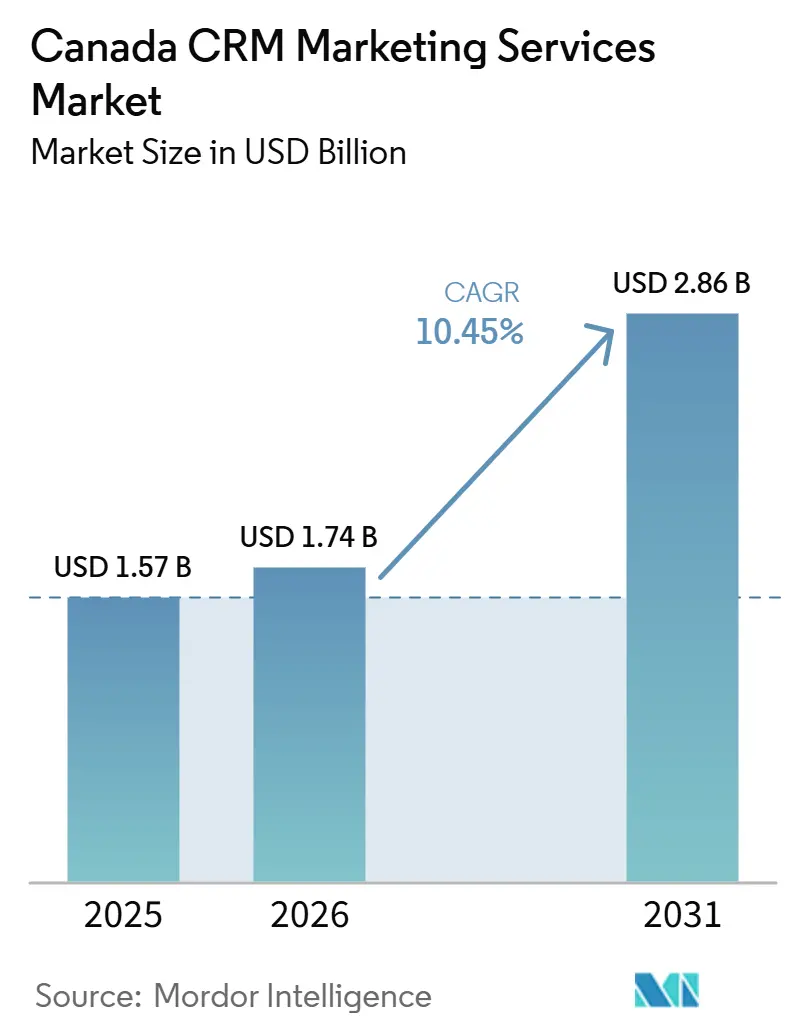

| Base Year Market Size (2025) | USD 1.57 Billion |

| Market Size (2026) | USD 1.74 Billion |

| Market Size (2031) | USD 2.86 Billion |

| Growth Rate (2026 - 2031) | 10.45% CAGR |

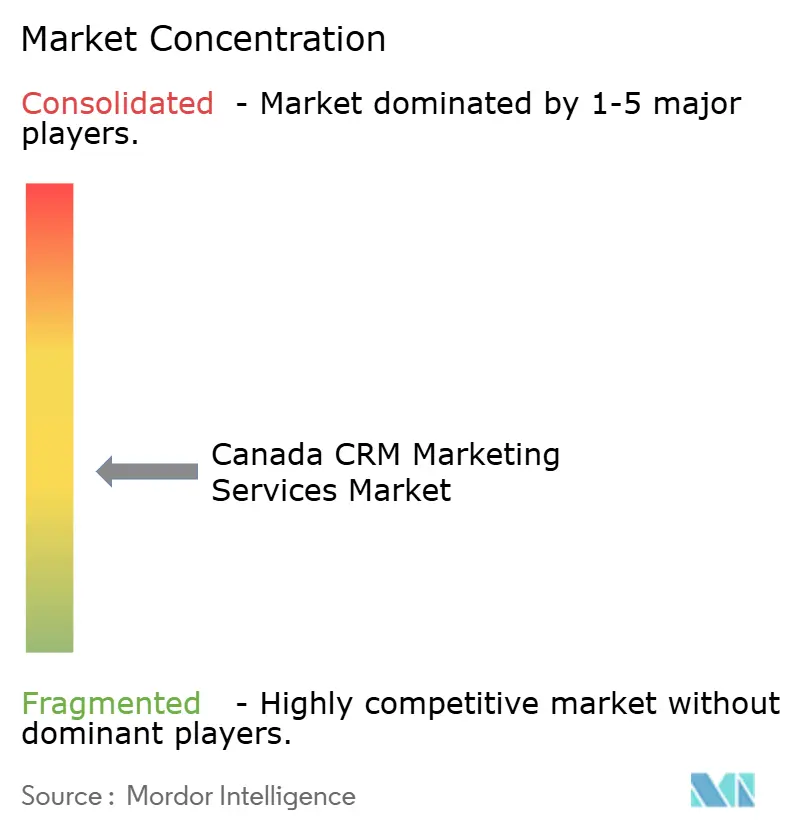

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada CRM Marketing Services Market Analysis by Mordor Intelligence

The Canada CRM marketing services market size is projected to be USD 1.57 billion in 2025, USD 1.74 billion in 2026, and reach USD 2.86 billion by 2031, growing at a CAGR of 10.45% from 2026 to 2031. The Canada CRM marketing services market is moving away from one-time platform deployment toward longer service relationships that cover strategy, data activation, analytics, and ongoing optimization. AI capabilities inside major CRM platforms are also changing service demand, because enterprises now want help with agent setup, governance, workflow design, and performance monitoring in live environments. The shift to first-party data collection is making CRM a more central system across Canadian marketing stacks, especially as browser-level privacy changes reduce the reliability of third-party targeting. Privacy modernization, especially around consent capture, audit readiness, and data portability, is turning CRM upgrades into required spending for many national brands. Execution bottlenecks still remain because fragmented legacy environments and limited specialist talent can stretch delivery timelines, but the Canada CRM marketing services market continues to benefit from durable demand tied to AI adoption, data unification, and compliance needs.

Key Report Takeaways

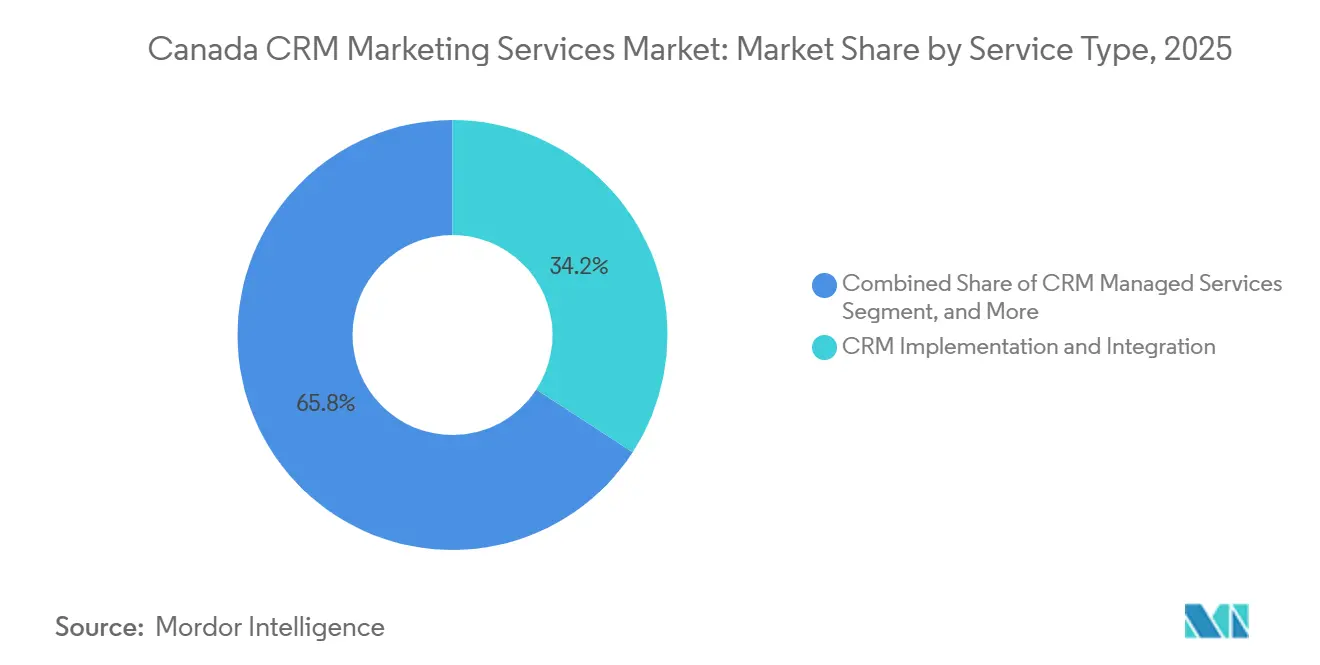

- By service type, CRM implementation held 34.18% of the Canada CRM marketing services market share in 2025, while CRM managed services are projected to expand at 15.91% CAGR through 2031.

- By enterprise size, large enterprises accounted for 67.83% of the Canada CRM marketing services market in 2025, while small and medium enterprises are projected to grow at 15.21% CAGR through 2031.

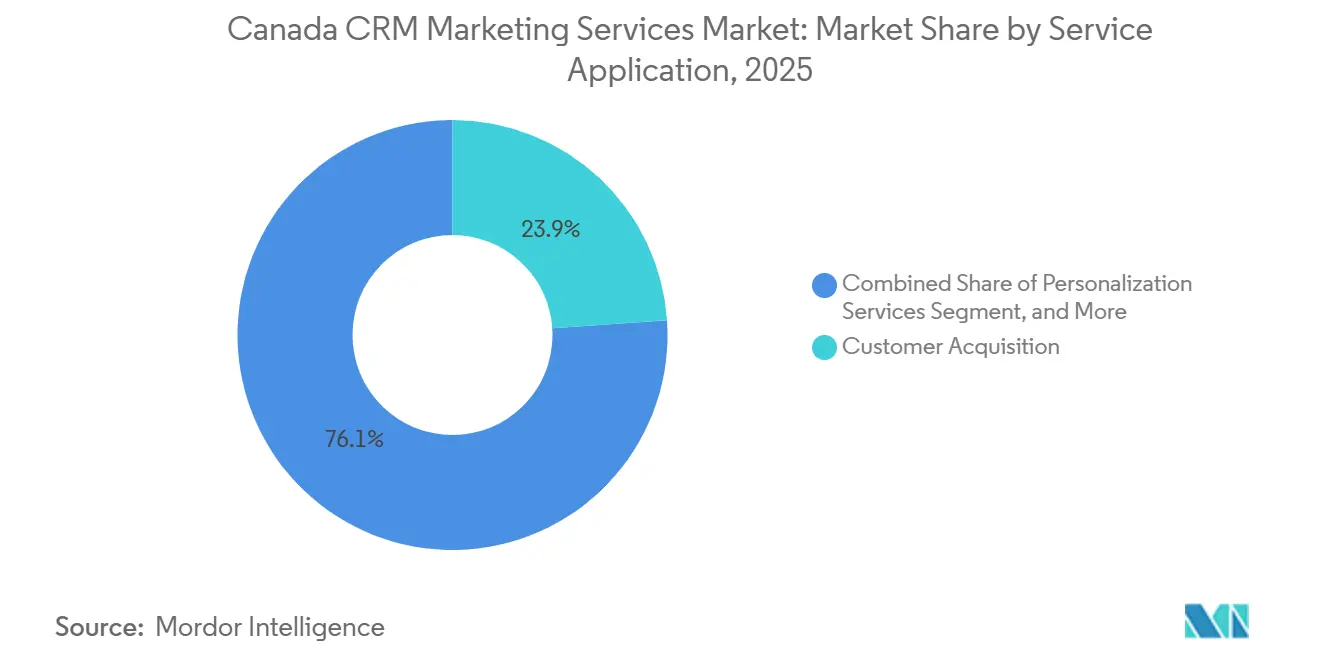

- By service application, customer acquisition accounted for 23.91% of the Canada CRM marketing services market size in 2025, while customer analytics and reporting are projected to advance at 17.33% CAGR through 2031.

- By end-user industry, banking, financial services, and insurance held 22.17% share in 2025, while retail and e-commerce are projected to grow at 16.74% CAGR through 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Canada CRM Marketing Services Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| AI-Driven Personalization in Customer Journey Orchestration | +3.2% | National, concentrated in Ontario, Quebec, and British Columbia | Medium term (2-4 years) |

| Rising Demand for Unified Customer Data Activation | +2.5% | National, strongest in Toronto, Vancouver, and Montreal enterprise hubs | Medium term (2-4 years) |

| Expansion of First-Party Data Strategies After Cookie Deprecation | +1.8% | National, stronger in Ontario and Quebec given BFSI and retail density | Short term (≤ 2 years) |

| Compliance-Led Modernization of Consent and Preference Management | +1.3% | National, intensified in Quebec and Ontario | Short term (≤ 2 years) |

| Shift Toward Revenue-Linked CRM Services and Closed-Loop Attribution | +1.0% | National, early gains in Toronto, Calgary, and Vancouver | Medium term (2-4 years) |

| Omnichannel Customer Engagement in Retail and Financial Services | +0.8% | National, concentrated across Toronto, Vancouver, and Calgary | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

AI-Driven Personalization in Customer Journey Orchestration

AI-led orchestration is changing what buyers expect from the Canada CRM marketing services market. Enterprises are no longer looking only for faster campaign execution, because they also want autonomous decision support across customer journeys. TD Bank launched TD AI Prism in June 2025, and the model processed 100 times more client data than earlier tools to predict needs and personalize marketing communications. Microsoft published internal Dynamics 365 data in June 2026 showing that sellers with high Copilot and agent usage achieved a 20% increase in deals closed, a 13% lift in lead-to-opportunity conversion, and 9.4% higher revenue per seller.[1]Microsoft Dynamics 365 Blog, “Agentic CRM in the Flow of Work: How AI Is Transforming Sales and Rebuilding Customer Trust,” Microsoft, microsoft.com As a result, the Canada CRM marketing services market is seeing more demand for AI model governance, agent monitoring, workflow tuning, and ongoing service support around production CRM environments.

Rising Demand for Unified Customer Data Activation

A unified view of the customer remains a basic requirement for stronger returns on CRM spending in the Canada CRM marketing services market. Many organizations still operate disconnected CRM, marketing automation, commerce, and analytics systems, which limits the value of personalization and measurement. That gap is pushing service buyers toward data unification programs that connect customer records, cloud data environments, and activation platforms into one working layer. Adobe expanded its agentic AI ecosystem in June 2026, while IBM was recognized in 2026 for combining Adobe Real-Time CDP with IBM watsonx Orchestrate to support AI-powered customer experiences, which shows how central unified customer data has become to service delivery. Providers that can connect CRM, data, and activation tools with repeatable delivery models are better placed to win high-value work in the Canada CRM marketing services market.

Expansion of First-Party Data Strategies After Cookie Deprecation

First-party data strategy has become an operating need rather than a future roadmap item in the Canada CRM marketing services market. Browser privacy changes have made cross-site targeting less dependable, so brands are investing more in identity resolution, consent frameworks, and server-side measurement. This change is pushing CRM closer to the center of audience management because first-party signals now need to be stored, governed, and activated through more controlled systems. Service demand is therefore expanding across CRM strategy, data engineering, integration, and managed optimization, especially for programs that route first-party signals into major advertising and engagement platforms. The Canada CRM marketing services market benefits from this shift because it supports bundled service work that spans planning, implementation, and long-term operating support.

Compliance-Led Modernization of Consent and Preference Management

Consent and preference management has become a core modernization driver in the Canada CRM marketing services market. Canada’s Anti-Spam Legislation requires documented express or implied consent before commercial electronic messages are sent, and organizations must be able to support those records during enforcement review.[2]Canadian Radio-television and Telecommunications Commission, “Guidance on Canada’s Anti-Spam Legislation,” CRTC, crtc.gc.ca Quebec’s Law 25 has been fully in force since September 22, 2024, and it requires stronger privacy-by-design controls, clearer data lineage, and data portability rights for deployments involving Quebec residents. These rules are turning consent capture, audit logging, and preference management into productized CRM service work rather than optional configuration tasks. Procurement in regulated sectors is also becoming more selective, because buyers increasingly expect data governance readiness and Canadian operating alignment as part of CRM delivery.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Fragmented Legacy MarTech and CRM Stacks | -1.8% | National, most acute in large BFSI and government organizations in Ontario and Quebec | Long term (≥ 4 years) |

| Limited Access to Skilled CRM Marketing Technologists | -1.3% | National, most severe in Toronto, Montreal, Vancouver, and Calgary | Medium term (2-4 years) |

| High Integration Complexity Across Data, Cloud, and Marketing Platforms | -1.0% | National, affects all geographies with multi-platform enterprise stacks | Medium term (2-4 years) |

| Privacy and Data Residency Constraints in Regulated Sectors | -0.7% | National, intensified by Quebec-specific Law 25 pressure and federal obligations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented Legacy MarTech and CRM Stacks

Fragmented legacy technology environments remain the strongest delivery constraint in the Canada CRM marketing services market. Large organizations often operate CRM, email, analytics, and content systems that were acquired separately and integrated only in limited ways. That structure makes transformation programs harder, because data cannot move cleanly across the customer engagement chain without custom work and repeated testing. The result is slower implementation, higher scope risk, and weaker margins on programs that would otherwise scale more efficiently. Until these environments are simplified, the Canada CRM marketing services market will continue to see slower conversion from initial transformation demand into recurring managed service revenue.

Limited Access to Skilled CRM Marketing Technologists

The Canada CRM marketing services market also faces a sustained talent constraint. CRM marketing technologists now need platform skills, data architecture knowledge, workflow design ability, and growing familiarity with AI controls inside the same delivery team. That combination is difficult to source at scale, especially in the main urban centers where demand is already concentrated. The talent gap increases buyer reliance on outside partners, but it also limits how quickly providers can staff projects and expand service capacity in the Canada CRM marketing services market. In practice, this is pushing more clients toward managed services relationships that provide continuity after go-live instead of trying to build full internal teams.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: CRM Implementation Leads Revenue, Managed Services Accelerates

CRM implementation held the largest share of the Canada CRM marketing services market at 34.18% in 2025. That lead reflected steady demand from BFSI, retail, and public sector organizations that were modernizing Salesforce, Microsoft Dynamics 365, and SAP environments. Implementation work remained central because many Canadian organizations were still building or replacing system-of-record environments rather than only refining mature deployments. Strategy services followed closely in importance, especially for buyers trying to connect CRM spending with more defined business outcomes.

CRM managed services are projected to grow at 15.91% CAGR from 2026 to 2031, making it the fastest-expanding service type in the Canada CRM marketing services market. Buyers are showing a clearer preference for subscription-like service support that covers administration, workflow updates, analytics delivery, and ongoing optimization after deployment. This shift is strongest where platform complexity is rising through AI features, multi-cloud links, and tighter compliance requirements. The Canada CRM marketing services industry is therefore moving toward longer operating relationships, because clients increasingly view steady specialist support as more practical than periodic project-only engagement.

By Enterprise Size: Large Enterprises Anchor the Market, SMEs Drive the Fastest Growth

Large enterprises held 67.83% of the Canada CRM marketing services market in 2025. Their lead came from earlier adoption of enterprise-grade platforms and the larger scale of transformation programs in financial services, insurance, and multinational retail. These environments generate more services demand because they usually involve complex integrations, broader governance requirements, and multi-team adoption programs. Compliance work also runs deeper in this customer group, especially where consent architecture, privacy assessment, and data residency design are tied to national operations.

Small and medium enterprises are projected to grow at 15.21% CAGR from 2026 to 2031 in the Canada CRM marketing services market. Cloud delivery models are lowering the infrastructure burden that once kept many smaller firms away from enterprise-grade CRM tools. Managed service options are also helping SMEs adopt advanced functionality without building large internal support teams. The Canada CRM marketing services industry is gaining depth in this segment because providers can package administration, automation, and reporting into more flexible delivery models for growth-stage companies.

By Service Application: Customer Acquisition Leads, Analytics and Reporting Sets the Pace

Customer acquisition retained the largest service application share at 23.91% in 2025, which kept it at the front of the Canada CRM marketing services market size by application. This lead reflected the continued importance of pipeline development, digital onboarding, and opportunity management for Canadian enterprises, especially in BFSI environments. Retention and campaign management also remained active service areas, but more of that work was being automated through AI-triggered communication workflows inside production CRM systems. Personalization and omnichannel management continued to gain weight because they rely on real-time behavioral data and stronger orchestration across channels.

Customer analytics and reporting are forecast to grow at 17.33% CAGR from 2026 to 2031, the fastest rate among service applications in the Canada CRM marketing services market. This shift shows that many buyers now want clearer measurement and attribution, not only more campaign output. Microsoft’s June 2026 internal CRM data, which showed 9.4% higher revenue per seller among high Copilot users, supports the growing emphasis on analytics-to-action loops inside commercial operations. Providers that can connect CRM records with ad signals, web data, and financial outcomes are capturing stronger demand because reporting expectations in the Canada CRM marketing services industry are becoming more outcome-focused.

By End-User Industry: BFSI Anchors Share, Retail and E-Commerce Sets the Pace

Banking, financial services, and insurance held the largest end-user share at 22.17% in 2025, giving the segment a leading position in the Canada CRM marketing services market. The segment benefits from Canada’s large financial sector and its mature use of CRM-linked digital transformation programs. TD Bank’s launch of TD AI Prism in June 2025 showed how financial institutions are using large-scale predictive models to personalize communications and better anticipate customer needs.[3]TD Bank Group, “TD Announces the Launch of a Revolutionary Predictive Foundation Model,” TD Bank Group, actualites.td.com BFSI demand also remains strong because governance, consent, and audit needs are deeply tied to how CRM systems are designed and operated.

Retail and e-commerce are projected to grow at 16.74% CAGR from 2026 to 2031 in the Canada CRM marketing services market. Growth in this segment is tied to omnichannel commerce, real-time personalization, and the broader move toward CRM-centered audience management after the decline of third-party tracking. The May 2026 selection of Intellect Design Arena’s eMACH.ai Digital Engagement Platform by 37 Canadian financial institutions across 5 provinces also shows that customer engagement investment is extending across service-intensive sectors that need digital relationship depth at scale. Healthcare, information technology and telecom, industrial manufacturing, and government all remained relevant demand pools, but retail and e-commerce moved faster as customer data and engagement programs became more immediate operating priorities.

Geography Analysis

Ontario remained the main center of demand in the Canada CRM marketing services market. Toronto continued to anchor large-enterprise activity because the province holds a high concentration of banking, insurance, pension, and retail headquarters. That concentration supports steady demand for CRM implementation, strategy, and managed services across complex national programs. The Toronto-Waterloo-Kitchener corridor also continued to matter for growth-stage demand, because it combines enterprise buyers with a dense ecosystem of technology specialists and service firms. This made Ontario a practical base for personalization pilots, RevOps-oriented CRM programs, and larger platform modernization work in the Canada CRM marketing services market.

Quebec formed a distinct demand environment within the Canada CRM marketing services market because Law 25 raised the compliance burden for CRM systems that handle Quebec residents’ personal information. The law requires stronger privacy-by-design architecture, more formal data lineage, and clearer consent records inside operational workflows.[4]Government of Quebec, “An Act to Modernize Legislative Provisions as Regards the Protection of Personal Information,” Publications du Québec, publicationsduquebec.gouv.qc.ca Quebec also adds bilingual delivery complexity, because consent flows, communications, and preference management must perform well in French and English. British Columbia remained important through Vancouver’s SaaS and technology base, where many scaling companies were formalizing CRM and RevOps processes for the first time.

Alberta and the Atlantic provinces represented smaller but still meaningful pockets of activity in the Canada CRM marketing services market. Alberta supported demand through energy-sector modernization, especially where B2B customer and contractor relationship programs were moving away from legacy CRM environments. The Atlantic region remained notable for active digital engagement investment among financial cooperatives and regional institutions, which created room for integrated CRM and customer experience programs. Across the Prairies, utilities and cooperative organizations added targeted demand where subscriber communication and field-service-linked engagement required more structured CRM support.

Competitive Landscape

The Canada CRM marketing services market remained moderately fragmented. Large global integrators such as Accenture, IBM, Capgemini, Deloitte, and TCS held a strong position in large enterprise and government work because they combine broad delivery capacity with major platform partnerships. At the same time, a large specialist ecosystem competed across Salesforce, Microsoft Dynamics 365, and HubSpot projects for mid-market and SME clients. This created a market structure where scale mattered in complex transformation work, while speed, pricing, and vertical familiarity mattered more in smaller and faster-turn contracts. The Canada CRM marketing services market, therefore, supported both global delivery models and focused domestic specialist strategies.

Competitive positioning is increasingly centered on AI-enabled delivery and repeatable accelerators in the Canada CRM marketing services market. Adobe expanded its agentic AI ecosystem in June 2026 by formalizing partnerships with Accenture, Capgemini, Cognizant, Deloitte Digital, IBM, Infosys, and TCS, which showed how platform and services players are aligning around packaged AI-led customer experience delivery.[5]Adobe, “Adobe Accelerates Agentic AI Adoption Through New Agency and Technology Partnerships,” Adobe, adobe.com IBM also continued to strengthen its Adobe-linked position through orchestration work built around Real-Time CDP and watsonx capabilities. These moves reflect a competitive focus on shortening time to value rather than competing only on headcount scale.

White space remained strongest in SMEs, bilingual Quebec delivery, and regulated sectors that require stronger Canadian operating alignment in the Canada CRM marketing services market. SAP and Cohere expanded their partnership in February 2026 to launch sovereign AI solutions globally, beginning in Canada, which reinforced the value of domestic control and regulated-sector readiness. Intellect Design Arena’s May 2026 deployment win across 37 Canadian financial institutions showed that focused platform-led engagement strategies can still secure meaningful scale in specialized segments. Competitive advantage in the Canada CRM marketing services market is therefore becoming more tied to delivery frameworks, compliance readiness, and practical AI integration than to brand reach alone.

Canada CRM Marketing Services Industry Leaders

Accenture plc

Adobe Inc.

Capgemini SE

CGI Inc.

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Adobe announced a major expansion of its agentic AI ecosystem at Adobe Summit, formalizing partnerships with Accenture, Capgemini, Cognizant, Deloitte Digital, IBM, Infosys, and TCS to package agentic AI solutions for key industry verticals. Adobe Marketing Agent became generally available in Microsoft Copilot, Gemini Enterprise, and IBM watsonx, broadening the surface area of CRM-linked AI deployments for Canadian enterprises.

- May 2026: Intellect Design Arena announced that 37 Canadian financial institutions, participating in the National Digital Banking Working Group, selected its eMACH.ai Digital Engagement Platform to deliver digital banking experiences to over 262,000 credit union and financial institution members across 5 provinces. The deal concluded an exclusive negotiation first announced in August 2025.

- April 2026: SAP Canada was awarded a 5-year Enterprise Resource Planning solutions contract by the Government of Canada through the Agile Procurement for Enterprise Planning Resource Solution framework, active from April 16, 2026, to April 16, 2031, reinforcing SAP’s position in the federal public sector CRM and ERP services market.

- February 2026: SAP and Cohere expanded their partnership to launch sovereign AI solutions globally, beginning with Canada, combining Cohere’s Canadian-developed foundation models with SAP’s sovereign enterprise platforms to serve regulated industries and government workloads requiring domestic AI and cloud control.

Canada CRM Marketing Services Market Report Scope

The Canada CRM marketing services market refers to the industry that provides platforms and services for managing customer relationships and improving marketing operations across Canadian businesses. It includes solutions for customer data management, campaign automation, analytics, personalization, and omnichannel engagement. These services help businesses enhance customer loyalty, support revenue growth, and comply with national and provincial data privacy regulations, such as PIPEDA. The market is influenced by Canada’s strong digital adoption, bilingual communication requirements, and increasing focus on secure, AI-driven customer engagement.

The Canada CRM Marketing Services Market Report is Segmented by Service Type (CRM Strategy and Consulting, CRM Implementation and Integration, CRM Migration and Modernization, CRM Managed Services, and CRM Training and Support), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Service Application (Customer Acquisition, Customer Retention and Loyalty, Campaign Management Services, Marketing Automation Services, Customer Analytics and Insights, Omnichannel Customer Engagement, and Personalization Services), and End-user Industry (Banking, Financial Services, and Insurance (BFSI), Healthcare and Life Sciences, Information Technology and Telecom, Retail and E-commerce, Industrial Manufacturing, Government and Public Administration, and Other End-user Industries). The Market Forecasts are Provided in Terms of Value (USD).

Source: https://www.mordorintelligence.com/industry-reports/north-america-crm-marketing-services-market

| CRM Strategy and Consulting |

| CRM Implementation and Integration |

| CRM Migration and Modernization |

| CRM Managed Services |

| CRM Training and Support |

| Large Enterprises |

| Small and Medium Enterprises |

| Customer Acquisition |

| Customer Retention and Loyalty |

| Campaign Management Services |

| Marketing Automation Services |

| Customer Analytics and Insights |

| Omnichannel Customer Engagement |

| Personalization Services |

| Banking, Financial Services, and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Information Technology and Telecom |

| Retail and E-commerce |

| Industrial Manufacturing |

| Government and Public Administration |

| Other End-user Industries |

| By Service Type | CRM Strategy and Consulting |

| CRM Implementation and Integration | |

| CRM Migration and Modernization | |

| CRM Managed Services | |

| CRM Training and Support | |

| By Enterprise Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Service Application | Customer Acquisition |

| Customer Retention and Loyalty | |

| Campaign Management Services | |

| Marketing Automation Services | |

| Customer Analytics and Insights | |

| Omnichannel Customer Engagement | |

| Personalization Services | |

| By End-user Industry | Banking, Financial Services, and Insurance (BFSI) |

| Healthcare and Life Sciences | |

| Information Technology and Telecom | |

| Retail and E-commerce | |

| Industrial Manufacturing | |

| Government and Public Administration | |

| Other End-user Industries |

Key Questions Answered in the Report

How large is the Canada CRM marketing services market?

The Canada CRM marketing services market size was USD 1.57 billion in 2025, reached USD 1.74 billion in 2026, and is forecast to reach USD 2.86 billion by 2031 at a 10.45% CAGR.

Which service type leads revenue in Canada CRM marketing services?

CRM implementation led the market with a 34.18% share in 2025, supported by platform modernization across BFSI, retail, and the public sector.

Which segment is growing the fastest by enterprise size?

Small and medium enterprises are projected to grow at 15.21% CAGR through 2031, helped by cloud delivery and outsourced managed service models.

Why is customer analytics and reporting gaining importance in Canada?

Customer analytics and reporting is forecast to grow at 17.33% CAGR because buyers increasingly want clear attribution, reporting depth, and stronger links between CRM activity and revenue outcomes.

Which end-user sector contributes the most demand?

BFSI held the largest end-user share at 22.17% in 2025, reflecting strong CRM investment across banking, insurance, and financial engagement platforms.

What is driving growth in retail and e-commerce CRM services?

Retail and e-commerce is projected to grow at 16.74% CAGR through 2031 as omnichannel commerce, real-time personalization, and first-party data programs move closer to the CRM core.

Page last updated on: