Canada Corrugated Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

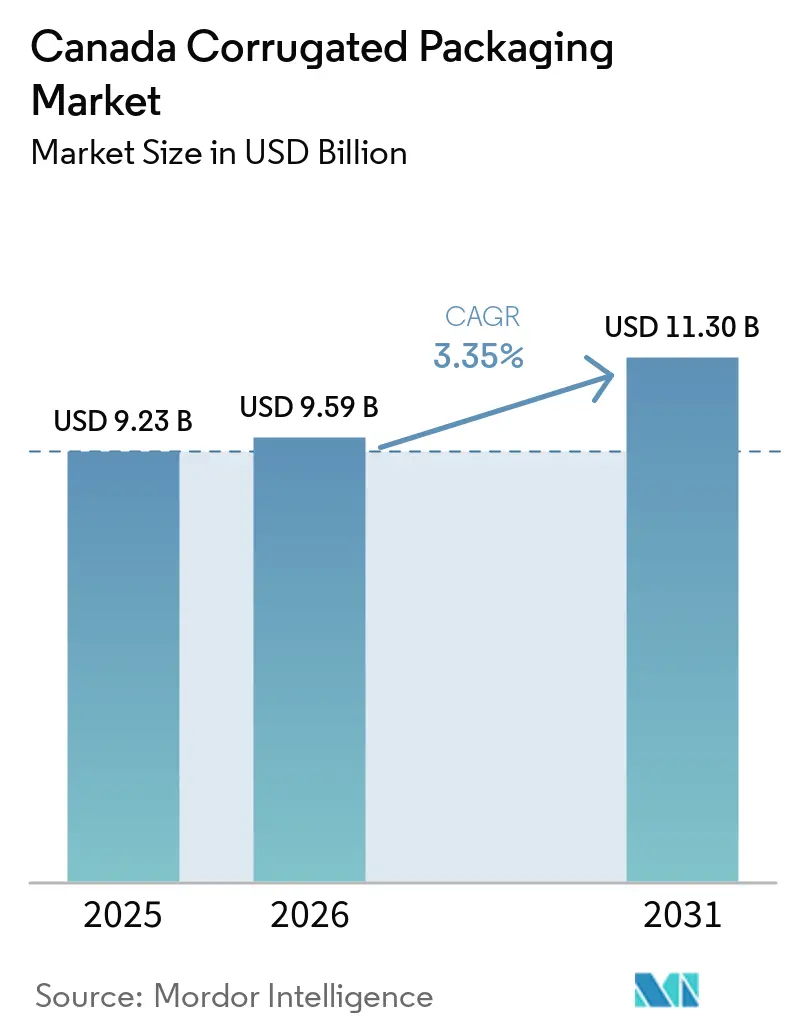

| Base Year Market Size (2025) | USD 9.23 Billion |

| Market Size (2026) | USD 9.59 Billion |

| Market Size (2031) | USD 11.30 Billion |

| Growth Rate (2026 - 2031) | 3.35% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Corrugated Packaging Market Analysis by Mordor Intelligence

The Canada corrugated boxes market size is projected to be USD 9.23 billion in 2025, USD 9.59 billion in 2026, and reach USD 11.30 billion by 2031, growing at a CAGR of 3.35% from 2026 to 2031. Demand momentum comes primarily from e-commerce parcel growth, provincial extended producer responsibility (EPR) rules that favor fiber-based formats, and sustained capacity rationalization that supports pricing discipline. Converters able to deliver recycled-content verification, short-run digital printing, and right-sizing automation are winning share as retailers fragment stock-keeping units and brand owners seek compliance solutions. At the same time, linerboard cost volatility and winter logistics challenges continue to compress margins for producers without an integrated fiber supply. Competitive intensity remains moderate because the three largest integrated players still control nearly half of domestic shipments, yet niche opportunities persist for regional converters offering agility, automation, and EPR advisory services.

Key Report Takeaways

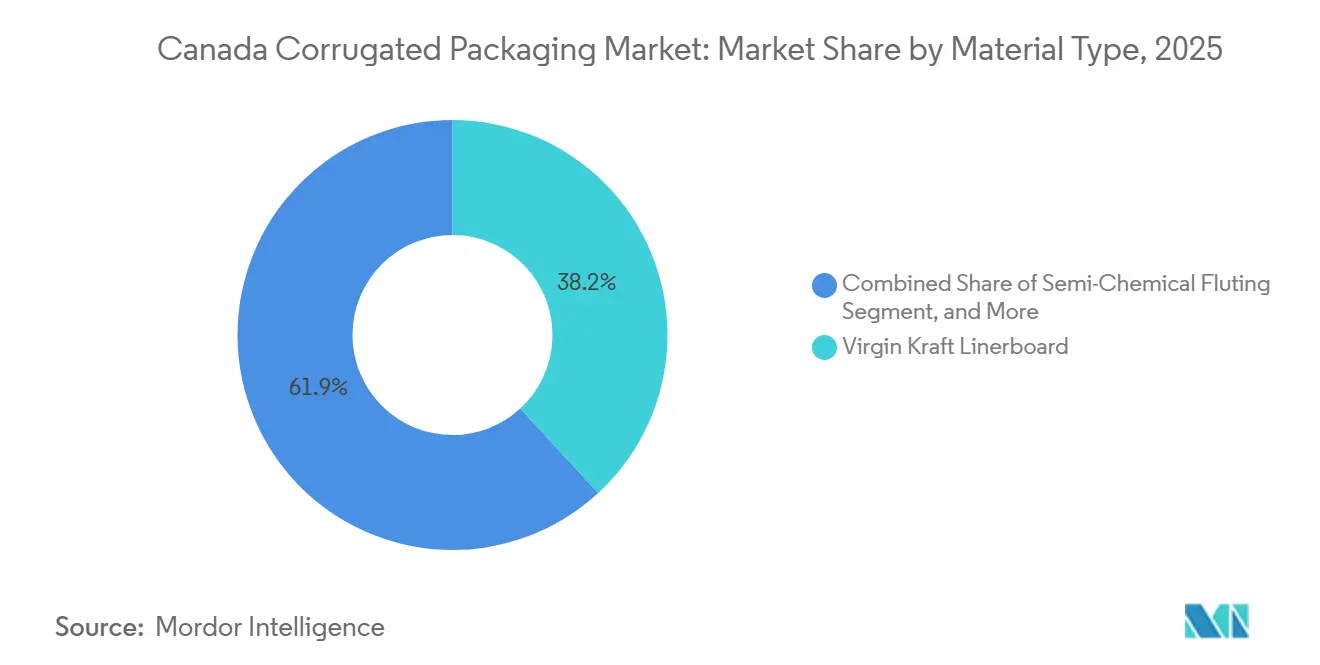

- By material type, the virgin kraft linerboard segment captured 38.15% of the Canada corrugated packaging market share in 2025.

- By flute type, the Canada corrugated packaging market size for a flute is projected to grow at an 4.23% CAGR between through 2031.

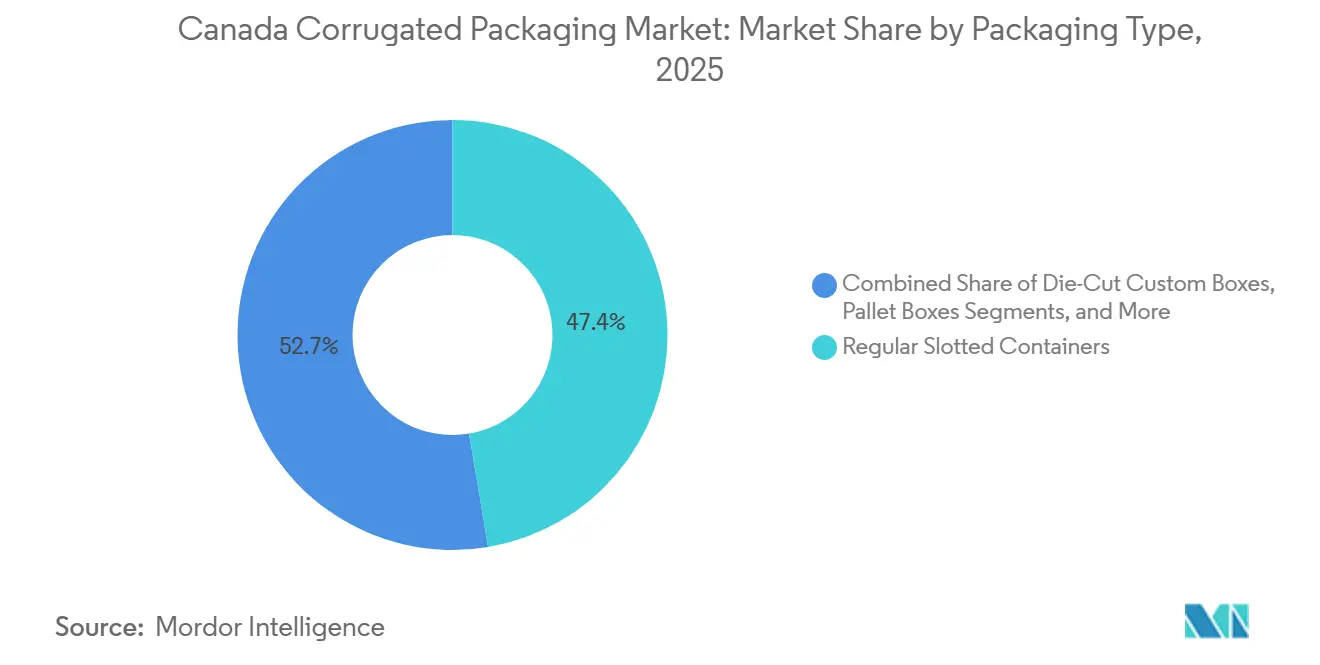

- By packaging type, the regular slotted containers segment captured 47.35% of the Canada corrugated packaging market share in 2025.

- By wall type, the Canada corrugated packaging market size for triple-wall is projected to grow at an 4.63% CAGR through 2031.

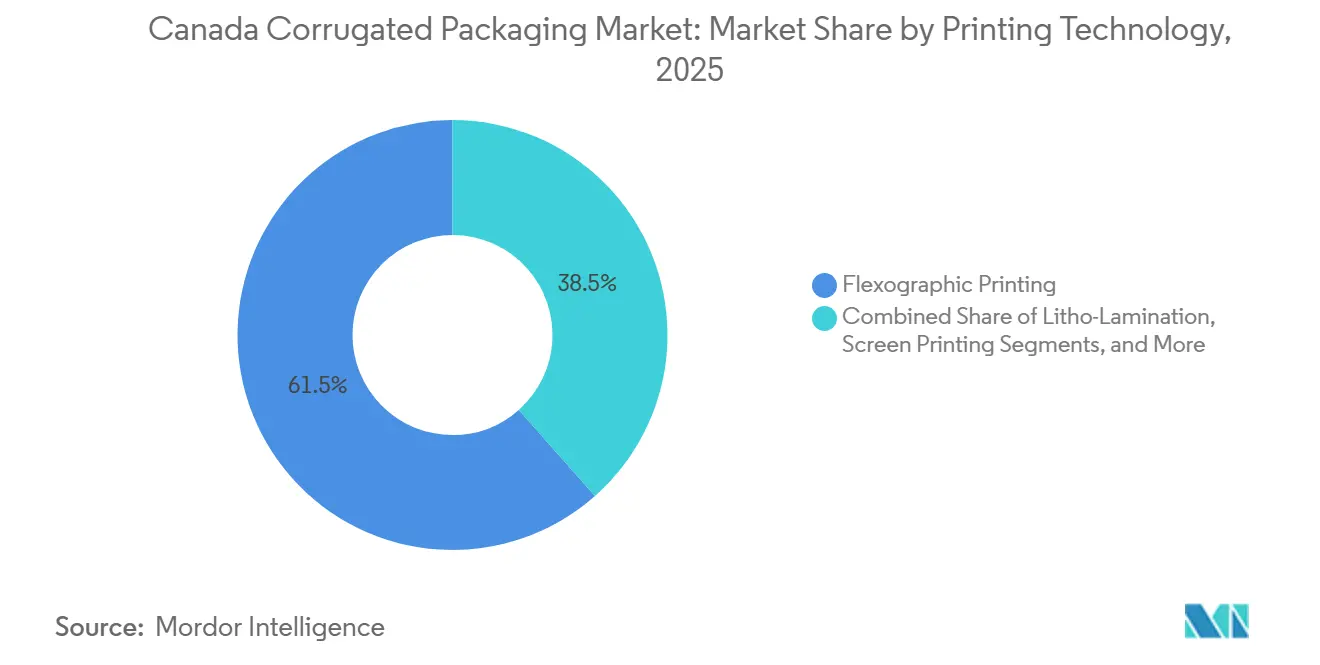

- By printing technology, the flexographic printing segment captured 61.53% of the Canada corrugated packaging market share in 2025.

- By end-user industry, the Canada corrugated packaging market size for e-commerce fulfillment centers is projected to grow at an 4.68% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Canada Corrugated Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising E-commerce and Direct-to-Consumer Logistics Acceleration | +1.2% | National, concentrated in Ontario, Quebec, and British Columbia | Short term (≤ 2 years) |

| Shift Toward Sustainable Packaging Driven by Federal and Provincial EPR Rules | +0.8% | National, with early enforcement in Quebec, Ontario, Alberta | Medium term (2-4 years) |

| Expansion of Processed Food and Beverage Manufacturing Capacity | +0.6% | National, strongest in Ontario, Quebec | Medium term (2-4 years) |

| Growing Adoption of Digital Printing for Retail-Ready and Subscription Packaging | +0.4% | National, early adopters in Ontario, British Columbia | Short term (≤ 2 years) |

| Investments in On-Demand, Right-Sizing Box Automation by Canadian Converters | +0.3% | National, concentrated in major manufacturing hubs | Medium term (2-4 years) |

| Growth in Cold-Chain Exports Requiring Moisture-Resistant Corrugated Formats | +0.2% | National, export corridors to United States, Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising E-Commerce and Direct-To-Consumer Logistics Acceleration

Online retail sales reached CAD 73.7 billion (USD 55.28 billion) in 2025, representing 6.1% of total retail trade. Fulfillment centers are demanding lighter, right-sized boxes that reduce dimensional-weight charges, which is pushing B-, E-, and micro-flute constructions into mainstream use. Parcel damage mitigation is another catalyst because thicker flutes lower return rates, an important metric for retailers facing tighter reverse-logistics budgets. The need for speed has steered converters toward automated case-erecting lines that switch between SKUs in seconds. As e-commerce penetration climbs each month, even conservative brands are revising structural box designs to reduce void fill and improve unboxing, locking in a multiyear growth runway for the Canada corrugated boxes market.

Shift Toward Sustainable Packaging Driven By Federal And Provincial EPR Rules

Quebec’s Bill 81 and similar programs across nine other provinces impose minimum recycled-content thresholds, fee modulation, and material bans that directly influence material selection. Ontario’s regulator levied CAD 2.78 million (USD 2.09 million) in fines on non-compliant producers in 2025, signaling a decisive shift from advisory to punitive enforcement. Alberta’s phased EPR rollout adds further compliance layers by 2026, compressing timeframes for converters and brand owners to meet reporting and recycled-content targets. Federal Plastics Registry reporting overlaps these rules, increasing administrative complexity but also elevating fiber-based packaging as a clear compliance path. Converters with documented post-consumer content and chain-of-custody certification now wield a competitive edge in the Canada corrugated boxes market

Expansion of Processed Food and Beverage Manufacturing Capacity

Food and beverage processing generated CAD 116 billion (USD 87 billion) in sales during 2024, with meat, dairy, and bakery alone totaling CAD 55.8 billion (USD 41.9 billion). Export-oriented processors ship CAD 33.8 billion (USD 25.35 billion) of consumer foods, most of which are shipped to the United States, thereby driving demand for double- and triple-wall export-grade cases that resist humidity and compression. Government funds of CAD 200 million (USD 150 million) support regional plants that prefer a flexible short-run box supply. Because Ontario and Quebec account for more than 85% of the national food output, converters near the Toronto-Montreal corridor enjoy steady base loads and opportunities to integrate graphics that meet bilingual labeling requirements. All these factors reinforce volume growth and margin stability for the Canadian corrugated boxes market.

Growing Adoption of Digital Printing for Retail-Ready and Subscription Packaging

Planet Group’s Domino X630i installation in February 2026 highlighted a transition toward plate-free workflows that cut make-ready time and enable variable designs.[1]Domino Printing Sciences, “Planet Group expands digital corrugated printing capability,” domino-printing.com Nine HP Indigo presses across ePac’s Canadian sites extend similar capabilities to flexible packaging, raising customer expectations for corrugated. Digital inkjet allows regional language variants, limited-edition graphics, and serialized coding without interrupting high-speed lines, which is critical as retailers shrink replenishment windows. While flexography remains economical on million-square-foot volumes, digital’s share is expanding quickly because SKU proliferation continues unabated. As brand owners pilot more direct-to-consumer programs, converters with digital capacity will secure those higher-margin, quick-turn contracts inside the Canada corrugated boxes market

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility of Kraft Linerboard and Recovered Fiber Prices | -0.6% | National, with exposure to North American pricing dynamics | Short term (≤ 2 years) |

| Competition from Flexible Plastic Mailers and Poly-Mailers | -0.3% | National, concentrated in e-commerce and subscription segments | Medium term (2-4 years) |

| Moisture Sensitivity During Winter Logistics and Port Dwell Times | -0.2% | National, acute in Atlantic provinces and Pacific export corridors | Short term (≤ 2 years) |

| Rail Bottlenecks and Labour Shortages Elevating Transit Risk and Costs | -0.4% | National, most severe in Western provinces and rural areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility of Kraft Linerboard and Recovered Fiber Prices

Producers announced a USD 70-per-tonne linerboard hike, effective March 2026, after three USD 40 increments between 2024 and 2025, reflecting tight supply as Red River and other mills closed. Old corrugated container feedstock averaged USD 45 per short ton in January 2026, yet export pull from Southeast Asia keeps inventories lean, especially for mills without captive collection. Because over 1 million tonnes of Canadian containerboard cross into the United States each year, domestic converters cannot fully pass through cost spikes to buyers with U.S. sourcing options. Smaller plants tied to spot fiber markets face the heaviest squeeze, eroding their ability to invest in automation or EPR compliance. Short-term cost whiplash therefore limits pricing visibility and capital planning across the Canadian corrugated boxes market.

Rail Bottlenecks and Labour Shortages Elevating Transit Risk and Costs

Manufacturing firms reported 27.5% expected labor shortages for early 2026, with 33.3% citing skilled-worker recruitment as a top obstacle. Truck driver vacancies have eased, but wages climbed to CAD 27.10 (USD 20.33) per hour, inflating freight rates on low-value, high-cube corrugated loads.[2]Kruger Packaging, “Kruger Packaging transformation project at Place Turcot,” paper-world.com Rural converters are disproportionately affected, as 25.1% expect transportation costs to rise, compared with 17.5% among urban peers. Rail service interruptions during peak grain and energy seasons further delay containerboard deliveries, forcing plants to raise safety stocks or pay premium intermodal rates. Winter port dwell times at Vancouver and Halifax increase the moisture risk for export-grade boxes unless shippers opt for heavier, triple-wall boxes, which increase fiber usage and costs. The combined effect dampens profit margins and investment appetite in the Canadian corrugated boxes market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Virgin Kraft Still Leads as Recycled Mandates Approach

Virgin Kraft accounted for 38.15% of 2025 volume and remains the performance benchmark for export cases, yet impending recycled-content thresholds under Bill 81 are elevating demand for certified post-consumer alternatives. Recycled linerboard now represents the largest single challenger, supported by Kruger’s USD 22.5 million conversion of its Place Turcot mill to 100% recycled saturating kraft.[3]Scotia Investments Limited, “Maritime Paper Dartmouth: Capital investment celebration,” scotiainvestments.ca Corrugating medium and semi-chemical grades supply cost-sensitive applications, while specialty boards address niche moisture-barrier needs.

The Canada corrugated boxes market share for virgin grades will edge lower, even as absolute tonnes rise with overall market growth. Fiber procurement strategies are shifting toward long-term recovered-paper contracts to secure supply before OCC exports erode domestic availability. Mill announcements indicate a balancing act between price stabilization and circular-economy commitments. Converters hedging with mixed-fiber recipes can soften the impact of USD 70-per-tonne linerboard increases, but only those with robust segregation and testing protocols can guarantee compliance across multiple EPR audits.

By Flute Type: Cushioning Needs Drive A Flute Revival

C Flute’s 27.39% share underscores its utility for retail distribution, yet parcel carriers are driving a counter-trend renaissance for A Flute, now the fastest-growing design at 4.23% CAGR through 2031. B and E Flutes thrive in subscription kits and shelf-ready trays because their thinner profiles accept high-definition graphics without sacrificing stacking strength. F Flute stays niche but gains mindshare as cosmetic and tech brands seek premium unboxing experiences.

The Canada corrugated boxes market size for micro-flutes is expanding as packaging engineers optimize dimensional weight and aesthetics simultaneously. Converters installing dual-profile corrugators can switch between C and E in minutes, improving asset utilization and serving both retail and parcel channels from a single line. Damage-rate analytics from major fulfillment centers show meaningful reductions when fragile goods move from C to A Flute boxes, justifying the marginal fiber increase. Consequently, the flute landscape is fragmenting, creating differentiated value propositions instead of a single cost curve.

By Packaging Type: Regular Slotted Containers Remain The Workhorse

Regular Slotted Containers (RSC) held a 47.35% share in 2025 and delivered a 5.03% CAGR, proving that standardization and automation still trump most alternatives. Die-cut custom boxes follow with the highest relative growth because retailers want shelf-ready designs that double as displays. Folding cartons, pallet boxes, and POP displays fill specialized roles but are being replaced by RSC variants that integrate tear-away panels and easy-open features.

Within the Canada corrugated boxes market, platform investments in high-speed RSC gluers pay quick dividends as e-commerce order volumes remain volatile yet directionally upward. Conversely, die-cut adoption rides on digital print economics: eliminating tooling charges turns cost-prohibitive short runs into viable marketing spend. Converters capable of both platforms can flex capacity towards whichever mix maximizes uptime, keeping margins resilient despite input-price gyrations.

By Wall Type: Triple-Wall Gains on Export and Cold-Chain Growth

Single-Wall captured 55.38% of 2025 shipments, yet Triple-Wall advanced fastest at 4.63% CAGR as frozen foods, meat exports, and heavy industrial goods required superior moisture and crush resistance. Double-Wall sits between, often selected for appliances and electronics, where stacking strength outweighs weight penalties. Single-Face remains a protective wrap for irregular items rather than a shipping container.

Canada's corrugated boxes market share is therefore tilting incrementally toward multi-wall boards, especially in corridors feeding U.S. and Asian distribution hubs. As exporters chase zero-damage metrics, triple-wall designs become insurance against humidity and handling abuse on longer transit legs. However, fiber cost spikes could slow penetration if converters cannot offset basis-weight increases with lighter liners or higher recycled content.

By Printing Technology: Flexo Dominates, Digital Scales Quickly

Flexographic printing accounted for 61.53% of volume in 2025, with unmatched speed on long-run SKUs. Digital inkjet, though only a fraction of total output, recorded a 5.12% CAGR, as installations like Planet Group’s X630i validate the commercial economics of runs under 10,000 boxes. Litho-laminated and hybrid workflows serve premium retail graphics where tactile coatings elevate shelf appeal. Planet Group's February 2026 installation of a Domino X630i digital press at its Hughes Decorr facility in Concord, Ontario, exemplifies the industry's pivot toward plate-free workflows that enable rapid prototyping, consistent repeat color, and fast turnaround for repeat orders, capabilities that align with brand owners' demand for agility and customization

Litho-Lamination offers superior graphics for premium applications but comes with a cost premium and longer lead times, limiting its use to high-value retail-ready packaging and seasonal promotions, whereas Screen Printing serves niche applications, such as tactile varnishes and specialty coatings that differentiate products on the shelf. The convergence of digital and flexo in hybrid workflows is emerging as a strategic response, enabling converters to print variable data and versioning digitally while maintaining flexo's speed and cost advantage for base graphics and solid colors.

By End User Industry: Fresh Produce Tops Volume, Fulfillment Leads Growth

Fresh food and produce consumed 38.63% of 2025 tonnage, reflecting agriculture’s dependence on ventilated, moisture-tolerant boxes. E-commerce fulfillment centers, although smaller in absolute volume, posted the highest CAGR of 4.68% as online penetration climbed month over month. Processed foods, beverages, electronics, personal care, and pharmaceuticals round out demand but show divergent needs in print quality and regulatory labeling. The Canada corrugated boxes market size attached to produce is mature, whereas fulfillment continues to accelerate with every percentage-point gain in digital retail.

Because returns are costly, fulfillment operators favor premium cushioning solutions, helping pull higher-flute and multi-wall formats into mainstream parcel operations. Meanwhile, bilingual packaging rules push personal care and pharma brands toward digital or litho-laminated graphics that maintain clarity across provinces. Electrical Products, Personal Care and Cosmetics, and Pharmaceuticals are smaller in volume but command premium pricing for custom die-cuts, high-graphic printing and compliance with regulatory labeling, creating opportunities for converters offering specialized capabilities and rapid turnaround.

Geography Analysis

Ontario and Quebec dominate the Canada corrugated boxes market, supported by CAD 394.6 billion (USD 295.95 billion) in combined 2023 manufacturing revenue and more than 85% of national food-processing sales. The dense Toronto-Montreal corridor hosts the majority of converting capacity and benefits from proximity to both domestic retailers and U.S. export routes. British Columbia, at 13.9% of retail revenue, serves Pacific export lanes, while Alberta’s 12.7% share is anchored in agriculture, energy, and the province’s phased EPR obligations that spur recycled-content demand.

Atlantic Canada has a smaller base, yet state support enabled Maritime Paper’s USD 14.1 million equipment upgrade, demonstrating the government's willingness to secure regional supply.[4]Statistics Canada, “Input and transportation costs, labour issues among headwinds for rural businesses,” statcan.gc.ca Potential modernization of Kruger’s Corner Brook mill to the tune of CAD 700 million (USD 525 million) would further solidify capacity in Newfoundland and Labrador, ensuring fiber supply for Eastern markets. Prairie provinces, Manitoba and Saskatchewan, are drafting EPR transition plans that will pass collection costs to producers, indirectly accelerating recycled linerboard uptake.

Cross-border trade layers additional complexity. Canada exported 1.05 million tonnes of containerboard to the United States in 2024, aligning Ontario and Quebec mills with American pricing cycles. British Columbia funnels moisture-resistant triple-wall boxes to Asian destinations via Vancouver, while Alberta’s exporters concentrate on U.S. Midwest corridors. Higher transportation and input costs reported by 35.4% of rural businesses constrain profitability outside metropolitan hubs yet open white-space opportunities for micro-converters deploying on-demand box lines near agricultural clusters.

Competitive Landscape

Market concentration remains moderate, with Cascades, Kruger, and the newly merged Smurfit WestRock plc accounting for nearly half of box shipments. Smurfit’s acquisition of WestRock positioned it as North America’s second-largest linerboard producer, while International Paper’s Red River mill shutdown removed roughly 3% of U.S. capacity and tightened regional supply, indirectly supporting Canadian mill pricing. Cascades divested its Richmond plant to Crown Paper Group for USD 49.13 million, illustrating portfolio pruning and regional realignment.

Strategic focus centers on three pillars: recycled-content capacity, digital printing, and automation. Kruger’s USD 22.5 million Place Turcot revamp added machine-learning controls that cut waste, and Crown’s Richmond purchase enhances mill-to-box integration on the Pacific coast. Smaller converters differentiate by installing digital presses and right-sizing machinery, targeting subscription commerce and multilingual SKUs that large integrated producers find less economical to produce.

New entrants from adjacent fiber segments, such as Hartmann’s molded-fiber tray expansion, present substitution threats for select produce formats. Nonetheless, the Canadian corrugated boxes market largely rewards converters with integrated fiber access and national footprints capable of meeting retailer just-in-time replenishment. Digitally enabled short-run capability is emerging as the critical tie-breaker when bids involve variable designs or rapid launch windows.

Canada Corrugated Packaging Industry Leaders

Cascades Inc.

Smurfit WestRock plc

Kruger Inc.

International Paper Company

Packaging Corporation of America

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Planet Group installed a Domino X630i digital aqueous inkjet press at its Hughes Decorr facility in Concord, Ontario, expanding full-color short-run capacity.

- January 2026: Cascades sold its Richmond, British Columbia, corrugated plant to Crown Paper Group for CAD 65.5 million (USD 49.13 million) to streamline its network.

- July 2025: Kruger proposed up to CAD 700 million (USD 525 million) in upgrades at Corner Brook Pulp and Paper, including biomass cogeneration and wind power.

- April 2025: Alberta launched Phase I of its packaging and paper EPR program, with Phase II scheduled for Oct 2026.

Canada Corrugated Packaging Market Report Scope

The scope of the Canada Corrugated Packaging Market report encompasses a comprehensive analysis of the industry's value and volume, defined as the total market for paper-based shipping containers consisting of a fluted corrugated medium sandwiched between one or more flat linerboards. The scope includes a regional assessment of the major Canadian provinces, an evaluation of regulatory shifts toward sustainable fiber-based packaging, and a competitive analysis of leading market players such as Cascades Inc., Smurfit WestRock plc, and International Paper Company.

The Canada Corrugated Packaging Market Report is Segmented by Material (Virgin Kraft Linerboard, Recycled Linerboard, Corrugating Medium, Semi-Chemical Fluting, and Other Materials), Flute Type (A Flute, B Flute, C Flute, E Flute, and F Flute), Packaging Type (Regular Slotted Containers, Die-Cut Custom Boxes, Folding Cartons, Point-of-Purchase Displays, Pallet Boxes, and Other Packaging Types), Wall Type (Single-Wall, Double-Wall, Triple-Wall, and Single Face), Printing Technology (Flexographic Printing, Digital Inkjet Printing, Litho-Lamination, Screen Printing, and Other Printing Technologies), End-User Industry (Processed Foods, Fresh Food and Produce, Beverages, Electrical Products, Personal Care and Cosmetics, E-commerce Fulfillment Centers, Pharmaceuticals, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Kraft Linerboard |

| Recycled Linerboard |

| Corrugating Medium |

| Semi-Chemical Fluting |

| Other Materials |

| A Flute |

| B Flute |

| C Flute |

| E Flute |

| F Flute |

| Regular Slotted Containers |

| Die-Cut Custom Boxes |

| Folding Cartons |

| Point-of-Purchase Displays |

| Pallet Boxes |

| Other Packaging Types |

| Single-Wall |

| Double-Wall |

| Triple-Wall |

| Single Face |

| Flexographic Printing |

| Digital Inkjet Printing |

| Litho-Lamination |

| Screen Printing |

| Other Printing Technologies |

| Processed Foods |

| Fresh Food and Produce |

| Beverages |

| Electrical Products |

| Personal Care and Cosmetics |

| E-commerce Fulfillment Centers |

| Pharmaceuticals |

| Other End-User Industries |

| By Material | Virgin Kraft Linerboard |

| Recycled Linerboard | |

| Corrugating Medium | |

| Semi-Chemical Fluting | |

| Other Materials | |

| By Flute Type | A Flute |

| B Flute | |

| C Flute | |

| E Flute | |

| F Flute | |

| By Packaging Type | Regular Slotted Containers |

| Die-Cut Custom Boxes | |

| Folding Cartons | |

| Point-of-Purchase Displays | |

| Pallet Boxes | |

| Other Packaging Types | |

| By Wall Type | Single-Wall |

| Double-Wall | |

| Triple-Wall | |

| Single Face | |

| By Printing Technology | Flexographic Printing |

| Digital Inkjet Printing | |

| Litho-Lamination | |

| Screen Printing | |

| Other Printing Technologies | |

| By End-User Industry | Processed Foods |

| Fresh Food and Produce | |

| Beverages | |

| Electrical Products | |

| Personal Care and Cosmetics | |

| E-commerce Fulfillment Centers | |

| Pharmaceuticals | |

| Other End-User Industries |

Key Questions Answered in the Report

How large is the Canada corrugated boxes market today?

The market reached USD 9.23 billion in 2025 and is set to rise to USD 9.59 billion in 2026.

What is the forecast CAGR for Canadian corrugated box demand?

Volume and value together are projected to grow at a 3.35% CAGR between 2026 and 2031.

Which segment has the highest Canada corrugated boxes market share?

Regular Slotted Containers led with 47.35% share in 2025.

Which end-use sector is expanding fastest?

E-commerce fulfillment centers are projected to grow at a 4.68% CAGR through 2031.

How are EPR regulations influencing packaging choices?

Provinces now mandate recycled content and reporting, so converters with certified post-consumer fiber gain preferred-supplier status.

Why are digital presses gaining popularity in corrugated plants?

They remove plate costs, accelerate turnaround, and support variable graphics, making them ideal for retailer-specific and subscription packaging.

Page last updated on: