Bulky Waste Collection Service Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

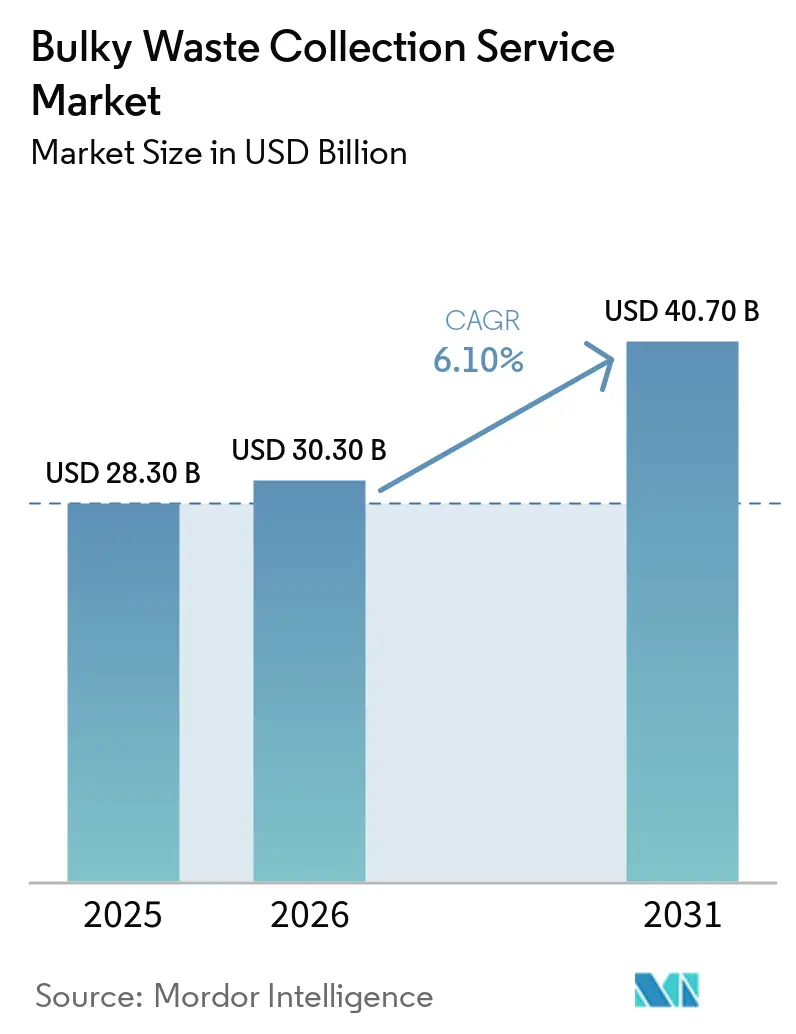

| Market Size (2026) | USD 30.30 Billion |

| Market Size (2031) | USD 40.70 Billion |

| Growth Rate (2026 - 2031) | 6.10% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bulky Waste Collection Service Market Analysis by Mordor Intelligence

The Bulky Waste Collection Service Market size is expected to grow from USD 28.30 billion in 2025 to USD 30.30 billion in 2026 and is forecast to reach USD 40.70 billion by 2031 at 6.10% CAGR over 2026-2031.

Growth aligns with urbanization, regulatory tightening, and the shift toward circular systems that prioritize diversion and reuse of oversized, non-containerizable items. Operators are standardizing digital tracking and compliance capabilities as municipalities elevate procurement criteria and link payments to diversion performance. Competitive behavior continues to pivot from tonnage-based hauling to value recovery, where AI-enabled sorting, fleet electrification, and renewable natural gas projects support service quality and margin resilience. The bulky waste collection service market is also seeing a broader role for municipal self-operation in select cities, intensifying bidding standards for private contractors while broadening opportunities for technology partnerships.

Key Report Takeaways

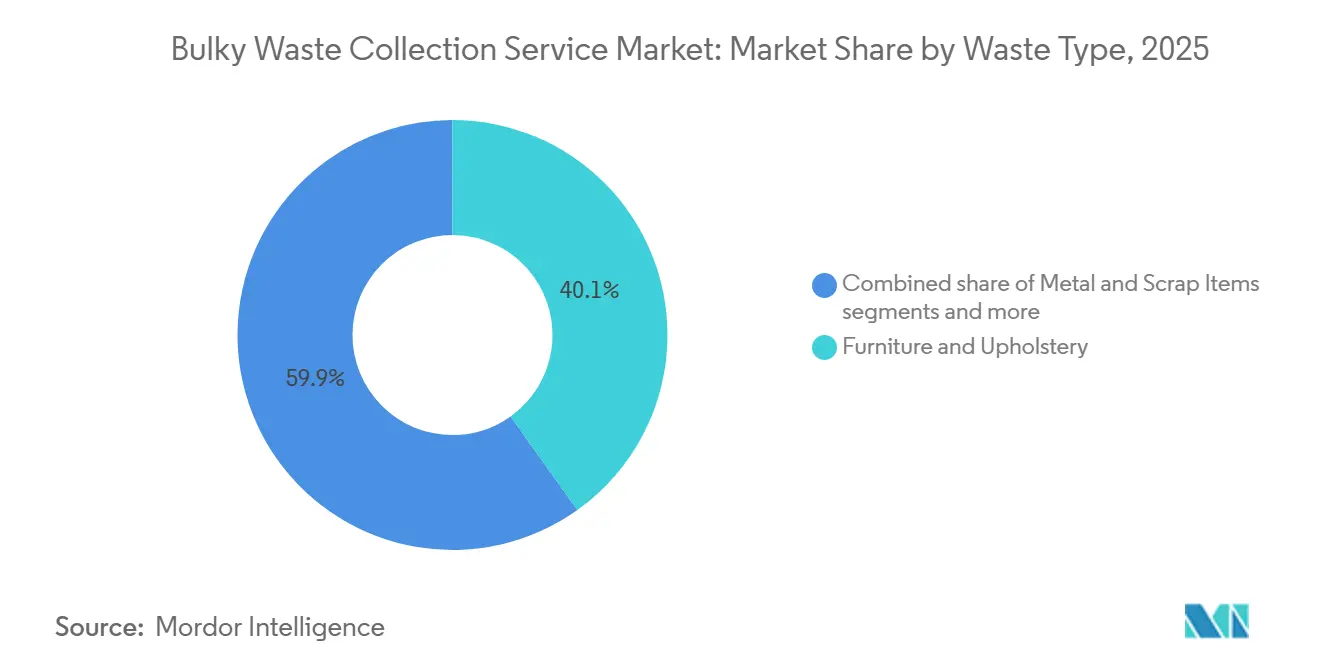

- By waste type, furniture and upholstery led with a 40.14% of the bulky waste collection service market share in 2025, while construction and demolition waste is forecast to advance at a 6.23% CAGR through 2031.

- By source, residential held 46.37% share in the bulky waste collection service market size in 2025, while municipal and government sources are projected to grow fastest at a 6.47% CAGR to 2031.

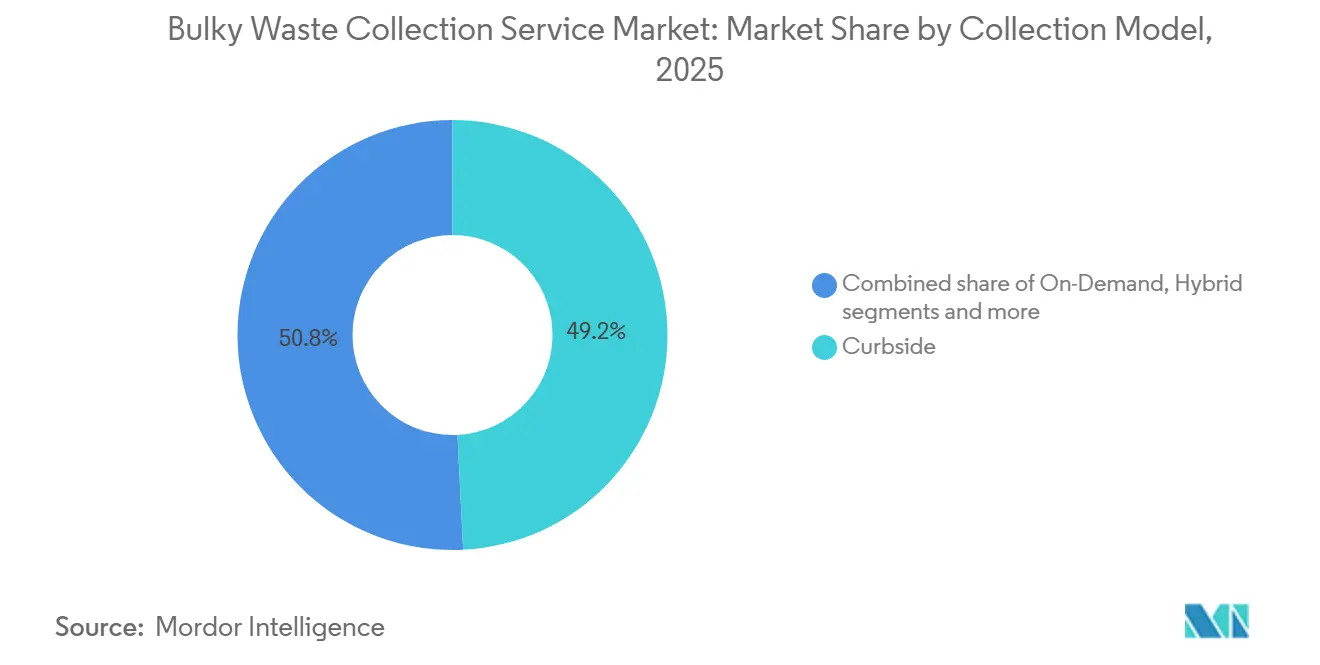

- By collection model, curbside accounted for 49.21% in 2025, while on-demand service are projected to expand at a 6.71% CAGR through 2031.

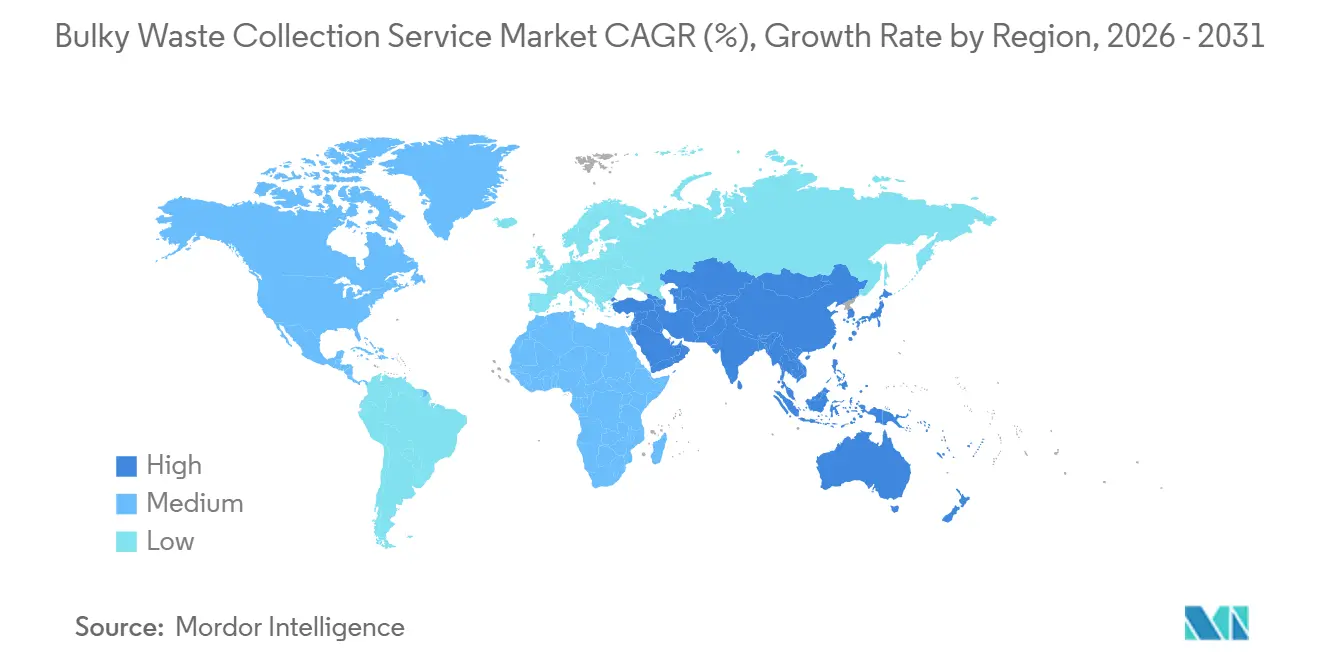

- By geography, North America led with a 35.70% share in 2025, while Asia-Pacific is projected to post the fastest CAGR of 6.52% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Bulky Waste Collection Service Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Urbanization and Municipal Solid Waste Generation | +2.5% | Global, with the highest intensity in Asia-Pacific, Sub-Saharan Africa, and Latin America | Long term (≥ 4 years) |

| Stringent Government Regulations on Waste Management | +1.8% | Global, led by the EU, North America, India, and emerging in Southeast Asia | Medium term (2-4 years) |

| Smart City Initiatives and Digital Infrastructure Development | +1.2% | North America and the EU core, with adoption across APAC | Medium term (2-4 years) |

| Increase in Construction and Demolition Activities | +0.9% | Global, particularly India, China, and the Gulf Cooperation Council states | Long term (≥ 4 years) |

| Growing Environmental Consciousness Among Consumers | +0.6% | Global, strongest in high-income urban centers | Long term (≥ 4 years) |

| Expansion of E-Commerce and Furniture Replacement Trends | +0.5% | North America, Western Europe, urban China, and India | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Urbanization and Municipal Solid Waste Generation

Rapid urban concentration continues to elevate bulky streams such as furniture, appliances, and renovation debris. Global waste volumes are projected to increase from 2.1 billion tonnes in 2023 to 3.8 billion tonnes by 2050, intensifying pressure on city systems that are already short of transfer capacity and specialized handling for oversized items. In lower-income settings, uncollected and mismanaged waste remains a structural barrier to formal capture, creating a long pipeline of latent demand as fiscal capacity, donor programs, and infrastructure financing close service gaps over time. Local authority data in England showed 25.2 million tonnes of waste collected in 2024-2025, indicating steady volumes that underscore the importance of dedicated solutions for oversized fractions that cannot be containerized. As urbanization advances, the bulky waste collection service market benefits from predictable replacement cycles and renovation activity in multi-family housing, which concentrates demand into municipal cores. The bulky waste collection service market also benefits from rising public expectations for safe, convenient removal, which steers users toward formal providers

Stringent Government Regulations on Waste Management

Policy tightening across leading jurisdictions is increasing traceability and diversion obligations, which drives the adoption of certified collection and sorting capabilities. In the European Union, the revised Waste Framework Directive entered into force on October 16, 2025, and requires Member States to establish Extended Producer Responsibility for textiles and footwear within 30 months, introducing new funding and operational flows to expand formal collection of the difficult, bulky fraction. England has increased funding for waste crime enforcement and is scaling tools such as drone surveillance and automatic number plate recognition to deter illegal operators that undercut compliant service. Regulatory emphasis on separate collection, eco-modulated fees, and pre-shipment sorting for exports is moving the system toward verifiable recovery rates, favoring operators with audit-ready digital records and robust quality control. India has codified updated construction and demolition requirements. It is rolling out national waste tracking, signaling a transition from voluntary practices to mandatory performance that expands demand for specialized bulky pick-ups and documented processing. The bulky waste collection service market is responding through compliance-led bids and partnerships that build capacity for regulated streams.

Smart City Initiatives and Digital Infrastructure Development

City programs that layer IoT, AI, and electrified fleets onto daily operations are reducing service costs and improving response times. Cambridge City Council’s Waterbeach Renewable Energy Network, underway in 2026, is designed to power a growing electric waste fleet and self-generate a majority of depot energy, supporting more sustainable and predictable collection economics. At sorting sites, SUEZ’s AutoDiag uses real-time camera analytics to detect contamination on sorting tables, thereby improving stream purity and reducing rework at selective collection centers. Municipal authorities are also formalizing appointment systems for oversized items, supported by online portals and digital authentication at public centers, thereby improving scheduling and reducing leakage into illegal dumping. The bulky waste collection service market benefits from these tools because route optimization and on-site quality control lower the marginal cost of on-demand pickups. Digitalization also enables performance-linked contracts, which help align municipal objectives with operators’ incentives.

Increase in Construction and Demolition Activities

Renovation and infrastructure cycles elevate bulky loads of rubble, lumber, and fixtures, prompting stricter controls on handling and throughput. In England, the 2026 update to the SR2022 No 3 permit framework governs construction, demolition, and excavation waste transfer stations, setting throughput, storage, and reporting criteria that standardize operations and accelerate the handoff from collection to processing. France’s public drop-off centers received over 16 million tonnes in 2021, with a large share from rubble and debris, reflecting sustained demand for specialized handling, especially as landfill restrictions tighten. Separate collection obligations for bulky fractions are increasing across municipalities, feeding more predictable volumes into formal channels and encouraging presorted pickups that reduce contamination. The bulky waste collection service market is increasingly embedded in construction project planning, where contractors face deadlines and quality expectations that make certified providers essential. Stronger linkage between building permits, compliance audits, and separate collection has raised the bar on documentation, which advantages operators that integrate digital manifests and tracking into standard workflows.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prevalence of Illegal Dumping and Informal Competition | -1.5% | Global, acute in low and middle-income countries, persistent in rural EU and US | Long term (≥ 4 years) |

| Shortage of Trained Workforce and Specialized Equipment | -0.8% | North America, Western Europe, and emerging in urban Asia | Medium term (2-4 years) |

| Lack of Standardized Waste Segregation Practices | -0.7% | Sub-Saharan Africa, South Asia, rural Latin America | Long term (≥ 4 years) |

| Limited Awareness in Rural and Developing Regions | -0.4% | Rural areas globally, particularly Sub-Saharan Africa and parts of the Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Prevalence of Illegal Dumping and Informal Sector Competition

Illegal disposal continues to divert material away from formal providers and imposes cleanup costs on local authorities. England recorded 1.26 million fly-tipping incidents in 2024-2025, with a significant share occurring on highways, and a measured public-sector spend to clear larger loads, which directly erodes the economics of compliant service models. Enforcement agencies have disrupted illegal exports and identified numerous unlicensed sites, but case volumes remain high relative to investigative capacity, indicating a persistent gap that sustains shadow activity. Waste crime is also a macroeconomic drag, with estimated multi-hundred-million-pound annual costs in the United Kingdom, which undermine investment in compliant networks and lower formal capture rates where cheap, illegal options persist. The bulky waste collection service market faces higher customer acquisition costs when enforcement is inconsistent, as households and small businesses weigh convenience and perceived risk when choosing between formal and informal channels. As digital waste tracking and targeted enforcement scale, leakage risks can recede, but near-term variability still complicates planning and utilization. Operator strategies in exposed geographies, therefore, depend on close coordination with municipalities to align communications, fee structures, and service windows with local enforcement rhythms.

Shortage of Trained Workforce and Specialized Equipment

Driver and technician gaps remain persistent across major markets, affecting collection reliability and operating costs. Industry data points to growing demand for CDL drivers, diesel technicians, and welders through 2026 as the workforce ages and competing sectors attract similar skill sets, lengthening time-to-fill and increasing training burdens for operators. Specialized equipment and safety protocols for handling heavy or hazardous bulky items require certified personnel, which concentrates capacity in firms with established training programs. The electrification of fleets and the introduction of advanced sorting and monitoring systems add to competency requirements in maintenance and operations, favoring larger players with structured upskilling programs. The bulky waste collection service market must also manage fleet availability and parts logistics for high-wear components, especially on compactors and lift mechanisms used during bulky pickups. As procurement increasingly references safety records and training evidence, firms that systematize workforce development can improve bid competitiveness and route productivity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Collection Model: On-Demand Service Gain Share via Digital Enablement

Curbside service accounted for 49.21% of the bulky waste collection market share in 2025, as long-standing municipal agreements maintained predictable, scheduled routes. On-demand formats are projected to grow faster, at a 6.71% CAGR through 2031, as app-based scheduling, IoT-enabled route optimization, and electrified fleets lower marginal pickup costs and improve service windows. Republic Services’ 2025 and 2026 investments in electric collection vehicles, renewable natural gas projects, and polymer processing demonstrate how downstream integration can offset collection volatility and enhance service proposals in municipal tenders. SUEZ’s WasteConnect and AutoDiag deployments demonstrate how connected containers, live quality monitoring, and flow analytics can increase route density and reduce contamination, which is critical for ad hoc operations. These bulky pickups vary widely in composition. The bulky waste collection service market is thus converging on hybrid operations that blend base-route efficiency with flexible capacity for same-day or next-day requests.

Public center policies reinforce this hybridization. The Aix-Marseille-Provence area revised access rules and daily limits for public drop-off centers in 2025 to standardize services and enhance valuation, thereby advancing diversion goals and reducing strain on curbside systems during seasonal peaks. In Germany, projects like Oberhavel’s free bulky waste delivery window for residents complement traditional curbside pickups and help divert volumes from unauthorized channels, while identity checks and residency proof close loopholes that previously allowed professional dumping. Local service updates, including per-collection volume caps and separate placement rules, continue to align field operations with processing needs and improve throughput at transfer sites. The bulky waste collection service market benefits when appointment systems and public center rules are well communicated, as they reduce missed collections, enhance the customer experience, and stabilize inbound quality. Price signals tied to appointment slots and off-peak incentives can further smooth demand, where regulations allow, thereby improving route productivity and asset utilization.

By Source: Municipal Procurement Drives Public-Sector Growth

Residential accounted for 46.37% of the bulky waste collection service market size in 2025 as households replaced furniture and appliances at a steady pace and relied on formal pickups for oversized items. Commercial and industrial generators are aligning with on-site sorting rules and separate collection requirements in local ordinances, creating recurring flows of pallets, fixtures, and equipment into contracted haul-off arrangements. Municipal and government sources are projected to grow fastest at a 6.47% CAGR through 2031, as performance-linked contracts and smart city investments expand the scale and scope of bulky pickup operations. Cambridge’s Waterbeach Renewable Energy Network illustrates the public sector’s shift toward integrated energy and fleet solutions that can support reliable collection schedules and lower lifecycle costs. The World Bank’s focus on results-based financing for waste systems underscores how municipalities are tying payments to outcomes such as diversion and fee recovery, thereby encouraging the adoption of app-based scheduling and digital tracking for bulky loads.

Local regulations and operating rules steer volumes into formal channels. French authorities continue to formalize access to public drop-off centers, including measures that restrict professional access in zones with nearby private alternatives and establish donation areas for reuse in partnership with social economy groups. Enforcement actions and publicity around fly-tipping sustain pressure on informal routes and encourage residents to book authorized pickups for oversized items. The bulky waste collection service market benefits as local governments standardize booking requirements, volume caps, and documentary evidence for access to public centers, reducing confusion for households and increasing the reliability of inbound flows. For operators, transparent municipal playbooks enhance route planning, reduce non-collection incidents caused by non-compliance, and support field team training to manage customer expectations at the curb.

By Waste Type: Construction Debris Emerges as Fastest-Growth Category

Furniture and upholstery led in 2025, with 40.14% of the bulky waste collection service market share, as households and offices cycled through sofas, tables, and chairs more frequently during post-pandemic reconfigurations. U.S. data on furniture discards show a large, rising volume, supporting steady pickup flows for bulky items and reinforcing the role of scheduled and on-demand services for items that cannot be containerized at curbside. Construction and demolition debris is projected to post the fastest 6.23% CAGR through 2031 as permit conditions and separate collection obligations proliferate across municipalities. The bulky waste collection service market is adjusting to project-linked pickups and tighter quality controls at transfer stations to reduce contamination and ensure throughput. England’s SR2022 No 3 permit regime sets clear storage and throughput parameters at transfer stations and requires regular reporting, which makes documented handoffs and pre-sorting protocols central to service design, GOV.UK. France’s network of drop-off centers demonstrates how public access infrastructure, combined with landfill restrictions, can maintain significant volumes of rubble and other bulky fractions in formal channels.

Policy evolution is expanding selective streams. The EU’s updated framework reinforces separate collection for textiles and footwear under Extended Producer Responsibility, directing funding toward sorting and reuse and compelling formal collection pathways for materials often associated with bulky pickups. Appliances and other white goods will continue to be shaped by WEEE and battery regulations, prompting more frequent separate collections and specialized depollution handling. On the commodity side, operators with integrated recycling assets can mitigate revenue variability during pricing troughs, as downstream polymer and renewable natural gas assets provide margin backstops independent of collection volumes. In this context, contractors that align pickup scheduling with drop-off center rules and integrate documentation standards into field operations can reduce rejection risk and maintain steady throughput. The bulky waste collection service market is therefore oriented toward a compliance-first approach that balances household convenience with processing quality requirements.

Geography Analysis

North America led with 35.70% of the bulky waste collection service market share in 2025, supported by steady furniture turnover and maturing Extended Producer Responsibility measures that subsidized mattress and furniture collection in several states. Reported company investments into renewable natural gas, polymers, and electrification in 2025 and 2026 indicate continued emphasis on value recovery that complements scheduled and on-demand bulky pickups. As municipalities tighten quality expectations and add digital reporting to curbside programs, operators with integrated downstream assets can differentiate on both compliance and economics. The bulky waste collection service market in Canada and Mexico is also navigating formalization trends, though informal activity remains a headwind due to uneven enforcement capacity. In this region, route density and workforce availability remain the decisive factors in securing multi-year contracts, particularly in large metropolitan areas with seasonal, bulky peaks.

Europe’s policy harmonization is reshaping collection economics and execution. In October 2025, the EU's updated Waste Framework Directive came into effect, mandating Extended Producer Responsibility for textiles and footwear. The directive also emphasized the separate collection of hazardous materials and set targets for reducing food waste. These changes broadened the scope of materials managed under official programs, heightening the demand for traceable routing and sorting. France’s public drop-off network serves as a mature template for how citizens and contractors route bulky items into formal channels, reflecting the impact of landfill restrictions and program design on user behavior. England’s data on local authority-collected waste and fly-tipping underscores the importance of enforcement to protect compliant operators and maintain progress toward diversion goals. As digital tracking advances in cross-border waste shipment rules and Member States operationalize textile EPR schemes, operators see new logistics requirements that favor those with strong systems integration. The bulky waste collection service market in Europe is, therefore, aligning route planning with public center access controls and appointment systems to ensure smooth handoffs and reliable throughput at sorting and recovery sites.

Asia-Pacific is projected to be the fastest-growing region at a 6.52% CAGR through 2031. India’s national digital waste-tracking program and recent updates to construction and demolition rules signal a shift toward formalized recovery and traceability, bringing more bulky loads into regulated channels. As major cities in the region scale curbside and appointment models for oversized items, policymakers are prioritizing quality and safety standards, which require better-trained crews and modernized fleets. In Southeast Asia and parts of Africa, improving enforcement and public education will be a prerequisite for reducing leakage into informal channels and increasing service penetration, especially for bulky waste. Academic work in Sub-Saharan Africa highlights that regulatory compliance with household segregation depends on clear communication and consistent enforcement, both of which directly affect routing bulky fractions toward formal collection. As governments roll out integrated systems and step up oversight, the bulky waste collection service market will benefit from broader formal participation and more stable processing flows.

Competitive Landscape

The bulky waste collection service market remains moderately concentrated in North America and Western Europe, with large integrated firms competing alongside municipal self-operation and a long tail of regional haulers in other geographies. Strategic focus has shifted toward value recovery and compliance capacity, where operators deploy capital into renewable natural gas, polymers, and hazardous waste capabilities to complement bulky pickups. Republic Services’ 2025 results and 2026 guidance included continued investment in electrified fleets and downstream processing, which positioned the company to improve service economics and compliance performance in municipal tenders. Veolia’s GreenUp 2024-2027 program directs growth investment into local energy, water technologies, and hazardous waste treatment, reflecting a multi-pronged approach to regulated materials and recovery infrastructure. The bulky waste collection services market is therefore defined by operators that can integrate collection, sorting, and recovery while meeting higher compliance thresholds.

Technology is central to competitive differentiation. SUEZ’s AI-enabled AutoDiag rollout at select collection centers demonstrates how real-time analytics can reduce contamination and improve line uptime, directly supporting higher purity and throughput in facilities that handle bulky items. Digital route optimization, connected containers, and customer-facing appointment systems also enable on-demand models that scale without eroding route density, which helps protect margins as service windows tighten. On the public side, Cambridge’s integrated energy and fleet project shows how municipal operators can embed renewable power into collection operations, which stabilizes costs and emissions while maintaining service reliability. As procurement frameworks place greater weight on sustainability, digital traceability, and safety, bidders that present integrated solutions will continue to improve win rates.

Compliance and policy alignment are widening the gap between leaders and the rest. The EU’s revised Waste Framework Directive sets a clear path for textile EPR and pre-shipment sorting, creating new logistics and reporting needs for bulky fractions often generated in residential and institutional settings. Operators that document the chain of custody from curbside to processing can align with these rules at a lower incremental cost than peers who retrofit systems under deadline pressure. In this environment, investments into staff training, safety standards, and digital recordkeeping are not discretionary but foundational to growth. The bulky waste collection service market is thus consolidating around capabilities that deliver transparent, high-quality service while monetizing recovered materials across multiple outlets.

Bulky Waste Collection Service Industry Leaders

Waste Management, Inc.

Republic Services, Inc.

Veolia Environnement S.A.

SUEZ S.A.

Biffa plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Republic Services reported 2025 revenue of USD 16.591 billion (+3.5%) and adjusted free cash flow of USD 2.43 billion (+11.5%). It invested over USD 1 billion in acquisitions and completed nine renewable natural gas projects. For 2026, it forecasts USD 17.05-17.15 billion in revenue and allocated USD 1 billion for M&A.

- January 2026: Cambridge City Council broke ground on the GBP 6.1 million Waterbeach Renewable Energy Network, pairing a 1 MW solar array with battery storage and 36 EV charging points to power 18 electric bin lorries by 2027, targeting 59% of depot energy needs from renewables, achieving >40% biodiversity net gain, and reducing waste fleet carbon emissions with payback through free clean energy within 15 years.

- February 2025: SUEZ launched AutoDiag®, France's first AI-powered waste quality monitoring tool, analyzing waste in real-time across 36 centers. Recognized at the AI Summit (February 10-11, 2025), it reduces defect rates by 20-30% and improves the purity of paper, cardboard, and plastic film streams.

Global Bulky Waste Collection Service Market Report Scope

The Bulky Waste Collection Service market encompasses specialized waste management services designed to collect, transport, and dispose of oversized, heavy, or non-containerizable items such as furniture, appliances, mattresses, carpets, and large household goods that exceed the capacity and handling capabilities of regular Municipal Solid Waste (MSW) collection systems. This market includes on-demand pickup services, scheduled curbside collection programs, drop-off centers, and contracted municipal services that use specialized vehicles, equipment, and trained personnel to manage waste streams that require alternative collection, processing, and disposal methodologies.

The Bulky Waste Collection Service Market Report is Segmented by Waste Type (Furniture & Upholstery, Metal & Scrap Items, White Goods/Appliances, Construction & Demolition, Others), Source (Residential, Commercial, Industrial, Municipal/Government, Others), Collection Model (Curbside, On-Demand, Hybrid, Contracted B2B, Others), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD Billion).

| Curbside |

| On-Demand |

| Hybrid |

| Contracted B2B |

| Others |

| Residential |

| Commercial |

| Industrial |

| Municipal/Government |

| Others (Religious Institutions, Temporary Disaster Relief Camps, Film/TV Production Sets) |

| Furniture & Upholstery |

| Metal & Scrap Items |

| White Goods/Appliances |

| Construction & Demolition |

| Others (Event-specific Waste, Biomedical/Institutional) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Collection Model | Curbside | |

| On-Demand | ||

| Hybrid | ||

| Contracted B2B | ||

| Others | ||

| By Source | Residential | |

| Commercial | ||

| Industrial | ||

| Municipal/Government | ||

| Others (Religious Institutions, Temporary Disaster Relief Camps, Film/TV Production Sets) | ||

| By Waste Type | Furniture & Upholstery | |

| Metal & Scrap Items | ||

| White Goods/Appliances | ||

| Construction & Demolition | ||

| Others (Event-specific Waste, Biomedical/Institutional) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size and outlook for the bulky waste collection service market?

The bulky waste collection service market size was USD 28.3 billion in 2025 and is projected to reach USD 40.7 billion by 2031, growing at a 6.1% CAGR over 2026-2031.

Which segments lead growth within the bulky waste collection service market?

Construction and demolition waste is the fastest-growing waste type, with a 6.23% CAGR; municipal and government sources lead growth at 6.47%; and on-demand services are projected to expand at a 6.71% CAGR.

Which region leads and which is growing fastest in the bulky waste collection service market?

North America led with 35.70% in 2025, while Asia-Pacific is projected to post the fastest CAGR of 6.52% through 2031.

How are regulations influencing the bulky waste collection service market?

The European Union revised Waste Framework Directive, stronger United Kingdom enforcement, and India’s national tracking initiatives are elevating traceability and recovery requirements, favoring compliant, digitally enabled operators.

What technologies are improving performance in the bulky waste collection service market?

AI-enabled sorting and monitoring, connected containers, route optimization, and fleet electrification are improving purity, lowering costs, and enabling reliable on-demand pickups.

What are the key challenges facing the bulky waste collection service market today?

Persistent illegal dumping and workforce shortages in drivers and technicians pressure margins and reliability, making enforcement coordination and training programs critical for sustained performance.

Page last updated on: