Brugada Syndrome Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

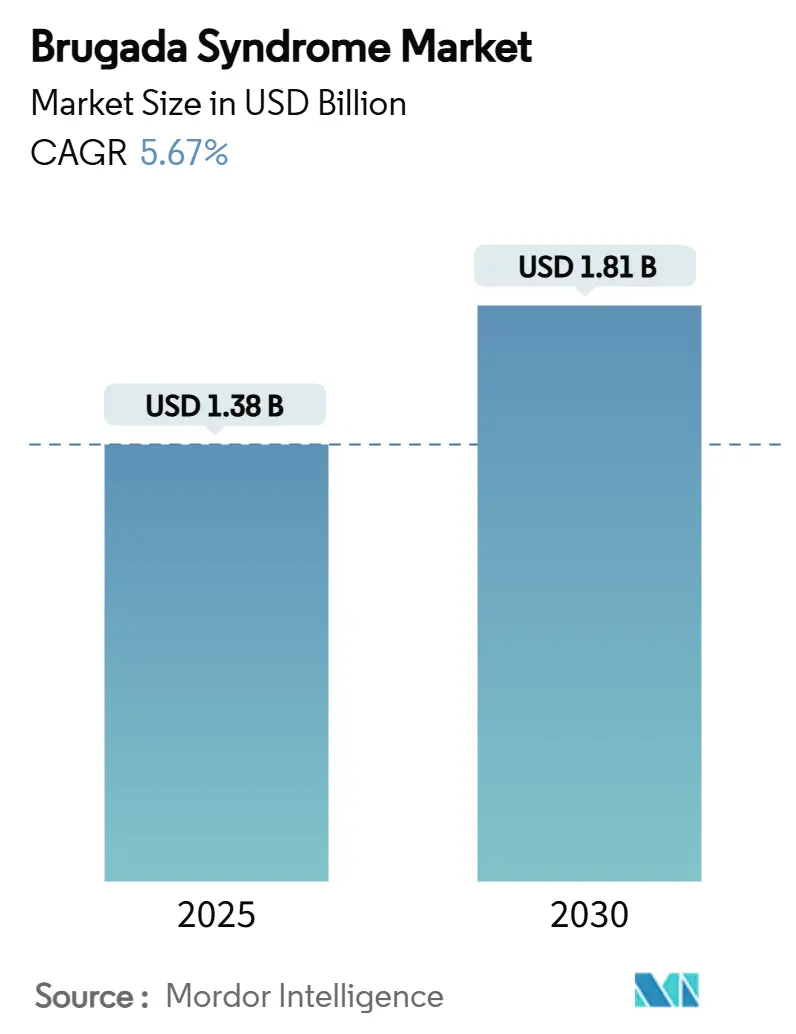

| Market Size (2025) | USD 1.38 Billion |

| Market Size (2030) | USD 1.81 Billion |

| Growth Rate (2025 - 2030) | 5.67% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brugada Syndrome Market Analysis by Mordor Intelligence

The global Brugada syndrome market reached USD 1.38 billion in 2025 and is on track to climb to USD 1.81 billion by 2030, reflecting a 5.67% CAGR. This market size expansion is propelled by rising implantable-cardioverter-defibrillator (ICD) adoption, accelerating artificial-intelligence electrocardiogram (AI-ECG) penetration and growing genetic-testing uptake. Increased recognition of Brugada syndrome as a significant cause of sudden cardiac death, particularly in Southeast Asia, continues to widen the diagnosed patient pool. Technological advances such as extravascular ICD systems and deep-learning ECG analytics are reshaping clinical decision pathways. A supportive policy environment—including orphan-drug incentives and newborn-screening pilots—fuels device and diagnostics research. Companies that successfully connect high-end interventional products with affordable, accessible screening solutions are strengthening their competitive positions in the Brugada syndrome market.[1]Center for Devices and Radiological Health, “Aurora EV-ICD System – P220012,” U.S. Food and Drug Administration, fda.gov

Key Report Takeaways

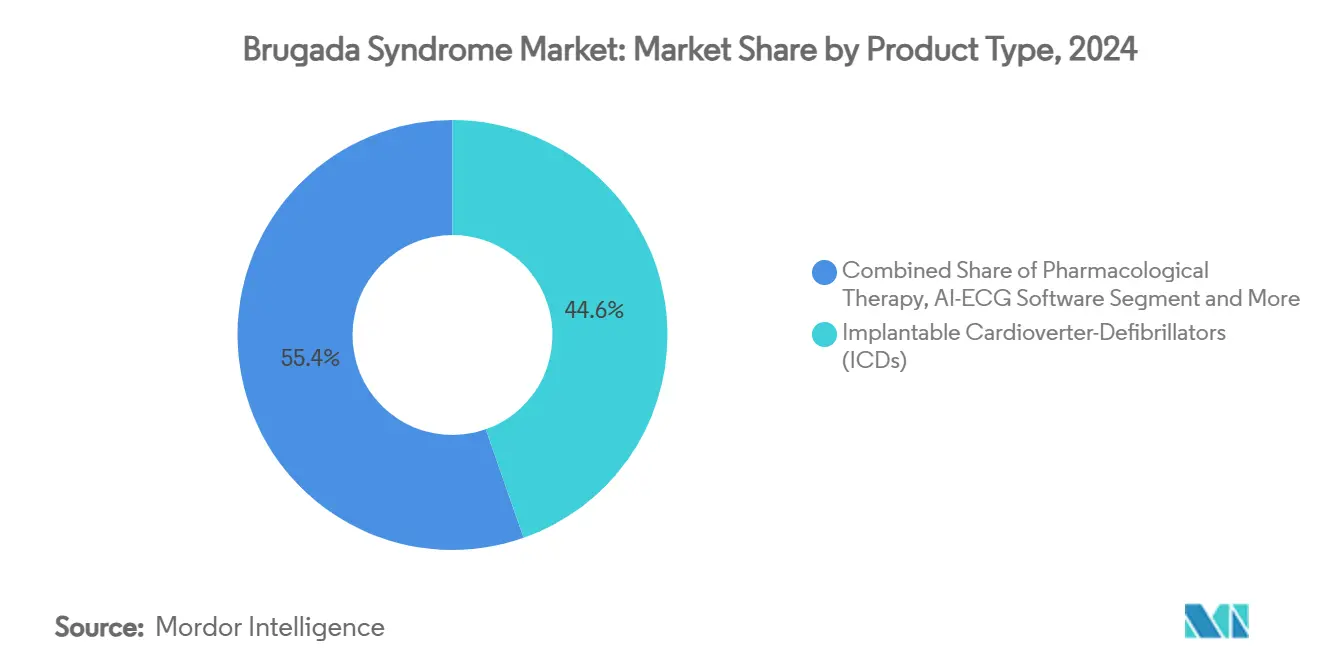

- By product type, implantable cardioverter-defibrillators held 44.62% of the Brugada syndrome market share in 2024. AI-ECG software is projected to expand at the fastest 9.77% CAGR through 2030.

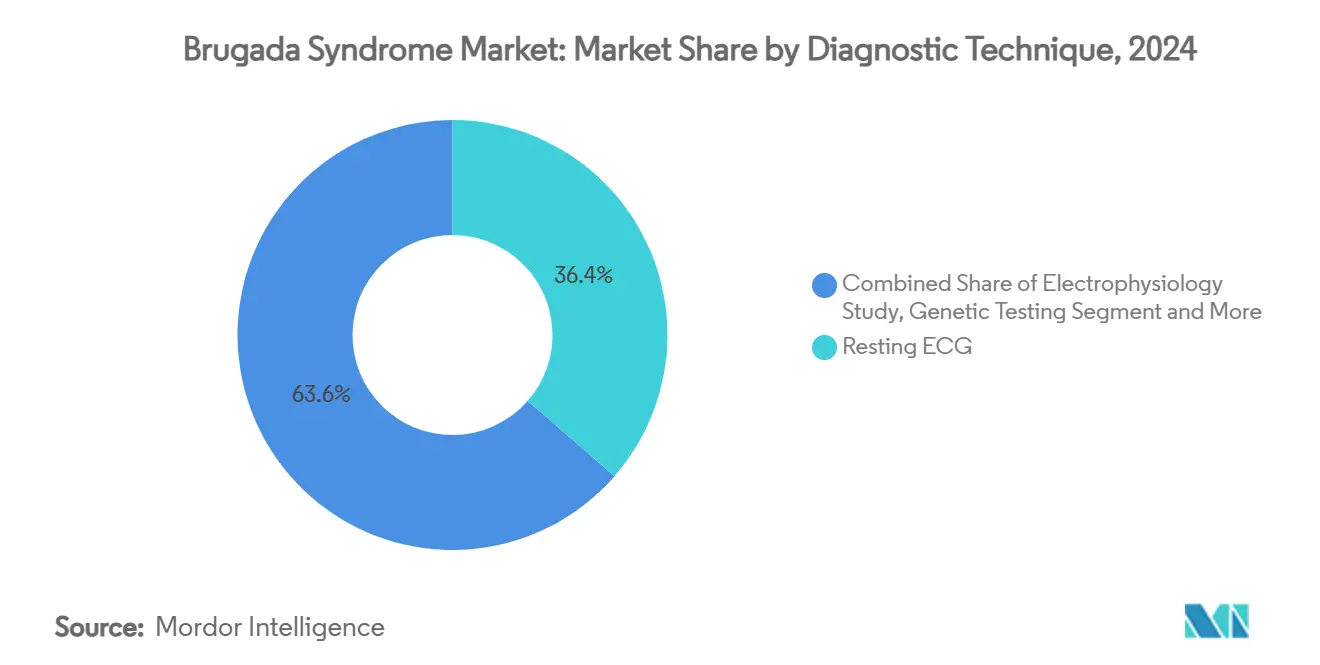

- By diagnostic technique, conventional resting ECG controlled 36.42% of the Brugada syndrome market size in 2024, whereas genetic testing is advancing at an 8.39% CAGR.

- By end user, hospitals retained 49.76% share of the Brugada syndrome market size in 2024, while home-care settings are growing at a 9.63% CAGR.

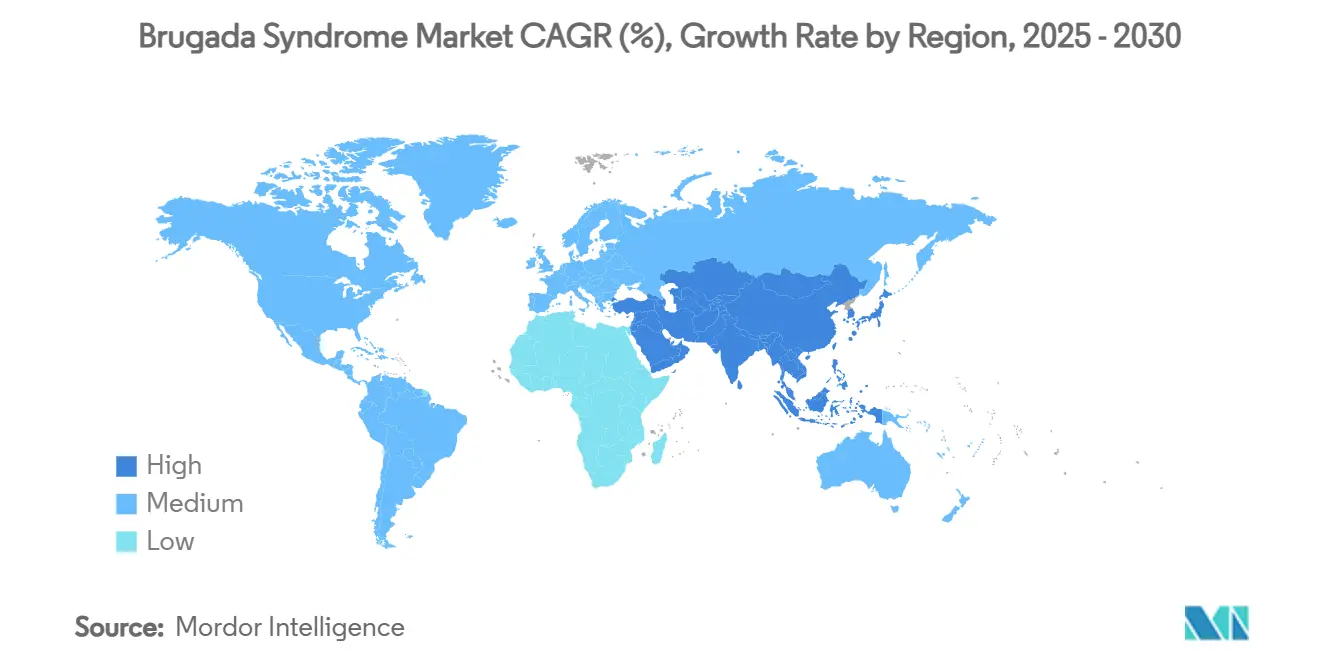

- By geography, North America led with 39.23% revenue share in 2024; Asia-Pacific is forecast to deliver an 8.05% CAGR to 2030.

Global Brugada Syndrome Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising ICD implantation | +1.2% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Growing awareness & screening programmes | +0.8% | Asia-Pacific, Middle East & Africa | Long term (≥ 4 years) |

| Advances in genetic-testing technologies | +0.9% | United States, European Union, Japan | Medium term (2-4 years) |

| Orphan-drug incentives accelerating R&D | +0.6% | North America, European Union | Long term (≥ 4 years) |

| AI-enabled ECG interpretation uptake | +1.1% | Developed markets worldwide | Short term (≤ 2 years) |

| Newborn genomic-screening pilots | +0.4% | Select high-income healthcare systems | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising ICD Implantation

Stronger evidence of ICD effectiveness has moved risk-benefit assessments decisively in favor of implantation for both symptomatic and asymptomatic patients. The FDA-cleared Aurora EV-ICD achieved 98.7% ventricular-arrhythmia termination while sidestepping vascular-lead complications, expanding eligibility to patients previously considered unsuitable. Medtronic’s OmniaSecure lead posted 97.5% acute success and projected 99.9% fracture-free survival at 2 years, reducing long-term durability concerns. These outcomes reinforce cardiologist confidence, foster payer willingness to reimburse and widen the Brugada syndrome market’s treated population. Device miniaturization and simplified implantation workflows further lift procedure volumes. In concert, North America and Europe continue to post the highest ICD penetration, but growth is now accelerating in Asia-Pacific as healthcare funding improves.

Growing Awareness & Screening Programmes

National and regional screening drives are revealing undiagnosed cases, especially in Southeast Asia where prevalence exceeds global averages. Indonesia’s telemedicine programme detected Brugada ECG patterns in 1.07% of 9,558 screened individuals—much higher than Western discovery rates—highlighting the upside potential from structured population screening.[2]Muzakkira Amir, “Telemedicine for Detecting Brugada Syndrome in Eastern Indonesia,” Annals of Medicine and Surgery, journals.lww.com The Dutch consensus on paediatric screening formalised protocols for fever monitoring and family history, offering a template that can be adapted elsewhere.[3]Puck Peltenburg, “Screening, Diagnosis and Follow-up of Brugada Syndrome in Children,” Netherlands Heart Journal, springer.com Educational campaigns by patient associations and cardiology societies amplify these efforts. Digital platforms disseminate symptom awareness and deliver at-home ECG kits, further expanding the diagnostic funnel. Collectively, these initiatives enlarge the addressable base for the Brugada syndrome market.

Advances in Genetic-Testing Technologies

High-throughput sequencing and better variant-interpretation algorithms now identify pathogenic mutations with greater sensitivity. A 30-year cohort study confirmed disease-causing variants in 20.8% of tested patients, with SCN5A mutations linking to higher arrhythmia risk. In China, novel mutations surfaced in 42.37% of patients, emphasising ethnic specificities that generic panels miss. Falling sequencing costs allow broader family cascade testing, boosting early detection and personalised care. Laboratories increasingly bundle Brugada panels with arrhythmia packages, creating economies of scale and a growing revenue stream inside the Brugada syndrome market. Insurers, observing clear prognostic value, are gradually expanding coverage to include genetic testing.

Orphan-Drug Incentives Accelerating R&D

Though Brugada syndrome affects a small global cohort, regulatory incentives tilt the risk-reward balance toward innovation. The US Orphan Products Grants Program funds early-stage trials targeting unmet needs, while EU frameworks offer fee waivers and 10-year exclusivity. These levers reduce development costs for novel pharmacotherapy, ablation catheters and conduction system pacing systems. Companies leverage accelerated review pathways and tax credits to justify investment in niche indications within the Brugada syndrome market. As a result, a growing pipeline of substrate-modification devices and sodium-channel modulating drugs is moving toward clinical testing phases. However, commercial viability still demands cross-indication platforms or technology transfer to broader arrhythmia applications.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High ICD costs & complication risk | -1.4% | Low- and middle-income countries | Medium term (2-4 years) |

| Limited patient pool discouraging R&D | -0.9% | Global | Long term (≥ 4 years) |

| Diagnostic-expertise variability | -0.7% | Asia-Pacific, Middle East & Latin America | Medium term (2-4 years) |

| Cultural reluctance toward device implantation | -0.5% | Select Asia-Pacific & African regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High ICD Costs & Complication Risk

Device prices, procedure charges and follow-up costs remain prohibitive for many health systems. In Kenya, 75% of eligible patients declined ICDs for financial reasons, and only 33.5% underwent implantation. Even where funding exists, complication rates present additional deterrents: inappropriate shocks occur in 24% of cases, and lead failure hits 29% within 10 years. These issues drive hesitancy among clinicians, patients and payers. While extravascular leads promise to reduce re-intervention needs, they do not yet eliminate the economic hurdle, tempering the growth slope of the Brugada syndrome market.

Limited Patient Pool Discouraging R&D

With roughly 0.5 per 1,000 global prevalence—and 6.8 per 1,000 in Thailand—the absolute patient count is small. Moreover, only 30% of cases are linked to identified SCN5A mutations, scattering the cohort across multiple genetic subtypes. Pharmaceutical firms calculate that narrow indications may not justify high-cost late-phase trials, steering budgets toward broader arrhythmia markets. Device developers offset this constraint through platform technologies adaptable to other ventricular-tachyarrhythmia indications, yet smaller start-ups face funding headwinds. The resulting innovation gap slows diversification of therapeutic options inside the Brugada syndrome market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: ICDs Anchor Revenue While AI-ECG Outpaces Growth

Implantable cardioverter-defibrillators captured 44.62% of the Brugada syndrome market share in 2024, making them the single largest revenue source within the overall Brugada syndrome market size. Their dominance reflects strong clinical-outcome evidence and deep reimbursement penetration in North America and Europe. Extravascular systems such as the FDA-approved Aurora EV-ICD are widening patient eligibility by eliminating vascular-lead complications, while Medtronic’s durable OmniaSecure lead technology is lowering long-term revision risk. Even so, price sensitivity in emerging economies is curbing volume expansion, creating room for cost-optimized devices from new entrants.

The product landscape is shifting as AI-ECG software posts a 9.77% CAGR—the fastest in the segment—driven by hospital digitization and consumer wearable adoption that promise earlier, non-invasive detection of at-risk patients. Genetic-testing kits and reagents are also rising on the back of falling sequencing costs and higher clinical-utility recognition, broadening family cascade screening. Pharmacologic agents such as quinidine maintain a niche role in symptomatic management, while pulsed-field ablation catheters like Abbott’s Volt system are gaining traction for substrate modification procedures. Together, these trends illustrate a pivot from reactive device therapy to proactive, data-driven disease management across the Brugada syndrome industry.

By Diagnostic Technique: Genetic Testing Accelerates Beyond Traditional ECG

Resting and provoked ECG retained 36.42% of the Brugada syndrome market share in 2024, supported by universal availability and low per-test cost. Ajmaline and flecainide challenge protocols remain essential for unmasking concealed patterns, yet their invasive nature and resource requirements limit scaling in primary-care settings. Electrophysiology studies deliver high specificity for risk stratification but are reserved for select high-risk cohorts because of procedural complexity.

Genetic testing is the fastest-growing modality at an 8.39% CAGR, reflecting its ability to identify pathogenic variants in 20.8% of patients and guide family screening, thereby expanding the Brugada syndrome market size addressed by preventive strategies. Deep-learning ECG analytics, achieving 0.976 area under the curve accuracy, are automating pattern recognition in both 12-lead and Holter data, reducing reliance on expert interpretation and accelerating triage. Cardiac MRI and CT fulfill complementary roles, ruling out structural cardiomyopathies that mimic Brugada syndrome, while wearable devices extend continuous monitoring to home settings. Collectively these advances signal an ongoing migration from episodic, clinic-based diagnostics to longitudinal, genetics-informed surveillance across the Brugada syndrome industry.

By End User: Home Care Disrupts the Hospital-Centric Model

Hospitals accounted for 49.76% of the Brugada syndrome market size in 2024, anchored by operating-room based ICD implantations and electrophysiology studies. Specialty cardiac clinics supplement hospital activity through device follow-up and advanced ablation procedures, maintaining stable mid-single-digit growth. Diagnostic laboratories are benefitting from higher genetic-test volumes as payers expand coverage, and academic institutes drive clinical-trial enrollment that feeds innovation pipelines.

Home-care settings are recording a 9.63% CAGR—the quickest among end users—as AI-equipped wearables and cloud-linked monitoring platforms enable safe, continuous arrhythmia surveillance beyond hospital walls. This decentralization lowers travel burdens for patients and reduces system costs, especially in geographies where specialist centers are sparse. Telemedicine frameworks established during the COVID-19 pandemic have normalized remote consultations, making physician oversight feasible for community-managed Brugada cohorts. The interplay of reimbursement support, patient preference for convenience and robust digital infrastructure is expected to lift home-care penetration steadily, reinforcing a broader move toward value-based, patient-centric delivery across the Brugada syndrome market.

Geography Analysis

North America captured 39.23% of 2024 revenue, reflecting robust reimbursement, mature electrophysiology infrastructure and high ICD penetration. The Brugada syndrome market size in this region is forecast to grow steadily as AI-ECG solutions gain Medicare and private-payer coverage. Europe leverages coordinated healthcare systems and active registries but faces pricing pressures that temper device ASPs. Asia-Pacific, by contrast, posts the fastest 8.05% CAGR, buoyed by high prevalence in Japan, Thailand and the Philippines and expanding specialist capacity. Thailand’s 6.8 per 1,000 prevalence translates into a disproportionately large at-risk cohort compared with Western populations. Governments across ASEAN are investing in electrophysiology labs, and private insurers in China are beginning to reimburse ablation and ICD therapies, feeding regional momentum.

Middle East & Africa remain nascent yet promising. Gulf states fund tertiary cardiac centers that import latest ICD platforms, whereas sub-Saharan Africa struggles with cost barriers. Latin America shows moderate uptake, with Brazil’s private insurance market underwriting ICDs for primary prevention. Across all emerging markets, the Brugada syndrome market share gains are tightly linked to economic growth, local manufacturing initiatives and training programmes that broaden physician expertise.

Although prevalence varies, a universal driver across regions is the migration of care from hospitals to outpatient and home settings. Governments see remote monitoring as a cost-containment lever, while patients value convenience. AI-driven ECG analysis and smartphone-based alerts are therefore scaling faster in Asia-Pacific and Latin America than in highly regulated Western systems. These dynamics underscore how geography influences both technology-mix adoption and overall Brugada syndrome market growth trajectory.

Competitive Landscape

The Brugada syndrome market remains moderately concentrated, with the top three ICD manufacturers—Medtronic, Abbott, Boston Scientific—commanding the bulk of device revenue. High regulatory barriers and complex supply chains deter new entrants. Nonetheless, diagnostic and digital-health segments are more fragmented, allowing nimble software firms and wearable-device makers to penetrate. Strategic collaborations are multiplying: Medtronic partners with AI analytics companies to integrate remote monitoring into its CareLink network, while Abbott licenses ECG-classification algorithms to embed in its smartphones-linked devices. Boston Scientific is diversifying through conduction-system pacing leads recently approved for expanded indication.

M&A activity focuses on digital-diagnostics tuck-ins that extend hardware lifecycle value. Venture capital flows toward cloud-ECG analytics and genetic-interpretation platforms able to service multiple arrhythmia indications. Competitive intensity is set to rise as Chinese device makers close quality gaps and target cost-sensitive emerging markets. Yet Western incumbents retain scale advantages in clinical-evidence generation and physician training programmes. Overall, success hinges on delivering integrated platforms that align screening, diagnosis, therapy and remote follow-up into a seamless pathway for Brugada syndrome patients.

Brugada Syndrome Industry Leaders

Medtronic plc

Abbott Laboratories

Boston Scientific Corporation

Biotronik SE & Co. KG

MicroPort Scientific Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Abbott received CE Mark for its Volt Pulsed Field Ablation System, posting 99.1% pulmonary-vein isolation success and launching commercial procedures across Europe.

- January 2025: AliveCor validated its Kardia 12L ECG System, showing equivalence to standard 12-lead ECGs for 35 cardiac determinations and reinforcing AI-enabled point-of-care screening viability.

Global Brugada Syndrome Market Report Scope

| Implantable Cardioverter-Defibrillators (ICDs) |

| Pharmacological Therapy |

| Catheter Ablation Equipment |

| Genetic Testing Kits & Reagents |

| AI-ECG Software |

| Wearable ECG Monitors |

| Others |

| Resting/Provoked ECG |

| Ajmaline/Flecainide Challenge Test |

| Electrophysiology Study |

| Genetic Testing |

| Cardiac Imaging (MRI/CT) |

| Hospitals |

| Specialty Cardiac Clinics |

| Diagnostic Centers & Laboratories |

| Academic & Research Institutes |

| Home-care Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Implantable Cardioverter-Defibrillators (ICDs) | |

| Pharmacological Therapy | ||

| Catheter Ablation Equipment | ||

| Genetic Testing Kits & Reagents | ||

| AI-ECG Software | ||

| Wearable ECG Monitors | ||

| Others | ||

| By Diagnosis Technique | Resting/Provoked ECG | |

| Ajmaline/Flecainide Challenge Test | ||

| Electrophysiology Study | ||

| Genetic Testing | ||

| Cardiac Imaging (MRI/CT) | ||

| By End User | Hospitals | |

| Specialty Cardiac Clinics | ||

| Diagnostic Centers & Laboratories | ||

| Academic & Research Institutes | ||

| Home-care Settings | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

1. What is the current value of the Brugada syndrome market?

The market was valued at USD 1.38 billion in 2025 and is expected to reach USD 1.81 billion by 2030 at a 5.67% CAGR.

2. Which product segment dominates revenue?

Implantable cardioverter-defibrillators hold the largest 44.62% revenue share, underscoring their position as the primary preventive therapy.

3. Why is Asia-Pacific the fastest-growing region?

High disease prevalence, expanding electrophysiology capacity and cultural shifts toward device acceptance are driving an 8.05% regional CAGR.

4. How is AI influencing Brugada syndrome diagnosis?

Deep-learning algorithms integrated into wearable and portable ECG systems detect characteristic patterns with cardiologist-level accuracy, enabling earlier and wider screening.

5. What restraints could slow market growth?

High ICD costs, procedural complication risks and limited R&D incentives stemming from a small patient pool present challenges, especially in developing economies.

Page last updated on: