Bronchopulmonary Dysplasia Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 535.55 Million |

| Market Size (2031) | USD 763.14 Million |

| Growth Rate (2026 - 2031) | 7.34% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bronchopulmonary Dysplasia Market Analysis by Mordor Intelligence

The Bronchopulmonary Dysplasia Market size is estimated at USD 535.55 million in 2026, and is expected to reach USD 763.14 million by 2031, at a CAGR of 7.34% during the forecast period (2026-2031).

Rising survival of extremely low-birth-weight infants, rapid diffusion of non-invasive ventilation that minimizes ventilator-induced injury, and an emerging pipeline of regenerative therapies together sustain the upward trajectory of the bronchopulmonary dysplasia market. Increased deployment of closed-loop oxygen titration devices, widening adoption of bundled drug regimens pairing surfactant with caffeine and vitamin A, and payer-driven shifts toward step-down critical-care centers further lift revenue prospects. Conversely, infrastructure gaps in low-income settings, the absence of approved disease-modifying pharmacotherapies, and the high upfront cost of advanced cell therapies temper overall momentum but have not derailed investment in the bronchopulmonary dysplasia market.

Key Report Takeaways

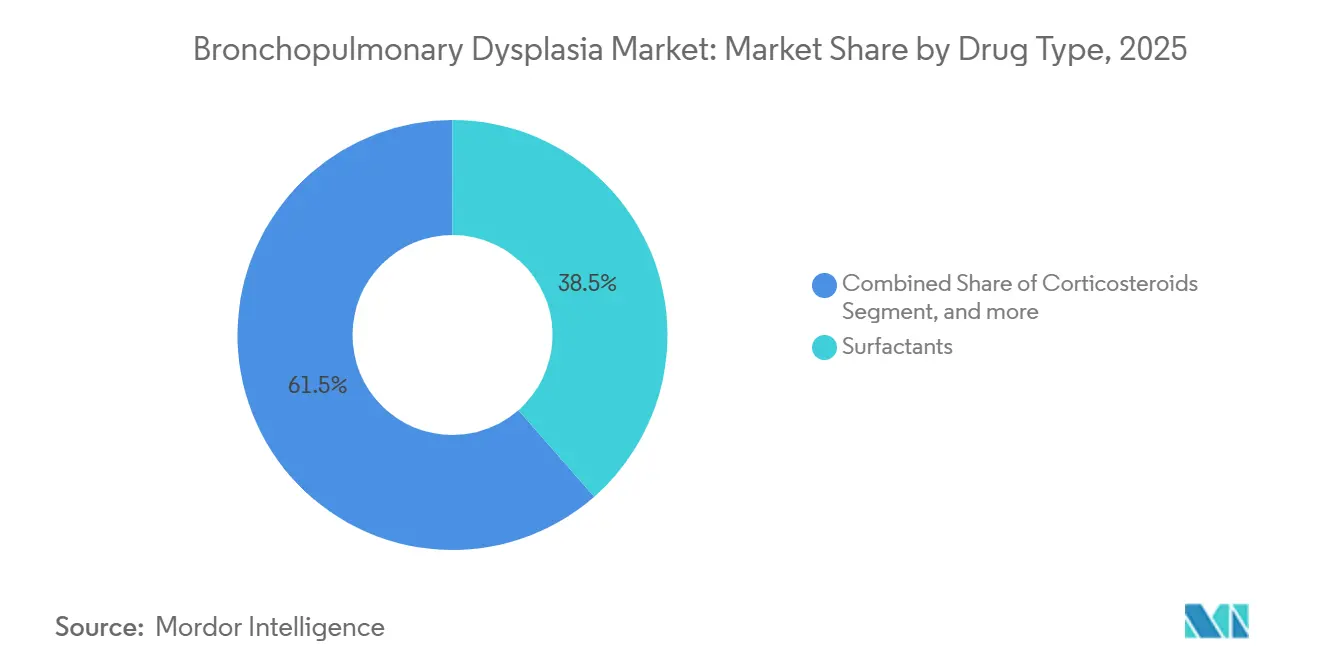

- By drug type, surfactants led with 38.54% of the bronchopulmonary dysplasia market share in 2025, while antibiotics and antivirals are forecast to expand at a 9.54% CAGR through 2031.

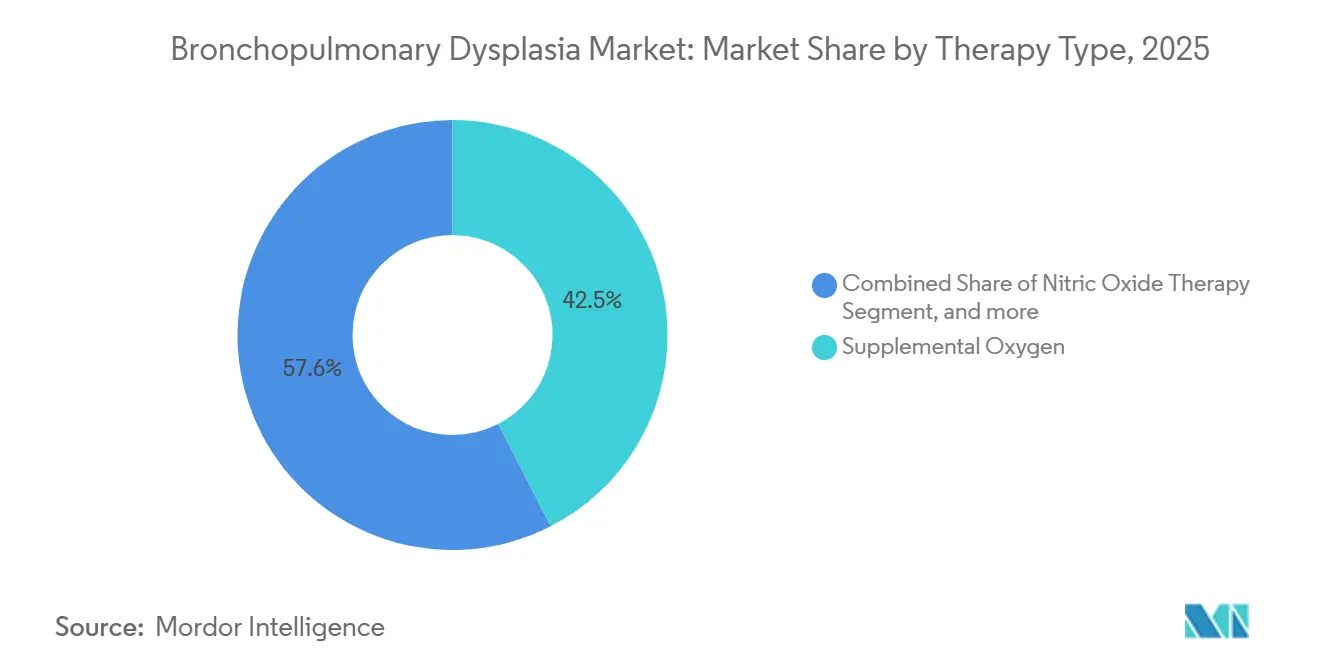

- By therapy type, supplemental oxygen accounted for 42.45% of the bronchopulmonary dysplasia market size in 2025 and stem-cell therapy is advancing at a 9.77% CAGR to 2031.

- By end-user, hospitals captured 66.43% revenue in 2025; critical-care centers record the fastest projected CAGR at 10.23% to 2031.

- By geography, North America controlled 43.54% revenue in 2025, whereas Asia-Pacific is projected to grow at an 8.54% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Bronchopulmonary Dysplasia Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising preterm birth incidence worldwide | +1.8% | South Asia, Sub-Saharan Africa, global | Medium term (2-4 years) |

| Improving neonatal survival rates | +1.5% | North America, Europe, urban Asia-Pacific | Long term (≥4 years) |

| Technological advances in respiratory support | +1.3% | North America, Europe, Japan, South Korea | Short term (≤2 years) |

| Expansion of research pipelines | +1.0% | North America, Europe | Long term (≥4 years) |

| Emergence of regenerative therapies | +0.9% | North America, Europe, select Asia-Pacific markets | Long term (≥4 years) |

| Predictive analytics in NICUs | +0.7% | North America, Western Europe, Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Preterm Birth Incidence Worldwide

Global preterm deliveries climbed to 13.4 million in 2024, equal to 10.6% of live births, fueled by rising maternal age, obesity, and medically indicated early deliveries. Infants born at 24–28 weeks now form 1.2% of all U.S. births and experience a 40%–60% BPD incidence, directly enlarging the Bronchopulmonary dysplasia market. In South Asia, only 22% of facilities currently stock surfactant, yet national procurement programs launched in 2024 are closing that gap and will unlock significant latent demand[1]UNICEF, “South Asia Newborn Care Strategy,” unicef.org.

Improving Neonatal Survival Rates Due to Intensive Care Availability

Survival to discharge for 25-week infants rose from 67% in 2019 to 74% in 2024 across U.S. Level III NICUs following standardized use of antenatal corticosteroids and early surfactant replacement. Longer survival, however, increases the pool of infants requiring prolonged ventilation, lifting utilization of supplemental oxygen, antibiotics, and nitric oxide. China added 1,200 NICU beds in 2024, bringing capacity to 8.5 beds per 1,000 live births, yet limited access to high-frequency ventilation persists, signaling ongoing equipment opportunity[2]National Health Commission of China, “Annual Health Statistics 2025,” nhc.gov.cn.

Technological Advancements in Neonatal Respiratory Support Systems

Non-invasive ventilation modalities now initiate 62% of respiratory support in U.S. NICUs, down from 48% in 2020, reducing intubation-related lung injury. Philips’ Oxy-CRG, cleared by FDA in 2025, cut hyperoxia episodes by 41% in trial settings and correlated with lower BPD incidence, underlining how precision gas management directly benefits the Bronchopulmonary dysplasia market. Drägerwerk’s Babylog VN800 predicts extubation readiness 24 hours ahead with 83% accuracy, shortening ventilation days by 18%.

Expansion of Research Pipelines Targeting Neonatal Lung Injury

Thirty-two investigational agents entered BPD development between 2024 and 2025, buoyed by FDA guidance endorsing surrogate endpoints such as oxygen dependence at 36 weeks. Airway Therapeutics’ AT-100 began a Phase 2b European trial in 2025, while Therabron Therapeutics’ TRB-N01 concluded Phase 1 dosing, evidencing stronger pharmaceutical commitment to the Bronchopulmonary dysplasia market.

Restraints Impact Analysis*

| Restraint | (~) (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of neonatal intensive care | −1.4% | Global, acute in middle-income countries | Medium term (2-4 years) |

| Inadequate neonatal care infrastructure | −1.1% | Sub-Saharan Africa, South Asia, rural Latin America | Long term (≥4 years) |

| Absence of approved disease-modifying drugs | −0.8% | Global | Long term (≥4 years) |

| Safety concerns around regenerative therapy | −0.5% | North America, Europe, Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Neonatal Intensive Care and Specialized Equipment

The average direct medical cost for a single U.S. BPD case requiring 90 NICU days is USD 320,000, with 40% tied to respiratory equipment and drugs[3]Health Affairs, “Economic Burden of Neonatal Care 2025,” healthaffairs.org. Budget limits delay ventilator upgrades in India, where typical units date from 2015, lacking lung-protective modes that could lower BPD incidence.

Inadequate Neonatal Care Infrastructure in Low-Income Regions

Sub-Saharan Africa holds only 0.8 NICU beds per 1,000 births, and fewer than 15% of facilities stock surfactant, curbing uptake of standard BPD preventive therapy. Generator failures caused ventilator outages exceeding four hours in 42% of Nigerian NICUs during 2024, contributing to neonatal mortality and highlighting infrastructure risk.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Type: Surfactants Hold Leadership While Anti-Infectives Surge

Surfactants commanded 38.54% of the 2025 bronchopulmonary dysplasia market share, driven by the adoption of Curosurf and Survanta. Hospitals now negotiate volume-based rebates, trimming net surfactant prices 12%–18% and pressuring margins. Antibiotics and antivirals are expected to grow at a 9.54% CAGR, as late-onset sepsis complicates 28% of prolonged ventilation cases, supporting double-digit growth in the Bronchopulmonary dysplasia market.

Bundled protocols pairing surfactant, caffeine citrate, and vitamin A curb BPD incidence by an extra 14% versus surfactant alone, stimulating cross-category revenue. The lack of head-to-head trials comparing animal-derived and synthetic surfactants limits payers' willingness to reimburse premium synthetic formulations until comparative effectiveness data become available.

By Therapy Type: Oxygen Remains Foundational, Regenerative Medicine Accelerates

Supplemental oxygen accounted for 42.45% of revenue in 2025; 18% of affected infants require home oxygen 6–24 months post-discharge, ensuring recurring cash flows for concentrator rentals and monitoring equipment. Price competition from Asian manufacturers compresses device margins, yet the rising survival of micro-preemies keeps volume growing in the bronchopulmonary dysplasia market.

Stem-cell therapy expands fastest at a 9.77% CAGR. PNEUMOSTEM’s interim Phase 2 success and USD 95 million of 2025 venture inflows position regenerative medicine to capture 8%–12% expenditure by 2030 if pivotal trials confirm durability and safety. Nitric oxide retains a niche, but Beyond Air’s portable generator cuts per-patient costs by 35% and is expanding access at community sites.

By End-User: Hospitals Dominate While Critical-Care Centers Gain Ground

Hospitals held 66.43% of 2025 revenue because BPD is diagnosed during the 78-day initial birth hospitalization for 26-week infants. Group purchasing agreements reduce equipment list prices by up to 30% but guarantee volume for suppliers. Critical-care centers will grow at a 10.23% CAGR as payers shift chronic BPD management to long-term ventilation facilities with per-diem costs 60% below those of acute NICUs, expanding the bronchopulmonary dysplasia market.

Pediatric skilled-nursing facilities are unevenly distributed; 22 U.S. states still lack specialized units, forcing interstate transfers and prolonging hospitalization. Integrated care networks, such as the Children’s Hospital of Philadelphia’s BPD center, lowered total costs by 28% and readmissions by 34% in 2024, demonstrating the value of end-to-end models.

Geography Analysis

North America retained 43.54% revenue in 2025 on the back of 1,100 Level III/IV NICUs and full reimbursement for USD 200,000–500,000 per-case costs. The FDA Breakthrough Therapy designation for two investigational drugs in 2025 drew USD 140 million of new capital to the bronchopulmonary dysplasia market. Physician shortages in Canada and uneven surfactant availability in Mexico underscore intra-regional variability.

Asia-Pacific will grow at an 8.54% CAGR through 2031, propelled by preterm volumes over 6 million in China and India and aggressive NICU expansion plans. Yet reimbursement ceilings well below true NICU cost in India and gaps in high-frequency ventilation in China reveal lingering access barriers. Japan and South Korea achieve sub-18% BPD incidence in very-low-birth-weight infants through strict protocols, illustrating attainable outcomes under constrained budgets.

Western Europe shows low single-digit growth as births decline, but technology adoption is rapid: 42% of NICUs deployed AI decision-support tools by 2025, and Germany set an EUR 8,500 reimbursement for integrated oxygen-titration monitoring. Sub-Saharan Africa houses 68% of global preterm births but only 14% of facilities stock surfactant, sharply limiting the bronchopulmonary dysplasia market despite high clinical need. Brazil and Argentina added NICU beds in 2024, yet 22% import tariffs and currency volatility prolong equipment payback periods.

Competitive Landscape

The bronchopulmonary dysplasia market is moderately fragmented: no company holds more than 12% share, and competition spans pharmaceuticals, devices, and emerging biologics. Chiesi Farmaceutici and AbbVie hold surfactant leadership but conceded 12%–18% net price owing to group purchasing negotiations in 2024. Medtronic, Philips, and Drägerwerk differentiate device portfolios through AI analytics and multiyear service bundling; Medtronic’s Neonatal Ventilation Insights cut extubation time by 2.3 days and secured 18 U.S. system contracts within six months of launch.

White-space sits in disease-modifying therapy and precision diagnostics. Airway Therapeutics’ AT-100 secured EMA Pediatric Investigation Plan approval in 2025, targeting European launch by 2028, while Medipost’s PNEUMOSTEM posted a 38% reduction in death or severe BPD and is scouting licensing partners. Proprietary data formats hinder cross-vendor interoperability, raising hospital switching costs and inching the bronchopulmonary dysplasia market toward ecosystem battles rather than stand-alone product skirmishes.

Bronchopulmonary Dysplasia Industry Leaders

Chiesi Farmaceutici S.p.A.

AbbVie

Medtronic

Fisher & Paykel Healthcare

GSK plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: UCLA researchers discovered a molecular switch that regulates blood vessel growth in preterm infants' lungs. Failure of this switch to promote regeneration can lead to bronchopulmonary dysplasia (BPD), a severe lung disease. This breakthrough may pave the way for new treatments to prevent or manage BPD in premature babies.

- August 2025: Airway Therapeutics, Inc., a clinical-stage biopharmaceutical company developing novel biologic therapies for respiratory, inflammatory, and infectious diseases announced that the European Medicines Agency (EMA) Pediatric Committee (PDCO) has approved its Pediatric Investigation Plan (PIP) for its investigational biologic, zelpultide alfa, in its initial indication for the prevention of bronchopulmonary dysplasia (BPD) in very preterm infants born between 22 and 27 weeks gestational age.

- November 2024: Oak Hill Bio, a clinical-stage neonatology and rare disease therapeutics company, and Chiesi, an international, research-focused biopharmaceutical company (Chiesi Group), announced that the first European patient has been enrolled in a Phase 2b clinical study, restarted in May, to assess the efficacy and safety of OHB-607, an investigational drug candidate being developed to prevent complications of extremely premature birth, including bronchopulmonary dysplasia (BPD), a serious condition for which there are no approved therapies.

Global Bronchopulmonary Dysplasia Market Report Scope

As per the scope of the report, bronchopulmonary dysplasia (BPD) is a chronic lung disorder primarily affecting premature infants who have received oxygen therapy and mechanical ventilation. It involves abnormal development of lung tissue, leading to inflammation and scarring. BPD can result in long-term breathing problems and respiratory issues in affected infants.

The Bronchopulmonary Dysplasia Market is Segmented by Drug Type (Corticosteroids, Diuretics, Bronchodilators, Surfactants, Antibiotics/Antivirals, and Other Supportive Drugs), Therapy Type (Nitric Oxide Therapy, Protein Replacement Therapy, Stem-Cell Therapy, and Supplemental Oxygen), End-User (Hospitals, Nursing Homes, and Critical-Care Centers), and Geography (North America, Europe, Asia-Pacific, MEA, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Corticosteroids |

| Diuretics |

| Bronchodilators |

| Surfactants |

| Antibiotics/Antivirals |

| Other Supportive Drugs |

| Nitric Oxide Therapy |

| Protein Replacement Therapy |

| Stem-Cell Therapy |

| Supplemental Oxygen |

| Hospitals |

| Nursing Homes |

| Critical-Care Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest Of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest Of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest Of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest Of South America |

| By Drug Type | Corticosteroids | |

| Diuretics | ||

| Bronchodilators | ||

| Surfactants | ||

| Antibiotics/Antivirals | ||

| Other Supportive Drugs | ||

| By Therapy Type | Nitric Oxide Therapy | |

| Protein Replacement Therapy | ||

| Stem-Cell Therapy | ||

| Supplemental Oxygen | ||

| By End-User | Hospitals | |

| Nursing Homes | ||

| Critical-Care Centers | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest Of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest Of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest Of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest Of South America | ||

Key Questions Answered in the Report

How large is the Bronchopulmonary Dysplasia market in 2026?

The Bronchopulmonary Dysplasia market size is USD 535.55 million in 2026.

How large is the Bronchopulmonary Dysplasia market in 2026?

The market is forecast to expand at a 7.34% CAGR, reaching USD 763.14 million by 2031.

Which therapy type is growing fastest?

Stem-cell therapy posts the highest CAGR at 9.77% through 2031 driven by positive Phase 2 data.

Why do surfactants dominate drug sales?

Surfactants remain first-line therapy and commanded 38.54% market share in 2025 due to universal use in very preterm infants.

Which region offers the most rapid growth opportunity?

Asia-Pacific will grow at an 8.54% CAGR owing to large preterm birth volumes and accelerating NICU expansion.

Who are the leading device suppliers?

Medtronic, Philips, and Drägerwerk lead in ventilators and monitoring systems, each leveraging AI-enabled platforms for differentiation.

Page last updated on: