Breast Tissue Markers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

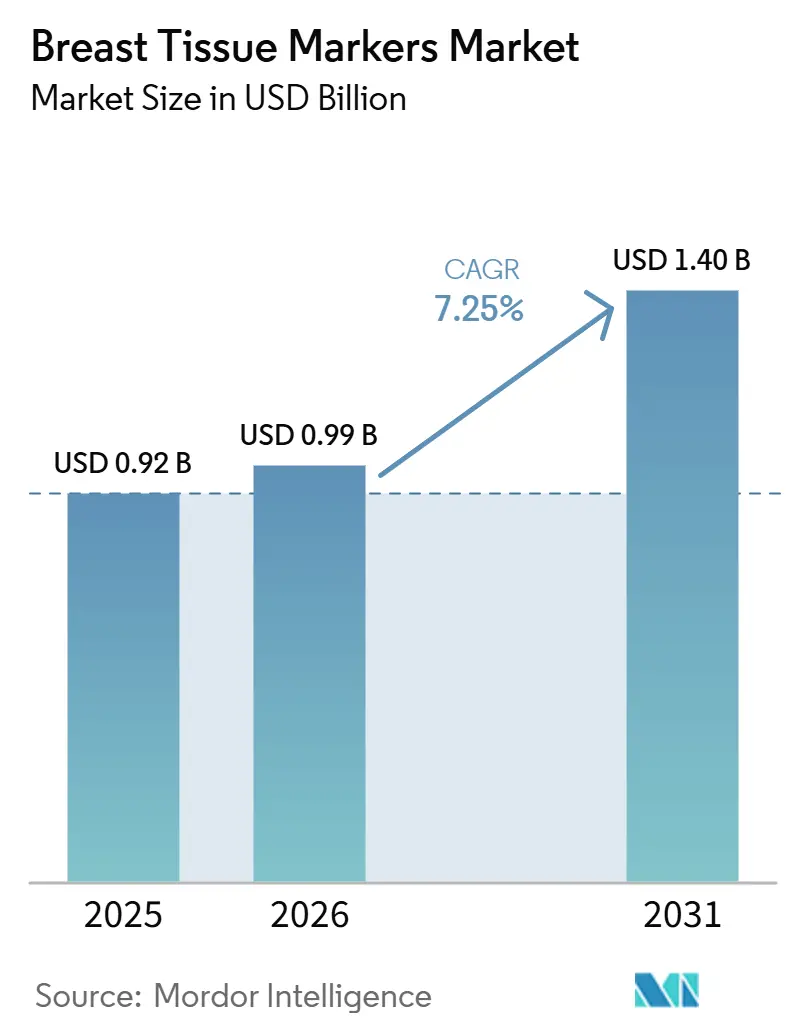

| Market Size (2026) | USD 0.99 Billion |

| Market Size (2031) | USD 1.40 Billion |

| Growth Rate (2026 - 2031) | 7.25% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Breast Tissue Markers Market Analysis by Mordor Intelligence

The Breast Tissue Markers Market size is expected to grow from USD 0.92 billion in 2025 to USD 0.99 billion in 2026 and is forecast to reach USD 1.40 billion by 2031 at 7.25% CAGR over 2026-2031.

The breast tissue markers market is advancing due to the steady rise in breast cancer diagnoses and biopsy procedures, which continues to support marker placement in routine care. In the United States, 321,910 women are expected to be diagnosed with invasive breast cancer in 2026, and another 60,730 are expected to be diagnosed with ductal carcinoma in situ, supporting demand for lesion localization and follow-up planning. Globally, the WHO recorded 2.4 million new breast cancer diagnoses in 2024, reinforcing the market’s demand base across screening, biopsy, therapy planning, and surgery. The market is also benefiting from the shift toward image-guided and wire-free care pathways, while outpatient procedure migration, demand for bioabsorbable formats, bundled product competition, migration risk, price sensitivity, and regulatory scrutiny continue to shape adoption.

Key Report Takeaways

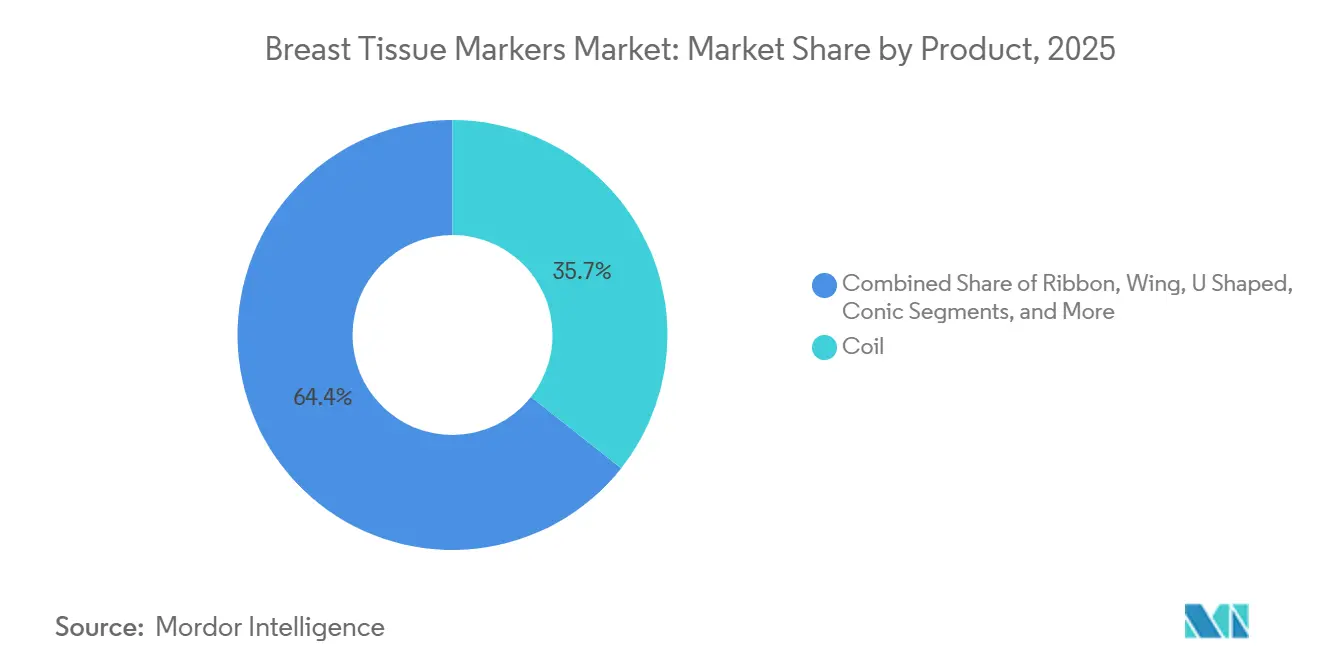

- By product, coil held 35.65% of revenue in 2025, while heart-shaped markers are projected to expand at 8.93% CAGR through 2031.

- By material, bio-absorbable markers accounted for 65.23% of revenue in 2025, and the same segment is forecast to record the fastest growth at 9.67% CAGR through 2031.

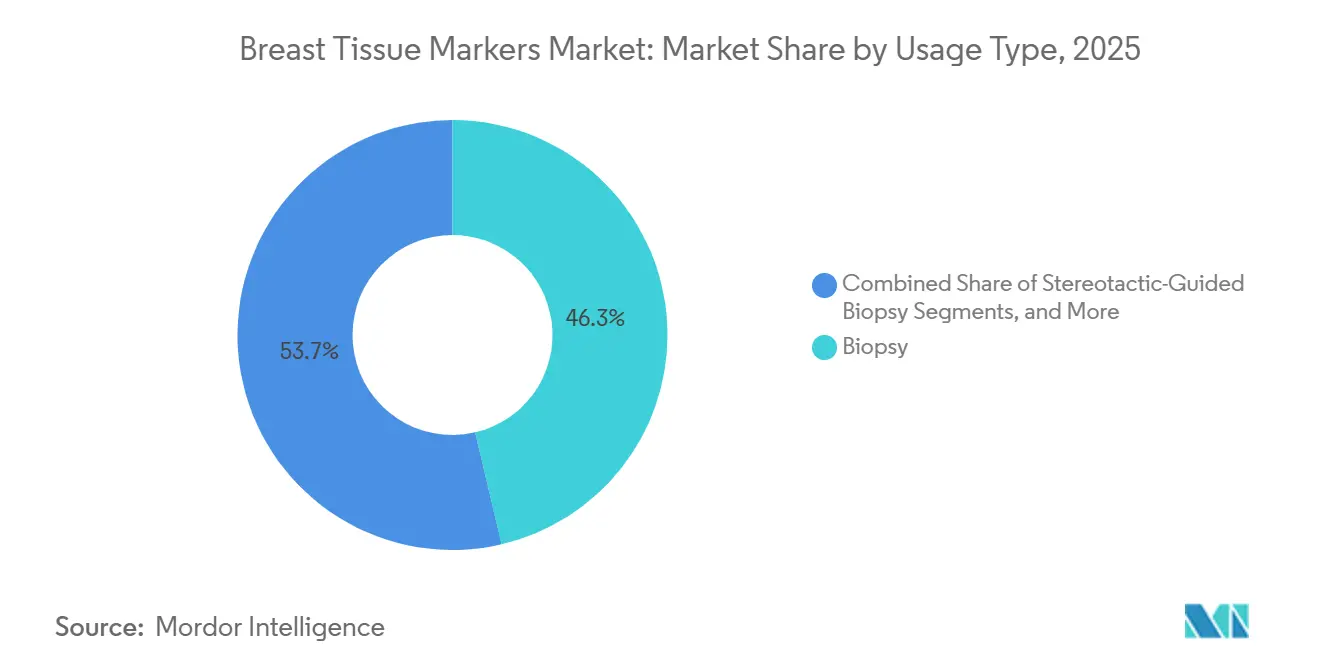

- By usage type, biopsy captured 46.34% of revenue in 2025, while surgical planning is projected to grow at 8.35% CAGR through 2031.

- By end user, hospitals represented 62.88% of revenue in 2025, while ambulatory surgical centers are projected to grow at 9.78% CAGR through 2031.

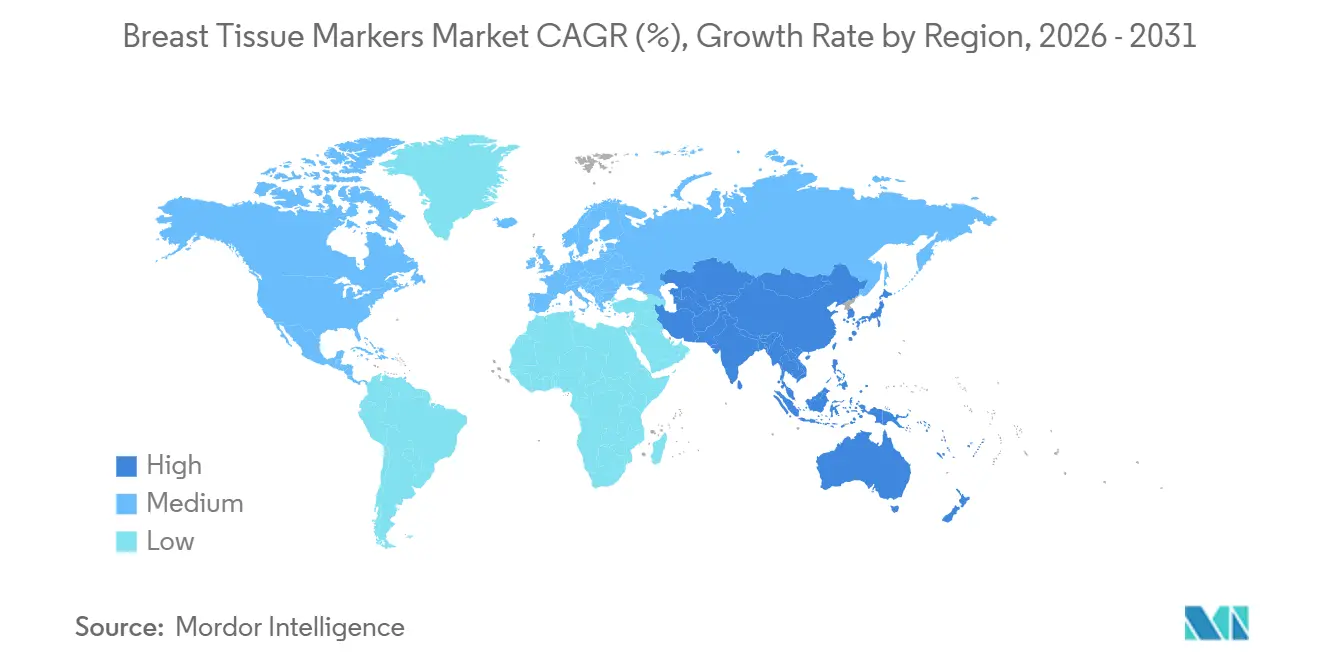

- By geography, North America held 38.56% of the global breast tissue markers market share in 2025, while Asia-Pacific is forecast to grow at 8.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Breast Tissue Markers Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising breast cancer screening and biopsy volumes | +2.0% | Global | Short term (≤ 2 years) |

| Shift toward non-wire, image-guided localization | +1.5% | North America & EU | Medium term (2-4 years) |

| Demand for MRI-visible and multi-modality compatibility | +1.2% | Global | Medium term (2-4 years) |

| Expansion of ambulatory and same-day breast procedures | +0.8% | North America, with early gains in EU and Australia | Short term (≤ 2 years) |

| Advancement in biodegradable and bioabsorbable materials | +0.7% | Global, with APAC gaining rapidly | Long term (≥ 4 years) |

| Improved clinical workflow and surgical planning | +0.5% | North America & EU, spill-over to APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Breast Cancer Screening and Biopsy Volumes Drive Structural Demand

The breast tissue markers market remains closely linked to the screening pathway, as abnormal findings that proceed to biopsy often require markers for future localization and imaging follow-up. Each additional screening mammogram creates a measurable probability of abnormal findings moving to biopsy, and many benign biopsies still require accurate site marking for downstream care. A nationwide AI-assisted screening study published in Nature Medicine in 2025 reported a breast cancer detection rate of 6.7 per 1,000 women in the AI-supported cohort and a biopsy positive predictive value of 64.5%, indicating that improved screening tools strengthened case quality rather than reduced marker placement needs.[1]Breastcancer.org, “Breast Cancer Facts and Statistics,” Breastcancer.org, breastcancer.org With the WHO reporting 2.4 million new breast cancer diagnoses globally in 2024, the breast tissue markers market continues to benefit from a broad clinical pipeline that is unlikely to weaken in the near term.[2]World Health Organization, “Breast Cancer,” WHO Fact Sheet, who.int

Shift toward Non-Wire, Image-Guided Localization Opens Adjacent Procedure Volume

The breast tissue markers market is expanding beyond basic clip placement, as wire-free and image-guided localization systems support both biopsy follow-up and surgical navigation. Clinicians have long used wire-guided localization for non-palpable breast lesions, but wireless systems eliminate same-day wire placement constraints and reduce dependence on operating room scheduling. In a French cancer center study covering the first 200 procedures, the Sirius Pintuition system achieved successful primary lesion excision and marker retrieval in all cases, while the re-excision rate required to achieve margin clearance was 9%. In February 2025, Mammotome and Sirius Medical entered an exclusive distribution agreement covering the United States and Germany, giving the system broader commercial access through an established breast care sales network.

Demand for MRI-Visible and Multi-Modality Compatibility Reshapes Product Design

The breast tissue markers market is shifting toward products that remain visible across multiple imaging modalities without creating excessive artifacts. A 2026 study available through PubMed Central evaluated five commercial markers and found artifact diameters ranging from 2.7 mm to 12.0 mm, with HydroMark and TriMark showing the smallest distortion among the tested devices.[3]Sarah E. Tomlinson-Hansen, “Breast Cancer Screening in the Average-Risk Patient,” StatPearls, ncbi.nlm.nih.gov In March 2026, Mammotome secured FDA clearance for HydroMARK Plus MR biopsy site markers and its in-room MR vacuum-assisted biopsy system, with the marker designed for visibility under T1 and T2 MRI sequences and ultrasound visibility for up to 12 months. In December 2025, VizMark received FDA 510(k) clearance for VM1, a non-metal marker intended to provide artifact-free visibility across MRI, mammography, X-ray, CT, and ultrasound, reflecting the market shift toward broader modality compatibility.

Expansion of Ambulatory and Same-Day Breast Procedures Reconfigures End-User Economics

The movement of lower-complexity procedures into ambulatory care settings is reshaping the breast tissue markers market. Same-day breast biopsy and marker placement align well with outpatient facilities because they reduce facility costs and shorten scheduling cycles for patients who do not require inpatient monitoring. A January 2026 meta-analysis covering 2,117 patients and 2,176 Magseed placements reported 99.3% placement accuracy within 10 mm of the target lesion and a 99.6% intraoperative retrieval rate, supporting efficient marker workflows in day-care environments.[4]N. Eisemann et al., “Nationwide Real-World Implementation of AI for Cancer Detection in Mammography Screening,” Nature Medicine, nature.com As more routine cases move outward, the breast tissue markers market is likely to split more clearly between high-volume outpatient demand and hospital-based demand associated with MRI-guided or otherwise complex procedures.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Marker migration and localization accuracy concerns | -1.2% | Global | Short term (≤ 2 years) |

| Reimbursement and coverage gaps for advanced markers | -0.9% | EU, Middle East & Africa, South America | Medium term (2-4 years) |

| Material compliance and sterilization complexity | -0.5% | EU, with spill-over to APAC | Medium term (2-4 years) |

| Limited training and clinical familiarity in emerging markets | -0.7% | APAC, MEA, South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Marker Migration and Localization Accuracy Concerns Persist Despite Advances

The breast tissue markers market continues to face a key clinical challenge, as marker displacement can affect localization accuracy between biopsy and surgery. This risk is more pronounced when the biopsy cavity changes shape, fills with fluid, or shrinks after systemic therapy, as these conditions can shift the marker position. A 2026 PubMed Central study found that the Scout radar reflector produced off-target temperature measurement artifacts ranging from -30°C to +100°C in nearby MRI voxels, while the French Sirius Pintuition study reported marker dislodgement during surgery in 17 of 200 cases, although surgeons successfully excised the primary lesion in all cases. As a result, the market continues to favor designs that improve tissue grip and reduce displacement during excision.

Reimbursement and Coverage Gaps Slow Adoption of Advanced Marker Formats

Reimbursement continues to influence the large-scale adoption of premium products in the breast tissue markers market, beyond clinical performance alone. Bio-absorbable and wireless systems often have higher per-procedure costs than standard metallic clips, which can limit procurement in price-sensitive health systems without direct payment support. In January 2026, France added the Magseed marker to its SE08 hospital reimbursement package at EUR 390.16 per placement, removing a clear financial barrier in that market. However, limited availability of similar frameworks across regions continues to slow adoption where hospitals must absorb the additional cost of advanced marker formats.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Coil Leads by Volume, Heart Geometry Captures Fastest Growth

Coil markers accounted for 35.65% of product revenue in 2025, making them the largest product format in the breast tissue markers market. Their leadership reflected established use with vacuum-assisted biopsy systems and strong clinical familiarity among radiologists interpreting mammography and MRI after placement. Coil formats also supported routine workflows because many breast imaging centers already used common delivery devices for deployment.

Heart-shaped markers are forecast to grow at a CAGR of 8.93% through 2031, making them the fastest-growing product category in the breast tissue markers market. Their adoption is supported by stronger tissue adherence in cases where cavity shape changes may increase displacement risk. Mammotome expanded access to HydroMARK Plus shapes in 2026, including Dragonfly and Hummingbird options with exposed wing structures that engage tissue after hydrogel hydration. Ribbon, wing, U-shaped, ring, conic, and Venus designs remain relevant in specific use cases, while product selection increasingly depends on imaging performance and surgical handling.

By Material: Bio-absorbable Markers Dominate Across Both Share and Growth

Bio-absorbable markers held 65.23% of the breast tissue markers market size within the material segment in 2025, making them the clear revenue leader. Their strong position reflected rising preference for products that reduce retained foreign-body load during long follow-up periods after treatment. This factor became more important as surveillance imaging increased and treatment pathways increasingly included systemic therapy before surgery.

The same segment is projected to expand at a CAGR of 9.67% through 2031, placing bio-absorbable products at the forefront of material growth in the breast tissue markers market. Carbon Medical Technologies received EU MDR certification for its BiomarC Tissue Marker System in April 2025, supporting European access for a non-metallic marker line designed for visibility under ultrasound, mammography, CT, and MRI. A 2025 US patent application describing a drug-refillable biodegradable tissue marker architecture indicated that the material category was moving toward broader functionality beyond site marking.

By Usage Type: Biopsy Anchors Volume, Surgical Planning Sees Fastest Expansion

Biopsy represented 46.34% of revenue in 2025, making it the largest usage type in the breast tissue markers market. This position reflected the high volume of core-needle and vacuum-assisted procedures in which clinicians placed a marker at sampling for future imaging correlation. The segment also covered stereotactic, ultrasound-guided, and MRI-guided biopsies, each requiring different visibility features and device compatibility.

Surgical planning is forecast to grow at a CAGR of 8.35% through 2031, showing expansion into workflows that continue after the initial biopsy. In March 2026, Mammotome received FDA clearance for the Prima MR Dual Vacuum-Assisted Breast Biopsy System, which supports in-room MR biopsy and marker deployment while reducing repositioning between steps. In May 2025, Elucent Medical received FDA Breakthrough Device Designation for EnVisio X1, a platform using a SmartClip tissue marker with real-time 3D surgical guidance. In March 2026, Cairn Surgical submitted a De Novo 510(k) application for its Breast Cancer Locator System after reporting negative margins in 94% of patients in its pivotal trial, indicating a broader shift toward patient-specific spatial guidance during excision.

By End User: Hospitals Command Volume While ASCs Drive the Growth Rate

Hospitals captured 62.88% of end-user revenue in 2025, giving them the largest share of the breast tissue markers market. Their lead came from access to MRI-guided biopsy suites, advanced stereotactic systems, and multidisciplinary oncology teams managing complex breast procedures. Hospitals also used a wider mix of premium marker types because patients receiving neoadjuvant therapy or advanced imaging often required longer-dwell and multi-modality visibility.

Ambulatory surgical centers are projected to expand at a CAGR of 9.78% through 2031, making them the fastest-growing end-user setting in the breast tissue markers market. This shift reflects lower overhead, smoother scheduling, and stronger alignment with same-day procedures that do not require inpatient care. Specialty clinics remain the smallest end-user group, but they often act as early adopters of newer wire-free localization platforms before broader hospital contracting follows.

Geography Analysis

North America accounted for 38.56% of global revenue in 2025, making it the largest regional bloc in the breast tissue markers market. High screening penetration, extensive breast imaging infrastructure, and reimbursement systems that support marker placement within routine biopsy workflows strengthen regional demand. The United States remains the core revenue base, supported by large case volumes, with 321,910 invasive breast cancer diagnoses and 60,730 ductal carcinoma in situ diagnoses expected in 2026. Mammotome also continues to expand HydroMARK Plus access across North American pathways following its 2026 regulatory clearances.

Europe remains a key contributor to the breast tissue markers market, supported by organized screening programs in Germany, France, the United Kingdom, and Italy that sustain biopsy referral volumes. Reimbursement and regulatory frameworks play a strong role in product adoption across the region. In France, the inclusion of Magseed in the SE08 reimbursement package at EUR 390.16 per placement in January 2026 reduced the cost barrier for wireless localization in hospital practice. EU MDR compliance standards also favor companies with stronger clinical evidence and established post-market systems, increasing entry barriers for smaller suppliers.

Asia-Pacific is the fastest-growing region, with the breast tissue markers market size projected to expand at a CAGR of 8.56% through 2031. China represents the largest regional opportunity, as breast cancer incidence has surpassed 300,000 new cases annually, and national screening expansion continues to widen the downstream pool for biopsy and marker placement. Large urban centers are advancing image-guided localization, while underserved cities provide room for broader adoption as infrastructure improves. Japan and South Korea are well-positioned for multi-modality marker uptake, Australia benefits from established reimbursement pathways, and growth across Asia-Pacific, the Middle East, and Africa, and South America is supported by screening expansion, private hospital investment, and the shift toward image-guided breast care.

Competitive Landscape

The breast tissue markers market has a moderately consolidated top tier, with Mammotome, Becton, Dickinson and Company, and Hologic holding strong positions through portfolios that integrate markers with biopsy tools, imaging systems, and surgical workflows. This structure gives scaled players an advantage, as hospitals often prefer fewer suppliers that can support equipment, disposables, and training. The market also favors companies with an installed base in biopsy devices, as marker selection often follows existing procurement pathways rather than isolated product comparisons. As a result, access to radiology suites and breast centers remains as important as individual marker design.

Hologic strengthened its position in July 2024 when it completed its USD 310 million acquisition of Endomagnetics Ltd, adding Magseed, Magtrace, and Sentimag to its broader breast surgery portfolio. Mammotome followed a different strategy by using its vacuum-assisted biopsy platform to link marker placement directly with the biopsy workflow, and it strengthened this position through its March 2026 FDA clearances for an in-room MR biopsy system and HydroMARK Plus MR markers. The company also expanded its commercial reach in February 2025 through a Sirius Medical distribution agreement in the United States and Germany, improving its exposure to wireless localization pathways. BD remained competitive through its delivery-system depth and established procurement relationships in routine hospital and biopsy center purchasing.

Smaller challengers targeted gaps that larger platforms did not fully address. VizMark entered the market discussion in December 2025 with FDA clearance for VM1, a non-metal marker designed for artifact-free visibility across all major imaging modalities. Elucent Medical advanced a software-linked navigation model through EnVisio X1, while Cairn Surgical developed patient-specific excision guidance. These developments show that market leaders continue to benefit from scale and installed-base strength, while product differentiation increasingly comes from artifact control, tissue anchoring, and integration with surgical navigation.

Breast Tissue Markers Industry Leaders

Argon Medical Devices, Inc.

Becton, Dickinson and Company

Mammotome (Devicor Medical Products, LLC)

Mermaid Medical A/S

Hologic, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Mammotome received CE mark certification for the HydroMARK Plus Breast Biopsy Site Marker, expanding European access to its hydrogel-titanium marker technology with ultrasound, mammography, and MRI visibility.

- March 2026: Mammotome received FDA clearance for the Mammotome Prima MR Dual Vacuum-Assisted Breast Biopsy System and HydroMARK Plus Breast Biopsy Site Marker for MR use, enabling a single-session MRI biopsy-and-mark workflow.

- March 2026: Cairn Surgical submitted a De Novo 510(k) application to the FDA for its Breast Cancer Locator System, a patient-specific 3D-printed surgical guide based on supine MRI data, after reporting negative margins in 94% of patients in its pivotal trial.

- January 2026: The FDA cleared Mammotome’s HydroMARK Plus Breast Biopsy Site Marker, Dragonfly Shape, under 510(k) K253761 as a Class II special controls device under 21 CFR 878.4300, adding a wing-shaped configuration to support tissue adhesion and reduce displacement during excision.

Global Breast Tissue Markers Market Report Scope

As per the scope of the report, breast tissue markers are tiny, implantable objects (usually made of titanium, stainless steel, or bio-absorbable materials) placed inside the breast during a biopsy. They serve as permanent landmarks to accurately identify the biopsy site for future mammograms, ultrasounds, or targeted surgical removal.

The breast tissue markers market is segmented by product, material, usage type, end user, and geography. By product, the market includes coil, ribbon, wing, U-shaped, conic, ring, heart, Venus, and other product types. By material, the market is segmented into bioabsorbable and non-absorbable. By usage type, the market is categorized into biopsy, stereotactic-guided biopsy, ultrasound-guided biopsy, MRI-guided biopsy, surgical planning, and other usage types. By end user, the market is segmented into hospitals, ambulatory surgical centers, diagnostic centers, and specialty clinics. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Coil |

| Ribbon |

| Wing |

| U Shaped |

| Conic |

| Ring |

| Heart |

| Venus |

| Other Product Types |

| Bio-absorbable |

| Non-Absorbable |

| Biopsy |

| Stereotactic-Guided Biopsy |

| Ultrasound-Guided Biopsy |

| MRI-Guided Biopsy |

| Surgical Planning |

| Other Usage Types |

| Hospitals |

| Ambulatory Surgical Centers |

| Diagnostic Centers |

| Specialty Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Coil | |

| Ribbon | ||

| Wing | ||

| U Shaped | ||

| Conic | ||

| Ring | ||

| Heart | ||

| Venus | ||

| Other Product Types | ||

| By Material | Bio-absorbable | |

| Non-Absorbable | ||

| By Usage Type | Biopsy | |

| Stereotactic-Guided Biopsy | ||

| Ultrasound-Guided Biopsy | ||

| MRI-Guided Biopsy | ||

| Surgical Planning | ||

| Other Usage Types | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Diagnostic Centers | ||

| Specialty Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the breast tissue markers space?

The breast tissue markers market stands at USD 0.99 billion in 2026 and is projected to reach USD 1.40 billion by 2031, growing at a 7.25% CAGR.

Which product type leads revenue today?

Coil markers lead the product mix with a 35.65% revenue share in 2025 because they remain widely used across established biopsy workflows.

Which material category is growing the fastest?

Bio-absorbable markers are both the largest material segment at 65.23% in 2025 and the fastest-growing one at 9.67% CAGR through 2031.

Why are hospitals still the largest end-user setting?

Hospitals held 62.88% of revenue in 2025 because they manage MRI-guided biopsy, advanced imaging procedures, and more complex oncology pathways.

Which region is growing the fastest through 2031?

Asia-Pacific is the fastest-growing region at 8.56% CAGR, supported by screening expansion, rising case volume, and broader image-guided care adoption.

What is changing competition in this space most?

Competition is shifting toward multi-modality visibility, lower artifact profiles, bio-absorbable materials, and systems that connect biopsy markers with surgical navigation.

Page last updated on: