Breast Milk Substitutes Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

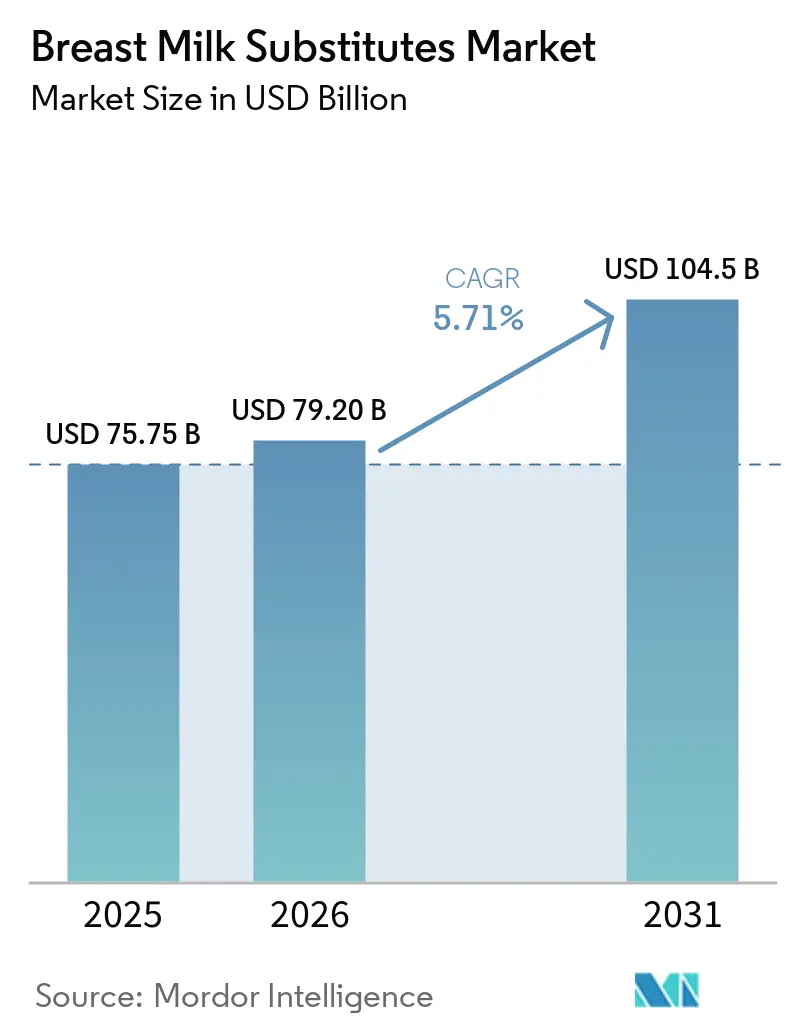

| Market Size (2026) | USD 79.20 Billion |

| Market Size (2031) | USD 104.5 Billion |

| Growth Rate (2026 - 2031) | 5.71% CAGR |

| Fastest Growing Market | Europe |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Breast Milk Substitutes Market Analysis by Mordor Intelligence

The Breast Milk Substitutes Market size is projected to expand from USD 75.75 billion in 2025 and USD 79.20 billion in 2026 to USD 104.5 billion by 2031, registering a CAGR of 5.71% between 2026 to 2031.

A shrinking global birth cohort is shifting competition from volume to value, compelling producers to load formulas with high-margin functional ingredients such as multi-human-milk-oligosaccharide (HMO) blends. Premiumization offsets demographic decline most visibly in China, where approvals for human-milk products accelerate innovation despite record-low fertility, and in Europe, where organic certification and contaminant rules drive up per-unit prices. Channel disruption is equally forceful: cross-border e-commerce platforms and livestreaming are eroding supermarkets' dominance while expanding consumer access to foreign-label premium goods. At the same time, policy reforms in the United States and China are loosening historic oligopolies, ushering in smaller entrants that rely on direct-to-consumer models, clean labels, and proprietary R&D pipelines.

Key Report Takeaways

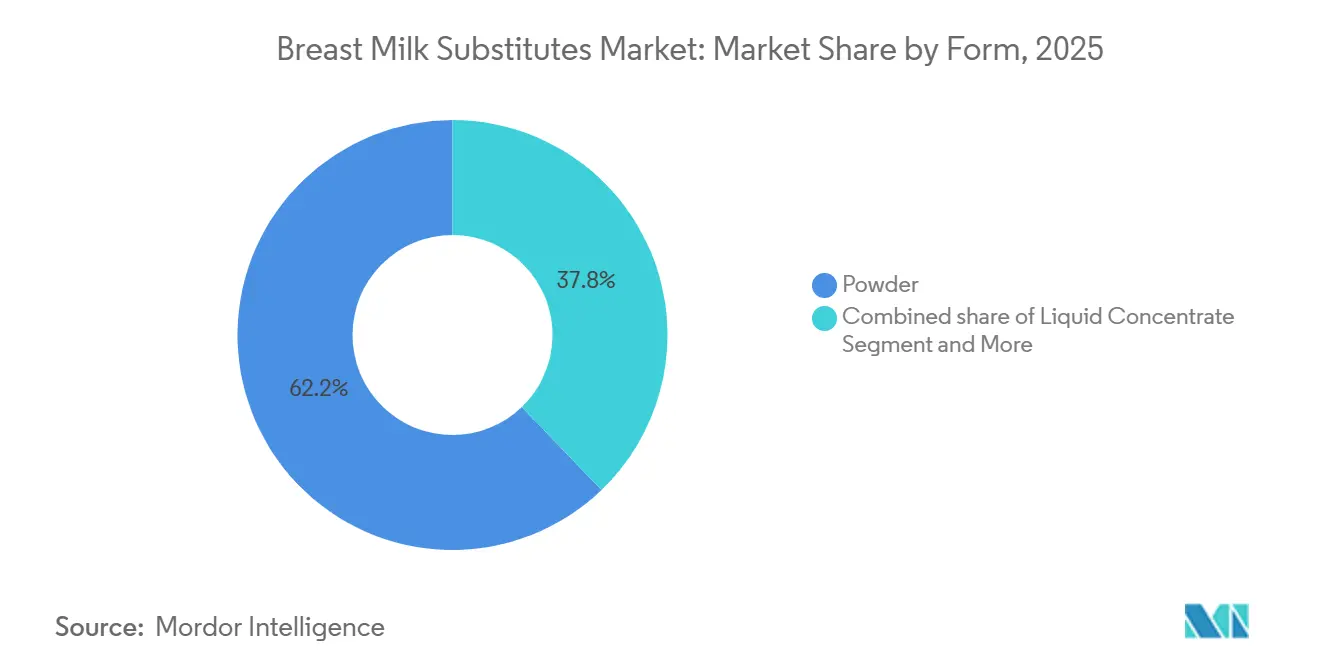

- By form, powder captured 62.18% of 2025 revenue, while liquid concentrate is forecast to expand at a 6.20% CAGR through 2031.

- By stage, Stage 1 formula held 47.18% share in 2025, whereas Stage 3 growing-up milk is projected to post a 5.93% CAGR to 2031.

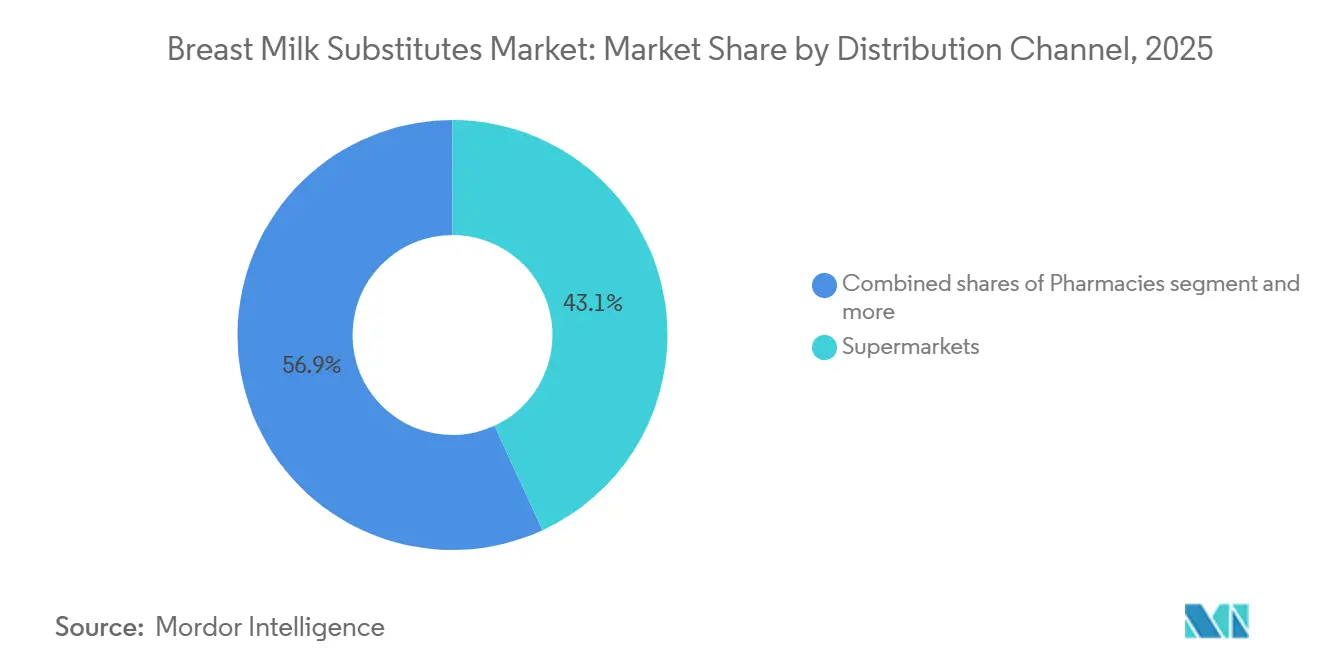

- By distribution channel, supermarkets and hypermarkets led with 43.12% contribution in 2025, yet online and e-commerce are advancing at a 6.35% CAGR.

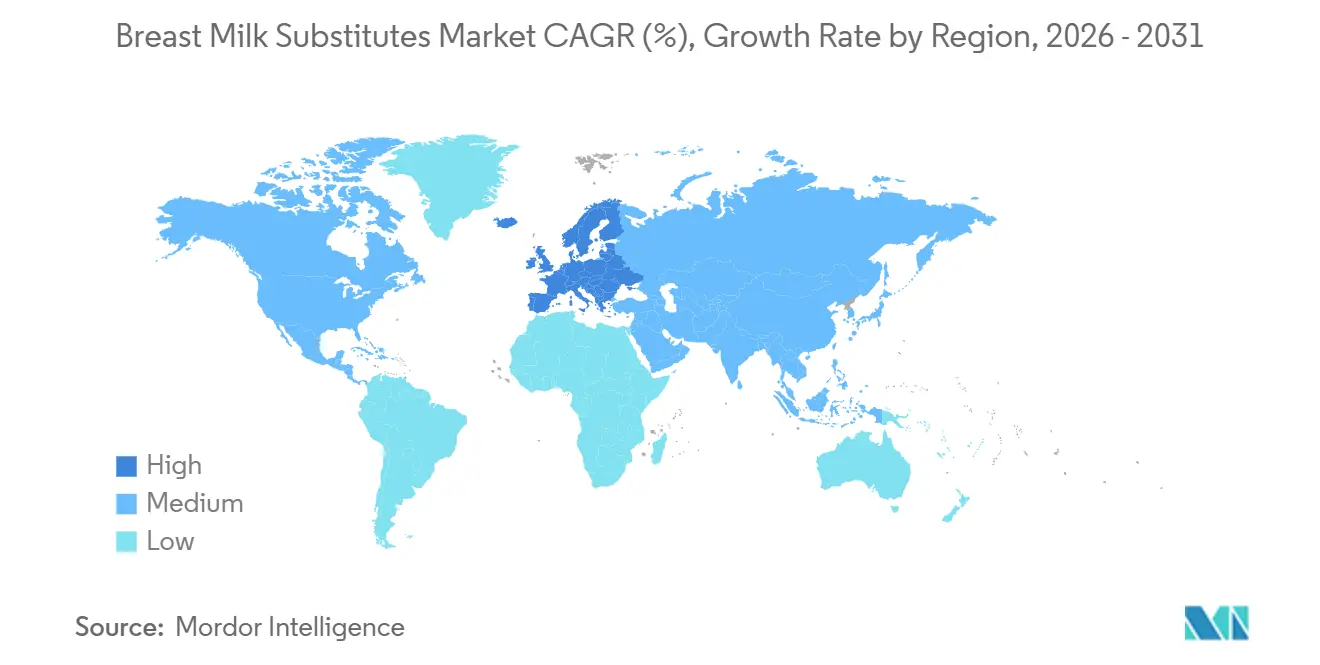

- By geography, Asia-Pacific accounted for 58.17% of market value in 2025, while Europe is on track to log the fastest 6.10% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Breast Milk Substitutes Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Female workforce participation and time-poor households | +1.2% | Global, highest in East and South Asia | Medium term (2-4 years) |

| Premiumization via HMOs, probiotics, and functional ingredients | +1.5% | North America, Europe, Asia-Pacific premium tiers | Long term (≥ 4 years) |

| E-commerce and cross-border platforms expand access | +0.9% | Asia-Pacific core, spill-over to Middle East & Africa | Short term (≤ 2 years) |

| Regulatory acceptance of goat-milk-based formula widens demand | +0.4% | North America, Europe, Australia | Medium term (2-4 years) |

| China HMO approvals and GB standards accelerate innovation | +0.8% | China, Hong Kong, Southeast Asia | Short term (≤ 2 years) |

| FDA post-2022 policies diversify U.S. supply and entrants | +0.5% | United States | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Female Workforce Participation and Time-Poor Households

Dual-income households are prioritizing convenience, lifting demand for ready-to-feed and liquid concentrates that erase mixing steps, even at a 30-40% price premium over powders. Time scarcity in Tier 1 Chinese cities, the absence of workplace lactation rooms, and parallel trends in India have elevated liquid formats from niche to mainstream. Brands such as Abbott’s USDA-certified Pure Bliss Organic target this cohort by pairing speed with signals of perceived quality. In emerging markets, premium Stage 2 and Stage 3 probiotic blends are outpacing overall category growth because they promise fewer nighttime disruptions.

Premiumization via HMOs, Probiotics, and Functional Ingredients

Following China’s 2026 clearance of 3'-sialyllactose, manufacturers are racing to launch five-plus-HMO recipes that command 40-50% premiums. Nestlé, Vinamilk, and FrieslandCampina now position multi-HMO lines as the closest mimic to human milk, while Danone links milk-fat-globule-membrane (MFGM) to long-term cognitive benefits. Suppliers able to secure regulatory green lights for novel oligosaccharides ahead of rivals gain both marketing clout and first-mover shelf space.

E-commerce and Cross-Border Platforms Expand Access

Tmall Global’s 38% share of China’s USD 540 billion cross-border e-commerce market enables foreign-label brands to bypass 12-month domestic registrations, pay lower taxes, and leverage livestreaming to convert shoppers in minutes. The A2 Milk Company used this loophole to lift English-label sales 17.2% in 2025, underscoring the channel’s strategic relevance. Regulators may tighten purchase caps, yet producers with private-domain ecosystems and in-house fulfillment will be best positioned to absorb any shock.

Regulatory Acceptance of Goat-Milk-Based Formula Widens Demand

FDA and Health Canada nods have propelled goat-milk formulas from specialty aisles to national chains, supported by digestibility claims that resonate with caregivers of mildly cow-milk-sensitive infants. Ability to piggyback on existing dairy herds in India and Australia lowers raw-milk costs, while a 20-30% shelf premium secures margins without the clinical burden of hypoallergenic labels.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining births in key markets reduce volume base | -1.8% | China, Japan, South Korea, Europe | Long term (≥ 4 years) |

| Stronger WHO Code implementation and digital marketing curbs | -0.6% | Southeast Asia, Latin America | Medium term (2-4 years) |

| EU deforestation/contaminant rules raise compliance costs | -0.4% | Europe, global supply chains | Short term (≤ 2 years) |

| Ingredient volatility and quality tightening | -0.3% | Global, premium tiers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Declining Births in Key Markets Reduce Volume Base

China’s 2025 birth rate of 5.63 per 1,000 and Europe’s 3.3% drop in births erode the baseline for formula demand. Manufacturers extend revenue windows by emphasizing Stage 3 and functional toddler drinks, but the structural gap left by shrinking cohorts cannot be fully offset by India or Africa, where per-capita spend remains low.

Stronger WHO Code Implementation and Digital Marketing Curbs

The 78th World Health Assembly’s 2025 resolution empowers governments to police online formula ads. Vietnam’s AI-driven VIVID system already monitors social posts for violations, and similar rollouts in Latin America are curbing digital customer acquisition[1]World Health Organization, “78th WHA Resolution on Digital Marketing,” who.int. Brands are reverting to pediatrician outreach and hospital partnerships that carry higher acquisition costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Convenience Fuels Liquids’ Momentum

Powder continues to capture the largest share of the breast milk substitutes market, accounting for 62.18% of the 2025 value due to its lower cost and long shelf life. Even so, liquid concentrate is projected to post a 6.20% CAGR, outstripping the overall breast milk substitutes market and reflecting the growing priority parents place on hassle-free night feeds. Ready-to-feed (RTF) lines from Abbott and Mead Johnson price at USD 2.00-plus per ounce yet move off shelves in North America’s urban hubs, where caregivers trade up for reliability.

In China and India, powder remains dominant because of ambient storage conditions, price sensitivity, and online bulk buying, which favor economical formats. Multinationals are therefore investing in aseptic packaging and extended shelf-life technology that could unlock liquids for these value-driven regions over the forecast horizon.

By Stage: Toddler Lines Lengthen Lifetime Value

Stage 1 accounted for 47.18% of 2025 revenue, but Stage 3 formulas are emerging as the fastest growth pocket, set to clock a 5.93% CAGR through 2031 YILI. The breast milk substitutes market for toddler nutrition is expanding because regulators in China and Southeast Asia now accept cognition and immunity claims that were once disallowed. Health-oriented parents perceive these products as essential rather than optional, thereby increasing their willingness to pay.

Stage 3 also benefits manufacturers by extending consumption to 36 months, effectively tripling revenue per child compared with 0-6-month formulas. Companies adept at aligning functional claims with local rulebooks will cement first-mover advantage in this segment of the breast milk substitutes market.

By Distribution Channel: Digital Funnels Reshape Reach

Supermarkets currently control 43.12% of global value, yet e-commerce is forecast to grow at 6.35% per year, the quickest pace among all channels. Cross-border stores on Tmall Global retain tax advantages and allow fast iteration of HMO-rich SKUs that have not yet cleared domestic labeling constraints.

Livestreaming, which generated USD 807 billion in GMV in China in 2024, blends product discovery with instant conversion. Brands that master private-domain traffic and subscription mechanics will de-risk future regulatory clampdowns while pulling repeat orders away from brick-and-mortar retail.

Geography Analysis

Asia-Pacific remains the revenue anchor, accounting for 58.17% of the 2025 global value, even as China’s record-low fertility rates impede volume expansion. Domestic champions such as Feihe deploy maternity-subsidy campaigns and multi-HMO pipelines to defend share against multinationals. India’s middle-class boom, coupled with Danone’s report that super-premium SKUs grow at twice the category rate, suggests the region will continue to set the global pace for premium adoption.

Europe, projected to log a 6.10% CAGR to 2031, profits from consumer trust in organic labels and new contaminant standards that tilt the playing field toward large players with robust compliance systems[2]Eurostat, “EU Births 2024,” ec.europa.eu/eurostat. The 2026 ARA-oil contamination recall knocked confidence in several mainstream brands, funneling demand to organic specialists that escaped the crisis.

North America regained supply stability once Abbott’s Sturgis plant reopened, pushing the company’s pediatric nutrition sales to USD 2.208 billion in 2024. Yet FDA reform now paves the way for smaller certified entrants, setting the stage for a long-term redistribution of shelf space. Latin America, the Middle East, and Africa remain smaller in absolute terms but offer surface-area growth opportunities as birth rates there remain comparatively high.

Competitive Landscape

Nestlé, Danone, Abbott, Reckitt/Mead Johnson, and Feihe collectively control the majority of global value. That concentration masks wide regional variation: China’s market is split among domestic names, while the United States only recently began diluting its long-standing oligopoly after Operation Stork Speed. Strategic battles cluster around three dimensions: (1) premium ingredient stacking validated by clinical endpoints, (2) vertical supply-chain integration that lowers compliance and ingredient risk, and (3) digital channel innovation that shortcuts legacy retail lock-ins.

Disruptors ByHeart and Bobbie emphasize clean labels (no corn syrup or palm oil) and own manufacturing sites to guarantee transparency. Incumbents are retaliating by licensing precision-fermented ingredients such as All G’s high-purity lactoferrin and accelerating their own direct-to-consumer pilots. Over the forecast horizon, the agility of brands in securing regulatory approvals for next-generation HMOs and other bioactives will be decisive in shaping share shifts across the breast milk substitutes market.

Breast Milk Substitutes Industry Leaders

Nestlé S.A.

Danone S.A.

Reckitt Benckiser

Abbott Laboratories

Feihe International, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: China’s SAMR approved 3'-sialyllactose, enabling five-plus-HMO formulations.

- January 2026: Princes Group completed the integration of Plasmon operations, forging an Italy-based production hub for formula and baby food.

- May 2025: The World Health Assembly adopted strict digital-marketing curbs for breast milk substitute

Global Breast Milk Substitutes Market Report Scope

As per the scope of the report, breast milk substitutes (BMS) refer to any food, such as infant formula or other milk products, marketed or represented as a partial or total replacement for breast milk. While the World Health Organization (WHO) recommends exclusive breastfeeding for the first six months of life, BMS are recognized as a necessary nutritional alternative in specific medical or social circumstances where breastfeeding is not possible, suitable, or adequate.

The breast milk substitutes market is segmented by form, stage, distribution channel, and geography. By form, the market is segmented into powder, liquid concentrate, and ready-to-feed (RTF). By stage, the market is segmented into Stage 1 (0–6 months), Stage 2 (6–12 months), and Stage 3 milk (12–36 months). By distribution channel, the market is segmented into supermarkets, pharmacies, online/e-commerce, and specialty baby stores.

Geographically, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Powder |

| Liquid Concentrate |

| Ready-to-Feed (RTF) |

| Stage 1 (0–6 months) |

| Stage 2 (6–12 months) |

| Stage 3 / Growing-up milk (12–36 months) |

| Supermarkets |

| Pharmacies |

| Online/E-commerce |

| Specialty Baby Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Form | Powder | |

| Liquid Concentrate | ||

| Ready-to-Feed (RTF) | ||

| By Stage (Age Group) | Stage 1 (0–6 months) | |

| Stage 2 (6–12 months) | ||

| Stage 3 / Growing-up milk (12–36 months) | ||

| By Distribution Channel | Supermarkets | |

| Pharmacies | ||

| Online/E-commerce | ||

| Specialty Baby Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast will global demand for breastfeeding alternatives grow through 2031?

Value is forecast to increase at a 5.71% CAGR, climbing from USD 79.2 billion in 2026 to USD 104.5 billion in 2031.

Which region will add the most incremental revenue?

Europe delivers the fastest 6.10% CAGR, driven by organic labels and tougher safety rules that boost premium pricing.

What format is expanding the quickest?

Liquid concentrate, backed by dual-income convenience, is projected to rise at 6.20% annually to 2031.

Why are Stage 3 products attracting investment?

They extend usage to 36 months, tripling lifetime value and enjoying looser health-claim rules in China and Southeast Asia.

Page last updated on: