Market Overview

| Study Period | 2019 - 2030 |

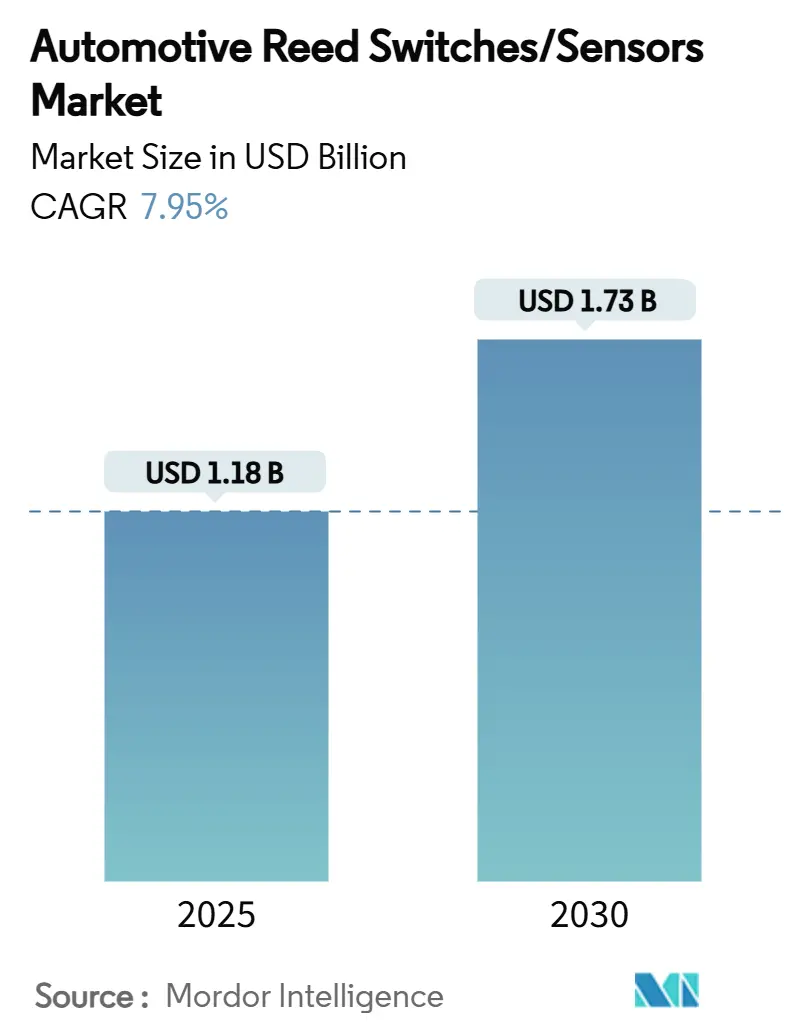

| Market Size (2025) | USD 1.18 Billion |

| Market Size (2030) | USD 1.73 Billion |

| Growth Rate (2025 - 2030) | 7.95% CAGR |

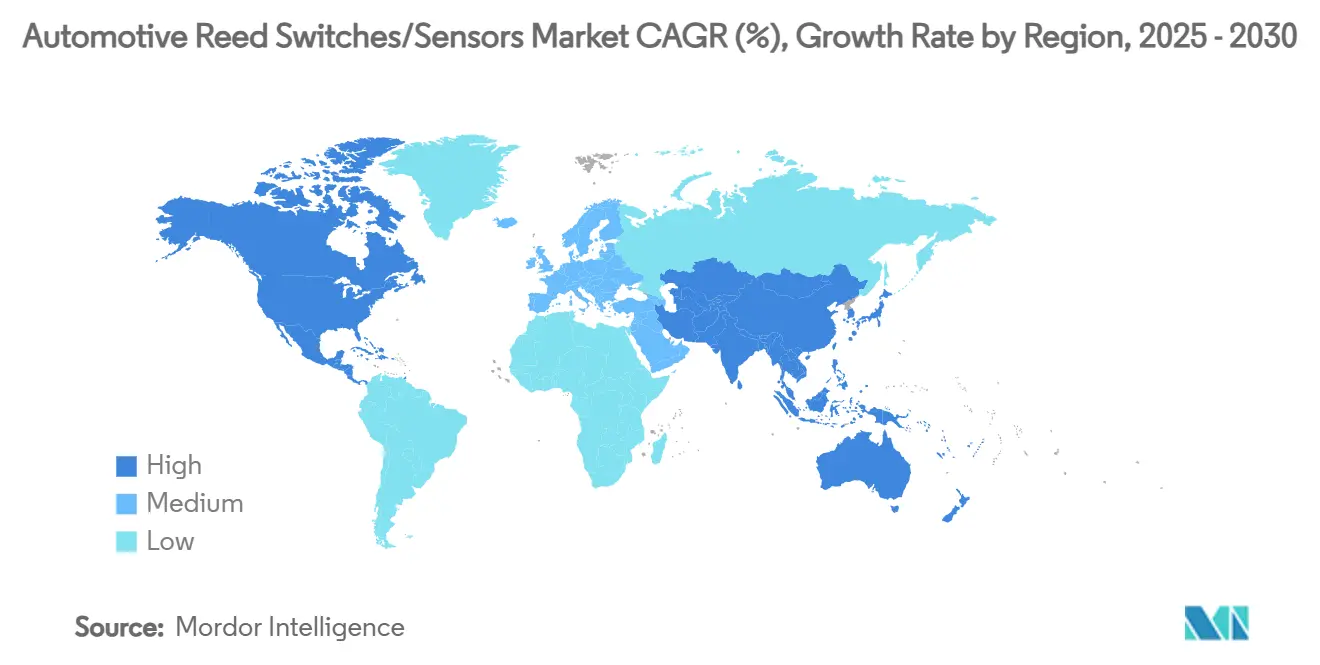

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

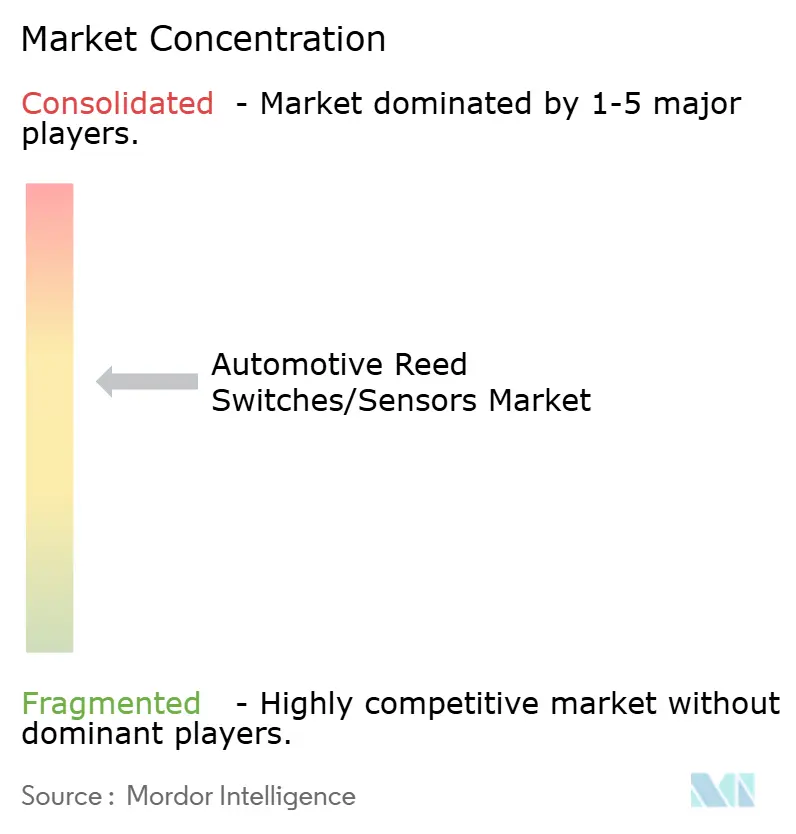

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Reed Switches/Sensors Market Analysis by Mordor Intelligence

The automotive reed switches/sensors market size is valued at USD 1.18 billion in 2025 and is projected to hit USD 1.73 billion by 2030, advancing at a 7.95% CAGR during the forecast period. Rapid electrification of powertrains, the EU General Safety Regulation II that took effect in July 2024, and the NHTSA automatic emergency-braking mandate driving compliance by September 2029 are forcing automakers to embed redundant, fail-safe switching across every platform. Reed switches retain share because their zero-standby-current draw and galvanic isolation meet battery-sleep and high-voltage-disconnect needs more economically than Hall-effect or AMR alternatives, even as nickel-iron alloy shortages encourage suppliers to vertically integrate. Competitive intensity is rising as Standex International, Littelfuse, and TE Connectivity add hermetic-sealing and alloy-rolling capacity to protect supply chains and defend against fast-scaling Asian rivals.

Key Report Takeaways

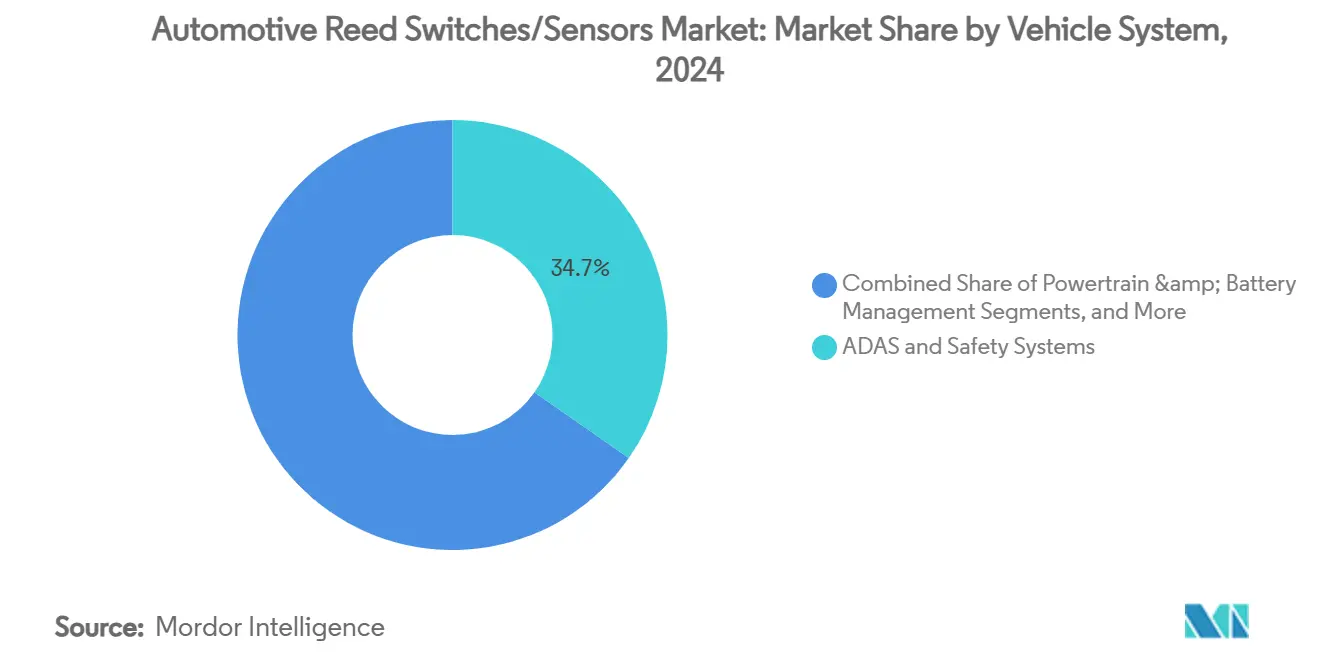

- By vehicle system, ADAS and safety systems held 34.68% of the automotive reed switches/sensors market share in 2024, whereas powertrain & battery management is projected to record the fastest 12.65% CAGR through 2030.

- By mounting type, surface-mount packages led with a 52.02% share of the automotive reed switches/sensors market in 2024 and are advancing at an 11.73% CAGR.

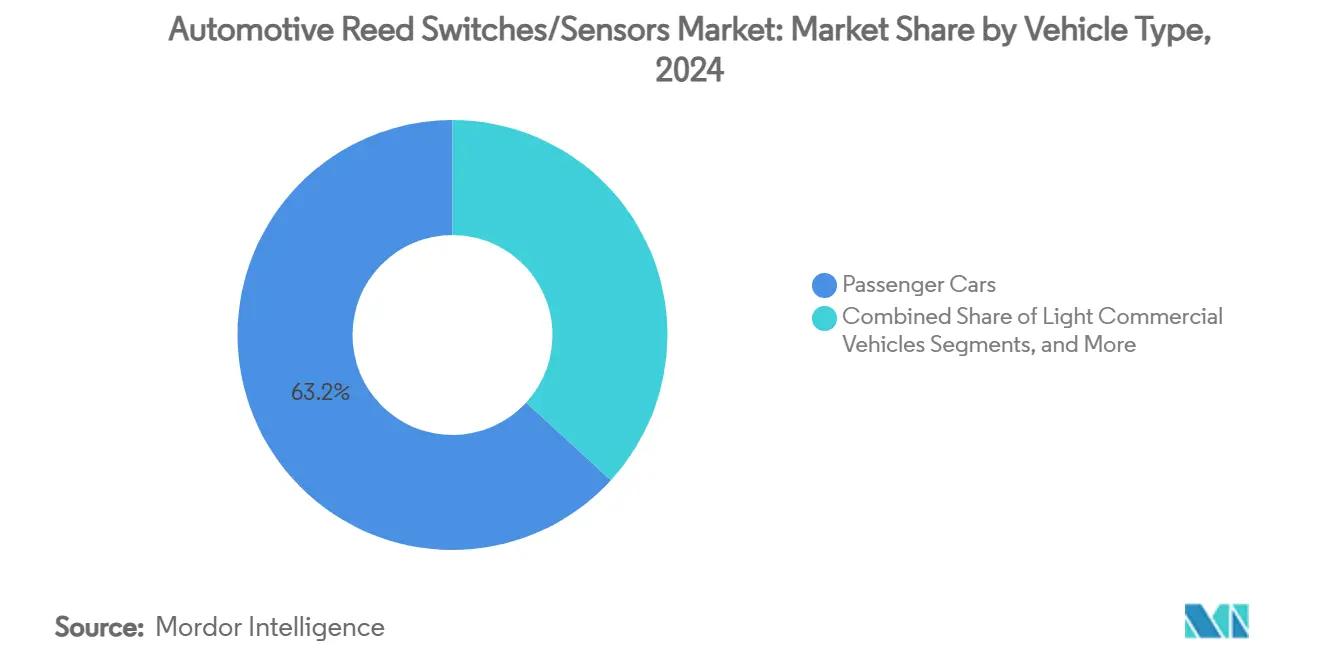

- By vehicle type, passenger cars accounted for 63.24% of the automotive reed switches/sensors market share in 2024 and are expanding at a 13.46% CAGR to 2030.

- By Sales Channel, OEM accounted for 81.60% of the automotive reed switches/sensors market share in 2024, and the aftermarket is expanding at a 11.63% CAGR to 2030.

- By geography, Europe contributed 27.54% of the automotive reed switches/sensors market revenue in 2024, while Asia-Pacific is set to grow at an 11.22% CAGR through 2030.

Global Automotive Reed Switches/Sensors Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising EV Production Boosts Battery-safe Reed Sensors | +2.1% | China, Europe, North America | Medium term (2-4 years) |

| Stricter Global Passive-safety Mandates | +1.8% | EU, North America (global spill-over) | Short term (≤ 2 years) |

| Shift Toward Steer-by-wire & Brake-by-wire Redundancy | +1.5% | North America, EU, Asia-Pacific | Medium term (2-4 years) |

| Proliferation Of Smart Keyless-entry & Door-latch Systems | +1.2% | Premium vehicle programs worldwide | Short term (≤ 2 years) |

| OEM Drive For Zero-standby-current Components | +0.9% | EV-focused regions worldwide | Long term (≥ 4 years) |

| Hydrogen Fuel-cell Vehicle Fluid-level Monitoring | +0.4% | Japan, South Korea, EU pilot regions | Long term (≥ 4 years) |

Source: Mordor Intelligence

Rising EV production boosts demand for battery-safe reed sensors

World electric-vehicle output continues to rise steeply, and every high-voltage battery pack now integrates multiple reed switches that guarantee spark-free isolation between control and power circuits. Their zero-standby-current characteristic maximizes parked-vehicle range, meeting stringent warranty targets. Continental’s latest e-motor rotor temperature sensor illustrates the push toward tighter ±3 °C tolerance, which lowers rare-earth magnet mass and reduces total motor cost while relying on hermetically sealed reed cores for galvanic isolation. Taifang Technology already mass-produces a battery intelligent monitoring system that uses reed triggers to detect collision-induced deformation and still meets ECE R100 compliance, showing how EV safety norms embed these switches as default second-line protectors. The technology’s robust magnetic sensitivity assures accurate actuation even when pack shielding, cell count, and thermal pads vary between vehicle trims. Manufacturers thus embed additional reed nodes around module disconnects to support predictive maintenance analytics, opening new service-oriented revenue streams.

Stricter Global Passive-safety Mandates

Regulators continue to tighten timelines for advanced emergency braking, emergency lane keeping and driver-drowsiness detection. The EU General Safety Regulation II, effective since July 2024, compels every new M1 and N1 vehicle to integrate redundant status sensors in seat-belt buckles and occupant modules where dry-reed contacts provide reliable closure verification. The United States NHTSA rule will enforce automatic emergency braking at speeds up to 90 mph by September 2029, with nighttime performance thresholds that demand fail-operational backup for optical and radar subsystems [1]“Federal Motor Vehicle Safety Standards; Automatic Emergency Braking,” National Highway Traffic Safety Administration, nhtsa.gov. Across these programs, reed switches serve as cost-effective watchdogs that alert control units when primary solid-state channels fail. Euro 7 emissions standards, released in May 2024, add tamper-proof onboard diagnostics ports that often employ reed switches within sealed captive shells, reinforcing the long-term compliance role of the component.

Shift Toward Steer-by-wire & Brake-by-wire Redundancy

Vehicle architectures are phasing out mechanical links in favor of wire-controlled actuation, and ISO 26262 ASIL D requirements stipulate 2-out-of-3 sensor paths. Reed switches fulfill the diversity element because they operate on purely magnetic contacts rather than semiconductor principles, thereby mitigating common-mode failure. ZF’s 2025 heavy-truck brake-by-wire win demonstrates growing acceptance beyond passenger vehicles, as fleet operators value weight savings and easier service procedures. Steer-by-wire columns benefit similarly; reed-position modules tolerate −40 °C to 125 °C temperature swings and maintain switching repeatability under vibration, meeting truck life-cycle targets. The shift pushes electronic content per vehicle toward USD 1,200 by 2030, but reed switches moderate total bill-of-materials because they require no signal-conditioning silicon or diagnostic current draw.

Rapid Proliferation Of Smart Keyless-entry and Door-Latch Systems

Passive Entry Passive Start platforms now pair biometric checks with NFC proximity tags. Door handles move flush with body panels, and multiple reed switches confirm latch travel, anti-pinch clearance, and mechanical override status. Tesla patents highlight retractable handles that rely on discrete reed triggers to guarantee positional feedback under snow or contamination, where optical or capacitive methods struggle. Reed immunity to radio-frequency noise prevents unlocking failures when Bluetooth Low Energy and ultra-wideband transceivers operate concurrently. Automakers also integrate the switch inside the emergency-release path, ensuring manual egress under 12-V power-loss conditions, a regulatory necessity for battery-electric models.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hall-effect & AMR Sensor Price Erosion | -1.4% | Asia-Pacific cost-focused producers | Short term (≤ 2 years) |

| Glass Reed Fragility In Harsh E-axle Vibration | -0.8% | Global heavy-duty and high-torque EVs | Medium term (2-4 years) |

| Supply-chain Risk For Nickel-iron Alloys | -0.7% | Global suppliers, China processing dominance | Medium term (2-4 years) |

| Upcoming Rohs Phase-out Of Mercury-wetted Reeds | -0.3% | EU and aligned markets | Short term (≤ 2 years) |

Source: Mordor Intelligence

Hall-effect & AMR sensor price erosion

Semiconductor costs fall predictably with node scaling, enabling Hall-effect suppliers to bundle signal conditioning and LIN bus outputs at lower system cost. AMR variants deliver higher sensitivity and omnipolar detection that appeals to design engineers seeking layout flexibility. Allegro MicroSystems’ recent TMR-VHT family meets ISO 26262 ASIL D self-diagnostic coverage, cutting into legacy reed share in safety loops that once required discrete redundancy[2] “TMR-VHT Automotive Sensor Family,” Allegro MicroSystems, allegromicro.com. Although solid-state parts still draw quiescent current, cost reductions of 8-10% per year narrow the price gap, prompting value-segment vehicles to adopt semiconductor solutions where zero current is not mission-critical.

Glass Reed Fragility In Harsh E-axle Vibration

E-axles generate high-frequency pulses from pulse-width-modulated motor drives and regenerative braking torque reversals. These vibrations exceed the stress limits of thin-wall glass envelopes, raising failure rates when switches are mounted directly on housings. Continental’s electric powertrain sensor roadmap now recommends shock-absorbing brackets or remote-mount harnesses to mitigate 20 G peak loads. Reinforced glass options exist but add cost and complexity versus epoxy-packaged Hall devices. Commercial vehicles, which see longer duty cycles, represent the most exposed segment.

Segment Analysis

By Vehicle System: ADAS Dominance Drives Safety Integration

ADAS and safety modules accounted for 34.68% of the automotive reed switches/sensors market share in 2024, underscoring regulators’ insistence that collision-avoiding functions include fail-safe sensor redundancy. Powertrain & battery management posts the fastest 12.65% CAGR because every traction battery string requires multiple reed switches to satisfy high-voltage isolation and thermal runaway containment. The automotive reed switches market size tied to body-comfort electronics remains stable, with steady demand for seat-track, sunroof, and HVAC-damper detection. Infotainment enclosures add moderate volume as OEMs secure tamper-proof access for over-the-air software gateways.

The revenue mix illustrates how electrification and safety legislation influence sensor architectures. Reed contacts sit alongside Hall and AMR silicon, forming diverse sensing trios that address ISO 26262 independence rules. Over the forecast horizon, the faster-growing powertrain segment will narrow the gap with ADAS, especially when solid-state battery packs require even more granular monitoring, further expanding the automotive reed switches market.

Note: Segment shares of all individual segments available upon report purchase

By Mounting Type: Surface-Mount Efficiency Drives Adoption

Surface-mount packages accounted for 52.02% of the automotive reed switches/sensors market in 2024 and exhibit an 11.73% CAGR, propelled by automated pick-and-place lines that lower labor cost and enable denser PCB layouts. Through-hole styles persist in high-shock powertrain brackets where mechanical retention is crucial. Threaded-panel modules and inline plug-ins serve diagnostic ports, making field replacement easier for fleet operators.

Surface-mount momentum mirrors the industry shift toward compact controllers housed inside battery trays, motor inverters, and smart-actuator pods. These enclosures frequently allocate less than 1 mm board-to-lid clearance, favoring low-profile reed packages. As automakers standardize on reflow-compatible solder alloys to withstand −40 °C to 150 °C excursions, surface-mount penetration will continue to outpace all other mount styles, reinforcing its lead within the broader automotive reed switches market.

By Vehicle Type: Passenger Car Innovation Leads Market

Passenger cars generated 63.24% of the automotive reed switches/sensors market revenue in 2024 and are forecast to expand at a 13.46% CAGR. Consumers demand more driver-assist features, and premium marques load vehicles with active-door, active-suspension, and zonal-network sensors that all incorporate reeds. Light commercial vans inherit these electronics rapidly, while heavy trucks integrate safety loops at a slower pace because total-cost-of-ownership dominates specification priorities.

In passenger applications, reed switches provide cost-effective zero-current solutions that extend battery park-sleep periods, a key selling point for urban EV buyers. Luxury OEMs pioneer advanced applications such as automated gull-wing closures and smart-frunk actuators, creating reference designs that filter to mainstream models. These dynamics should keep passenger cars the single largest slice of the automotive reed switches market size through 2030.

Note: Segment shares of all individual segments available upon report purchase

By Sales Channel: OEM Dominance with Aftermarket Growth

OEM contracts supplied 81.60% of the automotive reed switches/sensors market size in 2024 as automakers source sensors directly to ensure PPAP traceability and quality compliance. The aftermarket, however, expands at an 11.63% CAGR because growing electronics density means any latch or battery disconnect failure can immobilize the vehicle. Component suppliers now release drop-in equivalents earlier in the model life cycle, supporting independent repair shops.

Vehicle life expectancy continues to rise, and extended warranties boost replacement parts sales. As over-the-air software updates reinforce the need for hardware integrity, sensor components with unique IDs become crucial. This stimulates a healthy aftermarket stream that tempers OEM concentration, broadening overall access to the automotive reed switches market.

Geography Analysis

Europe retained 27.54% of the automotive reed switches/sensors market revenue in 2024 on the back of stringent safety and emissions directives that mandate redundant sensing and tamper-proof diagnostics. Germany leads integration depth, whereas France and Italy accelerate battery-electric programs that embed more reed nodes per vehicle. Euro 7 on-board monitoring rules further anchor demand by stipulating sealed access points that the hermetic reed switch supports.

Asia-Pacific is the fastest-growing region at 11.22% CAGR as China’s dominance in EV production drives immense volume for battery pack switches. Japan remains a sensor technology powerhouse, regularly launching compact reed variants optimized for 48-V architectures. South Korea and India add momentum through export-oriented vehicle programs, spreading adoption across budget and premium tiers.

North America shows solid expansion influenced by the NHTSA braking mandate and renewed on-shoring of component supply due to 25% tariffs on selected imports. Canada and Mexico integrate regional manufacturing, providing cost-effective assembly for reed packages tailored to US OEM specifications. Heavy-duty electrification and autonomous trucking pilots also lift sensor volume, broadening the reach of the automotive reed switches market.

Competitive Landscape

The field remains moderately fragmented, yet consolidation is advancing as top suppliers secure vertical control over contact alloy processing and hermetic sealing lines. Standex International leverages custom assembly automation to cut lead times for bespoke SPDT parts. Littelfuse expands hybrid sensor portfolios that bundle reed, Hall, and power-fusible links into single modules, offering OEMs a simplified sourcing route. TE Connectivity invests in in-house nickel-iron alloy rolling mills, reducing exposure to outside metal markets.

Asian entrants, notably from China and Taiwan, target commodity SPST volumes, pressuring price points in door-ajar and liquid-level niches. Sensata Technologies positions itself as a system integrator by coupling reed fail-safe switches with MEMS pressure sensors in battery disconnect units, aligning with OEM functional-safety road maps [3] “Electrification – e-Mobility Portfolio (Battery Disconnect Units, High-Voltage Fuses, MEMS Pressure Sensors),” Sensata Technologies, sensata.com. Hydrogen fuel-cell applications emerge as a white-space where Marquardt’s epoxy-sealed designs stake early leadership. Overall, rivalry centers on specialized packaging, vibration tolerance, and compliant contact plating as the automotive reed switches market matures alongside EV adoption.

Automotive Reed Switches/Sensors Industry Leaders

-

Standex International Corp.

-

TE Connectivity Ltd

-

ZF Friedrichshafen AG

-

Littlefuse Inc.

-

Continental AG

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- April 2025: Sensata Technologies launched the STPS500 Series PyroFuse, a breakthrough designed for high-voltage disconnection in under one millisecond. This state-of-the-art technology bolsters automotive battery safety, offering vital protection for electric and hybrid vehicles. Thanks to its dependable performance and rapid response, the PyroFuse swiftly addresses potential electrical hazards, marking a significant leap in automotive safety solutions.

- April 2025: TDK introduced a new line of cost-effective Hall-effect 2D position sensors, aiming to replace traditional reed contacts in compact actuator modules. These state-of-the-art sensors boast improved precision and longevity, catering perfectly to today's applications that prioritize space efficiency. With this debut, TDK is set to address the evolving challenges of modern engineering with its advanced solution.

- January 2025: ZF clinched a major contract to supply state-of-the-art brake-by-wire systems tailored for heavy-duty trucks. This milestone underscores the surging demand for sophisticated redundant switching solutions in commercial vehicles, spotlighting the industry's heightened emphasis on safety and reliability in heavy transport.

- January 2025: Honeywell unveiled a pioneering Battery Safety Electrolyte Sensor, aimed at bolstering the detection of thermal runaway incidents in electric vehicle battery packs. This state-of-the-art sensor is pivotal in overseeing electrolyte conditions, thereby augmenting the safety and dependability of electric vehicles. By adeptly pinpointing potential threats in their nascent stages, the sensor greatly enhances the performance and security of battery systems.

Global Automotive Reed Switches/Sensors Market Report Scope

The reed switch is an electrical switch operated by an applied magnetic field. It consists of a pair of contacts on ferrous metal reeds in an airtight glass envelope. The contacts are normally open, making no electrical contact. The switch is actuated (closed) by bringing a magnet near the switch. All areas of typical automotive systems incorporate low-profile, zero power consumption reed switch sensors to help them operate reliably and safely. Reed switch is used to support various automotive applications, such as speedometer, power window operation, infotainment, and in-vehicle navigation centers, side and rearview mirrors, cruise control and power steering, door lock actuation, etc. The aforementioned features of automotive reed switches/sensors have been considered in the scope of the market.

The automotive reed switches/sensors market has been segmented by application, vehicle type, and geography.

| By Vehicle System | Powertrain & Battery Management | ||

| ADAS & Safety Systems | |||

| Body & Comfort Electronics | |||

| Infotainment & Connectivity | |||

| HVAC & Thermal Management | |||

| Others | |||

| By Mounting Type | Surface Mount | ||

| Through Hole | |||

| Threaded / Panel | |||

| Inline / Plug-in | |||

| By Vehicle Type | Passenger Cars | ||

| Light Commercial Vehicles | |||

| Medium & Heavy Commercial Vehicles | |||

| Two-Wheelers & Three-Wheelers | |||

| Off-Highway & Special Vehicles | |||

| By Sales Channel | OEM | ||

| Aftermarket | |||

| By Geography | North America | United States | |

| Canada | |||

| Rest of North America | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Indonesia | |||

| Vietnam | |||

| Philippines | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Saudi Arabia | ||

| United Arab Emirates | |||

| Turkey | |||

| South Africa | |||

| Nigeria | |||

| Egypt | |||

| Rest of Middle East and Africa | |||

By Vehicle System

| Powertrain & Battery Management |

| ADAS & Safety Systems |

| Body & Comfort Electronics |

| Infotainment & Connectivity |

| HVAC & Thermal Management |

| Others |

By Mounting Type

| Surface Mount |

| Through Hole |

| Threaded / Panel |

| Inline / Plug-in |

By Vehicle Type

| Passenger Cars |

| Light Commercial Vehicles |

| Medium & Heavy Commercial Vehicles |

| Two-Wheelers & Three-Wheelers |

| Off-Highway & Special Vehicles |

By Sales Channel

| OEM |

| Aftermarket |

By Geography

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Indonesia | |

| Vietnam | |

| Philippines | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Rest of Middle East and Africa |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the size of the automotive reed switches market in 2025?

The automotive reed switches market size reached USD 1.18 billion in 2025 and is projected to climb to USD 1.73 billion by 2030.

Which vehicle system dominates demand for reed switches?

ADAS and safety systems contribute the largest share at 34.68%, reflecting regulatory emphasis on collision-avoidance integration.

Why are surface-mount reed switches gaining traction?

Surface-mount packages fit automated assembly lines and satisfy space constraints inside compact ECUs, which drives an 11.73% CAGR for this mounting style.

Which region is the fastest-growing market for automotive reed switches?

Asia-Pacific leads with an 11.22% CAGR, propelled by China’s rapidly scaling electric-vehicle production and Japan’s sensor innovation initiatives.

Page last updated on: July 6, 2025