Brazil Pet Veterinary Diets Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

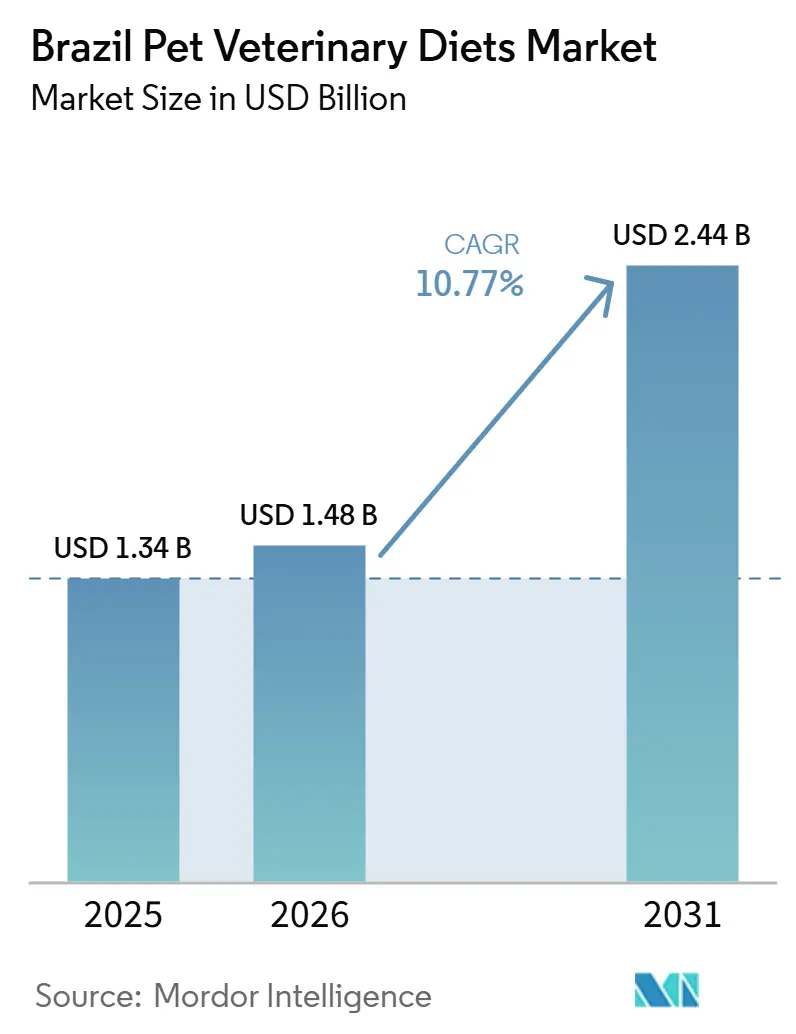

| Base Year Market Size (2025) | USD 1.34 Billion |

| Market Size (2026) | USD 1.48 Billion |

| Market Size (2031) | USD 2.44 Billion |

| Growth Rate (2026 - 2031) | 10.77% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Pet Veterinary Diets Market Analysis by Mordor Intelligence

The Brazil pet veterinary diets market size is projected to grow from USD 1.34 billion in 2025 to USD 1.48 billion in 2026 and is forecast to reach USD 2.44 billion by 2031 at 10.77% CAGR over 2026-2031. According to the Brazilian Association of Companies in the Pet Sector (Abempet), Brazil’s pet population reached 160.9 million animals in 2024, with cats growing 5.4% and dogs growing 2.8%, widening the base for condition-specific nutrition and giving the category a broader clinical demand pool[1]Source: Brazilian Association of Pet Industry Companies (ABEMPET), “General Information on the Sector,“ abempet.org.br.. Demand is being reinforced by higher diagnosis rates for chronic renal, urinary, digestive, metabolic, and obesity-related conditions, along with a larger aging companion animal base that stays on prescribed food for longer periods. Pet humanization is also keeping owners closer to veterinary care pathways, which supports repeat purchases, premium price acceptance, and better adherence to clinically guided diets over time. Access is widening as remote prescriptions, specialty retail, and clinic software shorten the path between diagnosis and refill, which gives the Brazil pet veterinary diets market a stronger reach beyond the largest urban centers.

Key Report Takeaways

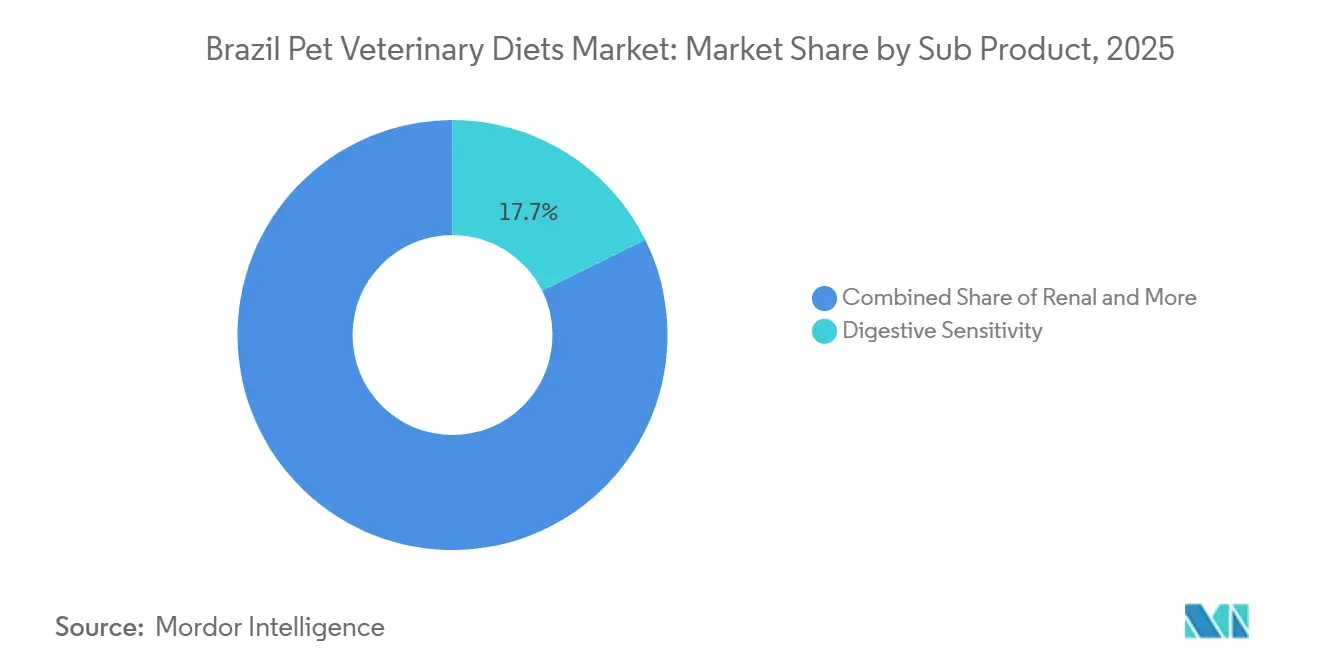

- By sub-product, digestive sensitivity was the largest segment, accounting for 17.7% of the Brazil pet veterinary diets market size in 2025, while obesity diets are the fastest-growing segment and are forecast to grow at a 11.3% CAGR between 2026 and 2031.

- By pet type, dogs were the largest segment, accounting for 67.3% of the Brazil pet veterinary diets market share in 2025, while cats were the fastest-growing segment and are projected to grow at a 12.1% CAGR between 2026 and 2031.

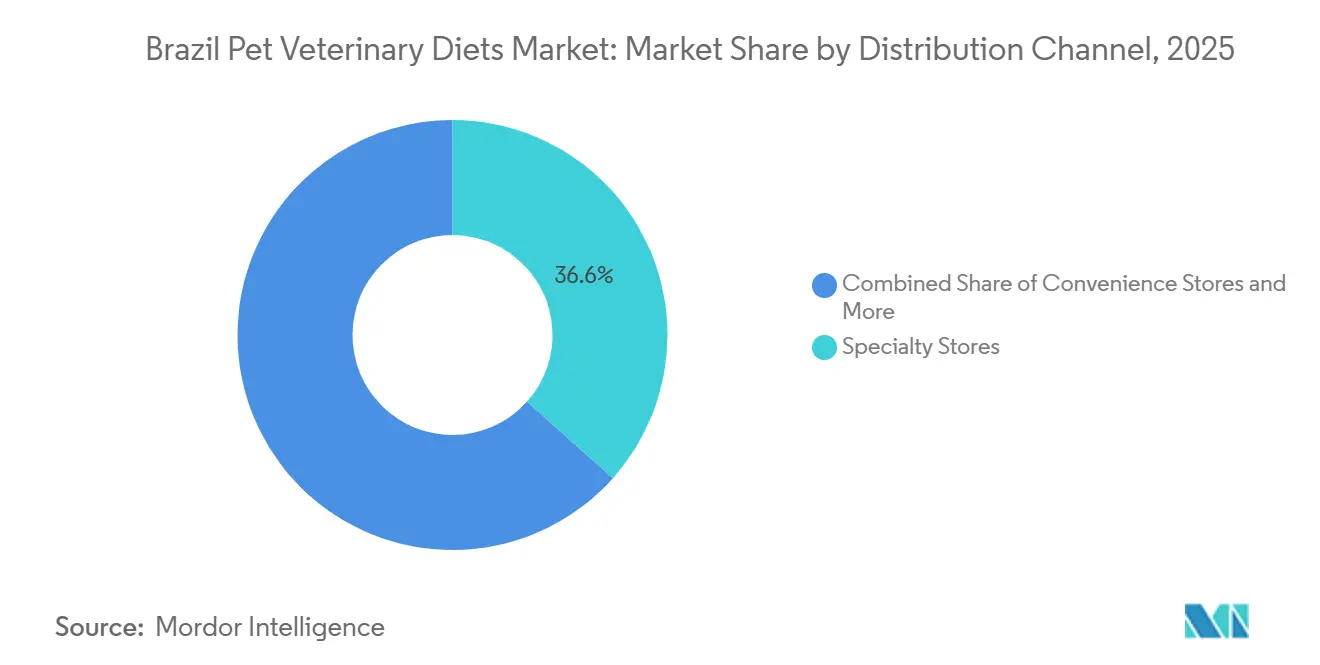

- By distribution channel, specialty stores were the largest segment with a 36.6% revenue share in 2025, while the online channel is projected to be the fastest-growing segment, growing at a 12.8% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Brazil Pet Veterinary Diets Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising chronic disease diagnosis in dogs and cats | +2.8% | National, concentrated in São Paulo, Rio de Janeiro, and Curitiba | Short term (≤ 2 years) |

| Pet humanization and premium health spending | +2.3% | National, with early gains in the Southeast and South | Medium term (2-4 years) |

| Veterinarian-led prescription influence | +1.8% | National, with urban clinics as primary prescribers | Medium term (2-4 years) |

| Expansion of specialty retail and e-commerce access | +1.5% | National, with digital channels extending to secondary cities | Short term (≤ 2 years) |

| Subscription refill and adherence models for chronic diets | +1.1% | Southeast and South, especially digital-first urban consumers | Medium term (2-4 years) |

| Integrated vet software, Customer Relationship Management (CRM), and nutrition recall targeting | +0.7% | Urban centers in the Southeast, with spillover into the South | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Chronic Disease Diagnosis in Dogs and Cats

The Brazil pet veterinary diet market is benefiting from a heavier chronic disease load across urban dogs and cats, which is turning more veterinary visits into longer treatment nutrition cycles. The 2025 peer-reviewed study, "Canine Obesity - Contributing Factors and Body Condition Evaluation" by Mariana T. Resende and co-authors, identified canine obesity as one of the most common nutritional disorders encountered in veterinary practice, underscoring the sustained need for weight-management formulas[2]Source: MDPI, “Canine Obesity: Contributing Factors and Body Condition Evaluation,“ Veterinary Sciences, mdpi.com.. A 2025 study based on records from the University of São Paulo veterinary hospital also showed that dietary intervention has become a routine part of managing metabolic disorders in dogs, confirming that food is now a regular therapeutic tool rather than an occasional add-on. These cases often progress into diabetes, renal disease, osteoarthritis, and digestive complications, and that gives prescribed nutrition a longer role across the animal’s life rather than a short recovery window. The same pattern is strengthening renal and urinary demand in cats, giving the Brazilian pet veterinary diets market a durable clinical base tied to repeat use rather than one-time diagnosis.

Pet Humanization and Premium Health Spending

The Brazil pet veterinary diets market is also supported by a shift in how owners approach health spending for companion animals, particularly in large urban households where pets are treated as part of the family budget. This shift is reflected in stronger demand for condition-specific products, including renal, gastrointestinal, and weight management diets, as owners increasingly seek long-term dietary solutions rather than short-term interventions. Farmina Pet Foods Holding N.V. reported Brazil revenue growth of 25% to BRL 400 million (USD 74 million) in 2024, indicating that premium clinical nutrition can scale when owners accept higher spending as part of regular health management. Veterinary recommendations continue to play a central role in driving this acceptance, as clinic-based endorsements lend credibility to higher-priced therapeutic products and encourage repeat purchasing behavior. This spending pattern is positioning treatment diets within the preventive care conversation, helping the category capture value beyond acute disease episodes and supporting a more stable long-term revenue mix in the Brazil pet veterinary diets market.

Veterinarian-Led Prescription Influence

Veterinarians remain the key gatekeepers in the Brazil pet veterinary diets market, and the regulatory structure keeps these products close to professional recommendations at every stage of purchase and refill. Under the Ministry of Agriculture, Livestock and Food Supply rules, products marketed as auxiliary foods for animals with physiological or metabolic disturbances must carry labeling for professional guidance, keeping the category clearly separate from general-purpose pet food. Federal Council of Veterinary Medicine rules also allow remote prescriptions, which expand specialist reach into cities where local veterinary nutrition support is thinner and clinic density is lower. This framework positions veterinarians at the center of diagnosis, product selection, follow-up, and refill behavior, thereby building trust and improving compliance in chronic care categories. It also makes subscription refill models and clinic-linked digital reminders more effective, because the original prescription relationship remains strong across the Brazil pet veterinary diets market.

Expansion of Specialty Retail and E-Commerce Access

Better access through specialty retail and digital channels is widening the Brazil pet veterinary diets market, especially for consumers who live outside the core clinic clusters of São Paulo and other large cities. Specialty Stores can validate prescriptions, provide trained counseling, and maintain a clinically oriented stock that is less common in broad retail formats. Brazil’s pet e-commerce underscores how quickly digital channels are becoming a serious channel for higher-value pet purchases.Farmina Pet Foods Holding B.V. inaugurated a BRL 45 million (approximately USD 8.0 million) distribution center in Bragança Paulista, São Paulo, in September 2025. The 10,500 m² facility is designed to strengthen the company's logistics network, increase production capacity, and reinforce Brazil's role as Farmina's export hub for South America[3]Source: Municipality of Bragança Paulista, “Municipal Administration Participates in the Inauguration of Farmina’s Distribution Center in Bragança Paulista,” braganca.sp.gov.br.. Mars, Incorporated opened a BRL 30 million (USD 5.1 million) distribution center in Extrema to improve supply response across key regions. As online refill fulfillment becomes easier after a veterinary recommendation, the category gains a wider, more stable buyer base, giving the Brazil pet veterinary diets market greater room to expand into secondary cities without waiting for new physical clinic networks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High tax burden and premium price sensitivity | -1.9% | National, most acute for middle-income households in secondary cities | Short term (≤ 2 years) |

| Income inequality and uneven affordability across cities | -1.4% | Northeast, North, and interior Southeast | Medium term (2-4 years) |

| Prescription leakage into general pet channels | -1.0% | National, more pronounced in online and supermarket segments | Short term (≤ 2 years) |

| Low long-term diet compliance and palatability drop-off | -0.8% | National, across all distribution channels | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Tax Burden and Premium Price Sensitivity

The Brazil pet veterinary diets market is still limited by the high final price of premium therapeutic food, and that price pressure is most visible when imported or premium-positioned products move outside top-income households. Brazil’s indirect tax structure raises shelf prices for clinically positioned diets, which narrows the addressable buyer pool and keeps many owners in a wait-and-see pattern even when veterinary advice is clear. This pressure has a direct competitive effect because domestic suppliers such as PremieRpet S.A. face fewer import-related burdens and can compete more aggressively on price while still holding a clinical positioning. At the same time, inflation and tighter disposable income conditions weaken the ability of lower-middle-income urban households to stay on prescribed food for the full treatment period. The result is that premium acceptance remains strongest at the top end of the market, while broader conversion in the Brazil pet veterinary diets market still depends on better affordability and sharper value communication.

Income Inequality and Uneven Affordability Across Cities

Income inequality also creates a visible regional split in the Brazil pet veterinary diets market, because demand potential is spread across the country but active buying power is concentrated much more heavily in the Southeast and South. Household income data from the Brazilian Institute of Geography and Statistics showed that average household income in the Northeast and North stayed below the Southeast, and that gap has a direct effect on willingness and ability to buy prescribed diets for long-term use. This affordability gap is exacerbated by uneven specialist clinic density, as internal medicine and veterinary nutrition services remain much more concentrated in São Paulo, Rio de Janeiro, and Curitiba than in secondary cities. Prescription leakage into general pet channels and weaker long-term compliance also affect demand, because owners may switch away after the first purchase if product use is not reinforced through clinical follow-up or if palatability becomes an issue. Telemedicine and digital refill tools can reduce the access gap, but they cannot fully solve the income barrier, which means growth in the Brazil pet veterinary diets market will still vary sharply by city and region.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub Product: Digestive Sensitivity Anchors the Market while Obesity Diets Accelerate

Digestive sensitivity held 17.7% market share in 2025 and represented the largest sub-product in the Brazil pet veterinary diets market. The segment benefits from frequent cases of chronic enteropathies, inflammatory bowel disease, food intolerance, and fat absorption issues, all of which make nutritional management a central part of treatment rather than a secondary step. Farmina Pet Foods Holding N.V. reinforced this space in 2025 with the launch of Gastrointestinal UltraCare Low Fat Canine at the World Small Animal Veterinary Association congress in Rio de Janeiro, which was presented for the treatment of chronic diarrhea, inflammatory bowel disease, and exocrine pancreatic insufficiency in dogs. Renal and urinary tract disease products also hold a firm place because many feline renal and urinary cases remain on therapeutic food for long periods, and that keeps these sub-products close to the category’s most stable recurring demand.

In Brazil, obesity diets are projected to expand at a 11.3% CAGR between 2026 and 2031, making it the fastest-growing subsegment of the Brazil pet veterinary diets industry. Premierpet S.A. launched its nutrição clínica úmidos line in 2025 and supported the installation of the first pet-specific dual-energy x-ray absorptiometry scanner in South America at the University of São Paulo, which strengthens obesity and metabolic disease research and gives the brand greater scientific visibility in this segment. Diabetes, oral care diets, derma diets, and other veterinary diets further broaden the therapeutic base, so the brazil pet veterinary diets industry is not dependent on a single condition cluster or breed pattern for growth.

By Pets: Dogs Dominate Revenue while Cats Drive Growth

Dogs held 67.3% market share in 2025 and remained the largest pet segment in the Brazil pet veterinary diets market because they combine the broadest installed population base with the most mature treatment relationship within veterinary channels. Their revenue lead also reflects a larger population of animals and their role in nearly 80% of pet food production volume in Brazil during 2025, giving dog-focused therapeutic products a stronger commercial base than any other species group. Dogs generally visit veterinarians more often for chronic condition management, which supports better diagnostic rates and stronger refill continuity for renal, digestive, obesity, and recovery diets. Other pets remain small because Brazil still has a limited range of therapeutic formulations for rabbits, birds, and small mammals, which keeps this segment structurally narrow over the forecast period.

In Brazil, in terms of market size, cats are forecast to grow at 12.1% CAGR between 2026 and 2031, making them the fastest-growing pet segment in the Brazil pet veterinary diets industry. Their momentum is linked to rising urban adoption in apartments. Feline clinical demand maps directly into renal insufficiency, lower urinary tract disease, and obesity management, which often lifts per-pet therapeutic spending because several conditions can coexist in the same patient over time. Virbac SA added Feluro and Pronefra in Brazil during 2025, which shows that suppliers are building more cat-centered nutritional support around urinary and renal care and are adjusting product strategy to the changing disease mix.

By Distribution Channel: Specialty Stores Lead while the Online Channel Disrupts

Specialty stores held 36.6% market share in 2025 and were the largest distribution channel in the Brazil pet veterinary diets market, supported by prescription validation, better product knowledge, and stronger trust at the point of sale. Many of these stores are linked to clinics or staffed by trained advisers, making them a more credible setting for conditions that require explanation, follow-up, and Stock Keeping Unit (SKU) matching after a veterinary diagnosis. Convenience stores, supermarkets, and hypermarkets carry a much narrower therapeutic assortment because clinically guided diets demand more careful stocking and greater consumer support than mass-market food lines. Other channels, including direct-from-clinic sales, still matter because the first prescription is often converted into an immediate purchase during the same consultation, which gives clinics an important role in early treatment adoption.

Brazil pet veterinary diets market size for the online channel is projected to expand at 12.8% CAGR between 2026 and 2031, making it the fastest distribution segment in the Brazil pet veterinary diets industry. Brazil’s pet e-commerce platform that scales is giving therapeutic products a wider digital shelf and a more practical refill path for consumers who already have a prescription in hand. Subscription refill models and telemedicine-linked renewal behavior are reducing drop-off after the first treatment cycle, which is especially important for products used in the management of obesity, renal, urinary, and digestive conditions. Mars, Incorporated strengthened this shift in 2025 by opening a distribution center in Extrema, Minas Gerais, which improved service speed across major regions and raised the pressure on smaller specialty retailers with weaker logistics depth.

Geography Analysis

The Southeast is the largest regional base for the Brazil pet veterinary diets market. São Paulo and Rio de Janeiro combine higher household income, denser clinic networks, and stronger acceptance of premium veterinary care, which gives prescribed nutrition a more stable commercial base than in most other regions. The University of São Paulo teaching hospital and its Pet Nutrology Service keep the region closely tied to the use of therapeutic diets, and the 2025 installation of the first pet-specific dual-energy X-ray absorptiometry scanner at CEPEN Pet added more local research capacity in obesity management. The South ranks second and remains important both as a demand center and as a supply base, with Nestle S.A. (Purina)’s new facility in Vargeão, Santa Catarina, reinforcing the region’s role in production and exports.

The Northeast and Central-West have smaller active revenue bases today, but both regions still offer meaningful headroom for the Brazil pet veterinary diets market as pet ownership broadens and channel access improves. The Northeast region already has scale, even though therapeutic diet penetration remains lower than in the Southeast and South. Household income levels in the Northeast and North were lower than in the Southeast, keeping affordability tighter for premium prescription diets that require long-term use. The Central-West benefits from Brasília’s income base and from the operational presence of PremieRpet S.A. in Dourados, which gives domestic supply a practical foothold in the interior. Remote prescribing and stronger logistics are starting to ease the access gap in secondary cities, even if they do not yet remove the pricing barrier that still shapes regional differences.

The North remains the smallest geography because urbanization is lower and specialty retail coverage is thinner than in the country’s more developed pet care corridors. Cities such as Belém and Manaus still rely more heavily on general pet channels, which are less suited to clinically guided nutrition and have narrower prescription-oriented assortments. Over the forecast period, broader online fulfillment should narrow some of that regional distance in the Brazil pet veterinary diets market by making refills easier to obtain after a veterinary recommendation. Even so, the Southeast and South are likely to retain the largest share of value because they combine clinic density, stronger premium spending, better-stocked therapeutic lines, and deeper manufacturer investment.

Competitive Landscape

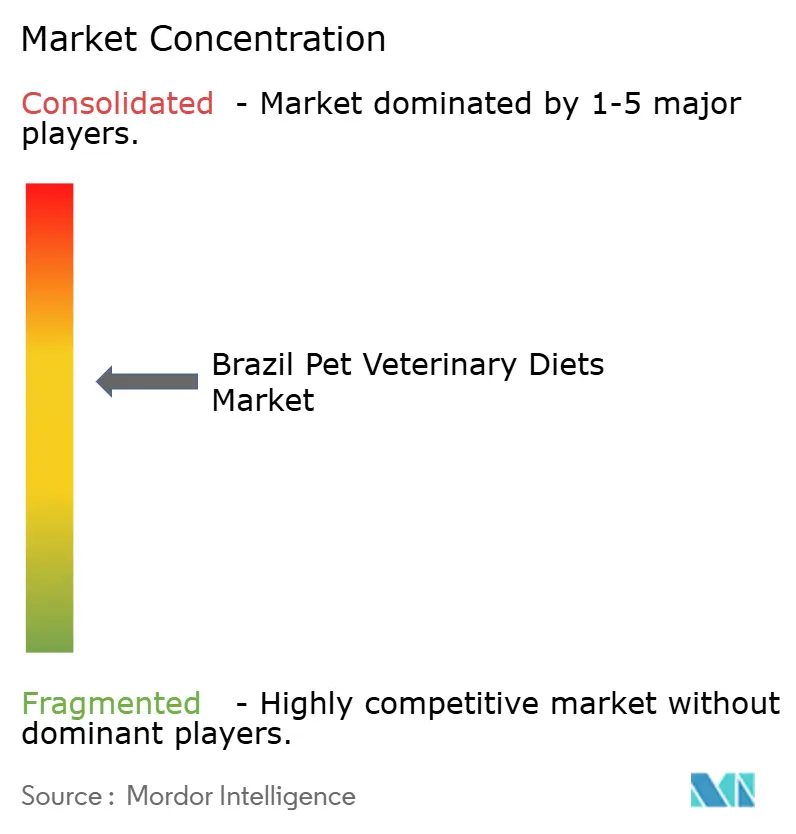

The Brazil pet veterinary diets market shows moderate concentration, with large multinational suppliers leading premium prescription care, while domestic players are building strength through pricing flexibility, research partnerships, and broader local access. Mars, Incorporated, Nestle S.A. (Purina PetCare Company), BRF S.A., Virbac SA, and PremieRpet S.A. (Grandfood Indústria e Comércio Ltda.) hold an advantage through veterinarian education programs, established clinical product portfolios, and long-standing relationships in specialty retail and veterinary channels. Virbac SA is differentiating through its Veterinary HPM range and its broader food-plus-supplement strategy, which connects nutritional management with urinary and renal support products, giving the brand a more integrated clinical profile. Open space remains strongest in mid-tier cardiac, dermatological, and post-surgical recovery products, where the category still looks less saturated than in renal and digestive care.

PremieRpet S.A. and Farmina Pet Foods Holding N.V. are narrowing the credibility gap by pairing product launches with research support and infrastructure investment, which gives them a stronger position against larger imported brands. PremieRpet S.A. backed the first pet-specific dual-energy X-ray absorptiometry scanner in South America and supported eight Brazil-authored studies at the 2025 American College of Veterinary Internal Medicine Forum, which shows a clear strategy of building scientific authority rather than relying only on shelf presence. Farmina Pet Foods Holding N.V. expanded its VetLife clinical line and opened its first South America distribution center in Bragança Paulista in 2025, targeting a 150% rise in production volume for Brazil and nearby export markets. Mars, Incorporated also expanded its logistics base in 2025 and added wet food capacity in Ponta Grossa, improving supply depth for Royal Canin SAS and reinforcing omnichannel responsiveness. These moves show that leading companies are competing more through science, fulfillment, and veterinary channel access than through straightforward price discounting.

Adimax Indústria e Comércio de Alimentos Ltda., Total Alimentos S.A., Special Dog Company Indústria e Comércio de Alimentos Ltda., and Affinity Petcare S.A. remain secondary participants, with greater exposure to less clinically complex nutrition tiers than the major prescription-focused leaders. Ministry of Agriculture, Livestock and Food Supply registration and labeling requirements create a meaningful barrier for any new entrant seeking to launch clinically positioned diets, favoring companies with an existing approval base and deeper regulatory experience. That barrier helps established suppliers protect shelf space, veterinarian trust, and repeat prescriptions across the Brazil pet veterinary diets market, even as local challengers become more visible. Competitive pressure is rising, but the field still favors companies that can combine compliant products, scientific support, and reliable national-scale distribution.

Brazil Pet Veterinary Diets Industry Leaders

Mars, Incorporated

BRF S.A.

Virbac SA

Nestle S.A. (Purina PetCare Company)

PremieRpet S.A. (Grandfood Indústria e Comércio Ltda.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: PremieRpet S.A. launched the PremieR Nutrição Clínica Úmidos line, a complete wet clinical range for dogs and cats covering obesity, diabetes, urinary tract conditions, and post-surgical recovery. The launch gave the company a stronger position in the fast-growing wet therapeutic segment.

- September 2025: Farmina Pet Foods Holding N.V. launched Gastrointestinal UltraCare Low Fat Canine at the World Small Animal Veterinary Association congress in Rio de Janeiro. The formula combined hydrolyzed protein, fat restriction, vitamin B12, and folic acid supplementation for chronic diarrhea, inflammatory bowel disease, and exocrine pancreatic insufficiency in dogs.

- June 2024: Virbac SA launched Feluro, an oral nutritional supplement for cats designed to support lower urinary tract health. The product is positioned at the intersection of veterinary nutritional support and companion animal disease management, combining dietary ingredients that help maintain normal bladder function and support urinary tract health.

Brazil Pet Veterinary Diets Market Report Scope

A pet veterinary diet, also known as a therapeutic or prescription diet, is a specialized pet food scientifically formulated to help manage, treat, or prevent specific medical conditions, including kidney disease, allergies, and obesity. The Brazil Pet Veterinary Diet Market Report is Segmented by Sub Product (Diabetes, Digestive Sensitivity, Oral Care Diets, Renal, Urinary Tract Disease, Derma Diets, Obesity Diets, and Other Veterinary Diets), by Pets (Cats, Dogs, and Other Pets), and by Distribution Channel (Convenience Stores, Online Channel, Specialty Stores, Supermarkets/Hypermarkets, and Other Channels). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

| Diabetes |

| Renal |

| Urinary Tract Disease |

| Digestive Sensitivity |

| Oral Care Diets |

| Derma Diets |

| Obesity Diets |

| Other Veterinary Diets |

| Cats |

| Dogs |

| Other Pets |

| Convenience Stores |

| Online Channel |

| Specialty Stores |

| Supermarkets/Hypermarkets |

| Other Channels |

| Sub Product | Diabetes |

| Renal | |

| Urinary Tract Disease | |

| Digestive Sensitivity | |

| Oral Care Diets | |

| Derma Diets | |

| Obesity Diets | |

| Other Veterinary Diets | |

| Pets | Cats |

| Dogs | |

| Other Pets | |

| Distribution Channel | Convenience Stores |

| Online Channel | |

| Specialty Stores | |

| Supermarkets/Hypermarkets | |

| Other Channels |

Key Questions Answered in the Report

What is the projected value of Brazil pet veterinary diets by 2031?

The category is forecast to reach USD 2.44 billion by 2031, rising from USD 1.48 billion in 2026 at a 10.77% CAGR over 2026-2031.

Which sub product category leads revenue in Brazil pet veterinary diets?

Digestive Sensitivity was the largest sub product in 2025 with 17.7% share, supported by frequent gastrointestinal conditions and longer treatment use.

Why are cats growing faster than dogs in therapeutic pet nutrition?

Cats are projected to grow at 12.1% CAGR because feline adoption is rising quickly in urban apartments and because cats show strong demand in renal, urinary, and obesity-related care.

Which sales channel is changing fastest for prescribed pet diets in Brazil?

The Online Channel is the fastest-growing route with a projected 12.8% CAGR, helped by refill convenience, telemedicine-enabled continuity, and stronger logistics investment.

Which regions are most important for demand?

The Southeast is the largest regional base, supported by a 46% share of Brazil's broader pet market, while the South remains the second key region for both demand and production.

How are leading companies competing in this category?

Companies are competing through clinical credibility, research support, product launches, and logistics expansion, with Mars, Incorporated, Nestle S.A. (Purina), PremieRpet S.A., Farmina Pet Foods Holding N.V., and Virbac SA all strengthening their positions through those routes.

Page last updated on: