Brazil Omega-3 Supplements Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

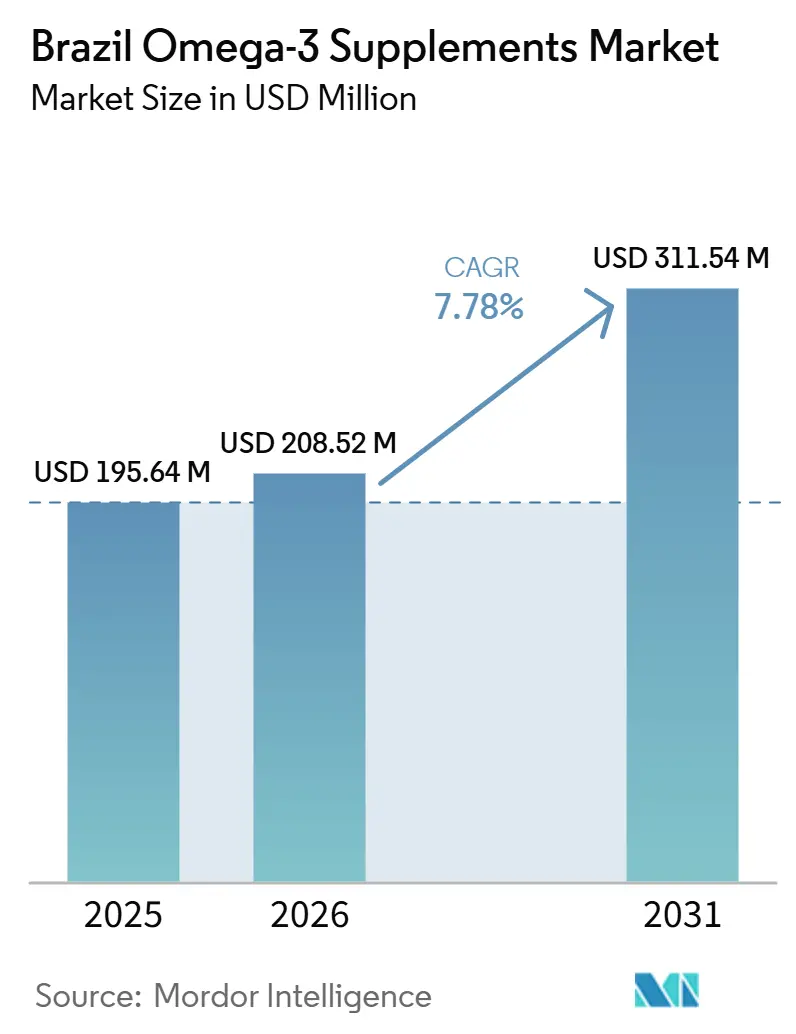

| Base Year Market Size (2025) | USD 195.64 Million |

| Market Size (2026) | USD 208.52 Million |

| Market Size (2031) | USD 311.54 Million |

| Growth Rate (2026 - 2031) | 7.78% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Omega-3 Supplements Market Analysis by Mordor Intelligence

The Brazil omega-3 supplements market size was valued at USD 195.64 million in 2025 to USD 208.52 million in 2026, and is forecast to reach USD 311.54 million by 2031, advancing at a CAGR of 7.78% over 2026-2031. The Brazil omega-3 supplements market remains closely tied to cardiovascular care because heart disease affected 14 million Brazilians and accounted for nearly 32.00% of total deaths in the country[1]Source: Brazilian Society of Cardiology, “Annual Report on Cardiovascular Disease Burden in Brazil,” Brazilian Society of Cardiology, cardiol.br. That disease burden keeps omega-3 closer to a routine physician-guided product than a purely optional wellness purchase. Post-pandemic health habits also kept repeat buying in place, especially among urban middle-income households that now treat supplements as part of everyday self-care. The Brazil omega-3 supplements market is also benefiting from wider access through pharmacies and online retail, while domestic factory projects are giving local brands more room to broaden format choice and speed up launches. Import dependence and new label compliance work still pressure margins, but the aging population and rising pediatric awareness continue to widen the long-run consumer base for the Brazil omega-3 supplements market.

Key Report Takeaways

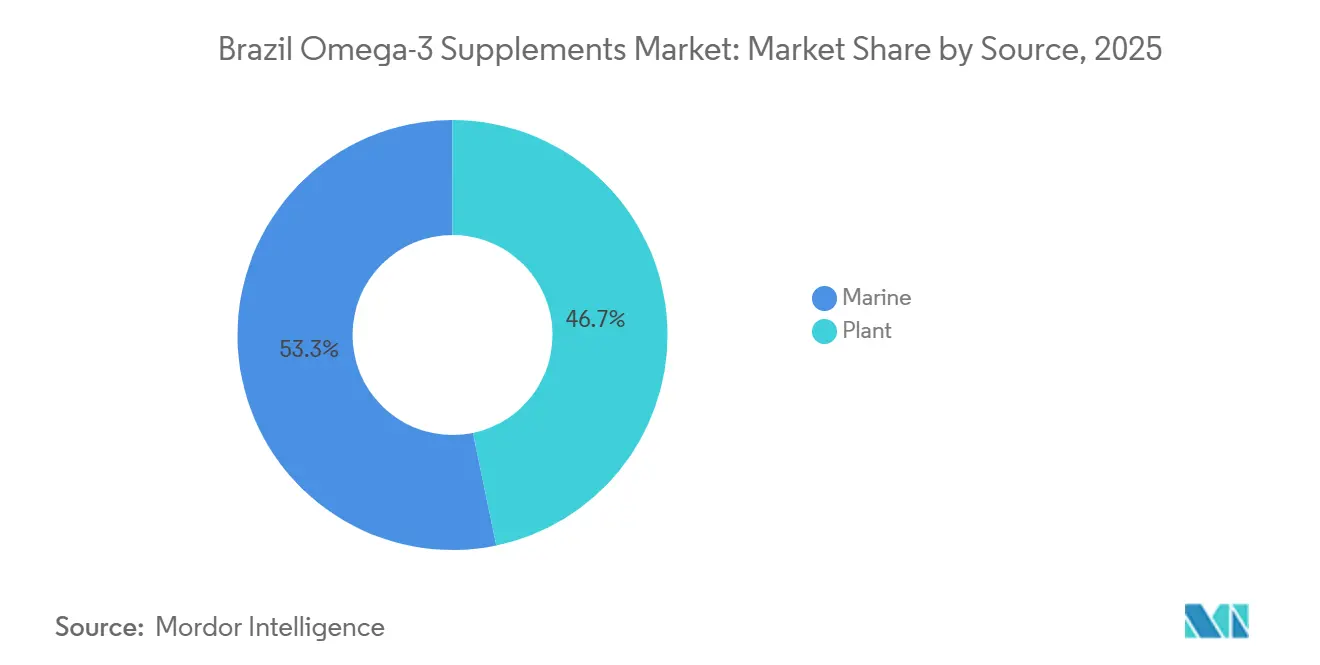

- By source, marine-derived omega-3 held 53.27% of revenue in 2025, while plant-based products are projected to expand at 8.84% CAGR through 2031.

- By form, softgels accounted for 56.21% of revenue in 2025, while capsules are forecast to grow at 8.25% CAGR through 2031.

- By end user, adults held 85.14% of demand in 2025, while children are expected to advance at 9.01% CAGR through 2031.

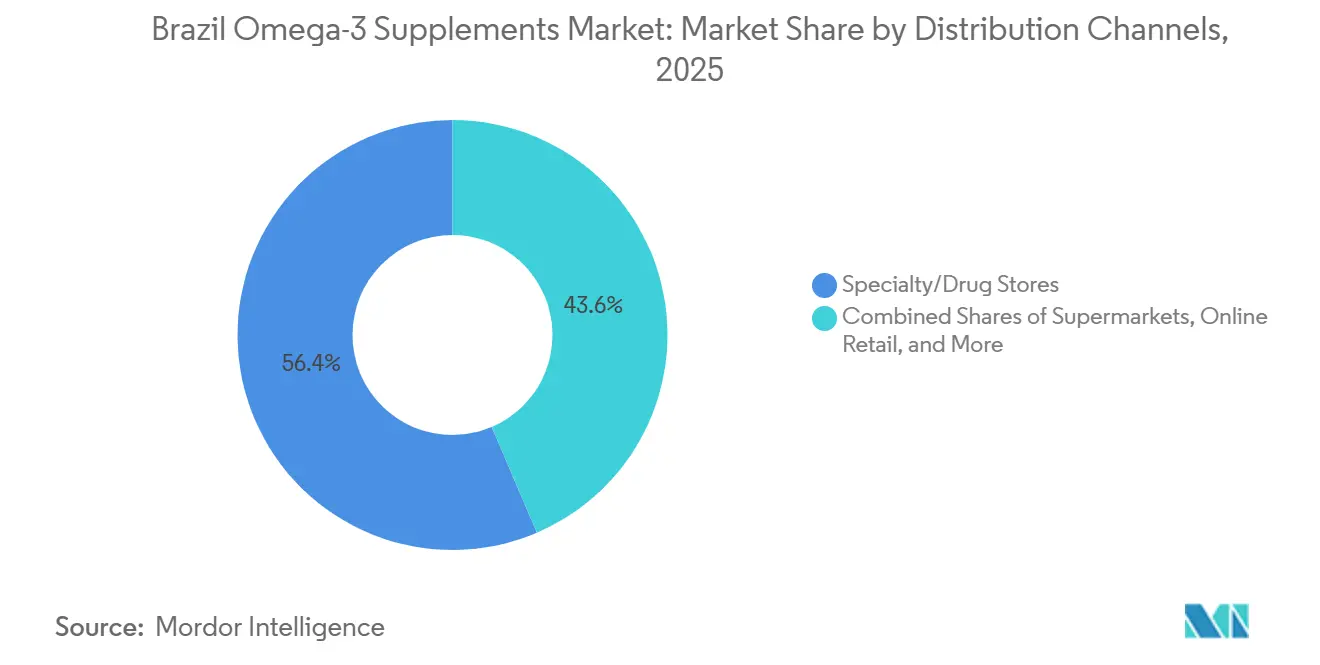

- By distribution channel, specialty and drug stores held 56.42% of revenue in 2025, while online retail is projected to grow at 8.67% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Brazil Omega-3 Supplements Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Consumer Awareness Of Cognitive and Heart Healthcare | +2.0% | National; concentrated in São Paulo, Rio de Janeiro, and Belo Horizonte urban corridors | Long term (≥ 4 years) |

| Expansion Of Sports Nutrition And Active Lifestyle Trends | +1.5% | São Paulo, Rio de Janeiro, Curitiba, and Brazil's fast-growing interior fitness markets | Medium term (2-4 years) |

| Increasing Aging Population Driving Sustained Demand For Overall Health Supplements | +1.3% | National; accelerated in São Paulo, Minas Gerais, and Rio Grande do Sul | Long term (≥ 4 years) |

| Increasing Availability Of Vegan And Sustainable Omega-3 Sources | +1.2% | São Paulo and Southern Brazil; spill-over to Northeast coastal cities | Medium term (2-4 years) |

| Expansion Of Domestic Supplement Manufacturing | +0.9% | São Paulo state (Valinhos, Campinas), Paraná, and Rio Grande do Sul industrial clusters | Medium term (2-4 years) |

| Rapid Growth Of E-Commerce And Digital Health Retailing | +1.4% | National; deepest penetration in Southeast and South Brazil | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Consumer Awareness of Cognitive and Heart Healthcare

Brazil's cardiovascular burden gives the Brazil omega-3 supplements market a steady base of medically guided demand. Heart disease affected 14 million Brazilians and accounted for nearly 32.00% of total deaths, which keeps physician recommendation pathways highly relevant for this category. Growth is now also being supported by stronger consumer interest in cognitive health, especially in products with DHA positioning for brain function and mood support. This matters because the category is no longer being framed only as a heart health purchase. The International Society of Sports Nutrition stated in January 2025 that omega-3 supplementation may reduce post-exercise muscle soreness and may provide neuroprotective benefits for people exposed to repeated head impacts[2]Source: International Society of Sports Nutrition, “ISSN Position Stand: Omega-3 Polyunsaturated Fatty Acids,” Journal of the International Society of Sports Nutrition, pmc.ncbi.nlm.nih.gov. That broader scientific framing gives brands in the Brazil omega-3 supplements market more room to speak to brain, recovery, and long-term wellness needs in the same purchase cycle.

Expansion of Sports Nutrition and Active Lifestyle Trends

The Brazil omega-3 supplements market is gaining support from a wider sports nutrition culture that now reaches beyond regular gym users. Omega-3 is increasingly sold alongside protein and creatine as a routine recovery product, helping it enter everyday supplement baskets rather than remain in a single-condition niche. The International Trade Administration reported in 2025 that Brazil's sports nutrition sales are estimated to exceed USD 1 billion, with clean-label products and functional ingredients gaining ground among younger, health-conscious consumers [3]Source: International Trade Administration, “Brazil Dietary Supplements and Sports Nutrition,” International Trade Administration, trade.gov. The ISSN position stand published in January 2025 also reinforced omega-3's role in muscle recovery, joint support, and cardiovascular markers in athletic populations. Fitness infrastructure growth in cities such as Goiânia, Campinas, and Ribeirão Preto is widening the reach of performance-oriented supplements. As that access improves, the Brazil omega-3 supplements market is moving closer to a recurring lifestyle purchase for younger adults.

Increasing Aging Population Driving Sustained Demand For Overall Health Supplements

An aging consumer base gives the Brazil omega-3 supplements market a durable demand floor. Brazil's population aged 60 and above exceeded 15.00% of the total by 2025, and this cohort is projected to surpass 35 million by 2030. Older consumers tend to show stronger repurchase behavior in omega-3 because cardiovascular, joint, and cognitive claims fit ongoing daily health management. Demand is also concentrated in Rio Grande do Sul, São Paulo, and Minas Gerais, where the pharmacy network and specialty supplement access are more developed. That alignment between older consumers and stronger retail infrastructure supports premium formats, combination products, and repeat physician-led purchases. It also shapes household habits because grandparents who use supplements often influence adoption within multi-generational families, which helps extend category familiarity to younger age groups.

Increasing Availability Of Vegan And Sustainable Omega-3 Sources

Vegan and sustainable formulations are giving the Brazil omega-3 supplements market a second source story beyond traditional fish oil. Algae-derived products are now more visible in specialty retail, and domestic brands are using them to appeal to consumers who want plant-based, contaminant-free, and sustainability-led products. This matters because controlled bioreactor cultivation reduces exposure to fishery swings and lowers the perception of purity risk that can affect marine-based products. Plant-based formulations also reduce the fishy aftertaste issue that causes some users to stop supplementation after a short period. ANVISA's RDC 843/2024 updated the safety assessment and authorization pathway for novel food ingredients, which supports a more workable route for next-generation inputs in this space. As a result, the Brazil omega-3 supplements market is gaining a source segment that solves both perception and supply concerns at the same time.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Dependence On Imported Raw Materials | -1.4% | National; most acute for encapsulators in São Paulo and Paraná processing hubs | Long term (≥ 4 years) |

| Strict Regulatory Requirements | -0.9% | National, affecting ANVISA registration timelines uniformly across all categories | Medium term (2-4 years) |

| Competition From Other Dietary Supplements | -0.7% | National; most pronounced in specialty and drug store channels with limited shelf space | Short term (≤ 2 years) |

| Supply Chain Volatility For Marine Ingredients | -0.8% | Global sourcing origins (Peru, Chile, Norway); impact most acute for marine oil-dependent manufacturers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Dependence on Imported Raw Materials

Import exposure remains one of the clearest structural limits on the Brazil omega-3 supplements market. The category relies on foreign supply for more than 85.00% of its raw marine omega-3 oil needs, which leaves local encapsulators exposed to currency swings, freight costs, and ocean-linked supply shifts. That exposure becomes more difficult when anchovy catch variability affects Peru and Chile, because ingredient pricing can change before manufacturers have time to reset retail prices. The result is a market where many domestic players act more as encapsulators and brand owners than as integrated producers. GOED reported in 2025 that the global EPA and DHA supply chain was recovering from earlier contraction, but that recovery still does not remove Brazil's dependence on imported marine inputs. Smaller operators in the Brazil omega-3 supplements market face the highest risk because they are less likely to hold long-term supply agreements or absorb extra certification and sourcing costs.

Strict Regulatory Requirements

Regulation also slows parts of the Brazil omega-3 supplements market even when demand conditions are favorable. ANVISA's supplement framework combines detailed ingredient rules, claim limits, and labeling obligations, which raises the compliance threshold for every producer and importer. The 24-month label adaptation period tied to the 2025 normative updates creates a real workload because existing registered products need reformulation checks, packaging changes, and claim reviews within a fixed window. Larger multinational firms can spread those costs across wider portfolios, while smaller domestic brands face a heavier burden on a per-product basis. Shelf competition adds another layer of pressure because vitamins, minerals, collagen, and protein supplements target many of the same health narratives and the same shopper budget. That means regulatory cost inflation can push some consumers toward lower-priced alternatives even when interest in omega-3 remains intact.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Marine Dominance Faces a Structural Challenger

Marine-derived omega-3 held 53.27% of the Brazil omega-3 supplements market share in 2025, reflecting the category's long-standing reliance on fish oil and the familiarity that Brazilian consumers already have with this format. Fish oil still benefits from a lower cost per milligram of EPA and DHA than algal alternatives, which supports broad placement in mass drug store and supermarket channels. Established supply links with Peruvian and Chilean refiners also help preserve marine products as the default choice for many mainstream brands. Quality-tested products have additionally built a trust layer in specialty retail, where purity and traceability help justify premium pricing.

Plant-based products are forecast to grow at 8.84% CAGR from 2026 to 2031, making them the fastest-growing source segment in the Brazil omega-3 supplements market. This growth is being supported by vegan lifestyle adoption, sustainability preferences, and the appeal of controlled cultivation that is not tied to fishery restrictions. The Brazil omega-3 supplements industry is also seeing plant-based products framed as a cleaner option because they avoid common concerns around marine contaminants and odor. That positioning matters for consumers who once tried fish oil and stopped because of taste or smell. The source mix is therefore shifting from a simple fish oil category to a two-track structure where plant-based products solve a different set of consumer concerns.

By Form: Softgels Define the Category, Capsules Redefine Growth

Softgels accounted for 56.21% of revenue in 2025, which kept them as the dominant delivery format in the Brazil omega-3 supplements market. Their leading position comes from familiarity, easy daily use, and good oxygen barrier protection that helps preserve oil quality. Softgels also fit well with the domestic encapsulation base that already supports a large share of local supplement output. This makes them the safest format for scale, repeat purchases, and shelf presence.

Capsules are projected to grow at 8.25% CAGR through 2031, and this makes them one of the clearest format opportunities within the Brazil omega-3 supplements market size. Growth is being driven by enteric coating and micro-encapsulation work that reduces fishy aftertaste, which is one of the main reasons users stop taking omega-3 on a regular basis. Gummies and liquid products address a different barrier because they appeal to people who dislike swallowing larger units, especially children and some adult wellness buyers. The Brazil omega-3 supplements industry is therefore moving toward a more diversified format mix rather than relying on softgels alone. Vitamedic's announced BRL 100 million investment in gummies, powders, gels, capsules, and sachets also shows how local manufacturers are treating format breadth as a core growth lever.

By End User: Adults Anchor Revenue, Children Accelerate Volume

Adults represented 85.14% of demand in 2025, which kept them as the clear revenue anchor for the Brazil omega-3 supplements market. This base is linked to physician guidance around cardiovascular, cognitive, and joint health, which gives adult purchases a more routine and less experimental pattern. Adult buyers also tend to show stronger long-term adherence than many other supplement users. That matters because value in this category depends not just on first purchase, but on steady replenishment.

Children are expected to grow at 9.01% CAGR through 2031, and this points to one of the strongest forward opportunities in the Brazil omega-3 supplements market size. The segment is expanding from a low base because only an estimated 30.00% to 40.00% of Brazilian parents regularly supplement their children, while usage exceeds 60.00% in the United States and Europe. Product design is helping unlock this gap, especially through easier-to-consume formats and more direct cognitive development positioning. Maternal and child-focused combinations, such as prenatal formulas with omega-3 DHA, also simplify the purchase decision and keep the category close to family health management. At the same time, adults aged 25 to 40 are increasingly using omega-3 in a proactive way for performance and focus, which broadens the adult base beyond reactive cardiovascular care.

By Distribution Channels: Specialty Stores Lead, Digital Commerce Disrupts

Specialty and drug stores held 56.42% of the Brazil omega-3 supplements market share in 2025, which reflects the importance of pharmacist guidance and health-led purchase decisions in this category. These outlets benefit from a trust advantage because omega-3 is often bought for cardiovascular, prenatal, and joint health rather than for impulse use. The setting also supports stronger average transaction value, since shoppers are more willing to choose registered and premium products in pharmacy environments. This keeps physical health retail central to current value capture.

Online retail is projected to grow at 8.67% CAGR through 2031, and channel expansion is closely linked to the wider shift in the Brazil omega-3 supplements market. Brazil's e-commerce sector reached USD 36.3 billion in 2025 and served 94 million online shoppers, which gives supplement brands a very large digital audience to target. Data presented at Brazil's 5th Supplements Forum in April 2026 showed digital platforms' share of total supplement sales rising from 3.70% to 6.10% within one year. Supermarkets and hypermarkets still play a useful supporting role for entry-level SKUs, especially for price-sensitive shoppers. At the same time, regulatory attention on unregistered products sold through marketplaces is likely to favor compliant brands that already have stronger control over listings and claims.

Geography Analysis

Brazil held the largest country position within the wider LAMEA omega-3 supplements space, and that leadership underpins the scale of the Brazil omega-3 supplements market through the forecast period. The country also serves as the main regional entry point for multinational supplement companies that want a commercial base in Latin America. This role matters because companies often use Brazil as the first market before extending operations to Argentina, Colombia, and Chile. That regional hub position keeps investment activity and brand launches concentrated in the Brazil omega-3 supplements market.

Demand inside Brazil is uneven and follows income, healthcare access, and retail infrastructure. The Southeast, especially São Paulo, Rio de Janeiro, and Minas Gerais, accounts for the largest national share of consumption because it combines higher disposable income with dense pharmacy and specialty store networks. São Paulo also concentrates much of the domestic supplement manufacturing base, including encapsulation and packaging operations that support faster supply response. The South region, especially Paraná, Santa Catarina, and Rio Grande do Sul, shows strong per-capita supplement spending and includes important local producers. Rio Grande do Sul stands out because its older population profile aligns well with omega-3 demand for cardiovascular, cognitive, and joint health.

The Northeast and Center-West remain lower-penetration areas within the Brazil omega-3 supplements market, but they also represent a meaningful growth corridor. Logistics costs and lower average income have historically limited specialty product availability in these regions. E-commerce is helping close that access gap as delivery networks widen and digital buying becomes more common. As online availability improves, these regions are likely to contribute a larger share of national volume growth between 2026 and 2031.

Competitive Landscape

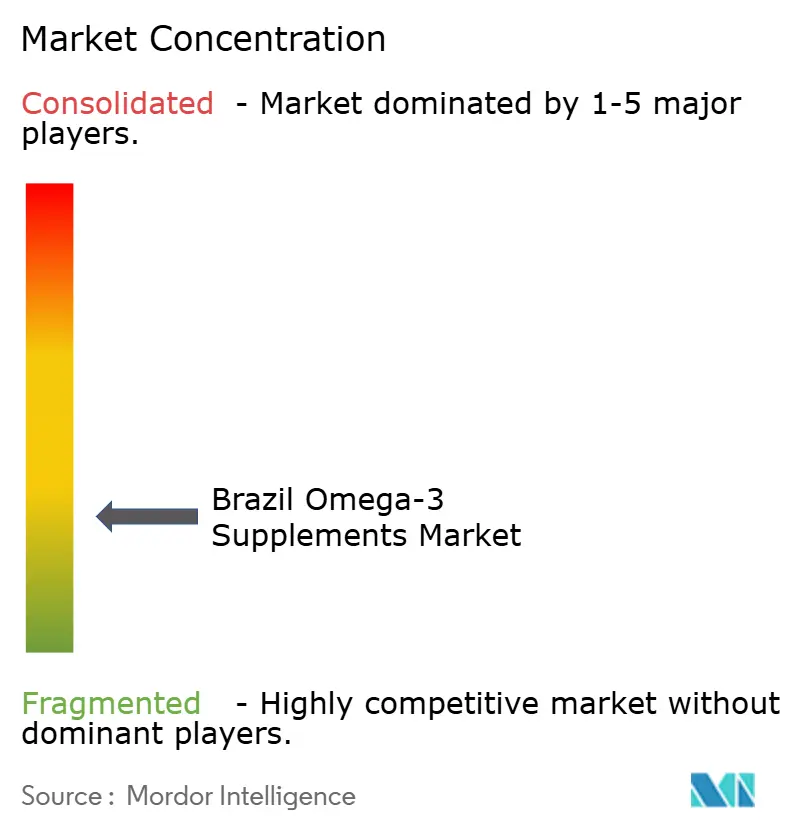

The Brazil omega-3 supplements market has a moderately consolidated structure, with multinational groups and agile domestic brands competing without a single company controlling the field. Nestlé through Nature's Bounty, Reckitt, Abbott Nutrition, and Amway remain important because they combine recognized branding with established distribution across mass and specialty channels. Domestic brands such as Vitafor, Maxinutri, Cimed Group, and Essential Nutrition compete by moving faster in product design, localization, and digital sales. This creates a market where scale matters, but speed and specialization also matter.

Competitive strategy in the Brazil omega-3 supplements market is split along clear lines. Multinationals generally lean on regulatory resources, broad portfolios, and brand familiarity, while domestic firms are investing more directly in capacity, formats, and narrower health claims. Vitafor's OMEGAFOR extensions, including eye health and vitamin-enriched variants, show how local players are trying to avoid simple price competition with plain fish oil products. Catarinense Pharma's Fontívia launch also points to a different route, since it targets nutritionists, nutrologists, and specialty channels rather than depending only on mass pharmacy traffic. Evonik's AvailOm powder launch in Brazil adds another layer because it enables contract manufacturers to move omega-3 into sports nutrition and functional food applications that are still underdeveloped locally.

The Brazil omega-3 supplements market still has room for white space in microencapsulation, enteric coating, and combined-functionality products that pair omega-3 with ingredients such as vitamin D, curcumin, or lutein. That white space matters because many companies are not only chasing volume, they are also trying to protect margins with more specialized formats. Domestic factory expansion by players such as Maxinutri and Vitamedic supports this direction because wider local capacity helps reduce launch times and broaden the SKU mix. Regulatory discipline remains an important competitive filter, which means brands with stronger compliance systems are likely to keep an advantage as the category grows.

Brazil Omega-3 Supplements Industry Leaders

Vitafor

Amway Corporation

Abbott Nutrition

NOW Health Group

Bayer AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Data presented at Brazil's 5th Supplements Forum (Sincofarma SP) confirmed that supplement sales had grown fivefold in five years, major retail chains now hold 59% of total supplement sales (up from 48%), and digital platforms' share rose from 3.7% to 6.1% in a single year, with ANVISA's enforcement spotlight on Mercado Livre for unregistered products signaling regulatory tightening in the online channel.

- March 2025: Nordic Naturals, in partnership with agency Laughlin Constable, launched the "The Power of Omega-3" national campaign on Global Omega-3 Day, repositioning omega-3 as a multi-indication lifelong wellness supplement spanning heart, brain, and immune health through integrated linear TV, streaming, social media, and experiential activations.

- March 2025: Businessman Eike Batista has entered the agri-food market by investing in the online sale of calcified marine algae capsules, known commercially as Elysium. The product, recognized by Brazil's National Health Surveillance Agency (Anvisa).

Brazil Omega-3 Supplements Market Report Scope

| Marine |

| Plant |

| Softgels |

| Capsules |

| Liquid |

| Gummies |

| Others |

| Adults |

| Children |

| Supermarkets/Hypermarkets |

| Specialty and Drug Stores |

| Online Retailers |

| Other Distribution Channels |

| By Source | Marine |

| Plant | |

| By Form | Softgels |

| Capsules | |

| Liquid | |

| Gummies | |

| Others | |

| By End User | Adults |

| Children | |

| By Distribution Channels | Supermarkets/Hypermarkets |

| Specialty and Drug Stores | |

| Online Retailers | |

| Other Distribution Channels |

Key Questions Answered in the Report

What is driving demand for omega-3 supplements in Brazil?

Demand is being supported by cardiovascular health needs, broader cognitive wellness interest, aging consumers, and stronger digital access. The category was valued at USD 195.64 million in 2025 to USD 208.52 million in 2026 and is forecast to reach USD 311.54 million by 2031 at a 7.78% CAGR.

Which source type leads sales in Brazil?

Marine-derived omega-3 led sales with a 53.27% revenue share in 2025 because fish oil remains familiar, widely available, and cost efficient for mainstream channels.

Why are plant-based omega-3 products growing faster?

Plant-based products are projected to grow at 8.84% CAGR through 2031 because they align with vegan demand, sustainability preferences, controlled cultivation, and cleaner taste positioning.

What makes online retail important for this category?

Online retail is forecast to grow at 8.67% CAGR through 2031 as Brazil had 94 million online shoppers and USD 36.3 billion in e-commerce sales in 2025, which expands category reach well beyond core urban pharmacy corridors.

Page last updated on: