Brazil Last Mile Delivery Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

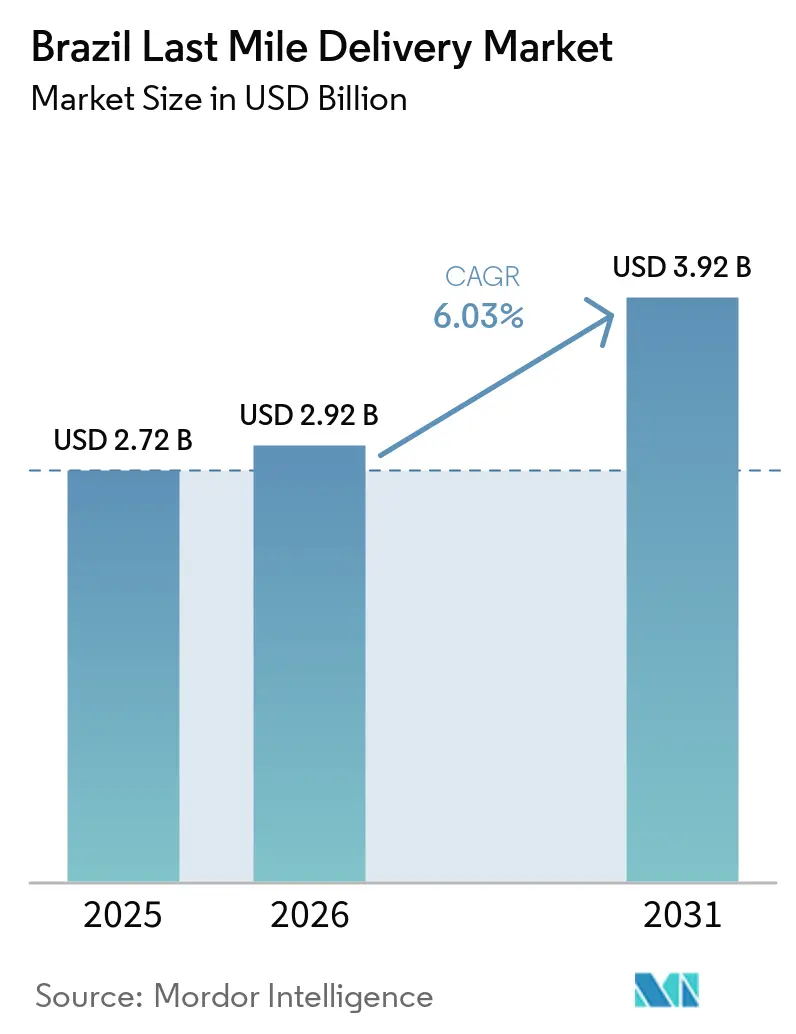

| Base Year Market Size (2025) | USD 2.72 Billion |

| Market Size (2026) | USD 2.92 Billion |

| Market Size (2031) | USD 3.92 Billion |

| Growth Rate (2026 - 2031) | 6.03% CAGR |

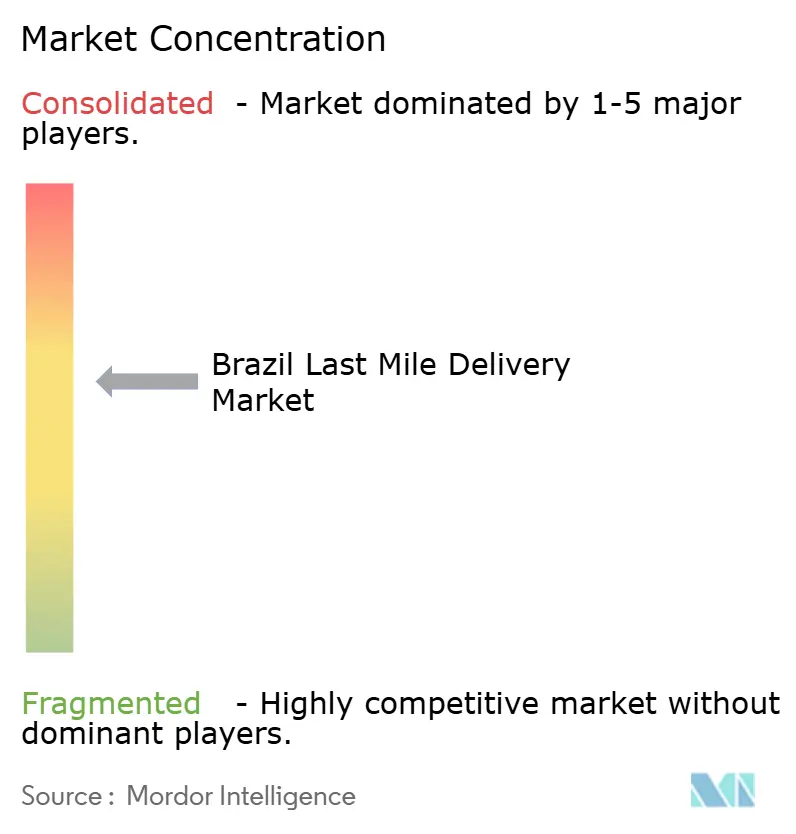

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Brazil Last Mile Delivery Market Analysis by Mordor Intelligence

The Brazil last-mile delivery market size was valued at USD 2.72 billion in 2025 and is estimated to grow from USD 2.92 billion in 2026 to reach USD 3.92 billion by 2031, at a CAGR of 6.03% during the forecast period (2026-2031).

Continued double-digit expansion of national e-commerce, route-densification across the Southeast corridor, and aggressive micro-fulfillment roll-outs by vertically integrated marketplaces are reinforcing structural demand for time-critical deliveries. Same-day services are advancing faster than the Brazil last-mile delivery market average as urban shoppers demand sub-hour fulfillment windows. At the same time, AI-driven routing platforms trim fuel burn and idle time, partially insulating operators from diesel and labor inflation. At the same time, customer-to-customer parcel flows are scaling on the back of peer-resale and gig-courier applications, introducing fresh competitive pressure but also diversifying revenue. Heightened foreign capital, exemplified by Meituan’s USD 1 billion Keeta launch and DHL’s fleet-electrification program, signals confidence that wider tax incentives and multimodal concessions will gradually loosen long-standing logistics bottlenecks.

Key Report Takeaways

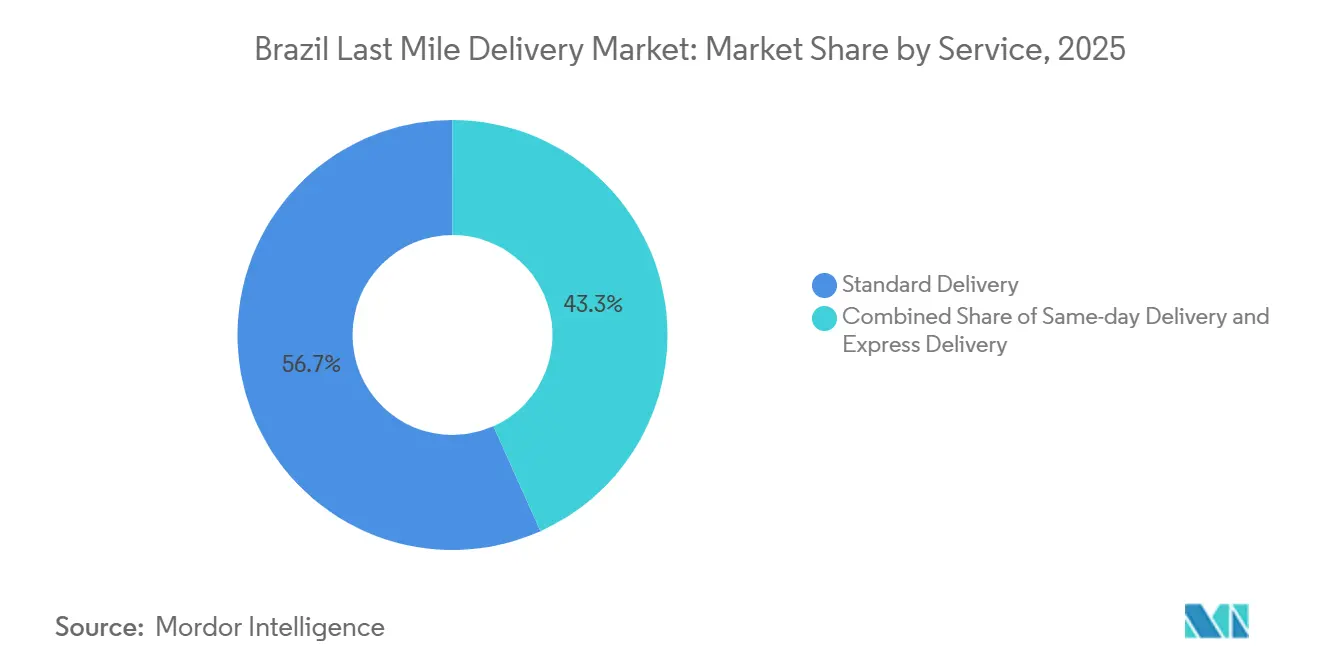

- By service, standard delivery led with 56.71% of Brazil last mile delivery market share in 2025, while same-day delivery is projected to expand at a 7.68% CAGR through 2031.

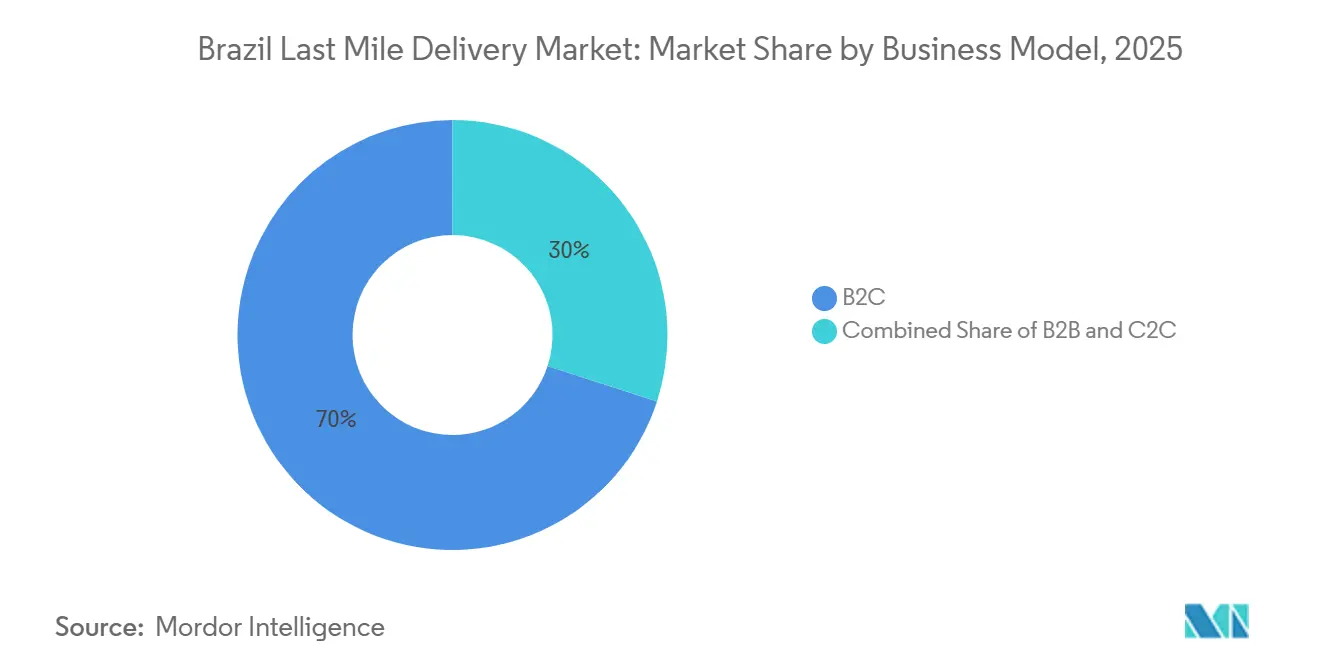

- By business model, the B2C segment accounted for 70% market size of 2025 volumes, whereas C2C is the fastest-growing flow, advancing at 7.80% CAGR to 2031.

- By end-user industry, e-commerce retail captured 46.07% market share of demand in 2025, while healthcare is forecast to post the strongest growth at 7.96% CAGR through 2031.

- By region, the Southeast commanded 48.6% Brazil last-mile delivery market share in 2025, yet the North is set to climb at a 6.51% CAGR over the same horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Brazil Last Mile Delivery Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive E-Commerce GMV Growth Post-COVID | +1.2% | National, led by Sao Paulo & Rio de Janeiro | Medium term (2-4 years) |

| Rapid Urbanization Boosting Delivery Density | +0.9% | Southeast & South; rising in Northeast capitals | Long term (≥ 4 years) |

| Fulfillment-Center Boom Around Tier-2 Cities | +0.8% | Northeast, Central-west, Minas Gerais, Goias, Bahia | Medium term (2-4 years) |

| AI-Driven Route-Optimization Platforms Adoption | +0.7% | Nationwide early adopters | Short term (≤ 2 years) |

| Q-Commerce Expansion in Secondary Cities | +1.0% | 240+ interior municipalities | Short term (≤ 2 years) |

| EV-Friendly Tax Incentives for Delivery Fleets | +0.5% | Highest uptake in Southeast & South | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Explosive E-Commerce GMV Growth Post-COVID

Brazil’s online GMV jumped 10.3% to BRL 259.8 billion (USD 52 billion) in 2026, adding 21.9 million incremental parcels and accelerating consumer expectations for sub-24-hour fulfillment[1]“E-commerce Gross Merchandise Value and Order Volumes 2025-2026,” ABIACOM, abiacon.com.br. Carriers countered by co-locating micro-fulfillment nodes within 15 km of dense urban cores, enabling MercadoLibre to pledge 48-hour delivery on 75% of orders. Store-as-warehouse strategies from Magalu and regional retailers are trimming last-mile distance, squeezing independent carriers that lack real estate scale.

Rapid Urbanization Boosting Delivery Density

Brazil's urbanization, with 87.6% of residents in cities, drives high last-mile delivery volumes, especially in Sao Paulo and Rio de Janeiro. Secondary cities like Belo Horizonte and Curitiba are seeing above-average parcel demand growth. High-density urban areas enable cost reductions through route optimization but face challenges like traffic congestion. Motorcycle couriers are increasingly used for agility, though inconsistent municipal regulations create compliance issues. Sao Paulo's Lei 18.349 mandates GPS tracking and safety protocols for moto-couriers, highlighting regulatory fragmentation[2]"Brazil Urban Population Statistics." IBGE, IBGE.GOV.BR. Nevertheless, peak-hour traffic routinely stretches delivery cycles to six hours, triggering heavier reliance on motorcycle couriers despite uneven municipal safety mandates.

Fulfillment-Center Boom Around Tier-2 Cities

Logistics real estate in Brazil's Northeast is growing at 9.3% annually, driven by e-commerce players decentralizing inventory to reduce costs and transit times. MercadoLibre, Amazon, and Shopee occupy over 775,000 square meters of warehouse space, with MercadoLibre aiming to cut shipping costs by up to 55% by 2025. Developer Log is investing heavily in the region, with major projects in Fortaleza and Joao Pessoa targeting high pre-lease occupancy. Brazil's 2025 tax reform and inadequate road infrastructure are driving a shift toward proximity to consumers and shorter last-mile deliveries. Tier-2 cities like Campinas and Feira de Santana are emerging as fulfillment hubs, reducing reliance on Sao Paulo's congested corridors.

AI-Driven Route-Optimization Platforms Adoption

Brazilian logistics operators are increasingly adopting AI-powered route-optimization platforms to improve delivery efficiency and reduce costs. Early adopters have reported up to 7% improvements in on-time deliveries and 40% cost savings. Platforms like SimpliRoute and RoutEasy dominate the market, offering dynamic routing solutions tailored to urban traffic challenges. Rising diesel prices and labor costs are driving adoption, but smaller carriers face barriers due to high subscription fees and integration complexities. This trend may consolidate market share among larger, tech-enabled operators.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Severe Metropolitan Traffic Congestion | −0.6% | Sao Paulo, Rio de Janeiro, Curitiba, Porto Alegre | Short term (≤ 2 years) |

| High Fuel and Labor Cost Inflation | −0.9% | Nationwide; acute in North & Northeast | Medium term (2-4 years) |

| Patchy Municipal Rules on Motorcycle Couriers | −0.3% | Major metros with divergent ordinances | Short term (≤ 2 years) |

| Inadequate Cold-Chain Nodes in Amazon & North | −0.5% | Amazonas, Para, Acre | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Severe Metropolitan Traffic Congestion

Traffic congestion in Sao Paulo and Rio de Janeiro is significantly increasing delivery times and costs, with federal highways largely rated as poor. Carriers are adopting measures like nighttime deliveries and micro-fulfillment centers, but noise ordinances and security concerns limit their effectiveness. Infrastructure investments have declined, and legal challenges are delaying key projects like the Ferrograo railway. These factors are expected to sustain congestion issues through 2028. Operators with dense urban networks and AI-driven routing are better positioned to navigate these challenges.

High Fuel and Labor Cost Inflation

Diesel imports 20% of national consumption, pegging domestic pump prices to volatile forex, pushing February 2025 rates to BRL 6.47 (USD 1.16) per liter[3]“Diesel Fuel Prices February 2025,” ANP, anp.gov.br. Concurrently, platform-driven bidding wars lifted minimum courier fees to BRL 7.50 (USD 1.35), squeezing independents into consolidation or exit despite a temporary BRL 0.32 (USD 0.05) subsidy rolled out in 2026. Diesel prices and rising delivery rates are squeezing margins for independent carriers in Brazil. Temporary government subsidies and rising labor costs are further complicating the market. Regional disparities in delivery fees and inflationary pressures are driving smaller operators out of the market. This is expected to accelerate M&A activity, with larger players acquiring distressed carriers to secure capacity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Same-Day Delivery Outpaces Standard Amid Urban Density Push

Standard delivery held 56.71% of Brazil last mile delivery market share in 2025, illustrating continued price sensitivity among non-urgent shoppers. Same-day services, however, are forecast to accelerate at 7.68% CAGR, the highest among service types, as dense urban clusters and micro-fulfillment penetration shorten physical distance to the end consumer. Amazon Now’s 15-minute promise in eight cities and iFood-Uber’s bundled subscription at BRL 21.90 (USD 3.95) reflect how marketplaces absorb logistics costs to convert frequency into loyalty.

The competitive schism is widening: vertically integrated platforms leverage scale to offer near-real-time delivery, while independents pivot toward express and scheduled slots where margin protection remains feasible. AI-enabled routing has trimmed same-day variable expense by roughly 20%, further reinforcing penetration into high-frequency categories such as grocery and beauty.

By Business Model: C2C Gains Traction as Peer Resale and Gig Platforms Expand

B2C channels held 70% of Brazil last mile delivery market size in 2025, yet customer-to-customer flows are growing the fastest at 7.80% CAGR as OLX, Enjoei, and instant-courier apps let individuals bypass conventional carriers. Lalamove’s driver pool in Rio ballooned 253% between 2024 and 2025, underscoring latent capacity unleashed by flexible onboarding mechanisms.

B2B demand, while niche, secures stable contractual throughput. Jadlog’s five-hub expansion added 24,000 m² and 34 docks, supporting corporate shipping during Black Friday peaks. Even so, the rising C2C slice is fragmenting volumes, eroding pricing discipline, and compelling established firms to differentiate via value-added tracking or returns handling to safeguard Brazil last mile delivery market size gains.

By End-User Industry: Healthcare Fastest-Growing amid Cold-Chain Investments

E-commerce retail absorbed 46.07% market share of parcels in 2025, followed by fashion, beauty, furniture, and consumer electronics, which each impose distinct handling profiles. Healthcare shipments, though smaller, are poised to climb 7.96% CAGR to 2031 as telemedicine and direct-to-patient models flourish, driving specialized refrigerated-transport demand. The share of Brazil last mile delivery market size tied to healthcare is forecast to double from 2026 to 2031[4]"Drought-Related Losses Amazonas." UFAM, ufam.edu.br..

Persistent cold-chain gaps north of the 10th parallel inflate logistics costs to a quarter of the final retail price, spurring opportunity for dedicated 2-8 °C fleets. MercadoLibre’s 2025 acquisition of Cuidamos Farma telegraphs a strategic pivot into pharmaceuticals, foreshadowing more vertical integration as regulations slowly codify temperature-control standards.

Geography Analysis

In 2025, the Southeast region held a dominant 48.6% market share, bolstered by the e-commerce demand and fulfillment infrastructure concentrated in Sao Paulo and Rio de Janeiro. Its dense roadway lattice and Santos port gateway allow sub-24-hour regional delivery, but congestion, diverse municipal tolling, and driver-fee inflation erode profitability. Destination-based taxation introduced in 2025 has spurred land-price escalation for peri-urban warehousing, with vacancy hovering below 5%, signaling sustained entry barriers for newcomers.

The North region is rapidly emerging as the fastest-growing area, boasting a 6.51% CAGR through 2031, fueled by strategic infrastructure investments and the decentralization of fulfillment centers. The Northeast is emerging as a cost-efficient staging ground as real estate developers pre-lease up to 90% of projects pre-completion. MercadoLibre and Shopee occupy more than 775,000 m² combined, cutting transit times by 36 hours versus shipping from Sao Paulo. DHL’s Brasilia hub further positions the Central-West as a bridge between agribusiness exports and rising intra-regional e-commerce demand.

Finally, the North’s logistical struggle with expensive cold-chain lanes and river-depth volatility should gradually subside as Madeira and Tapajos concessions reach financial close. Yet protracted indigenous litigation may delay full impact until after 2028, keeping premium margins intact for specialized players capable of multimodal orchestration.

Competitive Landscape

The Brazil last mile delivery market is moderately fragmented. MercadoLibre’s USD 6.8 billion 2025 logistics outlay and Amazon’s alliance with Rappi illustrate deep vertical integration that compresses merchant shipping fees by up to 40%. Together, they and Jadlog controlled upward of 40% of national volumes in 2025. Correios, while still influential for nationwide coverage, faces capital constraints that curtail technology upgrades.

Disruptive entrants such as Meituan’s Keeta and gig models from Uber and Lalamove are intensifying competition in urban cores, amplifying pressure on mid-tier independents. Technology remains the primary battleground: operators adopting AI routers and SaaS compliance dashboards unlock 10-15% fuel savings and faster SLA adherence. Meanwhile, FedEx’s January 2026 withdrawal underscores how global integrators face structural cost disadvantages without localized micro-fulfillment.

Regulatory fragmentation around motorcycle courier safety and impending carbon-pricing discussions incentivize scale players to lobby for unified frameworks, potentially widening the moat against small fleets. Cold-chain and healthcare logistics represent the chief white space, particularly in Amazonia, where incumbent under-investment and high spoilage costs permit premium pricing for temperature-controlled assets.

Brazil Last Mile Delivery Industry Leaders

-

Correios

-

Loggi

-

Mercado Envios

-

La Poste Group (including Jadlog)

-

Total Express

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Sequoia Logistica divested assets to MercadoLibre for USD 7.5 million and rebranded as Flash Courier, pivoting to high-value B2B contracts.

- April 2026: DHL inaugurated Cajamar and Brasilia warehouses within a BRL 118 million (USD 21.31 million) program to shift its Latin America hub from Miami.

- March 2026: Amazon Now launched in Sao Paulo with 15-minute grocery delivery, free for Prime users.

- November 2025: Jadlog opened five hubs, adding 24,000 m² and 2,000 vehicles to absorb Black Friday peaks.

Brazil Last Mile Delivery Market Report Scope

| Same-day Delivery |

| Express Delivery |

| Standard Delivery |

| Business-to-Business (B2B) |

| Business-to-Consumer (B2C) |

| Customer-to-Consumer (C2C) |

| E-commerce Retail |

| Fashion and Lifestyle |

| Beauty, Wellness and Personal Care |

| Home and Furniture |

| Consumer Electronics and Appliances |

| Healthcare and Medical Supplies |

| Others |

| North |

| Northeast |

| Central-west |

| Southeast |

| South |

| By Service | Same-day Delivery |

| Express Delivery | |

| Standard Delivery | |

| By Business Model | Business-to-Business (B2B) |

| Business-to-Consumer (B2C) | |

| Customer-to-Consumer (C2C) | |

| By End User Industry | E-commerce Retail |

| Fashion and Lifestyle | |

| Beauty, Wellness and Personal Care | |

| Home and Furniture | |

| Consumer Electronics and Appliances | |

| Healthcare and Medical Supplies | |

| Others | |

| By Region | North |

| Northeast | |

| Central-west | |

| Southeast | |

| South |

Key Questions Answered in the Report

How large will the Brazil last mile delivery market be by 2031?

The Brazil last mile delivery market size is projected to reach USD 3.92 billion by 2031, expanding at a 6.03% CAGR from 2026.

Which service type is growing the fastest?

Same-day delivery is forecast to post a 7.68% CAGR through 2031 thanks to dense urban demand and micro-fulfillment expansion.

Which region offers the highest growth potential?

The North is expected to lead with a 6.51% CAGR as multimodal concessions and rising online penetration unlock underserved corridors.

What is driving healthcare parcel growth?

Telemedicine adoption and pharmaceutical e-commerce are pushing healthcare shipments to a 7.96% CAGR, though progress depends on cold-chain upgrades.

How are fuel and labor costs influencing strategy?

Elevated diesel prices and rising courier fees compel carriers to adopt AI routing and densify networks to preserve margins.

Page last updated on: