Brazil Global Capability Centers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

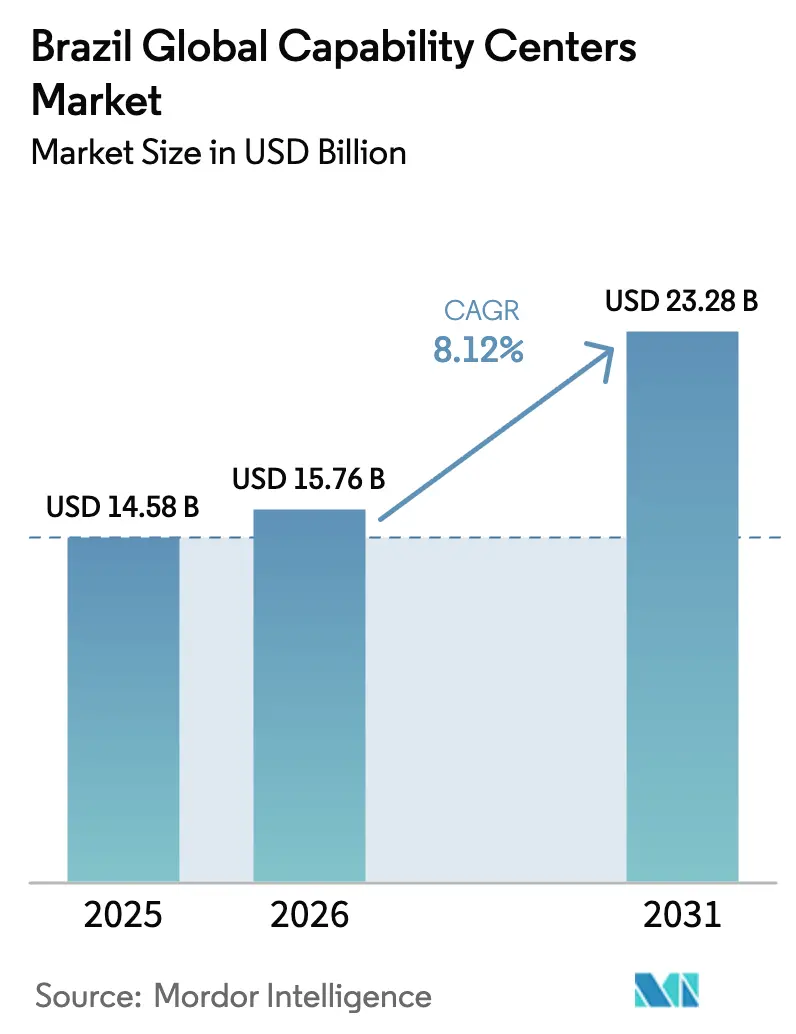

| Base Year Market Size (2025) | USD 14.58 Billion |

| Market Size (2026) | USD 15.76 Billion |

| Market Size (2031) | USD 23.28 Billion |

| Growth Rate (2026 - 2031) | 8.12% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Global Capability Centers Market Analysis by Mordor Intelligence

The Brazil Global Capability Centers market size was valued at USD 14.58 billion in 2025 and estimated to grow from USD 15.76 billion in 2026 to reach USD 23.28 billion by 2031, at a CAGR of 8.12% during the forecast period (2026-2031). Near-term expansion reflects multinationals combining cost savings with strategic value, especially the ability to execute sophisticated digital programs at scale. Large cloud providers have reduced infrastructure constraints, while government incentives such as Lei do Bem strengthen the fiscal rationale for new centers. The maturing talent pool now delivers advanced engineering and data-centric services, helping companies consolidate global workstreams in locations that preserve regulatory sovereignty and compliance. At the same time, location strategies are increasingly weighing ESG goals, with Brazil’s renewable energy matrix supporting low-carbon operations that differentiate the country from traditional offshore alternatives.[1]Associação Brasileira das Empresas de Software, “Brazilian Software Market Report 2024,” abes.org.br

Key Report Takeaways

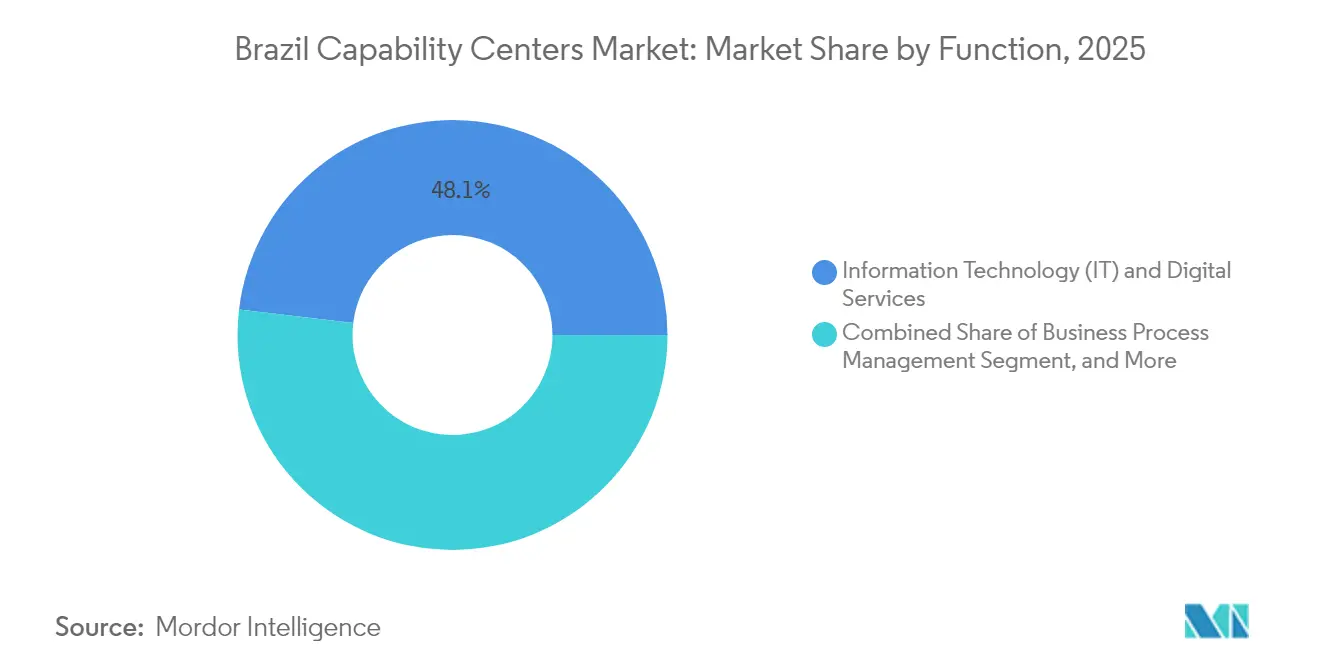

- By function, Information Technology and Digital Services held 48.10% of the Brazil Global Capability Centers market share in 2025 and is projected to post the highest CAGR of 8.62% through 2031.

- By engagement model, captive centers accounted for 61.75% of the Brazil Global Capability Centers market size in 2025, yet hybrid Build-Operate-Transfer approaches are projected to advance at a 8.95% CAGR.

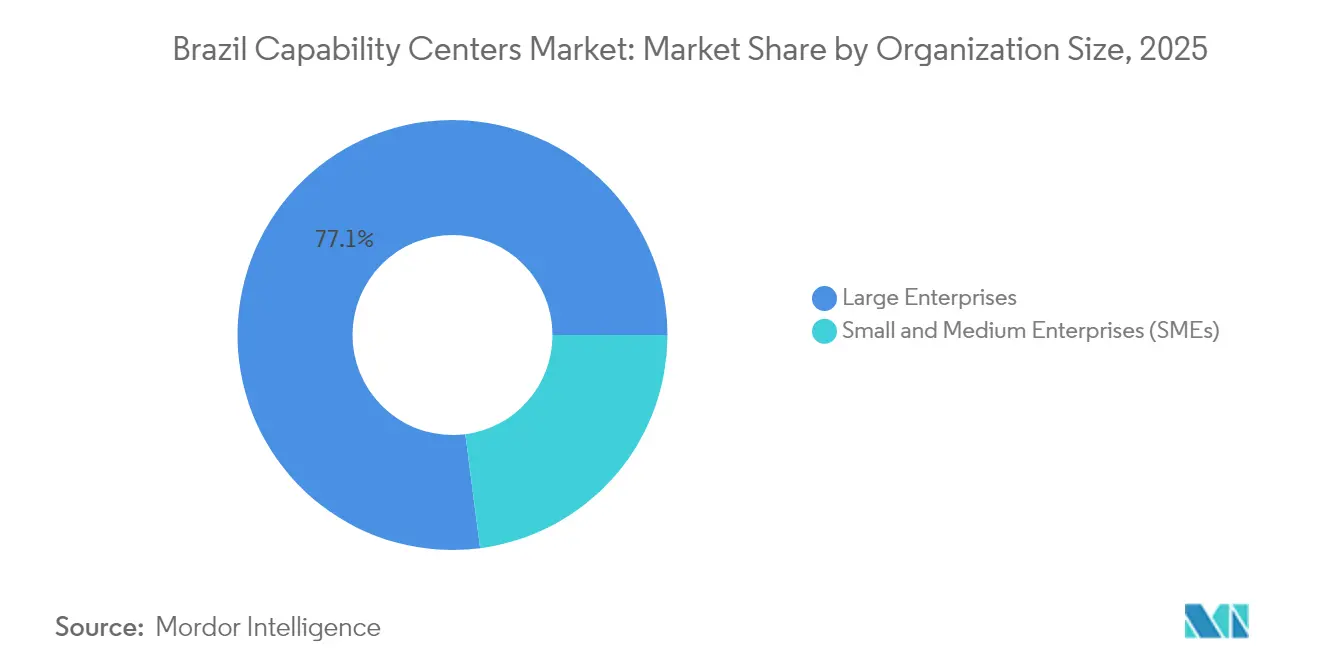

- By organization size, large enterprises contributed 77.05% of the 2025 revenue, whereas small and medium enterprises led the growth with a 10.07% CAGR.

- By industry vertical, retail and consumer goods captured 31.05% of the 2025 revenue, while banking, financial services, and insurance are forecast to expand at a 8.98% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil Global Capability Centers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost arbitrage from wage differentials | +2.1% | São Paulo and Rio de Janeiro | Medium term (2-4 years) |

| Growing pool of skilled digital talent | +1.8% | National metro hubs | Long term (≥ 4 years) |

| Government incentive programs | +1.5% | National innovation zones | Short term (≤ 2 years) |

| Nearshore time-zone alignment | +1.3% | U.S. and Canada | Medium term (2-4 years) |

| Hyperscaler cloud investments | +1.0% | Data-center corridors | Short term (≤ 2 years) |

| ESG-driven location strategies | +0.8% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cost Arbitrage From Wage Differentials

Senior software developers in Brazil earn USD 35,000-50,000 annually, compared to USD 120,000-150,000 in North America, resulting in a 60-70% direct labor savings. The differential also extends to real estate and shared-services costs, where reductions of 40-50% are typical. Although currency volatility can narrow spreads, multinationals still see meaningful total-cost advantages. Operational savings contribute directly to reinvestment in higher-value engineering work, enabling centers to shift their focus from maintenance tasks to innovation programs that accelerate digital growth agendas.

Growing Pool of Skilled Digital Talent

Brazil recorded a technology workforce exceeding 500,000 in 2024, with approximately 46,000 new STEM graduates entering the workforce annually.[2]Ministry of Education, “Higher Education Statistics 2024,” mec.gov.br Developer surveys indicate 78% proficiency in cloud architectures and 65% hands-on experience with artificial-intelligence libraries, a depth of skills that supports machine-learning operations, digital twin modeling, and predictive analytics. As a result, Global Capability Centers mandates now include complex product development and agile DevOps pipelines that were traditionally limited to on-shore headquarters. The long-term talent outlook remains positive, driven by sustained enrollment growth in computing disciplines and an active boot camp ecosystem.

Government Incentive Programs

The 2024 enhancement of Lei do Bem increased allowable R&D deductions to 200% and expanded eligibility to artificial-intelligence initiatives, reducing effective tax rates on qualifying projects by 15-25%. Coupled with accelerated depreciation on digital infrastructure, these benefits reduce payback periods on new center buildouts. Firms locating in designated innovation zones receive additional municipal exemptions on property and service taxes, creating region-specific cost ladders that guide site-selection models.

Nearshore Time-Zone Alignment

Eastern Brazil operates within one to three hours of U.S. Eastern Time, enabling real-time agile ceremonies and compressed iteration cycles. Customer-facing teams enjoy faster hand-offs, while development squads complete sprints without overnight delays. Companies report 20-30% shorter project timelines versus Asian offshore models, strengthening the business case for consolidating North American workloads in Brazil.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex labor regulations and compliance burden | -1.4% | Nationwide | Medium term (2-4 years) |

| High overall tax incidence outside incentive zones | -1.2% | Nationwide | Short term (≤ 2 years) |

| Persistent talent attrition and salary inflation | -0.9% | São Paulo and Rio de Janeiro | Medium term (2-4 years) |

| Currency volatility is impacting cost forecasts | -0.7% | Global operations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Complex Labor Regulations and Compliance Burden

Brazil’s Consolidacao das Leis do Trabalho mandates 13th-month salary, 30-day vacations, and extensive termination protocols that extend workforce adjustments by up to 90 days.[3]Ministério do Trabalho e Previdência, “Labor Relations and Employment Law Guide,” trabalho-e-previdencia.gov.br Mandatory social contributions increase total employment costs to nearly double the base pay, creating significant budget line items for the finance teams of Global Capability Centers. While the framework offers predictability, compliance workflows require dedicated legal and HR functions, raising the barriers for smaller entrants.

High Overall Tax Incidence Outside Incentive Zones

Aggregate federal, state, and municipal taxes can lift effective corporate tax rates above 45% for entities operating outside technology parks. The multilayer structure complicates cash-flow planning and inflates the hurdle rates that govern new-build approvals. Although larger multinationals secure special regimes through negotiated accords, smaller firms often delay expansion until they meet incentive-zone criteria.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Function / Capability: Digital-first Services Lead Adoption

Information Technology and Digital Services generated 48.10% of revenue in 2025, driven by cloud migration projects, data engineering pipelines, and AI-enabled automation. The segment’s 8.62% CAGR means it will compound the Brazil Global Capability Centers market size rapidly over the forecast horizon. Demand stems from global retailers, banks, and manufacturers consolidating scattered IT estates into standardized, cloud-native stacks managed from Brazilian hubs.

Engineering and R&D work now spans automotive firmware, industrial automation, and connected-product design. Siemens, Bosch, and other tier-one industrial companies added headcount dedicated to embedded software integration, illustrating a shift toward value-added engineering engagements. Business Process Management remains relevant for finance and HR tasks; however, growth is shifting toward analytics-heavy Knowledge Process Outsourcing, where Brazil’s bilingual talent delivers a competitive advantage in North-South trade corridors.

By Engagement Model: Hybrid BOT Gains Momentum

Captive centers controlled 61.75% of 2025 revenue, as intellectual property sensitivity drives direct ownership preferences in the banking, healthcare, and defense sectors. However, hybrid Build-Operate-Transfer models post a 8.95% CAGR, indicating that multinationals increasingly co-create facilities with local partners before assuming full control. The approach mitigates regulatory and real estate risks, speeds licensing, and reduces time-to-productivity by roughly one-third compared with green-field captives. [4]Accenture, “Build-Operate-Transfer Services in Latin America,” accenture.com .

Pure outsourcing retains a niche for discrete projects or for companies testing Brazilian delivery economics. Yet as ESG reporting pressures mount, firms insist on deeper oversight of labor practices and carbon footprints, reinforcing the captive and hybrid trajectory that keeps strategic levers in-house while preserving cost flexibility.

By Organization Size: SMEs Enter the Global Stage

Large enterprises accounted for 77.05% of the value in 2025, primarily due to their scale and capital intensity. Their portfolios encompass IT, engineering, and advanced analytics, and they frequently enter into multi-year occupancy contracts in Tier-III data center parks. With established global process owners, they expand Brazil Global Capability Centers' market share by migrating high-complexity workloads that demand domain knowledge and regulatory adjacency.

Small and medium enterprises, though starting from a low base, chart the fastest 10.07% CAGR. Cloud pay-as-you-go models remove capex hurdles, while local banks extend credit lines backed by Brazilian Development Bank guarantees. As digital commerce exports rise, SMEs are exploiting time-zone overlaps to serve U.S. clients, signaling a democratization of the Brazil Global Capability Centers industry that widens the addressable universe beyond traditional Fortune 500 sponsors.

By Industry Vertical: BFSI Surges Ahead

Retail and consumer goods occupied 31.05% market share in 2025 and continue to expand omnichannel and supply-chain analytics programs. Brands leverage the market capabilities of Brazil Global Capability Centers to refine last-mile logistics, optimize pricing engines, and roll out headless commerce platforms. Despite its maturity, the sector continues to commission AI-driven personalization and inventory planning pilots that sustain service demand.

Banking, financial services, and insurance are projected to grow at a 8.98% CAGR, the steepest among verticals. Brazil’s leadership in instant payments and open banking regulations fosters local expertise in API security, transaction monitoring, and digital identity validation. That know-how transfers to North American and European banks seeking faster compliance cycles. Secondary sectors, such as healthcare, manufacturing, and telecom, add diversified volume, especially as IoT deployments scale.

Geography Analysis

Primary hubs in São Paulo and Rio de Janeiro together capture a significant share of the Brazil Global Capability Centers market. São Paulo’s depth in financial services supplies domain-specific talent for risk modeling and fintech coding, while Rio offers cost-effective real estate and incentives that draw mid-sized captives. Both cities benefit from international airports and Tier-IV carrier-neutral data centers that meet the latency thresholds required for real-time workloads.

Second-tier metros, such as Belo Horizonte, Porto Alegre, and Recife, are emerging as diversification destinations. Operating expenses are 20-30% lower than in São Paulo, and universities consistently produce graduate cohorts. State authorities bundle payroll-tax discounts with expedited construction permits, further lifting the regional share of the Brazil Global Capability Centers market size.

Northern and Northeastern states remain nascent but show promise. Manaus anchors a free-trade zone that eliminates import duties on servers and networking equipment, aligning with ESG initiatives that favor low-carbon hydropower. However, limited senior talent density and transport logistics temper immediate scalability. Federal fiber-backbone extensions scheduled through 2027 aim to unlock broader participation.

Competitive Landscape

The market exhibits moderate concentration. Accenture, IBM, Tata Consultancy Services, and Infosys hold the largest installed footprints, leveraging standardized delivery frameworks and sector-specific accelerators. These incumbents actively reposition portfolios from legacy ERP support toward AI model operations, cloud orchestration, and cybersecurity. They pair global process templates with local language capabilities to meet the needs of both North-South and South-North client flows.

Brazilian specialists, including CI&T and TOTVS, capitalize on cultural proximity and deep familiarity with national compliance standards. Their agile squads deliver microservices architecture rewrites and data-driven customer-experience programs for regional unicorns. Hybrid engagement demand also opens space for mid-cap integrators that undertake facility setup and staff training before transitioning ownership.

Investments in automation shape competitive intensity. Vendors deploying low-code platforms, generative AI copilots, and site reliability engineering toolchains report productivity lifts exceeding 25%. Those gains translate into pricing flexibility that sustains the Brazil Global Capability Centers market against labor-cost inflation. Strategic partnerships with hyperscalers remain a common differentiator, enabling rapid provisioning of sovereign-cloud instances that satisfy data-residency statutes.

Brazil Global Capability Centers Industry Leaders

Accenture plc

International Business Machines Corporation (IBM)

Capgemini SE

Tata Consultancy Services Limited

Cognizant Technology Solutions Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Microsoft committed an additional USD 500 million to establish Azure sites in Belo Horizonte and Porto Alegre, expanding sovereign-cloud capacity.

- September 2025: Tata Consultancy Services opened its largest Latin American delivery center in São Paulo, adding 3,000 AI specialists for North American engagements.

- August 2025: Brazil’s government launched the National AI Strategy, allocating BRL 23 billion (USD 4.2 billion) over four years to attract R&D-intensive Global Capability Centers projects.

- July 2025: Accenture acquired Brazilian digital-engineering firm Dextra, integrating 800 professionals into its nationwide network.

Brazil Global Capability Centers Market Report Scope

The scope of the global capability center study for the market segmentation by the Function/Capability for (i) Information Technology (IT) and Digital Services segment is limited to Software Development, Cloud and Infrastructure Management, Cybersecurity, Data Analytics and AI/ML; (ii) Engineering / ER&D segment is limited to Product Design and Testing, Embedded Systems, Digital Twin / Simulation; (iii) Business Process Management (BPM) segment is limited to Finance and Accounting, HR, Payroll and Talent Management, Procurement, Customer Service; and (iv)Knowledge Process Outsourcing (KPO) segment is limited to Market Research and Insights, Risk and Compliance, Legal and Regulatory Support, Strategy and Consulting Support. Similarly, for segmentation by the Engagement Model, scope for (i) Hybrid Build-Operate-Transfer (BOT) is limited to Joint Venture / Strategic Partnership and Virtual Captive Model. The rest of the segment scope is as specified for the listed segment.

| Information Technology (IT) and Digital Services |

| Engineering / ER&D |

| Business Process Management (BPM) |

| Knowledge Process Outsourcing (KPO) |

| Captive (Self-Build) / In-house |

| Build-Operate-Transfer (BOT) |

| Hybrid Build-Operate-Transfer (BOT) |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| Banking, Financial Services, and Insurance (BFSI) |

| Telecom and IT |

| Healthcare and Life Sciences |

| Manufacturing, Automotive and Industrial |

| Retail and Consumer Goods |

| Other Industry Verticals |

| By Function / Capability | Information Technology (IT) and Digital Services |

| Engineering / ER&D | |

| Business Process Management (BPM) | |

| Knowledge Process Outsourcing (KPO) | |

| By Engagement Model | Captive (Self-Build) / In-house |

| Build-Operate-Transfer (BOT) | |

| Hybrid Build-Operate-Transfer (BOT) | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises (SMEs) | |

| By Industry Vertical | Banking, Financial Services, and Insurance (BFSI) |

| Telecom and IT | |

| Healthcare and Life Sciences | |

| Manufacturing, Automotive and Industrial | |

| Retail and Consumer Goods | |

| Other Industry Verticals |

Key Questions Answered in the Report

What is the projected value of the Brazil Global Capability Centers market in 2031?

The market is expected to reach USD 23.28 billion by 2031.

Which segment grows fastest through 2031?

Information Technology and Digital Services posts a 8.62% CAGR, the highest among functional capabilities.

Why are hybrid Build-Operate-Transfer models gaining popularity?

They enable companies to de-risk entry, tap into local expertise, and later assume full control without the need for lengthy greenfield setups.

How do government incentives affect Global Capability Centers' economics?

The Lei do Bem allows for 200% R&D tax deductions, reducing effective tax burdens by up to 25%.

Which cities outside São Paulo and Rio show rising Global Capability Centers activity?

Belo Horizonte, Porto Alegre, and Recife offer 20-30% lower operating costs and growing talent pools.

What challenges continue to restrain expansion?

Complex labor laws and high tax incidence outside incentive zones significantly impact cost models, particularly for smaller entrants.

Page last updated on: