Brazil Customer Data Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

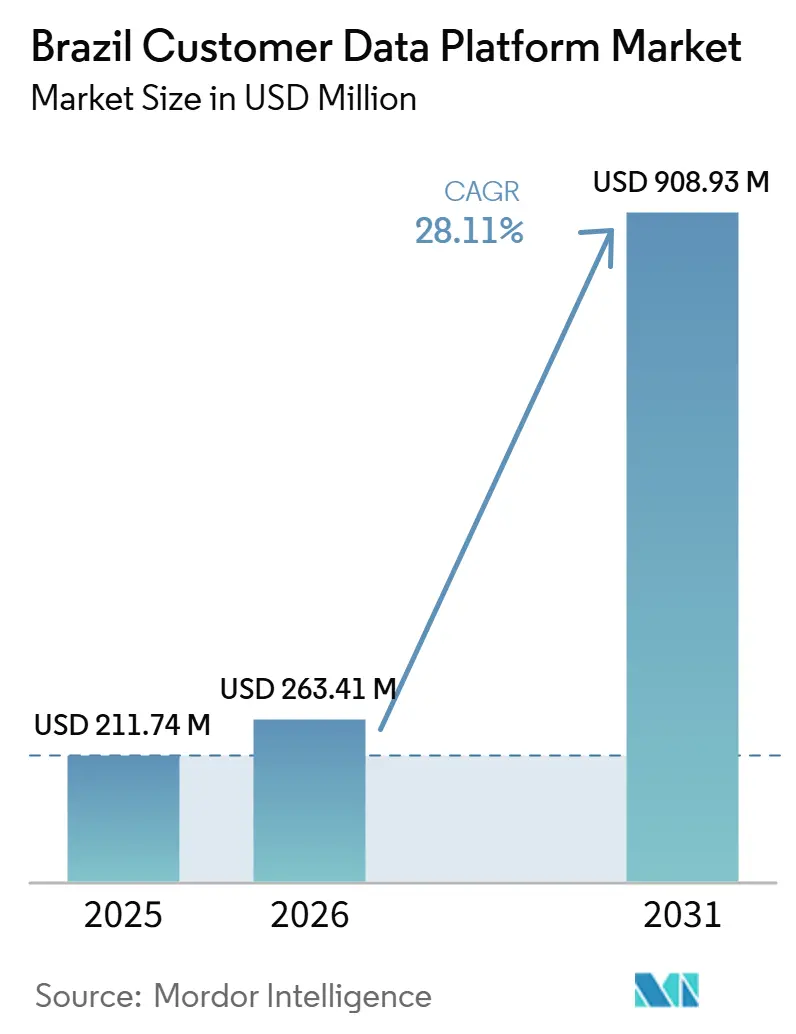

| Base Year Market Size (2025) | USD 211.74 Million |

| Market Size (2026) | USD 263.41 Million |

| Market Size (2031) | USD 908.93 Million |

| Growth Rate (2026 - 2031) | 28.11% CAGR |

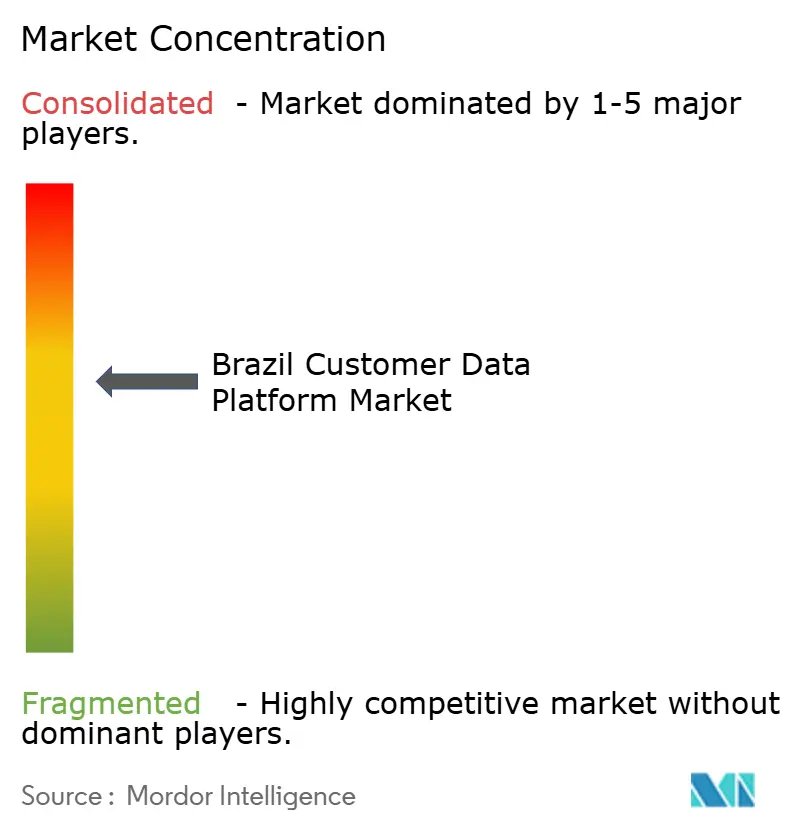

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Customer Data Platform Market Analysis by Mordor Intelligence

The Brazil Customer Data Platform Market size is expected to grow from USD 211.74 million in 2025 to USD 263.41 million in 2026 and is forecast to reach USD 908.93 million by 2031, at a 28.11% CAGR over 2026-2031. The Brazil Customer Data Platform Market is moving quickly as brands, retailers, banks, and media companies increasingly rely on first-party data as older third-party identifiers lose relevance. Privacy compliance is also shaping platform choices, since enterprises now need customer data systems that can support consent tracking, governance, and controlled activation across channels. Retail media and digital commerce are driving the same shift, as customer data is no longer just a marketing input and is increasingly tied to monetization, conversion, and retention. Large vendors still lead the enterprise end of the Brazil Customer Data Platform Market, but the next wave of growth is widening toward services, hybrid architectures, composable models, and SME-focused offerings that reduce deployment friction. This mix of regulatory pressure, revenue-linked use cases, and broader platform access is keeping the Brazil Customer Data Platform Market on a high-growth path.

Key Report Takeaways

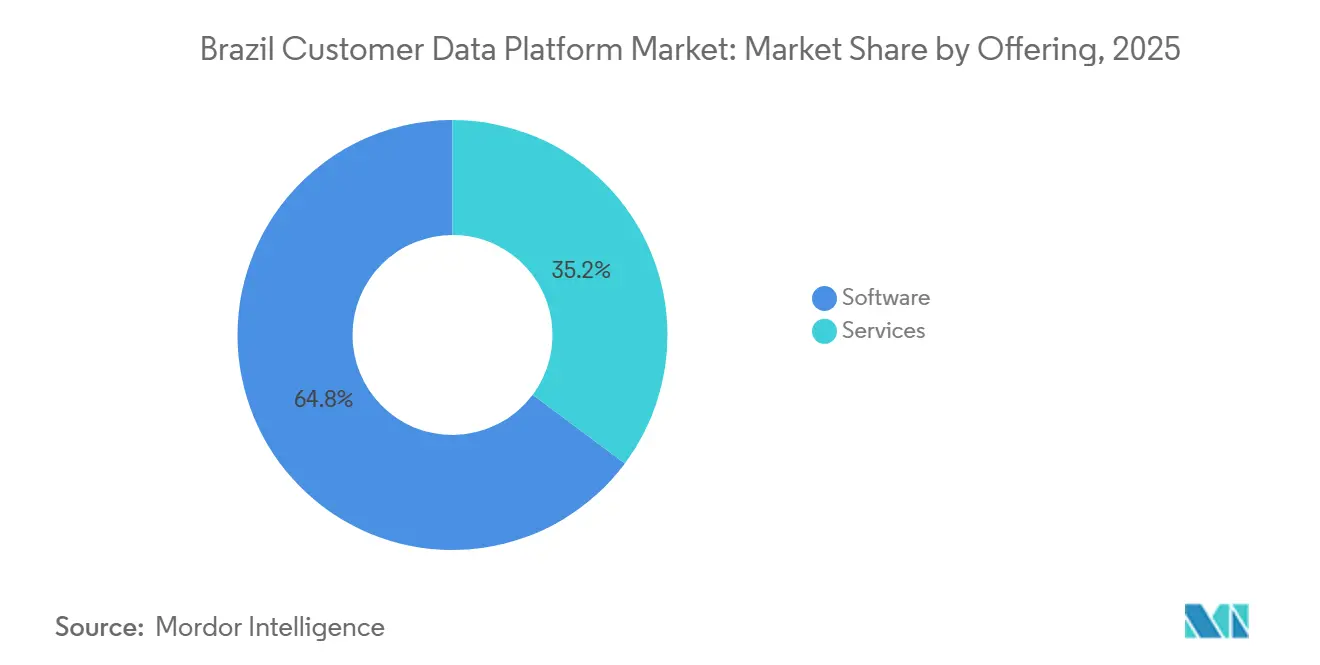

- By offering, software accounted for 64.81% of revenue in the 2025 Brazil Customer Data Platform Market, while services is projected to expand at a 31.24% CAGR through 2031.

- By deployment mode, cloud accounted for 72.19% share in 2025, while hybrid is projected to record the fastest growth at 34.48% CAGR through 2031.

- By organization size, large enterprises captured 58.74% share of the Brazil Customer Data Platform Market in 2025, while SMEs are projected to grow at 32.81% CAGR through 2031.

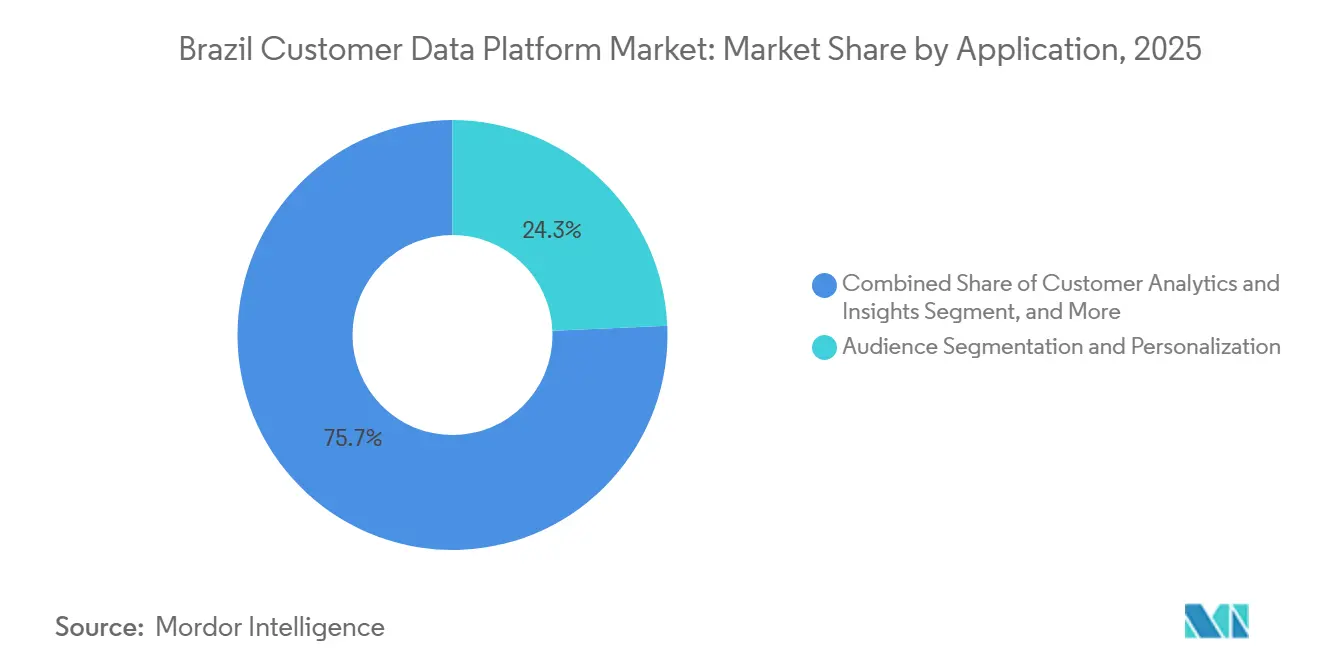

- By application, Audience Segmentation and Personalization led with 24.31% share in 2025, while Customer Analytics and Insights is projected to advance at 35.62% CAGR through 2031.

- By end-user industry, Retail and E-Commerce held 26.83% share in 2025, while Media and Entertainment is projected to expand at 33.19% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Brazil Customer Data Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating First-Party Data Migration in Retail And Media | +6.2% | National, with early concentration in São Paulo and Rio de Janeiro | Short term (≤ 2 years) |

| AI-Driven Identity Resolution and Personalization Demand | +5.8% | National, led by enterprise clusters in São Paulo | Short term (≤ 2 years) |

| Real-Time Omnichannel Activation Needs in E-Commerce | +5.1% | São Paulo, Rio de Janeiro, South Brazil | Short term (≤ 2 years) |

| Privacy-First Customer Graph Adoption for LGPD Compliance | +4.3% | National | Medium term (2-4 years) |

| Composable Data Stack Adoption in Enterprise Marketing Teams | +3.5% | São Paulo enterprise hub, with spillover to South Brazil | Medium term (2-4 years) |

| Retail Media Network Expansion Requiring Unified Audience Segments | +2.8% | National, concentrated in large marketplace and pharmacy retail chains | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerating First-Party Data Migration in Retail And Media

Retail and media companies in Brazil are treating first-party data as core operating infrastructure rather than a side tool. The shift away from third-party identifiers has made owned customer data more important for audience building, targeting, and campaign measurement. This is especially visible in retail formats where ad revenue now depends on the ability to unify store, app, website, loyalty, and transaction records into usable customer profiles. Pharmacy, grocery, and fashion chains are under pressure to organize these data assets faster because monetization only works when audience segments are accurate and permissioned. That is why the Brazil Customer Data Platform Market is moving from a discussion of marketing software toward a broader discussion of revenue and operating model. As a result, vendors that can support fast ingestion, profile stitching, and activation are gaining a stronger place in budget decisions across the Brazil Customer Data Platform Market.

AI-Driven Identity Resolution and Personalization Demand

Identity resolution is becoming one of the clearest product dividing lines in the Brazil Customer Data Platform Market. Brazilian enterprises are dealing with customer journeys that span apps, physical stores, marketplaces, websites, service channels, and payment touchpoints, which makes a single view of the customer much harder to maintain. Brazil also has a useful deterministic identifier base through CPF-linked data environments, which gives vendors a strong local advantage when they can combine stable identifiers with behavioral signals. Product releases across the category show that suppliers are investing heavily in AI-led segmentation, prompt-based activation, and faster use of unified customer records in live campaigns.[1]National Data Protection Authority, “ANPD Conclui Monitoramento De Encarregados De Dados E Avalia Sanção A 21 Empresas,” Governo do Brasil, gov.br The same direction is evident in Amperity’s push toward natural-language customer data workflows that connect insights directly with action. This keeps identity quality and activation speed at the center of vendor selection in the Brazil Customer Data Platform Market.

Real-Time Omnichannel Activation Needs in E-Commerce

The Brazil Customer Data Platform Market is also being lifted by the need to activate customer data without delay. Retailers and consumer brands now need live segments and current behavioral signals to support offers, media placements, retention actions, and journey triggers across channels. When data refresh is slow, campaign timing slips, and the value of personalization falls, even if the customer profile itself is correct. Vendors are responding by linking CDP workflows more closely with warehouse, campaign, and activation tools, enabling teams to move faster from audience definition to execution. Bloomreach’s CustomerLake partnership also reflects this direction, as it was built to reduce duplicate data movement and improve access to live customer records for campaign use. This matters in the Brazil Customer Data Platform Market because commerce and media buyers increasingly judge platforms on actionability, not only on data storage depth.

Privacy-First Customer Graph Adoption for LGPD Compliance

Privacy requirements are pushing the Brazil Customer Data Platform Market toward a stronger consent-aware architecture. Enterprises now need customer graphs that can unify data while preserving purpose, limiting access, and ensuring auditability. The enforcement climate became more visible in 2025, when ANPD concluded monitoring of 56 data controllers and began evaluating sanctions against 21 entities that did not meet data subject rights requirements.[2]Bloomreach, “Bloomreach Announces the General Availability of Loomi Marketing Agent,” Bloomreach, bloomreach.com That kind of oversight changes procurement behavior because customer data systems are evaluated on their governance readiness at the start of the buying process. In the Brazil Customer Data Platform Market, vendors that can map consent status, manage preference history, and separate governed storage from activation layers have a clearer advantage. This is making compliance a design requirement rather than a final checkpoint.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Total Cost Of Ownership for Mid-Market Buyers | -4.2% | National, most pronounced outside the São Paulo enterprise cluster | Short term (≤ 2 years) |

| Integration Complexity Across Legacy CRM and Commerce Systems | -3.8% | National | Medium term (2-4 years) |

| Shortage of Local CDP Implementation and Reverse-ETL Talent | -2.9% | National | Medium term (2-4 years) |

| Data Residency and Cross-Border Consent Complexity Under LGPD | -2.1% | National, concentrated in multinational enterprises | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Total Cost of Ownership for Mid-Market Buyers

High ownership cost remains a real brake on the Brazil Customer Data Platform Market outside the enterprise tier. Full deployments often require license commitments, implementation work, data engineering support, and ongoing managed services, which pushes the category beyond the reach of many mid-sized buyers. This cost issue is not only about software pricing; a large part of the burden comes from the need to clean data, connect tools, and maintain operational workflows after launch. That is why lower-cost composable models and Brazilian-native alternatives are gaining attention in the Brazil Customer Data Platform Market. Smaller firms are clearly becoming more comfortable with digital tools, and a joint Sebrae, FGV, and Google study found that nearly half of small Brazilian businesses had already used AI tools in 2025. Even so, many mid-market buyers still need simpler pricing and lighter deployment models before they can commit to a full CDP program.[3]Sebrae, FGV, and Google, “Transformação Digital,” DataSebrae, datasebrae.com.br

Integration Complexity Across Legacy CRM and Commerce Systems

Integration complexity is another major constraint on the Brazil Customer Data Platform Market. Many enterprises still operate with a mix of older CRM systems, custom commerce layers, ERP environments, and reporting workflows that were not built for fast API-led data movement. A CDP may look attractive at the product level, but the project becomes difficult when source systems have inconsistent schemas, duplicate identifiers, and weak governance rules. This is one reason services are growing faster than software in the Brazil Customer Data Platform Market, since buyers often need outside help to make the stack work in practice. Vendor strategy is already adapting to this pressure, and Bloomreach’s Databricks partnership was built on direct access to live data in the lakehouse to help teams avoid unnecessary ETL duplication. Until integration becomes simpler, deployment timelines and budget overruns will continue to limit adoption among many mid-sized organizations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Software Led While Services Moved Into A More Essential Role

Software accounted for 64.81% of the Brazil Customer Data Platform market in 2025, underscoring enterprises' continued preference for platform-led deployments over services-only approaches. Large buyers in retail, financial services, and media typically entered the category through established software vendors that could deliver pre-built identity, segmentation, orchestration, and governance capabilities within a single environment. This buying pattern reduced early-deployment risk and gave internal teams a clearer path to activation than with custom-built stacks. It also suited procurement teams that wanted faster implementation and recognizable vendor accountability. In the Brazil Customer Data Platform Market, software therefore remained the anchor layer for most enterprise spending in 2025.

That leadership does not mean services are secondary in the Brazil Customer Data Platform Market. Services is projected to expand at a 31.24% CAGR through 2031, reflecting the effort required to connect data sources, define governance rules, align consent flows, and ensure audiences remain usable after go-live. As deployments mature, enterprises usually discover that the hard part is not buying the platform but keeping customer profiles up to date and activation-ready across channels. This is why implementation consulting, managed activation, data quality management, and reverse-ETL support are becoming part of the expected operating model. Bloomreach’s June 2026 partnership with CustomerLake reflected this broader shift by combining platform capabilities with deeper alignment in delivery around warehouse-connected customer data use. The Brazil Customer Data Platform Market is therefore moving toward a structure where software wins the initial budget line, while services help determine long-term value capture.

By Deployment Mode: Cloud Stayed Dominant While Hybrid Became The Main Growth Path

Cloud held 72.19% of the Brazil Customer Data Platform market share in 2025, which kept it well ahead of other deployment approaches. The cloud model remains attractive because it supports faster rollout, easier scaling, and simpler connection with digital commerce, campaign, and analytics tools. It also aligns with the preferences of many enterprise teams for vendor-managed upgrades and a lower infrastructure burden. In the Brazil Customer Data Platform Market, cloud remains the default entry point for organizations seeking to unify customer data without bearing the full burden of in-house platform maintenance. That explains why most large deployments still begin with cloud-first architecture even when the final operating model becomes more mixed.

Hybrid deployment is projected to grow at a 34.48% CAGR through 2031, making it the fastest-growing model in the Brazil Customer Data Platform Market. The reason is practical: many regulated, data-intensive organizations want governed storage for sensitive identity records while still using cloud environments for activation and analytics. Hybrid architecture also gives enterprises more flexibility when they need to keep some data closer to internal systems or under tighter policy control. That balance is increasingly important in sectors such as BFSI, government, and parts of healthcare, where data movement is closely scrutinized. Rokt mParticle’s 2026 hybrid CDP direction on Snowflake AI Cloud showed that vendors are designing directly for this demand rather than treating hybrid as a temporary compromise. This keeps the hybrid at the center of the next investment cycle in the Brazil Customer Data Platform Market.

By Organization Size: Large Enterprises Led Revenue While SMEs Set The Faster Pace

Large enterprises held a 58.74% share of the Brazil Customer Data Platform Market in 2025, reflecting the capital intensity and process depth required for full-feature deployments. These buyers usually had larger data estates, broader channel footprints, and stronger internal teams, which made it easier to justify investments in identity resolution, orchestration, and analytics at scale. They also had more immediate financial upside from better customer data, as conversion, cross-sell, retention, and media monetization could move in tandem. In the Brazil Customer Data Platform Market, large enterprises therefore remained the main revenue base for global vendors during 2025. Their spending patterns also helped shape product direction across the category.

SMEs are projected to grow at a 32.81% CAGR through 2031, indicating the next major expansion layer in the Brazil Customer Data Platform Market. This acceleration is tied to composable models, usage-based pricing, and lighter implementation paths that lower the entry barrier for smaller buyers. It is also tied to a broader comfort level with AI-enabled business tools, not just among large firms but also across smaller businesses. A joint Sebrae, FGV, and Google study found that nearly half of small Brazilian businesses had already used AI tools in 2025, which suggests that data-led workflows are spreading into the SME base faster than many enterprise software categories did. That does not remove cost or integration barriers, but it does improve readiness for simpler CDP use cases around segmentation, activation, and customer insight. The Brazil Customer Data Platform Market is therefore likely to remain enterprise-led in revenue while becoming much broader in buyer mix through the forecast period.[4]Teradata, “Banco Bradesco, Harmonized Data Enables Customer Insights,” Teradata, teradata.com

By Application: Segmentation Held The Revenue Base While Analytics Drove The Next Wave

Audience Segmentation and Personalization accounted for 24.31% of the Brazil Customer Data Platform market share in 2025, making it the largest application area. This lead stemmed from its direct connection to two short-cycle outcomes: media monetization and conversion improvement. Buyers are often more willing to fund a CDP when they can tie the first use case to measurable campaign performance and audience activation. In the Brazil Customer Data Platform Market, segmentation became the clearest starting point because it turns unified profiles into visible action across channels. It also creates the internal operating habits that later support broader use cases.

Customer Analytics and Insights is projected to grow at a 35.62% CAGR through 2031, indicating that the Brazil Customer Data Platform Market is moving beyond simple profile storage. Once profiles are unified, enterprises start looking for churn prediction, lifetime value modeling, next-best-action logic, and clearer measurement of customer behavior. That progression is visible in new vendor releases that make analysis and activation feel more connected in daily work. Amperity’s Customer Data Agent, introduced in January 2026, was positioned to move teams from customer data questions to live segments and journeys through natural-language interaction. Consent and preference management also gained weight as ANPD oversight intensified in 2025, which reinforced the need for analytics and activation to sit on governed customer data foundations. The Brazil Customer Data Platform Market is therefore shifting from audience building toward smarter decision support built on the same customer record base.

By End-User Industry: Retail And E-Commerce Led While Media And Entertainment Advanced Fastest

Retail and E-Commerce accounted for 26.83% of the Brazil Customer Data Platform market size in 2025, keeping this segment at the forefront of the Market. The sector depends heavily on unified customer intelligence because the same data can support merchandising, loyalty, paid media, audience sales, and conversion optimization. Retailers also face shorter feedback loops than many other end users, which makes it easier to prove the value of better segmentation and journey orchestration. In the Brazil Customer Data Platform Market, this kept retail and e-commerce at the center of platform demand in 2025. The segment also highlighted the importance of first-party data as a commercial asset rather than merely a marketing dataset.

Media and Entertainment is projected to expand at a 33.19% CAGR through 2031, making it the fastest-growing end-user segment in the Brazil Customer Data Platform Market. Streaming platforms, gaming operators, and content networks need deeper personalization because discovery quality, engagement time, and retention are closely linked. BFSI remains another major adopter, and Teradata’s customer case with Banco Bradesco demonstrated how harmonized data enables deeper customer insights in a complex financial services environment. Healthcare and Life Sciences, IT and Telecom, Industrial Manufacturing, and Government and Public Administration also present long-cycle, data-rich relationships that fit CDP use cases. Bloomreach’s June 2026 release of Loomi Marketing Agent, used across retail, financial services, media, entertainment, and gaming, demonstrated how suppliers are building directly for more responsive cross-channel personalization. This keeps sector expansion broad, even though retail and e-commerce still set the main pace for the Brazil Customer Data Platform Market.

Geography Analysis

The Brazil Customer Data Platform Market remained concentrated in the Southeast in 2025, with São Paulo serving as the main center of enterprise demand. The city brings together the country’s largest banks, retailers, media groups, and technology buyers, which keeps procurement activity deep there. Large account sales, implementation partnerships, and product ecosystem relationships also tend to form first in São Paulo before spreading to other regions. Rio de Janeiro remained the second-largest commercial cluster in the Brazil Customer Data Platform Market, with strength in BFSI, media, government-linked activity, and large enterprise technology programs. South Brazil, led by Porto Alegre, Curitiba, and Florianópolis, continued to build relevance as a delivery base for SaaS firms, implementation specialists, and composable data tools.

The Northeast is becoming the most dynamic frontier within the Brazil Customer Data Platform Market. Cities such as Recife and Fortaleza are benefiting from digital economy investment and broader e-commerce adoption, which is widening the future buyer base. Demand in these areas often looks different from that in the Southeast because many consumers are more mobile-first and have thinner formal transaction histories. That makes flexible identity resolution and hybrid deployment models more relevant for new rollouts in the Brazil Customer Data Platform Market.

Brazil also remains the most technically developed CDP environment in South America, as defined in the draft. The country’s enterprise scale, stronger compliance pressure, and broader mix of retail, finance, media, and digital commerce use cases give it a wider operating base than neighboring markets. These conditions have pushed the Brazil Customer Data Platform Market further toward consent-aware architecture, more advanced activation models, and more demanding enterprise deployments. That lead is likely to hold through the forecast period because both regulatory requirements and buyer sophistication are advancing in tandem.

Competitive Landscape

The Brazil Customer Data Platform Market is moderately concentrated at the enterprise tier and fragmented in the mid-market. Adobe, Salesforce, Oracle, and SAP remain influential with large accounts because they offer broad suites that connect data management with orchestration, analytics, and enterprise software. Their position is strongest where buyers want platform breadth, long vendor track records, and multi-function integration across sales, service, commerce, and marketing. Even so, the Brazil Customer Data Platform Market is not consolidating around a small set of suppliers, as mid-sized buyers have different cost and deployment needs. That leaves room for composable vendors, local platforms, and vertical specialists to compete on flexibility and speed.

Composable players are changing the shape of competition in the Brazil Customer Data Platform Market by reducing dependence on proprietary data stores. Hightouch’s June 2026 launch of Lifecycle Studio showed how these vendors are extending beyond data movement into campaign-building workflows that appeal directly to CRM and lifecycle teams. Bloomreach’s June 2026 CustomerLake partnership pushed this competitive logic further by linking CDP capabilities more directly to warehouse-native customer data access. These moves matter because they narrow the gap between composable tools and monolithic suites while keeping costs and deployment choices more flexible.

The next openings in the Brazil Customer Data Platform Market are most visible in the mid-market and in vertical use cases. Buyers in healthcare, pharmacy retail, and BFSI increasingly need profile structures and governance controls that fit sector-specific realities rather than generic customer models. Amperity’s product direction in 2026 also showed how vendors are trying to build moats around easier use of identity-resolved customer data through natural-language workflows and real-time context. As a result, competition in the Brazil Customer Data Platform Market is shifting from simple platform comparisons to a contest over architecture fit, governed activation, and ease of operational use.

Brazil Customer Data Platform Industry Leaders

Salesforce, Inc.

Adobe Inc.

Oracle Corporation

SAP SE

Twilio Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Rokt mParticle launched Performance Engine, a capability suite anchored by an AI Audience Agent that converts first-party data into measurable advertising revenue lift across Google and Meta activation channels. The release extended the Rokt-backed USD 300 million platform investment and positioned Rokt mParticle as the first enterprise CDP to offer native performance-linked audience monetization at scale.

- June 2026: Hightouch launched Lifecycle Studio as the second module in its Agentic Marketing Platform, enabling CRM and lifecycle teams to generate fully built, personalized campaigns from a single AI prompt. The release closed a product gap between composable CDP infrastructure and owned-channel campaign execution, reinforcing Hightouch's positioning as a Gartner CDP Leader.

- June 2026: Bloomreach announced a launch partnership for Databricks' CustomerLake, an agentic CDP integrating directly with the enterprise data lakehouse. The integration extended Bloomreach's Loomi AI agent with real-time customer data access from enterprise warehouses, eliminating ETL pipeline duplication and enabling live customer intelligence for campaign execution.

- June 2026: Bloomreach brought its Loomi marketing agent to general availability, converting a single natural-language prompt into a complete, multi-channel campaign workflow. The platform served 1,400+ global enterprise brands across retail, financial services, and media verticals, with the release targeting the latency and personalization requirements of live-streaming and gaming use cases.

Brazil Customer Data Platform Market Report Scope

The Brazil customer data platform (CDP) market refers to the ecosystem of software and associated services that enable organizations in Brazil to collect, unify, and manage customer data from multiple touchpoints into a single, persistent database. These platforms are designed to break down data silos, creating comprehensive customer profiles that can be leveraged for advanced audience segmentation, personalized marketing campaigns, customer journey orchestration, and predictive analytics. The market encompasses cloud, on-premises, and hybrid deployment models tailored to the operational needs of large, small, and medium enterprises across sectors such as retail, BFSI, healthcare, and IT. By integrating strict consent and preference management capabilities, CDPs help Brazilian businesses comply with local data protection regulations (such as LGPD) while enhancing customer experience, driving brand loyalty, and improving overall marketing return on investment.

The Brazil Customer Data Platform Market Report is Segmented by Offering (Software, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Customer Data Collection and Profile Unification, Audience Segmentation and Personalization, Marketing Campaign and Customer Journey Orchestration, Customer Analytics and Insights, Consent and Preference Management, and Other Applications), and End-User Industry (Retail and E-Commerce, BFSI, Healthcare and Life Sciences, IT and Telecom, Media and Entertainment, Industrial Manufacturing, Government and Public Administration, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization |

| Marketing Campaign and Customer Journey Orchestration |

| Customer Analytics and Insights |

| Consent and Preference Management |

| Other Applications |

| Retail and E-Commerce |

| BFSI |

| Healthcare and Life Sciences |

| IT and Telecom |

| Media and Entertainment |

| Industrial Manufacturing |

| Government and Public Administration |

| Other End-User Industries |

| By Offering | Software |

| Services | |

| By Deployment Mode | Cloud |

| On-Premises | |

| Hybrid | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Application | Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization | |

| Marketing Campaign and Customer Journey Orchestration | |

| Customer Analytics and Insights | |

| Consent and Preference Management | |

| Other Applications | |

| By End-User Industry | Retail and E-Commerce |

| BFSI | |

| Healthcare and Life Sciences | |

| IT and Telecom | |

| Media and Entertainment | |

| Industrial Manufacturing | |

| Government and Public Administration | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the 2026 size of the Brazil Customer Data Platform Market?

The Brazil Customer Data Platform Market is projected at USD 263.41 million in 2026 and is forecast to reach USD 908.93 million by 2031, at a 28.11% CAGR

What is driving demand for customer data platforms in Brazil?

The main demand drivers are the shift toward first-party data, stronger privacy compliance needs under LGPD, and the need for real-time activation across retail, media, and digital commerce.

Which deployment model is most used in Brazil customer data platform deployments?

Cloud led with 72.19% share in 2025, while hybrid is projected to grow fastest at 34.48% CAGR through 2031.

Which application area is expanding the fastest in Brazil?

Customer Analytics and Insights is projected to grow fastest at 35.62% CAGR, while Audience Segmentation and Personalization held the largest 2025 share at 24.31%.

Which end-user segment leads adoption in Brazil?

Retail and E-Commerce led with 26.83% share in 2025 because unified customer data supports both monetization and conversion use cases.

How competitive is the Brazil customer data platform space?

Large enterprise demand is led by major global vendors, but the broader field remains fragmented because composable tools, local platforms, and vertical specialists compete aggressively in the mid-market.

Page last updated on: