Brazil Corrugated Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

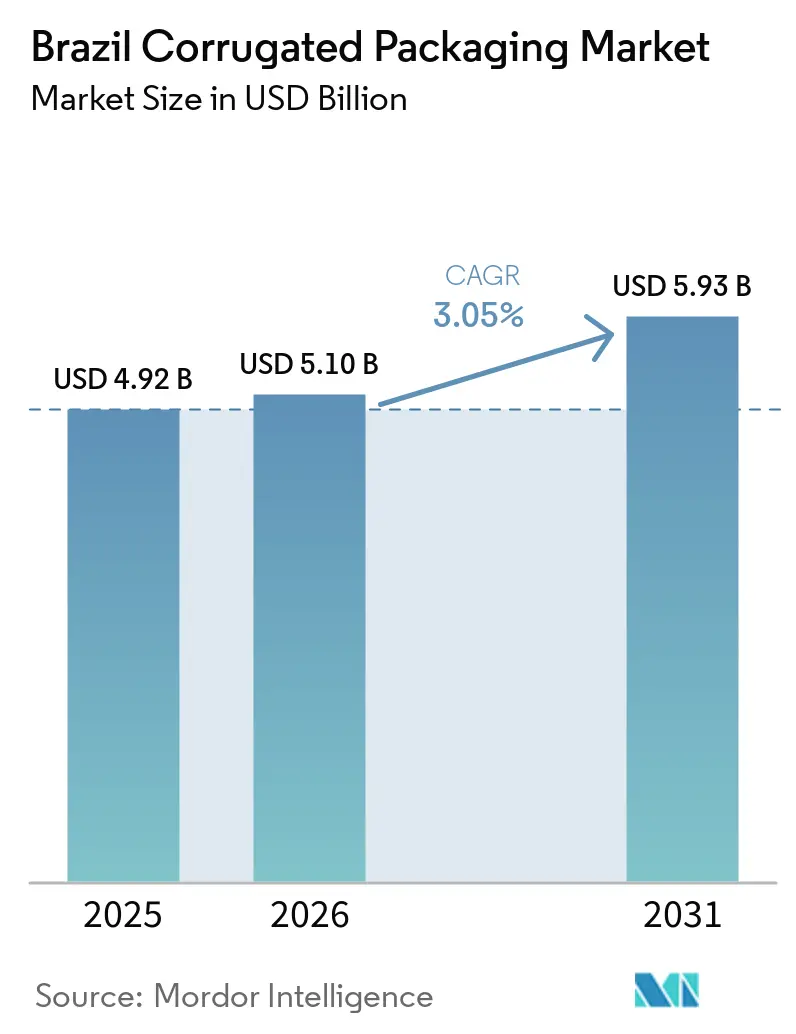

| Base Year Market Size (2025) | USD 4.92 Billion |

| Market Size (2026) | USD 5.10 Billion |

| Market Size (2031) | USD 5.93 Billion |

| Growth Rate (2026 - 2031) | 3.05% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Corrugated Packaging Market Analysis by Mordor Intelligence

The Brazil corrugated packaging market size is expected to grow from USD 5.10 billion in 2026 to USD 5.93 billion by 2031 at a 3.05% CAGR over 2026-2031. Mid-tier cities are driving structural change as e-commerce fulfillment centers outside the São Paulo-Rio axis capture parcel growth, forcing converters to re-map distribution hubs. Capacity expansions at Klabin’s Puma II complex and Smurfit WestRock’s Três Barras mill underpin supply security, yet recovered-paper shortages and pulp-price volatility keep costs unpredictable. Shelf-ready packaging adoption by modern grocery chains, together with tax incentives for recycling infrastructure under Lei 14.260/21, is reshaping material choices. At the same time, cold-chain produce exports are spawning niche demand for triple-wall, moisture-resistant formats, while digital inkjet presses are redefining short-run economics.

Key Report Takeaways

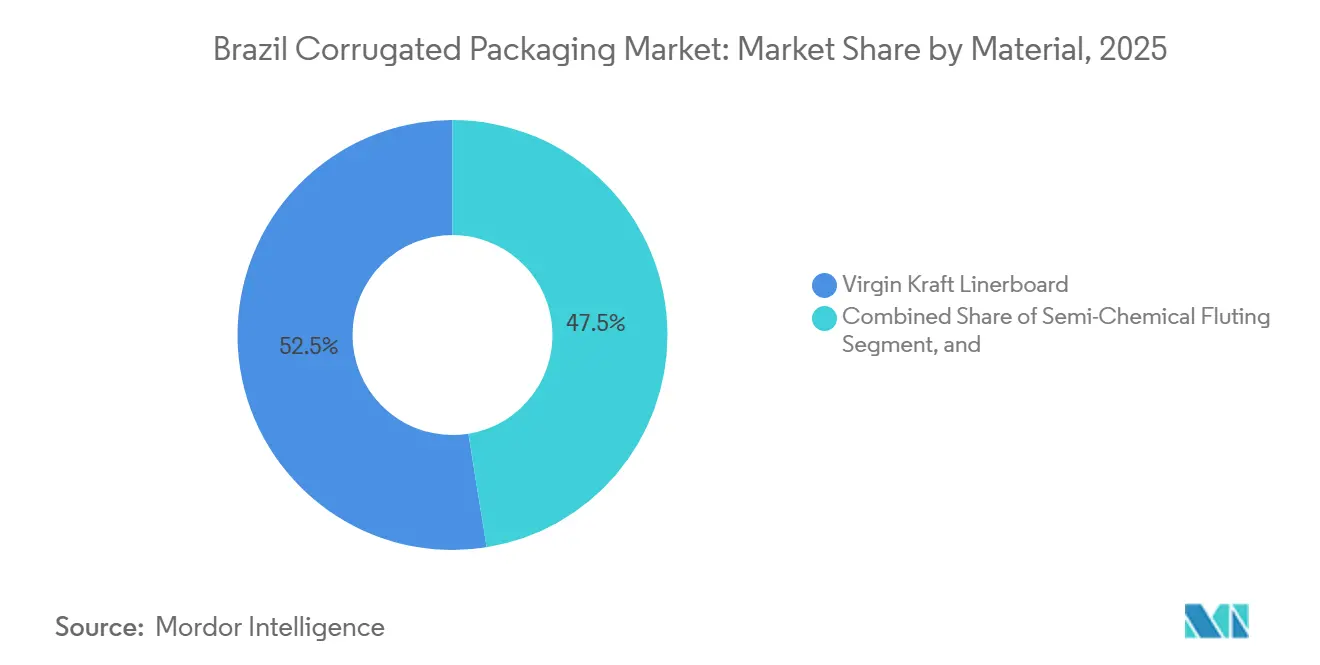

- By material, virgin kraft linerboard captured 52.54% of the Brazil corrugated packaging market share in 2025.

- By flute type, the Brazil corrugated packaging market size for the E flute segment is forecast to advance at a 5.12% CAGR through 2031.

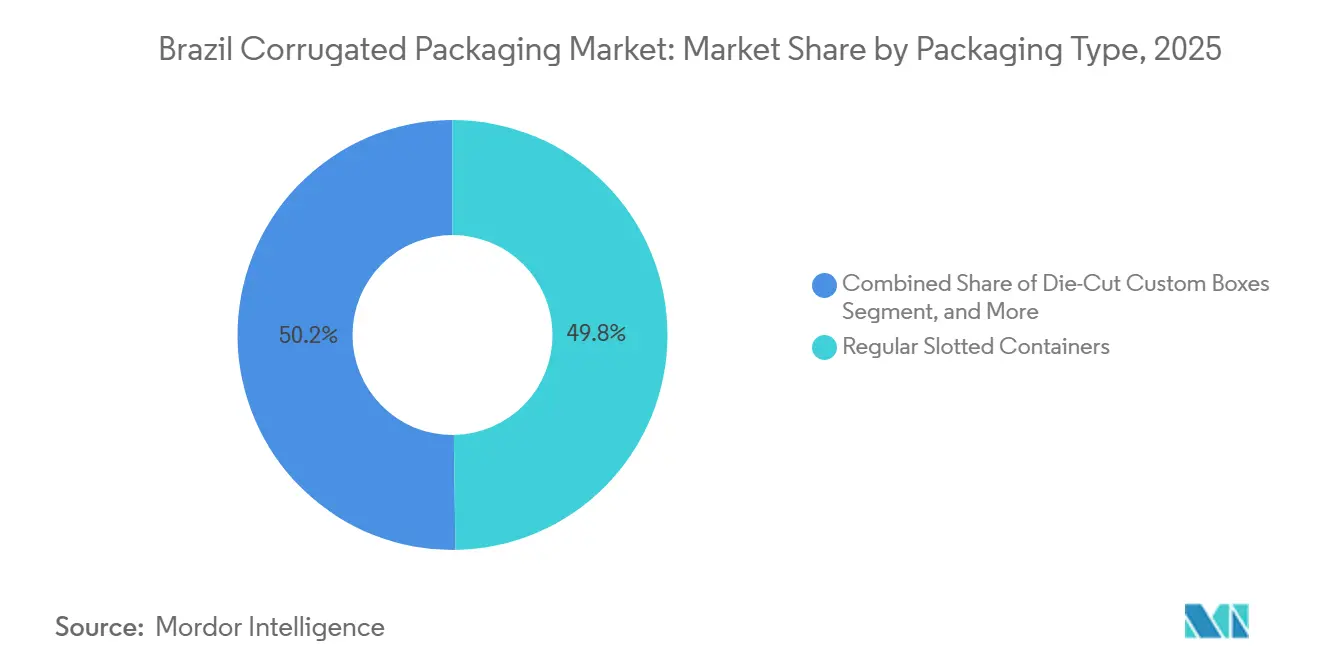

- By packaging type, regular slotted containers captured 49.78% of the Brazil corrugated packaging market share in 2025.

- By wall type, the Brazil corrugated packaging market size for the double-wall segment is forecast to advance at a 5.84% CAGR through 2031.

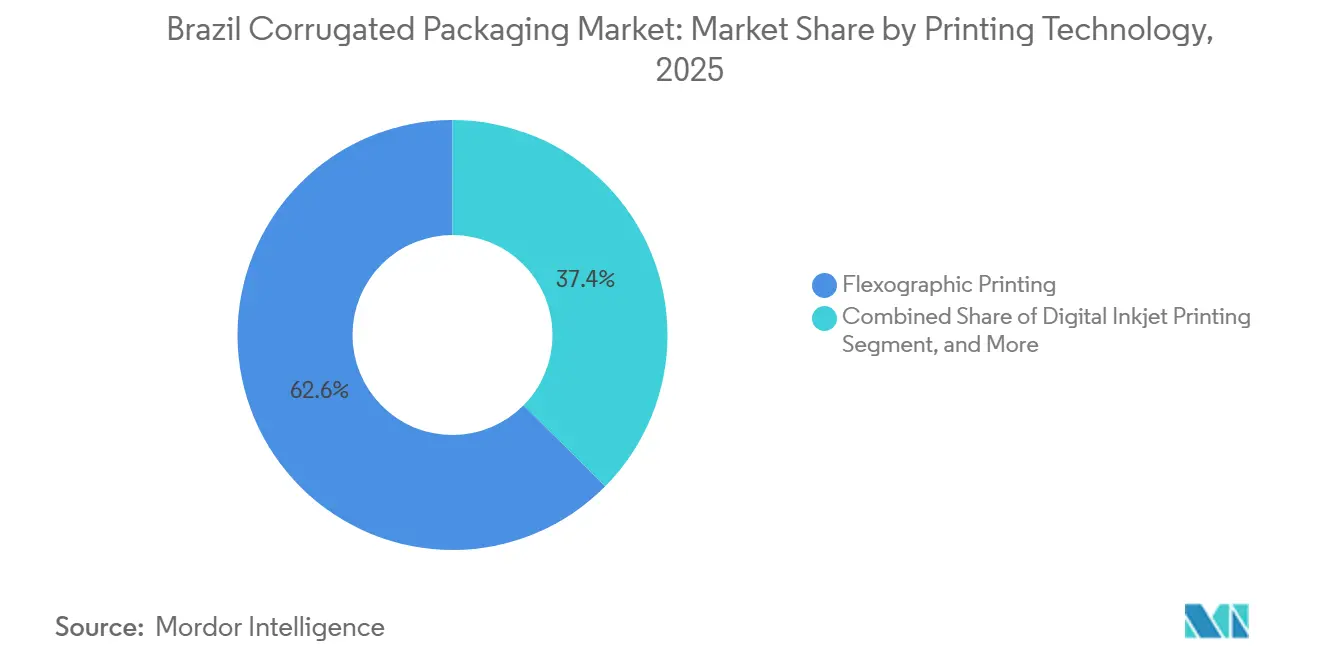

- By printing technology, flexographic printing captured 62.58% of the Brazil corrugated packaging market share in 2025.

- By end-user industry, the Brazil corrugated packaging market size for the e-commerce fulfillment centers segment is forecast to advance at a 5.91% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Brazil Corrugated Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising E-commerce Order Volumes From Mid-Tier Brazilian Cities | +0.9% | Southeast and South, with early gains in Curitiba, Belo Horizonte, Porto Alegre, Brasília | Medium term (2-4 years) |

| Rapid Capacity Additions At Klabin's Puma II Complex | +0.7% | National, with production concentrated in Paraná and distribution across Southeast and South | Short term (≤ 2 years) |

| Rising Adoption Of Shelf-Ready Packaging By Modern Grocery Chains | +0.5% | Southeast urban centers (São Paulo, Rio de Janeiro), expanding to South and Central-West | Medium term (2-4 years) |

| Government Tax Incentives For Recycled Fiber Use (Lei 14.260/21) | +0.4% | National, with stronger uptake in Southeast and South regions | Long term (≥ 4 years) |

| Brand Owner Shift Toward Premium Graphics On Corrugated Displays | +0.3% | Southeast and South, concentrated in São Paulo and Curitiba retail clusters | Medium term (2-4 years) |

| Cold-Chain Expansion For Fresh Produce Exports | +0.3% | South (Paraná, Santa Catarina, Rio Grande do Sul) and Northeast (Bahia, Pernambuco) export corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising E-commerce Order Volumes From Mid-Tier Brazilian Cities

Small and medium enterprises in Curitiba, Belo Horizonte, and other mid-tier cities generated 77% of 2025 online sales growth, redistributing parcel flows away from São Paulo.[1]Loggi, “E-Commerce Growth Analysis: Small and Medium Enterprises in Mid-Tier Brazilian Cities,” loggi.com Converters responded by opening satellite warehouses that raise working-capital needs, while lighter E flute boxes help minimize dimensional-weight freight. Limited local recycling forces heavier reliance on virgin kraft, tightening supply in export hubs and underscoring feedstock fragility. The trend positions e-commerce to overtake traditional retail demand by 2028 and accelerates adoption of digital printing for personalized graphics.

Rapid Capacity Additions at Klabin’s Puma II Complex

Klabin’s MP27 and MP28 lines added 910,000 tpy of virgin kraft capacity by mid-2023, giving Brazil its largest integrated linerboard hub.[2]Klabin S.A., “Puma II Complex Investment Update,” Investor Relations, ri.klabin.com.br Vertical integration shields Klabin from recovered-fiber volatility but locks the firm into a high fixed-cost model that needs utilization above 85% for margin stability. The mill’s Paraná location shortens haul distances to automotive and appliance clusters that demand triple-wall virgin boxes, granting Klabin a strategic freight edge. Competitors lacking similar scale face share erosion unless they match capacity or pivot toward recycled niches.

Rising Adoption of Shelf-Ready Packaging by Modern Grocery Chains

Carrefour and Grupo Pão de Açúcar expanded stores rapidly in 2025, embracing shelf-ready formats that slash in-store handling and speed stock rotation amid inflationary pressures. The design requires tight dimensional tolerances, die-cut tear-strips, and vivid graphics, prompting converters to invest in rotary die-cutters and digital pre-press workflows. Adoption started in high-wage São Paulo and Rio outlets but is spreading nationwide as regional chains modernize merchandising strategies. Larger converters with integrated design teams gain share, while small firms face equipment upgrade hurdles.

Government Tax Incentives for Recycled Fiber Use (Lei 14.260/21)

The statute channels nearly USD 94 million annually into collection and sorting, reducing feedstock volatility and narrowing virgin-recycled cost gaps in formal waste networks. Southeast and South projects capture most funds because they meet stringent compliance thresholds, whereas Northeast municipalities struggle with documentation and miss out on grants. Improved recovered-paper quality aligns with ISO 14001 mandates imposed by multinational buyers, providing converters a compliance-driven demand tailwind. However, uneven regional uptake prolongs supply fragmentation and keeps recycled linerboard pricing unstable.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Kraft Linerboard Pulp Prices Tied to FX Swings | -0.6% | National, acute in export-oriented South and Southeast | Short term (≤ 2 years) |

| Logistics Bottlenecks at Santos and Paranaguá Ports | -0.4% | South and Southeast export corridors | Medium term (2-4 years) |

| Structural Shortage of High-Quality Recovered Paper | -0.3% | National, severe in Northeast and Central-West | Long term (≥ 4 years) |

| Rising Digitalization Reducing Printed POS Volumes | -0.2% | São Paulo, Rio de Janeiro, Belo Horizonte | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Kraft Linerboard Pulp Prices Tied to FX Swings

Bleached eucalyptus kraft pulp averaged USD 580-640 per tonne in early 2025, but Brazilian real depreciation magnified domestic cost spikes for non-integrated converters. Mid-sized box plants under fixed-price contracts absorbed margin hits or forfeited clients, accelerating consolidation toward vertically integrated giants. Currency volatility also complicates hedging strategies because derivative premiums remain prohibitive for smaller players, reinforcing structural cost advantages for Klabin and Suzano.

Logistics Bottlenecks at Santos and Paranaguá Ports

Average vessel waits above five days in early 2025 inflated cold-chain storage expenses and delayed recovered-paper imports, especially for Paraná’s produce exporters. Port congestion undermines service reliability for small converters without priority berthing and curtails Brazil’s competitiveness in European and Asian fruit markets. Infrastructure upgrades are funded but will not complete until 2027, keeping logistics a mid-term growth drag on export-oriented packaging demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Virgin Kraft Dominance Masks Feedstock Fragility

Virgin kraft linerboard captured 52.54% share of Brazil corrugated packaging market size in 2025 because brand owners prioritize high burst strength and superior print surfaces for electronics, cosmetics, and premium retail applications. Semi-chemical fluting is projected to expand at 4.66% CAGR through 2031, benefiting from cushioning performance in heavy industrial goods and regional automotive supply chains. Recycled linerboard volumes remain supply-constrained, as domestic recovered-paper collection growth lags e-commerce demand despite Lei 14.260/21 incentives that improve infrastructure mainly in urbanized regions. Specialty coatings offering moisture resistance are gaining favor among produce exporters targeting European and Asian cold chains, although they remain niche due to higher formulation costs.

Klabin’s Puma II complex reset competitive dynamics by adding 910,000 tpy of virgin capacity, yet its success still hinges on sustainable demand from appliance and automobile plants that insist on virgin grades for triple-wall packaging. Independent recycled-linerboard producers cluster around São Paulo’s waste streams but now face cost spikes from port congestion and currency swings that affect imported recovered paper, eroding their price advantage. Geographic proximity of virgin kraft mills to eucalyptus plantations in Paraná and Santa Catarina reinforces a south-leaning production bias that lowers freight to fast-growing industrial parks. Over time, improved rural recycling networks could level costs, but until then converters will navigate a bifurcated supply landscape that ties material choice to region and end-use case.

By Flute Type: E Flute Gains Traction in E-Commerce

C flute retained 45.82% of market share in 2025 because its 4 mm profile balances stacking strength with material efficiency for processed foods and beverage logistics. E flute, at just 1.6 mm thick, is forecast to post 5.12% CAGR as e-commerce shippers pursue dimensional-weight savings and lighter parcels that travel through crowded urban hubs. Producers shifting to thinner flutes must retool corrugators, optimize starch recipes, and adopt high-precision knife systems to maintain board flatness, investments that disproportionately challenge smaller plants with older machinery. Thinner profiles also invite upgraded graphics because high-resolution imagery prints cleanly on smoother E flute surfaces, prompting installations such as Mazurky’s EFI Nozomi C18000 Plus digital press that enables short-run, regionalized campaigns.

Warehouse managers in the processed-food segment still favor C flute because cartons stack more safely on pallets that sit for weeks inside distribution centers, whereas personal-care brands and online fashion retailers quickly migrate to lighter E flute for freight cost relief. F flute, even thinner at 0.75 mm, competes directly with folding boxboard in cosmetics but demands precision corrugating and has yet to clear economic hurdles for large-scale adoption. The expanding flute portfolio forces integrated carton makers to juggle knife changeovers, inventory complexity, and different printing work flows while safeguarding crush performance during Brazil’s humid rainy season.

By Packaging Type: Die-Cut Custom Boxes Capture Brand Differentiation

Regular slotted containers accounted for 49.78% of 2025 shipments, dominating processed commodity foods thanks to their compatibility with automated case packers and lower board usage. Die-cut custom boxes are projected to grow at a 5.17% CAGR through 2031 as brand owners increasingly monetize the “unboxing moment” and demand structures that double as point-of-sale displays, particularly in the online beauty and electronics segments. Shelf-ready hybrids that open into display trays blur traditional definitions and require converters to master rotary die-cutting, multi-color flexo, and quick-change tooling to serve both high-run and short-run orders from national retailers. Folding cartons maintain a foothold in compact personal-care items, yet corrugated’s strength advantage and ability to carry heavier payloads are eroding that boundary.

Premium die-cut demand clusters in São Paulo and Curitiba, where multinational marketing teams reside, encourage converters to embed in-house structural designers and digital proofing to shorten concept-to-shelf cycles. In contrast, interior agricultural zones and cash-constrained SMEs still opt for standard RSCs to contain freight and tooling costs, preserving volume but delivering lower margins. Competitive upside lies in mastering rapid die changeovers and digital pre-press workflows that let converters meet both supermarket shelf-ready programs and limited-edition influencer boxes without inflating inventory or obsoleting plates.

By Wall Type: Double-Wall Growth Signals Industrial Demand

Single-wall configurations accounted for 55.26% share in 2025, underpinning e-commerce parcels, personal-care shipments, and fast-moving consumer goods that prioritize material efficiency and postal savings. Double-wall formats are on course to expand at a 5.84% CAGR as automotive parts, white-goods manufacturers, and agricultural exporters seek stronger compression resistance for forklift handling and rough roads in Brazil’s hinterlands. Triple-wall remains a specialized format for mango, citrus, and avocado exporters who need moisture-resistant coatings and a 900 kg dynamic load capacity, but converters who can laminate three webs profit from higher-margin, low-volume orders. Single-face corrugated, used mainly as cushioning sheets and end-cap inserts, holds a marginal share yet provides converters an entry-level path into value-added die-cut operations.

Industrial recovery in South-region clusters has renewed demand for double-wall cartons that can stack under heavy torque in tall racking systems and survive multimodal journeys to ports plagued by congestion. Producing these heavy boards requires corrugators with wider hot-plate sections, thicker glue lines, and enhanced quality inspection, pushing capital requirements beyond the reach of many small independents. Because double-wall users frequently specify virgin kraft facings for burst-strength assurance, integrated pulp-and-box players capture a feedstock advantage, further entrenching market concentration in premium heavy-duty formats.

By Printing Technology: Digital Inkjet Disrupts Short-Run Economics

Flexographic presses retained 62.58% share in 2025 thanks to unmatched speed and low cost on runs above 10,000 linear meters that dominate beverage, processed-food, and industrial box programs. Digital inkjet is poised to grow 5.18% CAGR because it eliminates plate costs and compresses lead times, making economic sense for region-specific promotions, influencer co-branding, and personalized gift packaging in runs as low as 500 units. Litho-lamination keeps its foothold in ultra-high graphics for luxury cosmetics and premium spirits, but digital’s 1,200 dpi resolution narrows the quality gap while slashing tooling expense. Hybrid workflows that pair digital pre-print with post-print flexography are emerging as converters explore crossover points that balance speed with artwork flexibility.

Mazurky’s EFI Nozomi installation validated digital’s commercial viability in Brazil by hitting 75 m/min throughput and executing five design changeovers in a single shift, an impossible feat on plate-driven presses. As inkjet head durability improves and cost per square meter falls, the run-length crossover threshold between flexo and digital will stretch well beyond 3,000 units, threatening older flexo lines that struggle with frequent changeovers. Converters still amortizing legacy assets weigh dual-investment strategies that layer digital cells onto existing converting lines, yet capital and technician shortages create barriers for smaller firms.

By End-User Industry: E-Commerce Fulfillment Centers Lead Growth

Processed foods commanded 30.14% of Brazil corrugated packaging market share in 2025, reflecting massive domestic consumption and supply chains optimized around high-speed RSC case packing. E-commerce fulfillment centers are forecast to expand at 5.91% CAGR because platforms like Mercado Livre extend seller bases into mid-tier cities, raising demand for lightweight, tear-strip boxes that facilitate returns and align with parcel sorter specifications. Fresh produce and beverage exporters rely on double-wall and triple-wall cartons engineered for cold storage humidity, while electrical and personal-care brands demand photo-quality graphics to reduce secondary packaging needs. Pharmaceutical shippers comply with ANVISA tamper-evidence rules that favor pre-glued crash-lock bottoms and chemical-resistant water-based inks.

Automotive and industrial component suppliers in Paraná and Santa Catarina favor heavy-duty double-wall for crankshafts, motors, and subassemblies shipped over rough highways to ports, paying premium prices for engineered inserts that lower damage claims. Cosmetics and personal-care marketers in São Paulo commission limited-edition digitally printed boxes to coincide with influencer campaigns, proving that high graphics and tight turnaround can command margins exceeding commodity processed-food cartons by 15-20%.[3]Agência Nacional de Vigilância Sanitária (ANVISA), “Tamper-Evident Packaging Requirements,” anvisa.gov.br As each end-user vertical seeks distinct performance and branding attributes, converters diversify substrate portfolios and printing assets to hedge against demand cyclicality.

Geography Analysis

Brazil’s Southeast and South regions collectively generated close to three-quarters of national corrugated output in 2025, reflecting the co-location of pulp capacity, consumer markets, and trunk-road infrastructure. São Paulo’s dense network of independent converters supplies the metropolitan retail base, yet mounting port congestion at Santos inflates freight costs and stretches lead times for export-oriented fresh-produce shippers. South-region mills in Paraná and Santa Catarina leverage shorter hauls to industrial clients and agricultural exporters, but they still depend on those same congested ports for outbound container traffic, exposing converters to schedule disruptions that undermine on-time delivery metrics.

Mid-tier cities such as Curitiba, Belo Horizonte, and Porto Alegre have emerged as secondary corrugated demand centers because e-commerce fulfillment hubs in these municipalities logged triple-digit parcel-volume growth during 2025. Converters are therefore building satellite warehouses within 250 kilometers of these hubs, a move that trims last-mile transit times yet raises working-capital requirements through higher finished-goods inventory. Although these cities benefit from paved highways and reliable power, their thinner recycling networks restrict recovered-paper availability, compelling greater reliance on virgin kraft grades and contributing to regional feedstock price disparities.

The Northeast region, encompassing Bahia, Pernambuco, and Ceará, remains structurally underserved despite accounting for 27% of Brazil’s population and a growing share of fruit exports bound for Europe and Asia. Local converters typically operate smaller single-wall corrugators that lack the equipment to produce moisture-resistant double-wall or triple-wall cartons demanded by cold-chain exporters, forcing packers to source boxes from São Paulo or Paraná at a 15-20% freight premium. Converters eyeing this white-space opportunity must weigh logistics hurdles, limited skilled labor pools, and uneven access to Lei 14.260/21 recycling incentives that currently concentrate in the more industrialized South and Southeast corridors.

Competitive Landscape

The Brazil corrugated packaging market is moderately concentrated, with Klabin, Smurfit WestRock, and International Paper anchoring an integrated tier that controls a significant share of pulp, linerboard, and box capacity. Klabin’s 910,000 tpy Puma II complex and its newer Piracicaba II mill collectively reinforce the company’s leadership in virgin kraft grades, enabling preferential service to appliance and automotive OEMs that demand high burst strength. Smurfit WestRock’s USD 150 million Três Barras expansion underscores an aggressive push to capture South-region e-commerce and shelf-ready volumes, while International Paper’s strategic options are in flux amid Suzano’s pending USD 15 billion acquisition proposal.

Regional converters such as Trombini, Ibema, and Papirus exploit proximity to agricultural belts and smaller customer bases by offering rapid design iterations, shorter order cycles, and localized after-sales support that giant integrators sometimes overlook.[4]Smurfit WestRock, “Três Barras Mill Expansion Announcement,” smurfitkappa.com These firms increasingly invest in digital inkjet presses and high-speed rotary die-cutters to defend niche positions in short-run, high-graphic displays demanded by cosmetics and personal-care brands. However, their limited bargaining power for kraft pulp and recovered paper, combined with rising plate and energy costs, compresses margins during commodity price spikes, prompting selective joint-ventures for fiber sourcing.

Technology adoption is becoming the primary competitive wedge as converters evaluate hybrid workflows that blend flexographic speed with digital flexibility. Early adopters like Mazurky have proven that high-resolution single-pass inkjet can meet e-commerce brand owners’ personalization needs while maintaining throughput compatible with mid-scale production. ISO 14001 certification is now a gatekeeping criterion for multinational buyers, favoring larger organizations with formal sustainability teams, although Lei 14.260/21 recycling incentives are gradually empowering smaller recycled-linerboard plants to compete on environmental credentials.

Brazil Corrugated Packaging Industry Leaders

Klabin S.A.

Smurfit Westrock plc

International Paper Company

Suzano S.A.

Mondi plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Klabin reported 2025 EBITDA of BRL 7.848 billion (USD 1.47 billion), anticipating higher paper output in 2026 as Puma II utilization climbs.

- January 2026: Loggi disclosed that SMEs in mid-tier cities generated 77% of 2025 e-commerce sales growth, prompting converters to re-locate inventory nodes.

- May 2025: Smurfit WestRock confirmed a USD 150 million investment to expand Três Barras mill capacity and upgrade flexographic lines for shelf-ready formats.

- March 2025: Klabin inaugurated the Piracicaba II plant, adding 240,000 tpy of kraftliner and corrugating medium to strengthen Southeast coverage.

Brazil Corrugated Packaging Market Report Scope

The Brazil Corrugated Packaging Market report encompasses a comprehensive analysis of fiber-based and polymer-based corrugated materials used for the containment, protection, and transport of goods across diverse industrial and retail sectors. The market refers to the industry that produces multi-layered boards, typically consisting of a fluted medium sandwiched between linerboards, designed to provide high strength-to-weight ratios and crush resistance for secondary and tertiary packaging.

The Brazil Corrugated Packaging Market Report is Segmented by Material (Virgin Kraft Linerboard, Recycled Linerboard, Corrugating Medium, Semi-Chemical Fluting, and Other Materials), Flute Type (A Flute, B Flute, C Flute, E Flute, and F Flute), Packaging Type (Regular Slotted Containers, Die-Cut Custom Boxes, Folding Cartons, Point-of-Purchase Displays, Pallet Boxes, and Other Packaging Types), Wall Type (Single-Wall, Double-Wall, Triple-Wall, and Single Face), Printing Technology (Flexographic Printing, Digital Inkjet Printing, Litho-Lamination, Screen Printing, and Other Printing Technologies), End-User Industry (Processed Foods, Fresh Food and Produce, Beverages, Electrical Products, Personal Care and Cosmetics, E-commerce Fulfillment Centers, Pharmaceuticals, and Other End-User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Kraft Linerboard |

| Recycled Linerboard |

| Corrugating Medium |

| Semi-Chemical Fluting |

| Other Materials |

| A Flute |

| B Flute |

| C Flute |

| E Flute |

| F Flute |

| Regular Slotted Containers |

| Die-Cut Custom Boxes |

| Folding Cartons |

| Point-of-Purchase Displays |

| Pallet Boxes |

| Other Packaging Types |

| Single-Wall |

| Double-Wall |

| Triple-Wall |

| Single Face |

| Flexographic Printing |

| Digital Inkjet Printing |

| Litho-Lamination |

| Screen Printing |

| Other Printing Technologies |

| Processed Foods |

| Fresh Food and Produce |

| Beverages |

| Electrical Products |

| Personal Care and Cosmetics |

| E-commerce Fulfillment Centers |

| Pharmaceuticals |

| Other End-User Industries |

| By Material | Virgin Kraft Linerboard |

| Recycled Linerboard | |

| Corrugating Medium | |

| Semi-Chemical Fluting | |

| Other Materials | |

| By Flute Type | A Flute |

| B Flute | |

| C Flute | |

| E Flute | |

| F Flute | |

| By Packaging Type | Regular Slotted Containers |

| Die-Cut Custom Boxes | |

| Folding Cartons | |

| Point-of-Purchase Displays | |

| Pallet Boxes | |

| Other Packaging Types | |

| By Wall Type | Single-Wall |

| Double-Wall | |

| Triple-Wall | |

| Single Face | |

| By Printing Technology | Flexographic Printing |

| Digital Inkjet Printing | |

| Litho-Lamination | |

| Screen Printing | |

| Other Printing Technologies | |

| By End-User Industry | Processed Foods |

| Fresh Food and Produce | |

| Beverages | |

| Electrical Products | |

| Personal Care and Cosmetics | |

| E-commerce Fulfillment Centers | |

| Pharmaceuticals | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current Brazil corrugated packaging market size and forecast growth rate?

The market stands at USD 5.10 billion in 2026 and is projected to reach USD 5.93 billion by 2031, expanding at a 3.05% CAGR.

Which end-user segment is expected to grow fastest through 2031?

E-commerce fulfillment centers are forecast to record the highest growth, advancing at a 5.91% CAGR as online retail expands into mid-tier cities.

How are Lei 14.260/21 incentives influencing material choices in the sector?

Tax-backed funding improves recovered-paper collection, narrowing cost gaps between recycled and virgin grades, though benefits remain concentrated in the South and Southeast regions.

Why are double-wall and triple-wall cartons gaining traction in the South?

Automotive, appliance, and agricultural exporters in Paraná and Santa Catarina require stronger compression resistance to survive long truck hauls and congested port dwell times.

What technological shift is most affecting short-run corrugated printing economics?

High-speed digital inkjet presses eliminate plate costs and enable profitable runs under 1,000 units, catering to personalized e-commerce packaging and regional promotions.

Where do geographic white-space opportunities exist for new corrugated capacity?

Northeast cold-chain export corridors and mid-tier cities like Belo Horizonte and Porto Alegre lack sufficient local supply, offering attractive entry points for converters with flexible assets.

Page last updated on: